Saudi Arabia Silica Sand Market Size, Share, Trends and Forecast by End Use and Region, 2026-2034

Saudi Arabia Silica Sand Market Size, Share, Trends & Forecast (2026-2034)

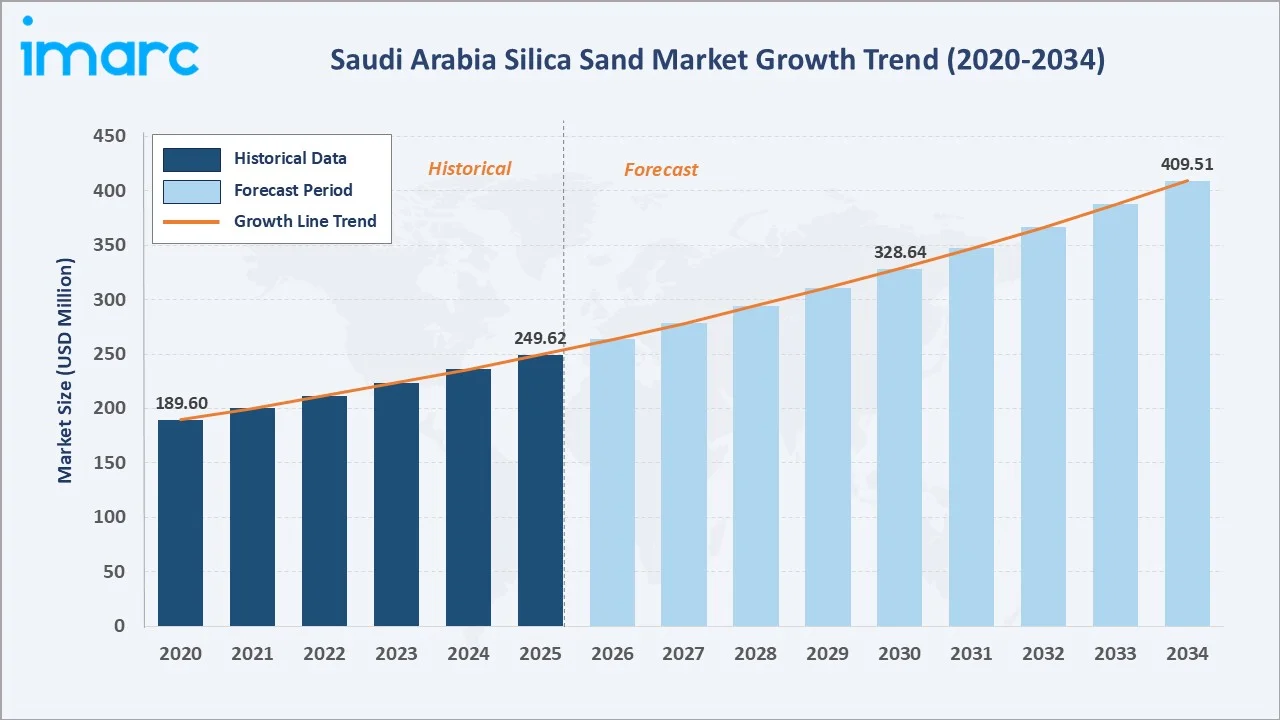

The Saudi Arabia silica sand market size reached USD 249.62 Million in 2025 and is projected to reach USD 409.51 Million by 2034, exhibiting a CAGR of 5.65% during 2026-2034. Vision 2030 infrastructure expansion, growing glass manufacturing, and hydraulic fracturing demand are the primary forces driving market growth.

