Saudi Arabia ICT Market Size, Share, Trends and Forecast by Type, Size of Enterprise, Industry Vertical, and Region, 2026-2034

Saudi Arabia ICT Market Size, Share, Trends & Forecast (2026-2034

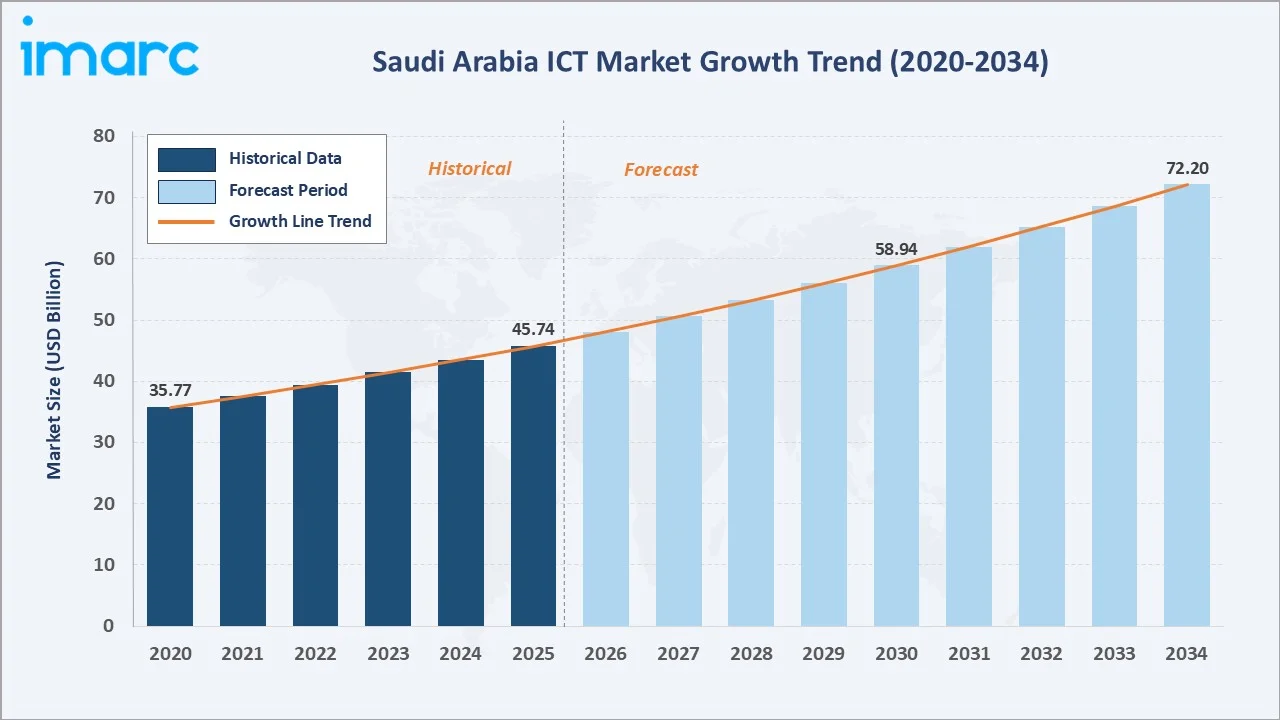

The Saudi Arabia ICT market size reached USD 45.74 Billion in 2025 and is projected to reach USD 72.20 Billion by 2034, exhibiting a CAGR of 5.04% during 2026-2034. Vision 2030 digital transformation, 5G rollout, smart-city investments, cloud localization, and enterprise AI adoption are the primary growth drivers.

