Saudi Arabia Retail Market Size, Share, Trends and Forecast by Product, Distribution Channel, and Region, 2026-2034

Saudi Arabia Retail Market Size and Share:

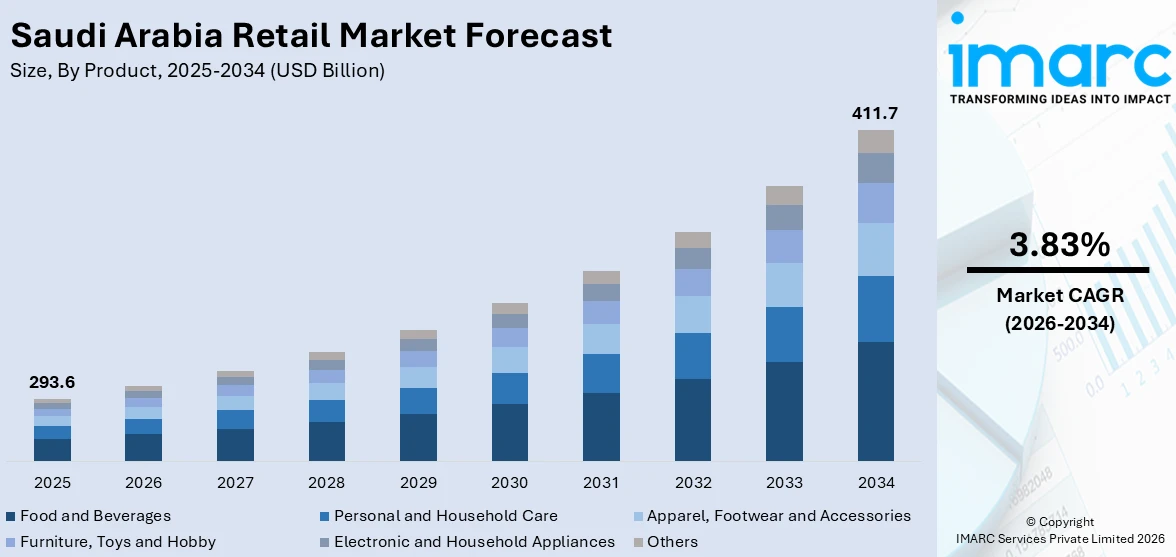

The Saudi Arabia retail market size was valued at USD 293.6 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 411.7 Billion by 2034, exhibiting a CAGR of 3.83% during 2026-2034. Northern and Central currently dominates the market in 2025. The growing focus on creating immersive and experiential shopping environments, combined with the rising consumer preferences for personalized shopping experiences, are driving the market. Additionally, the increasing investments in state-of-the-art distribution centers, alongside the rapid development of last-mile delivery solutions, are further expanding the Saudi Arabia retail market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 293.6 Billion |

| Market Forecast in 2034 | USD 411.7 Billion |

| Market Growth Rate 2026-2034 | 3.83% |

The market is primarily driven by a young, tech-savvy population with increasing disposable incomes. Over 60% of the Saudi Arabian population is under 35 years old, contributing to an average growth rate in consumer expenditure from 2022 to 2028 at 6.4% annually. This rise is fueled by an increased interest for international brands, e-commerce, and new-style retail. The diversification and digitalization push by the government is driving growth in sectors including food, electronics, and entertainment, with e-commerce projected to contribute 46% of the market by the year 2030. Amidst the setback caused by inflation, demand for high-end products continues to remain strong, causing retailers to prioritize personalization, affordability, and quick delivery as a way of addressing the shifting needs of the consumer. Government initiatives such as Vision 2030 are improving economic diversification, encouraging foreign investments, and enhancing consumer spending. The rise of digital payment solutions and smartphone penetration has accelerated online shopping growth, with platforms gaining traction. Additionally, urbanization and the expansion of mega-projects, such as NEOM and Riyadh Boulevard, are creating new retail hubs, further stimulating Saudi Arabia retail market growth.

