Self-Care Medical Devices Market Size, Share, Trends and Forecast by Device Type, End-User, Distribution Channel, and Region, 2026-2034

Self-Care Medical Devices Market Size, Share Analysis & Outlook:

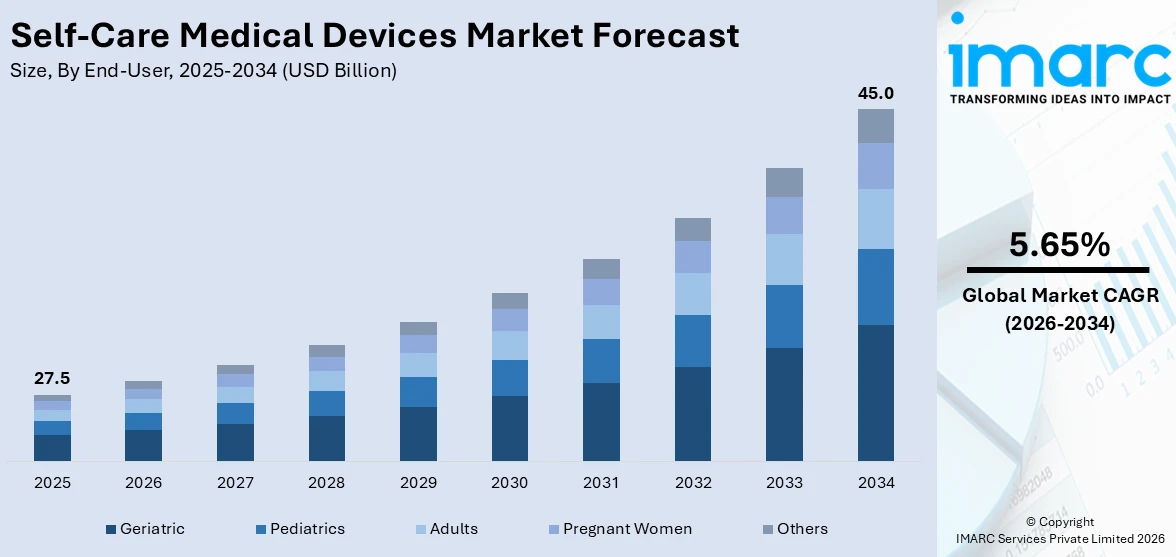

The global self-care medical devices market size is anticipated to reach USD 27.5 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 45.0 Billion by 2034, exhibiting a CAGR of 5.65% from 2026-2034. North America currently dominates the market, holding a market share of over 34.7% in 2025. The growing geriatric population and rising chronic diseases like diabetes and hypertension are increasing demand for self-care medical devices. Technological advances, including AI-driven platforms, wearables, and non-invasive monitoring, further enhance device adoption and functionality. Companies are launching innovative products and partnerships to stay competitive, expanding the self-care medical devices market growth.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 27.5 Billion |

| Market Forecast in 2034 | USD 45.0 Billion |

| Market Growth Rate (2026-2034) | 5.65% |

With healthcare expenses on the rise, self-care medical devices offer a cost-effective solution for patients. They reduce the need for frequent doctor visits and hospital stays, making them an attractive option for managing chronic and acute conditions. Moreover, continuous innovations in wearable technology, mobile health applications, and artificial intelligence (AI)-driven diagnostic tools are enhancing the functionality of various self-care medical devices. Enhanced features, such as real-time monitoring, data analysis, and integration with smartphones, are making these devices more efficient, accurate, and appealing to tech-savvy individuals. Apart from this, the growing awareness among people about the benefits of preventive healthcare and self-management of health conditions is driving the adoption of self-care medical devices. Individuals are more inclined to take control of their health, leading to higher demand for devices that offer convenience, accuracy, and reliability.

To get more information on this market Request Sample

The United States is a key region in the market owing to the rising cases of chronic conditions such as diabetes, hypertension, and respiratory disorders among the masses, which self-monitoring and therapeutic devices. These devices empower patients to manage their health effectively and reduce dependence on healthcare facilities. Besides this, the growing adoption of digital health platforms is transforming healthcare management by offering seamless access to services, including appointments, medication delivery, and preventive care. These platforms increase convenience, boost patient involvement, and broaden access to vital healthcare resources. For instance, in 2024, Pfizer introduced PfizerForAll, a digital health platform in the US that provides services such as same-day healthcare appointments, medication delivery, vaccine reservations, and financial assistance for Pfizer medications. The platform seeks to streamline healthcare administration and enhance service accessibility for individuals in America. Future expansions are planned to include additional healthcare needs.

Self Care Medical Devices Market Trends:

Rising Geriatric Population

The rise in the number of older individuals is acting as a major driver, as they have higher chances of acquiring long-term illnesses like diabetes, blood pressure, cardiovascular diseases, and arthritis. As per the United Nations (UN), the number of people 65 years and older will more than double, from 761 Million in 2021 to 1.6 Billion by the year 2050. The population 80 years and older is increasing at an even accelerated rate. In addition, aging population is an irreversible worldwide phenomenon fueled by the demographic transition of increased lifespans and reduced physical family size even among nations with young populations. In 2021, 1 out of 10 individuals globally was over the age of 65. The age group is estimated to account for 1 out of 6 individuals worldwide in 2050. Therefore, the increasing geriatric population is growing sales of self-care medical devices like blood glucose meters and blood pressure monitors that are vital in controlling these conditions.

Increasing Prevalence of Chronic Diseases

The global prevalence of chronic diseases like diabetes and hypertension is on the rise. Diabetes is a growing global challenge for people, households, and countries. 10.5% of the adult population aged 20-79 years worldwide has diabetes, and almost half of them are unaware of it, as per the International Diabetes Federation (IDF) Diabetes Atlas. IDF projections suggest that by 2045, there will be an estimated 783 Million adults, or 1 in 8, with diabetes, a 46% increase from today's number. Type 2 diabetes affects more than 90% of diabetes cases and is impacted by socio-economic, demographic, environmental, and genetic determinants. This generates demand for products that enable patients to self-monitor and control their condition in the home setting. In addition, continuous glucose monitors (CGMs) and blood pressure monitors are gaining traction because they are effective in controlling these conditions. For example, the penetration of CGMs has been supported by technology and growing affordability.

Technological Developments

The self-care medical devices market growth is being propelled by the rapid integration of artificial intelligence (AI), mobile health applications, and digital platforms that transform how individuals monitor and manage their health outside traditional clinical environments. The new innovations and precision and functionality of self-care medical devices are being enhanced by developments such as wearable technology and non-invasive glucose monitoring. For instance, in 2025, Seoul National University College of Engineering revealed that a research team headed by Professor Seung Hwan Ko from the Wearable Soft Electronics Lab in the Department of Mechanical Engineering has created a wearable electronic device that adheres to the skin like a bandage and allows for real-time, ongoing monitoring of blood pressure for prolonged durations. Currently, large companies are unveiling advanced product versions to meet these needs. For example, on 18 March 2024, Johnson & Johnson MedTech partnered with NVIDIA to boost AI abilities within surgical operations. This collaboration is also designed to speed up real-time surgical data analysis at the edge, making operations efficient and secure. Johnson & Johnson MedTech also intends to make it easier to develop and deploy AI models, enabling scalable integration in its digital surgery platform. As a result, firms are constantly applying for new product registrations to remain competitive, which is also driving market growth.

Self Care Medical Devices Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global self-care medical devices market, along with forecast at the global and regional levels from 2026-2034. The market has been categorized based on device type, end-user, and distribution channel.

Analysis by Device Type:

- Self-Monitoring of Blood Glucose (SMBG)

- PD

- Sleep Apnea Devices

- Insulin Pumps

- Body Temperature Monitors

- Inhalers

- Pedometers

- Blood Pressure Monitors

- Nebulizers

- Male External Catheters

- Holter Monitors

- Others

Self-monitoring of blood glucose (SMBG) stands as the largest component in 2025, holding 43.5% of the market share. Self-monitoring of blood glucose (SMBG) dominates the market, as it is crucial for diabetic patients to manage their blood sugar levels independently, driving significant demand globally. It typically includes glucose meters and continuous glucose monitoring systems (CGMs), offering convenience and real-time data for effective diabetes management. Additionally, the market for SMBG devices is characterized by ongoing technological advancements aimed at improving experience of the user, accuracy, and integration with digital health platforms. In February 2023, Afon Technology Ltd. announced on Twitter the introduction of a non-invasive blood glucose sensor, a wearable gadget launched in the beginning of 2024. It is entirely non-invasive and removes the necessity for needles or lancets, presenting a far more appealing choice for individuals managing diabetes. This segment is also fueled by the increasing prevalence of diabetes worldwide and the rising preference for home-based healthcare solutions, which is creating a positive self-care medical devices market outlook.

Analysis by End-User:

- Geriatric

- Pediatrics

- Adults

- Pregnant Women

- Others

Geriatric accounts for the majority of the market share. Geriatric individuals aged 65 and above are driving the demand for self-care medical devices due to their increasing healthcare needs and desire for independent living. Moreover, the growing number of geriatric users often require devices for chronic disease management, mobility aids, and remote monitoring solutions to maintain health and quality of life. According to the World Health Organization (WHO) by 2030, one out of every six people worldwide will be 60 years of age or older. During this period, the population aged 60 years and above will rise from 1 Billion in 2020 to 1.4 Billion. By 2050, the global population of individuals aged 60 years and older is projected to double to 2.1 Billion. The number of people aged 80 years or older is expected to triple from 2020-2050, reaching 426 Million. Hence, manufacturers and healthcare providers are focusing on developing user-friendly, intuitive devices tailored to the needs and preferences of this demographic, thereby shaping the self-care medical devices market growth trajectory.

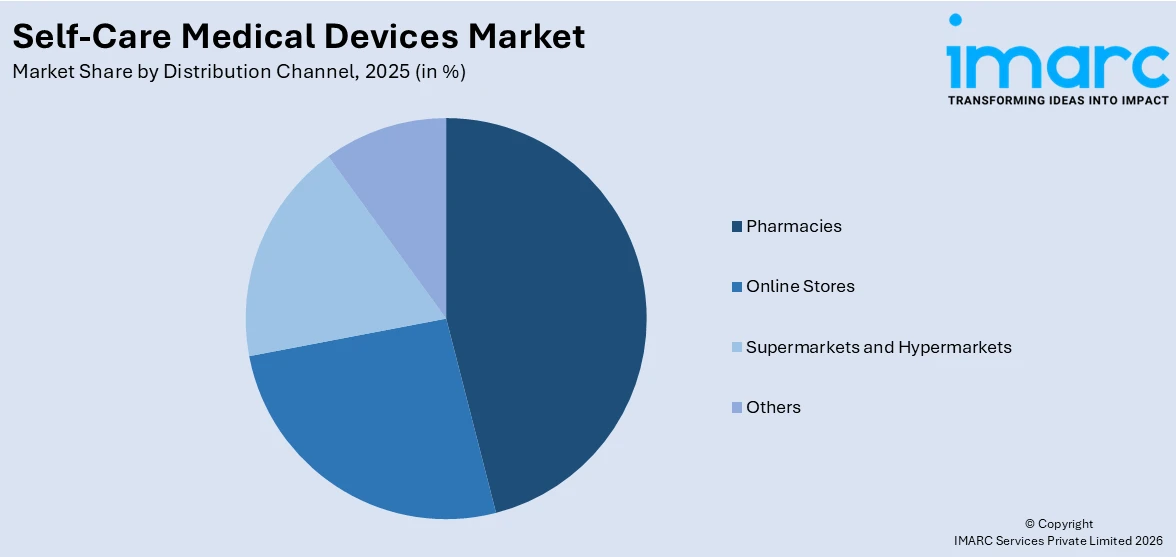

Analysis by Distribution Channel:

