Saudi Arabia Water Heater Market Size, Share, Trends and Forecast by Type and End-Use, 2026-2034

Saudi Arabia Water Heater Market Size, Share, Trends & Forecast (2026-2034)

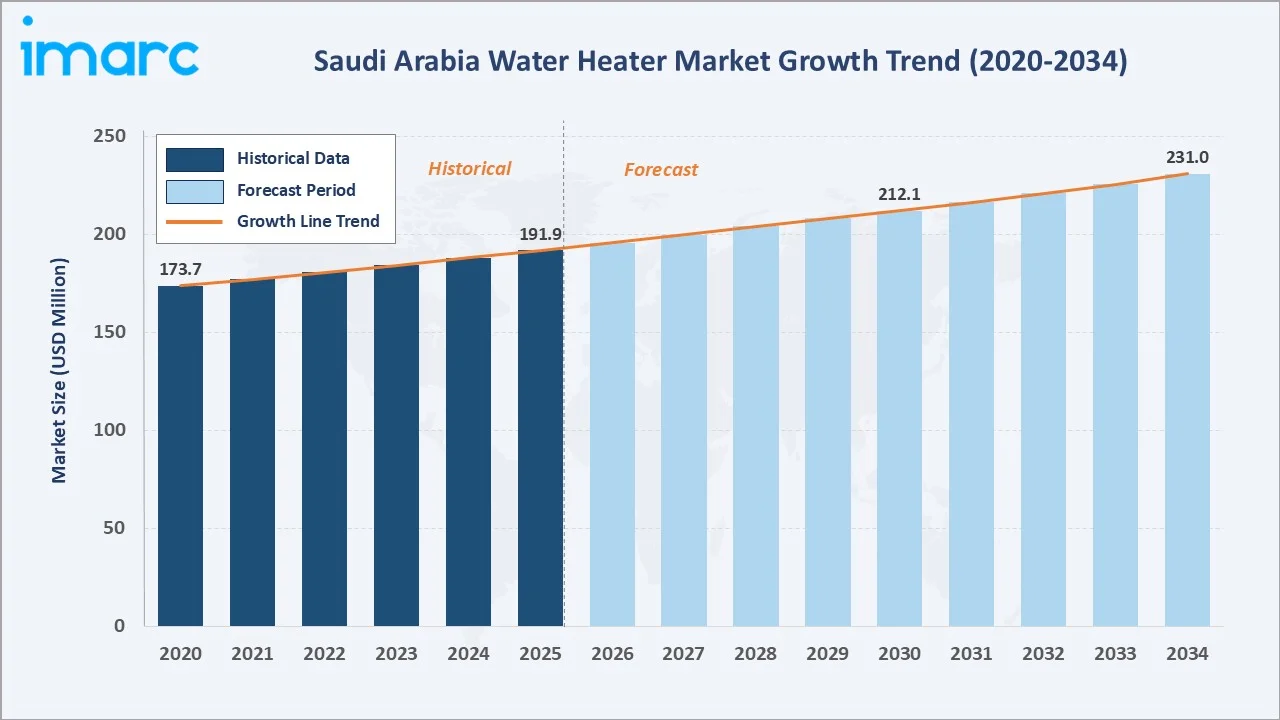

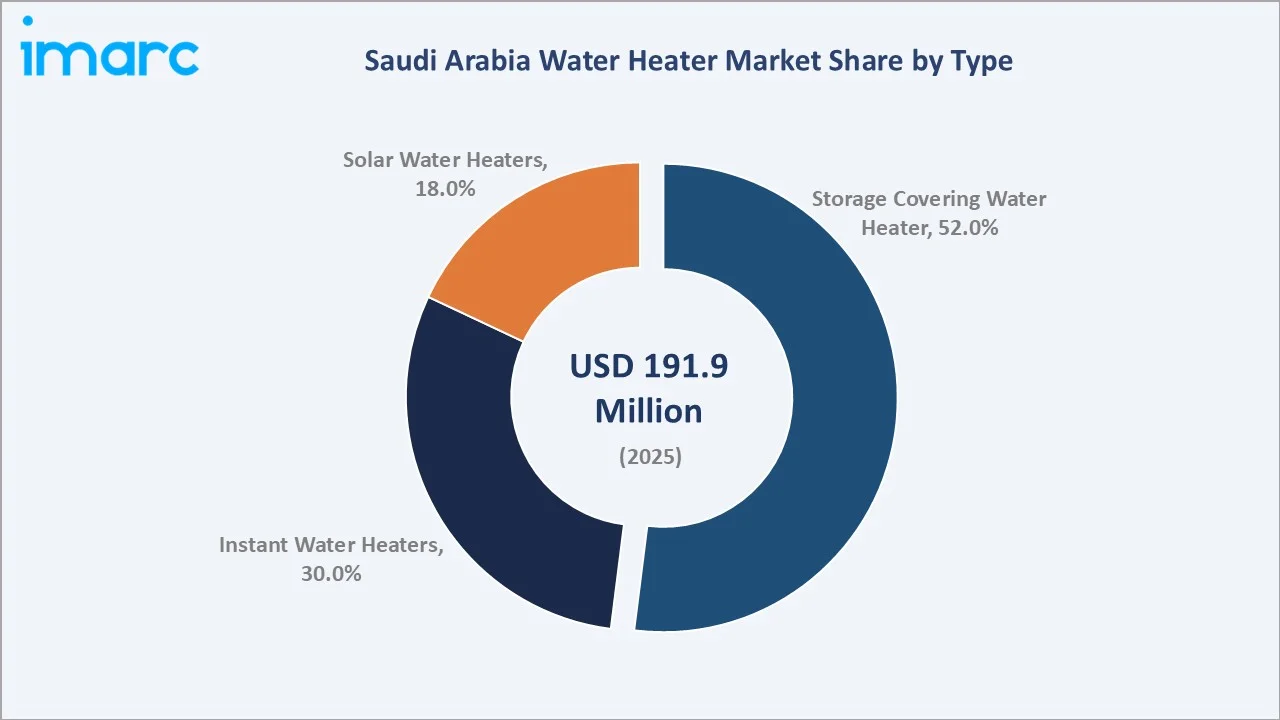

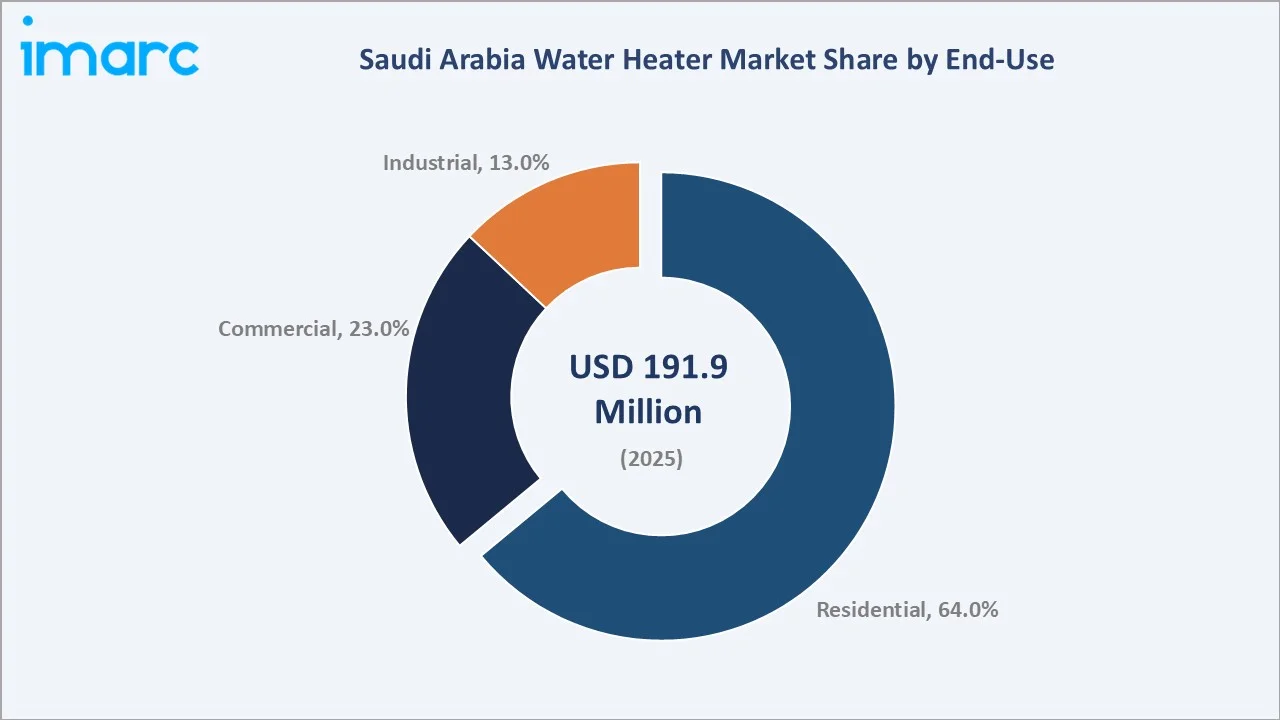

The Saudi Arabia water heater market size reached USD 191.9 Million in 2025 and is projected to grow to USD 231.0 Million by 2034, exhibiting a CAGR of 2.02% during 2026-2034. Rising residential construction under Vision 2030, expanding hospitality infrastructure, rapid population growth, and accelerated solar energy adoption are shaping strong Saudi Arabia water heater market growth. Storage Covering Water Heaters dominate with a 52.0% share in 2025, while the Residential segment accounts for 64.0% of national demand.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 191.9 Million |

|

Forecast Market Size (2034) |

USD 231.0 Million |

|

CAGR (2026-2034) |

2.02% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Type |

Storage Covering Water Heater (52.0%, 2025) |

|

Leading End-Use |

Residential (64.0%, 2025) |

The chart below illustrates the Saudi Arabia water heater market growth trend over 2020-2034, with new housing projects and Vision 2030 investments supporting the forecast trajectory.

