Saudi Arabia Industrial Robotics for Assembly Lines Market Size, Share, Trends and Forecast by Robot Type, Payload Capacity, Application, End-Use Industry, and Region, 2026-2034

Saudi Arabia Industrial Robotics for Assembly Lines Market Summary:

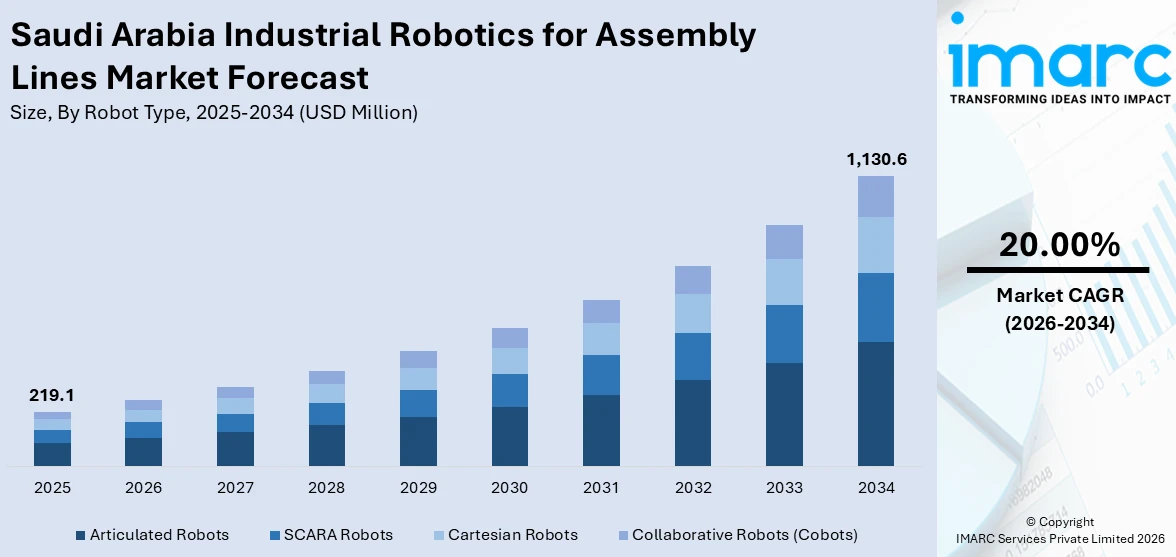

The Saudi Arabia industrial robotics for assembly lines market size was valued at USD 219.1 Million in 2025 and is projected to reach USD 1,130.6 Million by 2034, growing at a compound annual growth rate of 20.00% from 2026-2034.

The market is experiencing robust expansion driven by the Kingdom's strategic industrial transformation under Vision 2030, which prioritizes localized manufacturing and advanced automation technologies. Rising investments in automotive production facilities, electronics manufacturing, and metal fabrication are accelerating robotics adoption across assembly operations. Additionally, the shortage of skilled technical labor is pushing manufacturers toward automated solutions to maintain production efficiency and quality standards, significantly expanding the Saudi Arabia industrial robotics for assembly lines market share.

Key Takeaways and Insights:

- By Robot Type: Articulated robots dominate the market with a share of 42% in 2025, driven by their versatility across welding, painting, and complex assembly operations in automotive manufacturing.

- By Payload Capacity: 5 to 10 Kg leads with a share of 30% in 2025, reflecting widespread adoption in electronics assembly and automotive component handling applications.

