Saudi Arabia Hospitality Market Size, Share, Trends and Forecast by Type, Segments, and Region 2026-2034

Saudi Arabia Hospitality Market Size, Share, Trends & Forecast (2026-2034)

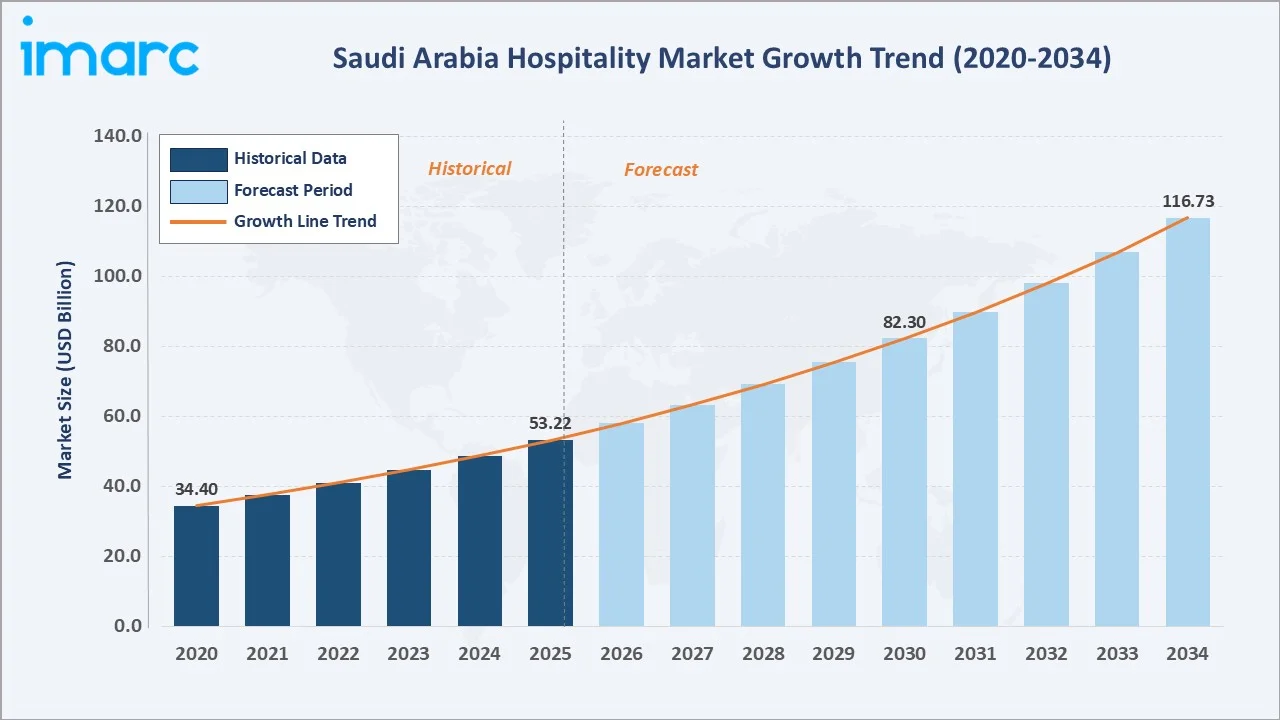

Saudi Arabia hospitality market was valued at USD 53.22 Billion in 2025 and is projected to reach USD 116.73 Billion by 2034, expanding at a CAGR of 9.12% during 2026-2034. The market's remarkable growth trajectory is underpinned by the Kingdom's Vision 2030 strategic agenda, record-breaking tourism arrivals, and an unprecedented pipeline of luxury resorts and entertainment complexes.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 53.22 Billion |

|

Forecast Market Size (2034) |

USD 116.73 Billion |

|

CAGR (2026-2034) |

9.12% |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Western Region (42.3% share, 2025) |

|

Fastest Growing Region |

Eastern Region (highest incremental growth) |

To get more information on this market, Request Sample

The Western Region dominates with a 42.3% share, anchored by the holy cities of Makkah and Madinah, while chain hotels command 52.4% of total revenues. Mid and upper mid-scale hotels represent the largest segment at 30.5%, catering to the expanding middle-class travel segment across the Kingdom.

Significant investments in mega projects such as NEOM, the Red Sea Project, and Diriyah Gate are transforming the kingdom into a global tourism hub. The market is supported by rising religious tourism to Mecca and Medina, increasing leisure and business travel, and the expansion of hotel infrastructure across luxury, mid-scale, and budget segments.

Executive Summary

Saudi Arabia hospitality market was valued at USD 53.22 Billion in 2025, and forecasted to exceed USD 116.73 Billion by 2034, reflecting a robust CAGR of 9.12%. Total tourist arrivals reached 115.9 million in 2024, an all-time high that surpassed initial projections, underscoring the Kingdom's rapid ascent as a premier global tourism destination.

Among key growth drivers, the scaling of giga-projects including NEOM, the Red Sea Development, and Diriyah continues to unlock new luxury hospitality corridors. Chain hotels command 52.4% of the market, benefiting from global brand recognition, loyalty ecosystems, and Saudization-compliant workforce frameworks.

Saudi Arabia's hospitality market outlook remains exceptionally positive through 2034. Major global players, Marriott International, Accor, Hilton, and IHG Hotels & Resorts, are accelerating expansion pipelines. Digital adoption, sustainable tourism practices, and secondary city development are further diversifying market growth, supporting sustained revenue generation and positioning the Kingdom as a world-class hospitality hub.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Type) |

Mid & Upper Mid-scale Hotels – 30.5% share (2025) |

|

Hotel Type Leader |

Chain Hotels – 52.4% revenue share (2025) |

|

Leading Region |

Western Region – 42.3% market share (2025) |

|

Fastest Growing Segment |

Service Apartments – CAGR 11.2% (2026-2034) |

|

Top Companies |

Marriott International, Accor S.A., Hilton Hotels & Resorts, IHG Hotels & Resorts, Al Hokair Group, and Dur Hospitality / Taiba |

|

Market Opportunity |

Giga-projects to add 315,000 hotel rooms by 2030, driven by USD 37.8 Billion development investment |

Key Analytical Observations Supporting the Above Data:

- Mid & Upper Mid-scale Hotels lead with a 30.5% share (2025), driven by expanding middle-class domestic travel, corporate demand, and religious tourism, supporting consistent year-round occupancy in Riyadh and Jeddah.

