Saudi Arabia Pet Care Market Size, Share, Trends and Forecast by Product Type, Pet Type, Distribution Channel, and Region, 2026-2034

Saudi Arabia Pet Care Market Size, Share, Trends & Forecast (2026-2034)

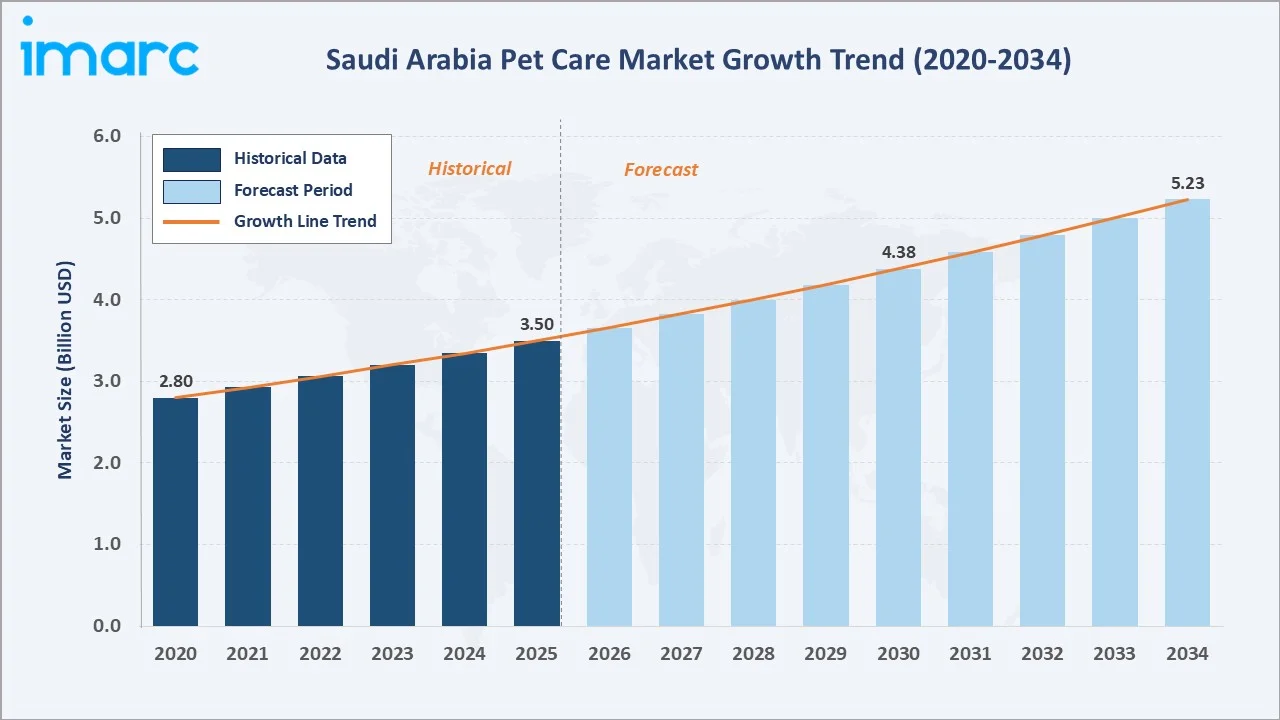

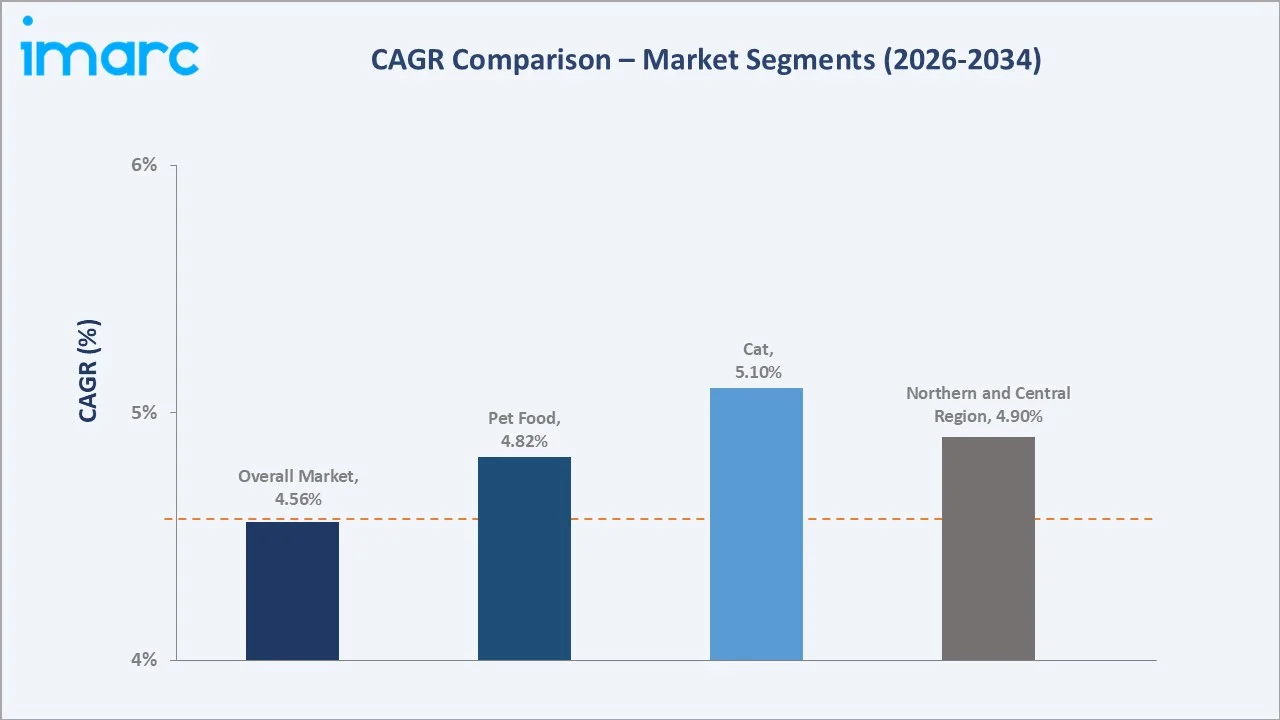

The Saudi Arabia pet care market reached USD 3.50 Billion in 2025 and is projected to reach USD 5.23 Billion by 2034, growing at a CAGR of 4.56% during 2026-2034. Rising pet ownership, growing disposable incomes, Western lifestyle influences, and increasing demand for premium pet products are the primary factors propelling this growth. Pet food dominates product type at 72.8% share (2025), while cat leads by pet type at 56.2%. The Northern and Central Region accounts for 40.3% of total market revenue, anchored by Riyadh's urban pet-owning population.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.50 Billion |

|

Forecast Market Size (2034) |

USD 5.23 Billion |

|

CAGR (2026-2034) |

4.56% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Product Type |

Pet Food (72.8%, 2025) |

|

Largest Pet Type |

Cat (56.2%, 2025) |

|

Dominant Region |

Northern and Central Region (40.3%, 2025) |

The market expanded from USD 2.80 Billion in 2020 to USD 3.50 Billion in 2025, anchored at USD 4.38 Billion in 2030, and projected to reach USD 5.23 Billion by 2034. Growth is supported by rising urbanization, expanding retail infrastructure, and Vision 2030's consumer market diversification agenda.

To get more information on this market, Request Sample

Pet food leads segment growth, driven by premiumization trends and rising cat and dog adoption rates. The cat pet type exhibits the highest CAGR at ~5.10%, reflecting the cultural shift toward indoor cat ownership among Saudi millennials.

Executive Summary

The Saudi Arabia pet care market reached USD 3.50 Billion in 2025, driven by accelerating pet humanization trends, rising per-capita incomes, and expanding retail and digital commerce infrastructure. Pet ownership has surged across urban Saudi households, particularly among younger demographics influenced by Western lifestyles. The market is projected to reach USD 5.23 Billion by 2034 at a 4.56% CAGR, underpinned by structural demand growth across food, grooming, and ancillary pet care categories.

Pet Food dominates at 72.8% share (2025), fueled by rising demand for premium, grain-free, and protein-rich diets. Cats account for 56.2% of pet type share, reflecting their suitability for apartment living in Saudi urban centers. The Northern and Central Region leads regionally at 40.3%, driven by Riyadh's dense pet-owning population and advanced retail ecosystem. In September 2024, Tree Digital Insurance Agency launched the Kingdom's first comprehensive pet insurance product, signaling market maturity.

Emerging opportunities include mobile grooming services, veterinary telemedicine, and smart pet-tech adoption. The e-commerce channel is growing rapidly as platforms such as Amazon.sa, PetZone, and MyPets expand selection and delivery capabilities. Saudi Arabia's 95% smartphone penetration rate and robust digital payment infrastructure create a strong foundation for continued online pet care market expansion through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

Pet Food - 72.8% share (2025) |

|

Largest Pet Type |

Cat - 56.2% share (2025) |

|

Dominant Region |

Northern and Central Region - 40.3% (2025) |

|

Fastest Growing Pet Type |

Cat (~5.10% CAGR, 2026-2034) |

|

Market Opportunity |

Premium pet food, e-commerce, pet insurance expansion |

Key Analytical Observations Supporting The Above Data:

- Pet Food at 72.8% product share (2025): Organic, protein-rich, and functional diets are gaining prominence as pet owners align pet nutrition with their own health priorities.

- Cat segment leads at 56.2% pet type share (2025): Cats are preferred for urban apartment living due to lower space requirements, driving consistent demand for cat food and accessories.

- Northern and Central Region dominates at 40.3% (2025): Riyadh's high-income urban demographics, modern retail formats, and largest veterinary clinic density anchor regional leadership.

- E-commerce penetration accelerating: Saudi Arabia's online pet product sales are growing at a double-digit rate, supported by 33.6 million e-commerce users by 2024.

Saudi Arabia Pet Care Market Overview

The Saudi Arabia pet care market encompasses all products and services designed to support pet health, nutrition, hygiene, and wellbeing. Core product categories include pet food (dry and wet), grooming products, veterinary supplies, accessories, and ancillary services. The market operates across offline specialty stores, pet boutiques, veterinary clinics, hypermarkets, and rapidly expanding online platforms.

Macroeconomic tailwinds are significant. Vision 2030's consumer market diversification, GDP growth in non-oil sectors, and a growing young urban population are reshaping household spending patterns. The General Authority for Statistics (GASTAT) reports increasing household expenditure on recreation and lifestyle products, within which pet care is an expanding subcategory. Regulatory oversight includes the Saudi Food and Drug Authority (SFDA), which governs animal welfare and import standards for pet food and veterinary products.

Market Dynamics

To evaluate market opportunities, Request Sample

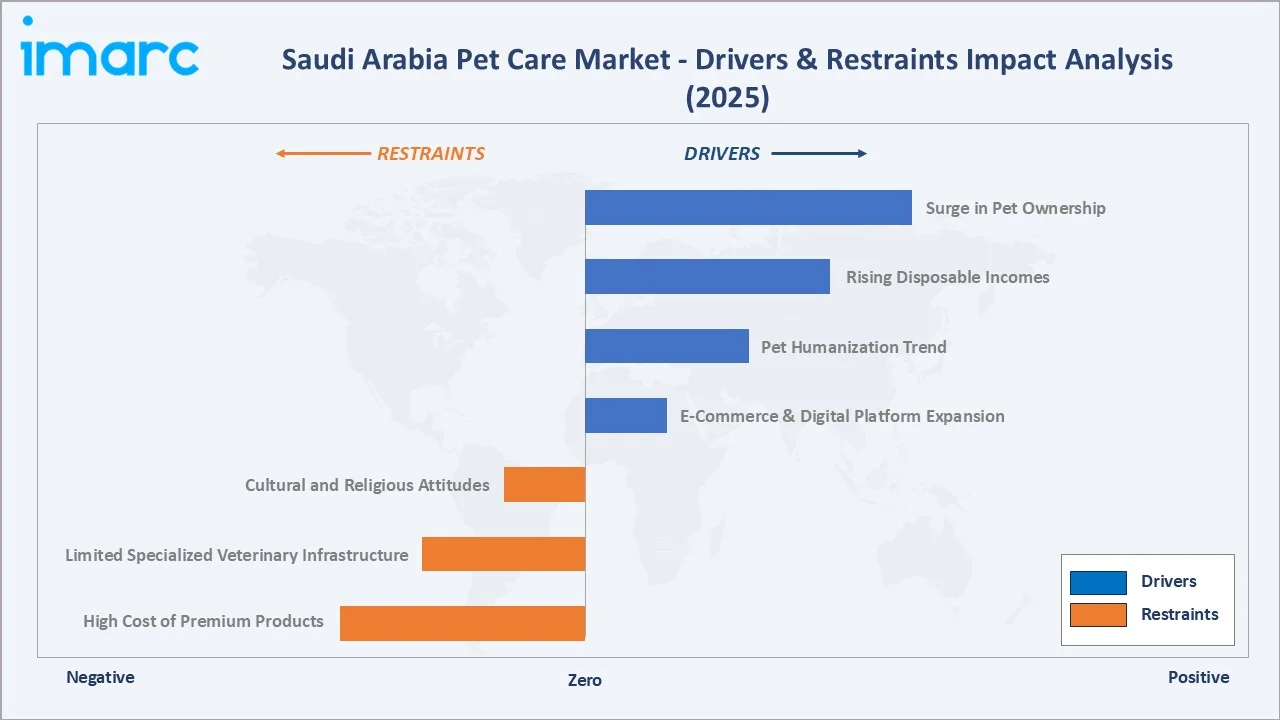

Market Drivers

- Surge in Pet Ownership: Urban Saudi households, especially millennials and Gen-Z consumers, are increasingly adopting cats and dogs. Pet ownership rates have risen markedly since 2020, supported by changing social dynamics and exposure to global pet culture through social media.

- Rising Disposable Incomes: Saudi Arabia's per-capita income growth under Vision 2030 economic reforms has enabled higher discretionary spending on premium pet products, including organic pet food, specialty veterinary care, and designer accessories.

- Pet Humanization Trend: Owners increasingly treat pets as family members. This drives spending on premium nutrition, wellness products, grooming services, and veterinary preventive care - elevating average revenue per pet owner year-on-year.

- E-Commerce & Digital Platform Expansion: Saudi Arabia's over 95% smartphone penetration and a 33.6 million e-commerce users by 2024 have accelerated online pet product sales. Platforms like Amazon.sa, PetZone, and MyPets offer broad selections with home delivery and mobile grooming booking.

Market Restraints

- Cultural and Religious Attitudes: Traditional perspectives in some segments of Saudi society limit broader pet adoption, particularly for dogs. This constrains addressable market size compared to Western benchmarks.

- Limited Specialized Veterinary Infrastructure: Despite growth, the number of specialized veterinary clinics per capita remains below international standards, reducing consumer confidence in pet healthcare.

- High Cost of Premium Products: Imported premium pet food and accessories carry price premiums due to logistics costs, import duties, and limited domestic manufacturing - creating affordability barriers for price-sensitive consumer segments.

Market Opportunities

- Premiumization of Pet Nutrition: Growing health consciousness among pet owners creates opportunities for brands offering functional, natural, and breed-specific diets. The premium pet food sub-segment is growing faster than the mass market.

- Mobile and On-Demand Services: Mobile grooming, on-demand veterinary consultation, and pet boarding subscription services represent high-growth white spaces. Saudi Arabia's urban density and digital readiness make these models viable.

- Pet Insurance Market: September 2024 saw the Kingdom's first pet insurance product launch. The segment is nascent but growing, with potential to expand veterinary spending and create recurring revenue streams for insurers and providers alike.

Market Challenges

- Import Dependency: The majority of premium pet food and grooming products are imported, exposing the market to supply chain disruptions, freight cost volatility, and currency exchange risk.

- Limited Local Manufacturing Base: Before DFF's planned plant, domestic pet food production was minimal. This restricts competitive pricing and slows market growth in price-sensitive segments.

- Lack of Awareness for Preventive Pet Healthcare: Consumer education around vaccination, dental care, and preventive nutrition remains limited outside major urban centers, constraining veterinary service market development.

Emerging Market Trends

1. Premiumization of Pet Food

Saudi pet owners are increasingly opting for grain-free, protein-rich, and organic pet food formulations. Human-grade ingredient standards are becoming a purchase trigger for high-income pet owners. Brands offering breed-specific and life-stage nutrition are outperforming mass-market competitors in revenue growth.

2. Rise of E-Commerce and Mobile Pet Services

Online pet product platforms, including Amazon.sa and PetZone, are growing rapidly as Saudi Arabia's digital commerce infrastructure matures. Click-and-groom and mobile veterinary consultation services are emerging as high-demand urban convenience solutions, particularly in Riyadh and Jeddah.

3. Smart Pet Technology Adoption

GPS pet trackers, automated feeders, health monitoring collars, and smart litter boxes are entering Saudi Arabia's urban pet owner market. Growing tech-savviness among younger Saudi pet owners is driving trial and adoption of these premium devices.

4. Emergence of Pet Insurance and Financial Products

Tree Digital Insurance Agency's 2024 launch of the Kingdom's first comprehensive pet insurance is a landmark development. Pet insurance reduces the financial barrier to veterinary care, encouraging owners to seek higher-quality services and spend more on preventive healthcare.

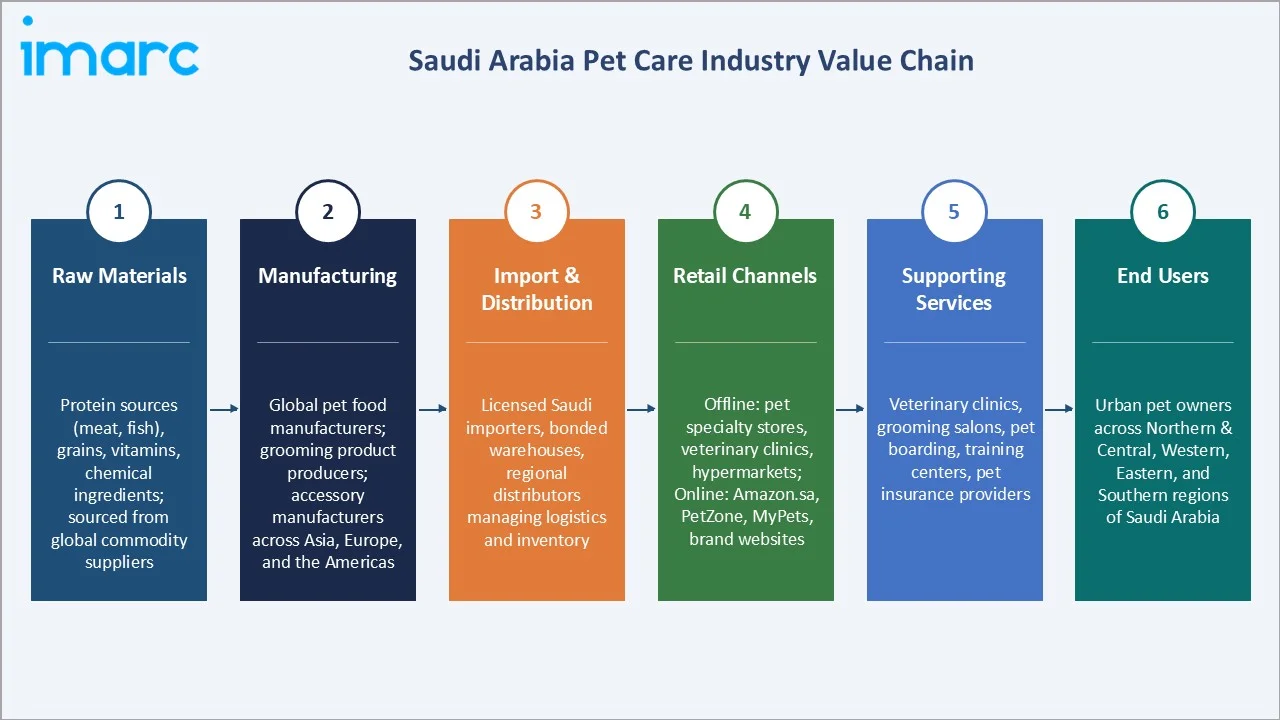

Industry Value Chain Analysis

Saudi Arabia's pet care value chain spans raw material sourcing through global pet product manufacturers, import and distribution channels, and multi-tier retail networks serving the Kingdom's growing pet-owning population.

|

Stage |

Key Participants |

|

Raw Materials |

Protein sources (meat, fish), grains, vitamins, chemical ingredients; sourced from global commodity suppliers |

|

Manufacturing |

Global pet food manufacturers; grooming product producers; accessory manufacturers across Asia, Europe, and the Americas |

|

Import & Distribution |

Licensed Saudi importers, bonded warehouses, regional distributors managing logistics and inventory |

|

Retail Channels |

Offline: pet specialty stores, veterinary clinics, hypermarkets; Online: Amazon.sa, PetZone, MyPets, brand websites |

|

Supporting Services |

Veterinary clinics, grooming salons, pet boarding, training centers, pet insurance providers |

|

End Users |

Urban pet owners across Northern & Central, Western, Eastern, and Southern regions of Saudi Arabia |

Distribution in Saudi Arabia typically follows a two-tier model: global brands supply licensed Saudi importers and regional distributors, who in turn serve retail outlets and e-commerce fulfillment centers. Local manufacturing by DFF is beginning to create an alternative domestic supply pathway.

Technology Landscape in the Saudi Arabia Pet Care Industry

Premium & Functional Pet Nutrition Technology

Advanced extrusion and wet-cooking technologies enable manufacturers to produce high-protein, grain-free, and breed-specific pet food formulations. Cold-pressed and freeze-dried processing preserves nutritional integrity - a key selling point for premium products gaining traction in Saudi Arabia's premium segment.

E-Commerce and Digital Platform Technology

AI-powered recommendation engines on Saudi pet e-commerce platforms help consumers identify suitable products based on pet breed, age, and health conditions. Real-time inventory management and last-mile delivery logistics powered by GPS routing software are enabling same-day delivery in major Saudi cities.

Smart Pet Technology and Wearables

GPS trackers, health monitoring collars, and automated feeders connected to mobile apps are entering Saudi Arabia's tech-savvy urban pet owner market. IoT-enabled devices allow owners to monitor pet activity, feeding schedules, and health metrics remotely, a growing product category with high average transaction values.

Veterinary Telemedicine

Mobile veterinary consultation platforms are emerging, allowing pet owners to access licensed veterinarians via video call. This addresses the geographic constraint of limited veterinary clinic density in secondary Saudi cities, while providing convenience for urban pet owners.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Pet Food |

72.8% |

2025 |

|

Pet Type |

Cat |

56.2% |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

Region |

Northern and Central Region |

40.3% |

2025 |

By Product Type

To access detailed market analysis, Request Sample

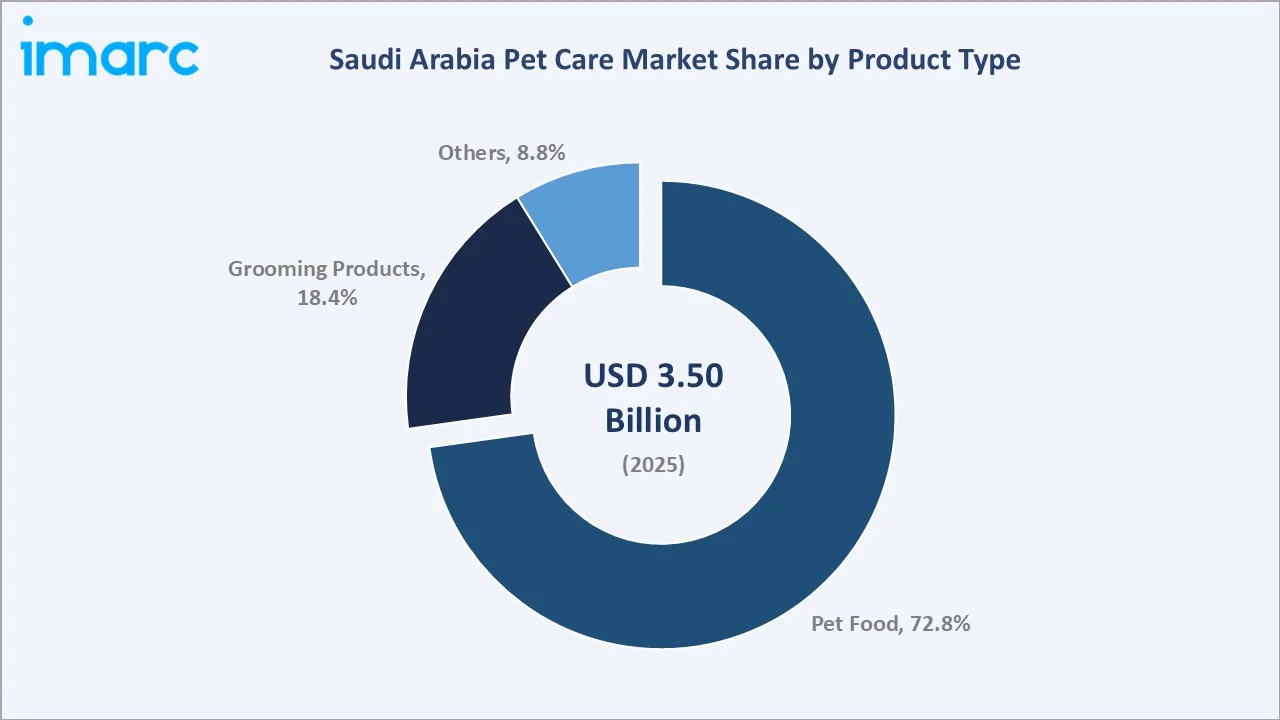

Pet food dominates at 72.8% market share (2025). Rising demand for premium, breed-specific, and life-stage formulations is expanding average revenue per purchase. Grooming products account for 18.4% (2025). This segment includes shampoos, conditioners, brushes, combs, clippers, and scissors. Growth is supported by rising awareness of pet hygiene, expansion of professional grooming salons, and increasing availability of specialized grooming products on e-commerce platforms. Others at 8.8% (2025) cover accessories, toys, bedding, litter, and veterinary supplies. This is a high-growth niche driven by premiumization and pet humanization trends.

By Pet Type

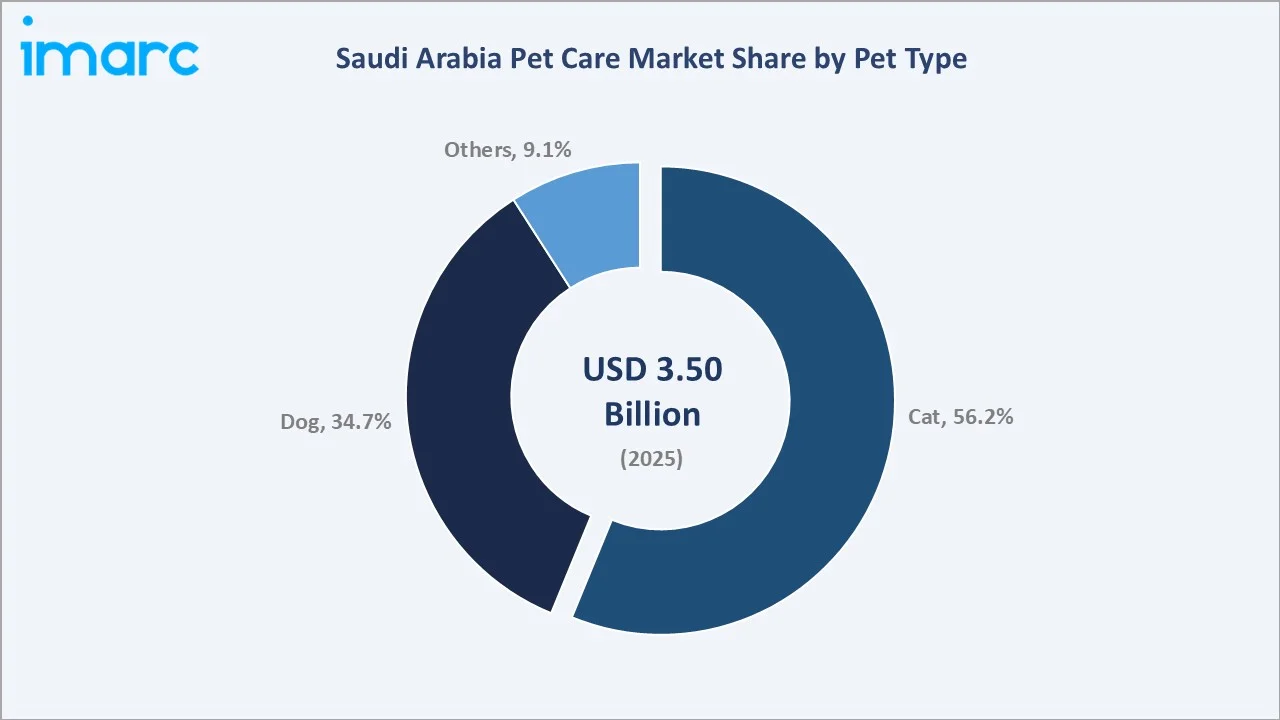

Cat leads at 56.2% share (2025). Cultural acceptance, suitability for apartment living, and lower maintenance requirements make cats the preferred pet choice among Saudi urban households. The cat segment is also the fastest growing at an estimated ~5.10% CAGR, driven by rising cat-specific premium food and accessory demand. Dog accounts for 34.7% (2025). Dog ownership is more prevalent in villa communities and expatriate households. Premium dog food brands, training services, and dog grooming are high-value sub-segments within this category. Others at 9.1% (2025) include birds, fish, and small animals - traditional pet types with stable but slower-growing demand profiles.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers & Characteristics |

|

Northern and Central Region |

40.3% |

Highest pet owner concentration around Riyadh; modern retail infrastructure; largest density of veterinary clinics and pet specialty stores; strong e-commerce adoption |

|

Western Region |

27.6% |

Jeddah and Makkah anchor demand; tourism and expatriate community driving pet services; coastal lifestyle supporting aquatic and specialty pet categories |

|

Eastern Region |

20.8% |

Expatriate-heavy workforce around Dammam and Dhahran; high disposable incomes in oil sector households; strong demand for imported premium pet brands |

|

Southern Region |

11.3% |

Emerging urbanization and infrastructure development; growing retail access; slower adoption but positive trajectory supported by Vision 2030 regional development |

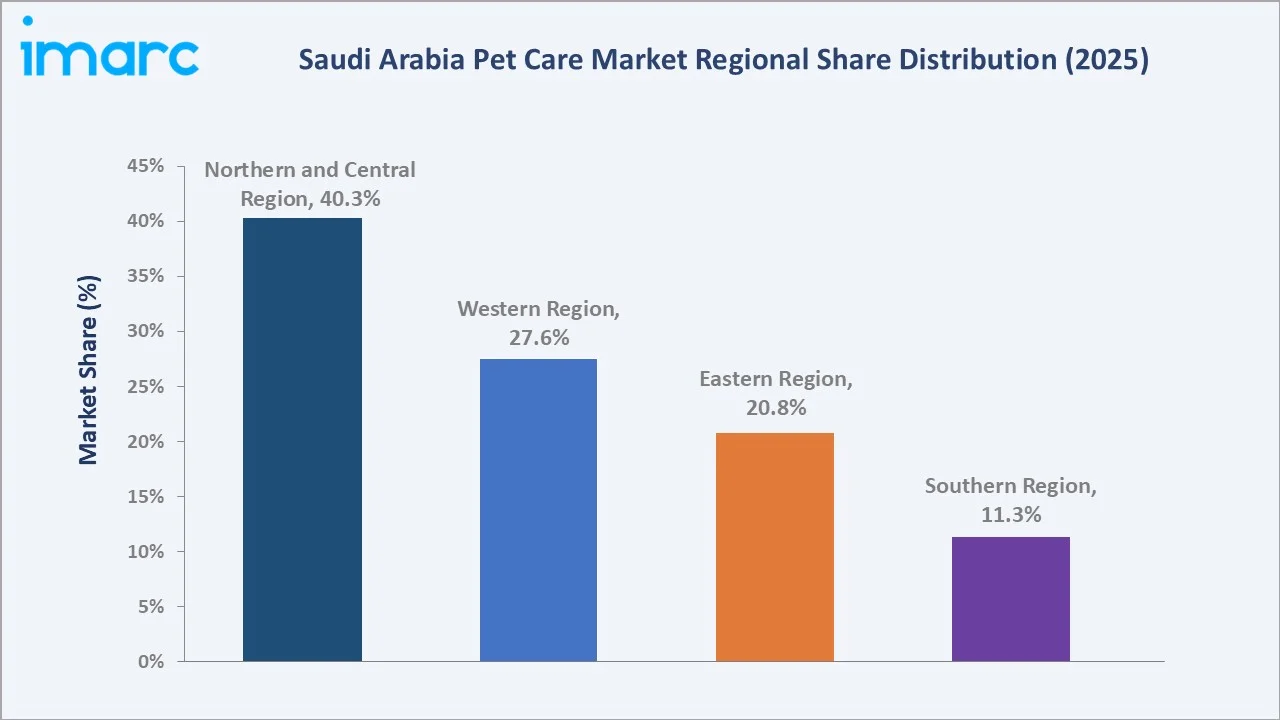

The Northern and Central Region's 40.3% dominance reflects Riyadh's status as Saudi Arabia's economic capital and most populous city. High-income urban demographics, advanced retail infrastructure, and the largest concentration of veterinary clinics and grooming salons anchor this region's market leadership. Its share is expected to remain dominant through 2034 as Riyadh's population continues to expand under Vision 2030 urban development plans.

The Western Region's 27.6% share is anchored by Jeddah's large urban population and cosmopolitan lifestyle. The Eastern Region benefits from high-income oil sector households and a significant expatriate community with established Western pet-ownership norms. The Southern Region, while smallest at 11.3%, represents an emerging growth frontier as infrastructure investment and retail modernization progress.

Competitive Landscape

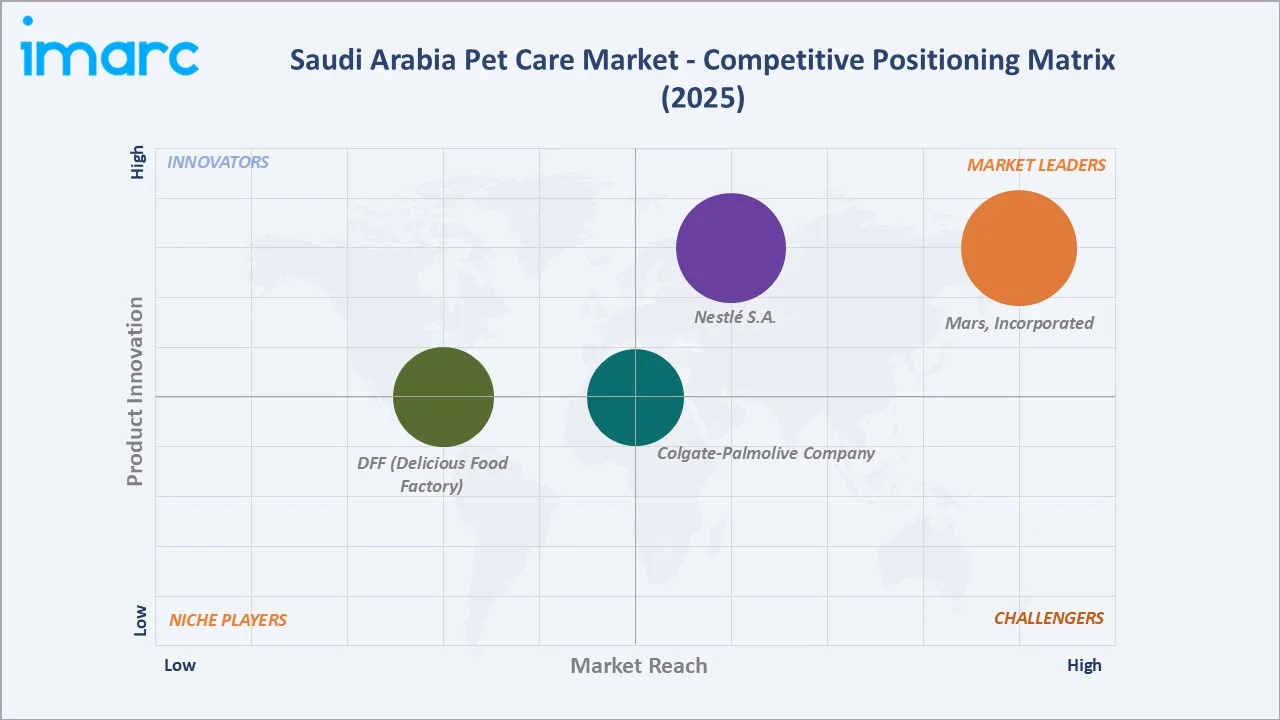

Saudi Arabia's pet care market is led by multinational pet food corporations alongside regional distributors and emerging local producers. Global brands including Mars Incorporated and Nestlé S.A. dominate the premium pet food segment through established distributor relationships, strong brand equity, and wide product portfolios catering to diverse pet nutritional needs.

|

Company Name |

Brand / Product Lines |

Market Position |

Core Strength |

|

Mars, Incorporated |

Whiskas, Pedigree, Royal Canin, Sheba |

Market Leader |

Operates Mars Petcare, largest global pet food portfolio; deep Saudi distribution network across modern and traditional trade |

|

Nestlé S.A. |

Purina Pro Plan, Friskies, Felix, Fancy Feast, Purina ONE, Cat Chow, Dog Chow |

Market Leader |

Operates Nestlé Purina PetCare, premium and mass-market dual positioning; strong brand recognition among Saudi pet owners |

|

Colgate-Palmolive Company |

Hill's Science Diet and Hill's Prescription Diet |

Established Player |

Operates Hill's Pet Nutrition, specialty nutrition backed by veterinary endorsements across Saudi clinics |

|

DFF (Delicious Food Factory) |

Horayra, Purevet, Kulaib |

Emerging Player |

First major Saudi-based pet food manufacturer; plans for 100,000-ton annual pet food output |

The competitive landscape is bifurcated: global multinationals dominate the premium and super-premium segments through their established brand equity and veterinary channel presence, while regional e-commerce retailers and emerging local manufacturers are carving out positions in the mid-tier and value segments through competitive pricing and localized product offerings.

Key Company Profiles

Mars, Incorporated

Mars, Incorporated is one of the world's largest pet care companies by revenue, with a comprehensive portfolio spanning nutrition, veterinary health, and pet services. In Saudi Arabia, Mars holds strong market share through its iconic brands available across hypermarkets, pet stores, and e-commerce platforms.

- Product Portfolio: Whiskas, Pedigree, Royal Canin, Sheba, and others.

- Strategic Focus: Dual positioning across mass-market (Whiskas, Pedigree) and super-premium (Royal Canin) segments; deepening veterinary clinic partnerships.

Nestlé S.A.

Nestlé S.A., which operates Nestlé Purina PetCare, is a global leader in pet nutrition, present in Saudi Arabia through an extensive portfolio of cat and dog food brands. Its strong distribution network and brand recognition make it a leading competitor in the premium pet food space.

- Product Portfolio: Purina Pro Plan, Friskies, Felix, Fancy Feast, Purina ONE, Cat Chow, Dog Chow, and others.

- Strategic Focus: Premium brand positioning through veterinary endorsement; expanding digital commerce presence on Amazon.sa and regional platforms.

Colgate-Palmolive Company

Colgate-Palmolive Company, which operates Hill's Pet Nutrition, occupies the science-based nutrition niche in Saudi Arabia, distributed primarily through veterinary clinics and specialty pet stores. Its Prescription Diet range is particularly relevant as Saudi veterinary care standards develop.

- Product Portfolio: Hill's Science Diet and Hill's Prescription Diet

- Strategic Focus: Veterinary channel-led growth; science-backed nutrition positioning for health-conscious pet owners.

Market Concentration Analysis

Saudi Arabia's pet care market exhibits moderate concentration at the premium branded level. Mars Incorporated and Nestlé S.A. collectively command an estimated 35-45% of Saudi Arabia's pet food market by value (2025), driven by their extensive brand portfolios and established distribution networks.

Below the premium tier, the market is significantly fragmented. Regional distributors, e-commerce platforms, and specialty retailers collectively serve a diverse consumer base - from budget-conscious expatriate workers to ultra-high-income Saudi pet enthusiasts purchasing premium imported brands. Price-competitive Asian pet food brands are gaining market share in the value tier, particularly on e-commerce platforms.

Consolidation trends are emerging at the importer and retail level. Saudi retail conglomerates are expanding their multi-brand pet care portfolios, and e-commerce platforms are leveraging their logistics infrastructure to offer private-label pet products alongside international brands. DFF's planned local manufacturing facility marks a structural shift that may reshape competitive dynamics in the mass-market pet food segment by 2027-2028.

Investment & Growth Opportunities

Fastest Growing Segments

The cat pet type segment (~5.10% CAGR) and e-commerce distribution channel (double-digit growth) represent the highest-velocity opportunities. Premium and functional pet food sub-categories, mobile grooming, and pet insurance are growing well above overall market CAGR of 4.56%.

Emerging Market Opportunities

- Premium and Functional Pet Nutrition: Saudi pet owners' increasing health awareness creates demand for grain-free, high-protein, breed-specific diets. First-mover international brands establishing veterinary channel partnerships have a significant advantage.

- Mobile Pet Services Platform: Saudi Arabia's urban density and high smartphone penetration make mobile grooming, on-demand veterinary consultation, and pet boarding booking platforms commercially viable with high repeat usage rates.

- E-Commerce Specialty Retail: The online pet product channel is underserved relative to general retail. Dedicated Saudi pet e-commerce platforms with subscription models for recurring consumables (food, litter, grooming supplies) offer high lifetime customer value.

Future Market Outlook (2026-2034)

The Saudi Arabia pet care market is projected to grow from USD 3.50 Billion in 2025 to USD 5.23 Billion by 2034 at a 4.56% CAGR. Three structural forces anchor this growth trajectory: (1) Saudi Arabia's demographic dividend - a young, urban-oriented population with rising pet ownership propensity; (2) Vision 2030's consumer market diversification driving retail expansion and lifestyle spending growth; and (3) the ongoing premiumization of pet care spending as pet humanization deepens.

The emergence of local manufacturing (DFF's planned plant) will materially improve price competitiveness in the mass market, potentially accelerating volume growth above current projections. The pet insurance market, e-commerce channel maturation, and smart pet technology adoption will further expand the sector's total addressable market. The Southern Region offers the highest incremental growth opportunity as infrastructure investment and retail modernization progress under Vision 2030 regional development plans.

By 2030, the market is expected to reach USD 4.38 Billion, reflecting compounding pet ownership growth, rising average spend per pet, and expanding ancillary services. The decade ending 2034 will likely see Saudi Arabia emerge as the Gulf Cooperation Council's dominant pet care market by absolute value, surpassing UAE.

Research Methodology

Primary Research

Primary research comprised structured interviews with 60+ industry stakeholders (2025), including Saudi pet specialty retailers, pet food brand representatives, veterinary clinic operators, e-commerce platform managers, and pet service entrepreneurs. Quantitative surveys with Saudi pet owners were conducted across Riyadh, Jeddah, and Dammam.

Secondary Research

Secondary research encompassed pet import and registration data, General Authority for Statistics (GASTAT) household expenditure surveys, Saudi Vision 2030 program documentation, e-commerce market data from CST, and company announcements from key market participants. Over 100 secondary sources were reviewed and triangulated.

Forecasting Models

Market size forecasts were developed using bottom-up models combining pet population growth rates, average spend per pet, and product category penetration dynamics. Key inputs include GASTAT demographic and income projections, Vision 2030 urban development forecasts, and e-commerce adoption curves validated against CST digital economy statistics.

Saudi Arabia Pet Care Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered |

|

| Pet Types Covered | Dog, Cat, Others |

| Distribution Channels Covered | Offline, Online |

| Regions Covered | Northern and Central Region, Western Region, Eastern Region, Southern Region |

| Companies Covered | Mars Incorporated, Nestlé S.A., Colgate-Palmolive Company, DFF (Delicious Food Factory), etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Saudi Arabia pet care market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Saudi Arabia pet care market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Saudi Arabia pet care industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Saudi Arabia Pet Care Market Report

The Saudi Arabia pet care market reached USD 3.50 Billion in 2025, driven by rising pet ownership, premiumization trends, and e-commerce channel expansion across the Kingdom.

The market is projected to grow at a CAGR of 4.56% during 2026-2034, reaching USD 5.23 Billion by 2034, supported by structural demand growth across all major categories.

Pet food leads with 72.8% market share in 2025. Premium, grain-free, and protein-rich formulations are driving above-average revenue growth within the segment.

Cat leads with 56.2% share in 2025. Cat suitability for apartment living in urban Saudi households and lower maintenance needs drive dominant adoption rates.

The Northern and Central Region leads with 40.3% share in 2025, anchored by Riyadh's high pet ownership density, advanced retail formats, and largest veterinary clinic concentration.

The Saudi Arabia pet care market is projected to reach USD 4.38 Billion by 2030, supported by sustained pet ownership growth, local manufacturing investment, and premium product demand.

Key players include Mars, Incorporated, Nestlé S.A., Colgate-Palmolive Company, and DFF (Delicious Food Factory), among others.

Online pet product sales are growing rapidly. Saudi Arabia's 95% smartphone penetration and platforms like Amazon.sa and PetZone are making pet care products accessible nationwide with home delivery.

DFF's 55,000 sqm plant near Riyadh will produce 60,000 tons dry and 40,000 tons wet pet food annually - reducing import dependency and creating competitive local brands for the Saudi market.

Vision 2030 drives consumer market diversification, retail sector expansion, and rising household incomes - all supporting growth in lifestyle spending categories including pet care.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)