Saudi Arabia Over-the-Counter Pain Relievers Market Size, Share, Trends and Forecast by Drug Type, Formulation, Distribution Channel, End User, and Region, 2026-2034

Saudi Arabia Over-the-Counter Pain Relievers Market Summary:

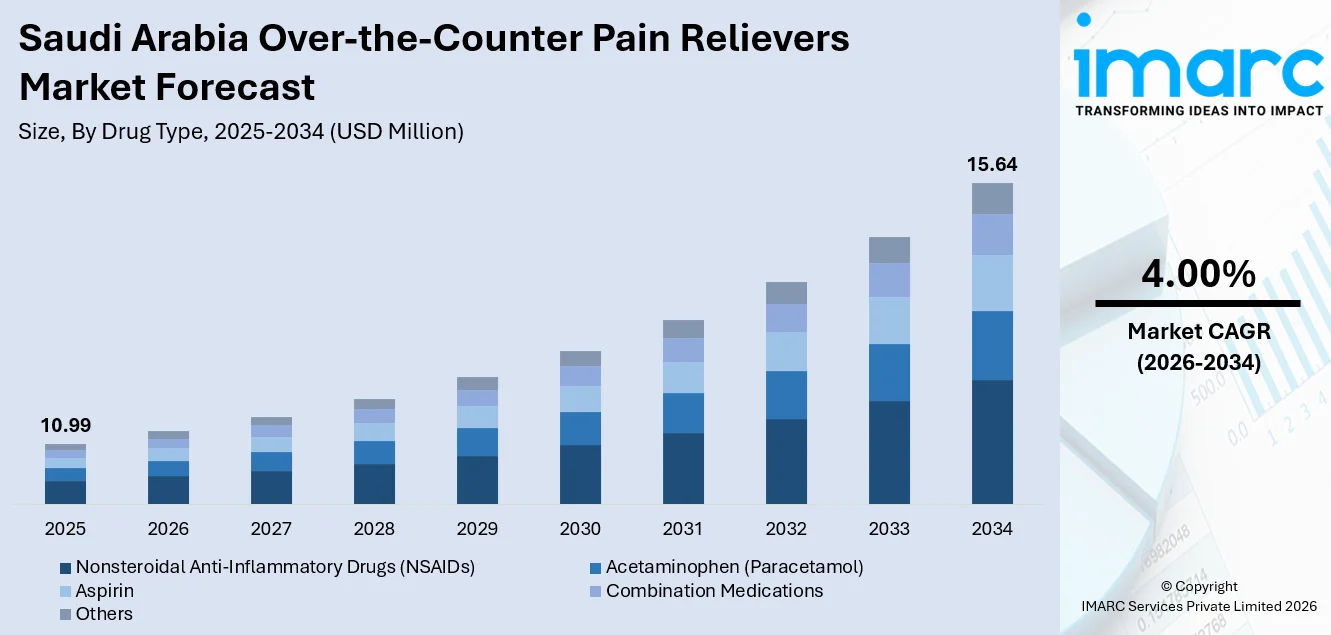

The Saudi Arabia over-the-counter pain relievers market size was valued at USD 10.99 Million in 2025 and is projected to reach USD 15.64 Million by 2034, growing at a compound annual growth rate of 4.00% from 2026-2034.

The market for over-the-counter (OTC) pain relievers in Saudi Arabia is growing due to the rising prevalence of chronic diseases, a tendency toward self-medication, and improved access to healthcare services. People increasingly rely on non-prescription analgesics for quick relief from common pain conditions. Healthcare reforms under Vision 2030 are strengthening the sector through modernization initiatives, wider pharmacy network accessibility, and enhanced service delivery. In addition, the expansion of digital health platforms and e-commerce channels is improving product reach. Developing regulatory frameworks that support safe OTC availability are also contributing to the market growth.

Key Takeaways and Insights:

- By Drug Type: Nonsteroidal anti-inflammatory drugs (NSAIDs) represent the largest segment with a market share of 35% in 2025, driven by their broad-spectrum efficacy against pain and inflammation, widespread physician familiarity, and strong individual preference for accessible relief.

- By Formulation: Tablets and capsules lead the market with a share of 48% in 2025, owing to their convenience, dosing accuracy, portability, and established consumer acceptance across all demographic segments.

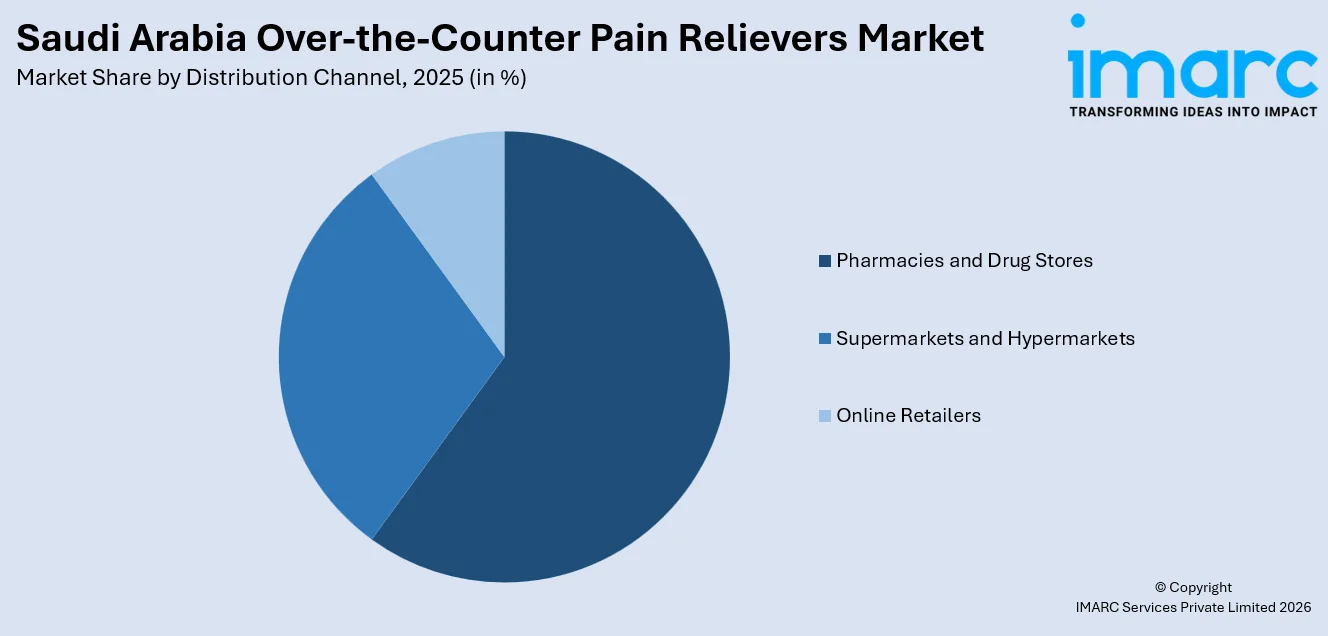

- By Distribution Channel: Pharmacies and drug stores dominate the market with a share of 60% in 2025. This dominance is because of professional pharmacist consultation availability, healthcare-associated trust, and extensive retail network coverage.

- By End User: Adults represent the largest segment with a market share of 56% in 2025, reflecting higher incidence of lifestyle-related pain conditions, workplace-associated musculoskeletal discomfort, and greater propensity for self-medicated pain management.

- By Region: Northern and Central Region dominate the market with a share of 30% in 2025, due to concentration of healthcare facilities, corporate establishments, and dense population clusters that drive high consumer demand for accessible pain management products.

- Key Players: The Saudi Arabia over-the-counter pain relievers market features a moderately competitive landscape, with established pharmaceutical manufacturers competing alongside regional distributors through product diversification, pharmacy partnerships, and digital commerce strategies.

To get more information on this market Request Sample

The market for OTC pain relievers in Saudi Arabia is influenced by a mix of demographic, lifestyle, economic, and structural healthcare elements. Rising population and gradual aging are increasing the occurrence of chronic pain disorders, while sedentary job habits, stress, and screen-heavy activities are elevating the rates of headaches and musculoskeletal pain in working-age individuals. The growing engagement in physical activity and sports is also driving the need for immediate pain relief options. Moreover, broader pharmacy networks, enhanced retail access, and increased pharmacist involvement are facilitating the acquisition of OTC analgesics. The rise of e-commerce and digital adoption is improving accessibility via online pharmacies and home delivery services. The move towards digital healthcare is evident in the Saudi Arabia e-pharmacy sector, which was valued at USD 1,086.6 Million in 2025, according to the IMARC Group, showcasing robust consumer adoption of online health purchases. Increased disposable incomes and the growing health consciousness are driving regular expenditure on self-care products, making OTC pain relievers vital components of household healthcare.

Saudi Arabia Over-the-Counter Pain Relievers Market Trends:

Rising Participation in Sports and Physical Activities

The growing focus on sports, fitness, and recreational activities in Saudi Arbia is catalyzing the demand for OTC pain relievers. Greater participation in gyms, organized sports, and community wellness initiatives is leading to a rise in minor muscle strains, exercise-related soreness, and short-term physical discomfort. This pattern is reinforced by national data, as the Physical Activity Statistics Bulletin 2024 from the General Authority for Statistics (GASTAT) reported that 58.5% of adults aged 18 and above engage in physical activity for at least 150 minutes per week, while 18.7% of children and adolescents meet daily activity recommendations. As activity levels rise, people increasingly rely on non-prescription analgesics for recovery support, expanding the market for accessible pain management solutions.

Improved Purchasing Power and Health Spending

Economic development and rising disposable incomes in Saudi Arabia are enabling individuals to increase spending on personal healthcare and wellness products, including OTC pain relievers. These products are increasingly viewed as routine household purchases rather than occasional necessities, reflecting changing consumption behavior. This shift is supported by broader economic trends; according to the Mid-Year Economic and Fiscal Performance Report FY2024, private consumption expenditure grew by 2.4% in real terms during the first half of FY2024 compared with the same period in the previous year. Higher purchasing power strengthens the demand for branded and premium analgesics, as a growing middle-class population prioritizes comfort, convenience, and timely access to reliable pain management solutions.

Growth of E-Commerce and Digital Health Purchasing Channels

Digital transformation in Saudi Arabia is significantly accelerating the adoption of online pharmacy platforms and e-commerce channels for OTC healthcare products, including pain relievers. People increasingly prioritize discreet purchasing, home delivery, and the convenience of digital access when managing minor health needs. This shift is expanding distribution beyond traditional retail pharmacies, enabling broader market penetration and stronger user engagement. The scale of this opportunity is reflected in data from the International Trade Administration, which projected that 33.6 million internet users in Saudi Arabia would participate in e-commerce by 2024. Online promotions, mobile applications, and enhanced logistics continue to support the rising demand and sustained market growth.

How Vision 2030 is Transforming the Saudi Arabia Over-the-Counter Pain Relievers Market:

Saudi Arabia’s Vision 2030 is transforming the over-the-counter pain relievers market by promoting healthcare modernization, improving access to pharmaceutical products, and encouraging greater individual wellness awareness. Investments in healthcare infrastructure, digital health platforms, and pharmacy network expansion are supporting wider availability of OTC medications across urban and semi-urban regions. The Vision’s emphasis on private sector participation is also attracting new pharmaceutical players and strengthening competition through innovation and diversified product offerings. The growing adoption of e-commerce and online pharmacy services aligns with the Kingdom’s digital transformation goals, reshaping distribution channels. Overall, Vision 2030 is strengthening the market growth by enhancing healthcare delivery, accessibility, and consumer-driven demand.

Market Outlook 2026-2034:

The Saudi Arabia over-the-counter pain relievers market is positioned for growth throughout the forecast period, driven by demographic shifts, healthcare infrastructure development, and evolving individual health behaviors. The market generated a revenue of USD 10.99 Million in 2025 and is projected to reach a revenue of USD 15.64 Million by 2034, growing at a compound annual growth rate of 4.00% from 2026-2034. Continued pharmacy network expansion, increasing digital commerce penetration, and regulatory reforms supporting broader OTC availability and are expected to sustain revenue momentum across all segments and regions.

Saudi Arabia Over-the-Counter Pain Relievers Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Drug Type |

Nonsteroidal Anti-Inflammatory Drugs (NSAIDs) |

35% |

|

Formulation |

Tablets and Capsules |

48% |

|

Distribution Channel |

Pharmacies and Drug Stores |

60% |

|

End User |

Adults |

56% |

|

Region |

Northern and Central Region |

30% |

Drug Type Insights:

- Acetaminophen (Paracetamol)

- Nonsteroidal Anti-Inflammatory Drugs (NSAIDs)

- Aspirin

- Combination Medications

- Others

Nonsteroidal anti-inflammatory drugs (NSAIDs) dominate with a market share of 35% of the total Saudi Arabia over-the-counter pain relievers market in 2025.

NSAIDs have emerged as the leading drug class for over-the-counter pain relief in Saudi Arabia, supported by their combined analgesic and anti-inflammatory effects. They are commonly used by consumers to address a wide range of everyday conditions, including musculoskeletal aches, headaches, dental pain, and menstrual cramps. Their broad therapeutic applicability and quick symptom relief make them a trusted choice for self-medication. As awareness about effective pain management grows, NSAIDs continue to dominate the market.

The segment’s market leadership is strengthened by widespread physician familiarity with NSAID pharmacology and strong consumer trust in well-known NSAID brands available through extensive pharmacy networks. The presence of diverse formulations at different price levels improves accessibility for consumers across varied income groups. The growing awareness about chronic inflammatory conditions and the need for effective pain management is also supporting the market demand. As a result, NSAIDs continue to serve as a preferred frontline option for self-medication in Saudi Arabia’s OTC pain relief market.

Formulation Insights:

- Tablets and Capsules

- Gels and Ointments

- Sprays

- Liquids and Syrups

Tablets and capsules lead with a market share of 48% of the total Saudi Arabia over-the-counter pain relievers market in 2025.

Tablets and capsules represent the largest segment due to their convenience, widespread availability, and strong user familiarity. These formats are easy to store, transport, and consume, making them a preferred option for managing common conditions, such as headaches, muscle pain, and fever. Tablets and capsules also offer accurate dosing, longer shelf life, and consistent therapeutic effects. Their broad presence across pharmacies and retail outlets further supports high adoption, reinforcing their dominance within the OTC pain relief segment.

The dominance of tablets and capsules is further strengthened by consumer preference for fast acting and reliable oral medications. Many individuals in Saudi Arabia rely on these formulations for quick relief in daily routines, supported by the growing health awareness and self-medication practices. Manufacturers also prioritize tablets and capsules because of efficient large-scale production and cost effectiveness. Availability of multiple strengths and combination products enhances consumer choice, while established regulatory frameworks support their continued leadership in the OTC pain relievers market.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Pharmacies and Drug Stores

- Supermarkets and Hypermarkets

- Online Retailers

Pharmacies and drug stores exhibit a clear dominance with a 60% share of the total Saudi Arabia over-the-counter pain relievers market in 2025.

Pharmacies and drug stores lead the market owing to their trusted role in providing safe and regulated access to medications. People prefer purchasing pain relievers from pharmacies because they ensure product authenticity, proper storage conditions, and availability of professional guidance when needed. These outlets offer a wide range of brands and formulations, making them convenient for managing common ailments such as headaches, fever, and muscle pain. Their strong presence across urban and rural areas supports high sales volumes.

The dominance of pharmacies and drug stores is further reinforced by the growing health awareness and increasing reliance on self-care solutions. Many individuals seek quick access to OTC pain relief products while valuing the reassurance of pharmacist recommendations. Pharmacies benefit from established supply chains, consistent inventory management, and strong regulatory compliance. Their integration with prescription services and expanding retail footprints continues to increase customer traffic and purchasing frequency. This growth is reflected in industry estimates, as the Saudi Arabia pharmacy retail market was valued at USD 18.9 billion in 2025 and is projected to reach USD 30.1 billion by 2034, according to the IMARC Group.

End User Insights:

- Adults

- Pediatric

- Geriatric

Adults dominate with a market share of 56% of the total Saudi Arabia over-the-counter pain relievers market in 2025.

Adults hold the biggest market share attributed to greater exposure to work-related stress, daily physical strain, and lifestyle-linked health concerns. This dominance aligns with demographic structure, as GASTAT’s 2024 population data shows that individuals aged 15 to 64 represent 74.7% of the total population. Headaches, back pain, joint discomfort, and muscle soreness are more common within this group, increasing dependence on convenient non-prescription pain relief options. Adults also frequently prefer self-medication for mild to moderate conditions, seeking quick relief without clinical visits.

The dominance of adults is further supported by the growing health awareness and proactive pain management practices among the working age population. Increased participation in physical activities, longer working hours, and sedentary routines contribute to recurring pain symptoms. Adults are more familiar with dosage guidelines and product choices, encouraging confident OTC purchases. Easy access to pharmacies and widespread availability of pain relievers further strengthen adult consumption, positioning this group as the primary end user segment in Saudi Arabia’s OTC pain relievers market.

Regional Insights:

- Northern and Central Region

- Western Region

- Eastern Region

- Southern Region

Northern and Central Region dominate with a market share of 30% of the total Saudi Arabia over-the-counter pain relievers market in 2025.

Northern and Central Region lead the market driven by their high population concentration, strong healthcare infrastructure, and greater access to pharmacies and retail drug outlets. Major urban centers in these regions have higher demand for self-care products, supported by busy lifestyles and widespread user awareness. The presence of large hospitals, clinics, and distribution networks also strengthens product availability, making OTC pain relievers easily accessible for managing common pain conditions.

The dominance of these regions is further reinforced by higher disposable incomes, urbanization, and increasing adoption of modern healthcare practices. Residents in Northern and Central Saudi Arabia often rely on OTC medications for quick relief from headaches, muscle pain, and fever without requiring medical consultations. Strong retail penetration, well established pharmacy chains, and greater promotional activity from pharmaceutical companies further drive sales. As healthcare access and consumer purchasing power remain strong, these regions continue to represent the largest user base for OTC pain relievers.

Market Dynamics:

Growth Drivers:

Why is the Saudi Arabia Over-the-Counter Pain Relievers Market Growing?

Expansion of Retail Pharmacy Networks and Accessibility

The continued expansion of pharmacy chains and modern healthcare retail outlets across Saudi Arabia is significantly improving user access to OTC pain relief products. Wider geographic reach, extended operating hours, and the availability of professional pharmacist guidance are enhancing purchasing convenience and individual confidence. Retail modernization, supported by organized product layouts and stronger supply chain networks, are further increasing product visibility and availability. This trend is reflected in recent developments, as in 2025 Aster Pharmacy launched its flagship “Trio” store in Riyadh. The store introduced a drive-through pharmacy and wellness concept and is part of plans to open 180 outlets across the Kingdom over the next 2–3 years with Abdul Mohsen Al Hokair Group.

Increasing Incidence of Lifestyle-Related Pain Conditions

Lifestyle changes in Saudi Arabia, marked by sedentary work patterns, limited physical activity, and elevated stress levels, are driving a higher incidence of pain-related conditions among the population. Musculoskeletal discomfort, back pain, and tension headaches are increasingly reported, particularly among working-age groups, leading to recurring needs for symptom relief. This trend is supported by recent academic findings, which is a study published in Cureus on April 21, 2025 reported that 54.3% of medical students at King Saud University in Riyadh experienced musculoskeletal pain. As a result, people are turning more frequently to OTC analgesics for routine pain management, sustaining consistent demand across demographics.

Demographic Growth and Aging Population Trends

Saudi Arabia’s population growth, combined with gradual aging trends, is increasing the share of individuals experiencing chronic and recurring pain conditions. Older adults commonly require ongoing pain management for joint stiffness, arthritis-related discomfort, and mobility limitations, supporting sustained demand for non-prescription analgesics. This demographic shift is underscored by findings from the Elderly Survey 2025, which reported that approximately 1.7 million people in Saudi Arabia were aged 60 years and above, accounting for 4.8% of the total population. Alongside this, family-oriented healthcare purchasing habits encourage households to keep OTC pain relievers readily available, reinforcing the steady market growth over time.

Market Restraints:

What Challenges the Saudi Arabia Over-the-Counter Pain Relievers Market is Facing?

Regulatory Scrutiny and Approval Delays for New OTC Formulations

The Saudi Food and Drug Authority maintains rigorous evaluation standards for OTC pharmaceutical products, which can extend market entry timelines for innovative formulations. Comprehensive safety and efficacy documentation requirements, combined with periodic regulatory framework updates, create procedural complexities that may delay product commercialization and limit the pace of portfolio diversification.

Limited Health Literacy in Rural and Remote Regions

Despite ongoing healthcare development across Saudi Arabia, notable gaps in health literacy remain between major cities and rural regions. In remote and underserved communities, limited awareness about proper self-medication practices and the benefits of OTC pain relievers reduces user confidence and uptake. This uneven understanding restricts market penetration, keeping demand largely concentrated in metropolitan areas and slowing broader expansion into less developed regions.

Price Sensitivity Among Fixed-Income Consumer Segments

A significant share of Saudi Arabia’s population, including expatriate workers and elderly individuals relying on pensions, faces financial limitations that reduce discretionary spending on OTC medicines. High price sensitivity within these groups discourages the purchase of premium pain relief products and shifts demand toward more affordable alternatives. This trend places pressure on pricing strategies and limits the market’s ability to generate higher revenue growth.

Competitive Landscape:

The Saudi Arabia over-the-counter pain relievers market shows a moderately competitive setup, with global pharmaceutical brands operating alongside regional distributors and newer local companies. Competition is driven by product innovation in formulations, pricing approaches, strong pharmacy shelf visibility, and the growing digital sales channels. Companies are focusing heavily on widening their distribution networks through partnerships with retail pharmacies, hospitals, and online platforms. Furthermore, evolving regulations and compliance requirements enforced by the Saudi Food and Drug Authority are influencing market access, shaping competitive strategies, and affecting positioning across the value chain.

Recent Developments:

- November 2025: Bayer announced a strategic MoU with Alpha Pharma to locally manufacture Aspirin Protect in Saudi Arabia, with production expected to begin in 2028. The partnership supported Saudi Vision 2030 by strengthening pharmaceutical localization and reducing reliance on imports. Bayer said the initiative will also transfer advanced manufacturing expertise to help build a more self-reliant healthcare system in the Kingdom.

Saudi Arabia Over-the-Counter Pain Relievers Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Drug Types Covered | Acetaminophen (Paracetamol), Nonsteroidal Anti-Inflammatory Drugs (NSAIDs), Aspirin, Combination Medications, Others |

| Formulations Covered | Tablets and Capsules, Gels and Ointments, Sprays, Liquids and Syrups |

| Distribution Channels Covered | Pharmacies and Drug Stores, Supermarkets and Hypermarkets, Online Retailers |

| End Users Covered | Adult, Pediatric, Geriatric |

| Regions Covered | Northern and Central Region, Western Region, Eastern Region, Southern Region |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Saudi Arabia Over-the-Counter Pain Relievers Market Report

The Saudi Arabia over-the-counter pain relievers market size was valued at USD 10.99 Million in 2025.

The Saudi Arabia over-the-counter pain relievers market is expected to grow at a compound annual growth rate of 4.00% from 2026-2034 to reach USD 15.64 Million by 2034.

Nonsteroidal anti-inflammatory drugs (NSAIDs) hold the largest revenue share of 35% in 2025, driven by their dual analgesic and anti-inflammatory efficacy, widespread physician familiarity, and strong consumer preference for accessible pain relief solutions.

Key factors driving the Saudi Arabia over-the-counter pain relievers market include the increasing demand for OTC pain relievers, as more people experience minor strains and exercise-related soreness. Supporting this trend, GASTAT’s Physical Activity Statistics Bulletin 2024 reported that 58.5% of adults achieve 150 minutes of weekly activity, driving recovery product use.

Major challenges include regulatory scrutiny extending approval timelines for new OTC formulations, limited health literacy in rural and remote communities, price sensitivity among fixed-income consumer segments, and distribution infrastructure gaps restricting product availability in underserved regions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)