Saudi Arabia Two-Wheeler Market Size, Share, Trends and Forecast by Type, Technology, Transmission, Engine Capacity, Fuel Type, Distribution Channel, End User, and Region, 2026-2034

Saudi Arabia Two-Wheeler Market Size, Share, Trends & Forecast (2026-2034)

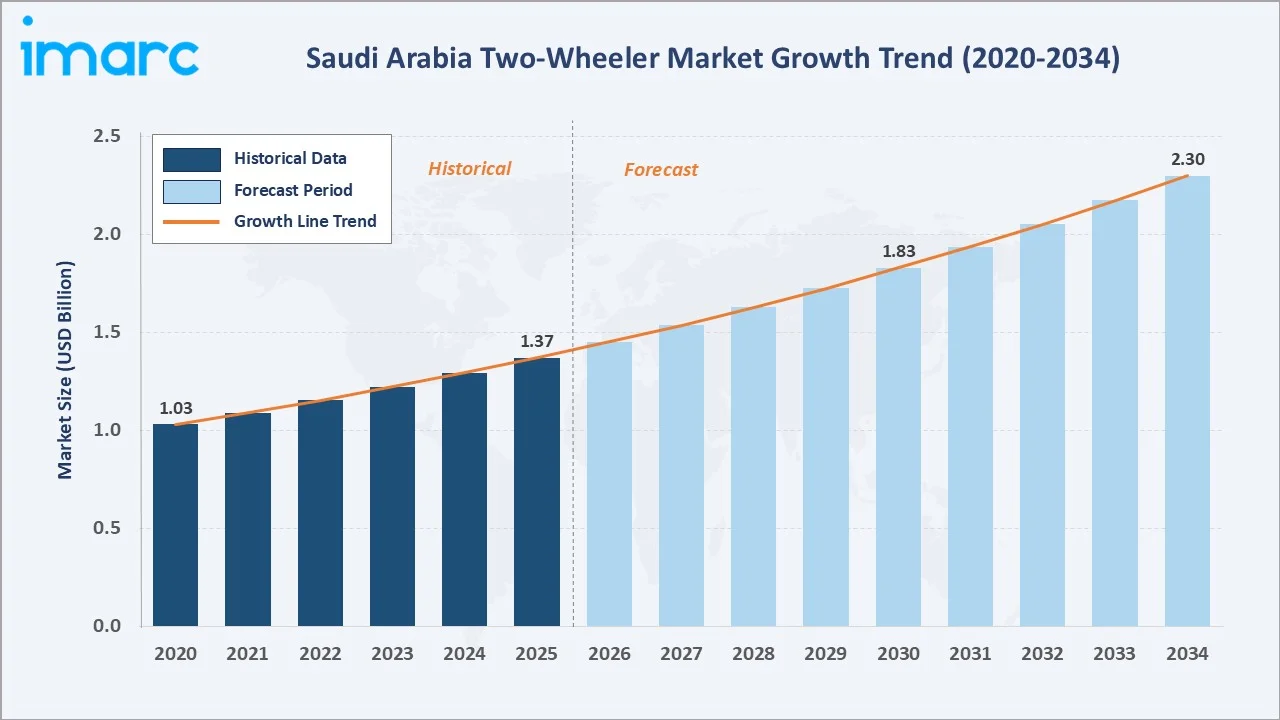

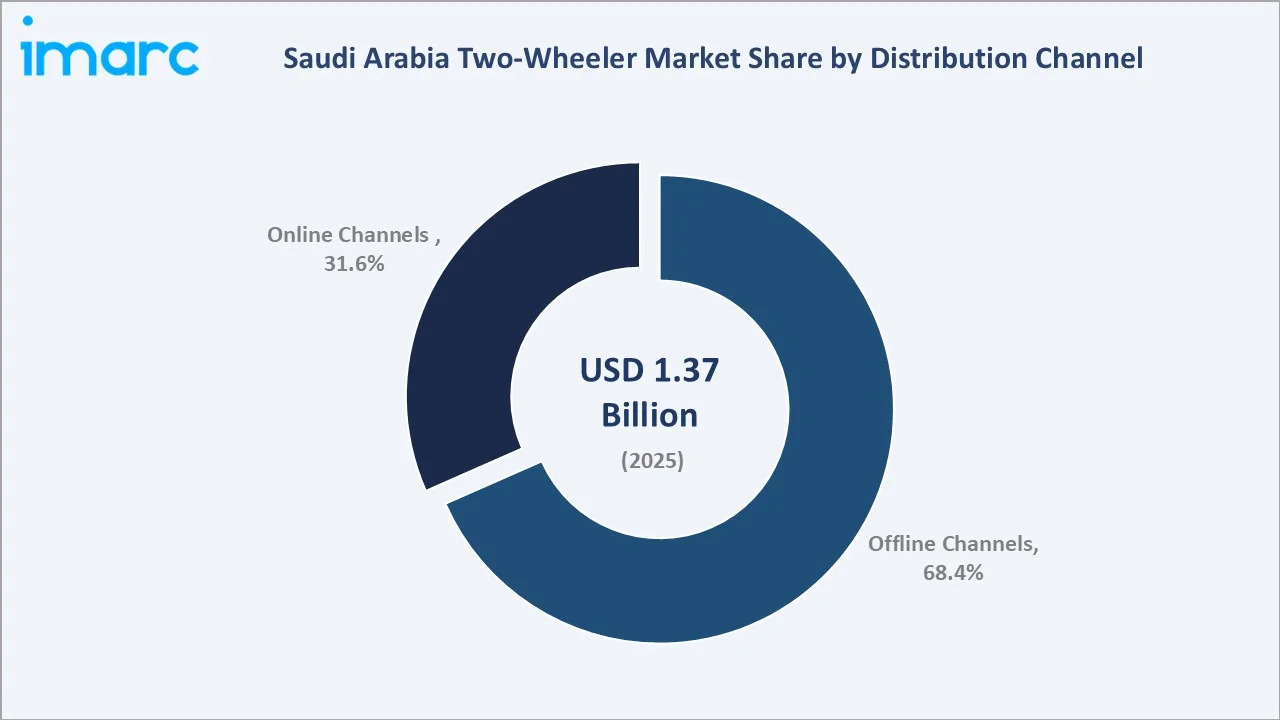

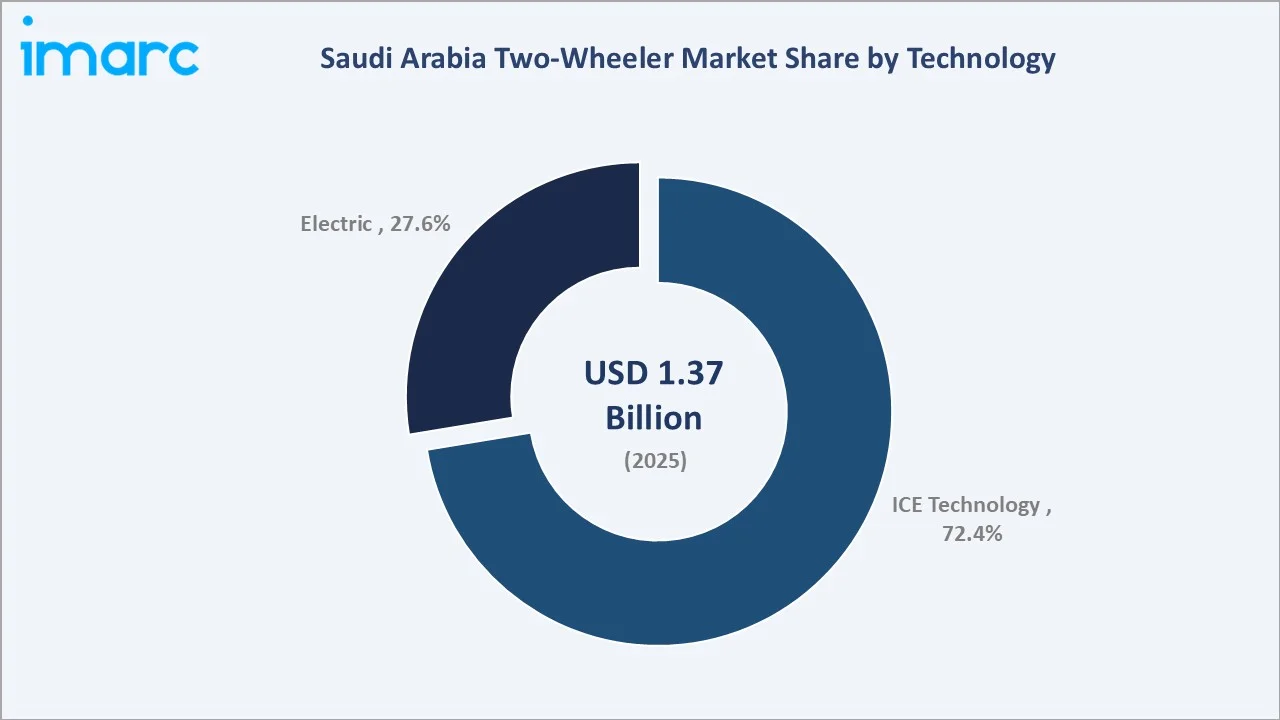

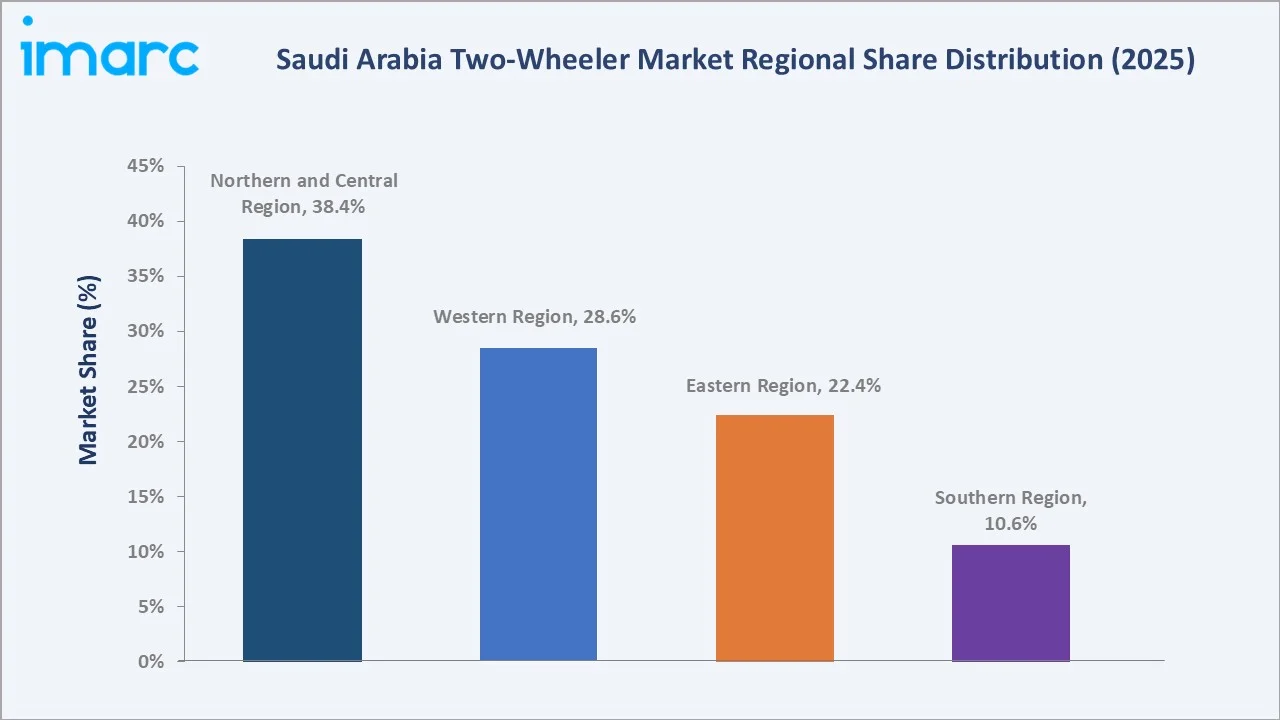

The Saudi Arabia two-wheeler market size was valued at USD 1.37 Billion in 2025 and is projected to reach USD 2.30 Billion by 2034, exhibiting a CAGR of 5.94% during the forecast period 2026-2034. The market is driven by the rapid expansion of gig-economy delivery platforms, rising urbanisation, and Vision 2030 mobility reforms. Offline Channels lead distribution at 68.4% in 2025, while ICE technology holds 72.4% of the technology mix alongside a fast-rising Electric segment at 27.6%. The Northern and Central Region leads regionally at 38.4%, driven by Riyadh’s logistics density and large expatriate workforce.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.37 Billion |

|

Forecast Market Size (2034) |

USD 2.30 Billion |

|

CAGR (2026-2034) |

5.94% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region (2025) |

Northern and Central Region (38.4%) |

|

Leading Technology (2025) |

ICE (72.4%) |

|

Leading Distribution Channel (2025) |

Offline Channels (68.4%) |

The chart below illustrates the Saudi Arabia two-wheeler market size from 2020 through 2034, contrasting the consistent historical expansion against the sustained forecast growth curve powered by delivery-economy expansion, EV policy tailwinds, and demographic-driven mobility demand.

