Seed Treatment Market Size, Share, Trends and Forecast by Type, Application Technique, Crop Type, Function, and Region, 2026-2034

Global Seed Treatment Market Size, Share, Trends & Forecast (2026-2034)

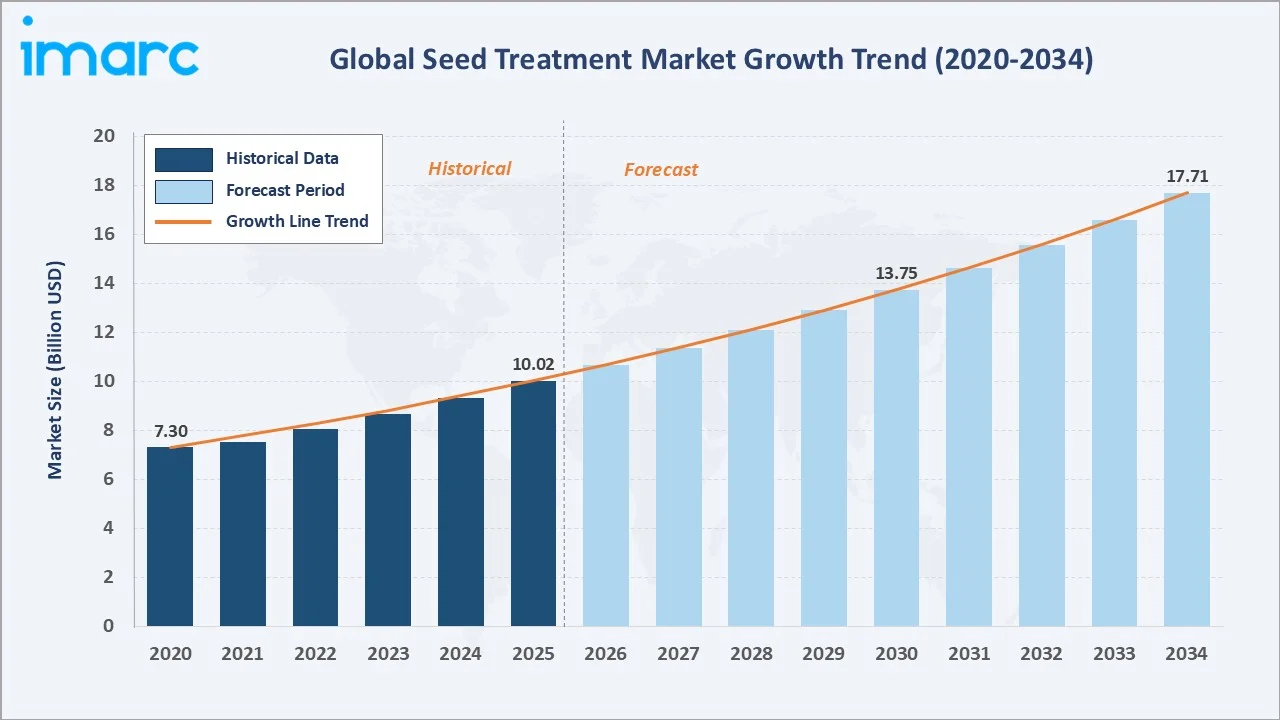

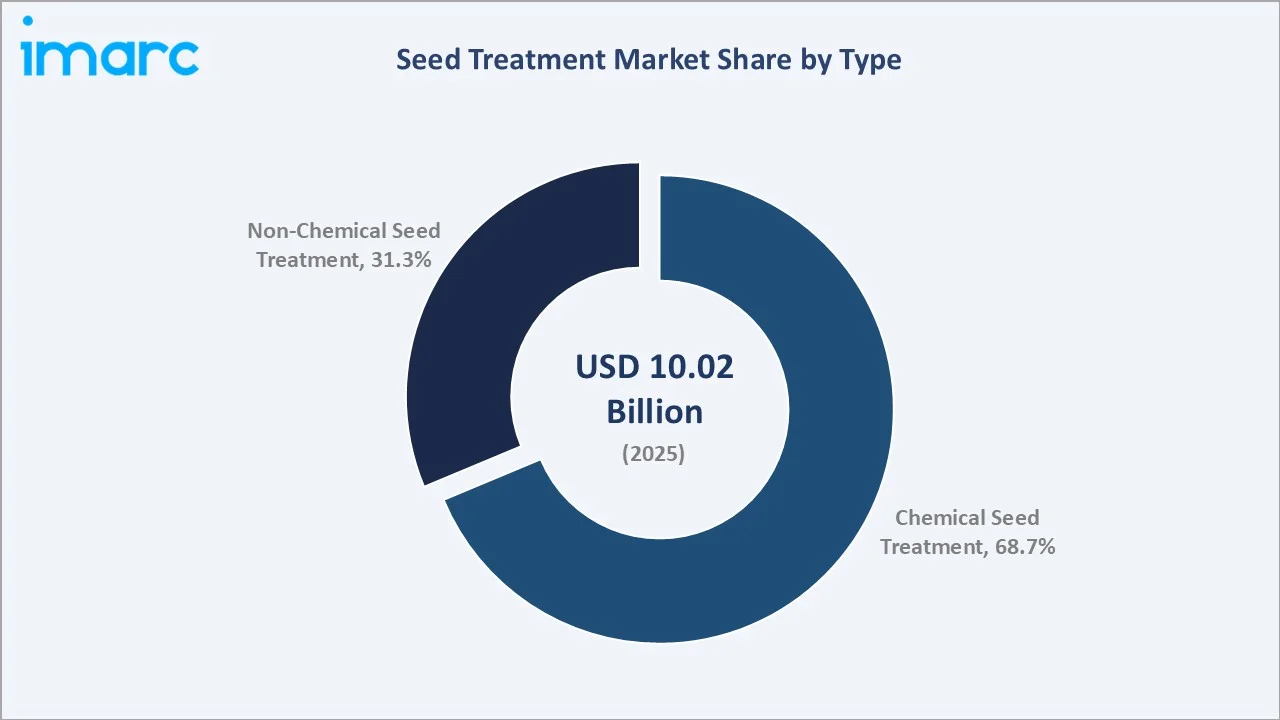

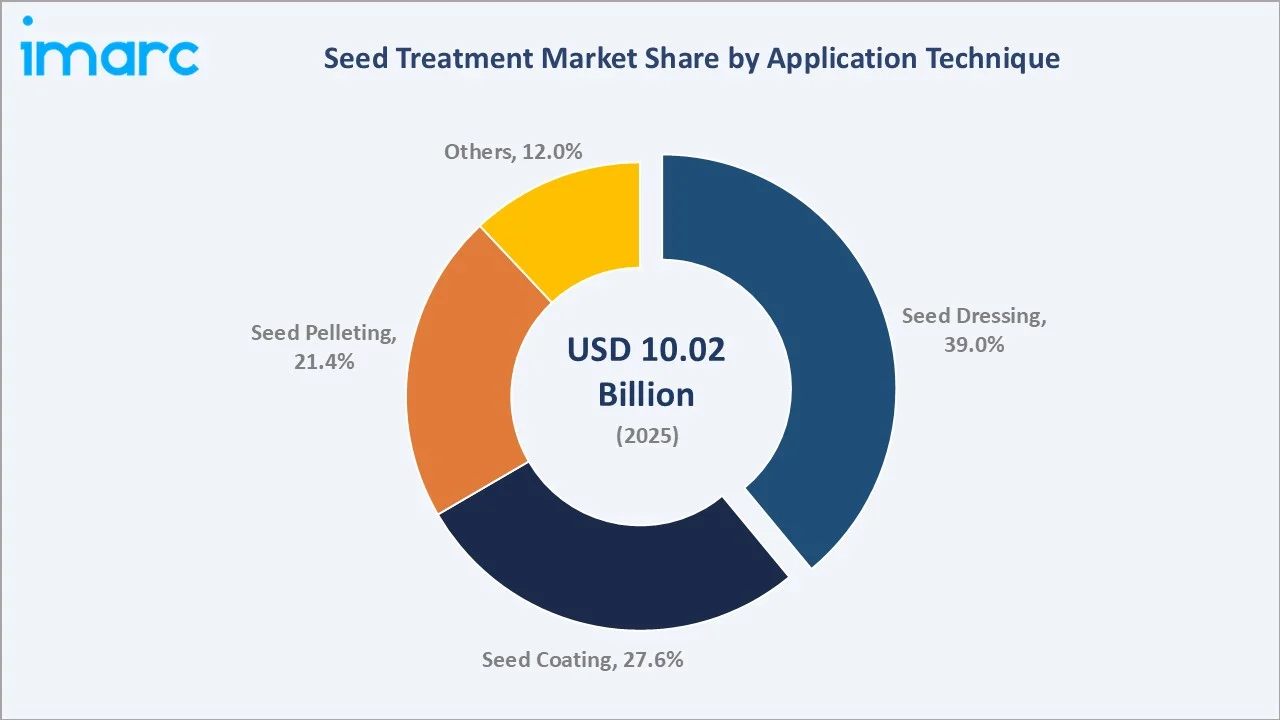

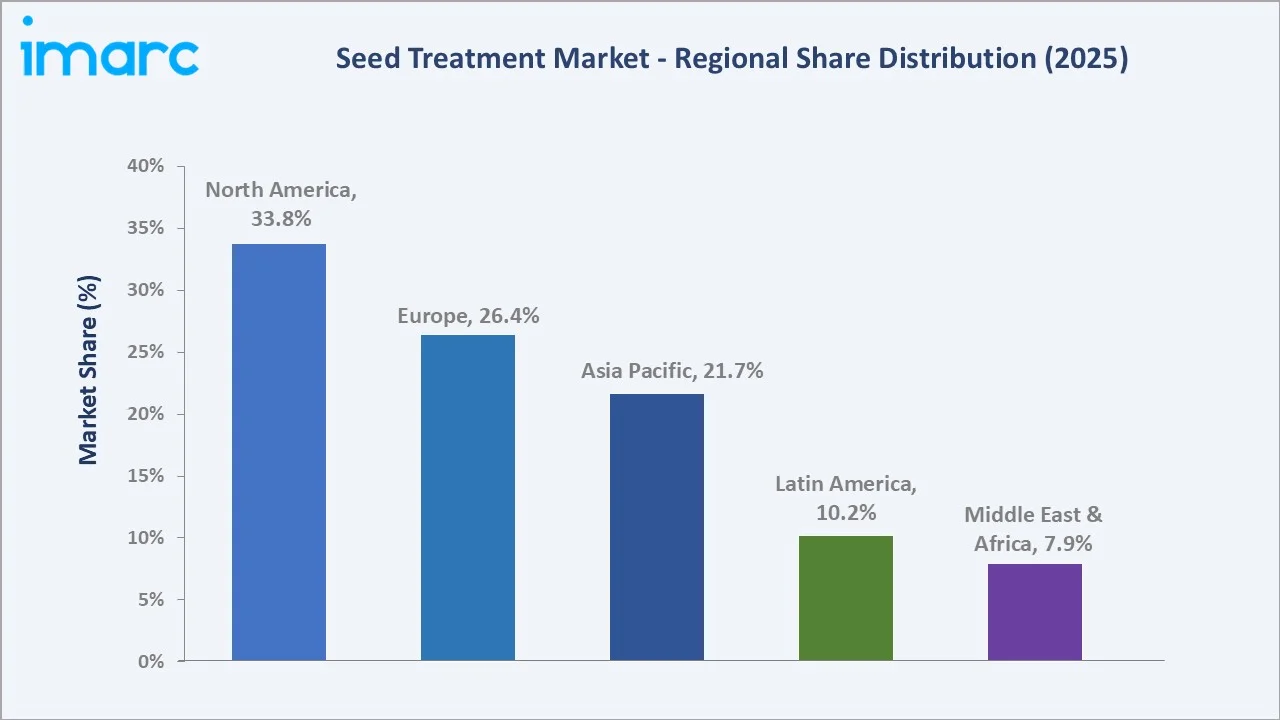

The global seed treatment market size was valued at USD 10.02 Billion in 2025 and is projected to reach USD 17.71 Billion by 2034, exhibiting a CAGR of 6.53% during the forecast period 2026-2034. Rising demand for high-yield hybrid seeds, biological formulation adoption, climate-driven pest pressure, and regulatory support for integrated pest management are driving growth. Chemical Seed Treatment leads the type segment at 68.7%, while Seed Dressing dominates the application technique segment at 39.0%. North America accounts for 33.8% of global revenue, the world's largest regional market.

Market Snapshot

The global seed treatment market growth trajectory from 2020 through 2034 contrasts a steady historical expansion base against a sustained forecast curve, powered by hybrid and GM seed penetration, biological formulation adoption, precision application equipment rollout, and rising treated acreage across major row crops.

|

Metric |

Value |

|

Market Size (2025) |

USD 10.02 Billion |

|

Forecast Market Size (2034) |

USD 17.71 Billion |

|

CAGR (2026-2034) |

6.53% |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (33.8%) |

|

Fastest Growing Region |

Asia Pacific |

To get more information on this market, Request Sample

Segment-level CAGR comparisons highlight Non-Chemical Seed Treatment and Seed Pelleting as the two fastest-growing categories within the global seed treatment industry analysis through 2034, reflecting regulatory tightening on synthetic chemistries and rising demand for precision sowing in high-value horticulture crops.