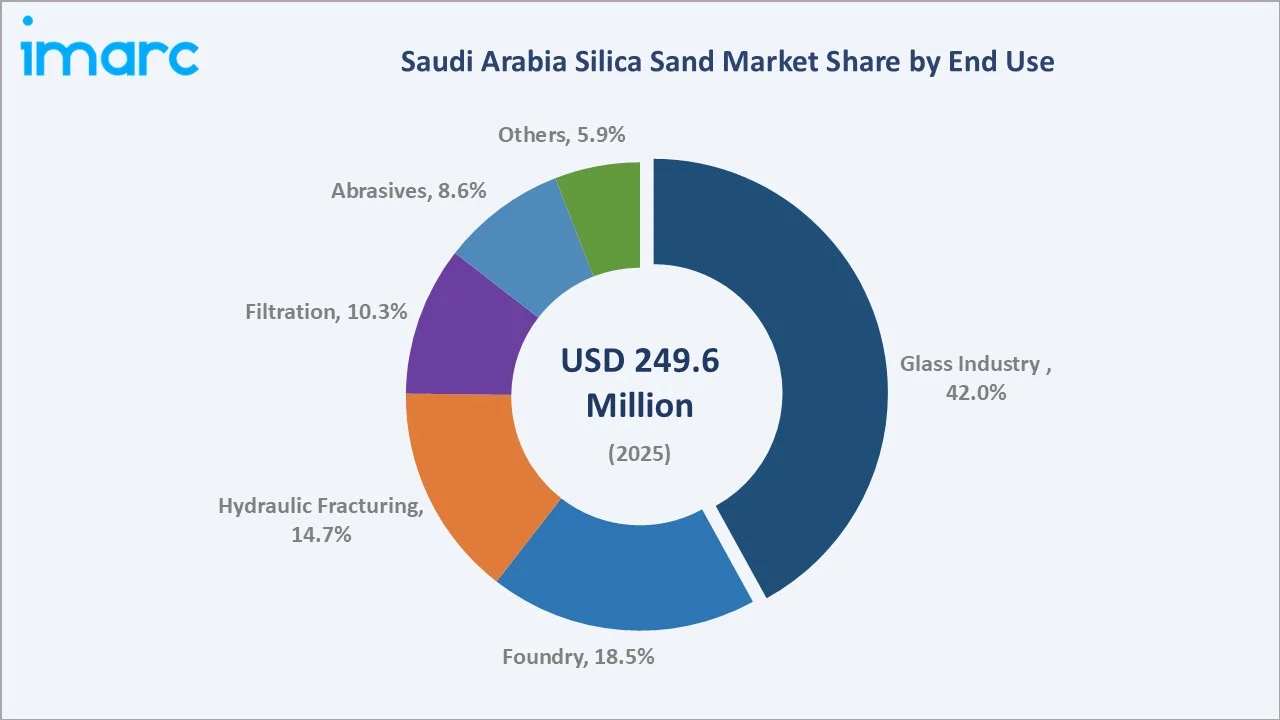

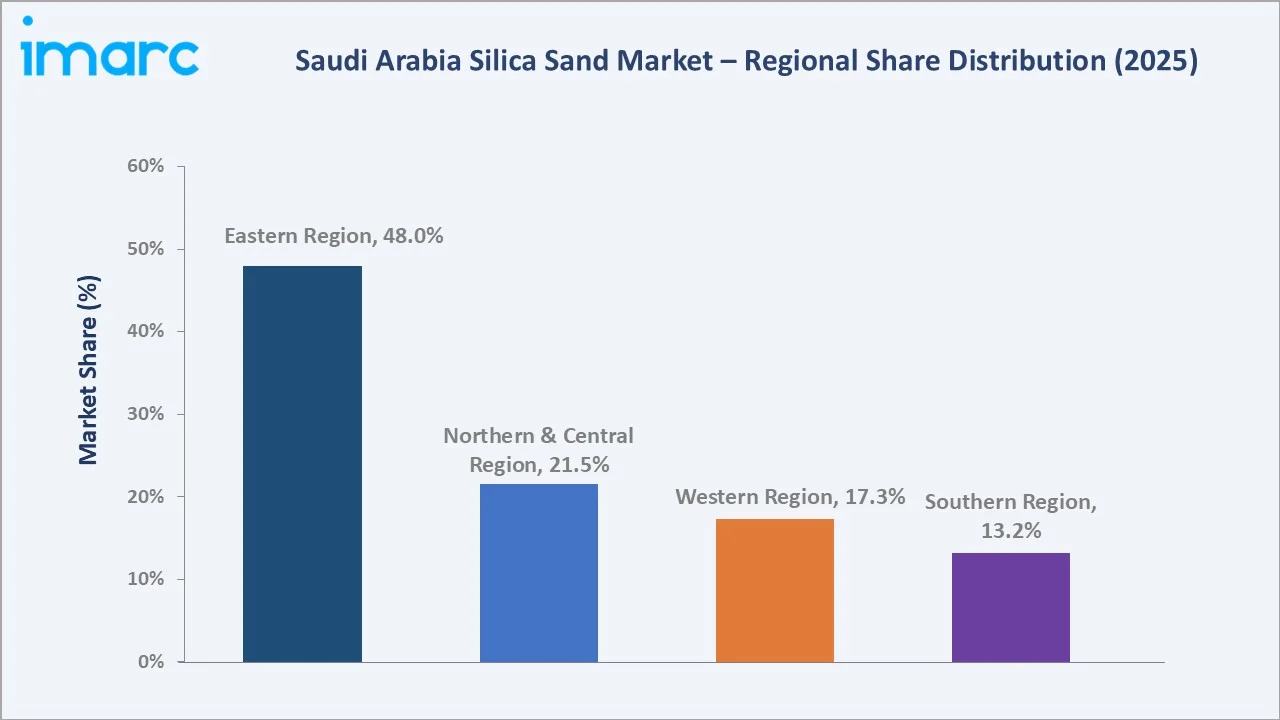

The glass industry dominates the end-use mix at 42.0% in 2025, while the Eastern Region commands a dominant 48.0% regional share in 2025, driven by oil and gas activities and proximity to major silica sand deposits across the Kingdom.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 249.62 Million |

|

Forecast Market Size (2034) |

USD 409.51 Million |

|

CAGR (2026-2034) |

5.65% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest End Use |

Glass Industry (42.0% share, 2025) |

|

Second Largest End Use |

Foundry (18.5% share, 2025) |

|

Leading Region |

Eastern Region (48.0% share, 2025) |

|

Second Region |

Northern & Central Region (21.5% share, 2025) |

The growth trajectory from 2020 through 2034, with historical expansion to USD 249.62 Million in 2025, reflects infrastructure-driven demand. The forecast to USD 409.51 Million captures accelerating construction, glass manufacturing, and unconventional gas extraction investment.