To get more information on this market, Request Sample

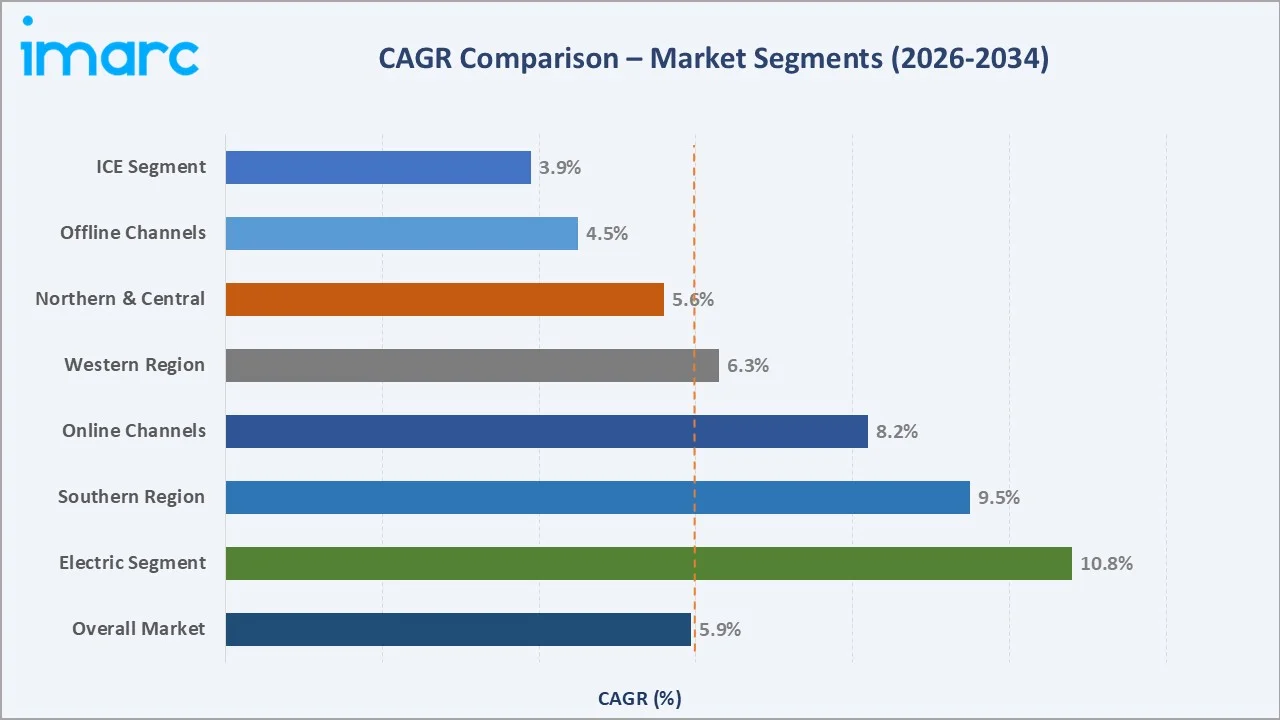

Segment-level CAGR comparisons highlighting the Electric segment and Online Channels as the two fastest-growing categories within the Saudi Arabia two-wheeler market analysis through 2034.

Executive Summary

The Saudi Arabia two-wheeler market is at a structural inflection point. Historically constrained by cultural preferences for passenger vehicles and restrictive licensing, the sector is now accelerating on the back of Vision 2030 reforms, rapid gig-economy growth, and an unprecedented wave of electric two-wheeler introductions. Valued at USD 1.37 Billion in 2025, the market is projected to reach USD 2.30 Billion by 2034 at a CAGR of 5.94%, representing approximately USD 0.93 Billion in incremental value over nine years.

Offline Channels retain a commanding 68.4% share of the distribution landscape in 2025, reflecting Saudi consumers’ preference for in-person test rides, dealership financing, and after-sales proximity. Online Channels at 31.6% are growing faster, driven by OEM direct-to-consumer platforms and Saudi Arabia’s e-commerce penetration rate exceeding 76% in 2024. On the technology axis, ICE dominates at 72.4%; however, the Electric segment’s 27.6% share positions Saudi Arabia as one of the most advanced E2W adoption markets in the MENA region, underpinned by declining battery costs and the government’s net-zero-by-2060 commitment.

The Northern and Central Region anchors demand at 38.4%, followed by the Western Region at 28.6%, the Eastern Region at 22.4%, and the Southern Region at 10.6%. Riyadh’s mega-urban logistics footprint and Jeddah’s port-city commerce are the twin growth engines sustaining near-term market expansion.

Key Market Insights

|

Insight |

Data |

|

Market Size (2025) |

USD 1.37 Billion |

|

Forecast Market Size (2034) |

USD 2.30 Billion |

|

CAGR (2026-2034) |

5.94% |

|

Leading Distribution Channel |

Offline Channels – 68.4% share (2025) |

|

Leading Technology |

ICE – 72.4% share (2025) |

|

Fastest-Growing Technology |

Electric – ~10%+ CAGR (2026-2034) |

|

Largest Region |

Northern and Central Region – 38.4% (2025) |

|

Second Region |

Western Region – 28.6% (2025) |

|

Top Companies |

Honda Motor Co., Ltd., Yamaha Motor Co., Ltd., Kawasaki Heavy Industries, Ltd., and Yadea Group Holdings Ltd |

Key Analytical Observations Supporting the Above Data:

- Offline Channels’ 68.4% dominance reflects the complex purchase journey of two-wheelers – test rides, customisation consultations, on-the-spot financing, and after-sales service agreements are dealership-centric activities that digital platforms cannot yet fully replicate in the Saudi market.

- ICE technology’s 72.4% share is sustained by Saudi Arabia’s extensive petrol fuelling network and competitive fuel pricing. However, the Saudi Green Initiative and NEOM’s zero-emission mobility mandate are structural catalysts accelerating the electric segment growth through the forecast period.

