Saudi Arabia Mobile Cloud Market Size, Share, Trends and Forecast by Service, Deployment, User, Application, and Region, 2026-2034

Saudi Arabia Mobile Cloud Market Summary:

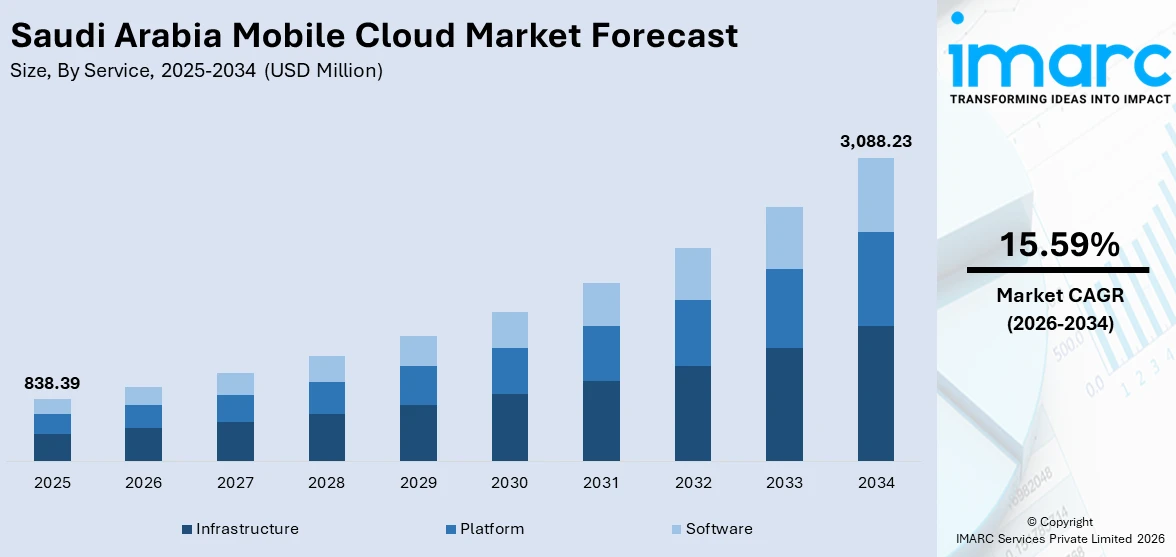

The Saudi Arabia mobile cloud market size was valued at USD 838.39 Million in 2025 and is projected to reach USD 3,088.23 Million by 2034, growing at a compound annual growth rate of 15.59% from 2026-2034.

The Saudi Arabia mobile cloud market is experiencing accelerated expansion as enterprises and consumers increasingly adopt cloud-based mobile solutions to support digital operations and connectivity. Rapid 5G network deployment, expanding data center infrastructure, rising demand for scalable enterprise platforms, and growing digital payment ecosystems are collectively driving adoption. Advancements in edge computing, artificial intelligence integration, and secure cloud architectures are further strengthening the Saudi Arabia mobile cloud market share.

Key Takeaways and Insights:

- By Service: Infrastructure dominates the market with a share of 40% in 2025, owing to the surge in hyperscaler investments, nationwide 5G rollout, and growing enterprise demand for robust computing, storage, and networking resources that underpin mobile cloud ecosystems.

- By Deployment: Public leads the market with a share of 52% in 2025. This dominance is driven by cost-effective scalability, rapid provisioning capabilities, and the increasing preference of enterprises for pay-as-you-go cloud models that reduce capital expenditure and accelerate digital transformation initiatives.

- By User: Enterprise exhibits a clear dominance in the market with 59% share in 2025, reflecting the accelerated digital transformation across banking, healthcare, oil and gas, and government sectors that demand scalable, secure mobile cloud solutions for operational efficiency and workforce mobility.

