Saudi Arabia Laundry Detergent Market Size, Share, Trends and Forecast by Product Type, Distribution Channel, Application, and Region, 2026-2034

Saudi Arabia Laundry Detergent Market Size, Share, Trends & Forecast (2026-2034)

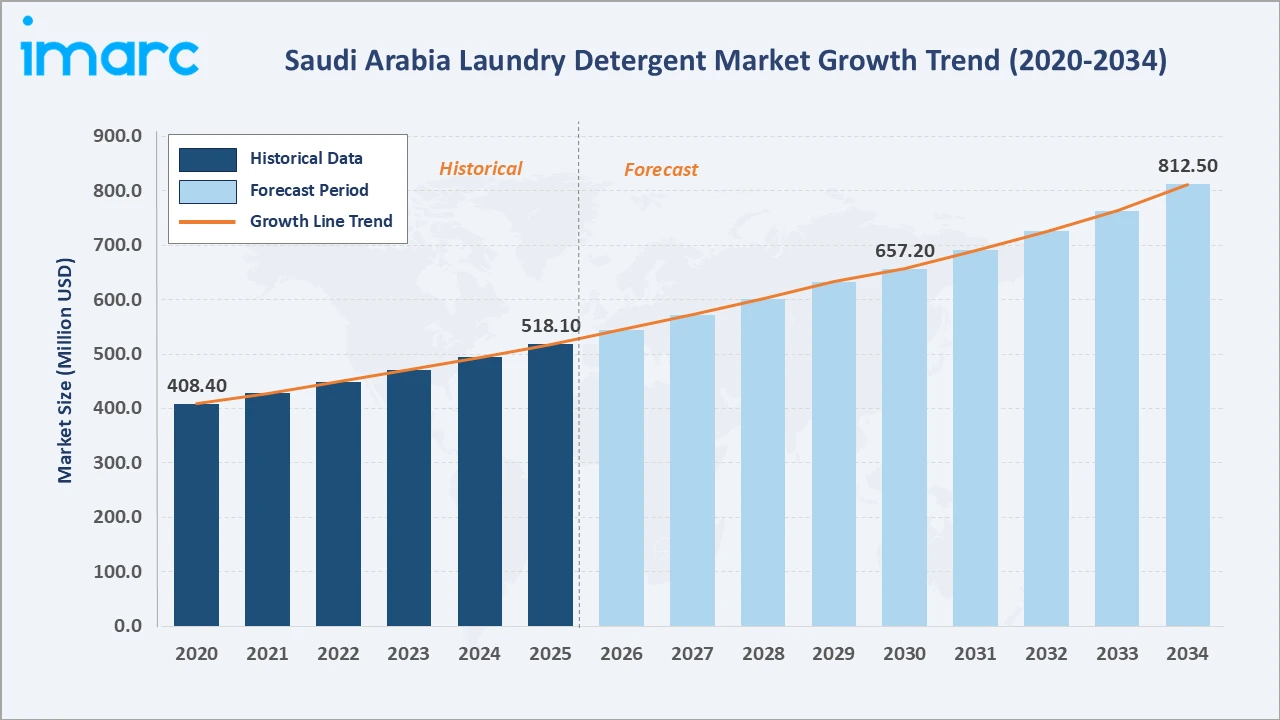

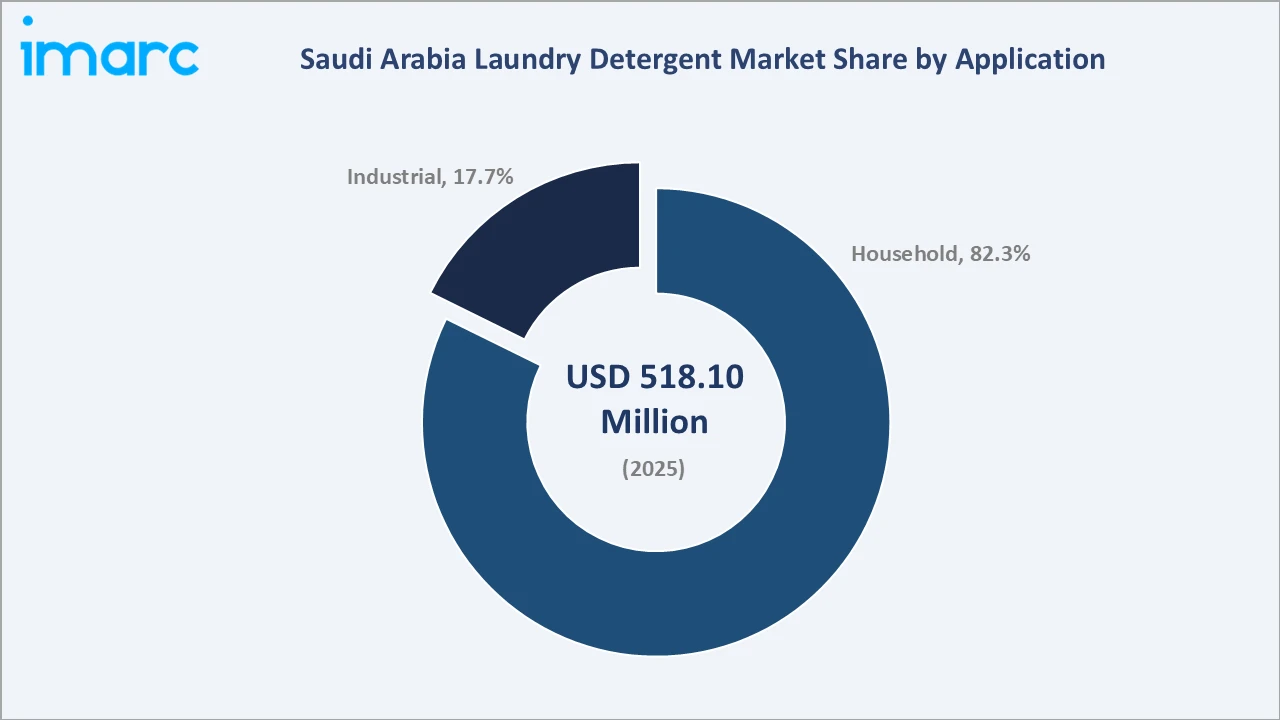

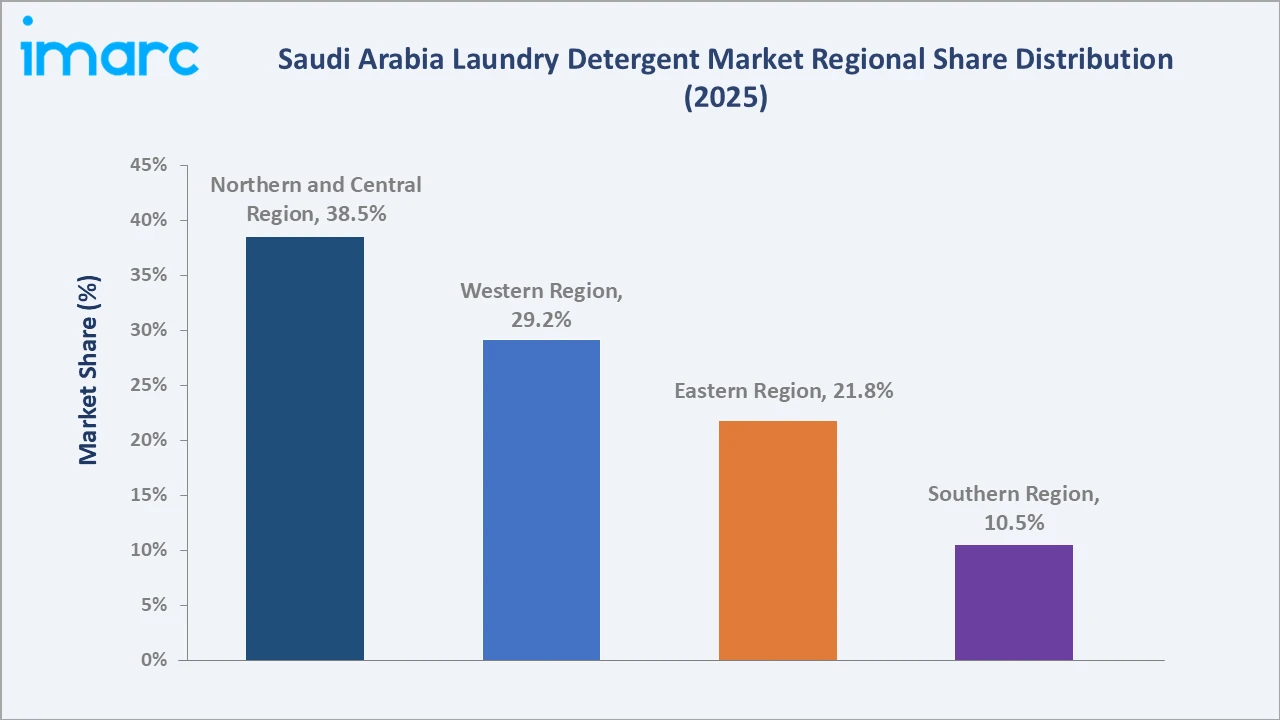

The Saudi Arabia laundry detergent market reached USD 518.1 Million in 2025 and is projected to reach USD 812.5 Million by 2034, exhibiting a CAGR of 4.87% during 2026-2034. Growth is anchored in the Kingdom's expanding population, which the General Authority for Statistics (GASTAT) estimated at around 35 million in mid-2024, alongside rising household formation and organized retail expansion. Powder remains the leading product type at 43.7% share (2025), while household application dominates end-use consumption at 82.3%. The Northern and Central Region, anchored by Riyadh, leads regionally at 38.5% share, supported by the highest population density and retail infrastructure concentration in the Kingdom.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 518.1 Million |

|

Forecast Market Size (2034) |

USD 812.5 Million |

|

CAGR (2026-2034) |

4.87% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

| Largest Product Type |

Powder (43.7%, 2025) |

| Largest Application |

Household (82.3%, 2025) |

| Dominant Region |

Northern & Central Region (38.5%, 2025) |

The market expanded from USD 408.4 Million in 2020 to USD 518.1 Million in 2025, is anchored at USD 657.2 Million by 2030, and is forecast to reach USD 812.5 Million by 2034. This trajectory reflects steady demand growth supported by population expansion, rising disposable incomes under Vision 2030's economic diversification, and gradual premiumization of the product mix toward liquid and pods/tablets formats.