To get more information on this market, Request Sample

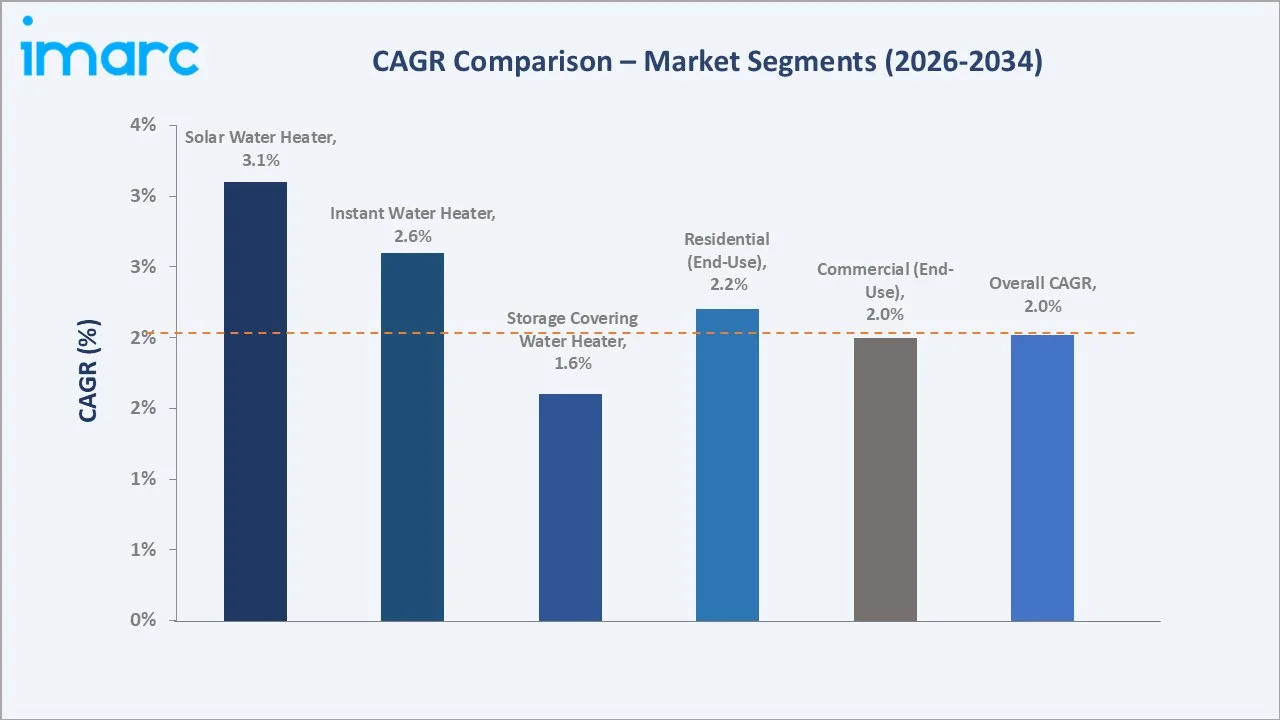

CAGR analysis highlights Solar and Instant Water Heaters as the fastest-growing product categories, driven by high solar radiation availability and on-demand heating preferences among modern consumers.

Executive Summary

The Saudi Arabia water heater market is transforming due to Vision 2030 housing initiatives, rising urbanization, and expanding hospitality infrastructure. Valued at USD 191.9 Million in 2025, it is projected to reach USD 231.0 Million by 2034, at a 2.02% CAGR. Growing demand for energy-efficient heating, solar-integrated products, and premium residential fittings is driving consistent volume expansion across urban and semi-urban zones.

Storage Covering Water Heaters lead the market with a 52.0% share in 2025, supported by reliability in large homes and villa formats. Instant Water Heaters hold 30.0% share, driven by compact apartments and water-saving preferences. Key trends include solar water heater adoption, smart connectivity features, heat pump deployment in commercial settings, and rising demand for corrosion-resistant tanks suited to hard water conditions.

The Residential segment commands 64.0% of demand in 2025, anchored by new housing supply across Riyadh, Jeddah, and Dammam. The Commercial segment contributes 23.0%, supported by hotels, malls, gyms, and public facilities. The Industrial segment holds 13.0%, driven by food processing, oil and gas operations, and manufacturing clusters. Collectively, these drivers position the Saudi Arabia water heater market for stable mid-single-digit expansion through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Type Segment |

Storage Covering Water Heater - 52.0% share (2025) |

|

Second-Largest Type Segment |

Instant Water Heater - 30.0% share (2025) |

|

Fastest-Growing Type Segment |

Solar Water Heater - 18.0% share (2025) |

|

Leading End-Use Segment |

Residential - 64.0% share (2025) |

|

Second End-Use Segment |

Commercial - 23.0% share (2025) |

|

Top Companies |

Ariston, A.O. Smith, Rheem, Bosch, Haier |

|

Market Opportunity |

Solar water heater scale-up under Vision 2030 renewable roadmap |

Key Analytical Observations Supporting the Above Data:

- Storage Covering Water Heaters' 52.0% dominance in 2025 reflects the Saudi preference for large-capacity tanks in villas and multi-bathroom homes, where simultaneous hot water draw is a routine requirement.

- Instant Water Heaters at 30.0% share in 2025 are expanding rapidly in apartments and studio-style housing, valued for compact footprint, on-demand output, and lower standing energy losses.

- Solar Water Heaters at 18.0% share in 2025 benefit from the Kingdom's high solar irradiance of over 2,200 kWh per square meter annually, making solar thermal one of the most cost-effective heating options.

- The Residential segment's 64.0% share in 2025 is reinforced by the Sakani housing program, launched in 2017, has supported over 750,000 Saudi families in accessing housing solutions, including homeownership, by 2024, fueling appliance demand.

- Commercial demand at 23.0% in 2025 is anchored by Saudi Arabia's hospitality expansion, with over 320,000 hotel rooms expected to be operational by 2030 under Vision 2030 tourism targets.

- Ariston Group, A. O. Smith Corporation, and Rheem Manufacturing Company collectively command a strong share of the formal market in 2025, driven by established distributor networks across Riyadh, Jeddah, and the Eastern Province.

Saudi Arabia Water Heater Market Overview

Water heaters are residential and commercial appliances that heat and store water using electricity, gas, heat pumps, or solar energy. In Saudi Arabia, the ecosystem spans OEMs, importers, component suppliers, distributors, retailers, e-commerce platforms, and installation contractors serving residential, commercial, and industrial users.

Applications cover homes, hotels, healthcare, education, gyms, laundries, food processing, and industrial sites. Growth is driven by Saudi Vision 2030, urbanization in NEOM and The Line, rising incomes, and solar adoption, while hard water conditions sustain replacement demand for scale-resistant systems.

