Saudi Arabia Non-Dairy Coffee Creamers Market Size, Share, Trends and Forecast by Type, Form, Source, Flavor, Distribution Channel, and Region, 2026-2034

Saudi Arabia Non-Dairy Coffee Creamers Market Summary:

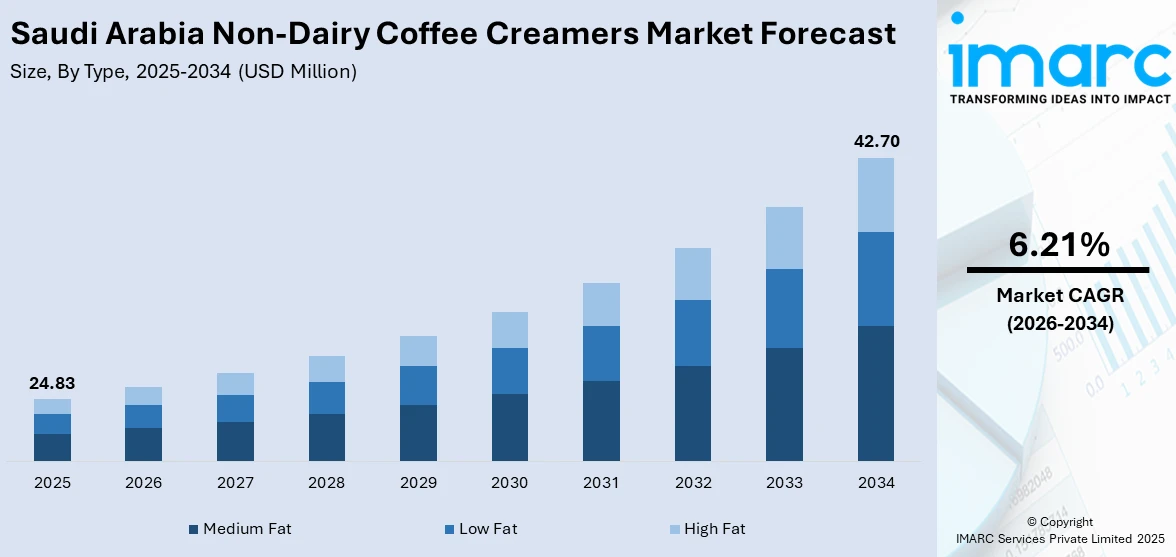

The Saudi Arabia non-dairy coffee creamers market size was valued at USD 24.83 Million in 2025 and is projected to reach USD 42.70 Million by 2034, growing at a compound annual growth rate of 6.21% from 2026-2034.

Market growth is primarily driven by the developing coffee culture, increasing health consciousness among consumers, and the rising adoption of plant-based alternatives. The market benefits from Saudi Arabia's thriving café scene, government support through Vision 2030 initiatives, and the growing prevalence of lactose intolerance, which collectively encourage consumers to explore non-dairy options. The Saudi Arabia non-dairy coffee creamers market share is expanding owing to e-commerce penetration and flavor innovation reshaping consumer preferences across the Kingdom.

Key Takeaways and Insights:

- By Type: Medium fat dominates the market with a share of 43% in 2025, driven by consumer demand for rich, indulgent textures that closely replicate traditional dairy cream while maintaining moderate calorie content.

- By Form: Powder leads the market with a share of 65% in 2025, attributed to superior convenience, extended shelf life of 12-24 months under ambient conditions, and elimination of refrigeration requirements in Saudi Arabia's high-temperature climate.

- By Source: Almond represents the largest segment with a market share of 30% in 2025, leveraging the ingredient's deep cultural resonance in Middle Eastern cuisine where almonds have been traditional staples for centuries, combined with favorable nutritional profiles including vitamin E content and natural antioxidants that appeal to health-conscious consumers.

- By Flavor: French vanilla leads the market with a share of 32% in 2025, reflecting its universal appeal and versatility across diverse coffee preparations, serving as the entry-level flavored creamer that facilitates consumer transitions from unflavored options while benefiting from year-round consumption patterns unlike seasonal offerings.

