Washing Machine Market Size, Share, Trends and Forecast by Product, Technology, Capacity, Application, End Use, and Region, 2026-2034

Global Washing Machine Market Size, Share, Trends & Forecast (2026-2034)

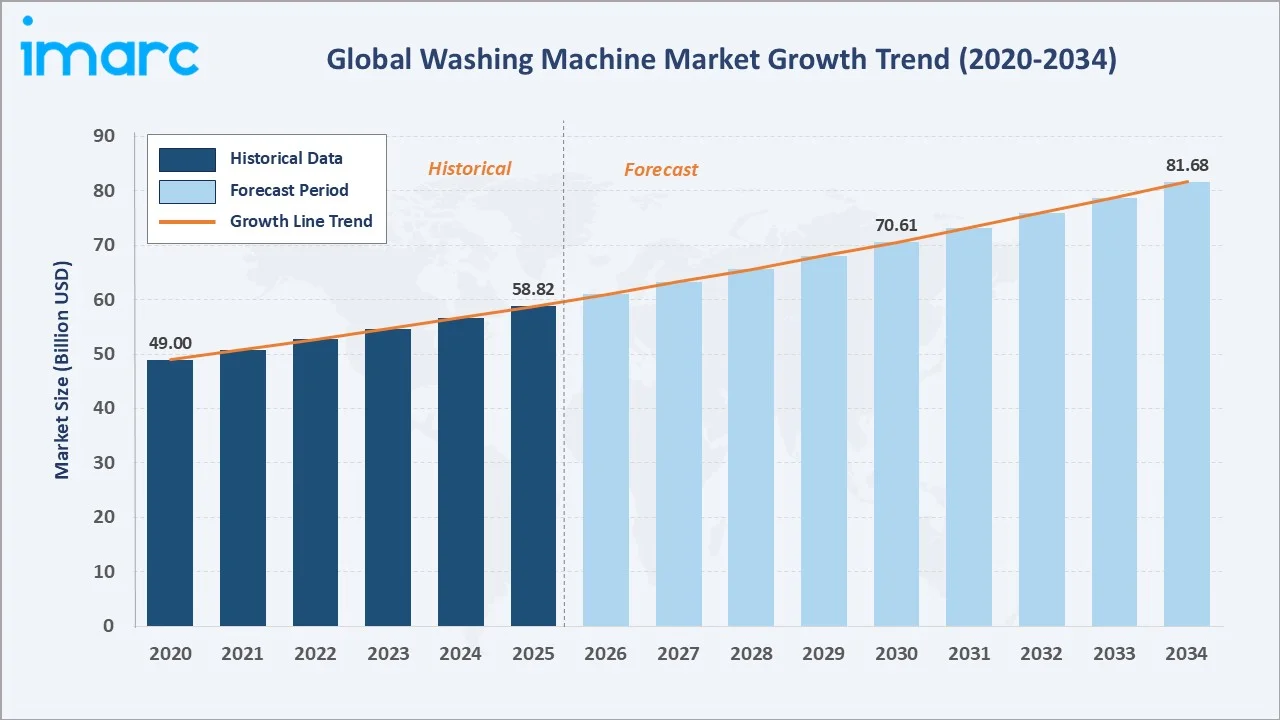

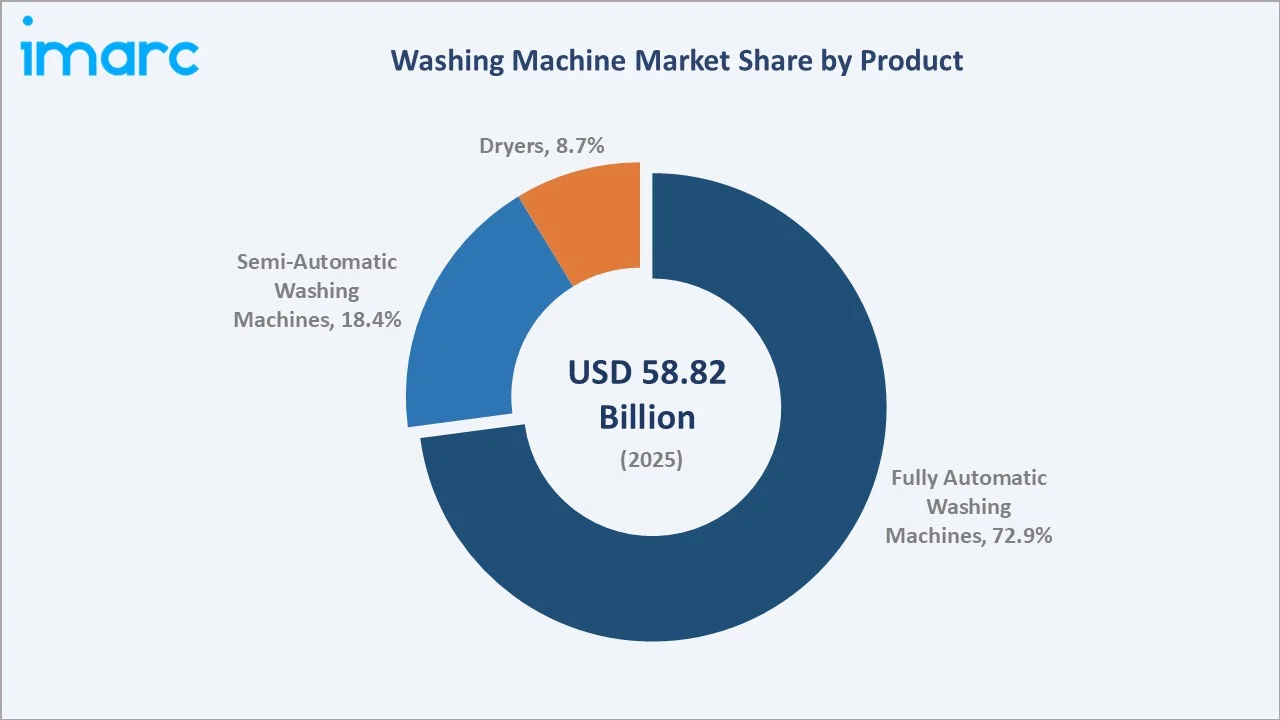

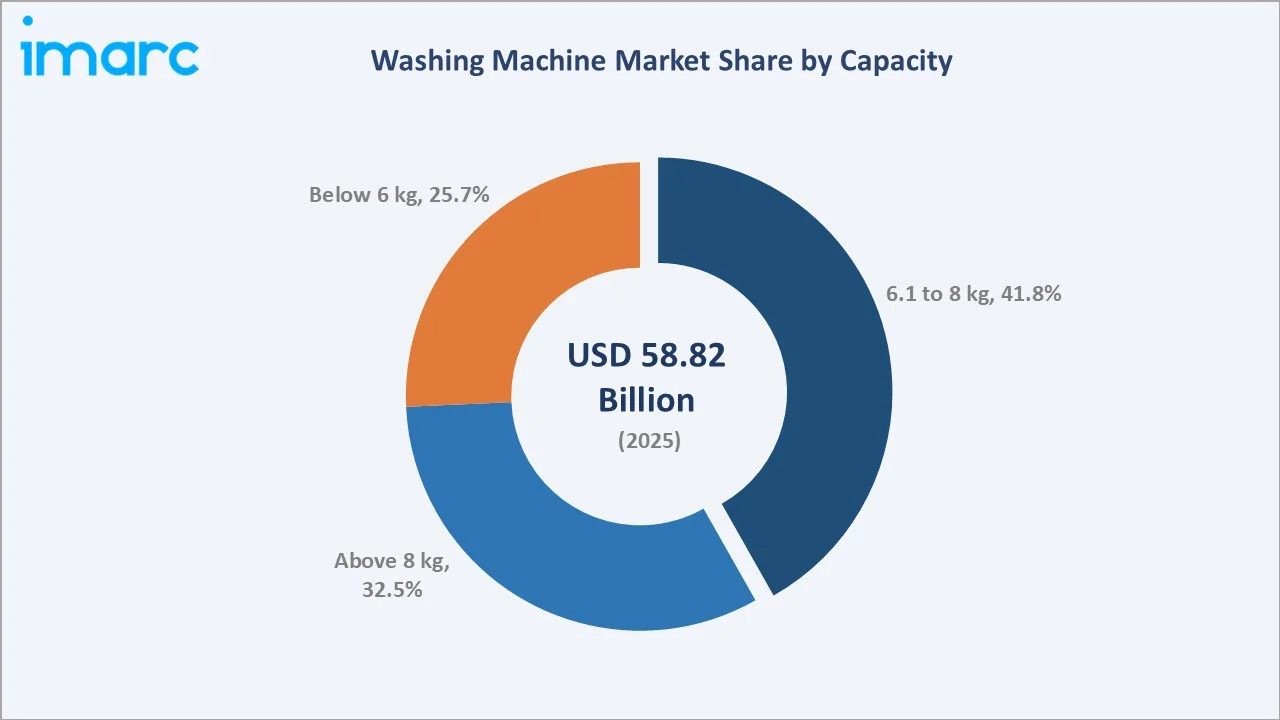

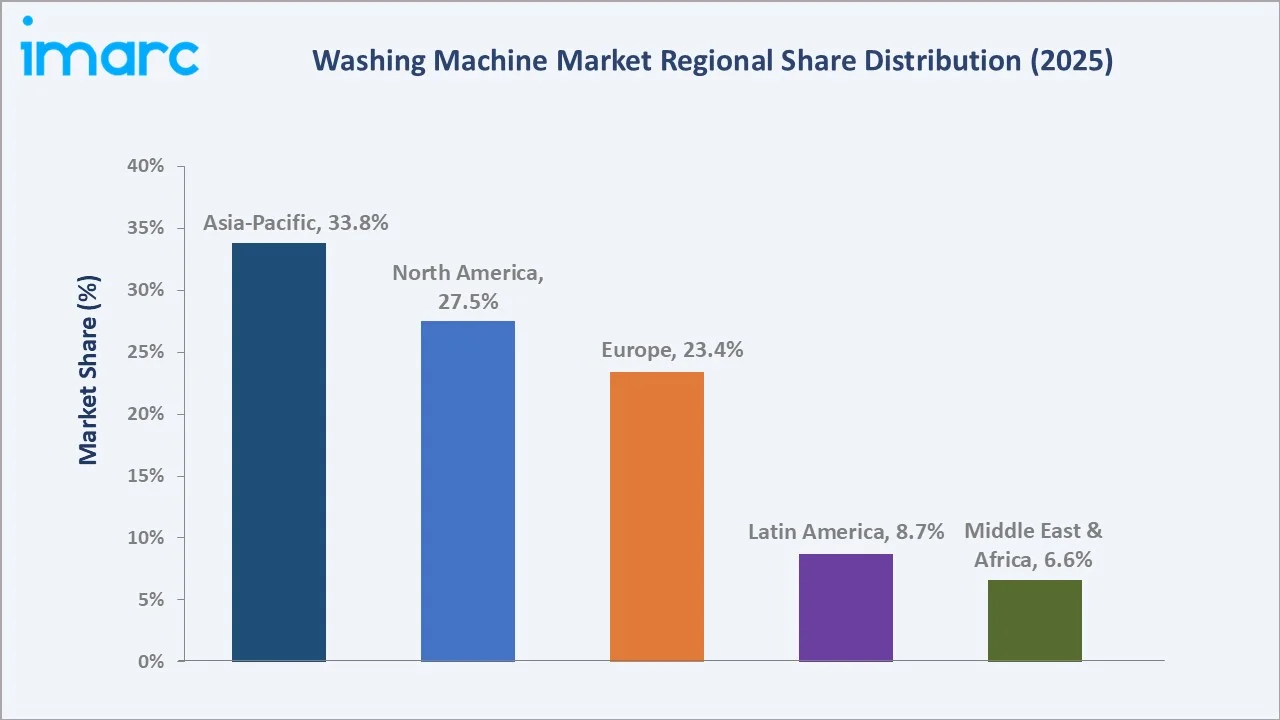

The global washing machine market size reached USD 58.82 Billion in 2025 and is projected to reach USD 81.68 Billion by 2034, exhibiting a CAGR of 3.72% during 2026-2034. Rising urbanization, growing middle-class disposable incomes, and the accelerating shift toward smart and AI-enabled appliances are the primary forces driving washing machine market growth.