To get more information on this market, Request Sample

Pods/Tablets represent the fastest-growing product type at an estimated 7.9% CAGR (2026-2034), reflecting rising consumer preference for convenient, pre-measured dosing formats. Liquid detergents follow at an estimated 5.7% CAGR, outpacing Powder's more moderate 3.3% growth as urban households increasingly shift toward premium, machine-friendly formulations suited to automatic washing machines.

Executive Summary

The Saudi Arabia laundry detergent market reached USD 518.1 Million in 2025, driven by the Kingdom's expanding population of approx. 35 million (GASTAT, 2024), a young demographic base with 71% of Saudi nationals under the age of 35, and continued organized retail expansion across the Kingdom's major cities. The market is projected to reach USD 812.5 Million by 2034 at a 4.87% CAGR, reflecting steady, structurally supported growth in one of the Gulf Cooperation Council's largest household and personal care markets.

Powder detergents command 43.7% of the 2025 market, reflecting entrenched consumer habits and cost-efficiency for larger family households, whose average size stood at approximately 5 members according to GASTAT's 2024 Family Statistics Report. Liquid detergents hold the second-largest share at 34.2%, supported by rising automatic washing machine penetration and premiumization trends. Household application dominates at 82.3% share, while the Northern and Central Region leads regionally at 38.5%, anchored by Riyadh's population concentration and retail density.

International manufacturers, including Procter & Gamble and Henkel, maintain established local manufacturing and distribution operations in the Kingdom, while domestic producers continue to expand private-label and industrial-grade offerings. The market outlook remains positive, supported by Vision 2030's industrial localization agenda, sustained urbanization, and rising demand for premium and eco-conscious laundry care formats through 2034.

Key Market Insights

|

Insight |

Data |

| Largest Product Type |

Powder - 43.7% share (2025) |

| Leading Application |

Household - 38.5% share (2025) |

|

Leading Region |

Northern and Central Region - 42.6% share (2025) |

| Fastest Growing Product Type | Pods/Tablets - ~7.9% CAGR (2026-2034) |

| Top Companies | The Procter & Gamble Company (P&G), Henkel AG & Co. KGaA, Unilever, and Saudi Industrial Detergent Company (SIDCO) |

| Market Opportunity | Domestic manufacturing localization under Vision 2030 |

Key Analytical Observations Supporting The Above Data:

- Powder leads at 43.7% share (2025) anchored by affordability and household scale: Saudi Arabia's average household size of approximately five members, per GASTAT's 2024 Family Statistics Report, sustains demand for cost-efficient, high-volume powder formats among multi-member Saudi families, which constitute about 86% of all households.

- Household application dominates at 82.3% due to population growth and urbanization: The Kingdom's population reached approx. 35 million in mid-2024 with a 4.7% annual growth rate, per GASTAT, directly expanding the consumer base for everyday household laundry care products.