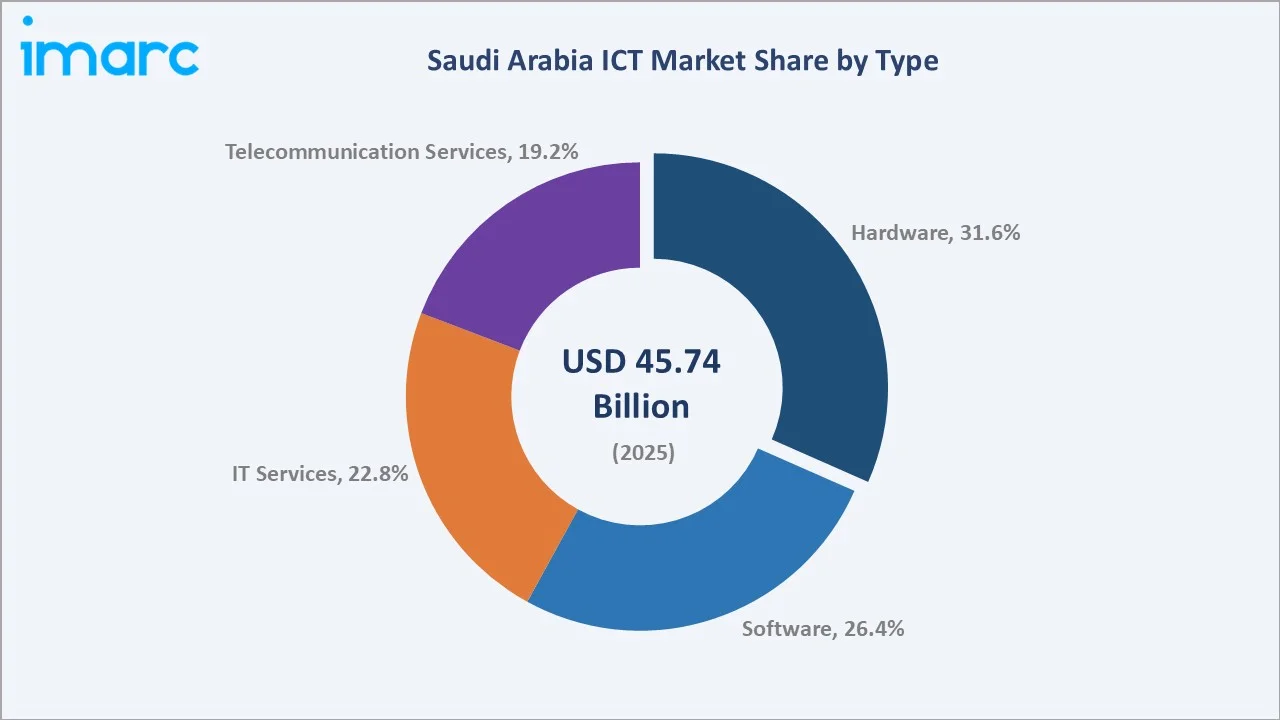

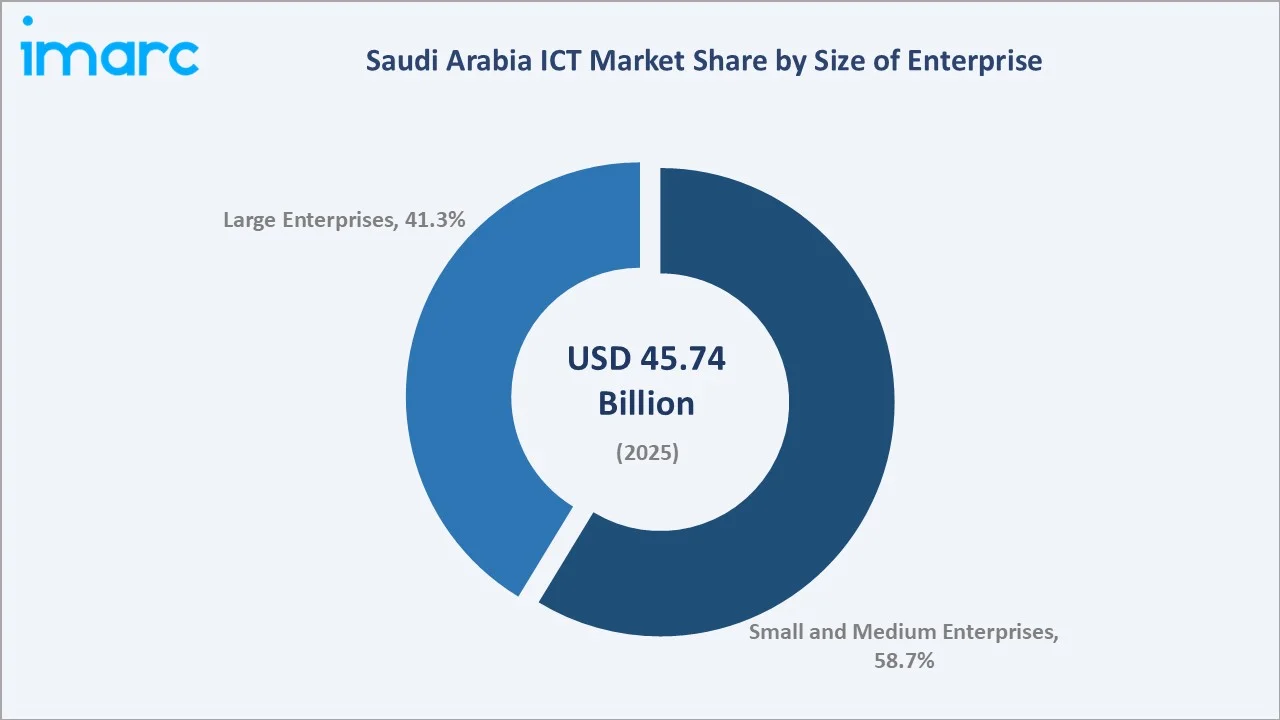

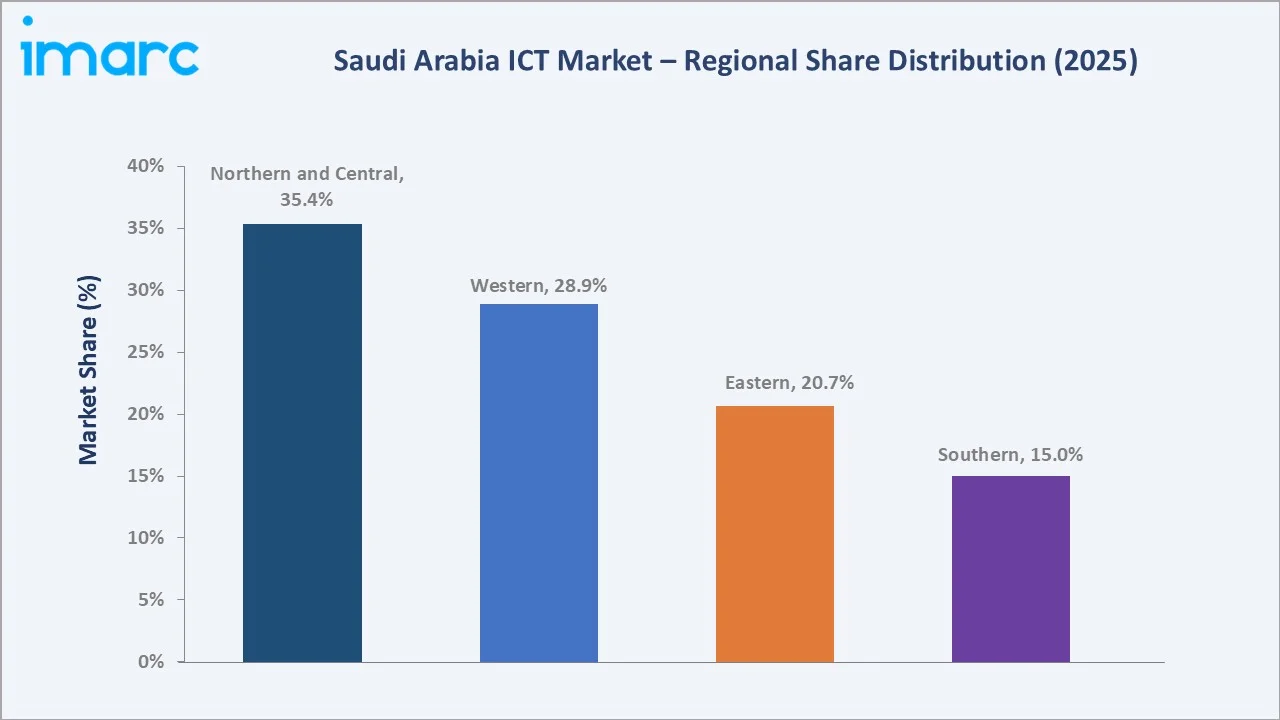

Hardware dominates the type mix at 31.6% in 2025, while Small and Medium Enterprises lead the size-of-enterprise segment at 58.7%. The Northern and Central Region commands a dominant 35.4% regional share in 2025, reflecting Riyadh's role as the national digital, financial, and government ICT hub.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 45.74 Billion |

|

Forecast Market Size (2034) |

USD 72.20 Billion |

|

CAGR (2026-2034) |

5.04% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Northern and Central Region (35.4% share, 2025) |

|

Second Largest Region |

Western Region (28.9% share, 2025) |

|

Leading Type |

Hardware (31.6%, 2025) |

|

Leading Size of Enterprise |

SMEs (58.7%, 2025) |

The Saudi Arabia ICT market growth trajectory from 2020 through 2034, with historical expansion to USD 45.74 Billion in 2025, reflects consistent digital transformation momentum, while the forecast to USD 72.20 Billion captures accelerating 5G rollout, cloud localization, AI adoption, and Vision 2030 smart-city-led spending.