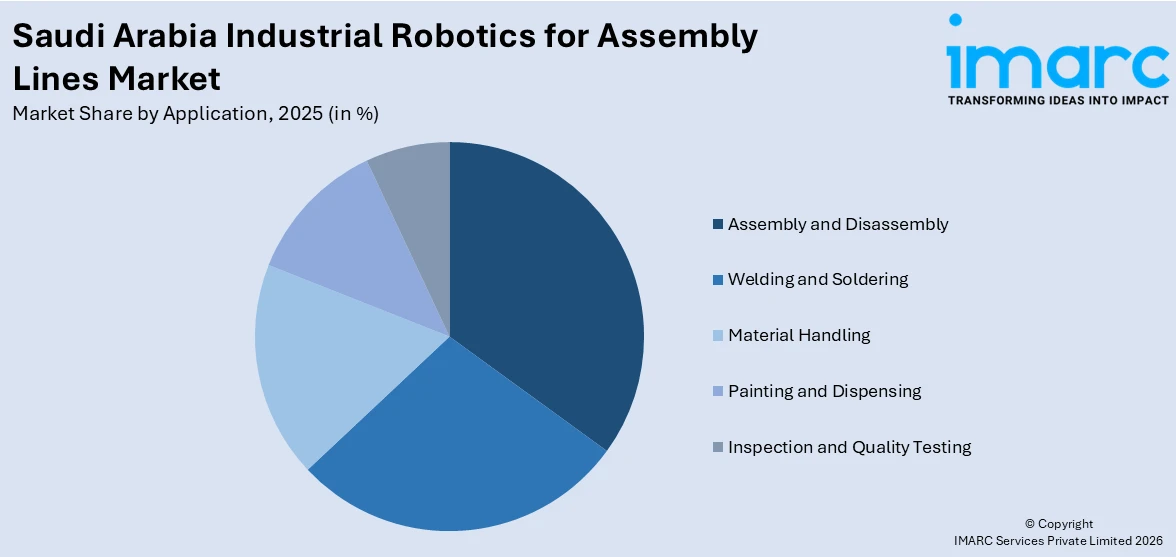

- By Application: Assembly and disassembly hold the largest share at 33% in 2025, supported by extensive integration in automotive production lines and electronics manufacturing facilities.

- By End-Use Industry: Automotive represents the largest share at 25% in 2025, fueled by major electric vehicle manufacturing initiatives and local production targets.

- By Region: The Northern and central region leads with 32% market share in 2025, anchored by Riyadh's position as the hub for advanced manufacturing infrastructure and government-backed automation initiatives.

- Key Players: The competitive landscape features both international robotics manufacturers and emerging local partnerships focused on establishing Saudi Arabia as a regional automation center through technology localization and manufacturing capacity development.

To get more information on this market Request Sample

Saudi Arabia's industrial robotics sector is transitioning from traditional automation to AI-powered smart manufacturing systems, driven by the Kingdom's ambitious Vision 2030 economic diversification strategy. The National Industrial Development and Logistics Program has identified over 800 investment opportunities worth approximately $266.4 billion, creating substantial demand for advanced robotic systems across manufacturing operations. In February 2024, Alat and SoftBank Group announced a USD 150 million joint venture to establish a fully automated manufacturing and engineering hub in Riyadh, with the facility expected to contribute USD 1 billion to Saudi Arabia's GDP by 2025. This development exemplifies the Kingdom's commitment to building indigenous robotics capabilities while attracting foreign technology partnerships. The automotive sector is experiencing particularly strong momentum, with Ceer's SAR 5 billion electric vehicle manufacturing complex in King Abdullah Economic City integrating robotics across stamping, welding, painting, and assembly operations. Meanwhile, electronics and semiconductor manufacturing initiatives are driving demand for precision robotics in clean room environments, positioning Saudi Arabia as an emerging hub for high-tech industrial automation throughout the Middle East region.

Saudi Arabia Industrial Robotics for Assembly Lines Market Trends:

Integration of Artificial Intelligence (AI) and Industrial Internet of Things (IIoT)

The convergence of AI and IoT technologies is fundamentally transforming Saudi Arabia's industrial robotics landscape, enabling predictive maintenance, real-time quality control, and adaptive manufacturing processes. Manufacturers are deploying smart robotic systems capable of learning from production data, optimizing workflows autonomously, and communicating seamlessly with other factory equipment through IoT networks. In 2025, Humanoid, an AI and robotics firm based in the UK, opened the first specialized humanoid robotics showroom in Riyadh in partnership with QSS AI & Robotics, the top robotics and AI company in Saudi Arabia aimed at localizing advanced technologies. The launch represents a significant advancement for AI innovation in the area and is part of a strategic alliance aimed at speeding up humanoid integration across vital sectors in the Kingdom.

Localization of Robotic Manufacturing and Technology Transfer

Saudi Arabia is establishing indigenous robotics manufacturing capabilities through strategic partnerships with global technology leaders, reducing dependence on imports while building local engineering expertise. This localization strategy encompasses not only robot assembly but also development of supporting ecosystems including component suppliers, system integrators, and maintenance service providers. Saudi Arabia revealed new initiatives that will utilize AI to facilitate the export of domestically-produced robots and improve efficiencies in the mining industry, amidst ongoing foreign direct investment influxes. The country acquired in foreign direct investment totaling 900 billion Saudi riyals ($240 billion), which has increased twofold since the inception of the Vision 2030 economic initiative in 2016, stated the kingdom’s Minister of Investment during the PIF Private Sector Forum in Riyadh.

Government-Driven Industrial Transformation Under Vision 2030

The Saudi government's comprehensive industrial modernization initiative is creating unprecedented demand for automation technologies across manufacturing sectors. Vision 2030's focus on economic diversification has mobilized substantial public and private investments in smart manufacturing infrastructure, with targeted programs supporting robotics adoption through financial incentives, regulatory frameworks, and skills development initiatives. In 2025, DBR77 signed a strategic memorandum of understanding with the Saudi Ministry of Industry to support the Future Factory Program, while the Advanced Manufacturing Hub Strategy outlined over 800 investment opportunities worth approximately USD 273 billion to accelerate deployment of Industry 4.0 technologies across Saudi Arabia's manufacturing landscape.

How Vision 2030 is Transforming the Saudi Arabia Industrial Robotics for Assembly Lines market:

Saudi Arabia’s Vision 2030 is playing a major role in transforming the industrial robotics market for assembly lines by accelerating automation, localization, and advanced manufacturing. As part of its goal to diversify the economy beyond oil, the Kingdom is investing heavily in smart factories, Industry 4.0 technologies, and digital transformation. This has increased demand for industrial robots that improve precision, productivity, and consistency in assembly line operations across sectors such as automotive, electronics, food processing, and pharmaceuticals. Government-backed initiatives like the National Industrial Development and Logistics Program (NIDLP) encourage manufacturers to adopt robotics to enhance global competitiveness and reduce operational costs. Vision 2030 also promotes local content and skills development, leading to partnerships with global robotics providers and the growth of local system integrators. Additionally, rising labor efficiency goals and workplace safety standards are pushing companies to automate repetitive and hazardous tasks. Together, these efforts are positioning Saudi Arabia as a regional hub for advanced, robotics-driven manufacturing.

Market Outlook 2026-2034:

The Saudi Arabia industrial robotics for assembly lines market is positioned for substantial growth as manufacturers accelerate automation investments to meet production targets under Vision 2030's economic diversification mandate. The market generated a revenue of USD 219.1 Million in 2025 and is projected to reach a revenue of USD 1,130.6 Million by 2034, growing at a compound annual growth rate of 20.00% from 2026-2034. The automotive sector's expansion, led by major electric vehicle manufacturing projects, will drive significant demand for sophisticated robotic systems capable of handling complex assembly operations with precision and flexibility. Electronics and semiconductor manufacturing initiatives are simultaneously creating opportunities for specialized robotics applications in clean room environments.

Saudi Arabia Industrial Robotics for Assembly Lines Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Robot Type |

Articulated Robots |

42% |

|

Payload Capacity |

5 to 10 Kg |

30% |

|

Application |

Assembly and Disassembly |

33% |

|

End-Use Industry |

Automotive |

25% |

|

Region |

Northern and Central Region |

32% |

Robot Type Insights:

- Articulated Robots

- SCARA Robots

- Cartesian Robots

- Collaborative Robots (Cobots)

Articulated robots dominate with a market share of 42% of the total Saudi Arabia industrial robotics for assembly lines market in 2025.