- Northern and Central Region leads with 38.5% share (2025): The region's dominance reflects Riyadh's status as the Kingdom's most populous administrative center and its concentration of organized retail infrastructure, including supermarkets and hypermarkets.

- Liquid detergents are gaining share through automatic washing machine adoption: Rising urban household incomes are shifting consumer preference toward liquid formats that offer superior compatibility with front-loading washing machines increasingly common in Saudi apartments and villas.

Saudi Arabia Laundry Detergent Market Overview

Saudi Arabia's laundry detergent market encompasses powder, liquid, gel, and pods/tablets formulations sold through supermarkets, hypermarkets, convenience stores, and online retail channels for household and industrial end-use. The market combines established local manufacturing, including Procter & Gamble's Dammam and Jeddah facilities operating since the 1960s and 1980s, with international brand distribution and a growing base of domestic private-label producers.

The industry operates under the Saudi Standards, Metrology and Quality Organization (SASO), which sets mandatory technical regulations, labeling, and conformity assessment requirements for household chemical and cleaning products sold in the Kingdom. Macroeconomic tailwinds include Vision 2030's economic diversification, non-oil GDP growth, and continued manufacturing localization incentives under the National Industrial Development and Logistics Program.

Market Dynamics

To evaluate market opportunities, Request Sample

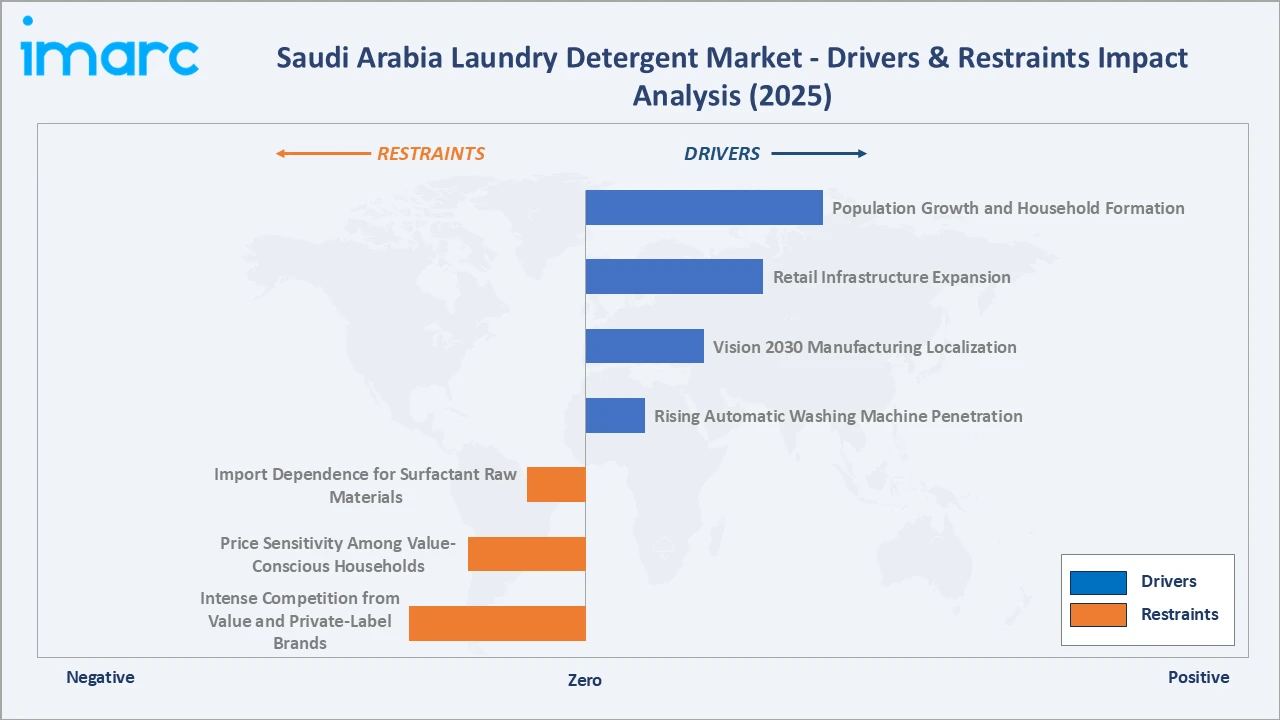

Market Drivers

- Population Growth and Household Formation: GASTAT recorded Saudi Arabia's population at around 35 million in mid-2024, up 4.7% year-on-year, with housing units occupied by Saudi households rising to 4.4 million, directly expanding the household base for laundry care consumption.