To get more information on this market Request Sample

In addition, the growing preference for convenience and premium shopping experiences is also significantly supporting the market. The influx of expatriates and tourists, supported by relaxed visa policies, has increased demand for luxury goods and international retail chains. In 2023, Saudi Arabia's travel and tourism industry recorded an impressive GDP contribution of SAR 444.3 Billion (approximately USD 118.45 Billion), fueled by 100 million tourist visits. International visitor spending grew by 57% to SAR 227.4 Billion (approximately USD 60.62 Billion), and domestic spending grew by 21.5% to SAR 142.5 Billion (approximately USD 37.99 Billion). The tourism sector supports more than 2.5 million jobs and is increasing retail demand in food, fashion, and entertainment industries. By 2034, the sector is estimated to contribute SAR 836.1 Billion (approximately USD 223.06 Billion) to GDP, with major opportunities for retail growth alongside Saudi Arabia's growing tourism economy. The Saudi government’s focus on entertainment and tourism, including events, has enhanced footfall in malls and retail outlets. Changing consumer behavior, with a shift towards health-conscious and sustainable products, is also shaping retail trends. Furthermore, the expansion of organized retail spaces and the adoption of omnichannel strategies by retailers are enhancing customer engagement, ensuring sustained market growth in the coming years.

Saudi Arabia Retail Market Trends:

Rise of Personalized and Experiential Shopping

In Saudi Arabia, a growing preference for personalized shopping experiences is a key factor driving retail market growth. Consumers increasingly seek products that reflect their personal values and aspirations, compelling retailers to innovate. Many are focusing on immersive environments through creative store designs, interactive displays, and engagement events. Virtual reality (VR) and augmented reality (AR) tools, such as virtual showrooms and AR try-on features, are becoming mainstream, enhancing the online shopping journey by helping customers make informed purchasing decisions. According to the Saudi Arabia retail market forecast, the demand for niche offerings including modest fashion and halal food options is rising. Notably, in March 2025, Tanmiah Food Company signed an MoU with Griffith Foods to expand halal product offerings, aiming to build Saudi Arabia’s first 100% halal ingredients facility.

Technological Advancements and AI Integration

Retailers across Saudi Arabia are rapidly adopting technology and data analytics to enhance operations and customer engagement. Tools such as mobile applications, AI-driven chatbots, and predictive data insights are used to personalize recommendations, optimize inventory management, and elevate customer service. In October 2024, Gupshup, a leading Conversational AI provider, launched its services in the Kingdom, offering its domain-specific Generative AI model, ACE LLM. This AI model empowers Saudi businesses to build intelligent, Arabic-language chatbots, promoting culturally nuanced consumer interactions. Such technological integration is reshaping customer engagement strategies, allowing brands to deliver personalized, human-like conversational experiences. The emphasis on innovation through AI is enhancing shopping experiences and building stronger brand loyalty and customer trust. Thus, this is further creating a positive Saudi Arabia retail market outlook.

Expansion of Logistics Infrastructure and Omni-Channel Retailing

The development of Saudi Arabia’s logistics infrastructure is significantly enhancing the retail market. Investments in state-of-the-art distribution centers and advanced last-mile delivery solutions ensure faster, more reliable product deliveries. As a result, the logistics market in Saudi Arabia reached USD 52.7 Billion in 2024 and is projected to grow at a CAGR of 4.9% from 2025 to 2033, according to the IMARC Group. In parallel, omni-channel retailing is rapidly gaining traction, driven by consumer demand for seamless transitions between online platforms, physical stores, and mobile applications. Retailers are investing heavily in integrated systems that unify shopping experiences across all channels. This strategy not only enhances customer convenience but also yields valuable data insights, enabling highly targeted and effective marketing efforts.

Saudi Arabia Retail Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the Saudi Arabia retail market, along with forecasts at the country and regional levels from 2026-2034. The market has been categorized based on product and distribution channel.