To get more information on this market, Request Sample

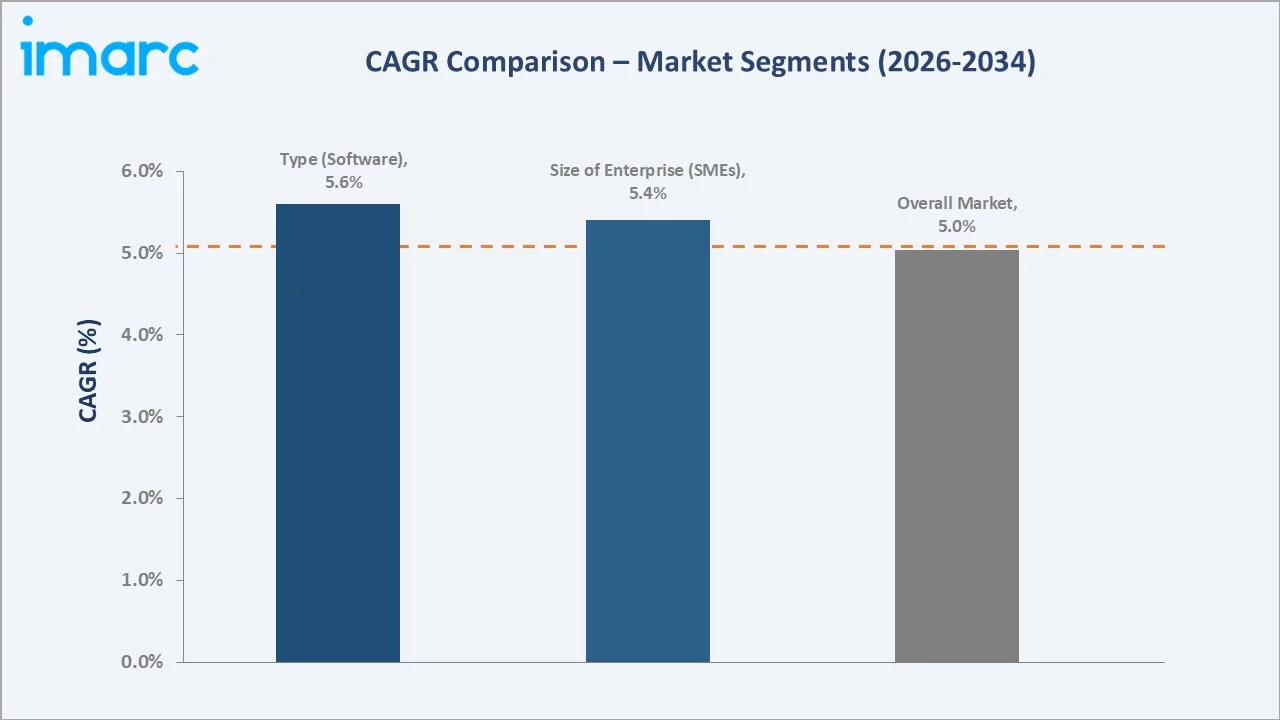

The CAGR trajectories across key type and size-of-enterprise sub-segments, with software at ~5.6% CAGR and SMEs at ~5.4% CAGR, are among the fastest-growing categories within the Saudi Arabia ICT industry through 2034.

Executive Summary

The Saudi Arabia ICT market is on a sustained growth trajectory from USD 45.74 Billion in 2025 to USD 72.20 Billion by 2034. ICT, a strategic enabler across Vision 2030 digital economy, smart government, and private-sector transformation programs, benefits from policy-led demand and recurring infrastructure replacement cycles.

Hardware dominates type at 31.6% in 2025, anchored by data-center build-out, 5G radio access infrastructure, and enterprise endpoint refresh cycles. Software (26.4%) commands growing preference driven by enterprise SaaS, AI platforms, and cybersecurity suites.

IT services (22.8%) serve cloud migration and integration demand, led by Elm, Accenture, and Tech Mahindra. Telecommunication Services (19.2%) are anchored by 5G monetization, enterprise connectivity, and fixed-line broadband delivered by stc, Mobily, and Zain KSA.

Small and medium enterprises lead at 58.7% in 2025, driven by Monsha'at digital support programs and affordable SaaS adoption. Large enterprises at 41.3% drive high-value ERP, cybersecurity, and hybrid-cloud spend.

The Northern and Central Region commands 35.4%, Western 28.9%, Eastern 20.7%, and Southern 15.0% of national ICT spend.

Key Market Insights

|

Insight |

Data |

|

Leading Type |

Hardware – 31.6% share (2025) |

|

Second Leading Type |

Software – 26.4% share (2025) |

|

Leading Size of Enterprise |

SMEs – 58.7% share (2025) |

|

Second Leading Size of Enterprise |

Large Enterprises – 41.3% share (2025) |

|

Leading Region |

Northern and Central Region – 35.4% share (2025) |

|

Top Companies |

stc, Mobily, Zain, Elm, Huawei Technologies Co., Ltd., Microsoft, Cisco Systems, Inc., Oracle |

Key Analytical Observations Supporting the Above Data:

- Hardware, with 31.6% in 2025, dominates because Vision 2030 mega-projects, including NEOM, Qiddiya, and The Line, require data centers, 5G RAN build-out, enterprise endpoints, and IoT sensors at unprecedented scale, supported by local manufacturing incentives.

- Software, at 26.4% in 2025, is a fast-growing segment driven by enterprise SaaS adoption, SDAIA-aligned AI platforms, and cybersecurity compliance software mandated under NCA guidelines.

- SMEs, at 58.7% in 2025, reflect the Kingdom's over 1.3 million registered SME base and Monsha'at-led digital enablement programs that accelerate SaaS, e-commerce, and fintech adoption.

- The Northern and Central Region, at 35.4% in 2025, reflects Riyadh's concentration of federal government agencies, financial institutions, multinational headquarters, and the King Abdullah Financial District (KAFD) driving outsized ICT demand.

Saudi Arabia ICT Market Overview

The ecosystem integrates global technology vendors, domestic telecom operators (stc, Mobily, Zain), system integrators, cloud providers (Microsoft Azure, AWS, Google Cloud), cybersecurity firms, and public-sector agencies such as SDAIA, NCA, DGA, and CITC steering policy and demand under the Vision 2030 framework.