- Retail Infrastructure Expansion: Continued growth of supermarket and hypermarket chains across major Saudi cities is widening product availability and driving trial of premium detergent formats.

- Vision 2030 Manufacturing Localization: Government-backed industrial diversification initiatives are incentivizing multinational consumer goods manufacturers, including Procter & Gamble, to expand local production capacity at existing Dammam and Jeddah plants.

- Rising Automatic Washing Machine Penetration: Increasing household incomes and urbanization are supporting a shift from manual to automatic laundering, favoring liquid and pods/tablets formats over traditional powder.

Market Restraints

- Import Dependence for Surfactant Raw Materials: The Kingdom's detergent manufacturers rely substantially on imported surfactants and specialty chemicals, exposing production costs to global petrochemical price cycles.

- Price Sensitivity Among Value-Conscious Households: A large expatriate population segment, comprising approximately 44.4% of total residents per GASTAT's 2024 estimates, sustains demand concentration in the value and mid-tier price bands, limiting premium segment expansion.

Market Opportunities

- Domestic Manufacturing Localization: Vision 2030's industrial localization agenda creates incentives for expanded domestic detergent production capacity, reducing import reliance and supporting Saudi-made content requirements in government and institutional procurement.

- Eco-Friendly and Concentrated Formulations: Rising consumer awareness of water conservation, a national priority given the Kingdom's arid climate, is creating demand for concentrated and reduced-packaging detergent formats.

Market Challenges

- Intense Competition from Value and Private-Label Brands: Expanding private-label detergent lines from major retail chains are compressing margins for both international and domestic branded manufacturers.

- Sustainability and Regulatory Compliance: Evolving SASO labeling and environmental compliance requirements are raising formulation and packaging costs for manufacturers operating in the Kingdom.

Emerging Market Trends

1. Premiumization Toward Liquid and Pods/Tablets Formats

Consumers are progressively trading up from traditional powder to liquid and pods/tablets formats, which offer measured dosing and compatibility with automatic washing machines increasingly common in urban Saudi households.

2. Expansion of Online and Direct-to-Consumer Retail

E-commerce platforms are expanding laundry care assortments with subscription and bulk-purchase options, mirroring broader Saudi retail digitization trends supported by the Communications, Space and Technology Commission's digital economy initiatives.

3. Growing Demand for Eco-Friendly and Water-Efficient Formulations

Given Saudi Arabia's arid climate and national water conservation priorities, demand is rising for concentrated detergents that reduce water use during the rinse cycle and minimize packaging waste.

4. Local Manufacturing Expansion Under Vision 2030

Multinational manufacturers are expanding Saudi-based production to align with Vision 2030's industrial localization targets, supported by government incentives for domestic value-add manufacturing.

Industry Value Chain Analysis

Saudi Arabia's laundry detergent value chain spans raw material sourcing, formulation and manufacturing, multi-tier distribution, and retail across offline and online channels serving both household and industrial end-use segments.

|

Stage |

Key Participants |

| Raw Materials |

Surfactant and chemical suppliers |

| Components |

Formulation and fragrance manufacturers |

| Manufacturing |

OEMs and local production facilities |

| Distribution |

Retailers and regional distributors |

| End Users |

Consumers |

Distribution in the Kingdom follows a multi-tier structure in which manufacturers supply national distributors and organized retail chains, which in turn reach household and institutional consumers through supermarkets, hypermarkets, convenience stores, and growing online retail channels.

Technology Landscape in the Saudi Arabia Laundry Detergent Industry

Concentrated and Water-Efficient Formulations

Manufacturers are developing concentrated powder and liquid formulations that reduce packaging volume and water requirements during rinsing, aligning with the Kingdom's water conservation priorities under Vision 2030's environmental sustainability programs.

Enzyme and Low-Temperature Wash Technology

Advanced enzyme-based formulations enable effective stain removal at lower wash temperatures, reducing household energy consumption while maintaining cleaning performance across fabric types common in Saudi households.

Smart Dosing and Digital Innovation

Leading global manufacturers, including Henkel, have introduced smart dosing technologies for their laundry care brands globally, a capability increasingly relevant to Gulf markets as automatic washing machine penetration rises.