Fully automatic machines dominate at 72.9% in 2025, while Asia-Pacific commands a dominant 33.8% regional share, reflecting unparalleled household appliance demand across China, India, and Southeast Asia.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 58.82 Billion |

|

Forecast Market Size (2034) |

USD 81.68 Billion |

|

CAGR (2026-2034) |

3.72% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia-Pacific (33.8% share, 2025) |

|

Second Largest Region |

North America (27.5% share, 2025) |

|

Leading Product Type |

Fully Automatic (72.9%, 2025) |

|

Leading Capacity Segment |

6.1 to 8 kg (41.8%, 2025) |

The global washing machine market growth trajectory from 2020 through 2034, with historical expansion to USD 58.82 Billion in 2025, reflects consistent household demand, while the forecast to USD 81.68 Billion captures accelerating smart appliance adoption, urbanization-led first-time buyer demand, and energy-efficiency regulations driving product upgrade cycles globally.

To get more information on this market, Request Sample

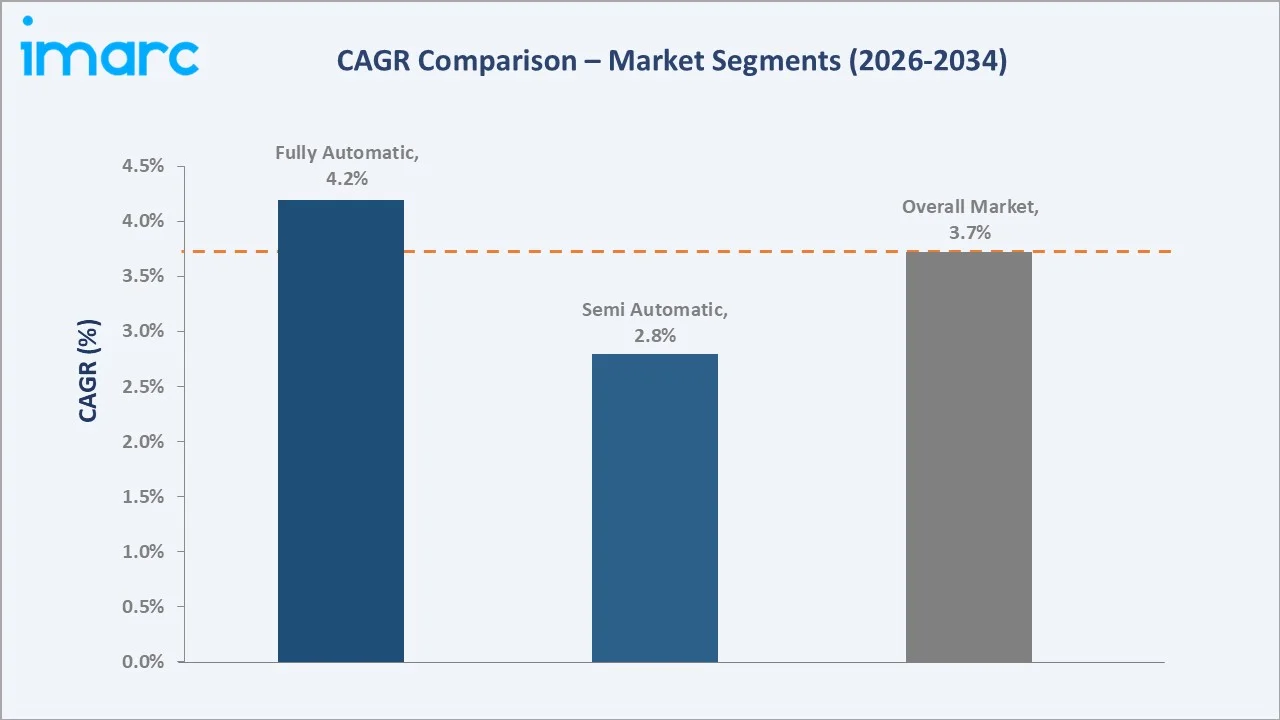

The CAGR trajectories across key product, capacity, and regional sub-segments, with the Above 8 kg capacity segment at ~4.5% CAGR and fully automatic machines at ~4.2% CAGR, are the fastest-growing categories within the global washing machine industry through 2034.

Executive Summary

The global washing machine market is on a sustained growth trajectory from USD 58.82 Billion in 2025 to USD 81.68 Billion by 2034. Washing machines, essential household and commercial appliances for textile cleaning, benefit from non-discretionary demand driven by urbanization, rising incomes, and hygiene awareness across all major global markets.

Fully automatic washing machines dominate at 72.9% in 2025, driven by consumer preference for convenience, preset wash programs, and AI-enabled fabric care. Semi-automatic machines (18.4%) retain adoption in price-sensitive emerging markets.

The 6.1 to 8 kg capacity segment leads at 41.8%, catering to the needs of medium-sized family households across major consumer markets.

Asia-Pacific (33.8%) dominates regionally, reflecting China's manufacturing scale and India's rapidly expanding urban consumer base. North America (27.5%) and Europe (23.4%) follow, driven by premium smart appliance adoption and regulatory compliance requirements compelling replacement of lower-efficiency washing machines with Energy Star and EU Eco-Design-rated models.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

Fully Automatic - 72.9% share (2025) |

|

Second Product Type |

Semi-Automatic - 18.4% share (2025) |

|

Leading Capacity |

6.1 to 8 kg - 41.8% share (2025) |

|

Leading Region |

Asia-Pacific - 33.8% share (2025) |

|

Second Largest Region |

North America - 27.5% share (2025) |

|

Top Companies |

Electrolux, Alliance Laundry System LLC, Godrej Enterprises, Haier Inc., IFB Industries Limited, LG Electronics, Mirc Electronics Limited, Panasonic Corporation, Robert Bosch GmbH, Samsung, Whirlpool Corporation |

Key Analytical Observations Expanding On The Above Data:

- Fully Automatic Dominance: Fully automatic washing machines, with 72.9% in 2025, dominate as rising incomes and consumer time-efficiency preferences drive households toward automated laundry solutions with intelligent wash programming and smart home connectivity.

- 6.1 to 8 kg Capacity Leadership: The 6.1 to 8 kg segment, with 41.8% in 2025, leads by optimally serving medium-sized families of three to five members, balancing water and energy efficiency with adequate daily laundry load capacity across all major regions.