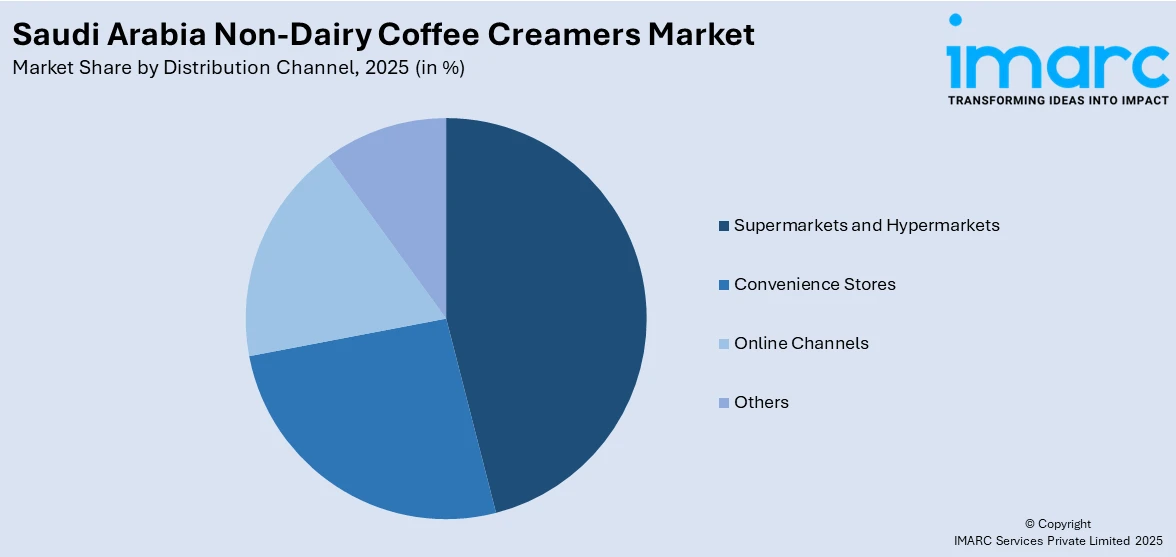

- By Distribution Channel: Supermarkets and hypermarkets represent the largest segment with a market share of 48% in 2025, driven by extensive shelf space enabling wide product assortments, competitive pricing strategies, in-store sampling programs, and the ability to maintain both refrigerated liquid and ambient powder options.

- By Region: Northern and Central Region dominates with 40% share in 2025, anchored by Riyadh's status as the capital housing significant portions of Saudi Arabia's population, with superior retail infrastructure, high disposable incomes, sophisticated café culture, and strategic investments.

- Key Players: Key players in Saudi Arabia’s non-dairy coffee creamers market are expanding flavored and healthier variants, including low-sugar and plant-based options, to match changing consumer preferences. Companies are strengthening retail presence through supermarkets and e-commerce, investing in attractive packaging, and running promotional campaigns. Many are also forming partnerships with cafés and foodservice chains to increase product visibility.

To get more information on this market Request Sample

The Saudi Arabian market for non-dairy coffee creamers is seeing healthy growth due to a shift in the country’s coffee culture and a growing interest in health and wellness among consumers. In 2024, there will be 3,556 cafes in Saudi Arabia, according to the World Coffee Portal, making them an integral part of daily life, especially in large cities such as Riyadh, Jeddah, and Dammam. The Saudi government’s Vision 2030 initiative includes a strong push to promote the country’s domestic coffee industry, with the Public Investment Fund (PIF) allocating $320 million in investments to grow the sector. The growth of the non-dairy coffee creamers market is also fueled by increased lactose intolerance, which is becoming more prevalent in this region, as well as by continued growth of Saudi Arabia’s health and wellness industry. Similarly, the continued opening of multiple vegan restaurants has contributed to the market’s growth. In 2025, plant-based diet supporter Ola Kayal planned to open Nabati Eatery in Al Rawdah (Jeddah) after years of hosting pop-up restaurants and delivering food to homes, providing a unique dining experience that is100% plant-based, gluten-free, refined sugar-free, and organic whenever possible. The restaurant seeks to enhance sustainability by eliminating bottled water and composting food scraps, while intending to partner with nearby farms for ingredient sourcing.

Saudi Arabia Non-Dairy Coffee Creamers Market Trends:

Rising Health and Wellness Consciousness

Expectations of Saudi consumers are changing as they are prioritizing health and wellness as in their purchasing decision. Apart from this, the increased consumer awareness of the many additional benefits that non-dairy coffee creamers have besides their traditional value of being a coffee creamer. is supporting the market growth According too IMARC Group, the Saudi Arabia health and wellness market exhibits a growth rate (CAGR) of 9.22% during 2026-2034, reflecting heightened awareness of preventive healthcare and nutritional choices. A 2025 retrospective study revealed that 67.3% of the Saudi population residing in Qassim region suffers from vitamin D deficiency, prompting consumers to seek fortified food and beverage products. This reflects the growth of the awareness of preventive healthcare and healthy eating choices among consumers in Saudi Arabia. A retrospective study conducted in the Qassim region of Saudi Arabia in 2025 demonstrated that an estimated sixty-seven percent (67.3%) of the population were vitamin D deficient. This statistic has encouraged consumers to seek out fortified food and beverage products. This trend is also present in coffee creamers. Many Saudi consumers prefer their coffee creamers to be free from lactose, cholesterol, and artificial additives. Due to the high prevalence of lactose intolerance in the region, the demand for plant-based alternatives is rapidly increasing. Many consumers are seeking digestive-friendly options but will not sacrifice taste or texture to find what they desire.

Plant-Based Product Proliferation

The plant-based movement has gained significant momentum in Saudi Arabia, with the plant-based food market growing. Government support has been instrumental, with Ayla's Choice becoming the first company to obtain a license from the Ministry of Environment, Water and Agriculture (MEWA) for plant-based product manufacturing in April 2024, paving the way for increased investment and innovation. Late 2023 saw Mowreq Specialized Agriculture and YesHEalth Group jointly break ground on Saudi Arabia's largest indoor vertical farming project, enhancing local production capabilities for plant-based ingredients. This trend extends to coffee creamers, where almond-based, coconut-based, and soy-based options are gaining traction.

Flavor Innovation and Premium Positioning

Manufacturers are continuously expanding flavor portfolios to capture diverse consumer preferences and create premium product lines. In These launches reflect manufacturers' strategic focus on creating experiential products that resonate with younger, adventurous consumers while addressing health concerns through reduced sugar formulations. Moreover, the rise in veganism in the country is offering a favorable market outlook. People are adopting vegan lifestyles as the availability of various plant-based food products is becoming more convenient. IMARC Group predicts that the Saudi Arabia plant-based food market is projected to reach USD 0.29 Billion by 2033. This will further increase the need for premium quality vegan coffee creamers.

How Vision 2030 is Transforming the Saudi Arabia Non-Dairy Coffee Creamers Market:

Saudi Vision 2030 is reshaping Saudi Arabia’s non-dairy coffee creamers market by supporting food sector growth, local manufacturing, and healthier consumer choices. As the Kingdom focuses on diversifying its economy beyond oil, investments in food processing and retail expansion are creating space for new dairy-free and plant-based creamer products. Vision 2030’s emphasis on improving public health is also encouraging demand for low-fat, lactose-free, and functional alternatives, especially among younger, urban consumers. Rising café culture, driven by tourism and lifestyle changes, is boosting consumption of coffee creamers across households and foodservice outlets. At the same time, initiatives to strengthen domestic production and reduce import dependency are encouraging local and international brands to establish operations in Saudi Arabia. With evolving consumer preferences, government-backed economic reforms, and expanding modern retail channels, Vision 2030 is playing a major role in accelerating innovation and long-term growth in the non-dairy coffee creamers segment.

Market Outlook 2026-2034:

The Saudi Arabia non-dairy coffee creamers market is poised for sustained growth throughout the forecast period, driven by demographic shifts, digital transformation, and evolving consumer preferences. The market generated a revenue of USD 24.83 Million in 2025 and is projected to reach a revenue of USD 42.70 Million by 2034, growing at a compound annual growth rate of 6.21% from 2026-2034. Urbanization continues to accelerate, creating concentrated consumer bases in major cities where café culture thrives. The online grocery market's expansion will enhance product accessibility, particularly benefiting premium and specialty non-dairy creamers. Government initiatives under Vision 2030 are also expected to further strengthen local manufacturing capabilities and supply chain infrastructure, potentially improving product availability and competitive pricing across the Kingdom.

Saudi Arabia Non-Dairy Coffee Creamers Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

Medium Fat |

43% |

|

Form |

Powder |

65% |

|

Source |

Almond |

30% |

|

Flavor |

French Vanilla |

32% |

|

Distribution Channel |

Supermarkets and Hypermarkets |

48% |

|

Region |

Northern and Central Region |

40% |

Type Insights:

- Low Fat

- Medium Fat

- High Fat

Medium fat dominates with a market share of 43% of the total Saudi Arabia non-dairy coffee creamers market in 2025.

Medium fat non-dairy coffee creamers dominate the market, driven by consumer demand for rich, indulgent textures that closely replicate traditional dairy cream experiences. The preference reflects the Kingdom's traditional coffee culture, where Arabic coffee and specialty preparations prioritize depth of flavor and creamy mouthfeel. Health-conscious consumers view medium fat formulations as optimal compromises, delivering satisfying sensory experiences without the full calorie burden of high-fat alternatives. The rise of ketogenic and low-carb dietary patterns has further strengthened this segment, with fitness-focused Saudis viewing medium fat creamers as functional additions providing sustained energy through healthy fats while avoiding excessive sugar content that characterizes many flavored alternatives.

The segment benefits from manufacturers' strategic positioning of medium fat variants as premium everyday products suitable for both home and office consumption. Medium fat creamers serve this demographic by offering creamy satisfaction without triggering guilt associated with high-fat options. The formulation's versatility across hot and cold coffee applications enhances its appeal, particularly as cold brew and iced coffee consumption grows among younger Saudi consumers. Manufacturers leverage advanced emulsification technologies to ensure medium fat creamers deliver consistent texture and stability, addressing technical challenges that previously limited plant-based alternatives' ability to match dairy performance.

Form Insights:

- Powder

- Liquid

Powder leads with a share of 65% of the total Saudi Arabia non-dairy coffee creamers market in 2025.

Powder non-dairy coffee creamers have superior convenience, extended shelf life, and precise dosing capabilities that appeal to both household and foodservice segments. This dominance aligns with the global tablet/powder segment's growth, demonstrating widespread consumer acceptance of dry formats across diverse markets. In Saudi Arabia's climate, where ambient temperatures frequently exceed 40°C during summer months, powder formulations eliminate refrigeration requirements, making them ideal for office environments, travel, and households with limited refrigerator capacity. Powder creamers' ability to maintain quality for 12-24 months under ambient conditions provides retailers significant flexibility in stock management and distribution planning, supporting market penetration even in remote areas where cold chain infrastructure may be limited or unreliable.

Consumer preference for powder formats extends beyond practical considerations to encompass customization capabilities that resonate with Saudi coffee culture's emphasis on personalized preparation. The format enables precise portion control, allowing consumers to adjust creamer strength according to individual taste preferences, a flexibility particularly valued in Saudi households where multiple family members may have distinct coffee drinking habits. For foodservice establishments, powder creamers offer cost-effective solutions with consistent performance across high-volume operations. Manufacturers are introducing instant-dissolving formulations that blend seamlessly in cold beverages, expanding powder creamers' application beyond traditional hot coffee to capture growing iced coffee consumption. This innovation trajectory, combined with inherent logistical advantages, positions powder formats for sustained market leadership despite emerging competition from premium liquid alternatives.

Source Insights:

- Almond

- Coconut

- Soy

- Others

Almond exhibits a clear dominance with a 30% share of the total Saudi Arabia non-dairy coffee creamers market in 2025.

Almond-based non-dairy coffee creamers lead the source segment, leveraging the ingredient's deep cultural resonance in Saudi Arabian cuisine where almonds have been integral to culinary traditions for centuries. This historical familiarity reduces consumer hesitancy when transitioning from dairy creamers, as almonds represent recognizable, trusted ingredients rather than novel plant sources requiring educational marketing. Almond milk's favorable nutritional profile, particularly its vitamin E content, appeals to health-conscious consumers seeking functional benefits beyond basic flavor enhancement. Almond creamers' naturally mild, slightly sweet flavor profile creates neutral bases that enhance coffee characteristics without overpowering subtle tasting notes, a quality particularly valued by specialty coffee enthusiasts frequenting Saudi Arabia's expanding café culture.

Premium positioning strategies significantly strengthen almond creamers' market dominance, as manufacturers emphasize sustainable sourcing practices, minimal processing, and superior ingredient quality to justify price premiums 20-30% above soy or coconut alternatives. Consumers associate almond milk with health-focused lifestyles and clean eating movements, perceptions reinforced through targeted marketing emphasizing natural origins and nutritional benefits. The segment benefits from innovation in almond processing technologies that improve extraction efficiency and reduce characteristic grittiness previously associated with almond-based beverages. Manufacturers are introducing barista-style almond creamers specifically formulated for optimal frothing performance, addressing professional and home enthusiast demand for café-quality microfoam in lattes and cappuccinos.

Flavor Insights:

- French Vanilla

- Caramel

- Hazelnut

- Irish Creme

- Others

French vanilla leads with a share of 32% of the total Saudi Arabia non-dairy coffee creamers market in 2025.

French Vanilla dominates the flavor segment, reflecting its universal appeal and versatility across diverse coffee preparations from light roasts to espresso-based drinks. The flavor's subtle sweetness and creamy vanilla notes create balanced enhancements that satisfy both traditional coffee purists and contemporary consumers seeking flavored experiences without overwhelming coffee's inherent characteristics. French Vanilla serves as an entry-level flavored creamer, positioned as a safe choice for consumers transitioning from unflavored to flavored options, a strategic positioning that drives trial and repeat purchases. This innovation demonstrates manufacturers' continuous efforts to modernize classic flavors with health-focused formulations addressing contemporary Saudi consumer concerns about sugar intake.

French Vanilla's market strength extends beyond product performance to encompass psychological associations with indulgence and comfort that resonate across demographic segments. The flavor benefits from year-round consumption patterns unlike seasonal offerings such as pumpkin spice or peppermint, ensuring consistent sales velocity that supports retail shelf space allocation and manufacturer production planning. Saudi Arabia's expanding café culture, creates substantial foodservice demand for reliable, crowd-pleasing flavors that French Vanilla satisfies. The flavor's compatibility with both hot and cold applications positions it advantageously as cold brew and iced coffee consumption grows among younger demographics. Manufacturers leverage French Vanilla as a platform for limited-edition innovations and seasonal variations, creating excitement and trial opportunities without alienating consumers who prefer familiar taste profiles.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Supermarkets and Hypermarkets

- Convenience Stores

- Online Channels

- Others

Supermarkets and hypermarkets exhibit a clear dominance with a 48% share of the total Saudi Arabia non-dairy coffee creamers market in 2025.

Supermarkets and hypermarkets command the distribution channel share in Saudi Arabia's non-dairy coffee creamers market. This dominance reflects large-format retailers' extensive shelf space allocation enabling wide product assortments that facilitate consumer comparison shopping and brand discovery. Major Saudi chains have established dedicated dairy alternative sections with prominent shelf placement, increasing visibility and accessibility for non-dairy creamers. These retailers leverage promotional strategies, in-store sampling programs, and strategic endcap displays to drive impulse purchases and encourage brand switching among consumers exploring plant-based alternatives. Large-format stores' dual capability to maintain refrigerated sections for liquid creamers while also stocking ambient powder options creates one-stop shopping destinations accommodating diverse consumer format preferences.

Supermarkets and hypermarkets serve as critical brand-building platforms where manufacturers execute integrated marketing strategies combining competitive pricing, promotional support, and educational initiatives that drive category growth. These retailers offer private-label alternatives that expand consumer choice while applying competitive pressure on branded products to justify premium positioning through superior quality or innovative formulations. The channel's importance extends to new product introductions, where major retailers function as gatekeepers determining which innovations receive market access and shelf allocation. Manufacturers prioritize relationships with key buyers, offering category management expertise, consumer insights, and collaborative promotional planning that strengthens mutual commercial success. The expansion of international hypermarket operators into secondary Saudi cities creates geographic distribution advantages, bringing non-dairy creamers to consumers previously reliant on traditional grocery stores with limited specialty product selections.

Regional Insights:

- Northern and Central Region

- Western Region

- Eastern Region

- Southern Region

Northern and Central Region leads with a share of 40% of the total Saudi Arabia non-dairy coffee creamers market in 2025.

The Northern and Central Region dominates the market share, driven by Riyadh's status as Saudi Arabia's capital and largest metropolitan area housing significant portions of the Kingdom's population. Urban concentration creates dense consumer markets with sophisticated café cultures, high disposable incomes, and exposure to international lifestyle trends supporting premium non-dairy creamer adoption. The region benefits from superior retail infrastructure, with major supermarket chains maintaining extensive store networks representing a major percentage of distribution channel share, and advanced cold chain logistics supporting both powder and liquid creamer distribution. Riyadh's role as the Kingdom's business and government center drives substantial office coffee consumption, with institutional buyers representing high-volume demand for bulk formats and consistent repurchase patterns.

The Northern and Central Region's market leadership reflects broader demographic and economic advantages that position it for accelerated growth relative to other areas. The region's urbanization rate as of 2025 concentrates consumers in accessible markets where modern retail formats thrive and specialty products achieve efficient distribution. Urban professional demographics align with non-dairy creamer target audiences, health-conscious, time-pressed consumers with sufficient disposable income to pay premiums for convenience and quality. Riyadh specifically hosts numerous international coffee chains and trendy third-wave specialty cafés that introduce consumers to diverse coffee preparations and complementary products, creating familiarity that transfers to at-home consumption. The Saudi government's Vision 2030 initiatives concentrate infrastructure investments and

Market Dynamics:

Growth Drivers:

Why is the Saudi Arabia Non-Dairy Coffee Creamers Market Growing?

Expanding Coffee Culture and Consumption

Saudi Arabia's flourishing coffee culture serves as the primary catalyst for non-dairy creamer market expansion, with the Kingdom operating numerous coffee shops. The café culture has evolved from traditional Arabic coffee gatherings to encompass international specialty coffee chains and trendy third-wave coffee establishments, particularly concentrated in major urban centers like Riyadh, Jeddah, and Dammam. In 2025, Lagardère Travel Retail has unveiled its own So! Coffee café brand in Saudi Arabia as it aims to enhance its foodservice and duty-free retail presence at airports throughout the Kingdom. The international travel retailer introduced So! Coffee began its operations in January 2016 and now has 65 locations in airports, train stations, and shopping centers throughout Poland, Romania, France, the Czech Republic, and Spain. This expanding infrastructure creates sustained demand for complementary products like creamers, with consumers seeking convenient ways to customize their coffee experiences both at home and in foodservice settings.

Health Consciousness and Dietary Restrictions

Rising health awareness and the prevalence of dietary restrictions are fundamentally reshaping Saudi consumer preferences toward non-dairy alternatives. This health consciousness extends to coffee consumption patterns, with consumers increasingly scrutinizing creamer ingredients for artificial additives, trans fats, and excessive sugar content. Moreover, the government is promoting healthy lifestyle habits among the masses, such as the organization of Saudi Walking Day in 2024 to encourage people to participate in simple physical activities. Non-dairy creamers position themselves as cleaner alternatives free from lactose, cholesterol, and animal-derived ingredients, appealing to both medically motivated consumers and those pursuing wellness-oriented lifestyles. The growing vegan and flexitarian movements further support market expansion as ethical and environmental considerations influence purchasing decisions.

E-commerce Growth and Digital Transformation

The rapid expansion of e-commerce infrastructure and digital payment systems has dramatically improved non-dairy creamer accessibility and convenience, particularly benefiting premium and specialty brands. E-commerce platforms enable consumers to access wider product varieties, read reviews, and compare prices, supporting informed decision-making. For manufacturers, digital channels provide direct consumer relationships, valuable data insights, and opportunities to introduce subscription models that ensure consistent repurchase patterns. The convenience of home delivery particularly appeals to busy professionals and families, who comprise significant portions of the coffee-consuming demographic in Saudi Arabia's increasingly urbanized society. Saudi Arabia e-commerce market is projected to attain USD 708.7 Billion by 2033, as per the information provided by IMARC Group.

Market Restraints:

What Challenges the Saudi Arabia Non-Dairy Coffee Creamers Market is Facing?

Premium Pricing Barriers

Non-dairy coffee creamers typically command higher price points compared to conventional dairy options, creating barriers for price-sensitive consumer segments. The production costs associated with sourcing, processing, and formulating plant-based ingredients often exceed those of traditional dairy manufacturing, resulting in retail prices that can be 20 to 40% higher than dairy creamers. In markets where dairy products receive government subsidies or benefit from established supply chains, non-dairy alternatives struggle to achieve price parity. This pricing gap particularly impacts mass-market penetration, limiting adoption among middle and lower-income households who prioritize value over specialty features.

Taste and Texture Challenges

Achieving taste and texture profiles that match or exceed traditional dairy creamers remains a significant technical challenge for manufacturers. Consumer expectations for creamy mouthfeel, smooth dissolution in hot beverages, and flavor that enhances rather than detracts from coffee quality require sophisticated formulation expertise. Some plant-based ingredients impart distinct flavors, such as coconut's tropical notes or soy's slightly beany taste, that may not appeal to all consumers accustomed to neutral dairy cream. Texture differences, including potential graininess in powder formulations or separation in liquid versions, can negatively impact consumer experiences and limit repeat purchases.

Market Competition and Consumer Awareness

The Saudi Arabia non-dairy coffee creamers market faces intense competition from both established international brands and emerging local players, creating market fragmentation that challenges brand loyalty development. Limited consumer awareness in certain regions and demographic segments about the availability and benefits of non-dairy creamers restricts market expansion potential. Traditional coffee consumption habits and cultural preferences for conventional dairy products present inertia that requires significant marketing investment to overcome. Additionally, the circulation of counterfeit or substandard products through informal channels can erode consumer confidence in the entire category, making quality assurance and brand differentiation critical but resource-intensive priorities.

Competitive Landscape:

The Saudi Arabia non-dairy coffee creamers market features a competitive landscape dominated by multinational corporations with established global presence alongside regional players seeking to capture growing demand for plant-based alternatives. Regional manufacturers capitalize on proximity advantages and cost competitiveness while adapting formulations to local taste preferences. The market has witnessed increased activity from plant-based specialists which position themselves as premium alternatives emphasizing clean ingredients and sustainability. Strategic partnerships between dairy companies and plant-based startups are becoming more prevalent, combining traditional manufacturing expertise with innovative product development capabilities. Competition extends beyond product quality to encompass distribution efficiency, brand positioning, and digital engagement strategies that resonate with Saudi Arabia's increasingly young, urban, and digitally connected consumer base.

Saudi Arabia Non-Dairy Coffee Creamers Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Low Fat, Medium Fat, High Fat |

| Forms Covered | Powder, Liquid |

| Sources Covered | Almond, Coconut, Soy, Others |

| Flavors Covered | French Vanilla, Caramel, Hazelnut, Irish Crème, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Convenience Stores, Online Channels, Others |

| Regions Covered | Northern and Central Region, Western Region, Eastern Region, Southern Region |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Saudi Arabia Non-Dairy Coffee Creamers Market Report

The Saudi Arabia non-dairy coffee creamers market size was valued at USD 24.83 Million in 2025.

The Saudi Arabia non-dairy coffee creamers market is expected to grow at a compound annual growth rate of 6.21% from 2026-2034 to reach USD 42.70 Million by 2034.

Medium fat dominates the market with a 43% share in 2025, reflecting consumer preference for richer, creamier textures that closely mimic traditional dairy cream while maintaining moderate calorie content.

Key factors driving the Saudi Arabia non-dairy coffee creamers market include the expanding coffee culture with numerous coffee shops across Saudi Arabia, rising health consciousness with heightened regional lactose intolerance prevalence, and e-commerce expansion with the online grocery market projected to increase by 2033. Government support through Vision 2030 initiatives and investment commitment of various key market players further strengthen market fundamentals.

Major challenges include premium pricing 20 to 40% higher than dairy creamers limiting adoption, technical difficulties replicating dairy taste and texture, intense competition from multinational and regional brands, and limited consumer awareness in certain demographic segments restricting market expansion.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade