Saudi Arabia Plant-Based Condiments Market Size, Share, Trends and Forecast by Source, Product, Application, End User, and Region, 2026-2034

Saudi Arabia Plant-Based Condiments Market Summary:

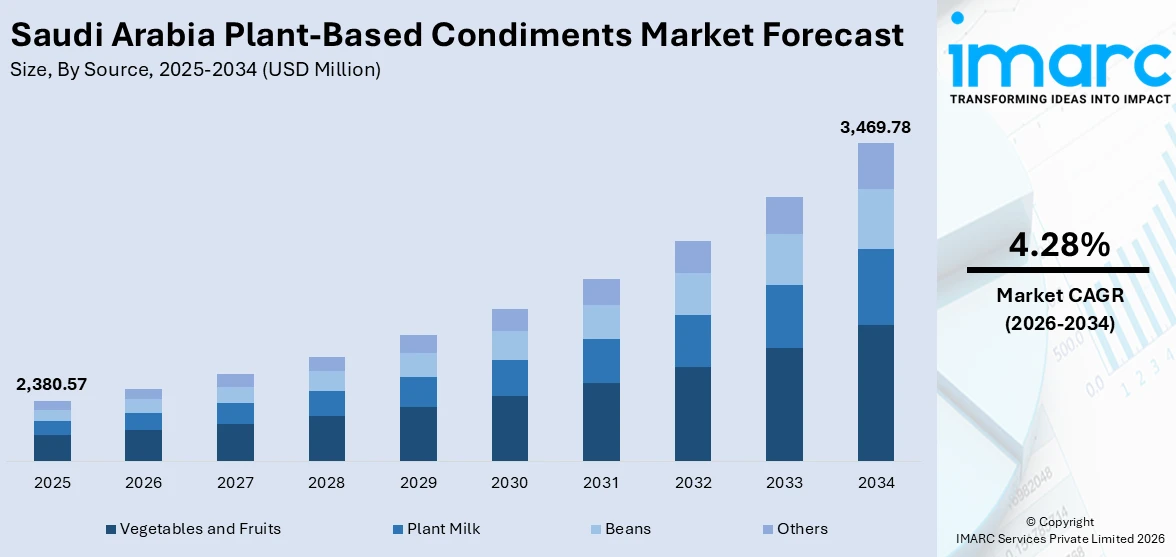

The Saudi Arabia plant-based condiments market size was valued at USD 2,380.57 Million in 2025 and is projected to reach USD 3,469.78 Million by 2034, growing at a compound annual growth rate of 4.28% from 2026-2034.

The Saudi Arabia plant-based condiments market is experiencing steady growth as consumers increasingly prioritize health-conscious dietary choices and sustainable food alternatives. Rising awareness about the environmental benefits of plant-based ingredients, coupled with the Kingdom's Vision 2030 initiatives promoting food security and local manufacturing, is accelerating market expansion. The growing influence of global culinary trends, rapid urbanization, and expanding foodservice infrastructure are reshaping consumption patterns across households and commercial establishments. Additionally, the proliferation of modern retail channels and e-commerce platforms is enhancing product accessibility, while government support for agricultural diversification and clean-label food production is strengthening the Saudi Arabia plant-based condiments market share.

Key Takeaways and Insights:

- By Source: Vegetables and fruits dominate the market with a share of 48% in 2025, owing to the widespread availability of locally sourced produce, strong consumer preference for natural ingredients, and traditional culinary practices that incorporate vegetable and fruit-based condiments such as tomato pastes and fruit-based dressings.

- By Product: Paste, purees, and sauce lead the market with a share of 36% in 2025, reflecting the integral role of tomato-based products and savory sauces in Middle Eastern cuisine, supported by their versatility across home cooking and commercial food preparation applications.

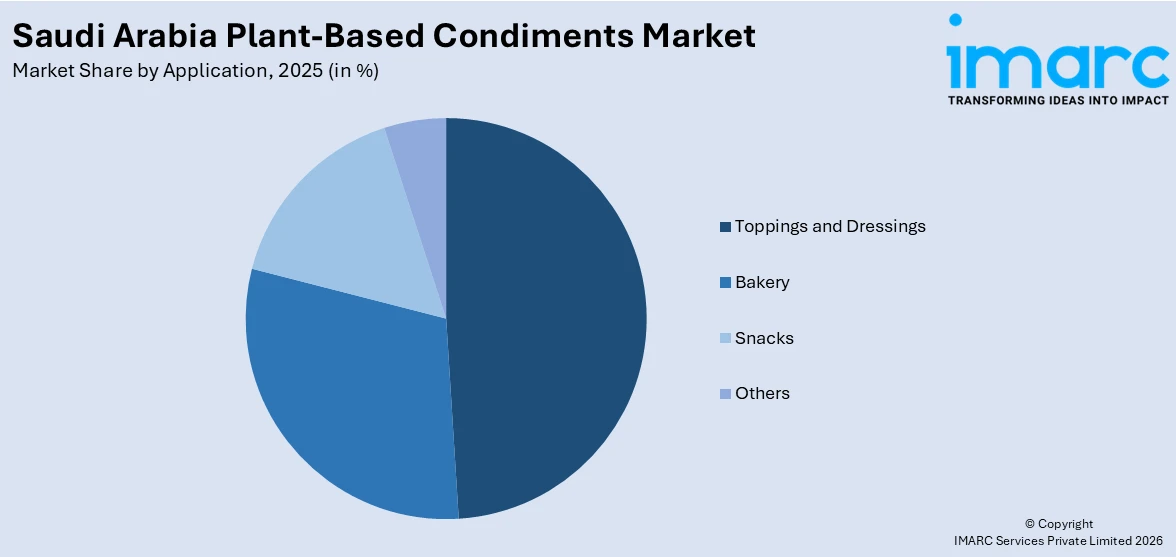

- By Application: Toppings and dressings exhibit a clear dominance with a 49% share in 2025, driven by growing consumer demand for flavor enhancement in home-cooked meals, expanding quick-service restaurant operations, and increasing popularity of international cuisines requiring diverse dressing options.

- By End User: Household and retail represent the largest segment with a market share of 72% in 2025, underpinned by the growing trend of home cooking, expansion of modern retail formats including hypermarkets and e-commerce platforms, and rising consumer preference for convenient ready-to-use condiment products.

- By Region: Northern and Central Region dominates the market with 38% share in 2025, driven by the concentration of Saudi Arabia's population in Riyadh, higher disposable incomes, advanced retail infrastructure, and the presence of numerous food processing facilities and distribution networks.

- Key Players: Leading companies drive the Saudi Arabia plant-based condiments market by expanding product portfolios, introducing health-focused formulations, and strengthening distribution networks. Their investments in local manufacturing, sustainable packaging, and strategic partnerships with foodservice operators boost market penetration and accelerate adoption across diverse consumer segments.

To get more information on this market Request Sample

The Saudi Arabia plant-based condiments market is advancing rapidly as government initiatives, shifting consumer preferences, and technological innovations converge to reshape the food industry landscape. The Kingdom's sustained investments in food processing infrastructure and agricultural modernization are creating favorable conditions for market expansion. Health consciousness is driving demand for clean-label, organic, and low-sodium condiment alternatives, with consumers increasingly scrutinizing product ingredients and seeking transparency in food labeling. The expanding quick-service restaurant sector and growing tourism industry are creating new consumption channels across urban centers, while e-commerce platforms are democratizing access to specialty plant-based products for consumers in suburban and rural areas. Saudi Arabia's position as a regional food manufacturing hub is strengthening through strategic partnerships between domestic and international companies focused on developing locally adapted, halal-certified condiment solutions that align with cultural preferences and dietary requirements.

Saudi Arabia Plant-Based Condiments Market Trends:

Rising Consumer Preference for Health-Conscious Condiment Alternatives

Saudi consumers are increasingly seeking plant-based condiments with cleaner labels, reduced sodium content, and natural ingredients. This shift reflects broader health awareness driven by rising obesity and diabetes prevalence rates across the Kingdom. Manufacturers are responding by reformulating products to eliminate artificial preservatives and additives while introducing organic variants. The Saudi Food and Drug Authority's nutritional labeling requirements have accelerated transparency, empowering consumers to make informed choices. This health-driven transformation is supporting Saudi Arabia plant-based condiments market growth as brands prioritize functional ingredients and wellness-oriented positioning.

Expansion of E-Commerce and Digital Retail Channels

Digital transformation is reshaping how Saudi consumers discover and purchase plant-based condiments, with online grocery platforms experiencing substantial expansion. E-commerce in Saudi Arabia's retail sector doubled between 2020 and 2025, with annual compound growth of 15% annually, according to a September 2024 report from Saudi Arabia’s Small and Medium Enterprises. Prominent retailers like Carrefour KSA and Nana offer specialist and health-focused condiment sections with same-day delivery in major cities. This digital accessibility is particularly appealing to younger, tech-savvy consumers who value convenience and product variety, driving broader market penetration.

Integration of Traditional Middle Eastern Flavors with Modern Formulations

Plant-based condiment manufacturers are innovating by combining traditional Middle Eastern taste profiles with contemporary health-conscious formulations. Products featuring tahini, hummus, and regional spice blends are being developed using plant-based ingredients to appeal to culturally rooted palates while meeting modern dietary preferences. International companies are launching localized variants, such as Arabic-spiced ketchup and regional seasoning blends, to capture market share. This fusion approach enables brands to honor culinary traditions while positioning products as healthier alternatives to conventional condiments.

How Vision 2030 is Transforming the Saudi Arabia Plant-Based Condiments Market:

Saudi Arabia's Vision 2030 initiative is fundamentally reshaping the plant-based condiments landscape through strategic investments in food security, sustainable agriculture, and local manufacturing capabilities. In 2024, Saudi Arabia's Agricultural Development Fund sanctioned SR2 Billion (USD 533.33 Million) in credit facilities and loans focused on enhancing food sustainability and security across the Kingdom. The initiative's emphasis on economic diversification has attracted multinational food companies to establish regional production facilities, reducing import dependence and creating employment opportunities. Government-backed programs promoting organic farming, water-efficient agricultural technologies, and food processing infrastructure are enabling domestic manufacturers to scale production of plant-based condiment ingredients. Additionally, the Saudi Green Initiative's sustainability targets are encouraging companies to adopt eco-friendly packaging and carbon-neutral production processes, positioning Saudi Arabia as a regional leader in sustainable food manufacturing.

Market Outlook 2026-2034:

The Saudi Arabia plant-based condiments market demonstrates promising growth potential as consumer preferences evolve toward healthier, sustainable food alternatives and government initiatives continue to strengthen domestic food manufacturing capabilities. The market generated a revenue of USD 2,380.57 Million in 2025 and is projected to reach a revenue of USD 3,469.78 Million by 2034, growing at a compound annual growth rate of 4.28% from 2026-2034. Rising urbanization, expanding foodservice infrastructure, and increasing tourism under Vision 2030 will create substantial demand for diverse plant-based condiment offerings across household and commercial segments.

Saudi Arabia Plant-Based Condiments Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

| Source | Vegetables and Fruits | 48% |

| Product | Paste, Purees, and Sauce | 36% |

| Application | Toppings and Dressings | 49% |

| End User | Household and Retail | 72% |

| Region | Northern and Central Region | 38% |

Source Insights:

- Plant Milk

- Beans

- Vegetables and Fruits

- Others

Vegetables and fruits dominate with a market share of 48% of the total Saudi Arabia plant-based condiments market in 2025.

The vegetables and fruits segment maintains commanding leadership in Saudi Arabia's plant-based condiments market, driven by the deeply rooted culinary tradition of incorporating tomato-based sauces, vegetable pastes, and fruit-derived dressings into Middle Eastern cuisine. Tomato pastes and purees represent a cornerstone of Saudi household cooking, serving as essential ingredients in traditional dishes and everyday meal preparation. Consumer familiarity with these ingredients, combined with their perceived naturalness and nutritional benefits, reinforces strong purchasing preferences across all demographic segments.

The segment benefits from established domestic and international supply chains that ensure consistent product availability at competitive prices. Local producers leverage the Kingdom's agricultural infrastructure to source fresh vegetables and fruits, while imported specialty ingredients cater to premium market segments. The growing emphasis on organic and pesticide-free produce is creating opportunities for differentiated product offerings. Additionally, the versatility of vegetable and fruit-based condiments across home cooking, foodservice, and food manufacturing applications supports sustained demand growth throughout the forecast period.

Product Insights:

- Table Dressings

- Paste, Purees, and Sauce

- Seasoning

- Pickled

Paste, purees, and sauce leads with a share of 36% of the total Saudi Arabia plant-based condiments market in 2025.

The paste, purees, and sauce category commands substantial market presence due to the essential role these products play in traditional Saudi and broader Middle Eastern culinary preparations. Cooking sauces and pastes serve as foundational ingredients in signature dishes including kabsa, machboos, and various stews that define the regional gastronomic identity. These products are integral to daily meal preparation across households, enabling consumers to achieve authentic flavors with minimal effort and preparation time.

Product innovation within this segment focuses on convenience formats, extended shelf life, and health-enhanced formulations. Manufacturers are introducing squeeze packs, single-serve sachets, and organic variants to appeal to evolving consumer preferences for portability and clean-label options. The expansion of quick-service restaurants and food delivery platforms is driving commercial demand for consistent, high-quality sauce products that meet stringent taste and safety standards. Furthermore, international brands are developing localized formulations featuring Arabic spices and regional flavor profiles to capture market share from established domestic producers, intensifying competition and fostering continuous product development across the category.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Bakery

- Snacks

- Toppings and Dressings

- Others

Toppings and dressings exhibit a clear dominance with a 49% share of the total Saudi Arabia plant-based condiments market in 2025.

Toppings and dressings command market leadership driven by diverse consumption occasions spanning home cooking, dining out, and food delivery. The proliferation of quick-service restaurants has substantially expanded dressing consumption, as these establishments integrate various plant-based condiments into their menu offerings and provide table-side options for customers seeking personalized flavor experiences. Consumer demand for flavor variety and customization continues to fuel product diversification across this application segment, encouraging manufacturers to develop extensive product portfolios.

The growing influence of social media and food influencers is shaping consumer preferences for innovative topping combinations and international dressing varieties, exposing Saudi consumers to global culinary trends and fusion flavor profiles. Health-conscious consumers are driving demand for low-calorie, plant-based dressing alternatives that deliver flavor without compromising nutritional goals, prompting reformulation efforts across the industry. Additionally, the expansion of food delivery platforms is creating new consumption occasions as restaurants package dressings with delivery orders, extending product reach beyond traditional retail and foodservice channels into home environments and strengthening brand visibility among residential consumers.

End User Insights:

- HoReCa

- Household and Retail

Household and retail represent the leading segment with a 72% share of the total Saudi Arabia plant-based condiments market in 2025.

The household and retail segment maintains commanding market dominance, reflecting the entrenched culture of home cooking among Saudi families and the expansion of modern retail infrastructure. The segment has demonstrated consistent growth over recent years, driven by evolving consumer lifestyles and increased product accessibility across the Kingdom. Supermarkets and hypermarkets serve as primary distribution channels, with private label offerings gaining traction among budget-conscious consumers seeking value without compromising quality.

The rising number of women entering the workforce, supported by government reforms, is driving demand for convenient ready-to-use condiments that reduce meal preparation time while maintaining authentic flavors. E-commerce platforms are enhancing accessibility, particularly in suburban areas, while subscription-based grocery services introduce consumers to new plant-based products. The segment benefits from diverse pack size options catering to various household sizes and consumption frequencies, from bulk economy formats to single-serve convenience packages, enabling manufacturers to address the needs of diverse consumer groups effectively.

Regional Insights:

- Northern and Central Region

- Western Region

- Eastern Region

- Southern Region

Northern and Central Region holds the largest share with 38% of the total Saudi Arabia plant-based condiments market in 2025.

The Northern and Central Region, anchored by the capital city Riyadh, dominates the Saudi Arabia plant-based condiments market through its concentration of population, purchasing power, and commercial activity. Riyadh generates approximately 40% of nationwide foodservice revenue, creating substantial demand for condiment products across both household and commercial segments. The region benefits from advanced retail infrastructure, including major hypermarket chains and the highest e-commerce penetration rates in the Kingdom, facilitating broad product accessibility.

The establishment of the Jeddah Food Cluster in November 2024, backed by SAR 20 Billion (USD 5.3 Billion) investment, is strengthening regional food manufacturing capabilities and supply chain efficiency. Major food producers and distributors maintain regional headquarters and distribution centers in the Northern and Central Region, ensuring optimal inventory management and rapid product delivery. Additionally, the region's diverse expatriate population drives demand for international plant-based condiment varieties, creating opportunities for niche product introductions catering to varied culinary preferences.

Market Dynamics:

Growth Drivers:

Why is the Saudi Arabia Plant-Based Condiments Market Growing?

Rising Health Consciousness and Demand for Clean-Label Products

Growing health awareness among Saudi consumers is significantly driving demand for plant-based condiments as alternatives to conventional products containing artificial additives and preservatives. Lifestyle diseases including obesity, diabetes, and cardiovascular conditions are prompting dietary shifts toward healthier food choices. Manufacturers are responding by developing clean-label formulations featuring transparent ingredient lists and natural preservatives. The Saudi Food and Drug Authority's implementation of enhanced nutritional labeling requirements in 2025 has further empowered consumers to make informed purchasing decisions. This regulatory environment encourages product innovation focused on reduced sodium, sugar-free variants, and organic certifications that command premium pricing.

Expansion of Foodservice Sector and Quick-Service Restaurant Networks

The rapid expansion of Saudi Arabia's foodservice industry is creating substantial commercial demand for plant-based condiment products across restaurants, cafes, and catering operations. The market has demonstrated strong growth trajectory and is expected to continue expanding throughout the forecast period, driven by urbanization and changing consumer lifestyles. Quick-service restaurant chains are increasingly featuring plant-based condiment options as both table accompaniments and menu ingredients to cater to health-conscious diners. The growth of cloud kitchens, which optimize operational efficiency through virtual brand management from single locations, is further accelerating condiment consumption. Additionally, mega-projects under Vision 2030 are integrating foodservice as critical components of new urban developments, creating substantial commercial opportunities for plant-based condiment suppliers seeking to establish presence in emerging markets.

Government Initiatives Supporting Local Food Manufacturing

Saudi Arabia's strategic focus on food security and economic diversification under Vision 2030 is creating favorable conditions for plant-based condiment manufacturing. The Kingdom's Ministry of Environment, Water, and Agriculture has implemented comprehensive greenhouse expansion plans to increase agricultural production capacity, supporting domestic ingredient sourcing for condiment production. Government financing programs through the Agricultural Development Fund provide accessible capital for food processing ventures, while the Sustainable Agricultural Rural Development Program offers incentives for expanding organic and plant-based food production projects. International food companies are establishing regional production facilities to meet local content requirements and access public contracts, bringing technological expertise and manufacturing capabilities that strengthen the domestic plant-based condiment industry.

Market Restraints:

What Challenges the Saudi Arabia Plant-Based Condiments Market is Facing?

Price Sensitivity and Competition from Conventional Products

Plant-based condiments often command premium prices compared to conventional alternatives, creating barriers for budget-conscious consumers. Rising inflation and government austerity measures are prompting some consumers to switch to less expensive brands or reduce purchase quantities. Private label products are gaining market share by offering competitive pricing, increasing pressure on branded plant-based offerings to demonstrate clear value differentiation. This price sensitivity limits market penetration in price-sensitive consumer segments.

Limited Consumer Awareness of Plant-Based Benefits

Despite growing health consciousness, many Saudi consumers remain unfamiliar with the specific nutritional and environmental benefits of plant-based condiments compared to traditional products. Consumer education regarding the advantages of plant-derived ingredients over conventional options requires sustained marketing investment. Cultural preferences for familiar products and resistance to dietary change among certain demographics present adoption challenges. Manufacturers must invest in awareness campaigns to communicate product benefits effectively.

Supply Chain Dependencies and Raw Material Volatility

Saudi Arabia's reliance on imported raw materials for plant-based condiment production creates vulnerability to global supply chain disruptions and price fluctuations. The Kingdom imports a substantial majority of its food products, exposing manufacturers to currency exchange risks and logistics uncertainties. Seasonal variations in agricultural output affect ingredient availability and pricing, potentially impacting production costs and retail pricing stability. Building domestic agricultural capacity and diversifying supplier networks are essential to mitigate these challenges.

Competitive Landscape:

The Saudi Arabia plant-based condiments market features a competitive landscape comprising established domestic manufacturers, multinational food corporations, and emerging specialty brands. Leading players compete through product innovation, distribution network expansion, and strategic partnerships with foodservice operators. Companies are investing in research and development to introduce health-enhanced formulations, sustainable packaging solutions, and locally adapted flavor profiles. The market structure encourages both price-based competition in mainstream segments and differentiation strategies in premium categories. Consolidation activity is increasing as larger players seek to acquire specialized capabilities and regional market access, while private label growth is intensifying competitive pressure across all segments.

Recent Developments:

- In March 2025, Tanmiah Food Company signed a Memorandum of Understanding with Griffith Foods to collaborate on creating halal-targeted sauces, seasonings, and ingredient solutions in Saudi Arabia. The partnership reflects Vision 2030 objectives related to food security and sustainability, with plans to establish an advanced research and development hub and the Kingdom's first facility entirely focused on halal ingredients production.

Saudi Arabia Plant-Based Condiments Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Sources Covered | Plant Milk, Beans, Vegetables and Fruits, Others |

| Products Covered | Table Dressings, Paste, Purees, and Sauce, Seasoning, Pickled |

| Applications Covered | Bakery, Snacks, Toppings and Dressings, Others |

| End Users Covered | HoReCa, Household and Retail |

| Regions Covered | Northern and Central Region, Western Region, Eastern Region, Southern Region |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Saudi Arabia Plant-Based Condiments Market Report

The Saudi Arabia plant-based condiments market size was valued at USD 2,380.57 Million in 2025.

The Saudi Arabia plant-based condiments market is expected to grow at a compound annual growth rate of 4.28% from 2026-2034 to reach USD 3,469.78 Million by 2034.

Vegetables and fruits dominated the market with a share of 48%, driven by the widespread use of tomato-based products and vegetable pastes in traditional Middle Eastern cuisine, combined with growing consumer preference for natural, locally sourced ingredients.

Key factors driving the Saudi Arabia plant-based condiments market include rising health consciousness among consumers, expanding foodservice sector and quick-service restaurant networks, government initiatives supporting local food manufacturing under Vision 2030, and the growth of e-commerce and modern retail channels.

Major challenges include price sensitivity and competition from lower-cost conventional products, limited consumer awareness about plant-based benefits, supply chain dependencies on imported raw materials, raw material price volatility, and the need for sustained marketing investment to drive consumer education and adoption.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)