Access the comprehensive market breakdown Request Sample

- Pharmacies

- Online Stores

- Supermarkets and Hypermarkets

- Others

In 2025, pharmacies hold a notable market share of 42.5%. Pharmacies provide an easy way for consumers to obtain self-care tools like blood pressure monitors, glucose meters, and respiratory aids. Their existence in both urban and rural settings improves market reach, addressing various demographic requirements. Pharmacies gain from pharmacists' knowledge in suggesting appropriate devices, which enhances consumer trust and guarantees efficient self-care management, leading to an optimistic outlook for the self-care medical devices sector. According to the statistics from the Organization for Economic Cooperation and Development (OECD), between 2000 and 2019, the ratio of pharmacists to the population rose by almost 40% on average in OECD countries with accessible time series data, reaching 86 pharmacists for every 100,000 residents. Thus, this significance highlights pharmacies' vital function in delivering crucial medical equipment directly to individuals worldwide.

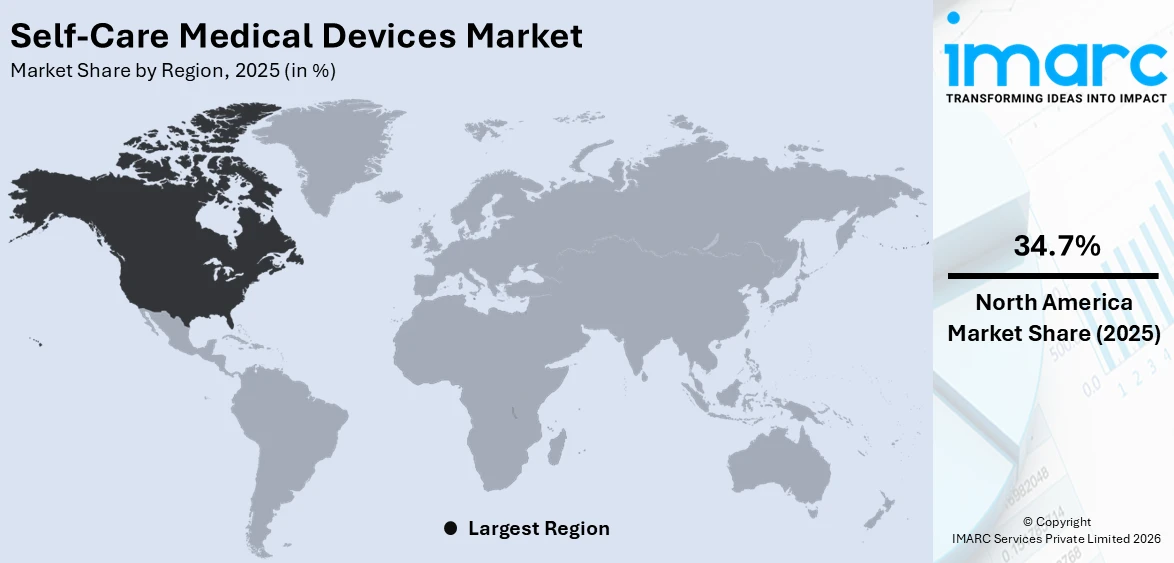

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- Europe

- Asia Pacific

- Middle East and Africa

- Latin America

In 2025, North America accounted for the largest market share of 34.7%. North America primarily includes individual consumers seeking convenient healthcare options at home, driven by the aging population's desire for greater independence and control over their health. The market caters extensively to personal health monitoring devices, such as glucose monitors, blood pressure monitors, and wearable fitness trackers, which empower users to manage their health proactively and independently. According to an article published on 22 May 2024, researchers from the University of California San Diego have created a wearable ultrasound patch capable of continuously and non-invasively monitoring brain blood flow. This soft, flexible patch is worn on the temple, providing three-dimensional cerebral blood flow data, a pioneering achievement in wearable technology. The team, led by Professor Sheng Xu, disclosed their innovation in Nature. According to the self-care medical devices market forecast, the region is anticipated to experience significant growth in the coming years due to the increasing adoption of health-monitoring technologies and the rising demand for convenient at-home healthcare solutions.