- The Northern and Central Region’s 38.4% share is attributable to Riyadh’s population exceeding 7.5 million (2024), its dense delivery-logistics ecosystem anchored by HungerStation and Jahez, and a large expatriate workforce relying on two-wheelers for affordable daily commuting.

Saudi Arabia Two-Wheeler Market Overview

Two-wheelers—including motorcycles, scooters, mopeds, and electric variants—serve both personal mobility and commercial logistics needs in Saudi Arabia. While historically dominated by motorcycles for delivery and rural utility use, the market is gradually diversifying toward urban scooters and electric two-wheelers, supported by Vision 2030 and smart-city initiatives.

Despite high overall vehicle ownership, two-wheeler penetration remains relatively low, indicating significant headroom for growth. The expansion of the gig economy—particularly food delivery and e-commerce logistics—is a key structural driver, with major platforms generating sustained demand for cost-efficient two-wheeler fleets across major cities such as Riyadh, Jeddah, and Dammam.

Macroeconomic fundamentals further support market potential, including a large and growing economy, substantial public investment under Vision 2030, and a young demographic profile that is increasingly open to alternative and flexible mobility solutions.

Market Dynamics

To evaluate market opportunities, Request Sample

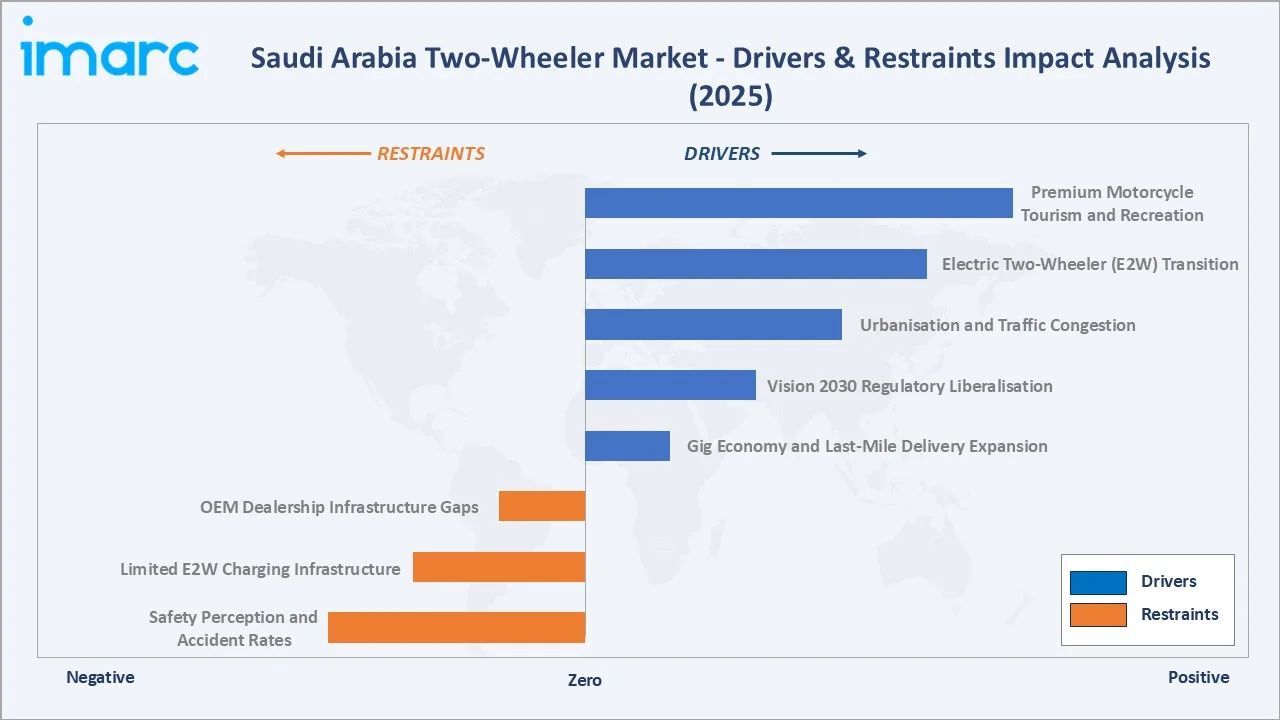

Market Drivers

- Gig Economy and Last-Mile Delivery Expansion: Rapid growth in e-commerce and food delivery is a primary demand driver, with two-wheelers widely preferred for cost-efficient and agile urban logistics.

- Vision 2030 Regulatory Liberalisation: Licensing reforms, evolving import policies, and the legalization of female riders have expanded the addressable consumer base and supported market inclusivity.

- Urbanisation and Traffic Congestion: High urbanisation and rising population density in major cities like Riyadh are increasing demand for time- and cost-efficient mobility solutions such as two-wheelers.

Market Restraints

- Safety Perception and Accident Rates: Two-wheeler accident fatality rates in the GCC remain among the highest globally, deterring adoption among safety-conscious consumers and creating liability concerns for commercial fleet operators, limiting growth velocity in the personal-use segment.

- Limited E2W Charging Infrastructure: While Saudi Aramco and NEOM are advancing EV charging networks, two-wheeler-specific charging infrastructure remains sparse outside Riyadh’s city centre, constraining electric segment adoption in tier-2 cities and rural regions where range anxiety is a critical barrier.

Market Opportunities

- Electric Two-Wheeler (E2W) Transition: Government electrification targets and declining battery costs are improving the viability of E2Ws, particularly in entry-level commuter segments.

- Premium Motorcycle Tourism and Recreation: Saudi Arabia’s scenic highway networks – including Asir Province’s mountain roads – are emerging as motorcycle-touring destinations. The premium segment above 500cc is growing at a disproportionately high CAGR, driven by leisure and adventure-riding communities in major cities.

Market Challenges

- OEM Dealership Infrastructure Gaps: Outside major cities, authorised dealership and service centre coverage remains thin. This limits consumer confidence in premium and electric two-wheeler purchases where specialist maintenance is essential, creating a structural barrier to penetration in secondary markets.