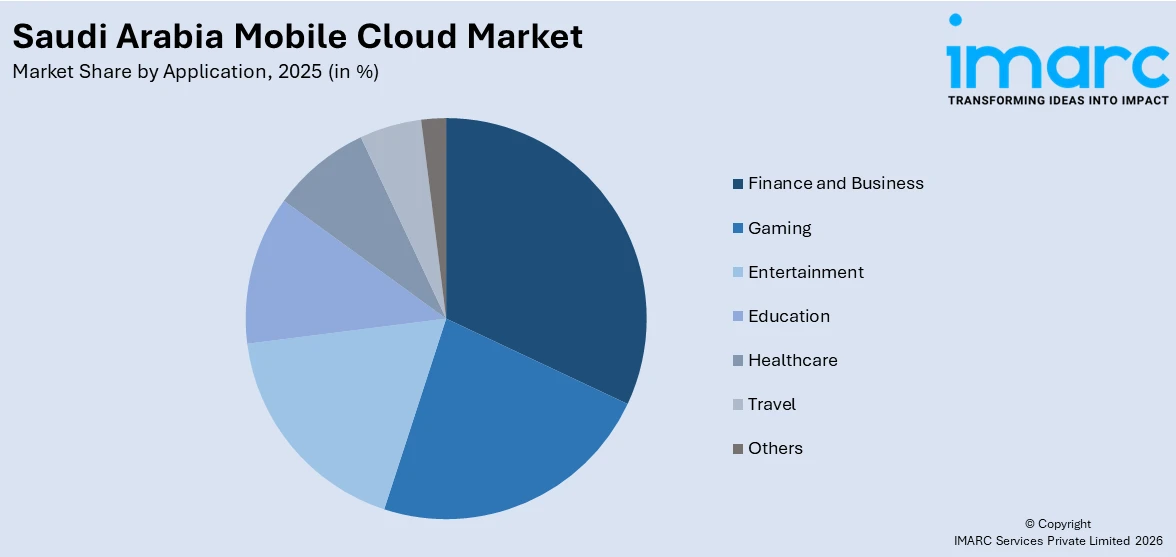

- By Application: Finance and business represent the biggest segment with a market share of 24% in 2025, reflecting the rapid expansion of digital banking, fintech platforms, and mobile payment ecosystems that rely on secure, low-latency cloud infrastructure for transaction processing and financial service delivery.

- By Region: Northern and Central Region is the largest region with 35% share in 2025, driven by the concentration of government institutions, corporate headquarters, and hyperscaler data centers in Riyadh, alongside the capital’s advanced 5G coverage and thriving technology startup ecosystem.

- Key Players: Key players in the Saudi Arabia mobile cloud market are intensifying competition by expanding data center capacities, forging strategic partnerships, investing in artificial intelligence and edge computing capabilities, and developing sovereign cloud platforms to capture enterprise demand and strengthen regional market positioning.

To get more information on this market Request Sample

The Saudi Arabia mobile cloud market is advancing rapidly as the Kingdom positions itself as a leading regional digital hub through massive investments in telecommunications infrastructure, cloud computing platforms, and artificial intelligence capabilities. The convergence of widespread 5G connectivity, expanding hyperscaler presence, and a young, digitally engaged population is accelerating the adoption of cloud-based mobile services across both enterprise and consumer segments. Financial services, healthcare, education, and entertainment industries are increasingly leveraging mobile cloud solutions to deliver seamless user experiences, enhance operational agility, and meet evolving regulatory requirements for data security and privacy. For instance, electronic payments in Saudi Arabia reached 79% of all retail payments in 2024, up from 70% in 2023, underscoring the rapid digitization of financial services that fuels demand for secure mobile cloud infrastructure. The proliferation of smart city initiatives, coupled with expanding enterprise mobility strategies and growing consumer appetite for on-demand digital services, is establishing a strong foundation for sustained market expansion across diverse and growing application verticals and emerging technology domains throughout the Kingdom.

Saudi Arabia Mobile Cloud Market Trends:

Accelerating 5G Infrastructure Expansion

Saudi Arabia is rapidly expanding its 5G network footprint, creating the essential high-speed connectivity layer for mobile cloud services. The Kingdom has achieved extensive nationwide 5G coverage, with major urban centers leading the rollout and deployment. Telecommunications providers are actively introducing advanced 5G Standalone technology across key cities, enabling ultra-low latency and enhanced network slicing for enterprise mobile cloud applications. This widespread infrastructure buildout is strengthening the foundation for cloud-based mobile services, improving data transmission speeds, and supporting the Saudi Arabia mobile cloud market growth.