Articulated robots have emerged as the preferred solution for Saudi Arabia's expanding manufacturing sector due to their exceptional versatility, extensive range of motion, and ability to perform complex operations in confined spaces. These multi-jointed robotic systems excel in applications requiring high precision and flexibility, particularly in automotive assembly lines where they handle welding, painting, material handling, and intricate component installation tasks. The Kingdom's automotive manufacturing expansion, exemplified by Ceer's electric vehicle complex in King Abdullah Economic City, relies heavily on articulated robots integrated across stamping, welding, painting, and final assembly operations to ensure production precision while reducing cycle times and enhancing workplace safety standards throughout manufacturing facilities.

The adoption of articulated robots is accelerating as Saudi manufacturers recognize their capability to be reprogrammed for multiple tasks, providing crucial production flexibility as companies scale operations and introduce new product lines. Electronics manufacturers particularly value these systems for precision assembly work, while metal fabrication facilities utilize them for complex welding patterns and material positioning. The robots' sophisticated control systems enable seamless integration with AI-powered quality inspection systems and IoT monitoring platforms, aligning with Vision 2030's emphasis on smart manufacturing infrastructure that enhances operational efficiency and competitive positioning in regional and global markets.

Payload Capacity Insights:

- Up to 5 Kg

- 5 to 10 Kg

- 10 to 20 Kg

- Above 20 Kg

5 to 10 Kg leads with a share of 30% of the total Saudi Arabia industrial robotics for assembly lines market in 2025.

The 5 to 10 kilogram payload capacity segment represents the optimal balance between precision handling and operational flexibility for Saudi Arabia's primary manufacturing applications. This weight class is particularly suited for electronics assembly operations, automotive component handling, and pharmaceutical packaging tasks that demand careful manipulation without the complexity and cost associated with heavier-duty systems. The segment's prominence reflects the Kingdom's strategic focus on high-value manufacturing sectors including electric vehicle battery assembly, electronic component production, and precision machinery fabrication, where components typically fall within this weight range and require consistent, accurate positioning throughout production processes.

Manufacturers are increasingly deploying robots in this payload category as Saudi Arabia develops its automotive supply chain ecosystem, with battery pack assembly, powertrain component installation, and electronic control unit integration all requiring handling capabilities in the 5-10 kilogram range. The collaborative robot subset within this payload class is experiencing particularly strong adoption, as these systems can work safely alongside human operators without extensive safety barriers, optimizing factory floor space while maintaining productivity standards. Electronics manufacturers establishing operations in industrial zones like NEOM and King Abdullah Economic City specifically select this payload range for circuit board assembly, component testing, and quality inspection applications that demand precision manipulation combined with rapid cycle times to meet competitive production targets.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Welding and Soldering

- Material Handling

- Assembly and Disassembly

- Painting and Dispensing

- Inspection and Quality Testing

Assembly and disassembly exhibit a clear dominance with a 33% share of the total Saudi Arabia industrial robotics for assembly lines market in 2025.

Assembly and disassembly operations constitute the core application driving industrial robotics adoption across Saudi Arabia's manufacturing sector, encompassing component integration, product assembly, fastening operations, and systematic disassembly for maintenance or recycling purposes. The automotive industry's expansion has created particularly strong demand for robotic assembly systems, with electric vehicle production requiring precise installation of battery modules, powertrain components, electronic systems, and interior fixtures. Electronics manufacturers are deploying sophisticated assembly robotics for circuit board population, device enclosure assembly, and component integration tasks that demand sub-millimeter precision and consistent quality across high-volume production runs.

The ability of modern robotic systems to be rapidly reprogrammed for different assembly sequences provides crucial flexibility as manufacturers respond to product design changes and market demands. Additionally, these systems integrate seamlessly with automated quality inspection technologies, using computer vision and sensor arrays to verify assembly accuracy in real-time and automatically flag defective units, thereby reducing waste while ensuring that finished products meet international quality standards required for both domestic consumption and export markets targeted under Vision 2030's economic diversification strategy.