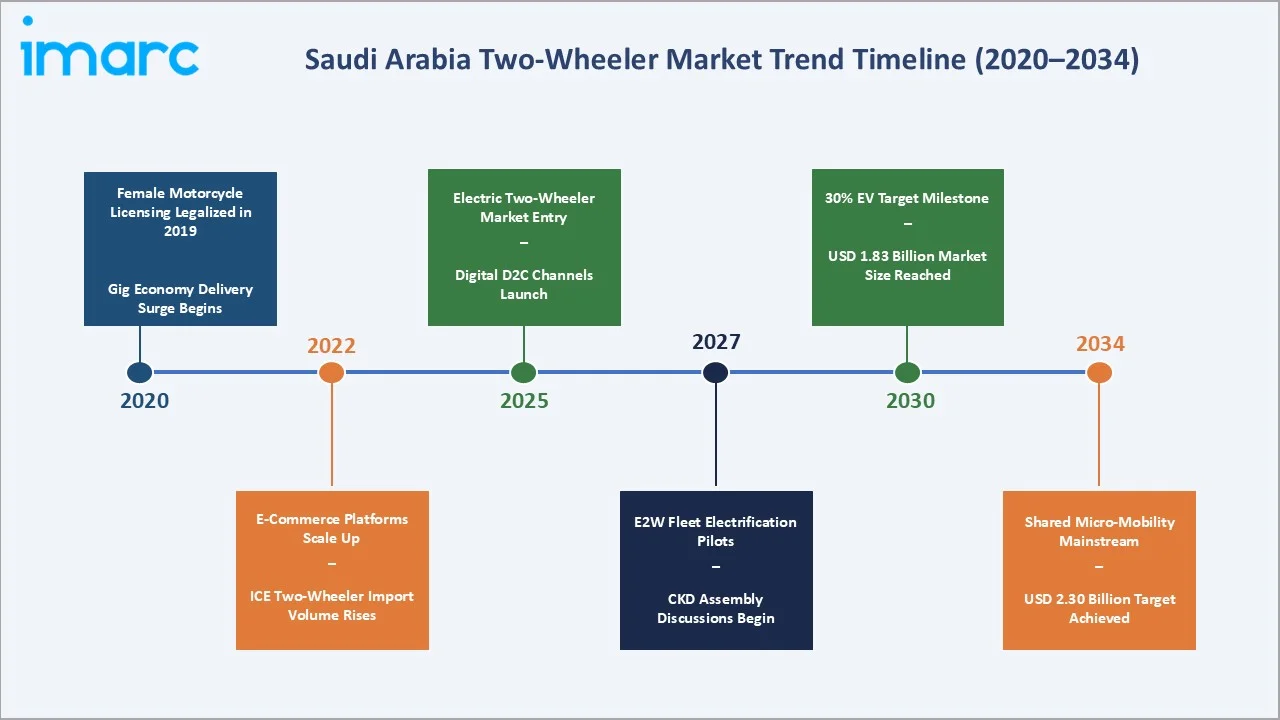

Emerging Market Trends

1. Electrification of Commercial Delivery Fleets

Delivery platforms across Saudi Arabia are increasingly piloting electric two-wheelers to reduce operating costs and align with sustainability goals. This corporate-led shift is emerging as a key driver of electrification and is expected to gradually reduce ICE dominance over the forecast period.

2. OEM Direct-to-Consumer (D2C) Digital Channels

OEMs such as Honda Motor Co., Ltd., Yamaha Motor Co., Ltd., and Chinese players, including Yadea Group Holdings Ltd. and NIU International, are expanding digital engagement through online platforms. While offline sales remain dominant, hybrid D2C models are gaining traction, supported by a growing base of digital-native consumers.

3. Shared Micro-Mobility and Smart-City Integration

Large-scale developments like NEOM and Riyadh’s smart-city initiatives are incorporating micro-mobility solutions into urban planning. Although still at an early stage, shared electric scooters are expected to emerge as a new mobility segment over the medium term.

4. Vision 2030 Localisation and CKD Assembly Ambitions

Saudi Arabia’s localization push under Vision 2030 is encouraging discussions around CKD assembly with international OEMs. Local production is expected to enhance cost competitiveness and support broader adoption of entry-level commuter segments.

5. Growing Female Ridership and New Consumer Segments

The 2019 licensing reform, enabling women to ride motorcycles, created an entirely new consumer demographic. By 2025, female registrations in the scooter and light motorcycle segments will have grown meaningfully, supported by targeted OEM marketing campaigns. This demographic trend will sustain above-average growth in scooter and automatic transmission sub-segments through 2034.