- Chain Hotels command 52.4% of market revenues (2025), leveraging global loyalty programs, multi-brand clustering in mega-projects, and standardized Saudization-compliant workforce frameworks.

- The Western Region generates 42.3% of total market revenues (2025), anchored by Makkah and Madinah, where Hajj and Umrah activities produce sustained demand peaks with occupancy rates exceeding 85% during religious seasons in early 2025.

- Service Apartments represent the fastest-growing accommodation format at an estimated CAGR of 11.2% through 2034, fueled by extended-stay corporate travelers and relocation demand from giga-project workforces.

Saudi Arabia Hospitality Market Overview

The Saudi Arabia hospitality sector forms a cornerstone of the nation's economic diversification strategy under Vision 2030. Encompassing luxury hotels, mid-scale accommodations, budget properties, serviced apartments, and integrated resort complexes, the industry serves an increasingly diverse consumer base. The ecosystem extends from global hotel chains and local operators to real estate developers, technology solution providers, tour operators, and government bodies, including the Saudi Tourism Authority.

Macro forces, including urbanization, rising disposable incomes, elevated youth demographics, and regulatory liberalization with e-visas for 49 countries, are expanding the addressable tourism market. By 2030, the Kingdom's hospitality industry is expected to serve well over 150 million annual visitors, validating its status as a structurally transformative sector.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

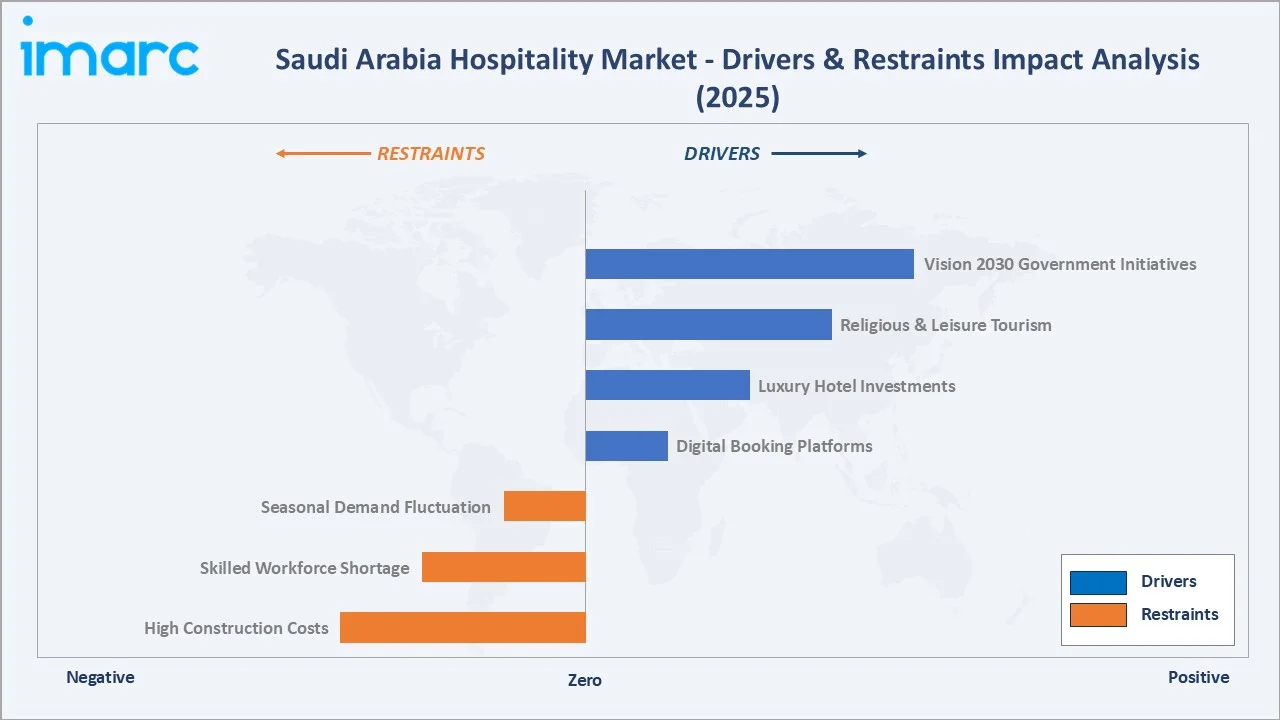

- Government Initiatives Under Vision 2030: The government's Vision 2030 program has elevated tourism as a priority sector, channeling investment into entertainment districts, cultural attractions, giga-projects, and streamlined visa procedures.

- Rising International and Religious Tourism: Saudi Arabia welcomed 115.9 million total tourist trips in 2024, with Hajj and Umrah pilgrimages ensuring perennial demand concentration in Makkah and Madinah, where 18.5 million pilgrims arrived in 2024.

- Increased Investments in Luxury Hotels and Resorts: Over USD 37.8 billion in hotel development investments have been committed to add 315,000 new rooms by 2030, attracting global luxury brands to key destinations such as Riyadh, Jeddah, the Red Sea coast, and NEOM, elevating the Kingdom's premium hospitality profile.