Market Dynamics

To evaluate market opportunities, Request Sample

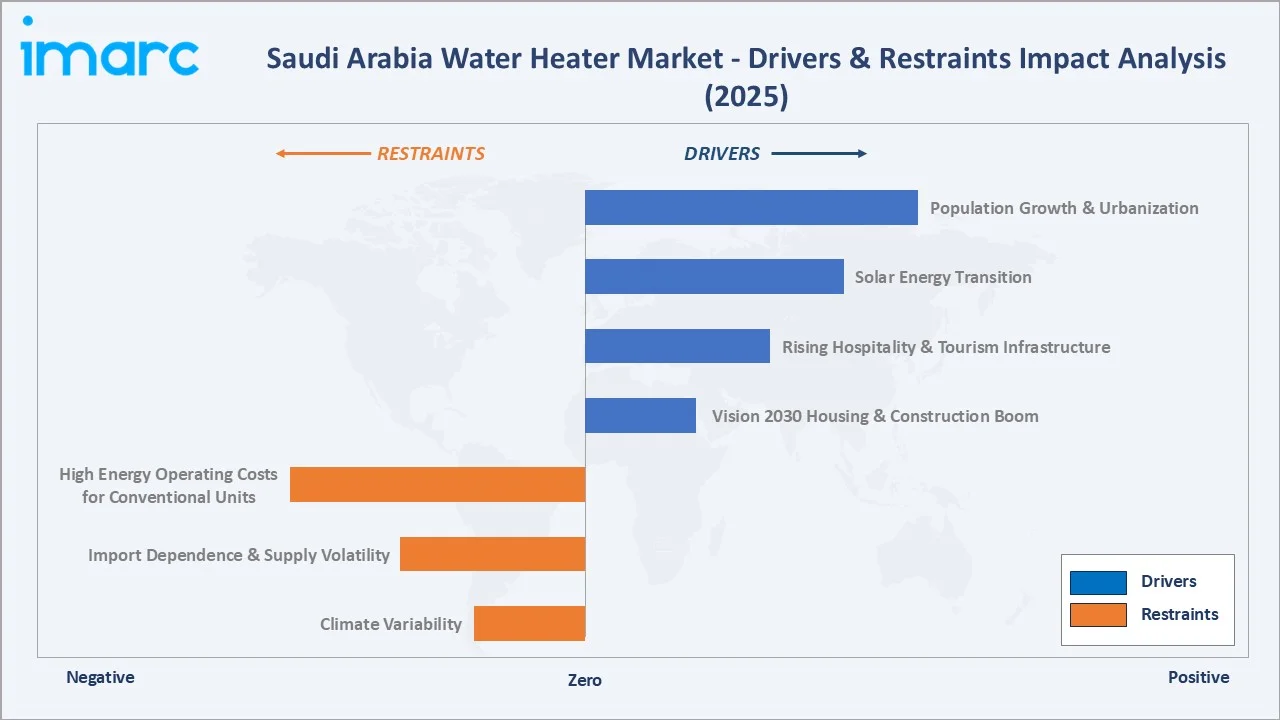

Market Drivers

- Vision 2030 Housing and Construction Boom: Over 1.3 million new housing units are planned under Saudi Arabia's Vision 2030 targets, directly translating into sustained water heater demand across Riyadh, Jeddah, and emerging giga-projects such as NEOM.

- Rising Hospitality and Tourism Infrastructure: Saudi Arabia targets 150 million visitors annually by 2030, adding over 320,000 hotel rooms. Each mid-scale hotel requires multiple commercial heaters, boosting premium segment demand through 2034.

- Solar Energy Transition under NREP: The National Renewable Energy Program is accelerating rooftop solar adoption, with government rebates for solar water heater installations reducing payback periods to under 4 years for residential users.

- Population Growth and Urbanization: Saudi Arabia’s population was approximately 32.2 million in 2022 and is projected to approach 40 million by 2030, with over 80% of the population living in urban areas, driving demand for appliances in multi-family housing developments. These drivers collectively reinforce Saudi Arabia water heater market growth, with housing supply, tourism, and renewable energy policy creating a structurally supportive demand environment through 2034.

Market Restraints

- High Energy Operating Costs for Conventional Units: Electricity tariff reforms implemented since 2018 increased residential energy costs, making inefficient storage water heaters expensive to operate and slowing replacement cycles among cost-conscious households in Saudi Arabia.

- Import Dependence and Supply Volatility: Saudi Arabia relies heavily on imported water heaters, exposing the market to freight cost fluctuations, global supply chain disruptions, currency volatility, and regulatory requirements such as SASO certification delays.

- Hard Water and Scale-Related Failures: High mineral content and water salinity in several regions contribute to scaling and corrosion in water heaters, causing premature component failure, reducing efficiency, and limiting consumer confidence in low-cost products.

Market Opportunities

- Solar Water Heater Scale-Up: Solar water heating adoption remains relatively limited in Saudi Arabia compared to mature markets like Israel, indicating strong growth potential supported by renewable energy targets and government initiatives under Vision 2030.

- Heat Pump Technology Introduction: Heat pump water heaters deliver significantly higher energy efficiency than conventional electric systems and are gaining adoption in commercial applications, creating a premium segment with strong cost savings and long-term growth potential.

- Smart and IoT-Enabled Products: Smart water heaters with IoT-enabled features like remote control, energy monitoring, and leak detection are gaining traction in premium housing and mega-projects, aligning with Saudi Arabia’s broader smart city development initiatives.

Market Challenges

- Unorganized Retail and Counterfeit Products: Presence of informal retail channels and counterfeit electrical products in Saudi Arabia creates pricing pressure on branded players while raising safety, quality, and warranty concerns for consumers in the water heater market.

- Limited Domestic Manufacturing Base: Limited domestic manufacturing capabilities in Saudi Arabia’s appliance sector increase reliance on imports, constraining local value addition despite government efforts under Vision 2030 to boost industrial localization and production capacity.