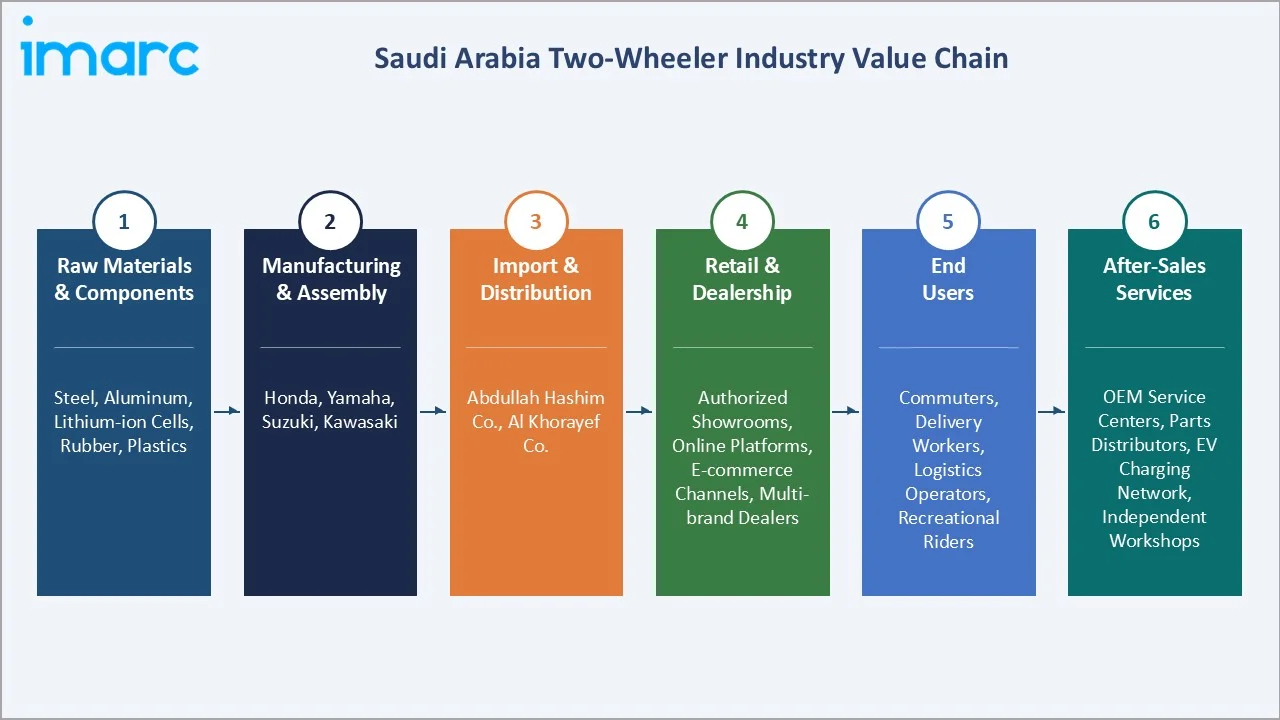

Industry Value Chain Analysis

|

Stage |

Key Activities |

Key Players / Examples |

|

Raw Materials & Components |

Steel, aluminium, rubber, battery cells, electronics procurement |

Saudi Aramco (materials), Contemporary Amperex Technology Co., Limited. (batteries), global tier-2 suppliers |

|

Manufacturing & Assembly |

Engine/motor assembly, frame fabrication, final vehicle build |

Honda Motor Co., Ltd., Yamaha Motor Co., Ltd., Kawasaki Heavy Industries, Ltd., Yadea Group Holdings Ltd., Niu International; potential Saudi CKD sites |

|

Import & Distribution |

Customs clearance, regional warehousing, fleet management |

Zakat, Tax and Customs Authority (ZATCA)-registered importers, Abdullah Hashim Co. (Honda), Al Khorayef Commercial Co. (Yamaha) |

|

Retail & Dealership |

Consumer sales, test rides, financing, after-sales service |

Authorised dealer networks in Riyadh, Jeddah, Dammam, Mecca, Medina |

|

End-User & Aftersales |

Personal commuting, commercial delivery, spare parts, and insurance |

Individual consumers, commercial fleets, and insurers |

The Saudi Arabia two-wheeler market value chain spans five integrated stages from component supply through end-consumer delivery. Each stage presents distinct competitive dynamics, investment requirements, and localisation potential under Vision 2030’s industrial development framework.

Technology Landscape

ICE Powertrain Technology: Fuel Injection and Emissions Compliance

Internal combustion engines continue to dominate the Saudi two-wheeler market, with a clear transition from carburettor systems to electronic fuel injection (EFI). Technologies such as Honda’s PGM-FI and Yamaha’s YMJET-FI enable precise air-fuel mixture control through real-time sensor feedback, improving fuel efficiency and ensuring compliance with Saudi emissions regulations aligned with Euro standards. Modern ICE models are also equipped with catalytic converters to reduce harmful emissions, while advancements such as multi-valve DOHC engine architectures allow manufacturers to achieve higher power output with improved fuel efficiency. These systems are engineered to maintain consistent performance across the Kingdom’s wide temperature variations, making them suitable for both urban and rural usage conditions.

Electric Powertrain Technology: Battery Systems and Motor Architecture

Electric two-wheelers in Saudi Arabia are built around lithium-ion battery systems, primarily using LFP and NMC chemistries, each offering different advantages in energy density and thermal stability. Given the Kingdom’s high ambient temperatures, LFP batteries are widely adopted for their superior resistance to heat-related degradation. Manufacturers are also integrating advanced battery management and thermal control systems to ensure consistent performance. Electric models typically use hub-mounted motors for cost efficiency and low maintenance, while premium variants are increasingly adopting mid-drive configurations for improved torque delivery and riding dynamics. Additional features such as regenerative braking and emerging battery swapping solutions are enhancing operational efficiency, particularly for commercial users.

Connected Vehicle Technology: IoT, Telematics, and OTA Updates

Connectivity is becoming a key feature in modern two-wheelers, especially in the growing electric segment. Manufacturers are incorporating telematics systems that enable real-time vehicle tracking, battery monitoring, and performance diagnostics. Over-the-air (OTA) update capabilities allow continuous software improvements, including updates to battery management systems and motor control algorithms, without requiring physical servicing. Smartphone integration further enhances user experience by providing access to vehicle status, ride data, and maintenance alerts. Advanced security features such as GPS tracking and remote immobilisation are also being integrated to address theft concerns and improve overall vehicle safety.

Digital Retail and Aftersales Technology

The retail and aftersales landscape for two-wheelers in Saudi Arabia is increasingly digital, with manufacturers offering online platforms that support the entire purchase journey, from model selection to financing and delivery. In the aftersales domain, digital tools are enabling more efficient service operations, including predictive maintenance systems that analyse vehicle data to identify potential issues in advance. Some service centres are also adopting augmented reality-based diagnostic tools to assist technicians and improve service accuracy. Additionally, the growth of e-commerce platforms for spare parts and the development of EV charging applications are improving accessibility and convenience for consumers across both urban and remote regions.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Type | 🔒 | 🔒 |

2025 |

| Technology | ICE | 72.4% |

2025 |

| Transmission |

🔒 |

🔒 |

2025 |

| Engine Capacity |

🔒 |

🔒 |

2025 |

| Fuel Type | 🔒 | 🔒 |

2025 |

| Distribution Channel | Offline Channels | 68.4% | 2025 |

| End User | 🔒 | 🔒 | 2025 |

| Region | Northern and Central Region | 38.4% | 2025 |

By Distribution Channel

Offline Channels account for 68.4% of the Saudi Arabia two-wheeler market in 2025. The offline segment’s dominance stems from the complex purchase journey inherent to two-wheelers – test rides, customisation consultations, financing, and after-sales service agreements are all dealership-centric activities that digital channels cannot yet fully replicate in Saudi Arabia’s current retail environment.

To access detailed market analysis, Request Sample

Online Channels at 31.6% reflect a market in mid-stage digital transition. Saudi Arabia’s e-commerce penetration rate reached 76% in 2024, and two-wheeler OEMs are increasingly offering online pre-order capabilities with showroom fulfilment.

By Technology

ICE technology commands 72.4% of the market in 2025, underpinned by Saudi Arabia’s widespread petrol fuelling infrastructure and consumer familiarity with ICE maintenance. The Electric segment holds 27.6% – a notably high share relative to regional peers – and is growing at a faster rate than the overall market, supported by falling battery costs and government-aligned EV mandates, including the Saudi Green Initiative.