To get more information on this market, Request Sample

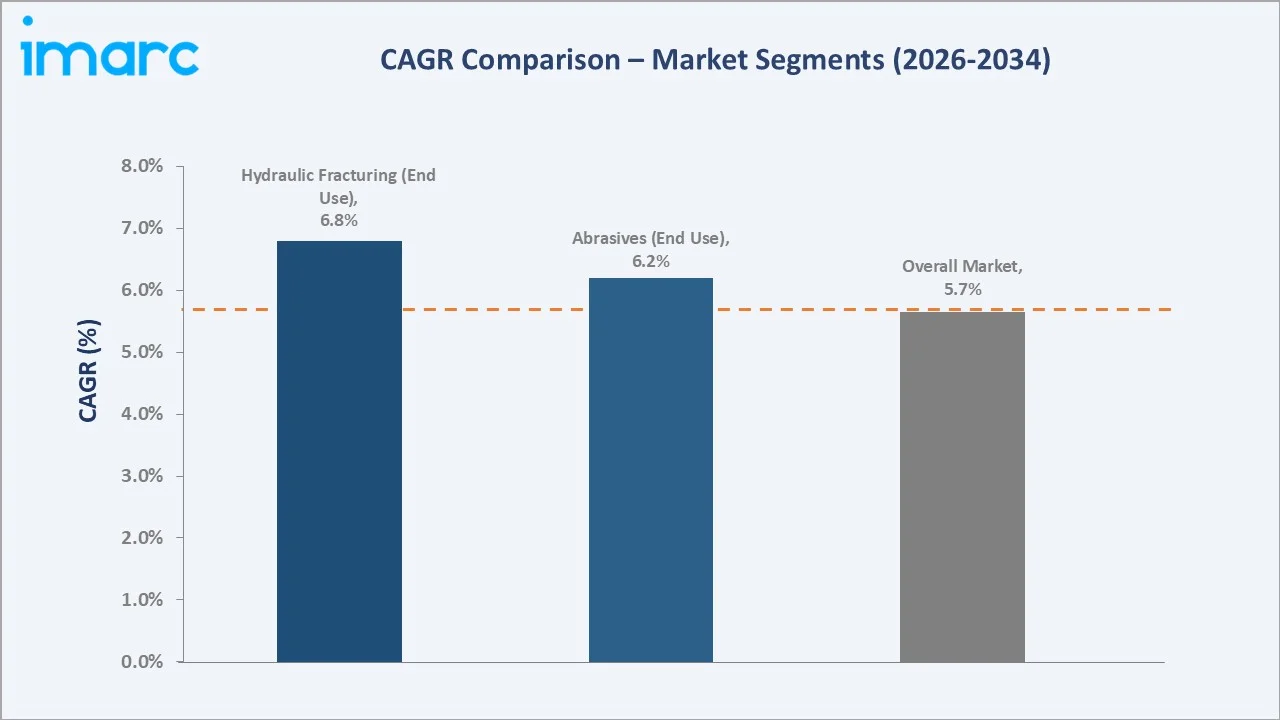

The CAGR trajectories across key end-use sub-segments, with Hydraulic Fracturing at ~6.80% CAGR and Abrasives at ~6.20% CAGR, are the fastest-growing categories within the Saudi Arabia silica sand industry analysis through 2034.

Executive Summary

The Saudi Arabia silica sand market is on a sustained growth trajectory from USD 249.62 Million in 2025 to USD 409.51 Million by 2034. Silica sand, a critical industrial mineral with high SiO2 purity, is essential across glass manufacturing, foundry casting, hydraulic fracturing, water filtration, and abrasive applications.

The glass industry dominates end-use at 42.0% in 2025, driven by expanding flat glass and container glass production for construction and automotive sectors. Foundry applications (18.5%) serve the growing metal casting industry. Hydraulic Fracturing (14.7%) benefits from Aramco's unconventional gas development targeting the Jafurah field, the Middle East's largest shale gas reserve.

The Eastern Region commands 48.0% in 2025, reflecting its concentration of oil and gas activities, industrial manufacturing, and proximity to silica sand deposits. Northern and Central Region (21.5%) and Western Region (17.3%) follow as significant contributors to overall market demand.

Key Market Insights

|

Insight |

Data |

|

Largest End Use |

Glass Industry – 42.0% share (2025) |

|

Second Largest End Use |

Foundry – 18.5% share (2025) |

|

Leading Region |

Eastern Region – 48.0% revenue share (2025) |

|

Second Region |

Northern & Central Region – 21.5% share (2025) |

|

Top Companies |

Muadinoon, Alsalam Almasi, Delmon, Al-Rasheed Co., Adwan Chemical Industries Co. Ltd. |

Key Analytical Observations Supporting the Above Data:

- Glass Industry, at 42.0% in 2025, dominates because Saudi Arabia's construction boom and automotive sector create non-discretionary demand for flat glass, container glass, and specialty glass requiring high-purity silica sand as the primary raw material input.

- Foundry applications, at 18.5% in 2025, reflect Saudi Arabia's expanding metal casting sector, driven by industrial diversification under Vision 2030 and growing domestic manufacturing capacity across Riyadh, Eastern Province, and Makkah.

- Eastern Region's 48.0% dominance reflects the structural concentration of Saudi Arabia's oil and gas, petrochemical, and industrial manufacturing base alongside abundant silica sand reserves.

- Hydraulic Fracturing at 14.7% is set for strong growth as Aramco's USD 25 billion unconventional gas investment program accelerates frac sand consumption for Jafurah and other unconventional reserves through 2034.

Saudi Arabia Silica Sand Market Overview

Silica sand is a granular material comprising silicon dioxide (SiO2) at purity levels exceeding 95%, with less than 0.6% iron oxide content in premium grades. Its exceptional properties including high melting point, chemical stability, low thermal expansion, and mechanical hardness make it indispensable across multiple industries.

Saudi Arabia holds over 1 billion tons of high-purity silica sand, with purity levels above 98%, placing it among the most valuable reserves in the world. The Kingdom's ecosystem integrates domestic miners, processing facilities, glass manufacturers, oil field services, water treatment utilities, and end-use industrial consumers.