Analysis by Product:

- Food and Beverages

- Personal and Household Care

- Apparel, Footwear and Accessories

- Furniture, Toys and Hobby

- Electronic and Household Appliances

- Others

Food and beverages stand as the largest component in 2025, holding around 33.7% of the market, driven by population growth, urbanization, and changing dietary preferences. As urban centers expand, consumers are becoming more inclined toward convenience foods and international dining options. Additionally, as the younger generation embraces diverse eating habits, the demand for healthier and more sustainable food choices rises. Retailers are responding to these trends by offering a broader range of products, including organic and plant-based alternatives, meeting the needs of a modern, health-conscious consumer base. This shift is also fostering innovation in the food sector, with new brands and products constantly emerging to cater to evolving consumer expectations.

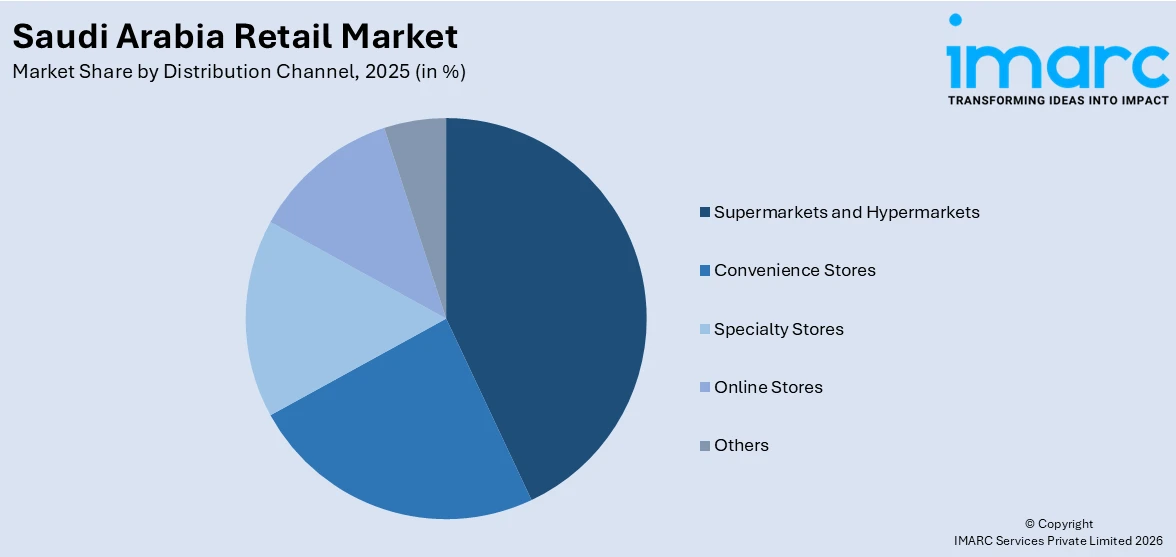

Analysis by Distribution Channel:

Access the comprehensive market breakdown Request Sample

- Supermarkets and Hypermarkets

- Convenience Stores

- Specialty Stores

- Online Stores

- Others

Supermarkets and hypermarkets lead the market, accounting for a significant share of food, groceries, and household goods sales. Leading chains such as Panda, Carrefour, and Lulu Hypermarket benefit from consumer preference for one-stop shopping, bulk purchases, and competitive pricing. These stores are expanding their footprint in urban and suburban areas, supported by government investments in retail infrastructure. Additionally, they are enhancing customer experience through loyalty programs, in-store promotions, and diversified product offerings. The integration of online ordering with in-store pickup (click-and-collect) is further improving their appeal. With Saudi consumers increasingly valuing convenience and variety, supermarkets and hypermarkets continue to play a pivotal role in the Kingdom’s retail ecosystem, particularly in the food and beverage segment.