End-Use Industry Insights:

- Automotive

- Electronics and Semiconductor

- Metal and Machinery

- Plastics and Chemicals

- Food and Beverage

- Others

Automotive leads with a share of 25% of the total Saudi Arabia industrial robotics for assembly lines market in 2025.

The automotive industry has emerged as the primary driver of industrial robotics demand in Saudi Arabia, reflecting the Kingdom's strategic commitment to establishing a domestic vehicle manufacturing ecosystem under Vision 2030's economic diversification framework. This sector's dominance is anchored by major initiatives including Ceer's SAR 5 billion (USD 1.3 billion) electric vehicle manufacturing complex in King Abdullah Economic City, which employs extensive robotics integration across stamping, welding, painting, and assembly operations. In March 2024, Ceer commenced construction of this state-of-the-art facility designed to produce both sedans and SUVs, with production increasing passenger vehicles annually by the decade's end, necessitating deployment of hundreds of robotic systems throughout the manufacturing value chain.

The automotive robotics market extends beyond vehicle assembly to encompass component manufacturing, with local production of batteries, powertrains, and electronic control systems requiring precision automation throughout sub-assembly operations. Robotics plays an indispensable role in ensuring production consistency, minimizing defects, reducing cycle times, and maintaining the workplace safety standards essential in automotive manufacturing environments. Vision 2030 specifically targets the establishment of original equipment manufacturers producing passenger vehicles annually within the Kingdom by 2030, creating sustained demand for advanced robotic systems. Furthermore, the emphasis on electric vehicle production intensifies robotics requirements, as EV manufacturing involves additional complexity in battery pack assembly, high-voltage electrical system integration, and advanced driver assistance system installation, all demanding the precision and consistency that industrial robotics uniquely provide.

Regional Insights:

- Northern and Central Region

- Western Region

- Eastern Region

- Southern Region

Northern and central region exhibits a clear dominance with a 32% share of the total Saudi Arabia industrial robotics for assembly lines market in 2025.

The Northern and Central Region, anchored by Riyadh, serves as Saudi Arabia's primary hub for industrial robotics deployment, benefiting from concentration of government-backed manufacturing initiatives, advanced infrastructure development, and strategic proximity to decision-making centers driving Vision 2030 implementation. This region hosts major automation projects designed to produce next-generation industrial robots for local and global markets. The Advanced Manufacturing Hub Strategy has identified substantial investment opportunities within this region, with industrial clusters increasingly equipped with robotic systems to enhance production capacity, quality control, and operational efficiency across diverse manufacturing sectors.

Riyadh's position as the capital provides access to skilled technical talent, research institutions, and government support programs facilitating robotics adoption among manufacturers. The region's industrial zones are attracting major technology investments such as Lenovo's 200,000 square meter manufacturing facility designed to employ robotics extensively in electronics production. Additionally, the Northern and Central Region benefits from government initiatives promoting smart manufacturing technologies, with the Saudi Authority for Industrial Cities and Technology Zones (MODON) providing incentives for automation investments. The concentration of automotive component suppliers, electronics manufacturers, and machinery producers in areas surrounding Riyadh creates robust demand for assembly line robotics, while the region's logistics infrastructure ensures efficient distribution of manufactured products to domestic and export markets.

Market Dynamics:

Growth Drivers:

Why is the Saudi Arabia Industrial Robotics for Assembly Lines Market Growing?

Vision 2030 and Advanced Manufacturing Hub Strategy

The Saudi government's comprehensive economic transformation program has established industrial automation as a central pillar for achieving diversification away from hydrocarbon dependence, creating unprecedented momentum for robotics adoption across manufacturing sectors. Vision 2030's specific emphasis on localizing production, developing high-value industries, and enhancing global competitiveness has mobilized substantial public and private capital toward smart manufacturing infrastructure. Government-backed entities including the Saudi Authority for Industrial Cities and Technology Zones (MODON) and the National Industrial Development and Logistics Program (NIDLP) are actively incentivizing investments in robotics, artificial intelligence, and Industry 4.0 technologies through targeted funding programs, regulatory support, and infrastructure development initiatives. In 2025, the Ministry of Industry and Mineral Resources in Saudi Arabia has collaborated with King Abdullah University of Science and Technology (KAUST) to initiate a strategic program aimed at speeding up the implementation of advanced manufacturing technologies throughout the Kingdom's industrial sector.