Market Dynamics

To evaluate market opportunities, Request Sample

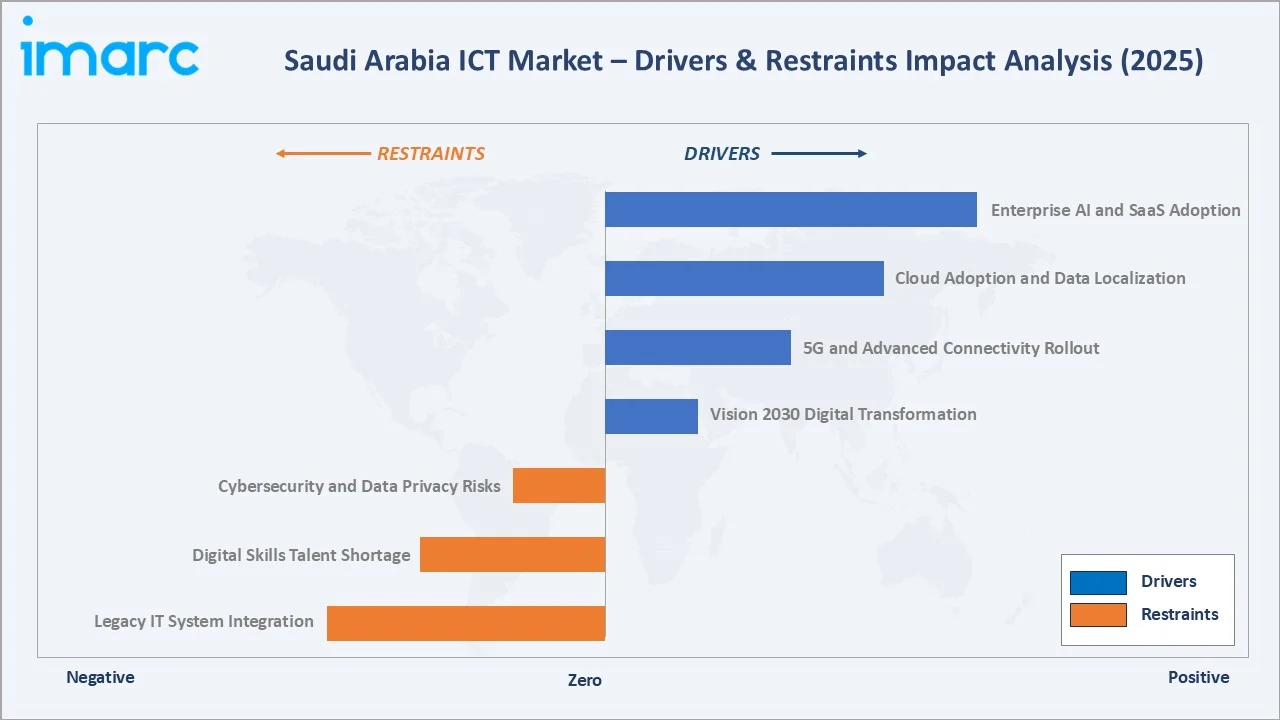

Market Drivers

- Vision 2030 Digital Transformation: Vision 2030 raises ICT's GDP contribution target from ~1% to 5% by 2030, directing multi-billion-dollar capital flows into data centers, AI, 5G, and smart-city platforms including NEOM, Qiddiya, and The Line.

- 5G and Advanced Connectivity Rollout: Saudi Arabia leads GCC in 5G with ~90% urban coverage and 370 Mbps average speeds, supporting 45 million IoT devices, underpinning enterprise, smart-city, and industrial automation applications.

- Cloud Adoption and Data Localization: Data localization policies combined with USD 1.78 Billion AI and data-center investment announced at LEAP 2025, involving Equinix, DAMAC, and Microsoft, are accelerating local cloud capacity and attracting hyperscaler in-country regions.

- Enterprise AI and SaaS Adoption: Enterprise adoption of SaaS, generative AI, and SDAIA-aligned Arabic AI platforms is transforming BFSI, healthcare, and government workflows, propelling a structural shift in ICT spend mix toward software and AI services over hardware.

Market Restraints

- Cybersecurity and Data Privacy Risks: Rapid digitization across government, BFSI, and enterprise sectors has elevated the frequency and sophistication of cyber threats, requiring continuous security spend and regulatory compliance investment under NCA frameworks and PDPL obligations.

- Digital Skills Talent Shortage: A shortage of cloud architects, AI engineers, and cybersecurity specialists constrain large-scale deployments; Huawei's 25,000-by-2030 training target and Microsoft Datacenter Academy address this gap but supply lags demand.

- Legacy IT System Integration: Legacy ERP, core-banking, and government systems require extensive migration and integration engineering to support modern cloud-native and AI-driven architecture, extend project timelines and inflating cost.

Market Opportunities

- Hyperscale Data-Center Expansion: Data-center capacity expansion driven by data localization and AI workloads creates sustained demand for hyperscale build-outs, with Saudi Arabia emerging as a regional hosting hub for AWS, Microsoft, Google Cloud, and Oracle in-country regions.

- AI and Generative AI Adoption: SDAIA-led AI adoption, LEAP-announced AI investments, and NEOM's AI-first design philosophy are creating premium-margin opportunities for Arabic-language AI models, generative AI, and industry-specific analytics platforms across BFSI and healthcare.

- Consumer and Fintech Platform Growth: Fintech, e-commerce, and digital-government platforms targeted at the Kingdom's young, mobile-first population are generating premium-margin ICT spend across payments, identity, digital banking, and citizen service platforms.

Market Challenges

- Project Delivery and Cost Pressure: Rapid Vision 2030 project ramp-up has driven competitive labor demand, escalated ICT project delivery costs, and creating execution risk where specialist talent bottlenecks compress scheduled delivery windows across mega-projects.

- Regulatory Complexity and Compliance Overhead: Divergent regulatory frameworks (CITC, SDAIA, NCA, PDPL) and evolving AI-governance guidelines require continuous compliance engineering and legal review, increasing the cost of go-to-market for both domestic and foreign ICT providers.

Emerging Market Trends

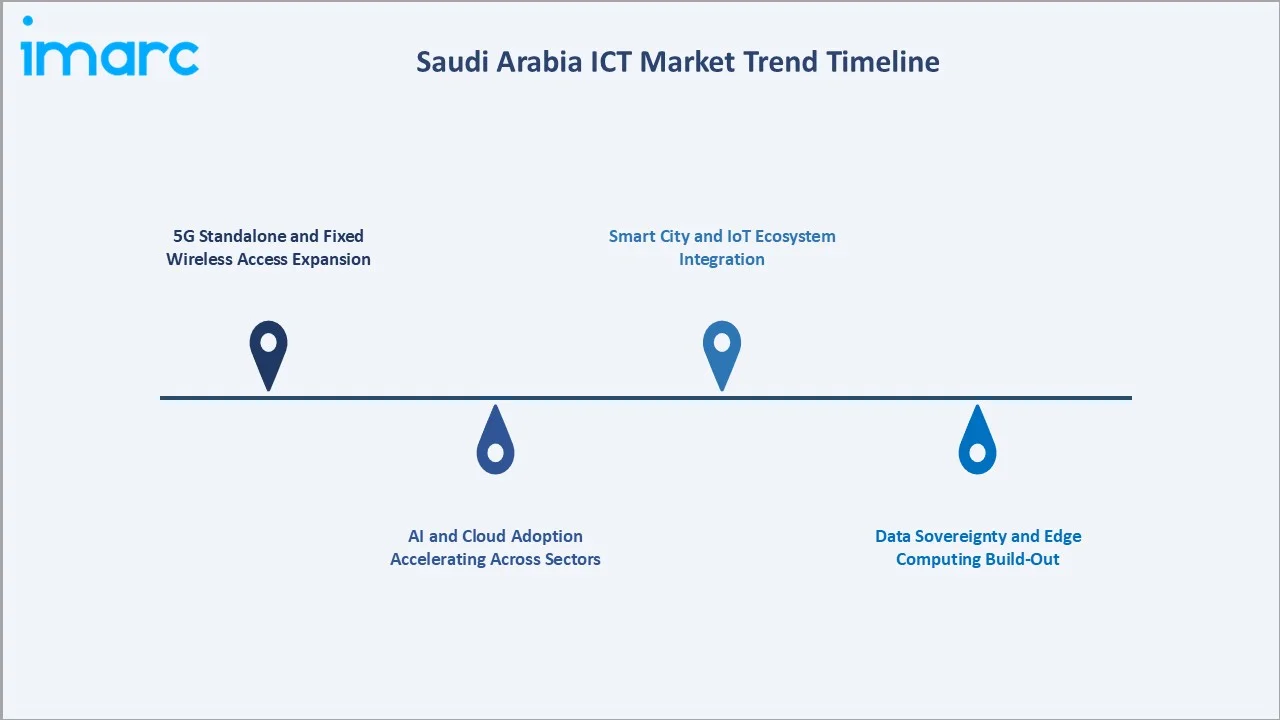

1. 5G Standalone and Fixed Wireless Access Expansion

Zain KSA's 2025 launch of 5G Standalone on 600 MHz in Riyadh and Jeddah enables VoNR, RedCap IoT devices, and network slicing. stc and Mobily are scaling SA rollouts, unlocking fixed wireless access (FWA), enterprise private networks, and low-latency edge computing use cases.

2. AI and Cloud Adoption Accelerating Across Sectors

LEAP 2025's USD 1.78 Billion AI commitment, PIF's Google Cloud Dammam AI hub partnership, and SDAIA's Arabic LLM initiatives are driving enterprise AI adoption across BFSI, healthcare, oil and gas, and government, shifting ICT spend mix toward AI platforms and GPU infrastructure.

3. Smart City and IoT Ecosystem Integration

NEOM, Qiddiya, The Line, and municipal smart-city rollouts are driving integrated IoT-cloud-AI platforms combining mobility sensors, energy management, and citizen service applications, creating a specialized stack distinct from traditional enterprise ICT procurement.

4. Data Sovereignty and Edge Computing Build-Out

Data localization mandates and sovereign cloud requirements are propelling regional data-center expansion by Microsoft, Google, Oracle, and AWS, with edge computing nodes emerging in Riyadh, Jeddah, and Dammam to support latency-sensitive manufacturing and OT workloads.

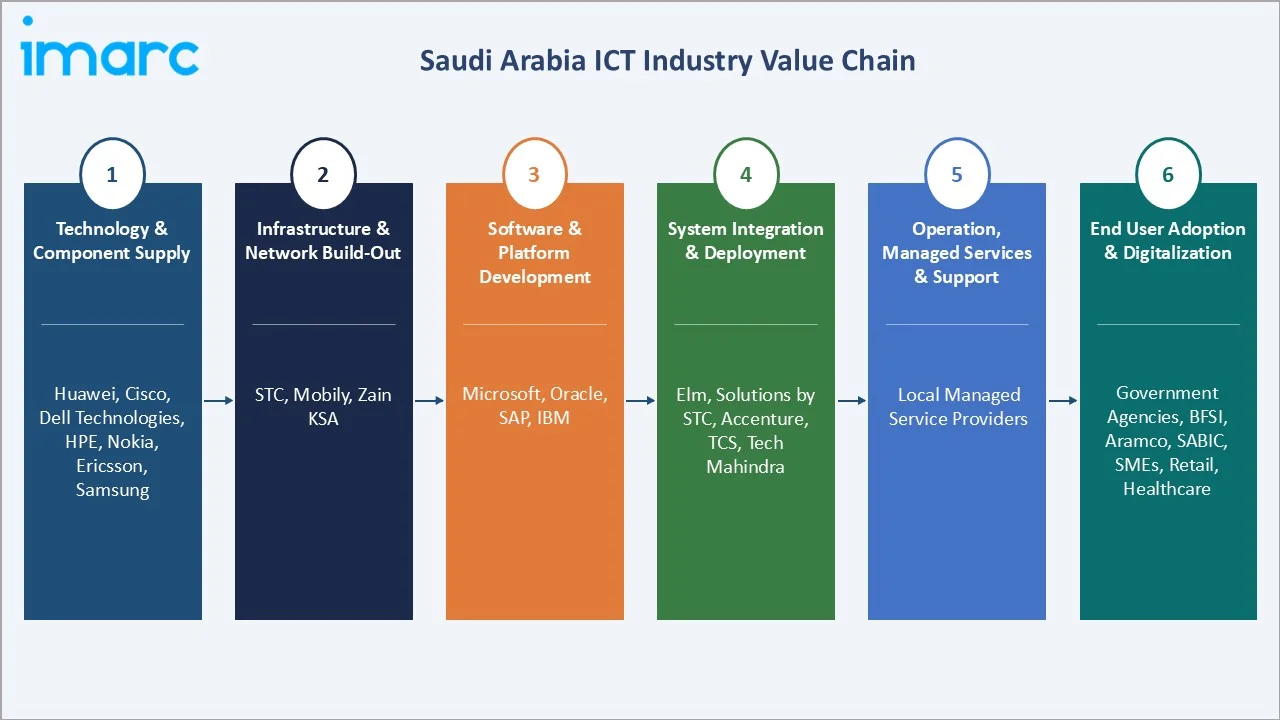

Industry Value Chain Analysis

The Saudi Arabia ICT value chain spans six stages from technology supply through end-user adoption. Software, platform, and managed-services stages capture the highest value-add margins, while infrastructure build-out and system integration generate significant project revenue for capable regional integrators.