The Electric segment’s 27.6% share reflects Saudi Arabia’s aggressive EV policy framework. Under NIDLP and broader GCC policies, EV adoption is being supported through import facilitation and localization efforts that improve affordability. Chinese OEMs such as Yadea, AIMA, and NIU are leading early growth with cost-competitive offerings, while Japanese players like Honda, Yamaha, and Suzuki are entering more gradually with a focus on quality and long-term positioning.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

Major Markets |

|

Northern and Central Region |

38.4% |

Riyadh mega-urban logistics, gig-economy density, high expat population, Riyadh Metro last-mile demand |

Riyadh, Al-Qassim, Ha’il |

|

Western Region |

28.6% |

Jeddah port commerce, Mecca/Medina pilgrimage logistics, Red Sea tourism, high delivery frequency |

Jeddah, Mecca, Medina, Taif |

|

Eastern Region |

22.4% |

Aramco industrial workforce, Dammam port logistics, and high household income supporting the premium segment |

Dammam, Khobar, Dhahran, Jubail |

|

Southern Region |

10.6% |

Agricultural utility demand, Asir tourism, Vision 2030 infrastructure investment, and improving connectivity |

Abha, Jizan, Najran |

The Northern and Central Region (38.4%) is led by Riyadh, which drives demand through its large population, strong delivery and logistics ecosystem, and rising last-mile connectivity needs, with Al-Qassim adding agriculture-driven utility demand. The Western Region (28.6%) is anchored by Jeddah’s commercial importance, while Mecca and Medina generate seasonal demand from pilgrimage-related logistics, further supported by Red Sea tourism.

The Eastern Region (22.4%) benefits from Dammam’s industrial base and Aramco-linked workforce, sustaining commuter demand and enabling higher penetration of premium motorcycles. Meanwhile, the Southern Region (10.6%) remains a high-growth market, where infrastructure development is improving accessibility, with utility motorcycles dominating and leisure usage gradually increasing in Asir and Jizan.

Competitive Landscape

The Saudi Arabia two-wheeler market is moderately fragmented, characterised by the co-existence of established Japanese OEM brand equity alongside an increasingly assertive cohort of Chinese E2W manufacturers and a small cluster of European premium brands. Japanese OEMs collectively hold an estimated 55-60% of the ICE segment, while Chinese brands are capturing the majority of new Electric segment registrations.

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

Honda Motor Co., Ltd. |

Honda |

Leader |

ICE motorcycles and scooters, the widest dealer network across Saudi Arabia |

|

Yamaha Motor Co., Ltd. |

Yamaha |

Leader |

ICE motorcycles and sport bikes have strong brand equity among enthusiasts |

|

Kawasaki Heavy Industries, Ltd. |

Kawasaki |

Challenger |

Premium ICE motorcycles, adventure and sport segment focus |

|

Suzuki Motor Corporation |

Suzuki |

Challenger |

ICE commuter motorcycles and scooters, value-segment strength |

|

Yadea Group Holdings Ltd. |

Yadea |

Emerging |

Electric two-wheelers, competitive sub-USD 1,000 price positioning |

|

Niu International |

NIU |

Emerging |

Smart electric scooters, IoT connectivity, urban commuter focus |

|

AIMA TECHNOLOGY GROUP CO., LTD. |

AIMA |

Emerging |

Electric motorcycles and scooters, an aggressive GCC market expansion |

The Saudi two-wheeler competitive landscape is characterised by a small number of Japanese OEM brands commanding dominant ICE market positions, alongside a rapidly growing cohort of Chinese E2W manufacturers challenging the established hierarchy through price competitiveness and electric product innovation.

Key Company Profiles

Honda Motor Co., Ltd.

Honda Motor Co., Ltd. is a manufacturer of motorcycles by volume and holds the leading market position in Saudi Arabia’s two-wheeler segment, supported by an extensive authorised dealer network spanning 12+ cities.

- Product Portfolio: Honda CB series, Honda Wave commuters, Honda PCX scooters, Honda CRF adventure range, Honda Gold Wing touring segment.

- Recent Developments: In May 2023, Honda introduced the EM1 e: electric scooter as part of its global electrification strategy, marking its first mass-market electric two-wheeler rollout and supporting its broader EV roadmap.

- Strategic Focus: Honda’s Saudi strategy centres on expanding its commuter motorcycle volume leadership while progressively introducing its E2W platform. The company is investing in dealer service centre upgrades to support the electric model after-sales readiness.

Yamaha Motor Co., Ltd.

Yamaha Motor is a two-wheeler brand in Saudi Arabia, with particular strength in the sport motorcycle segment and a loyal enthusiast community across major cities.

- Product Portfolio: YZF-R Series, MT Series – Hyper Naked

Recent Developments: In March 2022, Yamaha launched NEO'S electric scooter with a removable battery design in Europe - promoting both smarter short-distance urban mobility and carbon neutrality. - Strategic Focus: Yamaha’s Saudi strategy balances premium sport segment brand-building with volume commuter growth, while preparing its electric mobility platform EMF (Electric Motorcycle Framework) for GCC deployment.

Yadea Group Holdings Ltd.

Yadea is an electric two-wheeler manufacturer by volume and is rapidly expanding its GCC presence, capturing a significant share of Saudi Arabia’s growing Electric segment through competitive pricing and improving product quality.

- Product Portfolio: Yadea C-series and G-series electric scooters, Yadea T-series mid-range E2Ws, Yadea VFLY flagship electric motorcycle targeting premium urban consumers.

- Recent Developments: In March 2026, Yadea showcased world-class innovation at the Chongqing Smart Manufacturing Base, strengthening engagement with Thai dealers.

- Strategic Focus: Yadea’s GCC strategy targets commercial delivery fleet operators as a beachhead customer segment, leveraging sub-USD 1,000 entry-level pricing and a growing after-sales service infrastructure to build brand equity ahead of Japanese E2W entries.

Market Concentration Analysis

The Saudi Arabia two-wheeler market displays a bimodal competitive structure. In the ICE segment, Japanese OEMs leverage decades of brand equity, established dealer networks, and competitive landed pricing to maintain oligopolistic positions. Honda, Yamaha, Kawasaki, and Suzuki collectively account for an estimated 55-60% of the ICE segment volume in 2025, with Honda holding the single largest share.