Expansion of Automotive Production and EV Manufacturing

Saudi Arabia's accelerating domestic automotive production is creating substantial demand for industrial robotics throughout manufacturing value chains, particularly as the Kingdom pursues ambitious targets to establish itself as a regional automotive manufacturing hub. Vision 2030 specifically targets the establishment of original equipment manufacturers capable of producing passenger vehicles annually within the Kingdom by 2030, representing a transformative shift requiring extensive automation infrastructure. Electric vehicle production particularly intensifies robotics requirements due to complex battery pack assembly procedures, high-voltage electrical system integration challenges, and advanced driver assistance system installation demands, all necessitating the consistency and precision that industrial robotics uniquely deliver across modern automotive manufacturing facilities. IMARC Group predicts that the Saudi Arabia electric car market is projected to attain USD 5.52 Billion by 2034.

Labor Shortage and Skilled Workforce Constraints

The persistent scarcity of skilled technical labor represents a fundamental structural driver propelling industrial robotics adoption as Saudi manufacturers seek to maintain production volumes, ensure quality consistency, and achieve operational efficiency targets despite workforce availability challenges. Currently, a limited percentage of the Kingdom's workforce possesses the necessary technical skills to operate and maintain advanced manufacturing systems, with industry assessments indicating that a heightened need for additional trained professionals to meet escalating demand across automation-intensive sectors. Manufacturers operating in high-risk environments, including petrochemical facilities and metal fabrication plants, are adopting robotic handling and assembly systems to simultaneously address workforce shortages while meeting stringent safety standards and productivity objectives, positioning automation as a strategic response to fundamental labor market constraints rather than merely an efficiency enhancement initiative. The United Arab Emirates and Saudi Arabia are projected to need more than 1.5 million new workers by 2030. The kingdom will need approximately 650,000 additional employees to meet its developmental goals without the productivity improvements enabled by AI.

Market Restraints:

What Challenges the Saudi Arabia Industrial Robotics for Assembly Lines Market is Facing?

High Initial Capital Investment Requirements

The substantial upfront costs associated with implementing industrial robotics systems represent a significant barrier to adoption, particularly for small and medium-sized manufacturing enterprises operating with constrained capital budgets. Companies face initial investments frequently exceeding for comprehensive advanced automation systems, encompassing robot hardware, specialized tooling, programming interfaces, safety equipment, facility modifications, and integration with existing production infrastructure. These financial requirements extend beyond equipment procurement to include expenses for employee training, process redesign, system commissioning, and ongoing technical support, creating total cost of ownership considerations that can delay or prevent automation initiatives. Smaller manufacturers may find these investment thresholds prohibitive despite recognizing long-term efficiency benefits, limiting market penetration beyond large enterprises and government-backed industrial projects. Additionally, concerns about return on investment timelines in markets experiencing rapid technological evolution can create hesitation among decision-makers evaluating automation strategies.

Shortage of Skilled Technical Workforce for Robotics Operation

The severe scarcity of personnel with specialized knowledge in robotics programming, maintenance, and system integration represents a critical constraint on market expansion, as sophisticated automation systems require trained operators and technicians to achieve optimal performance. A major percent of manufacturing companies anticipate challenges in recruiting qualified personnel capable of implementing and maintaining AI-powered robotic systems, with current workforce skill levels insufficient to support large-scale automation deployment. This skills gap leads to inefficient utilization of robotics investments, increased downtime due to maintenance delays, extended commissioning periods, and suboptimal programming that fails to realize theoretical productivity improvements. The shortage extends across multiple technical disciplines including mechanical engineering, electrical systems, software programming, and industrial process optimization, requiring comprehensive training infrastructure that remains underdeveloped relative to market needs. Educational institutions are gradually expanding robotics and automation curricula, but near-term supply of qualified technicians remains inadequate to meet accelerating industrial demand driven by Vision 2030 initiatives.