- Installation Workforce Skill Gaps: Shortage of skilled technicians and certified installers, particularly for advanced and solar-based systems, affects installation quality and after-sales service, slowing adoption of efficient water heating technologies across regions beyond major cities

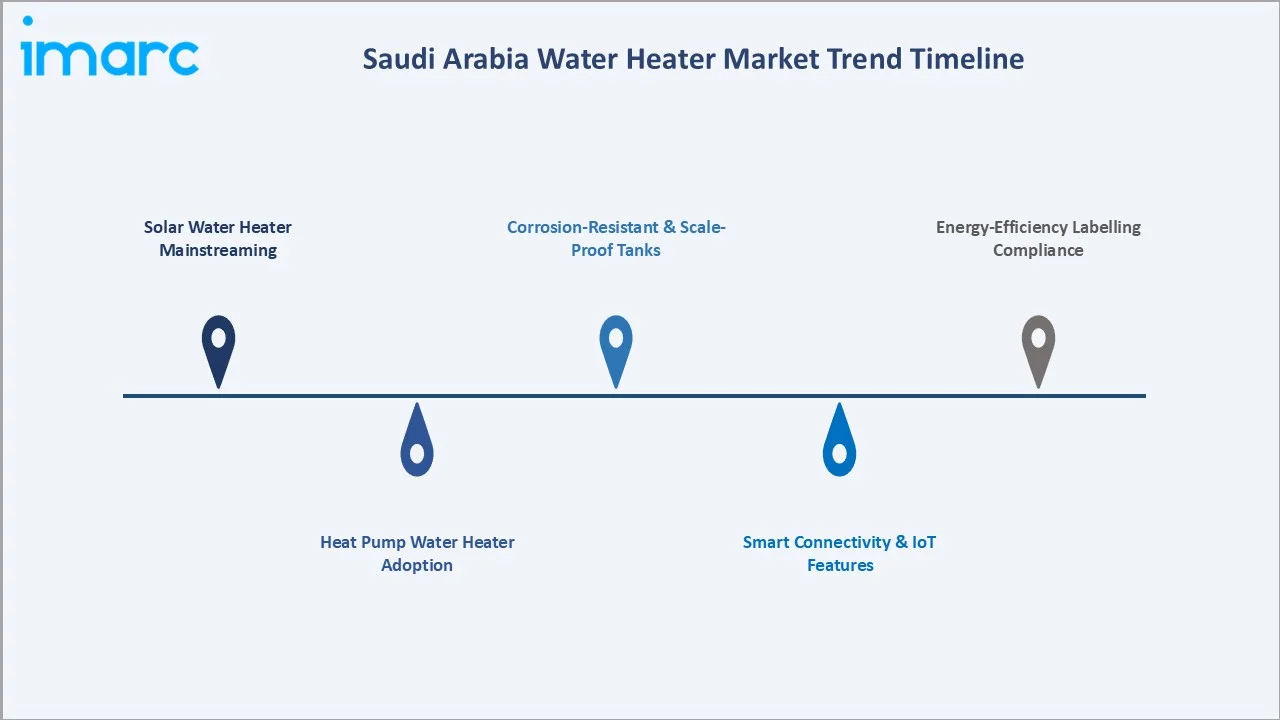

Emerging Market Trends

The Saudi Arabia water heater market trends reflect a clear shift toward efficiency, renewables, and digital intelligence, reshaping product mix and competitive dynamics through 2034.

1. Solar Water Heater Mainstreaming

Solar water heating adoption is increasing in Saudi Arabia, supported by renewable energy initiatives and Vision 2030, improving affordability and encouraging uptake among residential villa developments and new housing projects.

2. Heat Pump Water Heater Adoption

Heat pump water heaters are gaining adoption in commercial and premium residential applications, offering significantly higher energy efficiency than conventional electric systems and enabling substantial long-term operational cost savings.

3. Smart Connectivity and IoT Features

Leading manufacturers are introducing Wi-Fi-enabled water heaters with mobile app control, remote scheduling, and leak detection features, targeting smart homes and large-scale residential developments across Saudi Arabia’s giga-project ecosystem.

4. Corrosion-Resistant and Scale-Proof Tanks

Manufacturers are developing advanced tank materials such as glass-lined and coated systems to withstand mineral-rich water conditions, improving durability, extending product lifespan, and reducing maintenance and lifecycle costs.

5. Energy-Efficiency Labelling Compliance

Stricter SASO energy efficiency labeling regulations are raising minimum performance standards, reducing entry of low-quality imports and supporting increased adoption of certified, energy-efficient water heaters across the Saudi market.