Market Dynamics

To evaluate market opportunities, Request Sample

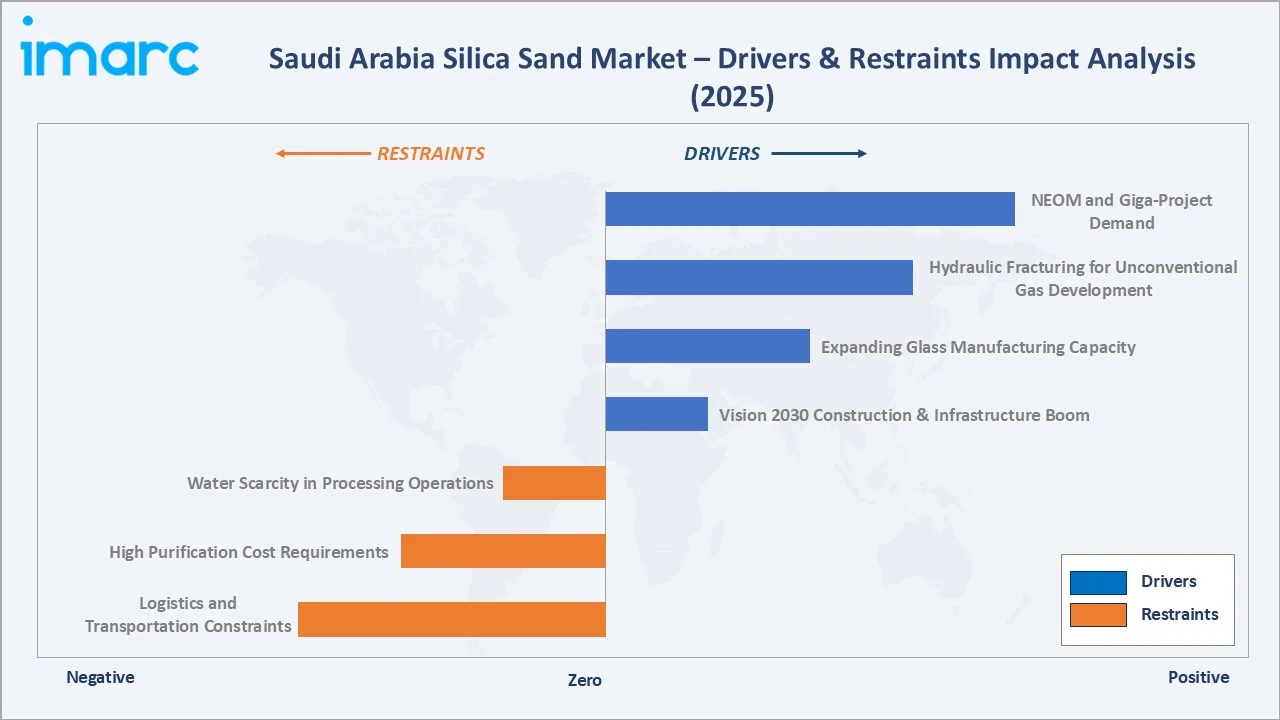

Market Drivers

- Vision 2030 Construction and Infrastructure Boom: Saudi Arabia's USD 1 trillion infrastructure pipeline significantly increases demand across construction materials, glass production for mega-projects such as NEOM, and industrial facility construction.

- Expanding Glass Manufacturing Capacity: Zoujaj Glass received approval in November 2023 to set up a sixth production line in Riyadh, increasing annual capacity by 25,000 MT. Domestic glass manufacturers are expanding their capacities to reduce import dependency, thereby directly boosting silica sand procurement volumes.

- Hydraulic Fracturing for Unconventional Gas: Aramco awarded USD 25 billion in contracts in June 2024 to expand upstream unconventional gas production, targeting 60% output increase. Jafurah shale gas field with 229 trillion cubic feet reserves drives substantial frac sand demand growth through 2034.

Market Restraints

- Logistics and Transportation Constraints: Saudi Arabia's vast geography creates distribution challenges from mining sites in Eastern and Northern regions to manufacturing facilities and construction projects across the Kingdom, increasing delivered costs for buyers in Western and Southern regions.

- High Purification Cost Requirements: Premium applications, including solar-grade silicon and high-clarity glass, require SiO2 purity above 99.5%, demanding capital-intensive processing infrastructure that limits supplier participation and elevates production costs significantly.

Market Opportunities

- NEOM and Giga-Project Demand: NEOM's construction requirements, with 20 to 40 GW of renewable energy capacity alongside extensive urban development, create enormous, sustained demand for construction-grade and specialty silica sand throughout the forecast period 2026 to 2034.

- Solar Energy Expansion: Saudi Arabia added approximately 2.1 GW of renewable power between 2022 and early 2024. Repdo plans 58.7 GW by 2030, with concentrated solar power plants using silica sand as heat transfer media, creating a growing premium application segment.

Market Challenges

- Water Scarcity in Processing Operations: Silica sand washing and classification requires significant water volumes, creating operational challenges in Saudi Arabia's water-scarce environment and increasing the cost base for domestic processing facilities that rely on wet processing technology.

- Environmental and Mining Regulatory Compliance: Increasing scrutiny over mining operations, dust emissions, and land rehabilitation in Saudi Arabia's mineral sector creates compliance cost pressures and potential project delays for silica sand producers seeking to expand capacity.