Integration of Edge Computing with Mobile Cloud Platforms

Edge computing is increasingly converging with mobile cloud architectures to enable real-time data processing at the network periphery, reducing latency for critical applications in healthcare, manufacturing, and logistics. Saudi Arabia's 5G edge cloud network ecosystem is expanding rapidly as enterprises seek distributed computing solutions closer to end users. This growing adoption reflects strong demand for localized processing capabilities that support autonomous operations, immersive digital experiences, and time-sensitive workloads. The integration of edge infrastructure with mobile cloud platforms is enhancing service delivery and operational efficiency across multiple industry verticals throughout the Kingdom.

Rise of AI-Powered Cloud Services

Artificial intelligence is becoming deeply embedded in mobile cloud platforms, enabling intelligent automation, predictive analytics, and personalized service delivery. The LEAP 2025 technology conference in February 2025 attracted approximately USD 14.9 Billion in AI-related investment commitments for Saudi Arabia. For instance, STC Group launched a sovereign large language model cloud platform in partnership with SambaNova at LEAP 2025, running the Llama 405B open-source frontier model to provide secure AI inference-as-a-service for Saudi enterprises.

How Vision 2030 is Transforming the Saudi Arabia Mobile Cloud Market:

Saudi Arabia’s Vision 2030 framework is fundamentally reshaping the mobile cloud landscape by prioritizing digital transformation as a cornerstone of economic diversification. The national strategy emphasizes cloud-first policies encouraging government agencies to migrate core systems onto cloud platforms, creating substantial demand for mobile cloud infrastructure. Smart city mega-projects, including NEOM and the Red Sea development, are generating unprecedented requirements for scalable cloud architectures supporting connected urban ecosystems. The digitization of government services, expansion of e-commerce, and cultivation of a knowledge-based economy are collectively driving enterprise reliance on advanced mobile cloud solutions. Strategic programs targeting technology innovation are fostering a vibrant startup ecosystem that leverages mobile cloud platforms for rapid scaling.

Market Outlook 2026-2034:

The Saudi Arabia mobile cloud market is positioned for robust expansion over the forecast period, underpinned by continuous investments in 5G infrastructure, hyperscaler data center deployments, and the proliferation of AI-enabled cloud services. Enterprise digital transformation across banking, healthcare, energy, and government sectors is expected to remain the primary demand catalyst, with organizations increasingly adopting cloud-native mobile solutions for workforce mobility and operational optimization. The market generated a revenue of USD 838.39 Million in 2025 and is projected to reach a revenue of USD 3,088.23 Million by 2034, growing at a compound annual growth rate of 15.59% from 2026-2034. The expansion of public cloud adoption, growing fintech and digital payment ecosystems, and increasing consumer demand for streaming, gaming, and on-demand services are expected to further accelerate growth. Continued government commitment to digital infrastructure development and data sovereignty frameworks will reinforce the market’s upward trajectory, positioning Saudi Arabia as a leading mobile cloud hub in the Middle East.

Saudi Arabia Mobile Cloud Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Service |

Infrastructure |

40% |

|

Deployment |

Public |

52% |

|

User |

Enterprise |

59% |

|

Application |

Finance and Business |

24% |

|

Region |

Northern and Central Region |

35% |

Service Insights:

- Infrastructure

- Platform

- Software

Infrastructure dominates with a share of 40% of the total Saudi Arabia mobile cloud market in 2025.

The infrastructure segment leads the Saudi Arabia mobile cloud market as enterprises and hyperscalers invest heavily in computing, storage, and networking resources to support the Kingdom’s expanding digital ecosystem. The surge in 5G deployment, edge computing requirements, and AI workload processing is driving substantial demand for scalable cloud infrastructure. Multinational technology providers are establishing dedicated cloud regions and availability zones within Saudi Arabia, reinforcing the local infrastructure base. For instance, Amazon Web Services announced a USD 5.3 Billion investment in 2024 to establish a new cloud infrastructure region in Saudi Arabia, with completion targeted for 2026.