|

Stage |

Key Players / Examples |

|

Technology & Component Supply |

Huawei, Cisco, Dell Technologies, HPE, Nokia, Ericsson, Samsung |

|

Infrastructure & Network Build-Out |

stc, Mobily, Zain KSA |

|

Software & Platform Development |

Microsoft, Oracle, SAP, IBM |

|

System Integration & Deployment |

Elm, Solutions by stc, Accenture, TCS, Tech Mahindra |

|

Operation, Managed Services & Support |

Local managed service providers |

|

End User Adoption & Digitalization |

Government agencies, BFSI, Aramco, SABIC, SMEs, retail, healthcare |

Integrated players combining network ownership, data-center capacity, and managed services, notably stc Group and Mobily, capture a disproportionate share of Vision 2030 ICT spend through end-to-end delivery capability that multinational vendors match only via local partnerships.

Technology Landscape in the Saudi Arabia ICT Industry

5G Standalone, FWA, and Network Slicing

5G SA deployments on 600 MHz and 3.5 GHz spectrum enable ultra-reliable low-latency communication for enterprise use cases. Network slicing supports dedicated virtual networks for smart-city, manufacturing OT, and public safety applications, monetizing 5G beyond consumer broadband.

Cloud, Hyperscaler Build-Out, and Hybrid Architectures

Microsoft, Google, Oracle, and AWS have committed to in-country data-center regions to comply with data localization policies. Hybrid architectures combining sovereign cloud, hyperscaler public cloud, and on-premises private cloud are standard for regulated BFSI and government workloads.

AI, Generative AI, and Arabic Language Models

SDAIA-led ALLaM and similar Arabic LLM initiatives, combined with enterprise GenAI pilots in BFSI, healthcare, and customer service, are positioning Saudi Arabia as a regional leader in Arabic-native AI. GPU infrastructure investments support training and inference at scale.

Cybersecurity and Data Sovereignty Architecture

NCA-driven Essential Cybersecurity Controls (ECC) and SDAIA data-protection standards require zero-trust networking, sovereign key management, and local data residency. Saudi firms including Elm and Solutions by stc partner with Palo Alto, Fortinet, and CrowdStrike to deliver compliant offerings.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Hardware |

31.6% |

2025 |

|

Size of Enterprise |

Small and Medium Enterprises |

58.7% |

2025 |

|

Industry Vertica |

🔒 |

🔒 |

2025 |

|

Region |

Northern and Central Region |

35.4% |

2025 |

By Type

Hardware commands a 31.6% share in 2025, anchored by 5G radio access network deployments, hyperscale data-center equipment, enterprise endpoints, and IoT sensor proliferation across smart-city and industrial automation use cases.

To access detailed market analysis, Request Sample

Software at 26.4% is a fast-growing segment, driven by enterprise SaaS adoption, cybersecurity platforms, Arabic-language AI solutions, and core-banking modernization. Growth is reinforced by regulatory sandboxes and SDAIA-backed AI platform initiatives.

IT services at 22.8% in 2025 encompass cloud migration consulting, managed services, and system integration, led by Elm, Accenture, and Tech Mahindra.

By Size of Enterprise

Small and medium enterprises dominate at 58.7% in 2025, reflecting the Kingdom's over 1.3 million SME base and Monsha'at's digital support programs that subsidies SaaS, e-commerce, and cloud adoption. Cloud-based ERP, fintech, and marketing platforms are the fastest-growing SME ICT spend categories.

Large enterprises at 41.3% in 2025 drive premium-margin spend through ERP, cybersecurity, hybrid-cloud, and AI platform investments. Aramco, SABIC, Ma'aden, stc, Al Rajhi Bank, and government ministries anchor enterprise-grade ICT demand, with dedicated IT budgets exceeding regional peers on both absolute and per-employee bases.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Northern and Central Region |

35.4% |

Riyadh digital hub; KAFD; federal ICT spend; Qiddiya |

|

Western Region |

28.9% |

NEOM mega-project; Jeddah commerce; Red Sea connectivity |

|

Eastern Region |

20.7% |

Aramco digital twins; Dhahran R&D; Dammam logistics |

|

Southern Region |

15.0% |

Smart tourism, agri-tech, regional digital inclusion |

The Northern and Central region dominates at 35.4% in 2025, anchored by Riyadh's role as the federal administrative and financial capital. KAFD, SDAIA, CITC, and most ministry digital transformation budgets are concentrated here, alongside the Qiddiya entertainment gigaproject and Saudi headquarters of most global and regional ICT vendors.

The Western region, at 28.9% in 2025, is powered by NEOM's USD 500 Billion build-out, Jeddah's commercial ecosystem, and Red Sea submarine cable landing stations. NEOM's AI-first and smart-city-first design creates specialized ICT procurement distinct from conventional enterprise categories.