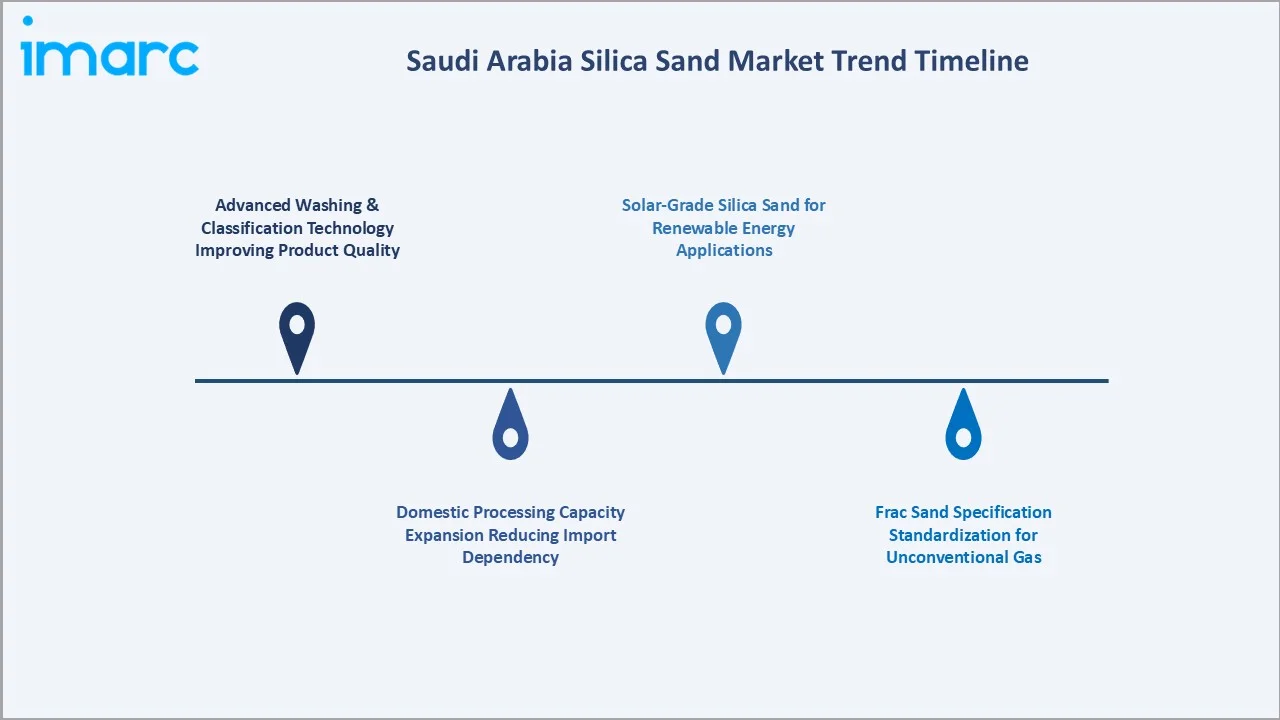

Emerging Market Trends

1. Advanced Washing and Classification Technology Improving Product Quality

Saudi producers are investing in multi-stage washing, attrition scrubbing, and hydraulic classification to meet increasing purity specifications from domestic glass manufacturers, foundries, and oil field services. Improved processing enables premium pricing and progressive import substitution across standard grade segments.

2. Domestic Processing Capacity Expansion Reducing Import Dependency

Key players, including Muadinoon and Al-Rasheed, are expanding processing capacity under the Kingdom's NIDLP industrial incentive programme. Saudi Arabia's National Industrial Development and Logistics Programme incentivizes domestic mineral processing investment, strengthening the domestic supply chain.

3. Frac Sand Specification Standardization for Unconventional Gas

Aramco's development of unconventional gas reserves is driving standardization of frac sand specifications, including grain size distribution, sphericity, and crush resistance. This creates a growing domestic frac sand market with defined API quality parameters benefiting certified producers.

4. Solar-Grade Silica Sand for Renewable Energy Applications

Saudi Arabia's renewable energy ambitions require ultra-high-purity silica for photovoltaic glass and concentrated solar power. This emerging high-value segment is attracting investment in advanced purification technologies from leading domestic and international silica producers targeting the Kingdom.

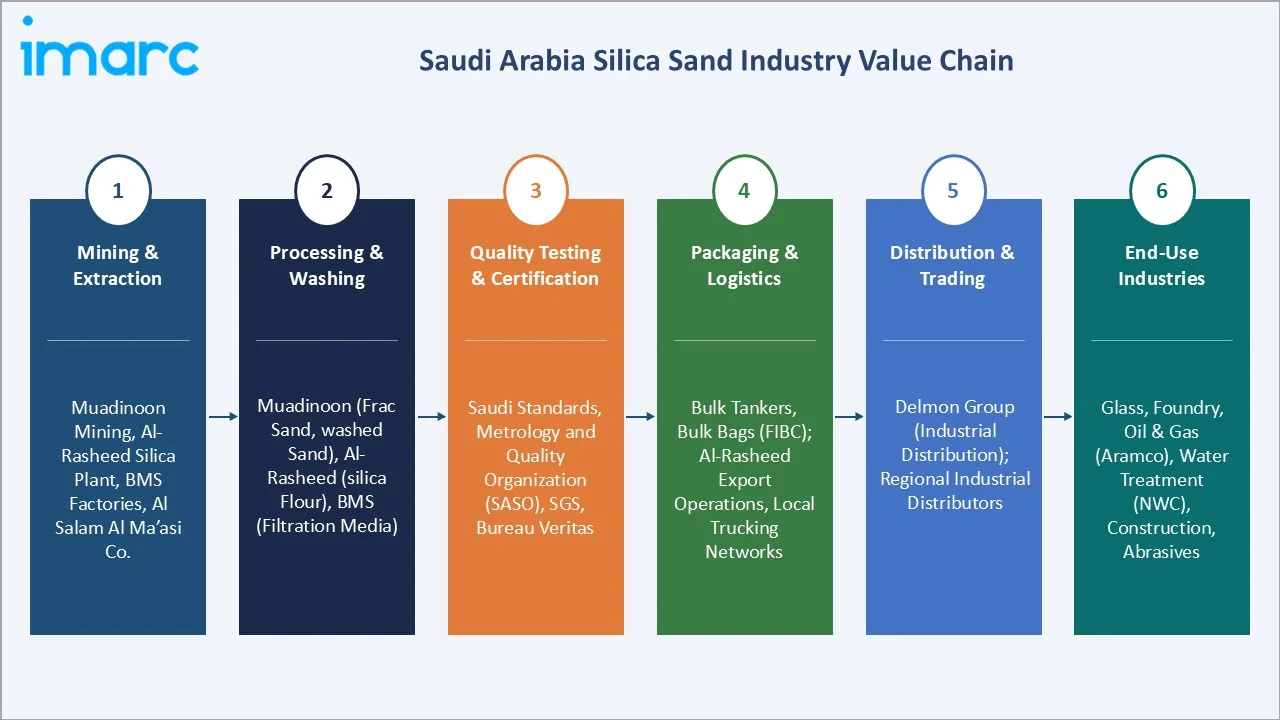

Industry Value Chain Analysis

The silica sand value chain in Saudi Arabia spans six interconnected stages, from raw material extraction through end-use industrial consumption. Each stage adds distinct technical and commercial value, with processing and purification capturing the highest margin contribution within the overall chain structure.