The growing emphasis on data sovereignty and localized processing is further accelerating infrastructure investment as regulated industries including banking, healthcare, and government mandate in-Kingdom data residency. The proliferation of smart city projects and industrial automation initiatives is generating sustained demand for distributed infrastructure capable of handling massive data volumes in real time. Leading global technology providers are establishing dedicated data center facilities across various provinces in Saudi Arabia, expanding enterprise access to localized cloud computing and artificial intelligence services while ensuring compliance with national data governance frameworks.

Deployment Insights:

- Public

- Private

- Hybrid

Public leads with a share of 52% of the total Saudi Arabia mobile cloud market in 2025.

The public cloud deployment model commands the largest share in Saudi Arabia's mobile cloud market, driven by its cost efficiency, rapid scalability, and ability to support organizations of all sizes without significant upfront capital investment. Enterprises are increasingly migrating workloads to public cloud platforms to accelerate application deployment, enable remote collaboration, and leverage advanced analytics capabilities. The flexibility of consumption-based pricing structures is particularly appealing to small and medium enterprises, democratizing access to enterprise-grade mobile cloud tools and reducing operational complexity across diverse industry sectors.

The expansion of global hyperscaler operations within the Kingdom is reinforcing public cloud adoption as organizations gain access to locally hosted services that meet regulatory compliance requirements. Small and medium enterprises are particularly benefiting from pay-as-you-go pricing structures that democratize access to enterprise-grade mobile cloud capabilities. For instance, Tencent Cloud announced a USD 150 Million investment in February 2025 to establish its first Middle East cloud region in Saudi Arabia with two availability zones, expanding public cloud options for gaming and real time applications, expected to become operational by end of 2025.

User Insights:

- Enterprise

- Consumer

Enterprise is the largest segment, accounting for 59% of the total Saudi Arabia mobile cloud market in 2025.

The enterprise segment holds the dominant position in Saudi Arabia’s mobile cloud market as large corporations, government entities, and mid-sized businesses accelerate their digital transformation journeys. Organizations across banking, oil and gas, healthcare, and telecommunications sectors are deploying mobile cloud solutions to enable workforce mobility, streamline operations, and enhance customer engagement through digital channels. The demand for integrated platforms that combine communication, collaboration, and enterprise resource planning capabilities on mobile devices is driving sustained cloud adoption. In January 2025, Nokia and Zain KSA signed an agreement to enhance indoor mobile coverage and enterprise connectivity across the Kingdom.

Enterprise adoption is further strengthened by the growing requirement for cybersecurity, data governance, and regulatory compliance capabilities embedded within mobile cloud platforms. Banks, telecommunications providers, and energy companies are contracting integrated managed security operations centers and sovereign cloud architectures to safeguard sensitive operational data while maintaining mobile accessibility. The rise of hybrid work models and the increasing digitization of government services are expanding the addressable enterprise market.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Gaming

- Finance and Business

- Entertainment

- Education

- Healthcare

- Travel

- Others

Finance and business hold the largest share at 24% of the total Saudi Arabia mobile cloud market in 2025.

The finance and business application segment captures the largest revenue share in Saudi Arabia's mobile cloud market, propelled by the rapid expansion of digital banking, mobile payment platforms, and cloud-based enterprise resource management solutions. The Kingdom's financial sector is undergoing a comprehensive digital overhaul as traditional banks, fintech startups, and payment processors migrate core operations to mobile cloud architectures to deliver seamless customer experiences. The growing number of active fintech companies reflects the accelerating pace of financial technology innovation that drives demand for scalable cloud infrastructure and secure mobile service delivery frameworks.