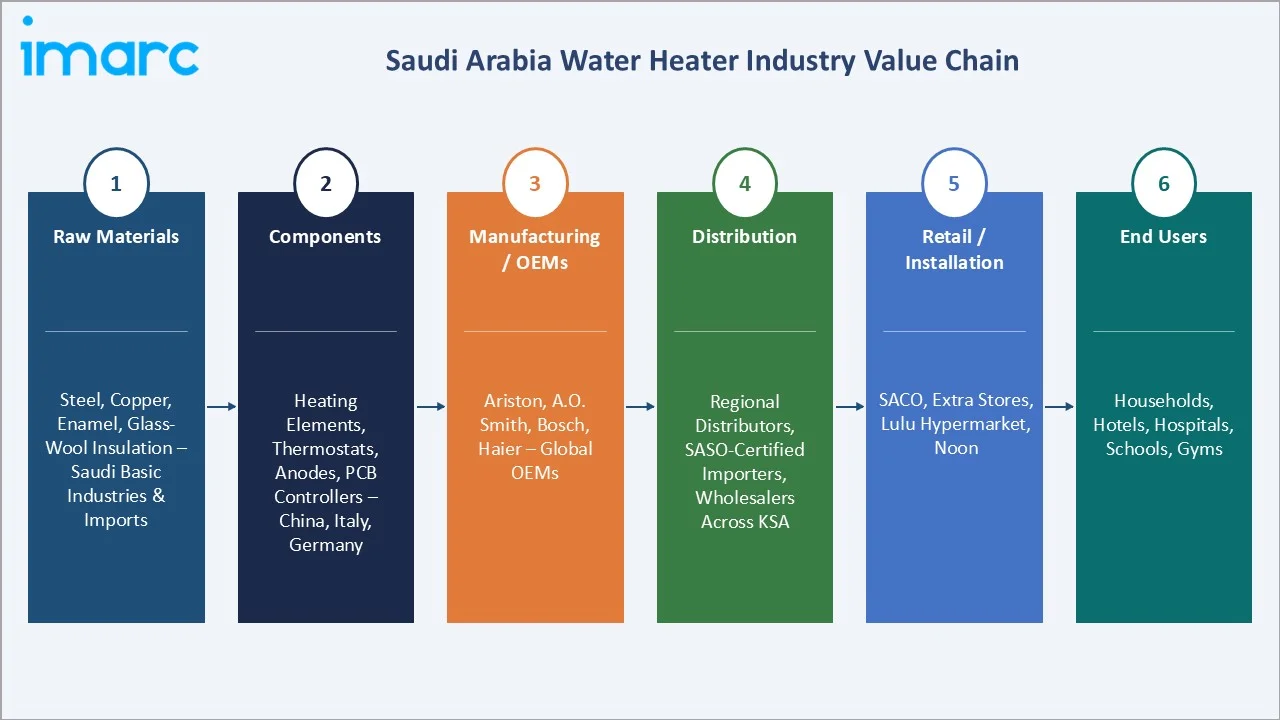

Industry Value Chain Analysis

The Saudi Arabia water heater value chain spans six stages, from raw materials to installation, each with distinct economic roles and competitive dynamics.

|

Stage |

Key Players / Examples |

|

Raw Materials |

Steel, copper, enamel, glass-wool insulation suppliers - sourced from Saudi Basic Industries (SABIC), plus regional imports |

|

Components |

Heating elements, thermostats, anodes, PCB controllers - imported from China, Italy, Germany, and Turkey |

|

Manufacturing / OEMs |

Ariston Thermo, A.O. Smith, Rheem, Bradford White, Bosch Thermotechnology, Haier, Midea, Alhafiz |

|

Distribution |

Regional distributors, SASO-certified importers, project wholesalers across Riyadh, Jeddah, Dammam |

|

Retail / Installation |

SACO, Extra Stores, Lulu Hypermarket, Noon, Amazon.sa, plumbing contractors, MEP project teams |

|

End Users |

Households, hotels, hospitals, schools, gyms, labor camps, food processing plants, oil and gas sites |

OEMs capture the largest share of economic value, given brand equity, SASO certification costs, and scale-driven procurement advantages. Installation contractors are becoming important partners, particularly for solar and heat pump systems requiring specialized skills.

Technology Landscape in the Industry

Advanced Tank and Heating Element Materials

Glass-lined, stainless steel, and coated tanks are increasingly used in water heaters, offering improved corrosion resistance in mineral-rich water conditions, enhancing durability and reducing maintenance and lifecycle costs.

Solar Thermal and Heat Pump Innovation

Solar thermal systems and heat pump water heaters are advancing in efficiency and adoption, offering significantly lower energy consumption than conventional systems and supporting growing demand for sustainable water heating solutions.

Smart Connectivity and IoT Integration

Manufacturers are integrating Wi-Fi-enabled controls, mobile applications, and smart monitoring features into water heaters, enabling remote operation, energy tracking, and predictive maintenance for modern residential and commercial applications.

Automation and Safety Systems

Modern water heaters incorporate safety features such as automatic shut-off, temperature regulation, and dry-burn protection, with SASO standards ensuring compliance, improved reliability, and safer operation across residential and commercial installations.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Storage Covering Water Heater |

52.0% |

2025 |

|

End-Use |

Residential |

64.0% |

2025 |

By Type

Storage Covering Water Heaters hold a 52.0% share in 2025, widely used in villas for high hot water demand. Medium-capacity tanks dominate, with corrosion-resistant materials preferred in mineral-rich water conditions.

To access detailed market analysis, Request Sample

Instant Water Heaters account for 30.0% of the market in 2025, driven by apartment dwellers and renters seeking compact, on-demand heating solutions with minimal standby energy loss. Solar Water Heaters contribute 18.0% share, growing rapidly on the back of government incentives and high solar resource availability across the Kingdom.

By End-Use

The Residential segment dominates with a 64.0% share in 2025, supported by homeownership initiatives like Sakani, with rising villa and apartment construction driving strong demand for water heaters across urban regions.

The Commercial segment holds 23.0% share in 2025, led by hotels, malls, fitness clubs, and healthcare facilities. Vision 2030 tourism expansion is adding hundreds of new hotels, each requiring centralized water heating solutions. The Industrial segment at 13.0% is anchored by food processing, dairies, petrochemical operations, and oil and gas field support services.