Processing and purification represent the critical value-add stage where raw excavated silica sand is transformed into commercially viable industrial grades. Investments in washing, classification, and purification equipment directly determine a producer's ability to serve premium applications, including glass manufacturing, frac sand, and water filtration.

Distribution and logistics form the commercial bridge between producers and end-use industries, with proximity to demand centers in the Eastern Region providing meaningful cost advantages. Leading distributors such as Delmon Group leverage broad industrial networks to supply silica sand alongside complementary industrial materials.

|

Stage |

Key Players / Examples |

|

Mining & Extraction |

Muadinoon Mining, Al-Rasheed Silica Plant, BMS Factories, Al Salam Al Ma'asi Co. |

|

Processing & Washing |

Muadinoon (frac sand, washed sand), Al-Rasheed (silica flour), BMS (filtration media) |

|

Quality Testing & Certification |

Saudi Standards, Metrology and Quality Organization (SASO), SGS, Bureau Veritas |

|

Packaging & Logistics |

Bulk tankers, bulk bags (FIBC); Al-Rasheed export operations, local trucking networks |

|

Distribution & Trading |

Delmon Group (industrial distribution); regional industrial distributors |

|

End-Use Industries |

Glass, Foundry, Oil & Gas (Aramco), Water Treatment (NWC), Construction, Abrasives |

Saudi Arabia's NIDLP programme provides direct financial support for domestic mineral processing investment, reducing the capital barrier for producers seeking to upgrade from raw extraction to higher margin processed silica supply. This is progressively shifting value capture toward domestic processing facilities.

Technology Landscape in the Saudi Arabia Silica Sand Industry

Mining and Extraction Technology

Open-pit mining using hydraulic excavators, scrapers, and conveyor systems dominates silica sand extraction in Saudi Arabia. Dry mining methods prevail given the arid climate, with pneumatic classification systems separating grain sizes post-extraction. GPS-guided equipment improves extraction efficiency and reduces waste significantly.

Processing and Purification Technology

Wet processing using scrubbing, spiral classifiers, and hydrocyclones achieves SiO2 purity above 98% for glass-grade applications. Flotation and magnetic separation technologies remove iron oxide and heavy mineral contaminants for high-purity grades. Thermal treatment achieves ultra-high purity exceeding 99.5% SiO2 for solar applications.

Frac Sand Processing Technology

Proppant coating technologies, applying resin coatings onto silica grains, enhance crush resistance and flow conductivity for deep unconventional gas well applications. Jafurah field conditions require frac sand meeting API RP 19D specifications for intermediate-strength proppant performance at elevated reservoir pressures.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

End Use |

Glass Industry |

42.0% |

2025 |

|

Region |

Eastern Region |

48.0% |

2025 |

By End Use

The glass industry commands 42.0% in 2025, owing to its fundamental role as the primary raw material for flat glass, container glass, and specialty glass production. Expanding domestic glass manufacturing under Vision 2030 industrial diversification reinforces the segment's dominant position through the forecast period.

To access detailed market analysis, Request Sample

Foundry applications at 18.5% in 2025 serve Saudi Arabia's growing metal casting industry. With 19 foundries operational in 2024, concentrated in Riyadh, Eastern Province, and Makkah, foundry-grade silica sand demand reflects ongoing industrial manufacturing expansion and Vision 2030 diversification goals.

Hydraulic fracturing at 14.7% is positioned for the strongest growth, driven by Jafurah and other unconventional gas reserves requiring API-specification frac sand as proppant. Abrasives (8.6%) serve industrial cleaning, surface preparation, and sandblasting across construction and industrial maintenance. Others (5.9%) include ceramics, sports facilities, and specialty chemical applications, which are growing as the Kingdom diversifies its industrial base under Vision 2030.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Eastern Region |

48.0% |

Aramco upstream ops; Jubail industrial complex; silica sand deposits; frac sand |

|

Northern & Central Region |

21.5% |

NEOM giga-project; Riyadh construction boom; Tayma silica mining zone |

|

Western Region |

17.3% |

Jeddah industrial growth; Red Sea development; glass and filtration demand |

|

Southern Region |

13.2% |

Emerging construction, NWC water treatment projects, infrastructure investment |

The Eastern Region's 48.0% dominance in 2025 is driven by the structural concentration of Saudi Arabia's largest industrial base. Jubail Industrial City, the world's largest industrial complex, alongside Aramco's upstream and downstream operations create multi-application silica sand demand across glass, foundry, frac sand, and filtration uses.

Northern and Central Region, with 21.5% in 2025, is experiencing the most transformative growth trajectory through 2034. Associated infrastructure development are accelerating silica sand demand for construction-grade and specialty applications, making this the fastest-growing regional market.