The proliferation of digital wallets, contactless payments, and real-time transaction processing platforms is reinforcing the need for high-performance, secure mobile cloud environments. Enterprises across retail, logistics, and professional services are also leveraging cloud-based business applications to enhance supply chain visibility, automate workflows, and improve decision-making through data analytics. The continued expansion of national real-time payment infrastructure is generating escalating transaction volumes that necessitate robust mobile cloud capabilities for uninterrupted financial service delivery across diverse consumer and commercial channels throughout the Kingdom.

Regional Insights:

- Northern and Central Region

- Western Region

- Eastern Region

- Southern Region

Northern and Central Region represents the leading segment with 35% share of the total Saudi Arabia mobile cloud market in 2025.

The Northern and Central Region commands the largest share of Saudi Arabia's mobile cloud market, anchored by Riyadh's status as the Kingdom's administrative, financial, and technological capital. The concentration of government ministries, multinational corporate headquarters, banking institutions, and technology startups in the capital city drives outsized demand for mobile cloud infrastructure and services. Riyadh houses the densest cluster of hyperscaler cloud zones, with multiple global technology providers establishing dedicated cloud regions and data center facilities within the capital to serve enterprise and public sector clients.

The region's advanced telecommunications infrastructure, featuring extensive 5G coverage across Riyadh, provides a strong connectivity foundation for mobile cloud service delivery. Government digitization programs, the expansion of e-commerce fulfillment networks, and the growth of fintech operations within the capital are sustaining high adoption rates. Additionally, the Qassim area contributes to regional demand through agricultural technology platforms and smart logistics initiatives that leverage mobile cloud capabilities. Telecommunications operators are continuously enhancing network infrastructure through advanced standalone technologies, further strengthening connectivity for mobile cloud applications across the region.

Market Dynamics:

Growth Drivers:

Why is the Saudi Arabia Mobile Cloud Market Growing?

Accelerating Enterprise Digital Transformation

Saudi Arabia's enterprise sector is undergoing a fundamental digital shift as organizations across banking, healthcare, energy, and government accelerate their migration to cloud-native mobile platforms. Large corporations and public institutions are deploying integrated mobile cloud solutions to enable remote workforce management, streamline procurement processes, and deliver digital services to citizens and customers. The banking and financial services sector remains a leading contributor to enterprise cloud spending, reflecting the critical importance of mobile cloud infrastructure in supporting digital banking operations, regulatory compliance, and customer-facing applications. The healthcare industry is also emerging as a significant driver, with the government prioritizing substantial investments in digital health technologies. Organizations are focusing cloud investments on artificial intelligence, data analytics, and mobile-first service delivery, creating sustained demand for scalable infrastructure and platform services that form the backbone of the mobile cloud ecosystem.

Surging Fintech and Digital Payment Ecosystems

The rapid growth of fintech companies and digital payment platforms in Saudi Arabia is a powerful catalyst for mobile cloud adoption, as these services require highly scalable, low-latency cloud infrastructure to process millions of daily transactions. The Kingdom's electronic payment penetration has risen sharply in recent years, indicating a fundamental consumer shift toward digital financial services. The expanding base of active digital wallet customers is generating substantial demand for cloud-based mobile processing capabilities. Widespread contactless payment adoption further underscores the ecosystem's maturity, while real-time payment infrastructure continues to expand. The growing number of fintech startups, combined with regulatory support from the Saudi Central Bank, is fostering innovation in mobile lending, insurance technology, and wealth management applications that rely entirely on cloud-delivered mobile platforms. This convergence of consumer adoption and fintech innovation is creating a virtuous cycle of demand for mobile cloud services across the financial value chain.

Rapid Data Center Infrastructure Expansion

Saudi Arabia is experiencing an unprecedented wave of data center investments that directly strengthens the mobile cloud market by expanding local computing capacity and reducing latency for end users. Global technology companies and regional operators are committing substantial capital to establish new facilities across the Kingdom, driven by growing enterprise demand and data sovereignty requirements. Leading industry conferences have served as platforms for major announcements regarding planned data center capacity expansions by prominent investment firms and regional infrastructure developers. These investments are complemented by strategic initiatives from global hyperscalers seeking to establish dedicated cloud regions within the Kingdom, with multiple providers committing to new public cloud regions and sustainable data center developments. The expanding physical infrastructure base is reducing barriers to mobile cloud adoption by ensuring localized processing, improved service reliability, and compliance with national data residency regulations.