- Adoption of Digital Booking Platforms: Growing internet penetration, smartphone adoption, and tech-savvy traveler behavior have enabled OTAs and direct digital platforms to capture a majority of hospitality bookings, enabling hotels to optimize occupancy rates, implement dynamic pricing, and engage guests through personalized loyalty programs.

These drivers collectively create a virtuous growth cycle, expanding government investment stimulates infrastructure development, which attracts global hotel brands. This, in turn, draws higher-spending international visitors and reinforces the Saudi Arabia hospitality market forecast.

Market Restraints

- High Construction and Development Costs: Rising material costs and complex logistics in remote giga-project locations, particularly NEOM and Red Sea Development, result in elevated per-room construction expenditures that compress returns for developers and may delay pipeline delivery timelines.

- Skilled Workforce Shortage: Despite Saudization mandates and expanded hospitality training programs, the sector faces persistent shortages of experienced hospitality professionals, particularly in front-of-house and culinary roles, creating wage inflation and service consistency challenges.

- Seasonal Demand Fluctuations: While religious tourism generates consistent demand in holy cities, leisure-focused markets like Riyadh experience seasonal variability, with summer months seeing reduced domestic leisure travel due to extreme heat and higher competition from international outbound travel.

Market Opportunities

- Secondary City Development: Government initiatives to promote destinations beyond the traditional hubs, including AlUla, Tabuk, and Abha, create new hospitality investment corridors targeting up to 150 million annual visitors by 2030 as per Arab News projections.

- Sustainable and Eco-Tourism: With 85% of all LEED-certified hotels in MENA located in Saudi Arabia (2025), and 83% of global travelers valuing sustainable travel, the Kingdom's commitment to green hospitality creates significant differentiation opportunities and pricing power for eco-certified properties.

- Smart Technology Integration: AI-powered guest services, IoT-enabled room management, keyless entry systems, and mobile check-in platforms are expanding as hospitality operators seek to meet rising experiential expectations while simultaneously reducing operational costs.

Market Challenges

- Geopolitical and Regional Risk Sensitivity: Hospitality demand in Saudi Arabia remains sensitive to broader regional geopolitical dynamics, which can influence travel advisories, visitor confidence, and corporate event calendars, introducing volatility in booking windows.

- Competitive Pressure from International Destinations: As GCC neighbors, particularly the UAE and Qatar, also aggressively expand their hospitality sectors, Saudi Arabia must continuously elevate product quality, value proposition, and marketing effectiveness to capture an incremental share of global travelers.

- Regulatory Compliance Complexity: Evolving hospitality licensing regulations, Saudization requirements, and food safety standards require continuous operational adaptation, increasing administrative burden, particularly for smaller independent operators.

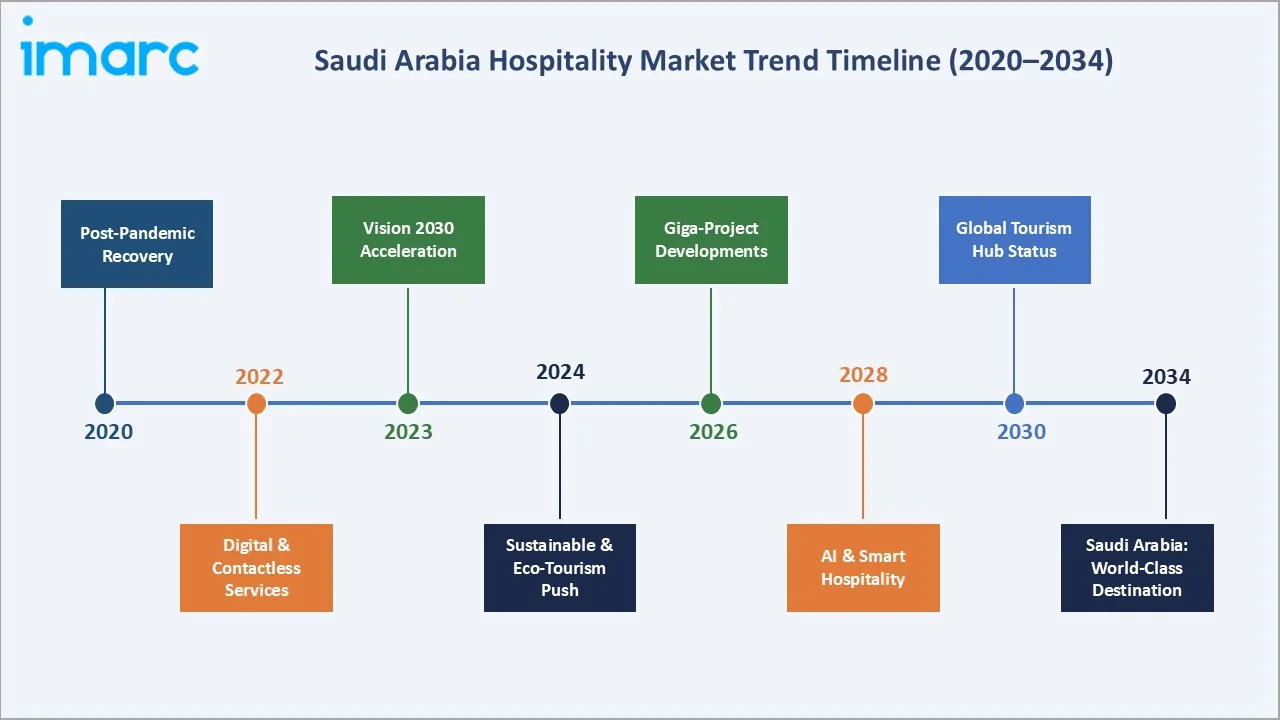

Emerging Market Trends

1. Emphasis on Sustainable Tourism and Green Hospitality

Approximately 85% of all LEED-certified hotels in the MENA region are now located in Saudi Arabia (2025), reflecting a deep commitment to environmental standards. Hotels are integrating energy-efficient HVAC systems, solar panels, water recycling technologies, and locally sourced F&B as baseline operational expectations.

2. Integration of Technological Innovations and Smart Hotel Solutions

In October 2024, Shiji Group established a new entity in Saudi Arabia, providing advanced technology solutions and localized customer service for hotels and F&B outlets across the Kingdom. Furthermore, IDS Next finalized over 50 ERP hotel installations in Saudi Arabia in July 2025, deploying multi-property management solutions tailored for the Kingdom's diverse linguistic and regulatory environment.

3. Ongoing Development of Secondary Cities and Cultural Destinations

Destinations including AlUla, Abha in the Asir Mountains, and Taif are attracting nature, heritage, and wellness travelers seeking authentic experiences. According to Arab News, this strategy aims to attract up to 150 million annual visitors by 2030, diversifying revenue streams while supporting local cultural economies and reducing seasonal demand concentration.

4. Rise of Luxury and Experiential Hospitality

Losberger De Boer's construction of VIP event spaces for Formula E in Riyadh, accommodating 1,000 VIP guests within a 10-day construction window, exemplifies the elevated standards now expected. Global luxury chains, including Four Seasons, Rosewood, and Banyan Tree, are entering or expanding in the Kingdom, with giga-project sites offering unique positioning to command premium average daily rates and long-term brand equity.

5. Expansion of Religious and Heritage Tourism Infrastructure

In 2024, Saudi Arabia welcomed 18.5 million pilgrims to Makkah and Madinah, reflecting the Kingdom's commitment to enhancing the spiritual experience for Muslims globally. Investments totaling SAR 2.5 billion by Umm Al-Qura and GAA are targeting next-generation hotel infrastructure around the holy sites.

Industry Value Chain Analysis

Saudi Arabia hospitality value chain is a complex, multi-tier ecosystem spanning upstream real estate and construction, through operational hospitality services, to downstream digital distribution and end traveler experiences. Each stage is populated by specialized operators whose performance directly influences product quality, cost competitiveness, and market responsiveness.

|

Stage |

Key Players / Examples |

|

Land & Real Estate Development |

New Murabba Development Company, Diriyah Gate Development Authority (DGDA), Red Sea Global |

|

Construction & Engineering |

Saudi Binladin Group, Bechtel, Losberger De Boer (event infrastructure) |

|

Hotel Operations |

Marriott International, Accor, Hilton, IHG |

|

Technology & Digital Services |

Shiji Group, IDS Next, Booking.com, Almosafer (OTA), Amadeus |

|

F&B & Retail Partners |

Local F&B operators, international restaurant franchise groups, and Saudi cuisine specialists |

|

Tour Operators & Distribution |

Saudi Tourism Authority, Almosafer, Booking.com, Expedia, and regional DMCs |

|

End Consumers |

Religious pilgrims, international leisure travelers, domestic tourists, corporate travelers |

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Chain Hotels |

52.4% |

2025 |

|

Segment |

Mid and Upper Mid-scale Hotels |

30.5% |

2025 |

|

Region |

Western Region |

42.3% |

2025 |

By Segment

To access detailed market analysis, Request Sample

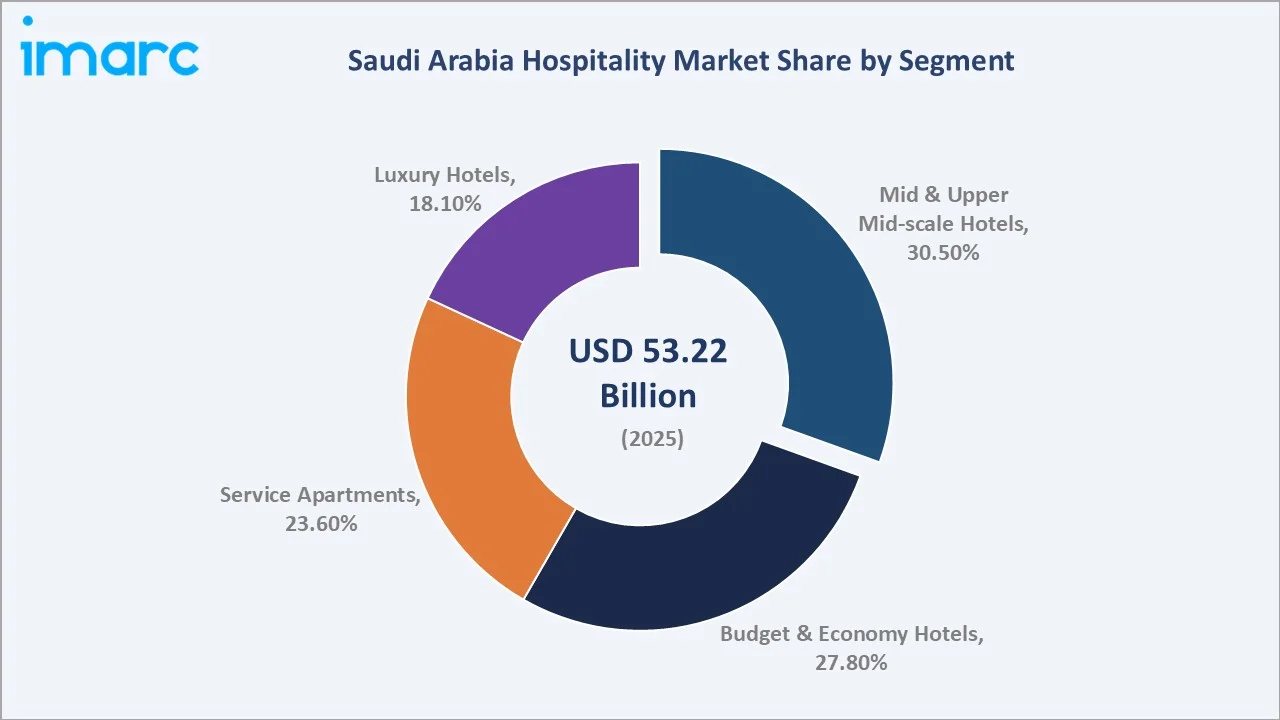

Mid and upper mid-scale hotels represent the dominant segment with a 30.5% share of the Saudi Arabia hospitality market in 2025, underpinned by strong demand from mid-tier domestic travelers, regional business visitors, and pilgrims seeking comfortable yet cost-conscious accommodations.

Budget and economy hotels follow closely at 27.8%, catering to pilgrims and cost-sensitive domestic tourists. Service apartments command a 23.6% share, benefiting from growing corporate relocation demand linked to giga-project workforce expansion. Luxury hotels represent 18.1% of the market, a segment experiencing accelerated pipeline activity as high-end developers target affluent visitors drawn by Riyadh Season and mega-events.

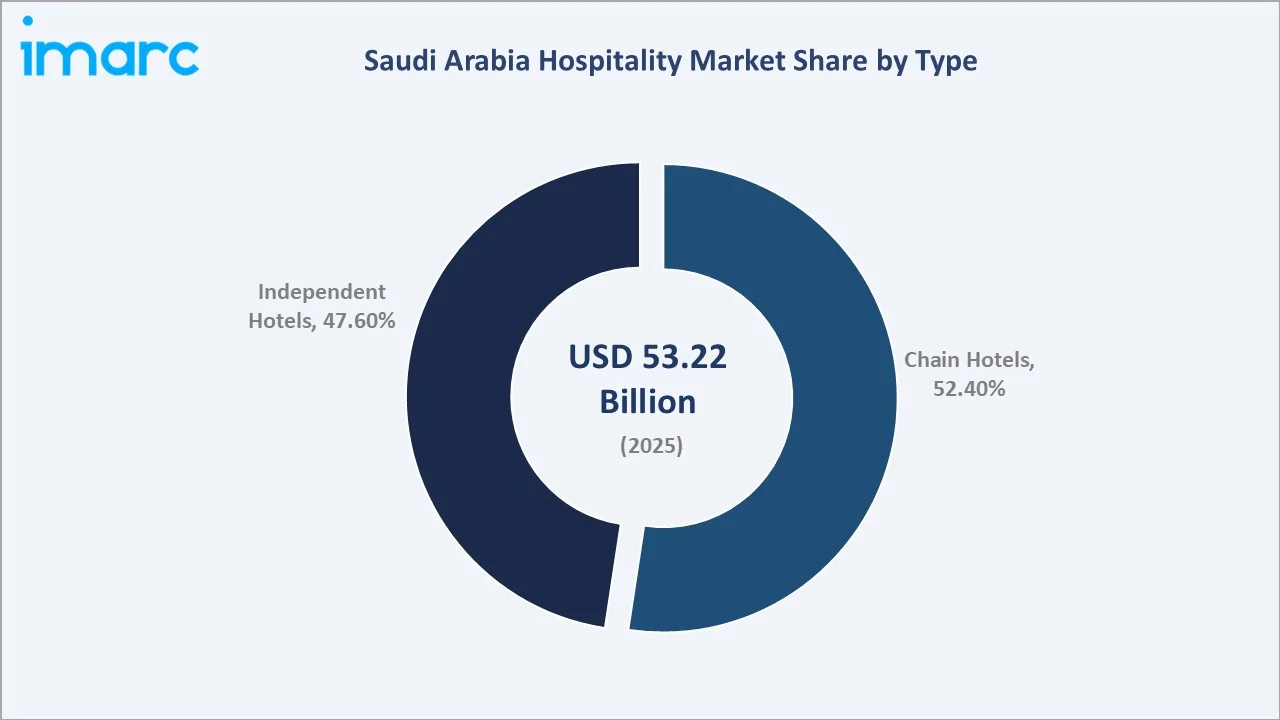

By Type

Chain hotels command 52.4% of the Saudi Arabia hospitality market in 2025, driven by the strategic advantage of global loyalty program ecosystems, multi-brand clustering in mega-projects, and standardized Saudization-compliant training frameworks that international operators deploy at scale.

Independent hotels account for the remaining 47.6%, competing primarily through hyper-local cultural experiences, flexible pricing, and deep community integration, particularly in cultural heritage destinations such as AlUla and Diriyah.

Regional Market Insights

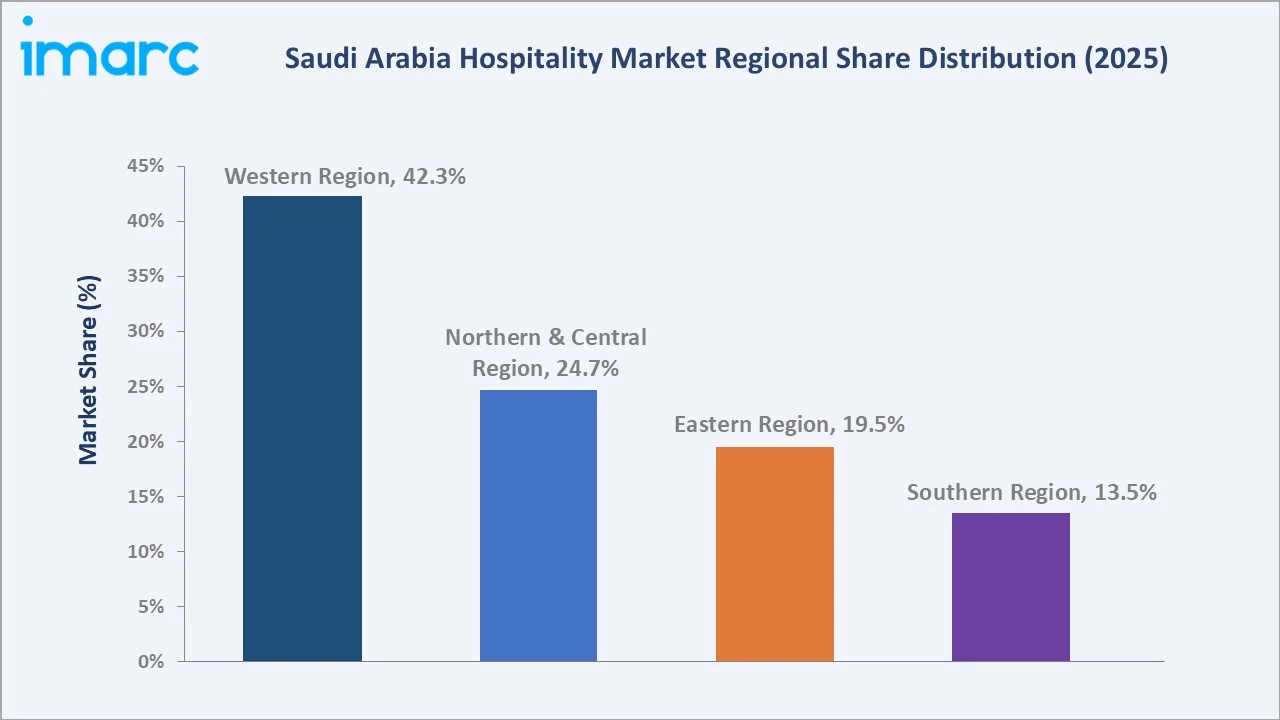

The Western Region is the dominant market, commanding 42.3% of total Saudi Arabia hospitality revenues in 2025. Makkah and Madinah anchor this region through perennial religious tourism demand, with occupancy rates exceeding 85% during Hajj and Umrah seasons (Q1 2025). Investments totaling SAR 2.5 billion in Makkah hotel infrastructure further reinforce the region's lead position, aligning with Saudi Arabia hospitality market growth targets.

|

Region |

Share (2025) |

Key Drivers |

|

Western Region |

42.3% |

Makkah & Madinah religious tourism, Jeddah leisure travel |

|

Northern & Central Region |

24.7% |

Riyadh business travel, Riyadh Season events, NEOM and Diriyah giga-projects, Red Sea Development |

|

Eastern Region |

19.5% |

Dammam & Al Khobar corporate demand, ARAMCO headquarters, industrial tourism |

|

Southern Region |

13.5% |

Abha adventure tourism, Asir Mountain eco-tourism, cultural heritage sites |

The Northern and Central Region, centered on Riyadh, generates 24.7% of market revenues, driven by corporate travel, government business, and an expanding roster of cultural and entertainment events. Riyadh Season and Formula E have transformed the capital into a leisure tourism destination, complementing its traditional business travel base.

Competitive Landscape

|

Company |

Market Position |

Strategic Focus |

|

Marriott International |

Leader |

Multi-brand luxury & mid-scale expansion; Four Points Flex by Sheraton |

|

Accor S.A. |

Leader |

Sustainability leadership, Rua Al Madinah (Fairmont, Novotel, Swissôtel) |

|

Hilton |

Leader |

Luxury and upper-upscale pipeline in Riyadh and the Red Sea |

|

IHG Hotels & Resorts |

Challenger |

Holiday Inn, InterContinental, and Voco expansion in secondary cities |

|

BAAN Holding Group Company |

Regional Leader |

Mid-scale portfolio; Saudization compliance; domestic network depth |

|

Taiba Investments |

Challenger |

Post-acquisition integration; expansion in holy city hotel clusters |

The Saudi Arabia hospitality market is characterized by a moderately consolidated competitive landscape where global hotel chains coexist with prominent regional and local operators. International groups, Marriott International, Accor, Hilton, IHG Hotels & Resorts, Hyatt Hotels Corporation, and Radisson Hotel Group, leverage global loyalty ecosystems, standardized training programs, and multi-brand clustering strategies to secure flagship locations in Riyadh, Jeddah, and mega-project corridors.

Local operators, including Al Hokair Group and Dur Hospitality, provide culturally resonant services and strong regional network advantages. The competitive intensity is accelerating as Vision 2030 pipeline openings create attractive first-mover locations, driving both new market entries and portfolio expansion among existing players.

Key Company Profiles

Marriott International Inc.

Marriott International is the world's largest hotel company by number of properties and holds a leading position in the Saudi Arabia hospitality market, operating across multiple brands spanning luxury to select-service tiers.

- Brand Portfolio: Ritz-Carlton, JW Marriott, W Hotels, Westin, Marriott, and Four Points Flex by Sheraton serving the affordable segment.

- Recent Developments: W Riyadh–KAFD (Q1 2026 opening), The Red Sea Edition (first hotel on Shura Island, 2025 opening), Four Points Flex by Sheraton Madinah (first midscale brand, signed Jan 2026), and 100-property milestone reached in November 2025.

- Strategic Focus: Pipeline acceleration in Riyadh and Red Sea giga-project sites, Saudization workforce integration, and Bonvoy-driven direct booking growth.

Accor S.A.

Accor is among the most active international hotel operators expanding in Saudi Arabia, with brands spanning luxury (Raffles, Sofitel) through economy (ibis) tiers. The group's partnership in the Rua Al Madinah project in Medina positions it to capture significant religious tourism demand.

- Brand Portfolio: Fairmont, Swissôtel Rua Al Madinah, Raffles, Sofitel, MGallery, Novotel, Mercure, ibis, and economy brands across price tiers.