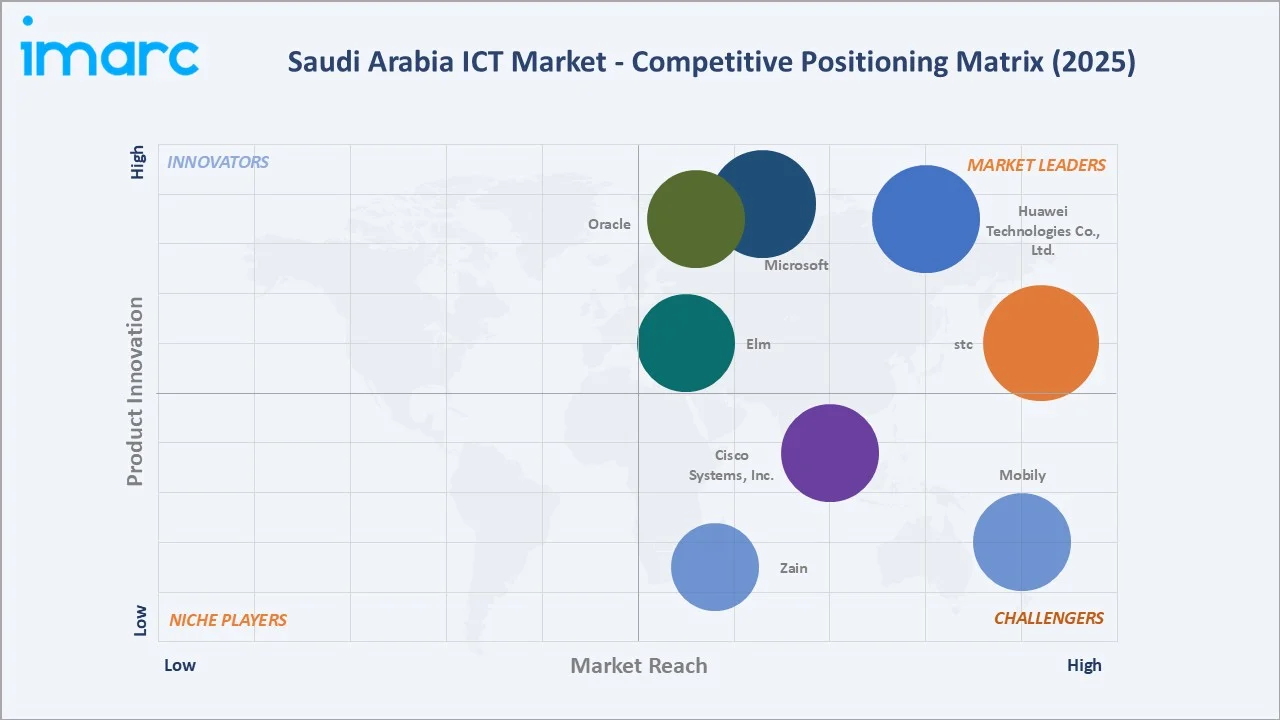

Competitive Landscape

The Saudi Arabia ICT market is moderately consolidated, with three domestic telecom operators (stc, Mobily, Zain KSA) anchoring connectivity, while system integrators (Elm, Solutions by stc) and global vendors (Huawei, Microsoft, Cisco, Oracle, IBM, AWS) compete across hardware, software, and services.

|

Company Name |

Key Products / Offerings |

Market Position |

Strategic Focus |

|

stc |

5G Mobile, FTTH, Solutions by stc |

Leader |

5G leadership; end-to-end digital services; data-center expansion |

|

Mobily |

5G, enterprise connectivity, Mobily Business, fibre, IoT |

Strong Challenger |

Enterprise digital and IoT focus; network densification |

|

Zain |

5G SA, Yaqoot, enterprise fiber, cloud services |

Challenger |

5G SA innovation; 600 MHz rollout; enterprise services |

|

Elm |

Digital government, cybersecurity, smart services |

Leader |

Government digitization; secure platforms; Thiqah integration |

|

Huawei Technologies Co., Ltd. |

5G RAN, cloud, AI platforms, data-center infrastructure |

Leader |

Vision 2030 anchor partner; skills academies; R&D |

|

Microsoft |

Azure, Microsoft 365, Dynamics, AI Copilot, data-center region |

Leader |

AI and cloud localization |

|

Cisco Systems, Inc. |

Networking, security, collaboration, data-center switching |

Challenger |

Enterprise networking; cybersecurity; data-center fabric |

|

Oracle |

OCI cloud regions, database, ERP, industry cloud |

Leader |

OCI cloud region; government and BFSI ERP |

Key players include stc, Mobily, Zain, Elm, Huawei Technologies Co., Ltd., Microsoft, Cisco Systems, Inc., Oracle, and others.

Key Company Profiles

stc

stc is the Kingdom's largest telecom and digital services group, with integrated mobile, fixed, enterprise, data-center, and digital services capabilities. stc's scale, PIF ownership, and Vision 2030 alignment make it the backbone of Saudi Arabia's ICT infrastructure.

- Product Portfolio: 5G, FTTH, Solutions by stc, center3 data centers, stc Pay, Jawwy, stc Play.

- Recent Developments: In December 2025, stc partnered with Six Flags Qiddiya City as its official “Speed Partner,” positioning itself as the primary provider of advanced connectivity and digital infrastructure for the destination. This collaboration supports the park’s launch and aligns with its goal of delivering a seamless, technology-driven visitor experience. Through this partnership, stc is implementing an integrated digital ecosystem designed to enhance the overall guest journey. Its solutions aim to streamline processes, reduce friction, and enable visitors to fully enjoy the entertainment offerings.

- Strategic Focus: stc 's strategy centers on end-to-end digital platform delivery, leveraging 5G scale, fiber reach, and center3 data-center capacity to bundle connectivity, cloud, cybersecurity, and fintech under an integrated enterprise and consumer franchise.

Mobily

Mobily is Saudi Arabia's second-largest telecom operator with strong enterprise, wholesale, and consumer mobile businesses. Mobily's network densification and enterprise IT subsidiary Mobily Infotech enable integrated connectivity and managed-services offerings.

- Product Portfolio: 5G mobile, fiber, IoT, cloud, managed ICT services.

- Recent Developments: In February 2025, Mobily concluded its participation at LEAP 2025 by signing a series of strategic partnership agreements with global, regional, and local technology companies. These agreements span critical technology areas such as digitalization, artificial intelligence, cybersecurity, and IoT. Mobily announced a major investment of approximately $905 million in data centers, submarine cables, and fiber networks, further strengthening its infrastructure and supporting Saudi Arabia’s ambition to become a global digital hub.

- Strategic Focus: Mobily's strategy prioritizes enterprise digital services, IoT platforms, and managed security operations, leveraging its urban-dense 5G footprint and enterprise customer base to grow B2B ICT revenue faster than consumer-mobile average.

Elm

Elm is a leading Saudi digital-services company majority-owned by PIF, specializing in government digitization, secure platforms, and smart-city services. Elm's Thiqah acquisition (USD 907 Million) strengthens its government BPO and digital-services franchise.

- Product Portfolio: Digital government, identity, cybersecurity, smart services.

- Recent Developments: In April 2025, Elm Co. finalized its acquisition of the entire stake held by Public Investment Fund in Thiqah Business Services Co., after meeting all conditions outlined in the share purchase agreement. The company confirmed that all regulatory requirements, including the transfer of ownership, have been completed. The transaction was funded through Elm’s internal resources along with financing facilities, in line with the agreement terms.