Regional Analysis:

- Northern and Central Region

- Western Region

- Eastern Region

- Southern Region

The Northern and Central Region, particularly Riyadh, represents the largest retail hub in Saudi Arabia, accounting for a dominant share of the country's retail sales. As the capital and most populous city, Riyadh boasts high consumer spending power, supported by a concentration of affluent residents, government employees, and expatriates. The region is home to mega-malls such as Riyadh Park and Granada Center, alongside luxury retail destinations catering to premium shoppers. Rapid urbanization, infrastructure development, and Vision 2030 projects, such as Qiddiya and King Abdullah Financial District, are further stimulating retail growth. Additionally, the region benefits from strong logistics networks, making it a key distribution center for both local and international retailers. With rising demand for modern retail formats and e-commerce, the Northern and Central Region remains the most dynamic and competitive market in the Kingdom.

Competitive Landscape:

The Saudi retail market features intense competition among key players adopting diverse strategies to strengthen their market position. Major hypermarket and supermarket chains are expanding their physical footprints while enhancing digital capabilities through omnichannel integration, offering click-and-collect and same-day delivery services. E-commerce platforms are aggressively investing in logistics, AI-driven personalization, and localized payment solutions to capture the growing online shopper base. Specialty retailers are differentiating through exclusive brand partnerships, VIP loyalty programs, and experiential store formats. Regional players are leveraging local market knowledge and government incentives to compete with international brands. Across segments, competitors are focusing on price optimization, private label expansion, and sustainability initiatives to appeal to cost-conscious and environmentally aware consumers. The market is also seeing increased mergers and partnerships as players seek to consolidate their positions in this rapidly changing retail landscape.

The report provides a comprehensive analysis of the competitive landscape in the Saudi Arabia retail market with detailed profiles of all major companies.

Latest News and Developments:

- March 2025: The Public Investment Fund (PIF) of Saudi Arabia launched Al Waha Duty-Free Company, the first Saudi-owned customs-free business in the Kingdom. The company intends to become an industry leader in travel retailing, rerouting a larger percentage of travel expenditures toward the Saudi economy. Moreover, Al Waha also plans to build luxury retail establishments in selected locations across the Kingdom, providing a wide variety of products, including premium Saudi merchandise.

- February 2025: Aster Pharmacy, the retail division of Aster DM Healthcare, opened for business in Saudi Arabia, launching 15 locations throughout Riyadh, notably its flagship outlet at Trio Plaza.

- December 2024: Zid launched ‘Total Commerce’, an integrated platform that reportedly combines multiple facets of modern retail into a single platform, allowing businesses to sell their products through a variety of channels and easily deliver goods to consumers.

- December 2024: Cenomi Retail, the master licensee of Subway in Saudi Arabia, launched 14 new Subway locations across the Kingdom in a single day. These 14 locations were strategically opened as part of the company’s efforts to improve its standing in the rapidly growing food and beverage sector in Saudi Arabia.

- December 2024: Apple revealed plans for retail expansion in Saudi Arabia, beginning with the opening of its online Apple Store in 2025. The company also plans to open numerous premier Apple Store outlets in Saudi Arabia beginning in 2026.

Saudi Arabia Retail Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Products Covered | Food and Beverages, Personal and Household Care, Apparel, Footwear and Accessories, Furniture, Toys and Hobby, Electronic and Household Appliances, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Convenience Stores, Specialty Stores, Online Stores, Others |

| Regions Covered | Northern and Central Region, Western Region, Eastern Region, Southern Region |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Saudi Arabia retail market from 2020-2034.

- The Saudi Arabia retail market research report provides the latest information on the market drivers, challenges, and opportunities in the regional market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Saudi Arabia retail industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Saudi Arabia Retail Market Report

The Saudi Arabia retail market was valued at USD 293.6 Billion in 2025.

The growth of the Saudi Arabia retail market is driven by factors such as a young, tech-savvy population, rising disposable income, increasing demand for international brands, e-commerce growth, government initiatives like Vision 2030, and the rise of experiential shopping environments and personalized experiences.

The Saudi Arabia retail market is projected to exhibit a CAGR of 3.83% during 2026-2034, reaching a value of USD 411.7 Billion by 2034.

The largest segment in the Saudi Arabia retail market in 2024 was the food and beverages sector, accounting for around 33.7% of the market share.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)