Executive Summary

The global seed treatment market is undergoing a structural transformation driven by the convergence of biological innovation, precision agriculture, and climate-resilient farming. Valued at USD 10.02 Billion in 2025, the market is forecast to reach USD 17.71 Billion by 2034 at a CAGR of 6.53%. The FAO estimated global cereal production crossed 2,850 million tons in 2024, with rising pest pressure making seed treatment a critical yield-protection layer across row crops.

Chemical Seed Treatment commands the dominant type share at 68.7% in 2025, anchored by broad regulatory approval and cost-effectiveness across US corn, Brazilian soybean, and European cereal acreage. Non-Chemical Seed Treatment at 31.3% is the fastest-growing category, fuelled by organic acreage crossing 96 million hectares globally.

North America dominates with a 33.8% share in 2025, led by the US, where approximately 90% of corn seed is treated before planting. Europe holds 26.4% and Asia Pacific 21.7%. Latin America's 10.2% share is driven by Brazilian soybean expansion, while the Middle East and Africa contribute 7.9%.

Key Market Insights

|

Insight |

Data |

|

Largest Type Segment |

Chemical Seed Treatment (68.7% in 2025) |

|

Leading Application Technique |

Seed Dressing (39.0% in 2025) |

|

Leading Region |

North America (33.8% in 2025) |

|

Fastest-Growing Segment |

Non-Chemical Seed Treatment |

|

Top Companies |

Bayer AG, Syngenta, BASF, Corteva, FMC Corporation |

|

Market Opportunity |

Biological formulations and precision application |

Key Analytical Observations Supporting the Above Data:

- Chemical Seed Treatment's 68.7% dominance in 2025 reflects its role as the default protection layer across over 300 million acres of US and Brazilian row crops.

- Seed Dressing leads at 39.0% in 2025, driven by low equipment requirements and direct-to-seed simplicity enabling broad farmer adoption.

- North America's 33.8% dominance reflects near-saturation treatment penetration in US corn and early precision equipment deployment.

- Non-Chemical Seed Treatment expands at above-market CAGR as Trichoderma, Bacillus, and Pseudomonas formulations enter mainstream deployment.

- The top five global players: Bayer AG, Syngenta, BASF, Corteva, and FMC Corporation are estimated to account for 55-60% of global revenue in 2025.

- Precision application and nanotechnology encapsulation enable up to 40% lower active ingredient use per seed.

Global Seed Treatment Market Overview

Seed treatment refers to the application of chemical, biological, or physical agents to seeds before sowing to protect germination, enhance early-stage vigour, and defend against soil-borne pests and diseases. Modern platforms combine fungicides, insecticides, nematicides, biologicals, and polymer coatings into integrated formulations applied at commercial facilities or on-farm equipment.

Applications span the full agricultural sector: corn, soybean, wheat, rice, cotton, canola, sugar beet, pulses, and high-value vegetable and horticulture seeds. Seed treatment is increasingly a non-discretionary input in commercial agriculture, given the premium cost of hybrid and GM seed varieties requiring protection from germination loss.

Macroeconomic enablers include global cereal production crossing 2,850 million tons in 2024, world population rising toward 8.5 billion by 2030, shrinking arable land per capita, and climate variability driving pest pressure. Government initiatives across the US, EU, China, India, and Brazil are accelerating registration pathways for advanced formulations.