The Electric segment presents a structurally different competitive landscape – effectively a greenfield opportunity within a brownfield market. Chinese manufacturers dominate in price, with Yadea E2Ws available below USD 1,000 in Saudi Arabia. Established Japanese OEMs are still ramping their E2W model portfolios for the GCC market, creating a transient window for Chinese and European E2W specialists to capture brand loyalty before Japanese OEMs deploy full E2W ranges anticipated between 2026 and 2028.

Investment & Growth Opportunities

Fastest-Growing Segments

The Electric two-wheeler sub-segment is the fastest-growing opportunity within the Saudi Arabia two-wheeler market, projected to grow at a CAGR of approximately 10%+ during 2026-2034. Online distribution channels represent the second-highest growth opportunity, as Saudi Arabia’s digital commerce infrastructure matures and OEM D2C capabilities expand.

Key Investment Opportunities

- Electric Two-Wheeler Assembly (CKD): Vision 2030 localization goals and NIDLP incentives are encouraging OEMs to explore local CKD assembly, particularly in industrial hubs like Jubail, to reduce costs and access local content benefits.

- Last-Mile Fleet Electrification Contracts: Partnerships with major delivery platforms such as HungerStation LLC, Jahez International Company for Information Systems Technology, and Amazon.com, Inc. offer scalable, recurring revenue opportunities as demand for electrified delivery fleets rises.

- Charging Infrastructure as a Service: Limited availability of E2W charging infrastructure in key cities like Riyadh, Jeddah, and Dammam creates strong investment potential, especially in high-traffic commercial and mobility hubs.

- Digital Aftersales and Insurance Platforms: Low two-wheeler insurance penetration and evolving digital ecosystems open opportunities for insurance, roadside assistance, and connected aftersales services.

Future Market Outlook (2026-2034)

The Saudi Arabia two-wheeler market will expand from USD 1.37 Billion in 2025 to USD 2.30 Billion by 2034, supported by structural drivers that are secular rather than cyclical. At a CAGR of 5.94%, the market will add approximately USD 0.93 Billion in incremental revenue – growth underpinned by urbanisation deepening two-wheeler utility, electrification reshaping the technology mix, and gig-economy formalisation creating durable commercial demand.

The technology mix will undergo the most dramatic transformation over the forecast period. The Electric segment, at 27.6% in 2025, is projected to approach 45-50% by 2034 as battery cost curves continue declining and Saudi EV policy support intensifies. ICE will not contract in absolute terms but will yield a proportional share as the E2W model variety and charging infrastructure improve progressively across Saudi cities.

Regional growth will be broadly distributed. The Southern Region offers the highest CAGR potential off a low 10.6% base, while the Northern and Central Region maintains absolute volume leadership. The Western Region will benefit from Hajj/Umrah tourism recovery and Tabuk Province’s NEOM development activity, which will create a new premium mobility consumption cluster by the late 2020s.

Research Methodology

IMARC Group’s research methodology integrates rigorous primary and secondary research frameworks with proprietary bottom-up and top-down market estimation models validated against industry benchmarks and analogous GCC market trajectories.

Primary Research

In-depth interviews were conducted with two-wheeler OEM executives, dealership principals, fleet operators, government officials from ZATCA and NIDLP, and industry associations across Saudi Arabia. A minimum of 30 primary interviews were conducted per research cycle, with insights validated through triangulation across multiple independent sources.

Secondary Research

Secondary sources include Saudi General Authority for Statistics (GASTAT), Ministry of Transport publications, ZATCA customs import data, General Organization of Social Insurance (GOSI) workforce statistics, company annual reports, IEA EV Outlook, and regional trade publications covering the GCC automotive and mobility sector.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models incorporating GDP growth rates, urbanisation indices, fuel price trajectories, EV adoption curves, regulatory change indicators, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic uncertainty.

Saudi Arabia Two-Wheeler Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Scooters, Mopeds, Motorcycle, Electric Two-Wheeler |

| Technologies Covered | ICE, Electric |

| Transmissions Covered | Manual, Automatic |

| Engine Capacities Covered | <100cc, 100-125cc, 126-180cc, 181-250cc, 251-500cc, 501-800cc, 801-1600cc, >1600cc |

| Fuel Types Covered | Gasoline, Petrol, Diesel, LPG/CNG, Battery |

| Distribution Channels Covered | Offline Channels, Online Channels |

| End Users Covered | Personal, Commercial |

| Regions Covered | Northern and Central Region, Western Region, Eastern Region, Southern Region |

| Companies Covered | Honda Motor Co., Ltd., Yamaha Motor Co., Ltd., Kawasaki Heavy Industries, Ltd., Suzuki Motor Corporation, Yadea Group Holdings Ltd., Niu International, AIMA TECHNOLOGY GROUP CO., LTD., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Saudi Arabia two-wheeler market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Saudi Arabia two-wheeler market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Saudi Arabia two-wheeler industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Saudi Arabia Two-Wheeler Market Report

The Saudi Arabia two-wheeler market was valued at USD 1.37 Billion in 2025, supported by gig-economy delivery expansion, urbanisation, and Vision 2030 regulatory reforms that broadened the addressable consumer base significantly.

The market is projected to reach USD 2.30 Billion by 2034, growing at a CAGR of 5.94% during 2026-2034, driven by electrification, last-mile logistics demand, and expanding digital sales channels.

The Saudi Arabia two-wheeler market is forecast to grow at a CAGR of 5.94% during 2026-2034, reflecting sustained growth across commercial delivery, personal mobility, and the rapidly growing electric two-wheeler segment.

Offline Channels lead with a 68.4% share in 2025, driven by consumer preferences for in-person test rides, dealership financing, and after-sales service network proximity across major Saudi cities.

Electric technology holds a 27.6% share in 2025, one of the highest in the MENA region. Growth is supported by government EV incentives, falling battery costs, and a 30% EV penetration target by 2030.

The Northern and Central Region leads with a 38.4% share in 2025. Riyadh’s population density, gig-economy logistics infrastructure, and large expatriate workforce are the primary demand drivers.

Key drivers include gig-economy expansion, Vision 2030 mobility reforms, urbanisation exceeding 84%, female motorcycle licensing reforms from 2019, and growing commercial logistics demand from food-delivery platforms.

Leading players include Honda Motor Co., Ltd., Yamaha Motor Co., Ltd., Kawasaki Heavy Industries, Ltd., Suzuki Motor Corporation, Yadea Group Holdings Ltd., Niu International, and AIMA TECHNOLOGY GROUP CO., LTD., which are rapidly gaining share in the growing electric segment through competitive pricing.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)