Pods and Single-Dose Technology

Water-soluble film-based pods and tablets are gaining traction as a convenient, pre-measured alternative to powder and liquid formats, particularly among smaller urban households and single-person residences.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Product Type | Powder |

43.7% |

2025 |

| Distribution Channel |

🔒 |

🔒 |

2025 |

| Application |

Household |

82.3% |

2025 |

|

Region |

Northern and Central Region |

38.5% |

2025 |

By Product Type

Powder detergents lead at 43.7% market share (2025), reflecting deep-rooted consumer habits and cost efficiency for Saudi Arabia's larger multi-member households, which GASTAT reports average approximately five members.

To access detailed market analysis, Request Sample

Liquid detergents hold 34.2% share and are growing at an estimated 5.7% CAGR, outpacing Powder as urban households increasingly adopt automatic washing machines. Pods/Tablets, at 12.6% share, are the fastest-growing format at an estimated 7.9% CAGR, driven by convenience-focused premiumization, while Gel holds the remaining 9.5% share, growing at an estimated 5.0% CAGR as a mid-tier alternative between powder and liquid formats.

By Application

Household application dominates at 82.3% market share (2025), directly correlated with the Kingdom's population growth to around 35 million residents and household expansion to 4.4 million Saudi-occupied housing units, per GASTAT's statistics.

Industrial application, comprising 17.7% share, is supported by institutional laundering demand from hospitality, healthcare, and commercial laundry service providers, sectors poised for continued expansion under Vision 2030's tourism and services diversification agenda.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers & Characteristics |

|

Northern and Central Region |

38.5% |

Highest population density centered on Riyadh; extensive organized retail network; strong government and institutional procurement activity |

| Western Region |

29.2% |

High religious tourism and pilgrimage traffic through Makkah and Madinah; major port city of Jeddah supporting import-linked distribution |

|

Eastern Region |

21.8% |

Industrial and petrochemical base supporting institutional laundering demand; growing urban household consumption in Dammam and Khobar |

|

Southern Region |

10.5% |

Emerging retail infrastructure development; gradual household income growth supporting incremental detergent demand |

The Northern and Central Region's 38.5% dominance reflects Riyadh's status as the Kingdom's capital and most populous administrative center, home to the highest concentration of organized retail infrastructure and government-linked institutional procurement. This region is estimated to grow at approximately 4.2% CAGR (2026-2034).

The Western Region's 29.2% share is anchored by Jeddah's role as the Kingdom's largest commercial port, alongside Makkah and Madinah's sustained religious tourism traffic, and is estimated to grow at approximately 5.0% CAGR. The Eastern Region's 21.8% share reflects its industrial base and urban household growth in Dammam and Khobar, estimated at approximately 5.3% CAGR, the second-fastest among all regions. The Southern Region, while smallest at 10.5% share, is projected as the fastest-growing region at approximately 6.0% CAGR, supported by emerging retail infrastructure and rising household incomes.