- Asia-Pacific's Regional Leadership: Asia-Pacific's 33.8% dominance reflects China's position as the world's largest appliance manufacturer and India's rapidly expanding urban middle class driving first-time buyer demand at scale.

- North America Premium Segment: North America, with 27.5% in 2025, benefits from high average selling prices driven by premium smart appliance adoption, IoT integration requirements, and regulatory mandates under ENERGY STAR programs compelling periodic replacement.

Global Washing Machine Market Overview

A washing machine is a household or commercial appliance designed to wash laundry through mechanical action, water, and detergent. Products range from basic single-tub manual washers to fully integrated smart appliances with Wi-Fi connectivity, AI fabric sensing, automatic detergent dosing, and app-based remote control. Product categories are defined by automation level, load configuration (top-load vs front-load), drum capacity, spin speed, energy label rating, and smart connectivity features.

The global ecosystem integrates steel and polymer raw material suppliers, motor and electronic component OEMs, appliance assembly manufacturers, logistics and distribution networks, e-commerce platforms, organized retail chains, after-sales service providers, and energy regulation bodies, spanning residential, commercial laundry, hospitality, and healthcare end-use sectors across all major global geographies.

Market Dynamics

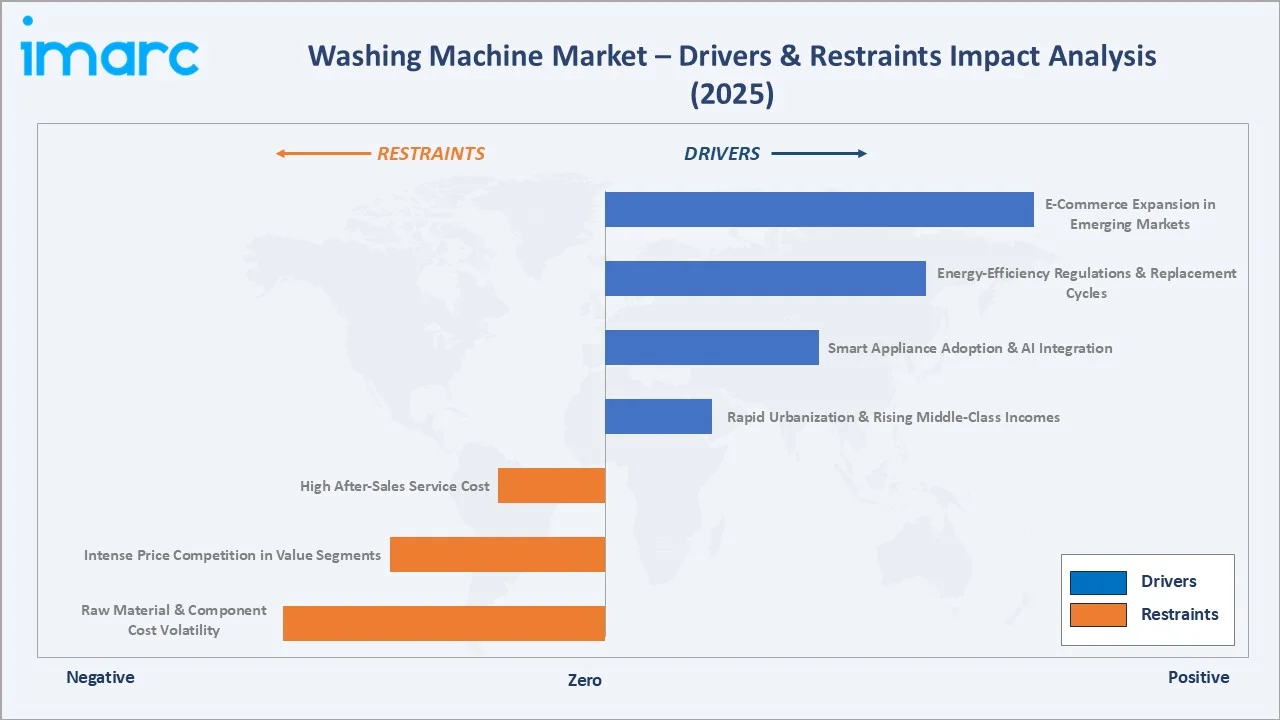

Market Drivers

- Rapid Urbanization and Rising Middle-Class Incomes: Rapid urbanization across Asia-Pacific and Latin America is expanding the addressable household appliance market, with urban households 3-4x more likely to own a washing machine versus rural counterparts, adding millions of first-time buyers annually. By 2030, China and India together will account for 66% of the world middle class population, thereby increasing the demand of washing machines in the market.

- Smart Appliance Adoption and AI Integration: Consumer preference for fully automatic washers with AI fabric sensors, intelligent wash optimization, and smartphone-integrated control panels is accelerating product upgrade cycles and average selling price inflation across all major markets.

- Energy-Efficiency Regulations and Replacement Cycles: ENERGY STAR (North America), EU Eco-Design Directive, and India BEE star rating mandates are compelling consumers to replace older, less efficient models with energy-rated units, generating sustained replacement demand above organic household formation rates.

Market Restraints

- Raw Material and Component Cost Volatility: Volatile steel, copper, and semiconductor component pricing increases the bill-of-materials cost for manufacturers, compressing margins especially in price-competitive emerging market value segments where price elasticity is high.

- Intense Price Competition in Value Segments: Intense pricing competition from Chinese and domestic manufacturers in value-segment washing machines, particularly in India and Southeast Asia, is constraining margin expansion for established global brands in the fastest-growing emerging markets.

Market Opportunities

- Smart Home Ecosystem Integration: Smart home ecosystem integration with platforms such as Amazon Alexa, Google Home, and Apple HomeKit is creating premium product differentiation opportunities and expanding the IoT-connected washing machine addressable market significantly.

- E-Commerce Channel Expansion in Emerging Markets: The rapid expansion of e-commerce in India, Southeast Asia, and Brazil is removing geographic distribution barriers, enabling brands to reach tier-2 and tier-3 city consumers through digital-first purchasing experiences and targeted marketing.

Market Challenges

- Water Conservation and Sustainability Regulations: Water scarcity concerns and regulatory pressure for reduced-water-consumption appliances require significant R&D investment in water-recycling and ultra-low water consumption washing technologies, raising development costs for manufacturers.

- High After-Sales Service Costs: Extended warranty periods and rising after-sales service costs in developing markets increase total ownership cost perception and reduce replacement frequency in value-sensitive consumer segments with limited disposable income.

Emerging Market Trends

1. AI and Machine Learning Integration Redefining Laundry Performance

AI-powered washing machines using fabric recognition sensors, load-weight detection, and water hardness measurement are enabling fully automated wash cycle optimization. Samsung's AI DD and LG's AI Direct Drive technologies demonstrate commercial viability of machine-learning laundry, reducing energy consumption by 15-20% versus conventional fully automatic models, while improving fabric protection outcomes.

2. Front-Load Premium Segment Expansion

Front-load washing machines, with superior cleaning performance, higher spin speeds, and lower water consumption versus top-load models, are gaining share across urban households in Asia-Pacific, Europe, and North America, supported by declining price premiums as manufacturing scale increases and consumer education improves regarding lifecycle cost advantages.

3. Washer-Dryer Combo Adoption in Space-Constrained Urban Markets

Washer-dryer combination appliances are gaining traction in compact urban apartments across Japan, South Korea, European cities, and high-density urban centers, where separate washer and dryer placement is impractical, driving premium pricing and meaningful margin expansion for manufacturers targeting urbanization-driven demographic shifts.

4. Water and Energy Efficiency Innovation as Competitive Differentiator

Eco-bubble technology, steam wash cycles, and cold-water detergent activation systems are progressively reducing energy consumption per wash cycle by 30-40%, enabling brands to meet tightening EU Eco-Design and US Department of Energy efficiency standards while commanding premium positioning in increasingly sustainability-aware consumer segments.

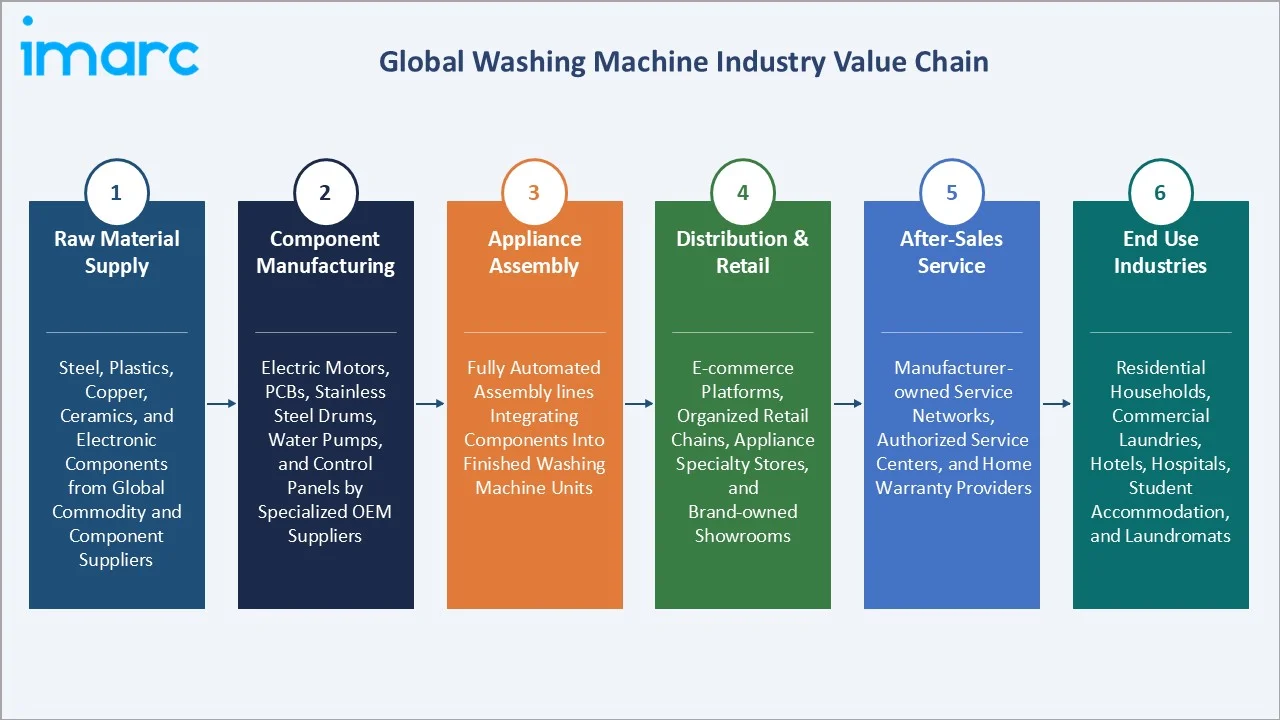

Industry Value Chain Analysis

The washing machine value chain spans six stages from raw material sourcing through end-user operation. Appliance assembly, embedded software development, and after-sales service capture the highest value-add margins, while distribution logistics and marketing investment generate significant working capital requirements favoring large, well-capitalized global OEMs over smaller regional players.

|

Stage |

Key Activities / Examples |

|

Raw Material Supply |

Steel, plastics, copper, ceramics, and electronic components from global commodity and component suppliers |

|

Component Manufacturing |

Electric motors, printed circuit boards, stainless steel drums, water pumps, and control panels produced by specialized OEM suppliers |

|

Appliance Assembly |

Fully automated assembly lines operated by major manufacturers integrating components into finished washing machine units |

|

Distribution & Retail |

E-commerce platforms, organized retail chains, appliance specialty stores, and brand-owned showrooms |

|

After-Sales Service |

Manufacturer-owned service networks, authorized service centers, independent technicians, and home warranty providers |

|

End Use Industries |

Residential households, commercial laundries, hotels, hospitals, student accommodation, and laundromats |

Vertically integrated manufacturers with captive component procurement, in-house motor production, and proprietary software platforms, such as Samsung Electronics and LG Electronics, achieve structural cost and product differentiation advantages over pure-play assemblers relying entirely on third-party component sourcing across global supply chains.

Technology Landscape in the Washing Machine Industry

Motor Technology: Direct Drive and Inverter Motor Systems

Direct Drive motor technology, pioneered commercially by LG Electronics, eliminates the belt-and-pulley drive system by mounting the motor directly to the drum, reducing vibration, noise, energy consumption, and failure rates. Inverter motor technology, now widely adopted across premium and mid-market fully automatic washing machines globally, enables variable speed operation that optimizes wash performance and power consumption dynamically.

Smart Connectivity: IoT, Wi-Fi, and App Integration

Wi-Fi-enabled washing machines with companion smartphone applications allow remote operation, wash cycle monitoring, push-notification alerts, and over-the-air software updates. Integration with Amazon Alexa, Google Home, and Apple HomeKit is enabling voice-command laundry initiation and smart home routine integration, increasingly demanded by premium segment consumers in North America, Europe, and urban Asia-Pacific markets.

Water and Energy Efficiency: Eco-Bubble and Steam Technology

Samsung's EcoBubble technology dissolves detergent in air before water enters the drum, enabling effective cold-water washing at temperatures that reduce fabric damage and energy consumption. Steam wash cycles penetrate fabric fibers at the microscopic level, sanitizing garments without full hot-water immersion, meeting both energy-efficiency mandates and consumer demand for hygienic textile care.

Market Segmentation Analysis

The report includes following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Fully Automatic |

72.9% |

2025 |

|

Technology |

Smart Connected |

🔒 |

2025 |

|

Capacity |

6.1 to 8 kg |

41.8% |

2025 |

|

Application |

Hospitatlity |

53.8% |

2025 |

| End Use | Commercial | 51.2% | 2025 |

|

Region |

Asia Pacific |

33.8% |

2025 |

By Product

Fully automatic washing machines command a 72.9% majority share in 2025, driven by increasing consumer preference for convenience, time savings, and the declining price premium of fully automatic over semi-automatic models in emerging markets. The penetration of fully automatic machines is accelerating fastest in India, Southeast Asia, and Latin America as urban income levels rise, organized retail expands, and e-commerce reduces access barriers for first-time buyers.

To access detailed market analysis, Request Sample

Semi-automatic washing machines (18.4%) in 2025 retain strong adoption in price-sensitive rural and semi-urban markets across India, Bangladesh, and Sub-Saharan Africa, where their lower purchase price, simpler maintenance requirements, and water-supply flexibility provide practical advantages over fully automatic alternatives. Dryers (8.7%) represent a growing premium sub-segment expanding fastest in Europe and North America.

By Capacity

The 6.1 to 8 kg capacity segment leads with 41.8% share in 2025, representing the optimal balance between household laundry requirements for medium-sized families and energy and water efficiency performance. This capacity range dominates urban household purchases across Asia-Pacific, Europe, and North America, matching typical family sizes of three to five members who require sufficient drum capacity for daily laundry loads without excessive water or energy waste.

Above 8 kg (32.5%) in 2025 is the fastest-growing capacity segment, driven by large-family adoption in China and India, commercial laundry applications in hotels and hospitals, and the trend toward fewer, larger wash loads to optimize energy and water consumption per kilogram of laundry cleaned.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia-Pacific |

33.8% |

Rising middle-class incomes; rapid urbanization; China and India household appliance demand |

|

North America |

27.5% |

Premium smart appliance adoption; ENERGY STAR-driven replacement cycles; high ASP market |

|

Europe |

23.4% |

EU Eco-Design Directive compliance; front-load premium penetration; sustainability mandates |

|

Latin America |

8.7% |

Brazil and Mexico urbanization; growing disposable income; first-time buyer demand |

|

Middle East & Africa |

6.6% |

GCC hospitality sector growth; rising household appliance penetration; urban expansion |

Asia-Pacific's 33.8% market dominance in 2025 is driven by China's position as both the world's largest washing machine manufacturer and its largest consumer market, combined with India's accelerating first-time buyer demand fueled by urbanization, rising household incomes, and government-led rural electrification programs expanding the addressable appliance market to previously underserved consumer segments.

North America, with 27.5% in 2025, is experiencing sustained demand driven by smart appliance adoption, ENERGY STAR-driven replacement cycles, and premium washer-dryer combo penetration in urban apartment markets.

Europe (23.4%) is shaped by the EU Eco-Design Directive, compelling trade-up to A-rated efficient front-loaders and accelerating premiumization of the installed base across Western and Central European markets.

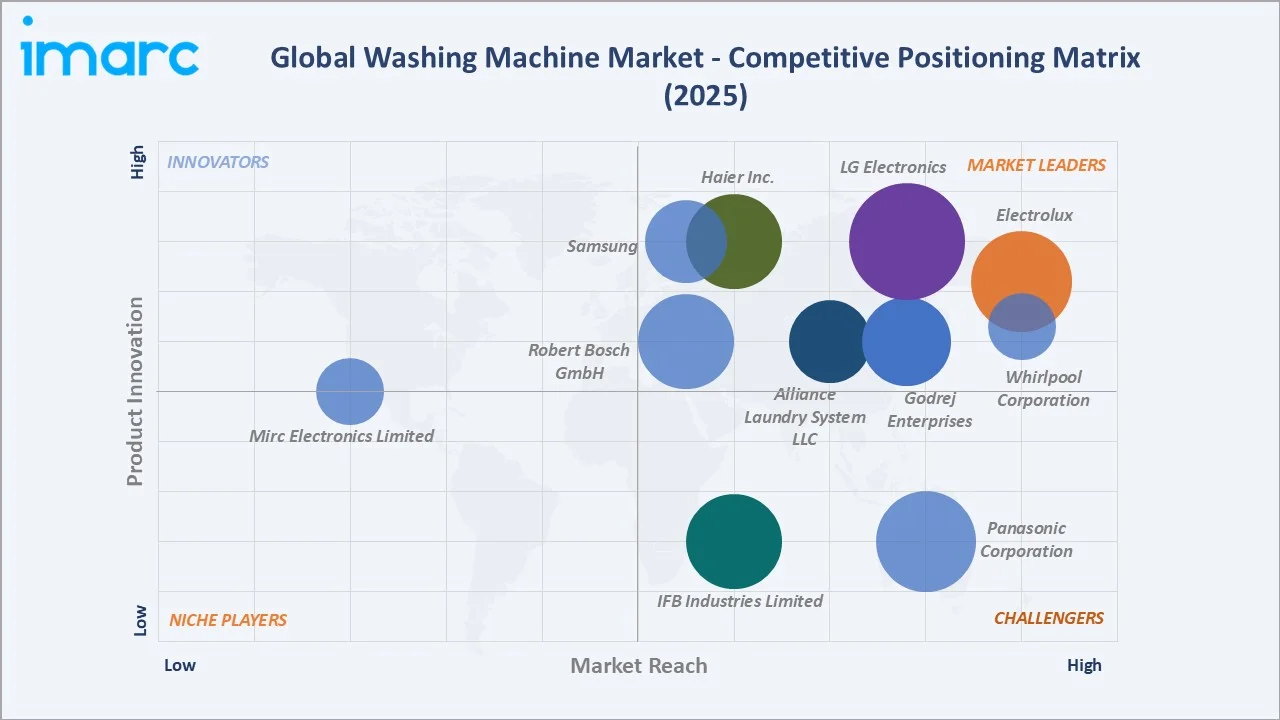

Competitive Landscape

The global washing machine market is moderately concentrated, with leading players holding dominant positions in their home markets while competing globally.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

|

Electrolux |

Front-load Washing Machines |

Leader |

European premium; eco-design and sustainability leadership |

|

Alliance Laundry System LLC |

Speed Queen, UniMac, Huebsch |

Leader |

US commercial laundry; vended and multi-housing segments |

|

Godrej Enterprises |

Fully automatic and semi-automatic |

Leader |

India market leader; value and semi-automatic segments |

|

Haier Inc. |

Top-load, front-load, Semi-automatic |

Leader |

Asia-Pacific and global scale; GE Appliances; IoT integration |

|

IFB Industries Limited |

Front-load and top-load washers |

Challenger |

India premium front-load specialist; strong service network |

|

LG Electronics |

Front-load and top-load washers |

Leader |

Global premium; Direct Drive motor; AI laundry optimization |

|

Mirc Electronics Limited |

Onida semi-automatic and fully automatic |

Emerging |

India mid-market; value pricing; regional distribution |

|

Panasonic Corporation |

Fully automatic and semi-automatic washers |

Challenger |

Japan and Asia-Pacific; Nano Aqua technology; energy focus |

|

Robert Bosch GmbH |

Front-load machines |

Leader |

Europe premium; Home Connect smart integration; i-DOS tech |

|

Samsung |

Fully automatic and semi-automatic washers |

Leader |

Global premium; AI-powered; SmartThings ecosystem leader |

|

Whirlpool Corporation |

Fully automatic and semi-automatic washers |

Leader |

North America leader; multi-brand; smart laundry portfolio |

Key players include Electrolux, Alliance Laundry System LLC, Godrej Enterprises, Haier Inc., IFB Industries Limited, LG Electronics, Mirc Electronics Limited, Panasonic Corporation, Robert Bosch GmbH, Samsung, Whirlpool Corporation, and others.

Key Company Profiles

Samsung

Samsung is a global leader in premium washing machines, offering AI-powered EcoBubble, Bespoke AI, and QuickDrive series with smart home connectivity and superior energy efficiency. Samsung commands a leading share in the premium fully automatic segment across Asia-Pacific, North America, and Europe, leveraging the SmartThings ecosystem to create appliance stickiness and cross-category purchasing.

- Product Portfolio: Fully automatic and semi-automatic washers

- Recent Developments: In January 2025, Samsung India expanded its Bespoke AI Laundry Series with 9 kg front-load washing machines featuring AI Energy Mode, AI Control, and Hygiene Steam technology designed for modern Indian households.

- Strategic Focus: Samsung's washing machine strategy centers on AI feature leadership, SmartThings ecosystem integration, and premium product differentiation to defend margin in increasingly price-competitive global markets while expanding addressable share in India and Southeast Asia.

LG Electronics

LG Electronics is a global washing machine leader known for its Direct Drive motor technology delivering quiet operation, superior vibration control, and extended appliance lifespan. LG's AI Direct Drive, EZDispense automatic detergent dosing, and TurboWash technologies position it as the premium energy-efficiency and fabric-care leader across all major global markets.

- Product Portfolio: Front-load and top-load washers

- Recent Developments: In December 2025, LG Electronics expanded its home appliance portfolio in India with the launch of a new range of AI-powered washing machines featuring its upgraded AI DD 2.0 technology. The lineup, comprising multiple models across front-load, top-load, and washer-dryer categories, is designed to deliver enhanced fabric care by automatically detecting fabric type, weight, and soil levels to optimize wash cycles.

- Strategic Focus: LG focuses on Direct Drive motor technology differentiation, AI-powered laundry optimization, and smart home connectivity to maintain premium positioning across North America, Europe, and Asia-Pacific, with growing investment in front-load segment penetration in India.

Haier Inc.

Haier is the world's largest home appliance company by volume, operating globally through the Haier, Aqua, GE Appliances, and Candy brands. Haier's multi-brand strategy enables simultaneous competition across premium, mid-market, and value segments globally, with strength in Asia-Pacific and growing North American share through the GE Appliances portfolio acquisition.

- Product Portfolio: Top load, front-load, Semi-automatic machines

- Recent Developments: In April 2026, Haier launched its new F11 washing machine series in India, introducing an AI-powered, feature-rich solution designed to enhance laundry convenience, hygiene, and efficiency for modern households. The range incorporates advanced technologies such as Ultra Fresh Air, which keeps clothes fresh and odor-free for extended periods after a wash cycle, along with a full AI color touch panel that simplifies user interaction.

- Strategic Focus: Haier leverages its multi-brand portfolio and manufacturing scale to compete across all price segments simultaneously, using GE Appliances to strengthen North American premium share while leveraging cost structures to compete aggressively in Asia-Pacific and emerging markets.

Whirlpool Corporation

Whirlpool Corporation is the leading washing machine brand in North America, operating through the Whirlpool, Maytag, and KitchenAid brands. Whirlpool's multi-brand portfolio spans premium (KitchenAid), mid-market (Whirlpool), and reliability-focused (Maytag) consumer segments, enabling comprehensive coverage of the North American residential and light commercial laundry market with differentiated positioning at each price tier.

- Product Portfolio: Fully automatic and semi-automatic washers

- Recent Developments: In September 2024, Whirlpool Corporation has introduced an innovation in its latest smart front-load washers with the launch of the FreshFlow Vent System. This system is designed to address common issues with front-load machines, particularly moisture buildup and odors, by helping keep both the washer and clothes fresh.

- Strategic Focus: Whirlpool focuses on North American market leadership through its multi-brand portfolio, national service network, and connected appliance investment, while pursuing margin expansion in premium smart laundry and washer-dryer combination segments in urban apartment markets.

Market Concentration Analysis

The global washing machine market is moderately concentrated at the global level, with no single company holding more than 10-12% of total global revenue. Asia-Pacific, representing 33.8% of the market, is served primarily by South Korean, Chinese, and Japanese manufacturers, while North American and European markets have their own distinct competitive ecosystems centered on established brands with decades of consumer trust.

Consolidation is advancing through strategic acquisitions, with Haier's GE Appliances acquisition representing the most significant cross-regional consolidation event in the market. Premium segment consolidation is being driven by smart appliance ecosystem investments that favor large, technology-investing incumbents over smaller regional manufacturers with limited R&D budgets for AI and IoT feature development.

Investment & Growth Opportunities

Fastest-Growing Segments

The Above 8 kg capacity segment at ~4.5% CAGR through 2034 is the highest-growth segment, driven by large-family adoption and commercial laundry expansion in emerging markets. Fully automatic smart washing machines with AI fabric sensing and IoT connectivity represent the highest-margin investment opportunity across all major global markets, commanding substantial price premiums over conventional models.

Emerging Markets

India at ~4.4% CAGR through 2034 is the fastest-growing individual country market, driven by rising incomes, urban migration, government rural electrification, and organized retail expansion. Southeast Asia (Indonesia, Vietnam, Philippines), Brazil, and Mexico represent additional high-growth frontiers for value-segment and mid-range fully automatic washing machines over the forecast period.

Venture & Investment Trends

Private equity interest in appliance component manufacturers, AI-enabled smart home management software platforms, and IoT connectivity middleware is growing. Water-recycling washing machine technology developers and AI laundry optimization startups are attracting venture investment as sustainability mandates tighten globally and consumer demand for environmental accountability in durable goods purchasing rises.

Future Market Outlook (2026-2034)

The global washing machine market is forecast to expand from USD 58.82 Billion in 2025 to USD 81.68 Billion by 2034 at a CAGR of 3.72%, adding USD 22.86 Billion in incremental annual market value over the forecast period. This sustained growth reflects non-discretionary household demand, rising emerging market penetration from urbanization, and smart appliance upgrade cycles in developed economies driven by regulatory efficiency mandates and consumer preference for intelligent home automation integration.

Three forces will most significantly shape the washing machine industry through 2034: AI-powered appliance management reaching 40-50% of premium washing machine sales by 2030; India and Southeast Asia first-time buyer demand adding 200-300 million addressable households; and energy and water efficiency regulatory mandates driving accelerated replacement cycles across North America and Europe, sustaining premium segment growth above GDP trends.

Research Methodology

Primary Research

Primary research encompassed structured interviews with washing machine industry stakeholders, including senior commercial managers at major appliance OEMs, retail channel executives, energy regulation specialists, and household appliance distribution professionals. Primary data validated market sizing, product segment shares, capacity distribution, regional demand estimates, and technology adoption timelines across all geographies covered in this report.

Secondary Research

Key secondary sources include UN World Urbanization Prospects, IEA Tracking Clean Energy Progress reports, ENERGY STAR certified appliance databases, EU Eco-Design Regulation documentation, AHAM (Association of Home Appliance Manufacturers) industry data, Statista global appliance market data, and company annual reports from Samsung Electronics, LG Electronics, Whirlpool Corporation, Haier Group Corporation, and AB Electrolux.

Forecasting Models

Market size estimations and growth projections were derived using top-down and bottom-up forecasting models, incorporating GDP growth rates, urbanization indices, household formation data, income elasticity of appliance demand, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic uncertainty and regulatory change scenarios.

Washing Machine Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered |

|

| Technologies Covered | Smart Connected, Conventional |

| Capacities Covered | Below 6 kg, 6.1 to 8 kg, Above 8 kg |

| Applications Covered | Healthcare, Hospitality, Others |

| End Uses Covered | Commercial, Residential |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Electrolux, Alliance Laundry System LLC, Godrej Enterprises, Haier Inc., IFB Industries Limited, LG Electronics, Mirc Electronics Limited, Panasonic Corporation, Robert Bosch GmbH, Samsung, Whirlpool Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the washing machine market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global washing machine market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the washing machine industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Washing Machine Market Report

The global washing machine market size reached USD 58.82 Billion in 2025, supported by consistent household demand growth driven by urbanization, rising disposable incomes, and the accelerating adoption of smart and fully automatic washing machines in emerging economies.

The market is projected to reach USD 81.68 Billion by 2034, growing at a CAGR of 3.72% during 2026-2034, driven by Asia-Pacific urbanization, smart appliance upgrade cycles in developed markets, and energy-efficiency regulation-driven replacement demand in North America and Europe.

Fully automatic washing machines lead with a 72.9% product share in 2025, reflecting consumer preference for convenience, automated wash programming, and intelligent fabric care features that eliminate the need for manual intervention at any stage of the laundry process.

The 6.1 to 8 kg capacity segment leads with a 41.8% share in 2025, optimally serving medium-sized family households of three to five members, offering an efficient balance between daily laundry load capacity and energy and water consumption per cycle across all major markets.

Asia-Pacific commands a dominant 33.8% market share in 2025, driven by China's position as the world's largest washing machine manufacturer, India's rapidly expanding urban middle-class first-time buyer demand, and high household appliance penetration rates across developed APAC economies.

The Above 8 kg capacity segment is the fastest-growing at approximately 4.5% CAGR through 2034, driven by large-family adoption in China and India, commercial laundry applications in hotels and hospitals, and consumer preference for fewer, larger wash loads to reduce total energy and water consumption.

Leading companies include Electrolux, Alliance Laundry System LLC, Godrej Enterprises, Haier Inc., IFB Industries Limited, LG Electronics, Mirc Electronics Limited, Panasonic Corporation, Robert Bosch GmbH, Samsung, Whirlpool Corporation, and others.

The principal growth drivers include rapid urbanization and rising middle-class incomes across Asia-Pacific and Latin America, accelerating smart and AI-enabled appliance adoption, energy-efficiency regulatory mandates compelling product upgrades, and e-commerce expansion removing distribution barriers in emerging markets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)