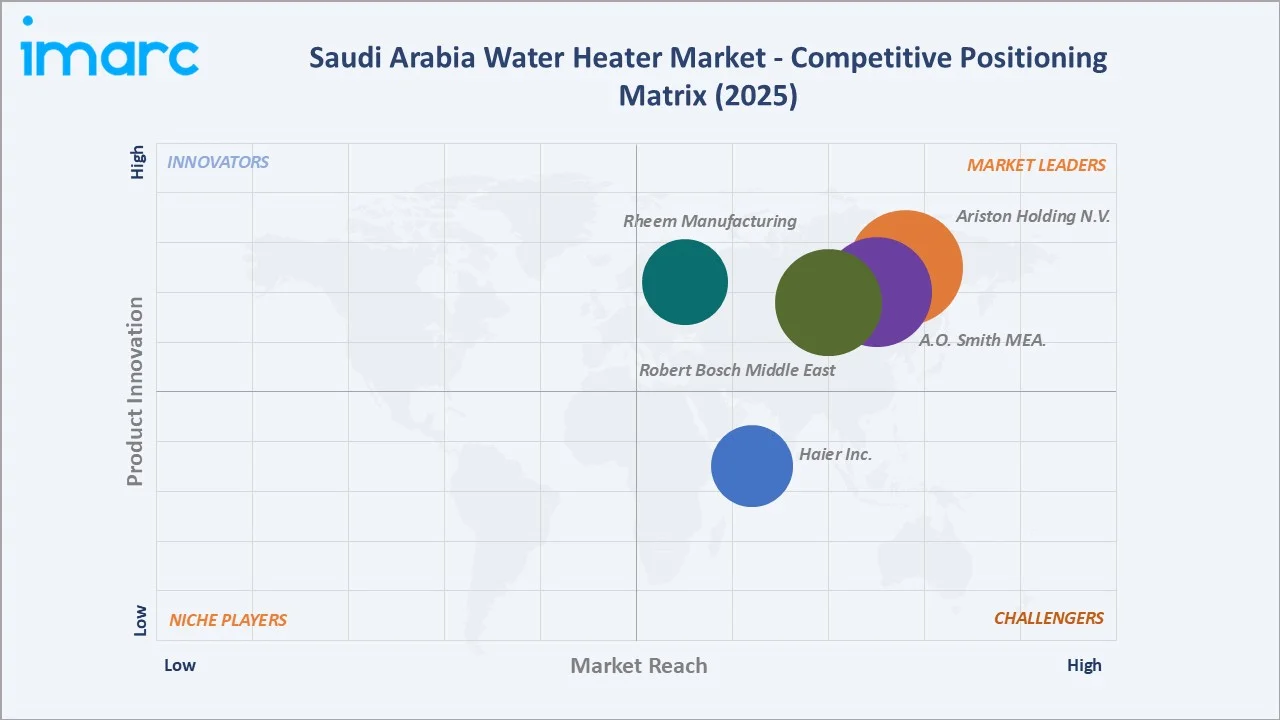

Competitive Landscape

|

Company Name |

Key Brand |

Market Position |

Core Strength |

|

Ariston Holding N.V. |

Ariston |

Leader |

Italian heritage, wide Saudi distribution, premium positioning |

|

A.O. Smith MEA. |

A.O. Smith, State Water Heaters |

Leader |

Glass-lining technology, long warranties, commercial strength |

|

Rheem Manufacturing Company |

Rheem, Maximus |

Leader |

Solar-electric hybrid models, U.S. brand recognition |

|

Robert Bosch Middle East |

Bosch |

Challenger |

German engineering, heat pump and tankless focus |

|

Haier Inc. |

Haier |

Challenger |

Mid-price positioning, large tank portfolio |

The Saudi Arabia water heater market is moderately consolidated at the top tier, with Ariston Holding N.V., A.O. Smith MEA., and Rheem Manufacturing Company commanding a significant combined share in 2025. Competitive intensity is increasing as Chinese and Turkish imports such as Haier Inc., Midea, and Alarko continue to expand presence through price-competitive models and aggressive retail partnerships.

Key Company Profiles

Ariston Holding N.V.

Ariston Holding N.V., headquartered in Italy, is a global thermal comfort leader operating in 150+ countries. The company reported €2.6 billion revenue in FY2025 and maintains a strong Middle East presence through energy-efficient, SASO-compliant water heating solutions.

- Product & Service Portfolio: Ariston offers electric storage and instant water heaters, gas heaters, solar thermal systems, and heat pump-based solutions, complemented by smart connected technologies for residential and commercial applications.

- Recent Developments: Ariston reported a recovery in revenues to €2.6 billion in FY25, driven by growing demand for energy-efficient and smart heating solutions, while simultaneously strengthening its Middle East presence through the acquisition and ramp-up of a water heater manufacturing facility in Egypt to serve regional markets.

- Strategic Focus: Ariston focuses on expanding energy-efficient, heat pump and smart-connected water heating technologies while strengthening its Middle East manufacturing and distribution footprint to align with regional sustainability and localization initiatives.

A.O. Smith MEA.

A. O. Smith Corporation, headquartered in Milwaukee, USA, is a global leader in water heating and treatment solutions. The company reported approximately USD 3.0 billion revenue in 2024, with international markets including the Middle East contributing to its diversified growth strategy.

- Product & Service Portfolio: A. O. Smith provides electric and gas storage water heaters, tankless systems, heat pump water heaters, boilers, and water treatment solutions for residential, commercial, and industrial applications globally.

- Recent Developments: In 2024, A. O. Smith maintained stable revenues of around USD 3.0 billion while accelerating investments in energy-efficient water heating technologies and expanding its premium commercial portfolio, with increased focus on heat pump and high-efficiency systems for global hospitality and infrastructure sectors, including the Middle East.

- Strategic Focus: A. O. Smith focuses on expanding energy-efficient, premium water heating and treatment technologies, with emphasis on heat pumps, commercial applications, and international market growth aligned with urbanization and sustainability trends.

Robert Bosch Middle East

Robert Bosch GmbH, headquartered in Gerlingen, Germany, is a global technology leader with €90.5 billion revenue in 2024. Its Home Comfort division (formerly Thermotechnology) is a key segment delivering advanced heating and hot water solutions globally and across the Middle East.

- Product & Service Portfolio: Bosch offers electric storage and instantaneous water heaters, gas tankless systems, heat pumps, boilers, and smart energy management solutions under brands like Bosch and Buderus for residential, commercial, and industrial applications.

- Recent Developments: In 2024, Bosch reported €90.5 billion global revenue while expanding its Energy & Building Technology segment, alongside strong Middle East growth to €574 million (+18% YoY), driven by rising demand for energy-efficient heating and hot water solutions.

- Strategic Focus: Bosch focuses on expanding heat pump-based, energy-efficient, and digitally connected heating solutions while strengthening partnerships in large-scale infrastructure and hospitality projects across Saudi Arabia and the broader Middle East.

Market Concentration Analysis

The Saudi Arabia water heater market exhibits a moderately concentrated structure at the top tier, with the top five players - Ariston, A.O. Smith, Rheem, Bosch, and Haier - collectively holding approximately 55-60% of organized channel revenue in 2025, supported by SASO certifications, established distributor networks, and after-sales service coverage.