Market Restraints:

What Challenges the Saudi Arabia Mobile Cloud Market is Facing?

Data Sovereignty and Regulatory Compliance Complexity

Stringent data sovereignty requirements and evolving regulatory frameworks present significant challenges for mobile cloud providers and adopters in Saudi Arabia. Many organizations, particularly in banking, healthcare, and government, remain cautious about hosting sensitive information on external cloud platforms due to data residency mandates and cybersecurity compliance obligations. The National Cybersecurity Strategy mandates comprehensive security frameworks including cloud-specific protocols, adding layers of complexity to deployment decisions. These regulatory constraints can slow migration timelines and increase implementation costs for enterprises seeking to fully leverage mobile cloud solutions.

Shortage of Skilled Cloud and Cybersecurity Professionals

The limited availability of qualified cloud computing and cybersecurity talent represents a critical bottleneck for mobile cloud market expansion in Saudi Arabia. The Kingdom faces a significant shortage of cybersecurity professionals, while only a limited proportion of information technology workers possess the advanced skills needed to address sophisticated cloud security threats. This talent gap constrains the ability of enterprises to design, deploy, and manage complex mobile cloud environments effectively, often forcing reliance on external managed service providers and slowing the pace of internal capability development.

High Initial Deployment Costs and Infrastructure Complexity

The substantial upfront investment required for deploying comprehensive mobile cloud solutions, including integration with legacy systems, security architecture implementation, and staff training, poses a barrier for many organizations. Building nationwide 5G infrastructure to support mobile cloud services requires extensive investment in base stations, fiber backhaul, and dense small-cell networks. Saudi Arabia’s vast geographic expanse, encompassing deserts and remote regions, makes comprehensive network deployment particularly expensive and technically challenging, potentially limiting uniform mobile cloud access across all areas of the Kingdom.

Competitive Landscape:

The Saudi Arabia mobile cloud market features an increasingly competitive landscape as global hyperscalers, regional telecommunications providers, and specialized cloud service companies vie for market share. Companies are differentiating through sovereign cloud offerings, AI-integrated platforms, strategic data center investments, and tailored enterprise solutions that address local regulatory requirements. Partnerships between international technology firms and Saudi entities are intensifying, enabling localized service delivery and compliance with data sovereignty mandates. Market players are expanding their portfolios to include edge computing, managed security services, and industry-specific cloud solutions, while investing in workforce development and innovation hubs to strengthen their competitive positioning in this rapidly evolving market.

Saudi Arabia Mobile Cloud Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Services Covered | Infrastructure, Platform, Software |

| Deployments Covered | Public, Private, Hybrid |

| Users Covered | Enterprise, Consumer |

| Applications Covered | Gaming, Finance and Business, Entertainment, Education, Healthcare, Travel, Others |

| Regions Covered | Northern and Central Region, Western Region, Eastern Region, Southern Region |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Saudi Arabia Mobile Cloud Market Report

The Saudi Arabia mobile cloud market size was valued at USD 838.39 Million in 2025.

The Saudi Arabia mobile cloud market is expected to grow at a compound annual growth rate of 15.59% from 2026-2034 to reach USD 3,088.23 Million by 2034.

Infrastructure dominated the market with a share of 40%, driven by hyperscaler data center investments, 5G network deployments, and growing enterprise demand for scalable computing, storage, and networking resources across the Kingdom.

Key factors driving the Saudi Arabia mobile cloud market include accelerating enterprise digital transformation, surging fintech and digital payment ecosystems, rapid data center infrastructure expansion, nationwide 5G deployment, and growing adoption of AI-powered cloud services.

Major challenges include data sovereignty and regulatory compliance complexity, shortage of skilled cloud and cybersecurity professionals, high initial deployment costs, infrastructure coverage gaps in remote regions, and the need for comprehensive workforce development programs.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)