- Strategic Focus: Elm's strategy focuses on deep government digitization partnerships, secure identity and payments platforms, and smart-city delivery, positioning it as the primary domestic integrator for Vision 2030 public-sector ICT programs.

Huawei Technologies Co., Ltd.

Huawei is the leading global ICT infrastructure partner in Saudi Arabia, with deep engagements across 5G networks, data centers, cloud services, AI platforms, and workforce development programs aligned to Vision 2030 digital transformation objectives.

- Product Portfolio: 5G RAN and core, HUAWEI CLOUD, AI computing, data-center solutions, enterprise Wi-Fi.

- Recent Developments: In February 2026, Huawei launched its first ICT one-stop training center in Saudi Arabia, reinforcing its commitment to developing local talent and strengthening the Kingdom’s digital capabilities. The new facility is designed to provide comprehensive, hands-on training across key network and infrastructure domains, helping enhance the technical expertise of both Huawei employees and their partners. It aims to improve service delivery standards while supporting large-scale telecom and infrastructure projects across the country.

- Strategic Focus: Huawei's strategy combines large-scale infrastructure delivery, localization partnerships, and skills academies to anchor its role as a Vision 2030 technology backbone, while expanding enterprise cloud and AI offerings to compete with US hyperscalers.

Market Concentration Analysis

The Saudi Arabia ICT market is moderately concentrated, with stc, Mobily, Zain KSA, Elm, and Huawei collectively estimated to hold 55-60% of domestic ICT revenue across connectivity, system integration, and infrastructure layers, while global hyperscalers (Microsoft, Google, AWS, Oracle) are rapidly gaining share via in-country cloud regions.

PIF-led consolidation (Thiqah into Elm, center3 under stc) is restructuring the competitive landscape around scale champions. M&A activity including Happiest Minds' acquisition of Gavs Middle East is bolting regional delivery depth onto mid-tier international players.

Investment & Growth Opportunities

Fastest-Growing Segments

Software at ~5.6% CAGR through 2034 is the highest-growth type segment, driven by enterprise SaaS, AI platforms, and cybersecurity suites. SMEs at ~5.4% CAGR represent the broadest-based opportunity, supported by Monsha'at programs and pay-as-you-go cloud pricing models.

Emerging Regions

The Western Region, anchored by NEOM, is the fastest-growing ICT sub-geography. NEOM's USD 500 Billion build-out, The Line's AI-first smart-city model, and Red Sea tourism gigaprojects create a specialized procurement pipeline for edge computing, IoT, and AI platforms through 2034.

Venture & Investment Trends

PIF, SVC, and sovereign venture funds have allocated USD 700+ Million in AI-compliance and digital-risk venture capital. Foreign direct investment via LEAP 2025 partnerships with Equinix, DAMAC, Microsoft, Huawei, Google, and Oracle is reshaping domestic capacity.

Future Market Outlook (2026-2034)

The Saudi Arabia ICT market is forecast to expand from USD 45.74 Billion in 2025 to USD 72.20 Billion by 2034 at a CAGR of 5.04%, adding USD 26.46 Billion in incremental market value. The trajectory reflects sustained Vision 2030 momentum and compounding digitalization across the economy.

Three technology forces will most significantly shape the market through 2034. First, AI and Arabic-language generative AI will shift software and services spend mix toward premium-margin platforms. Second, sovereign cloud and edge computing will drive data-center capex at 2-3x current levels.

Third, 5G Advanced and early 6G research will redefine enterprise connectivity economics, enabling network-slice-based services and deterministic connectivity for industrial OT, mobility, and immersive consumer applications, creating new monetization layers for telecom operators and enterprise ICT providers.

Research Methodology

Primary Research

Primary research included structured interviews with Saudi telecom executives, SDAIA and NCA public-policy contributors, enterprise CIOs across BFSI, oil and gas, healthcare, and government, and regional channel partners serving Riyadh, Jeddah, and Dammam ICT buyers.

Secondary Research

Key secondary sources include CITC telecommunications indicators, SDAIA AI reports, MCIT Digital Government statistics, stc, Mobily, and Zain financial filings, PIF disclosures, LEAP 2025 announcements, Monsha'at SME statistics, IDC and Gartner regional ICT trackers, and GSMA Intelligence data.

Forecasting Models

Market size estimations used combined top-down (GDP, ICT-to-GDP ratio, government digital spend) and bottom-up (operator revenue, enterprise ICT spend surveys) models. Scenario analysis across Vision 2030 baseline, optimistic, and conservative cases accounts for oil-price and geopolitical variability.

Saudi Arabia ICT Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Hardware, Software, IT Services, Telecommunication Services |

| Size of Enterprises Covered | Small and Medium Enterprises, Large Enterprises |

| Industry Verticals Covered | BFSI, IT and Telecom, Government, Retail and E-commerce, Manufacturing, Energy and Utilities, Others |

| Regions Covered | Northern and Central Region, Western Region, Eastern Region, Southern Region |

| Companies Covered | stc, Mobily, Zain, Elm, Huawei Technologies Co., Ltd., Microsoft, Cisco Systems, Inc., Oracle, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Saudi Arabia ICT market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Saudi Arabia ICT market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Saudi Arabia ICT industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Saudi Arabia ICT Market Report

The Saudi Arabia ICT market reached USD 45.74 Billion in 2025, reflecting consistent demand from Vision 2030 digital transformation, 5G deployment, and enterprise cloud and AI adoption.

The market is projected to reach USD 72.20 Billion by 2034, growing at a CAGR of 5.04% during 2026-2034, driven by smart-city mega-projects, cloud localization, and enterprise AI adoption.

Hardware leads with 31.6% type share in 2025, supported by data-center build-out, 5G radio access network expansion, enterprise endpoint refresh cycles, and IoT sensor adoption.

Small and Medium Enterprises lead at 58.7% in 2025, benefiting from Monsha'at digital support programs, affordable SaaS offerings, and fast-growing fintech and e-commerce adoption.

The Northern and Central Region commands a dominant 35.4% share in 2025, led by Riyadh's role as the federal, financial, and corporate capital of Saudi Arabia.

Software is among the fastest-growing type segments, driven by enterprise SaaS, Arabic AI platforms, SDAIA-backed generative AI initiatives, and NCA-mandated cybersecurity software.

Leading players include stc, Mobily, Zain, Elm, Huawei Technologies Co., Ltd., Microsoft, Cisco Systems, Inc., Oracle, and others.

Key applications include e-government, smart-city platforms, BFSI digital banking, oilfield digitization, healthcare informatics, retail and e-commerce platforms, and smart-tourism services across Vision 2030 pillars.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)