Market Dynamics

To evaluate market opportunities, Request Sample

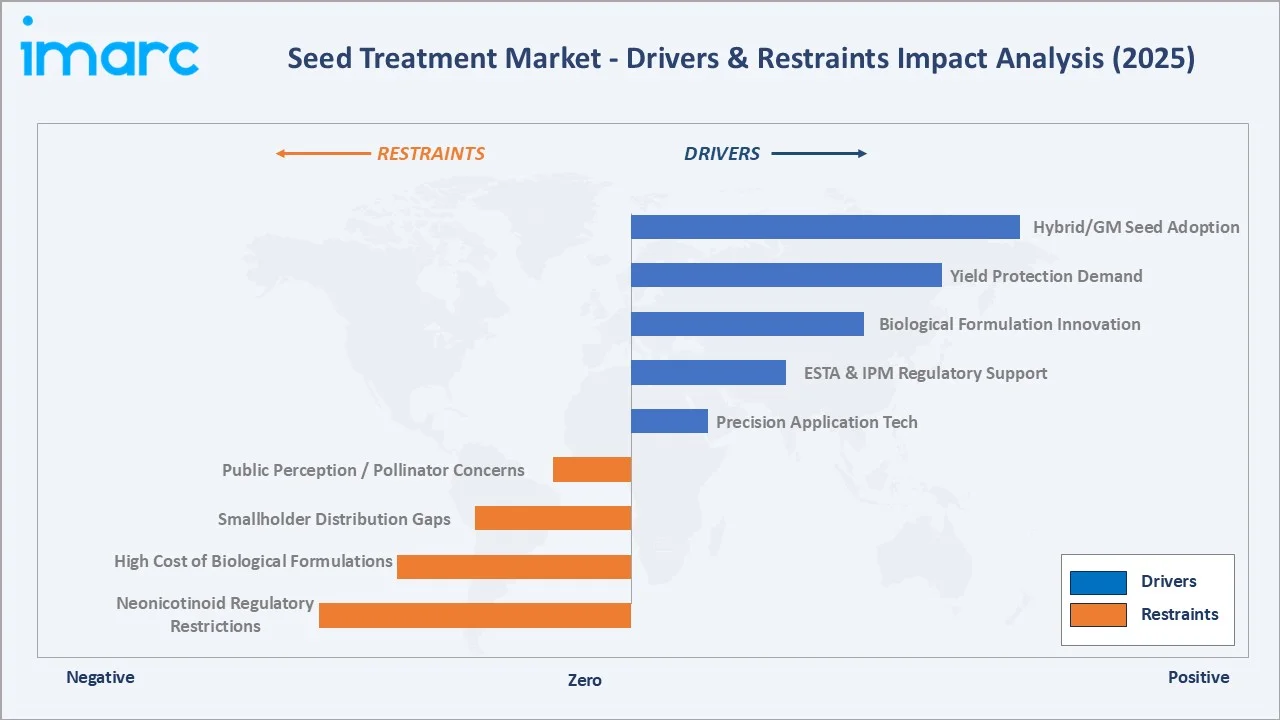

Market Drivers

- Rising Demand for Yield Protection Across Hybrid Seeds: Up to 30% of global rice yield is lost annually to fungal diseases such as rice blast, with similar pressure across corn, soybean, and wheat. Seed treatment reduces early-season losses by 15-25%, making it economically essential for premium hybrid and GM seed varieties costing 3-8 times more than conventional alternatives.

- Technological Advancements in Biological and Precision Treatments: Advancements in precision application, nanotechnology encapsulation, and biological formulations are transforming efficacy standards. In May 2024, Bee Vectoring Technologies advanced its Clonostachys rosea CR-7 biological agent for soybean seed treatment, illustrating the pace of biological innovation entering the market.

- Supportive Regulations and Government Programmes: Initiatives like the European Seed Treatment Assurance Scheme (ESTA) and integrated pest management mandates across North America are driving professionalisation of seed treatment. Government R&D funding across the US, EU, China, and India is accelerating product registration timelines for advanced formulations.

Market Restraints

- Regulatory Restrictions on Neonicotinoids: The European Union's 2018 ban on outdoor neonicotinoid use and ongoing US EPA reviews are constraining chemical seed treatment formulations. Manufacturers face higher reformulation costs and extended registration timelines, creating structural pricing pressure on chemical insecticide seed treatments.

- High Cost of Biological Formulations: Biological seed treatments typically cost 20-40% more per acre than conventional chemical alternatives. Cost sensitivity among smallholder farmers in South Asia and Sub-Saharan Africa slows biological adoption despite strong agronomic need, limiting emerging-market penetration.

Market Opportunities

- Precision Agriculture and Digital Traceability: Automated seed coating systems and cloud-connected traceability platforms are opening recurring-revenue service models for seed treatment companies partnering with precision agriculture providers such as Climate FieldView and John Deere Operations Center.

- Emerging Market Penetration in Asia Pacific and Latin America: Rising oilseed production in India, expanding Brazilian soybean acreage, and growing hybrid seed penetration across China create a structurally underpenetrated seed treatment opportunity for global and regional players.

Market Challenges

- Public Perception and Pollinator Concerns: Concerns about neonicotinoid impact on bee populations have intensified regulatory scrutiny across North America and Europe, requiring continuous stewardship investment and reformulation spending from global chemical seed treatment manufacturers.

- Fragmented Smallholder Distribution Channels: In South Asia and Sub-Saharan Africa, fragmented farm sizes, limited commercial treatment infrastructure, and informal seed distribution channels constrain market penetration despite strong agronomic need for seed protection inputs.

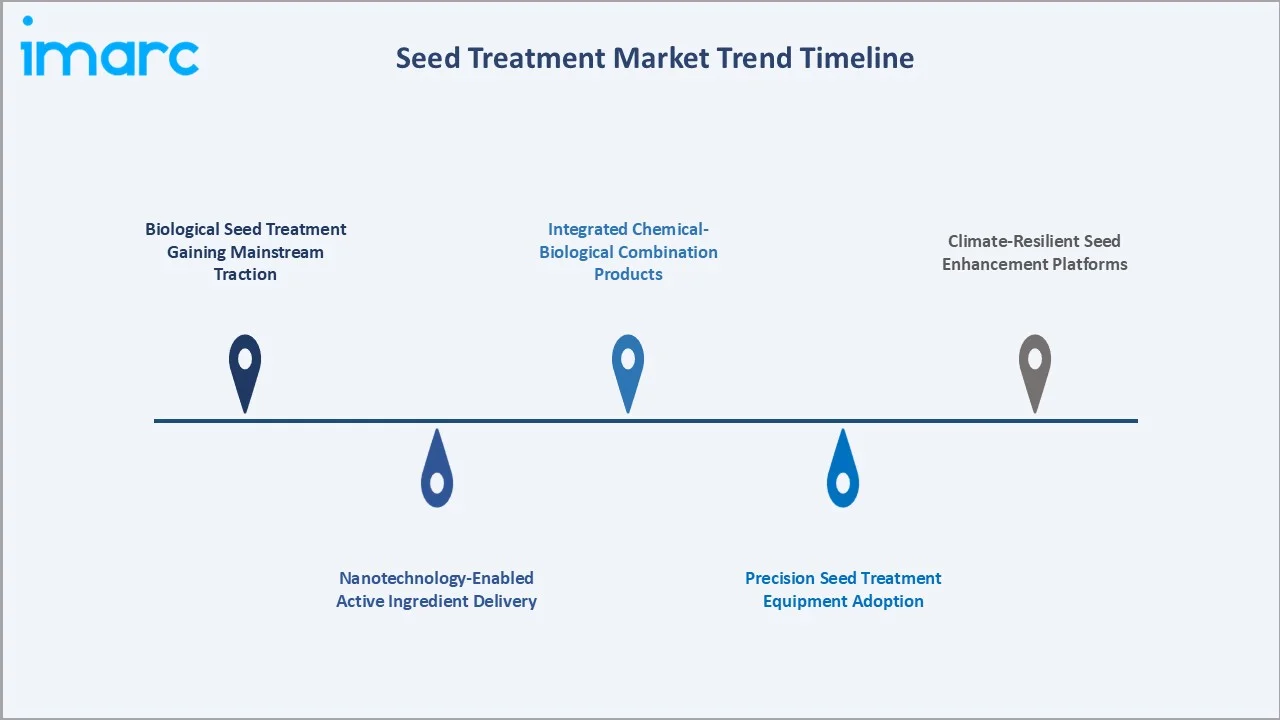

Emerging Market Trends

1. Biological Seed Treatment Gaining Mainstream Traction

Biological agents, including Trichoderma, Bacillus subtilis, and Pseudomonas strains, are moving from niche to mainstream deployment. In January 2025, UPL Corp launched ATROFORCE, a Trichoderma atroviride bionematicide for cotton, underscoring the shift toward microbial-first formulations.

2. Nanotechnology-Enabled Active Ingredient Delivery

Nano-encapsulation allows active ingredients to release gradually as seeds germinate, improving efficacy by up to 35% while reducing active ingredient use by 30-40%. The trend is attracting R&D investment from Bayer, Syngenta, and BASF.

3. Precision Seed Treatment Equipment Adoption

Automated closed-loop treatment equipment with optical verification and cloud-connected application logs is becoming standard across commercial facilities in North America and Europe, improving uniformity by over 20% versus legacy systems.

4. Integrated Chemical-Biological Combination Products

Combination products pairing chemical fungicides with biological inoculants are emerging as a premium category, addressing immediate pest pressure and long-term soil microbiome health. Early 2024-2025 launches show strong farmer acceptance at premium price points.

5. Climate-Resilient Seed Enhancement Platforms

In February 2024, SaliCrop pioneered a climate-smart seed enhancement technology for abiotic stress tolerance in arid regions, reflecting a broader shift toward resilience-focused platforms.

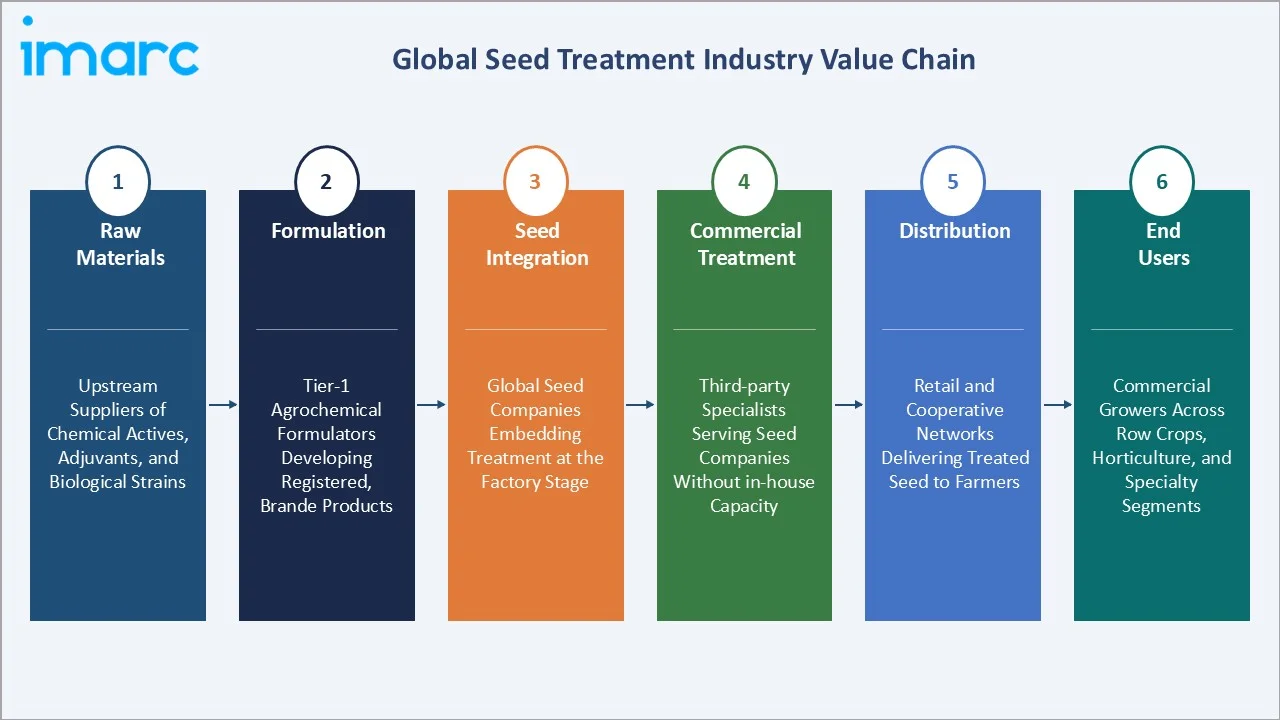

Industry Value Chain Analysis

The seed treatment value chain spans six integrated stages from active ingredient supply through end-user farmer adoption. Active ingredient manufacturers occupy the upstream position, supplying chemical molecules and microbial strains to formulation companies. Formulators include the highest strategic value by combining actives, coatings, and adjuvants into regulated branded products with multi-country registration.

Seed companies increasingly integrate seed treatment at the factory level, capturing a premium margin through pre-treated offerings. Commercial treatment facilities and on-farm treaters serve smaller seed companies and growers without in-house capacity. Downstream distribution flows through agricultural retailers, cooperatives, and direct-to-farm channels to end-user farmers.

|

Stage |

Key Players |

|

Raw Materials |

Upstream suppliers of chemical actives, adjuvants, and biological strains |

|

Formulation |

Tier-1 agrochemical formulators developing registered, branded products |

|

Seed Integration |

Global seed companies are embedding treatment at the factory stage. |

|

Commercial Treatment |

Third-party specialists serving seed companies without in-house capacity |

|

Distribution |

Retail and cooperative networks delivering treated seed to farmers |

|

End Users |

Commercial growers across row crops, horticulture, and specialty segments |

Technology Landscape in the Seed Treatment Industry

Biological Formulation Technology: Microbial Strains and Shelf-Life Innovation

The biological seed treatment landscape is undergoing rapid maturation. Microbial inoculants dominate the stack, with Trichoderma, Bacillus subtilis, and rhizobia species leading commercial deployment. Formulation shelf-life, a historical constraint, is improving with new stabilisation techniques enabling 24+ month product shelf life in 2025, expanding global distribution feasibility.

Precision Application Equipment and Automation

Closed-loop batch treaters and in-line dosing systems reduce operator exposure while improving active ingredient uniformity on the seed coat. Adoption is approaching saturation across US and European commercial treatment facilities by 2025. Bayer, Syngenta, and Incotec are investing in next-generation equipment with optical verification and cloud-based QA dashboards.

Nanotechnology and Encapsulation Platforms

Polymer-based and lipid-based nano-carriers enable sustained release of active ingredients during germination, reducing environmental runoff and improving efficacy per milligram of active ingredient applied. The technology is transitioning from research to commercial deployment in premium formulations through 2028.

Digital Traceability and IoT-Connected Treatment

Cloud-connected treatment equipment with real-time application logs, batch traceability, and regulatory reporting is entering mainstream deployment, supporting ESTA compliance in Europe, EPA reporting in the US, and emerging requirements across Latin America and the Asia Pacific.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Type | Chemical Seed Treatment |

68.7% |

2025 |

| Application Technique | Seed Dressing |

39.0% |

2025 |

| Crop Type | Corn/Maize |

31.8% |

2025 |

| Function | Seed Protection |

38.7% |

2025 |

|

Region |

North America |

33.8% |

2025 |

.webp)

By Type

Chemical Seed Treatment commands a 68.7% majority share in 2025, reflecting its established role as the default protection layer for global row crops. The segment benefits from broad regulatory approval, cost-effectiveness at scale, and strong distribution supporting US corn, Brazilian soybean, and European cereal acreage. Chemical formulations provide broad-spectrum protection against fungi, insects, and nematodes at farmer-accessible price points.

To access detailed market analysis, Request Sample

Non-Chemical Seed Treatment at 31.3% in 2025 is the fastest-growing sub-segment, driven by regulatory tightening on synthetic chemistries, expanding organic acreage globally, and premium pricing tolerance among growers serving speciality and export-grade produce. Biological formulations based on Trichoderma, Bacillus, and Pseudomonas strains are capturing most of the non-chemical growth.

By Application Technique

Seed Dressing leads the application technique segment at 39.0% in 2025, driven by its operational simplicity, low equipment requirements, and direct-to-seed application that enables broad adoption across smallholder and commercial farms. The technique supports uniform distribution of fungicides, insecticides, and biological agents, protecting young plants against soil-borne diseases, pests, and abiotic stress at minimal incremental cost.

Seed Coating at 27.6% in 2025 is widely adopted across high-value vegetable and specialty seed categories, offering uniform active ingredient distribution and improved handling for precision planters. Seed Pelleting at 21.4% serves niche markets requiring precision sowing, including lettuce, carrot, onion, and sugar beet. The remaining Others category at 12.0% captures film coating, encrusting, and emerging hybrid techniques gaining traction through 2034.

Regional Market Insights

|

Region |

Market Share (2025) |

Key Growth Drivers |

|

North America |

33.8% |

Corn/soybean acreage, EPA registrations, precision equipment |

|

Europe |

26.4% |

ESTA compliance, vegetable/fruit production, and biological adoption |

|

Asia Pacific |

21.7% |

India oilseed growth, China's hybrid seed penetration |

|

Latin America |

10.2% |

Brazilian soybean expansion, drought resilience demand |

|

Middle East & Africa |

7.9% |

GCC food security, UAE agricultural investment |

North America commands a 33.8% global revenue share in 2025, the most dominant regional position in the global seed treatment market. The United States is the single most important national market, driven by approximately 90% seed treatment penetration in corn acreage, expanding soybean and cotton adoption, and early deployment of precision application equipment. In 2024, UPL Corp received US EPA registration for NIMAXXA bionematicide, reinforcing North America's innovation leadership.

Europe, with 26.4% in 2025, is anchored by vegetable, fruit, and cereal production across Germany, France, the UK, and Italy. Asia Pacific holds 21.7% in 2025and is the fastest-growing regional market. Per the OECD-FAO Agricultural Outlook 2021-2030, India's per capita vegetable oil consumption is projected to reach 14 kg by 2030, driving a 3.4% annual rise in domestic oilseed production.

Latin America contributes 10.2% in 2025, with Brazil holding approximately 91.4% of the regional market in 2022, per industry reports. Recent droughts and heat waves have driven farmers toward seed treatments enhancing drought tolerance. The Middle East and Africa region represents 7.9% in 2025.

Competitive Landscape

|

Company |

Brand / Platform |

Market Position |

|

Bayer AG |

Poncho |

Leader |

|

Syngenta |

CruiserMaxx |

Leader |

|

BASF |

Obvius |

Leader |

|

Corteva |

LumiGEN |

Leader |

|

FMC Corporation |

Ethos |

Challenger |

|

UPL |

NIMAXXA |

Challenger |

|

Nufarm |

NipsIt Inside, Nipsit SUITE and INTEGO Solo |

Emerging |

The seed treatment competitive landscape is characterised by a small number of global agrochemical majors commanding substantial seed company relationships and distribution reach, alongside biological specialists and regional players challenging the established hierarchy in emerging markets. The top five players - Bayer, Syngenta, BASF, Corteva, and FMC - collectively account for approximately 55-60% of global revenue in 2025.

Competition centres on patented active ingredients, biological pipeline depth, distribution reach, and seed company partnerships that secure formulation-stage integration. Strategic priorities across the leader set include biological R&D investment, regulatory registration capability across multiple geographies, and digital traceability platforms that support compliance with ESTA, EPA, and emerging Latin American requirements.

Key Company Profiles

Bayer AG

Bayer Crop Science is the global leader in seed treatment, with integrated capabilities spanning active ingredient R&D, seed breeding, and commercial treatment across North America, Latin America, Europe, and the Asia Pacific.

- Product & Platform Portfolio: Poncho, Gaucho, Votivo, EverGol Energy, Raxil.

- Recent Developments: In May 2022, Bayer Vietnam launched Routine Start 280FS (Routine Start), a new seed treatment product to protect early-season rice seeds from rice blast fungi, improving crop productivity and resource efficiency for rice farmers.

- Strategic Focus: Bayer's strategy centres on integrated seed-plus-treatment offerings, biological pipeline expansion, and digital advisory via the Bayer Climate FieldView platform, leveraging its seed leadership to drive premium treatment penetration.

Syngenta

Syngenta, owned by ChemChina, is a top-tier global seed treatment supplier across cereals, oilseeds, and specialty crops, with distribution reach across more than 90 countries.

- Product & Platform Portfolio: CruiserMaxx, Victrato, Vibrance, Apron, Maxim, Dividend.

- Recent Developments: In November 2025, Syngenta announced Seedcare innovation, Victrato seed treatment, is now registered by the U.S. Environmental Protection Agency for soybeans and cotton. Delivering the most robust level of protection against plant-parasitic nematodes and diseases in a single molecule, Victrato will be available in 2025 in preparation for the 2026 planting season, subject to state approvals.

- Strategic Focus: Syngenta is expanding biological and hybrid chemical-biological formulations, deepening Asia Pacific penetration, and advancing sustainable agriculture through its Good Growth Plan.

BASF

BASF's Agricultural Solutions division is a major global force in seed treatment, offering integrated crop protection, seed enhancement, and biological formulations.

- Product & Platform Portfolio: Acceleron, Obvius, Stamina, Integral, Poncho VOTiVO.

- Recent Developments: In November 2025, BASF announced that Integral Pro, an innovative fungicide seed treatment, has received official registration in France for use on sunflower.

- Strategic Focus: BASF's strategy prioritises integrated digital advisory services linked to seed treatment, biological pipeline depth, and expanded presence in Brazilian and Argentine soybean complexes.

Market Concentration Analysis

The global seed treatment market exhibits moderate-to-high concentration, with Bayer AG, Syngenta, BASF, Corteva, and FMC Corporation collectively accounting for approximately 55-60% of global revenue in 2025. This reflects high R&D capital intensity, multi-country registration requirements, and the strategic value of integrated seed-plus-treatment offerings.

The market is experiencing a bifurcated structural dynamic. At the premium tier, consolidation is accelerating: complex biological pipelines and multi-country registration require massive R&D investment that only the largest players can sustain, structurally advantaging Bayer, Syngenta, BASF, and Corteva in securing exclusive factory-treatment relationships.

Simultaneously, the biological segment is generating new challengers. Specialists, including UPL, Incotec, Germains, and Advanced Biological Marketing, are building differentiated portfolios attracting premium pricing and seed company partnerships in high-growth organic and specialty segments.

Investment & Growth Opportunities

Fastest-Growing Segments

Non-Chemical Seed Treatment is the highest-growth type sub-segment through 2034, driven by biological innovation, expanding organic acreage, and tightening neonicotinoid regulations. Seed Pelleting is the fastest-growing application technique, fuelled by premium horticulture and vegetable seed demand.

Emerging Market Expansion

Asia Pacific, led by India and China, offers the highest long-term growth runway as hybrid seed adoption and commercial treatment penetration rise from low bases. Latin America's Brazilian soybean complex remains structurally attractive.

Venture & Private Investment Trends

Notable transactions include Bayer's continued biological investment, Syngenta's Good Growth Plan R&D allocation, and venture rounds in start-ups including Indigo Ag, Pivot Bio, and SaliCrop. Precision equipment start-ups are attracting growing capital.

Future Market Outlook (2026-2034)

The global seed treatment market forecast projects steady expansion from USD 10.02 Billion in 2025 to USD 17.71 Billion by 2034 at a CAGR of 6.53%, a near-doubling underpinned by biological mainstreaming, precision application adoption, and rising treated acreage.

Three technology discontinuities are likely to reshape the market through 2034. Biological mainstreaming, supported by improved shelf-life and efficacy, will shift the type mix away from purely chemical formulations. Nanotechnology encapsulation will enable sustained-release active delivery. Precision application with digital traceability will become a regulatory requirement across premium markets by 2028-2030.

By 2034, the industry is forecast to have completed a structural transition from chemistry-first positioning to platform-based offerings combining chemical, biological, and digital components. Competitive advantage will accrue to players with deep biological pipelines, strong seed company partnerships, and multi-country regulatory capability.

Research Methodology

Primary Research

Primary research encompassed over 40 structured interviews conducted in 2024-2025 with seed treatment industry stakeholders including product directors at global formulation companies, commercial seed treater operators, distribution partners, regulatory experts across the US EPA and European Food Safety Authority, seed company procurement leads, and end-user growers across North America, Europe, Asia Pacific, and Latin America.

Secondary Research

Secondary sources include the FAO Crop Production Yearbook, OECD-FAO Agricultural Outlook 2021-2030, USDA, European Commission agriculture reports, ESTA publications, company annual reports, patent filings, regulatory registration databases, and industry publications covering agrochemicals, seeds, and integrated pest management through 2025.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up models, incorporating GDP growth rates, agricultural output data, hybrid seed penetration curves, treated acreage ratios, and historical patterns. Scenario analysis (base, optimistic, and conservative) was performed to account for regulatory, climate, and commodity price uncertainty.

Seed Treatment Market Report Coverage

|

Attribute |

Details |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Unit |

USD Billion |

|

Market Size (2025) |

USD 10.02 Billion |

|

Market Forecast (2034) |

USD 17.71 Billion |

|

CAGR (2026-2034) |

6.53% |

|

Segmentation |

Type, Application Technique, Crop Type, Function, Region |

|

Regional Analysis |

North America, Europe, Asia Pacific, Latin America, MEA |

|

Companies Covered |

Bayer AG, Syngenta, BASF, Corteva, FMC Corporation, UPL, Nufarm, etc. |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the seed treatment market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global seed treatment market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the seed treatment industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Seed Treatment Market Report

The global seed treatment market was valued at USD 10.02 Billion in 2025, driven by rising hybrid seed adoption, biological formulation growth, and expanding treated acreage.

The market is projected to reach USD 17.71 Billion by 2034, growing at a CAGR of 6.53% during 2026-2034, driven by biological mainstreaming, precision equipment adoption, and treated acreage expansion.

Chemical Seed Treatment leads with a 68.7% share in 2025, driven by cost-effectiveness, broad regulatory approval, and strong protection against fungi, insects, and nematodes across global row crop acreage.

Seed Dressing leads with a 39.0% share in 2025, driven by low equipment requirements, direct-to-seed simplicity, and broad farmer adoption across cereals, oilseeds, and pulses worldwide.

North America leads with a 33.8% share in 2025, driven by approximately 90% treatment penetration in US corn, expanding soybean and cotton adoption, and early precision application equipment deployment.

Key drivers include rising yield protection demand, hybrid and GM seed adoption, biological formulation innovation, precision application equipment, climate resilience needs, and supportive government pest management programmes.

Non-Chemical Seed Treatment is the fastest-growing type segment, supported by regulatory tightening on synthetic chemistries, rising organic acreage exceeding 96 Million hectares globally, and biological formulation innovation.

Leading companies include Bayer AG, Syngenta, BASF, Corteva, FMC Corporation, UPL, and Nufarm.

Biological treatments using Trichoderma, Bacillus, and Pseudomonas microbes are mainstreaming rapidly, offering residue-free crop protection, meeting rising regulatory demand, and enabling premium pricing across organic and specialty acreage.

Precision application equipment and digital traceability systems improve active ingredient uniformity by over 20%, reduce chemical use by 30-40%, and support regulatory compliance across major commercial treatment facilities globally.

Neonicotinoid restrictions in the EU and US EPA reviews are reshaping chemical formulations, while ESTA and IPM programmes are elevating quality assurance standards and accelerating biological treatment adoption across major markets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)