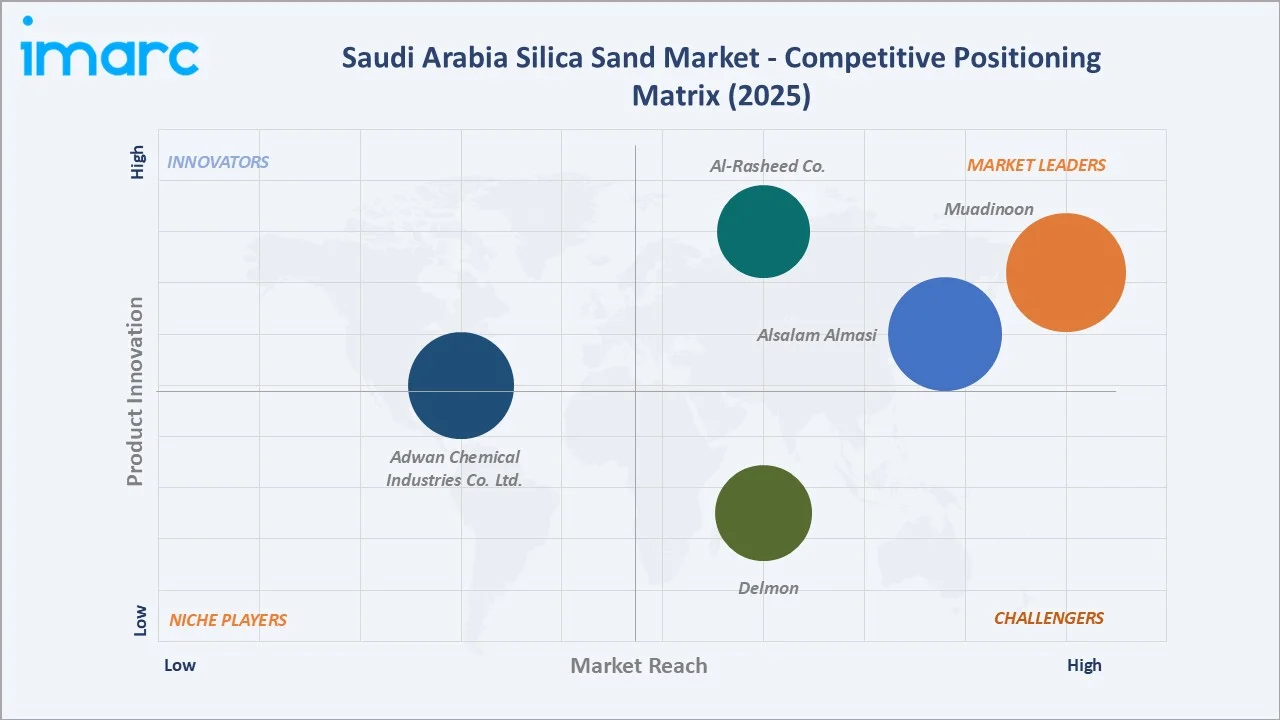

Competitive Landscape

The Saudi Arabia silica sand market is moderately concentrated, with a few domestic producers holding strong regional positions, while international specialty grade supply supplements domestic capacity. Key players invest in processing capability, quality certification, and distribution networks to capture Vision 2030-linked demand growth.

|

Company |

Key Products |

Market Position |

Strategic Focus |

|

Muadinoon |

Frac sand, washed silica sand, silica sand |

Leader |

Frac sand & oil field supply; Northwestern Region (Tabuk/Tayma) focus |

|

Alsalam Almasi |

Industrial silica sand |

Leader |

Glass & construction; multi-sector supply chain |

|

Delmon |

MINTREAT Silica sand |

Challenger |

Distribution network; multi-product industrial supply |

|

Al-Rasheed Co. |

Silica sand |

Leader |

Export-oriented; Middle East market leadership |

|

Adwan Chemical Industries Co. Ltd. |

Industrial Silica sand |

Emerging |

Specialty chemical applications: growing market |

Key players include Muadinoon, Alsalam Almasi, Delmon, Al-Rasheed Co., Adwan Chemical Industries Co. Ltd., and others.

Key Company Profiles

Muadinoon

Muadinoon headquartered in Saudi Arabia, is a leading producer of frac silica sand, washed silica sand, and silica powder serving oil and gas, foundry, glass, and water treatment sectors. The company focuses on high specification frac sand meeting API standards for unconventional gas applications.

- Product Portfolio: Frac silica sand, washed silica sand, silica powder, and specialty silica grades for oil and gas and industrial applications.

- Strategic Focus: Muadinoon's strategy centres on capturing growing frac sand demand from Saudi unconventional gas development while expanding processed silica supply for glass and filtration markets.

Al-Rasheed Co.

Al-Rasheed Co. is a leading manufacturer of silica sand, silica flour, and frac sand in the Middle East. Founded in 2000, the company serves both local markets and international exports, establishing an extensive reach across the GCC and broader regional markets with consistent product quality.

- Product Portfolio: Silica sand grades, silica flour, frac sand, and specialty silica products for glass, foundry, oil and gas, and construction applications.

- Recent Developments: In July 2024, Mohammed Hadi Al-Rasheed & Partners Company announced that it was granted a mining license for a high-purity silica deposit by the Ministry of Industry and Mineral Resources. Moreover, in January 2025, the company also launched a new silica powder production line capable of ultra-fine particles down to 10 microns.

- Strategic Focus: Al-Rasheed differentiates through consistent product quality, export market development, and a broad product range covering glass-grade through frac sand grades, positioning as a single-source supplier for multi-application customers.

Delmon

Delmon is a diversified industrial services and materials company with extensive Saudi Arabia experience covering oil and gas supplies, chemical production, and industrial raw materials. The group serves major industrial projects across the Kingdom through an established multi-product distribution network.

- Product Portfolio: MINTREAT Silica sand

- Strategic Focus: Delmon leverages its broad industrial distribution network and EPC contractor relationships to supply silica sand alongside complementary industrial materials, creating bundled supply value for large project customers across Vision 2030 mega-developments.