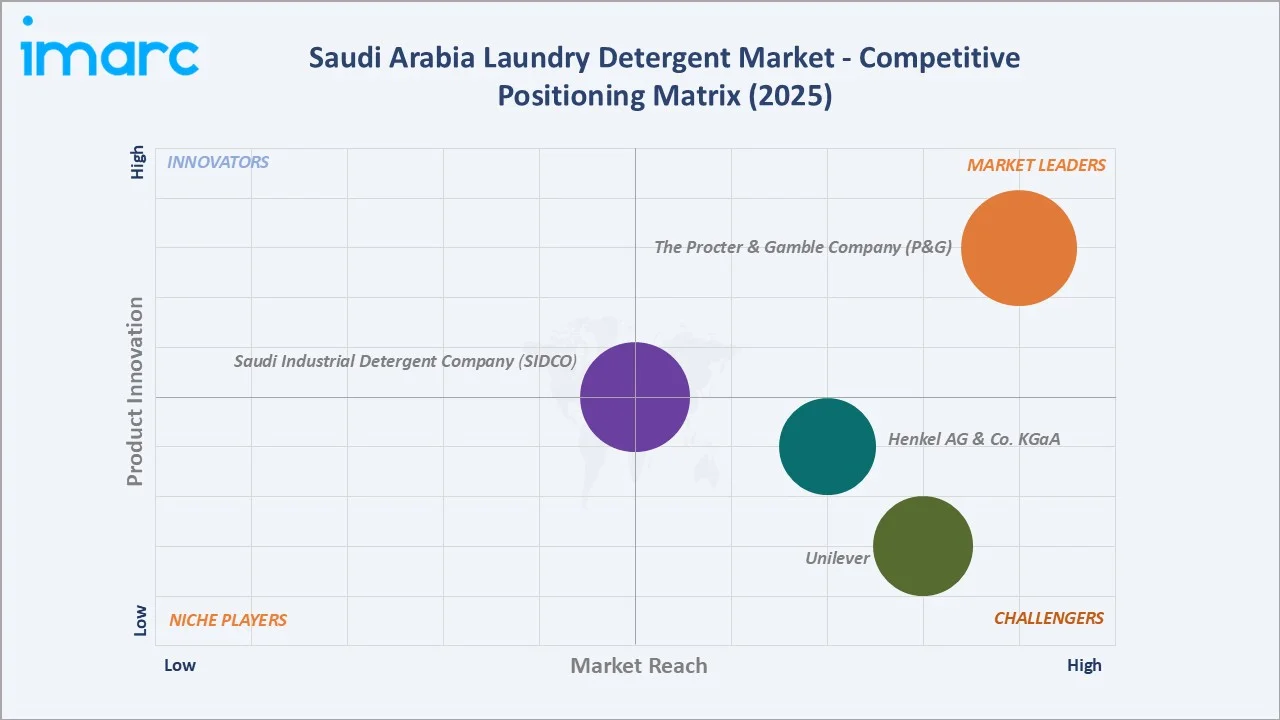

Competitive Landscape

Saudi Arabia's laundry detergent market is moderately concentrated, led by multinational manufacturers with established local production and distribution operations, alongside a growing base of domestic private-label and industrial-grade producers.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

The Procter & Gamble Company (P&G) |

Tide, Ariel, Downy, Bonux |

Market Leader |

Deep market penetration, a tailored dual-brand strategy, localized manufacturing, and a strong commitment to premium cleaning performance |

| Henkel AG & Co. KGaA | Persil | Strong Challenger |

Developed region-specific products based directly on local consumer habits, such as Persil Abaya Shampoo and detergents targeted for washing thobes |

| Unilever | OMO, Comfort |

Strong Challenger |

Localized manufacturing, high-performance fabric-specific formulas, and a strong sustainability focus |

| Saudi Industrial Detergent Company (SIDCO) | Gento and Extra White | Established Player |

Operating out of a purpose-built facility in Dammam's Second Industrial Park |

Key Company Profiles

The Procter & Gamble Company (P&G)

The Procter & Gamble Company (P&G) is the leading manufacturer in Saudi Arabia's laundry detergent market, operating two manufacturing plants in Jeddah and Dammam since the 1960s and 1980s respectively, and serving as a regional distribution hub for more than 15 countries.

- Product Portfolio: Tide, Ariel, Downy, Bonux, and others.

- Strategic Focus: Continued localization of manufacturing and raw material sourcing in alignment with Vision 2030's industrial development objectives.

Henkel AG & Co. KGaA

Henkel AG & Co. KGaA, which operates through Henkel Saudi Arabia Detergent Co. Ltd., holds a global leadership position in laundry and home care under its Persil brand and maintains regional manufacturing operations in Saudi Arabia.

- Product Portfolio: Persil

- Strategic Focus: Sustainability-led manufacturing and smart dosing technology innovation across its global laundry care brand portfolio.

Unilever

Unilever maintains a longstanding presence in Saudi Arabia's laundry care segment through its OMO and Comfort brands, which provide specialized Abaya detergents for dark fabrics and smart-series liquids designed for auto-dose machines, distributed via established regional retail partnerships.

- Product Portfolio: OMO, Comfort

- Strategic Focus: Expansion of value and mid-tier product lines to serve Saudi Arabia's broad household consumer base.

Market Concentration Analysis

Saudi Arabia's laundry detergent market exhibits moderate concentration at the branded level, with Procter & Gamble, Henkel, and Unilever collectively holding the majority of branded household detergent value share, while the industrial and private-label segments remain more fragmented among domestic manufacturers such as SIDCO.

The market's structural fragmentation at the value tier reflects Saudi Arabia's diverse consumer base, spanning price-sensitive expatriate households, who comprise approximately 44.4% of the total population per GASTAT's estimates, and Saudi national households with stronger brand loyalty to established international detergent brands.

Consolidation trends remain limited, with multinational manufacturers focused on expanding local manufacturing capacity rather than pursuing acquisitions, in line with Vision 2030's preference for direct industrial investment and localization over consolidation-led market entry.

Investment & Growth Opportunities

Fastest Growing Segments

Pods/Tablets (~7.9% CAGR), Liquid detergents (~5.7% CAGR), and the Southern Region (~6.0% CAGR) represent Saudi Arabia's highest-growth investment vectors through 2034, reflecting premiumization and emerging regional retail development trends.

Emerging Market Opportunities

Vision 2030's industrial localization financing creates a viable pathway for global detergent manufacturers to expand Saudi-based production capacity, benefiting from industrial zone infrastructure and government procurement preference for locally manufactured goods.

Investment Themes

- Concentrated and Eco-Friendly Formulation Development: Saudi Arabia's water conservation priorities create opportunity for manufacturers introducing concentrated, reduced-water-use detergent formats.

- Digital and E-Commerce Retail Investment: Growth of online grocery and household product retail creates opportunity for direct-to-consumer laundry care subscription models.

- Industrial and Institutional Laundry Service Contracts: Expansion of Saudi Arabia's hospitality and healthcare sectors under Vision 2030 is generating demand for industrial-grade detergent supply contracts.

Future Market Outlook (2026-2034)

The Saudi Arabia laundry detergent market is projected to grow from USD 518.1 Million in 2025 to USD 812.5 Million by 2034, at a 4.87% CAGR, reflecting steady, structurally supported growth underpinned by continued population expansion and Vision 2030's economic diversification. The market is anchored at USD 657.2 Million by 2030, roughly the midpoint of the forecast trajectory.

Three structural forces anchor the market's growth trajectory through 2034: sustained population growth, with GASTAT recording a 4.7% annual increase in 2024; continued premiumization toward liquid and pods/tablets formats as automatic washing machine penetration rises; and Vision 2030's industrial localization agenda, which is expected to expand domestic manufacturing capacity and reduce import dependence over the forecast period.

Research Methodology

Primary Research

Primary research comprised structured engagement with laundry detergent distributors, retail category managers across major Saudi cities, and industry participants to validate market size, segmentation, and competitive dynamics.

Secondary Research

Secondary research encompassed the General Authority for Statistics (GASTAT) population and household data, Saudi Standards, Metrology and Quality Organization (SASO) regulatory documentation, Vision 2030 industrial development program disclosures, and company disclosures from Procter & Gamble and Henkel regarding their Saudi Arabia manufacturing operations.

Forecasting Models

Market value forecasts were developed using a combination of bottom-up household consumption modeling and top-down market sizing, validated against GASTAT population and household growth projections, and cross-checked against segment-level historical growth patterns for Product Type, Distribution Channel, Application, and Regional breakups.

Saudi Arabia Laundry Detergent Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Powder, Liquid, Gel, Pods/Tablets |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Online Stores, Convenience Stores, Others |

| Applications Covered | Industrial, Household |

| Regions Covered | Northern and Central Region, Western Region, Eastern Region, Southern Region |

| Companies Covered | The Procter & Gamble Company (P&G), Henkel AG & Co. KGaA, Unilever, Saudi Industrial Detergent Company (SIDCO), etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Saudi Arabia laundry detergent market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Saudi Arabia laundry detergent market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Saudi Arabia laundry detergent industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Saudi Arabia Laundry Detergent Market Report

The Saudi Arabia laundry detergent market reached USD 518.1 Million in 2025, driven by population growth to around 35 million and continued retail infrastructure expansion across the Kingdom.

The market is projected to grow at a CAGR of 4.87% during 2026-2034, reaching USD 812.5 Million by 2034, supported by Vision 2030 economic diversification and premiumization trends.

Powder detergents lead at 43.7% share (2025), driven by affordability and Saudi Arabia's larger average household size of approximately five members.

Pods/Tablets grow fastest at an estimated 7.9% CAGR (2026-2034), driven by rising demand for convenient, pre-measured dosing formats among urban households.

Household application leads with 82.3% share (2025), directly linked to the Kingdom's population growth and household formation trends.

The Northern and Central Region leads with 38.5% market share (2025), anchored by Riyadh's population density and organized retail concentration.

Leading companies include The Procter & Gamble Company (P&G), Henkel AG & Co. KGaA, Unilever, and Saudi Industrial Detergent Company (SIDCO), among others.

Vision 2030 is driving manufacturing localization, industrial diversification, and domestic supply chain development, encouraging multinational manufacturers to expand local production capacity.

The market is projected to reach approximately USD 657.2 Million by 2030, supported by continued population growth and premiumization toward liquid and pods/tablets formats.

The market was valued at USD 408.4 Million in 2020, expanding to USD 518.1 Million by 2025 at a historical CAGR broadly consistent with the 2026-2034 forecast rate.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)