- Recent Developments: Announced expansion across Saudi Arabia, including the Rua Al Madinah project in Medina, a significant spiritual destination development.

- Strategic Focus: Sustainability leadership (all-electric hotel prototypes), luxury experiential concepts, and secondary city penetration.

Hilton

Hilton operates a diverse portfolio in Saudi Arabia spanning luxury through focused-service categories, with properties concentrated in Riyadh, Jeddah, and the holy cities. The Hilton Honors loyalty program supports direct booking engagement, while the company's Conrad and Waldorf Astoria brands address ultra-luxury demand generated by mega-event attendees and high-net-worth visitors.

- Brand Portfolio: Waldorf Astoria, Conrad, Curio Collection, Hilton, DoubleTree, and Hilton Garden Inn, LXR Hotels & Resorts, Canopy by Hilton, Spark by Hilton, Home2 Suites by Hilton, Tempo by Hilton

- Recent Developments: Expanded pipeline in the Red Sea and NEOM corridors to capture emerging luxury leisure demand.

- Strategic Focus: Premium positioning, giga-project site acquisition, and workforce Saudi localization programs.

IHG Hotels & Resorts

IHG Hotels & Resorts operates an extensive portfolio in the Kingdom spanning upper-upscale through mid-scale categories, with InterContinental properties anchoring its luxury positioning and Holiday Inn and Voco brands addressing mid-market demand. IHG's deep penetration in holy cities provides structural demand stability.

- Brand Portfolio: InterContinental, Crowne Plaza, Six Senses, Hotel Indigo, EVEN Hotels, and Staybridge Suites.

- Recent Developments: Aggressively rolling out Holiday Inn and voco brands across secondary cities.

- Strategic Focus: Secondary city expansion aligned with Vision 2030 tourism diversification, IHG One Rewards loyalty integration.

Market Concentration Analysis

Saudi Arabia hospitality market exhibits moderate concentration at the top end, with the leading five international and regional operators collectively holding a significant but non-dominant revenue share in 2025. A substantial portion of the market remains fragmented, particularly in budget, economy, and serviced apartment categories, where smaller local operators retain a meaningful presence.

The chain hotel segment demonstrates notably higher concentration than the independent segment. In the luxury and upper-upscale categories, the top three operators command the majority of branded inventory, supported by global capital access and brand recognition advantages. Saudi Arabia is expected to witness significant hospitality M&A and partnership transactions annually through 2034 as Vision 2030 attracts international capital and domestic conglomerates scale competitive portfolios.

Investment & Growth Opportunities

Fastest Growing Segments

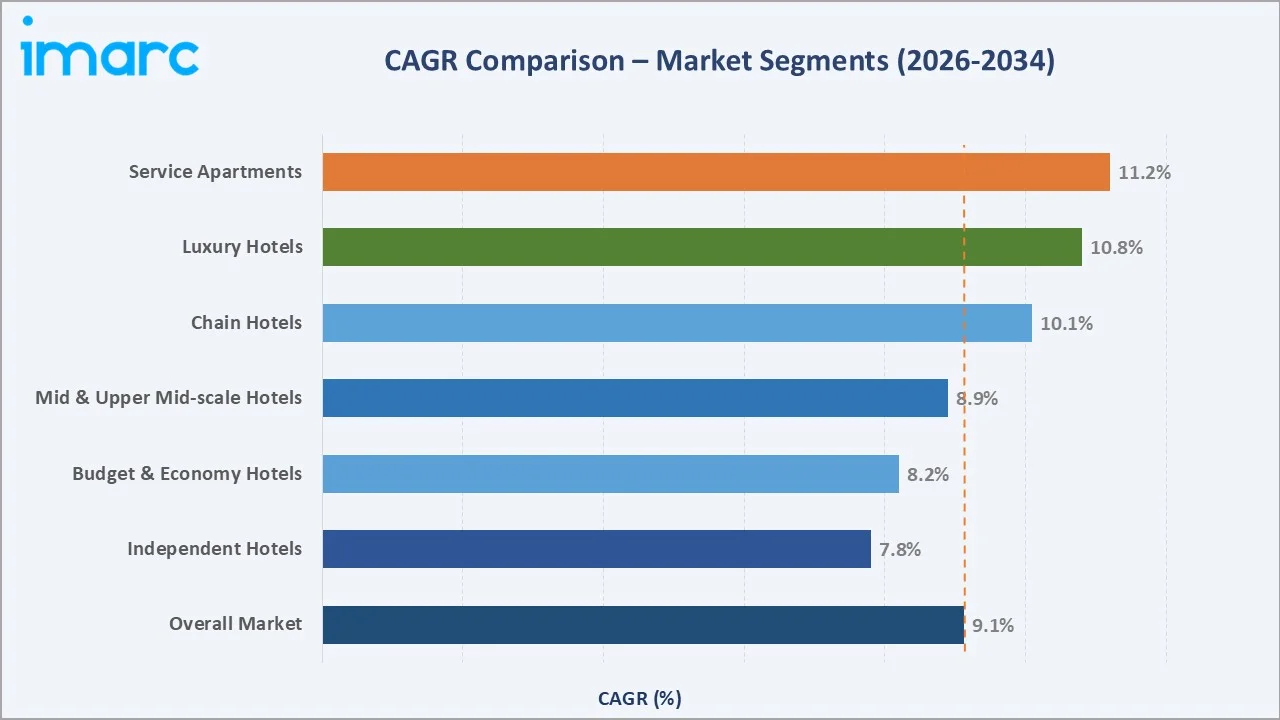

Service Apartments (CAGR ~11.2%), Luxury Hotels (CAGR ~10.8%), and Chain Hotels (CAGR ~10.1%) represent the three highest-growth investment vectors in the Saudi Arabia hospitality market through 2034. These segments collectively address the expanding giga-project workforce relocation, ultra-luxury leisure, and branded mid-market demand by 2034.