Fragmentation rises sharply in the mass-market and unorganized segments, where dozens of Chinese, Turkish, and regional brands compete on price through retail chains and online platforms. This bifurcated structure - concentrated at the premium end and fragmented at the value end - mirrors the typical evolution path of mid-stage appliance markets in the GCC region.

Consolidation is advancing through distribution partnerships and exclusive Saudi agency agreements. The entry of Haier, Midea, and Rheem via stronger local collaborations highlights how global OEMs are tightening control over Saudi Arabia’s rapidly expanding water heater demand.

Investment & Growth Opportunities

Fastest-Growing Segments

Solar water heaters are expected to see steady growth in Saudi Arabia, supported by Saudi Vision 2030 and renewable energy targets. The Kingdom aims to reach 50% power generation from renewables by 2030, which indirectly supports solar thermal adoption in residential and commercial applications.

Heat pump water heaters remain a nascent but fast-emerging segment, gaining traction in commercial facilities such as hotels, hospitals, and laundries due to their high energy efficiency and lower operating costs amid electricity price reforms.

Emerging Project Opportunities

Mega-projects such as NEOM Saudi Arabia, The Line Saudi Arabia, The Red Sea Project Saudi Arabia, and Qiddiya Saudi Arabia are driving large-scale construction, creating strong demand for water heating systems across residential, hospitality, and mixed-use developments.

Venture and Strategic Investment Trends

Strategic investment is flowing into smart appliance startups, solar thermal assemblers, and local manufacturing facilities. Saudi Industrial Development Fund (SIDF) financing is enabling local assembly ventures, while Public Investment Fund-backed housing programs are driving scale procurement contracts for OEMs.

Future Market Outlook (2026-2034)

The Saudi Arabia water heater market forecast projects a steady expansion from USD 191.9 Million in 2025 to USD 231.0 Million by 2034 at a CAGR of 2.02% - representing a value increase of approximately USD 39 Million over the forecast period. Growth will be supported by Vision 2030 housing delivery, tourism infrastructure scale-up, and renewable energy transition.

Three transformational themes will reshape the market through 2034. First, solar and heat pump technologies will collectively shift the product mix toward renewables. Second, smart connectivity will become standard in premium residential models, enabling energy dashboards and leak detection. Third, stricter SASO efficiency labelling will eliminate low-grade imports and favor certified branded players.

By 2034, Saudi Arabia’s water heater market is expected to gradually shift from conventional electric systems toward a more diversified mix, supported by Vision 2030 Saudi Arabia. Adoption of solar, heat pump, and smart-connected units is likely to rise, with early investors in energy-efficient and smart technologies gaining a competitive advantage.

Research Methodology

Primary Research

Primary research included structured interviews and surveys conducted in 2024-2025 with water heater OEM country managers, distributor principals in Riyadh and Jeddah, SASO-certified importers, MEP contractors executing giga-project hotel contracts, and procurement heads of hospitality and healthcare groups across the Kingdom.

Secondary Research

Secondary sources included OEM annual reports (Ariston, A.O. Smith, Rheem, Bosch), Saudi General Authority for Statistics (GASTAT) data, SASO regulatory publications, Saudi Ministry of Housing (Sakani) updates, Saudi Energy Efficiency Center reports, trade publications, customs import records, and industry association databases.

Forecasting Models

Market estimation and forecasting use a combined top-down and bottom-up approach, incorporating Saudi housing starts, hotel room pipeline, electricity tariff trends, import volumes, population growth data, and Vision 2030 construction milestones under base, optimistic, and conservative macroeconomic scenarios.

Saudi Arabia Water Heater Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | GW thermal, Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Storage Covering Water Heater, Solar Water Heater, Instant Water Heater |

| End-Uses Covered | Residential, Commercial, Industrial |

| Companies Covered | Ariston Holding N.V., A.O. Smith MEA., Rheem Manufacturing Company, Robert Bosch Middle East, Haier Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Saudi Arabia Water Heater Market Report

The Saudi Arabia water heater market size reached USD 191.9 Million in 2025, supported by strong residential construction, expanding hospitality infrastructure, and accelerating solar water heater adoption across the Kingdom.

The market is projected to reach USD 231.0 Million by 2034, growing at a CAGR of 2.02% during 2026-2034, driven by Vision 2030 housing delivery, tourism growth, and renewable energy transition.

Storage Covering Water Heaters lead with a 52.0% share in 2025, preferred in villas and large homes for their reliability, multi-bathroom capacity, and strong familiarity among Saudi consumers.

The Residential segment dominates with a 64.0% share in 2025, anchored by Saudi Arabia's Sakani homeownership program and strong housing supply across Riyadh, Jeddah, and Dammam regions.

Key drivers include Vision 2030 housing construction, hospitality expansion, solar energy adoption, population growth, rising urbanization, and government incentives for energy-efficient appliances across the Kingdom.

Leading companies include Ariston Holding N.V., A.O. Smith MEA., Rheem Manufacturing Company, Robert Bosch Middle East, and Haier Inc. and more.

Solar Water Heaters hold 18.0% share in 2025, supported by high solar irradiance, government rebates, and Vision 2030 renewable targets driving rapid adoption across residential and commercial segments.

Instant Water Heater growth is driven by apartment housing expansion, studio living trends, water-saving awareness, and compact form factor advantages suiting urban renters and young Saudi households.

Smart Wi-Fi controls, heat pump systems, solar thermal integration, corrosion-resistant tanks, and SASO energy labelling are modernizing the market and shifting demand toward premium, efficient models.

Hospitality represents the largest commercial end-use, driven by hotel construction under Vision 2030, expected to add over 320,000 rooms by 2030, requiring centralized and high-capacity water heating.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)