Technology Integration and Legacy System Compatibility

Manufacturers face substantial technical challenges in integrating advanced robotic systems with existing production equipment, enterprise resource planning systems, and quality management platforms, particularly when modernizing facilities constructed around legacy technologies. Achieving seamless interoperability between new automation equipment and established manufacturing infrastructure requires specialized expertise, custom interface development, and careful process engineering to prevent disruptions to ongoing production. Many Saudi industrial facilities operate machinery and control systems from multiple vendors spanning different technological generations, creating compatibility complexities when implementing Industry 4.0-enabled robotics featuring IoT connectivity and cloud-based monitoring capabilities. Cybersecurity concerns associated with networked manufacturing systems add additional complexity, as companies must protect proprietary production data and prevent unauthorized access while enabling the connectivity necessary for smart manufacturing benefits. These integration challenges can extend implementation timelines, increase project costs beyond initial estimates, and create operational risks if not carefully managed throughout deployment and commissioning phases.

Competitive Landscape:

The Saudi Arabia industrial robotics for assembly lines market features a competitive landscape characterized by both established international robotics manufacturers and emerging local partnerships focused on technology localization and indigenous capability development. Global industry leaders maintain market presence through direct sales channels, authorized distributors, and strategic partnerships with local system integrators who provide customization and after-sales support services. The market is experiencing a transformative shift with the emergence of Saudi-backed manufacturing initiatives. This development signals the Kingdom's strategic intent to build domestic manufacturing capacity while reducing import dependence and fostering technology transfer that develops local engineering expertise across robotics design, production, and maintenance disciplines.

Saudi Arabia Industrial Robotics for Assembly Lines Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Robot Types Covered | Articulated Robots, SCARA Robots, Cartesian Robots, Collaborative Robots (Cobots) |

| Payload Capacities Covered | Up to 5 Kg, 5 to 10Kg, 10 to 20 Kg, Above 20 Kg |

| Applications Covered | Welding and Soldering, Material Handling, Assembly and Disassembly, Painting and Dispensing, Inspection and Quality Testing |

| End-Use Industries Covered | Automotive, Electronics and Semiconductor, Metal and Machinery, Plastics and Chemicals, Food and Beverage, Others |

| Regions Covered | Northern and Central Region, Western Region, Eastern Region, Southern Region |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Saudi Arabia Industrial Robotics for Assembly Lines Market Report

The Saudi Arabia industrial robotics for assembly lines market size was valued at USD 219.1 Million in 2025.

The Saudi Arabia industrial robotics for assembly lines market is expected to grow at a compound annual growth rate of 20.00% from 2026-2034 to reach USD 1,130.6 Million by 2034.

Articulated robots dominate the market with a 42% share in 2025, driven by their exceptional versatility and extensive application across automotive welding, painting, and complex assembly operations. These multi-jointed systems provide the flexibility necessary for diverse manufacturing tasks while delivering the precision required in high-value industries including electric vehicle production and electronics assembly throughout the Kingdom's expanding industrial base.

Key factors driving the Saudi Arabia industrial robotics for assembly lines market include comprehensive government support under Vision 2030's industrial transformation agenda, accelerating automotive production initiatives particularly in electric vehicle manufacturing, and persistent skilled labor shortages compelling manufacturers to adopt automation solutions.

Major challenges include high initial capital investment requirements frequently exceeding million for comprehensive systems, severe shortage of skilled personnel possessing necessary technical capabilities, and complex technology integration requirements when incorporating advanced robotics with existing production infrastructure and legacy systems. These barriers particularly impact small and medium-sized enterprises while creating workforce development imperatives and necessitating careful project planning for successful automation implementation across the manufacturing sector.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade