Saudi Arabia Real Estate Market Size, Share, Trends and Forecast by Property Type and Region, 2026-2034

Saudi Arabia Real Estate Market Size & Forecast 2026-2034

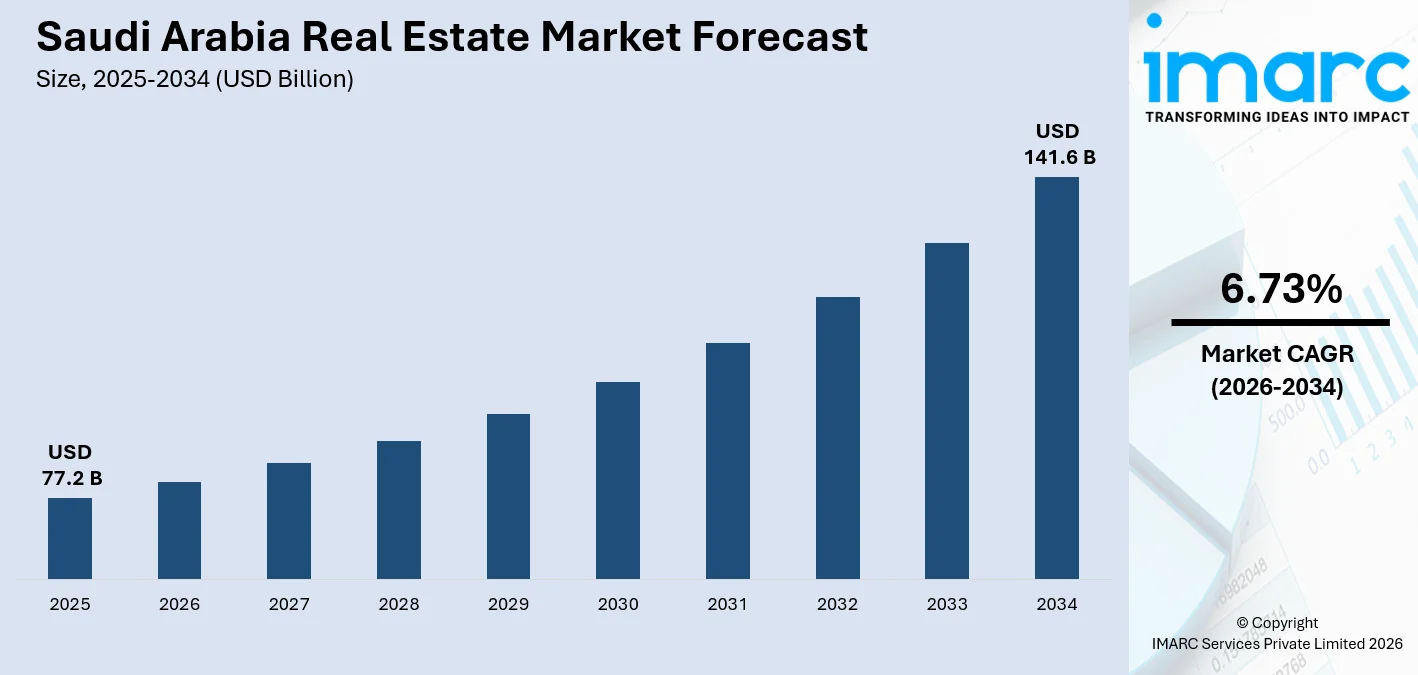

The Saudi Arabia real estate market size, valued at USD 77.2 Billion in 2025, is projected to reach USD 141.6 Billion by 2034, growing at a CAGR of 6.73% from 2026-2034, driven by Vision 2030's ambitious economic diversification initiatives and massive infrastructure investments. According to data from the General Authority for Statistics, the 1.7% year-on-year rise in Q2 2024 real estate prices, driven by a 2.8% increase in residential property values, reflects strengthening housing demand and growing investor confidence, thereby accelerating overall momentum in the Saudi Arabia real estate market.

To get more information on this market Request Sample

Saudi Arabia Real Estate Industry Analysis — Key Insights

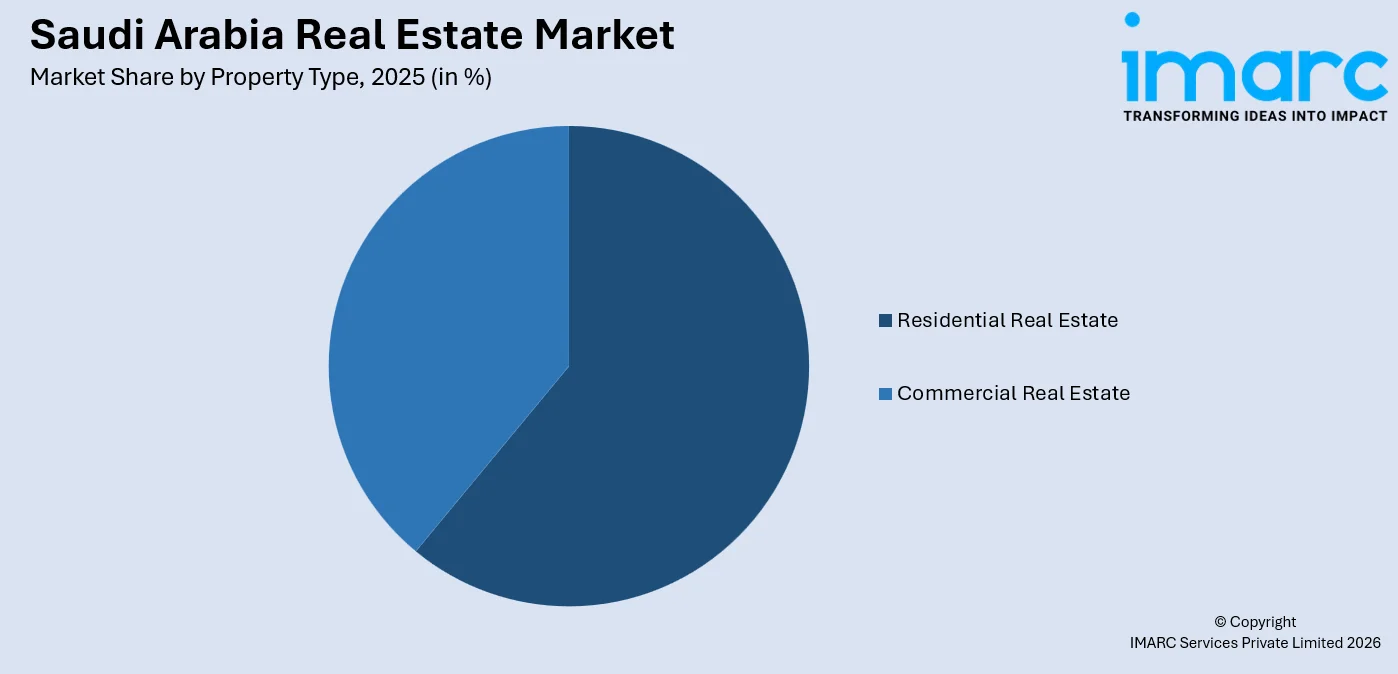

- Residential real estate led the property type with 60.5% in 2025 - reflecting strong government housing initiatives and population growth, with the Sakani program supported 62,023 Saudi families since the beginning of the year until the end of August 2023, through subsidized financing and accelerated development approvals.

- Northern and Central region leads regionally with 35.0% market share in 2025 - positioning the capital as the primary real estate hub, driven by Vision 2030's Regional Headquarters Programme requiring multinational companies to establish bases there by 2024.

Saudi Arabia Real Estate Trends and Dynamic 2026

Market Trends

Mega-project acceleration reshapes real estate development across the Kingdom

Vision 2030's giga-projects are fundamentally transforming Saudi real estate landscape with unprecedented scale and ambition. In October 2025, NEOM secured contracts worth $24 billion, creating sustained demand across residential, commercial, and hospitality segments.

Foreign ownership liberalization attracts global investment capital

Saudi Arabia's new property law, effective January 2026, enabling foreign ownership in major cities, reducing transaction taxes. Destination Saudi Report 2024 revealed that Saudi Arabia real estate market growth accelerated as international investors gained access to residential and commercial properties, with 84% of global high-net-worth individuals expressing interest in Makkah and Madinah assets.

Digital transformation enhances market transparency and efficiency

Technology adoption revolutionizes real estate transactions through blockchain and AI integration. In December 2023, Ejar recorded 8 million digital leases, providing institutional investors with enhanced Saudi Arabia real estate market forecast.

- PropTech Integration: Platforms like Quant utilize satellite data analyzing for real-time property insights and investment decisions.

- Smart City Development: NEOM integrates AI for urban planning with blockchain-based transactions, managing future residents.

- Sustainable Construction: New Murabba embeds 25% energy-reduction targets with fast-track zoning compressing.

- Mixed-Use Development: Project connecting to the Grand Mosque, Masar offers 24,000 hotel units with 13,000 residential units targeting extended-stay pilgrims.

Growth Drivers

Vision 2030 economic diversification creates sustained real estate demand

The Kingdom's strategic shift from oil dependency drives massive infrastructure investments across multiple sectors. In 2024, the Public Investment Fund reported $913 billion in assets under management, funding tourism, entertainment, and urban regeneration projects that generate continuous real estate development opportunities.

Population growth and urbanization intensify housing requirements

Saudi Arabia's population reached 35.3 million in 2024, rising 4.7% year-on-year, with household sizes shrinking to create annual demand for new homes. Urban population concentration at 85% by 2024, projected to reach 86.3% by 2030, drives sustained residential and commercial real estate development.

Tourism expansion fuels hospitality and leisure property development

Government targets for 150 million annual visitors by 2030, catalyze a hospitality pipeline. Red Sea Phase 1 infrastructure cleared the way for 8,000 hotel rooms across 22 islands, 50 hotels, and 6 inland sites in the mountainous and desert regions.

- Regulatory Reform: New property laws enable foreign ownership and reduce transaction costs, attracting international capital and expertise.

- Infrastructure Investment: The National Industrial Development and Logistics Program plans 59 logistics centers expanding warehouse inventory by 2030.

- Corporate Relocation: Regional headquarters requirements drive Grade A office demand, with Riyadh achieving 98% occupancy rates in premium districts.

- Affordable Housing Programs: Government initiatives like Sakani provide subsidized financing and expedited approvals to boost homeownership.

Market Restraints

Construction cost inflation pressures project feasibility and developer margins: Rising material prices, labor shortages, and concurrent mega-project demand create significant cost pressures for developers. International contractors now require escalation clauses adding contingencies to project packages, while smaller contractors have exited fixed-price contracts amid commodity price volatility.

Supply-demand imbalances create housing shortages in key urban markets: Despite record housing delivery, demand significantly outpaces supply in major cities. Current development plans fall short of requirements, particularly for mid-income households, creating affordability challenges and limiting market accessibility for first-time buyers.

Market concentration risks from mega-project resource allocation: Large-scale government developments can crowd out private developers lacking similar land pipelines and utility access. The special economic zone model, while accelerating approvals, may create competitive disadvantages for traditional real estate companies with limited government partnerships.

Saudi Arabia Real Estate Market Segmentation Analysis

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Property Type | Residential Real Estate | 60.5% | 2025 |

| Region | Northern and Central Region | 35.0% | 2025 |

Property Type Insights

Access the comprehensive market breakdown Request Sample

Residential Real Estate - 60.5% market share (2025) | Leading Property Type

The residential sector dominates through strong government support and demographic momentum with strong homeownership. In November 2025, Saudi municipalities announced agreements to construct 100,000 houses through Chinese partnerships by 2030, addressing critical supply shortages in major urban centers.

Commercial real estate expansion accelerates through Vision 2030's business hub development, with Grade A office supply reaching 6.4 million sqm in Riyadh and financial services sector growth of 5.3% between 2023 and 2024. King Abdullah Financial District achieved high pre-leasing rates, reflecting sustained corporate demand and international headquarters relocations.

|

Segment Breakdown Residential Real Estate (60.5%) - Apartments · Villas · Others · Commercial Real Estate - Offices · Retail · Hospitality · Others |

Regional Insights

Northern and Central Region - 35.0% market share (2025) | Leading Region

Northern and Central Region:

NEOM's development along the northwestern Red Sea coast represents the region's transformation into a futuristic urban center. The region attracts significant real estate investment and international attention.

|

Metric

|

Details

|

|---|---|

|

Market Share in 2025

|

35.0%

|

|

Key States

|

Tabuk, NEOM, Qurayyat |

|

Major Growth Drivers

|

NEOM mega-project, sustainable development, technology integration |

|

Outlook

|

High-potential emerging market |

|

Regional Breakdown Northern and Central Region (35.0%) · Western Region · Eastern Region · Southern Region |

Western Region:

Jeddah's strategic Red Sea location drives tourism and trade-focused development, with total residential stock reaching 899,000 units and 8,000 new units completed in Q3 2024. The Red Sea Project and giga-project developments position the region as a luxury hospitality and waterfront living destination.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Jeddah, Makkah, Madinah |

|

Major Growth Drivers

|

Red Sea tourism, religious tourism, coastal development |

|

Outlook

|

Strong tourism-driven growth potential |

Eastern Region:

The Dammam Metropolitan Area is driven by industrial and logistics expansion. Enhanced port infrastructure and cargo throughput growth support warehousing and commercial property demand across the region.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Dammam, Dhahran, Khobar |

|

Major Growth Drivers

|

Industrial development, logistics hubs, port expansion |

|

Outlook

|

Fastest regional growth trajectory |

Southern Region:

Development focuses on creating new urban centers and improving infrastructure connectivity. The region benefits from proximity to NEOM developments and emerging tourism initiatives, though it represents a smaller portion of current real estate activity compared to established metropolitan areas.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Abha, Najran, Jazan |

|

Major Growth Drivers

|

Regional connectivity, infrastructure development, tourism potential |

|

Outlook

|

Steady development growth |

Market Outlook 2026-2034

What is the future outlook of the Saudi Arabia real estate market?

The Saudi Arabia real estate market is expected to sustain steady revenue growth through 2034.

Vision 2030's strategic implementation creates sustained momentum across all property segments, with mega-projects providing continuous development pipelines and foreign ownership liberalization attracting international capital. The market benefits from demographic tailwinds, government support, and economic diversification initiatives that position Saudi Arabia real estate market trends for robust expansion through the forecast period and beyond.

Saudi Arabia Real Estate Market — Leading Key Players

Leading companies drive market development through diverse project portfolios, strategic partnerships, and innovation in sustainable construction. These players leverage government initiatives and Vision 2030 opportunities to expand across residential, commercial, and mixed-use developments throughout the Kingdom.

| Company | Leading Brands | Highlights |

|---|---|---|

| Abdul Latif Jameel | Abdul Latif Jameel Real Estate | Expanded Jeddah residential portfolio |

| Dar Al Arkan | Shams Ar Riyadh | $1.2 billion Jeddah land transaction; Branded residence development through Dar Global |

| Jenan Real Estate Company | Several projects include Laguna Villa, Dana Palaces, Khobar Views, Villaggio, Khobar Gardens, Dana Bay, Dana Beach Resort, Loopagoon Water Park, Life Square, and Dana Beach Walk | Housing development with various projects like Life Square, Laguna Villas, Dana Places, and more. |

Some of the other key players existing in the Saudi Arabia real estate market are ROSHN Group, Saudi Real Estate Company (Al Akaria), Jabal Omar Development Company, EMAAR, ETC.

Latest Development & News

- In January 2026, Saudi Arabia reached a significant milestone in its property sector with the introduction of the Real Estate Excellence Award 2025 (REA25). Launched in conjunction with the Real Estate Future Forum 2026 in Riyadh, the inaugural REA shifts industry recognition from mere project scale and ambition to tangible execution, accountability, and long-term outcomes.

- In October 2025, the National Housing Company (NHC) entered into agreements and memoranda of understanding with several leading Chinese firms as part of its strategy to develop 100,000 Saudi-Chinese housing units by 2030. The collaboration includes two framework agreements for the construction of more than 24,000 residential units. The partnerships focus on strengthening supply chains and advancing the localization of construction industries through digital solutions provided via NHC’s SupplyPro platform.

Saudi Arabia Real Estate Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Property Types Covered |

|

| Regions Covered | Northern and Central Region, Western Region, Eastern Region, Southern Region |

| Companies Covered | Abdul Latif Jameel, Dar Ar Alkan, Emaar, Jabal Omar Development Company, Jenan Real Estate Company, Kingdom Holdings Company, SEDCO Development (SEDCO Holding), etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Saudi Arabia real estate market from 2020-2034.

- The Saudi Arabia real estate market research report provides the latest information on the market drivers, challenges, and opportunities in the regional market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Saudi Arabia real estate industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Saudi Arabia Real Estate Market Report

The Saudi Arabia real estate market was valued at USD 77.2 Billion in 2025.

The Saudi Arabia real estate market is anticipated to reach a value of USD 141.6 Billion by 2034.

Residential real estate dominates the market with a share of 60.5%, driven by government housing initiatives, population growth, and the housing program supporting families through subsidized financing.

Some of the major players in the Saudi Arabia real estate market include Abdul Latif Jameel, Dar Al Arkan, Jenan Real Estate Company, etc.

Key trends include PropTech integration through platforms analyzing satellite data, smart city development with AI-powered urban planning, and blockchain-based property transactions. Sustainable construction standards and mixed-use development models are increasingly prevalent across major projects.

Northern and Central Region currently leads the Saudi Arabia real estate market, accounting for a share of 35.0%. The capital benefits from Vision 2030's strategic initiatives, mandatory corporate relocations, and concentrated infrastructure investments.

Growth drivers include Vision 2030's economic diversification creating investment opportunities, population expansion generating housing demand, foreign ownership liberalization attracting international capital, and government programs supporting affordable housing development. Tourism expansion and corporate relocation mandates further amplify demand.

Key challenges include construction cost inflation pressuring project margins, supply-demand imbalances creating housing shortages in major cities, and mega-project resource concentration potentially crowding out smaller developers. Affordability constraints affect first-time buyers despite government support programs.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)