Market Concentration Analysis

The Saudi Arabia silica sand market is moderately concentrated at the domestic level, with a few established producers holding strong positions. Eastern Region producers, including Muadinoon and Al-Rasheed maintain significant shares in frac sand and industrial segments, while the fragmented construction-grade market accommodates smaller regional suppliers.

Consolidation in specialty silica segments including glass-grade and frac sand is more advanced than general construction-grade supply. Vision 2030 mega-project requirements are attracting investment from domestic mineral companies seeking to capture growing demand, potentially accelerating capacity expansion and market consolidation through 2030.

Investment & Growth Opportunities

Fastest-Growing Segments

Hydraulic Fracturing at approximately 6.80% CAGR through 2034 is the highest-growth end-use segment, driven by Aramco's Jafurah shale gas development requiring API-specification frac sand at growing volumes. Solar-grade ultra-high-purity silica represents an emerging premium growth opportunity aligned with Vision 2030 renewable energy targets.

Emerging Applications

Photovoltaic glass production for Saudi Arabia's 58.7 GW renewable energy target by 2030 requires high-purity silica sand, creating a growing specialist market. NEOM's construction peak demand across 2026-2030 represents the largest single volume growth opportunity in construction-grade silica during the entire forecast period.

Investment Trends

Saudi Arabia's NIDLP programme provides financial incentives for domestic mineral processing investment, making silica sand capacity expansion financially attractive. International silica companies are evaluating joint ventures with domestic producers to access Saudi reserves while contributing advanced processing technology and global quality certification credentials.

Future Market Outlook (2026-2034)

The Saudi Arabia silica sand market is forecast to expand from USD 249.62 Million in 2025 to USD 409.51 Million by 2034 at a CAGR of 5.65%, adding USD 159.89 Million in incremental annual market value. This sustained growth reflects infrastructure-linked, non-discretionary demand characteristics across all major end-use segments.

Three structural forces will shape the market most significantly through 2034. First, NEOM and giga-project construction will create peak silica sand demand between 2026 and 2030, requiring significant supply chain investment to meet construction schedule requirements. Second, Jafurah unconventional gas development will sustain frac sand demand growth beyond 2030. Third, renewable energy manufacturing creates new premium silica demand for solar and photovoltaic applications.

Domestic processing capacity will expand as producers invest to serve Vision 2030 project requirements. International quality standards including ISO and API certification will become minimum requirements for major project supply, raising barriers for smaller producers while benefiting established players with certified quality systems and track records.

Research Methodology

Primary Research

Primary research encompassed structured interviews with Saudi Arabia silica sand industry stakeholders including mine operators, processing plant managers, EPC procurement specialists, glass manufacturers, and oil field services companies. Primary data validated market sizing, end-use segment shares, and technology adoption trends.

Secondary Research

Key secondary sources include Saudi Geological Survey mineral statistics, Saudi Aramco annual reports, National Water Company project documentation, Saudi Vision 2030 progress reports, SASO industrial standards, USGS Mineral Commodity Summaries (Silica), and trade publications covering Saudi industrial and construction sectors.

Forecasting Models

Market size estimations used a combination of top-down and bottom-up forecasting models incorporating Saudi GDP growth rates, construction investment data, oil and gas production forecasts, glass manufacturing capacity plans, and historical silica sand consumption patterns. Scenario analysis accounted for macroeconomic uncertainty.

Saudi Arabia Silica Sand Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| End Uses Covered | Glass Industry, Foundry, Hydraulic Fracturing, Filtration, Abrasives, Others |

| Regions Covered | Northern and Central Region, Western Region, Eastern Region, Southern Region |

| Companies Covered | Muadinoon , Alsalam Almasi, Delmon, Al-Rasheed Co., Adwan Chemical Industries Co. Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Saudi Arabia Silica Sand Market Report

The Saudi Arabia silica sand market reached USD 249.62 Million in 2025 and is projected to reach USD 409.51 Million by 2034, growing at a CAGR of 5.65% during the forecast period 2026-2034.

Glass Industry leads with a 42.0% share in 2025, followed by Foundry at 18.5% and Hydraulic Fracturing at 14.7%, reflecting Saudi Arabia's expanding glass manufacturing capacity and oil and gas unconventional gas development programs.

The Eastern Region dominates with a 48.0% share in 2025, driven by Saudi Aramco's oil and gas operations, Jubail Industrial City, and proximity to major silica sand deposits concentrated in the Eastern and Northern regions of the Kingdom.

Key drivers include Saudi Vision 2030's USD 1 trillion infrastructure pipeline, Aramco's unconventional gas development program at Jafurah, expanding domestic glass manufacturing capacity, and the National Water Company's USD 20 billion water infrastructure investment program through 2030.

Leading companies include Muadinoon, Alsalam Almasi, Delmon, Al-Rasheed Co., Adwan Chemical Industries Co. Ltd., and others.

The Saudi Arabia silica sand market is forecast to grow at a CAGR of 5.65% during 2026-2034. Hydraulic Fracturing is the fastest-growing end-use segment at approximately 6.80% CAGR, followed by Abrasives at 6.20% CAGR, driven by Aramco's unconventional gas development programs.

Key challenges include water scarcity in processing operations due to Saudi Arabia's arid climate, increasingly strict environmental and mining regulatory compliance requirements, logistics constraints from remote mining locations, and the high capital cost of purification technology required for premium application grades.

Hydraulic fracturing is the fastest-growing application at approximately 6.80% CAGR, driven by Jafurah shale gas development and unconventional gas programs. Solar-grade ultra-high-purity silica for photovoltaic glass and renewable energy applications represents the highest-value emerging growth segment through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)