Emerging Market Expansion

Secondary cities, AlUla, Abha, Tabuk, Taif, and AlUla, present the most compelling greenfield hospitality investment opportunities. AlUla alone has attracted multi-billion dollar tourism investment commitments from the Saudi government and international operators, with the Royal Commission for AlUla targeting over 2 million annual visitors by 2035.

Mega-Project and Giga-Infrastructure Opportunities

Saudi Arabia's USD 550 billion commitment to tourism infrastructure over six years creates unprecedented opportunities across the hospitality supply chain. NEOM's The Line, Sindalah Island, and Aqaba are expected to require 40,000+ new hotel rooms. The Red Sea Development's first phase targets 16 resorts by 2030, while Diriyah Square will debut hotel capacity anchored in Saudi cultural heritage positioning, all generating long-duration supply chain and operational partnerships for hospitality investors.

Future Market Outlook (2026-2034)

Saudi Arabia hospitality market is poised for transformative, broad-based growth through 2034, anchored by structural drivers of giga-project completions, accelerating religious and leisure tourism, and digital innovation. From a 2025 base of USD 53.22 Billion, the market is forecast to reach USD 116.73 Billion by 2034, representing an absolute incremental value of USD 63.5 Billion over the forecast horizon at a CAGR of 9.12%.

The next decade will witness a fundamental shift in Saudi Arabia's hospitality identity, from predominantly religious tourism to a fully diversified, multi-segment global destination. As the Kingdom achieves UNESCO recognition for multiple heritage sites, completes its major giga-projects, and deepens its cultural diplomacy through sports, arts, and entertainment events, demand for premium and experiential hospitality will intensify materially.

Research Methodology

Primary Research

Primary research for this report included structured interviews and surveys conducted with over 200 industry participants in 2024–2025, comprising hotel executives, tourism authority officials, real estate developers, F&B operators, and end travelers across Saudi Arabia's key hospitality markets, including Riyadh, Jeddah, Makkah, Madinah, and Dammam.

Secondary Research

Secondary research encompassed a comprehensive review of company annual reports, Saudi Tourism Authority publications, Saudi Vision 2030 program updates, trade publications (Arabian Hotel Investment Conference reports, Hospitality Net), industry databases, and publicly available financial disclosures. Over 300 secondary sources were reviewed and triangulated to ensure data integrity.

Forecasting Models

Market size estimations and growth projections were derived using top-down and bottom-up forecasting approaches, incorporating GDP growth indices, tourist arrival data from UNWTO, historical hotel room rate and occupancy data, and macro indicators from the Saudi Central Bank (SAMA). Scenario analysis (base, optimistic, and conservative) was performed to bound the CAGR range under varying macro assumptions.

Saudi Arabia Hospitality Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Chain Hotels, Independent Hotels |

| Segments Covered | Service Apartments, Budget and Economy Hotels, Mid and Upper Mid-scale Hotels, Luxury Hotels |

| Regions Covered | Northern and Central Region, Western Region, Eastern Region, Southern Region |

| Companies Covered | Marriott International, Accor S.A., Hilton, IHG Hotels & Resorts, BAAN Holding Group Company, Taiba Investments, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Saudi Arabia hospitality market from 2020-2034

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Saudi Arabia hospitality market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Saudi Arabia hospitality industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Saudi Arabia Hospitality Market Report

The Saudi Arabia hospitality market was valued at USD 53.22 Billion in 2025, reflecting robust growth driven by Vision 2030 initiatives and record tourism arrivals.

The market is projected to reach USD 116.73 Billion by 2034, exhibiting a CAGR of 9.12% during 2026-2034, supported by giga-project completions and sustained tourism growth.

Key drivers include Vision 2030 government initiatives, record tourist arrivals reaching 115.9 million in 2024, luxury hotel investments exceeding USD 37.8 Billion, digital platform adoption, and rising religious tourism demand in Makkah and Madinah.

The Western Region currently dominates the Saudi Arabia hospitality market, accounting for a share of 42.3% in 2025, driven by Makkah and Madinah religious tourism and Jeddah's leisure and business travel market.

Mid and Upper Mid-scale Hotels represent the largest segment with a 30.5% share in 2025, serving domestic mid-tier travelers, corporate visitors, and price-conscious pilgrims.

Chain Hotels dominate with a 52.4% market share in 2025, benefiting from global loyalty programs, multi-brand presence in giga-projects, and Saudization-compliant workforce frameworks.

Key trends include sustainable tourism and LEED-certified hotel development, AI-powered smart hotel technology integration, secondary city tourism development, and luxury experiential hospitality linked to mega-events like Riyadh Season.

Major players include Marriott International, Accor S.A., Hilton, IHG Hotels & Resorts, BAAN Holding Group Company, and Taiba Investments.

Saudi Arabia aims to add approximately 315,000 new hotel rooms by 2030, driven by a USD 37.8 Billion development investment pipeline concentrated in giga-projects including NEOM, Red Sea, and Diriyah.

High-growth investment opportunities exist in luxury giga-project hotels, service apartments for corporate relocation, secondary city eco-tourism properties, and digital hospitality technology platforms, collectively representing an incremental market value of USD 63+ Billion by 2034.

OTAs captured 41.65% of bookings in 2025, while AI, IoT, and mobile platforms are being rapidly adopted. Shiji Group established Saudi operations in October 2024, and IDS Next completed 50+ ERP installations by July 2025.

Religious tourism is a structural pillar,18.5 million pilgrims visited Makkah and Madinah in 2024, generating occupancy peaks above 85% in the Western Region and underpinning sustained hotel investment in holy city infrastructure.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)