Key Regional Takeaways:

United States Self-Care Medical Devices Market Analysis

The United States stands as one of the largest and most sophisticated market for self-care medical devices, characterized by exceptionally high healthcare expenditure exceeding three trillion dollars annually, advanced technological adoption across consumer segments, and increasingly comprehensive insurance coverage that now frequently reimburses remote patient monitoring solutions as cost-effective alternatives to traditional care delivery. The country faces a significant chronic disease burden, with conditions including diabetes, cardiovascular disease, chronic obstructive pulmonary disease, and sleep disorders affecting hundreds of millions of Americans and creating substantial ongoing demand for home monitoring equipment that enables condition management and complication prevention. The Centers for Medicare and Medicaid Services has strategically expanded reimbursement codes for remote patient monitoring services, creating financial incentives for both healthcare providers and patients to adopt self-care technologies as standard components of chronic disease management programs. Digital health platforms are proliferating rapidly, offering integrated services that combine device data collection with telehealth video consultations, electronic prescription management, medication adherence tracking, and personalized wellness coaching delivered through mobile applications. Regulatory support through Food and Drug Administration initiatives specifically focused on home-use devices and artificial intelligence-enabled diagnostics accelerates innovation cycles while maintaining rigorous safety standards through risk-based classification systems and post-market surveillance requirements. In December 2024, the Food and Drug Administration released final recommendations for streamlining the approval process for medical devices that use artificial intelligence, with the guidance recommending information to include in predetermined change control plans as part of marketing submissions for artificial intelligence-enabled medical devices, facilitating faster deployment of advanced self-care technologies while maintaining appropriate regulatory oversight and patient safety protections.

Europe Self-Care Medical Devices Market Analysis

Europe's self-care medical devices sector is distinguished by stringent regulatory standards that prioritize patient safety, strong governmental emphasis on health technology assessment, and accelerating adoption of digital health solutions supported by comprehensive national eHealth strategies. The European Union's Medical Device Regulation provides extensive oversight encompassing device lifecycle management, clinical evidence requirements, post-market surveillance obligations, and unique device identification, while simultaneously accommodating technological innovation through adaptive frameworks that recognize the dynamic nature of software-driven medical devices. The aging population across European nations, with many countries experiencing median ages above forty-five years, drives substantial demand for home-based monitoring solutions that enable independent living, reduce caregiver burden, and decrease healthcare system strain from chronic condition management. Countries are implementing ambitious national digital health strategies that integrate self-care devices into broader healthcare ecosystems with particular emphasis on interoperability standards ensuring device data flows seamlessly into electronic health records, and data protection compliance with the General Data Protection Regulation requirements for sensitive health information. The European Health Data Space initiative, agreed upon through landmark negotiations in March 2024, is revolutionizing healthcare delivery by granting individuals unprecedented access to their electronic health data while facilitating secure cross-border health data exchange, supporting the integration of self-care device data into comprehensive longitudinal health records that inform clinical decision-making. Throughout 2024 and into 2025, the European Commission has been actively updating medical device regulations, including the implementation of unique device identifier systems that enable device tracking throughout the supply chain, expert panel designations providing specialized scientific guidance, and enhanced guidance documents on software classification.

Asia Pacific Self-Care Medical Devices Market Analysis

The Asia Pacific region represents the fastest-growing geographic market for self-care medical devices globally, driven by enormous populations exceeding four billion people, rapidly rising disposable incomes particularly among expanding middle classes, increasing health awareness through public education campaigns, and substantial government initiatives to strengthen healthcare infrastructure and achieve universal health coverage goals. Countries including China, India, Japan, South Korea, and Southeast Asian nations are experiencing rapid adoption of digital health technologies and home-based medical devices as components of healthcare system modernization strategies. The region faces significant chronic disease burden with diabetes, cardiovascular disease, and respiratory conditions affecting hundreds of millions of individuals, combined with persistent healthcare access challenges particularly in rural and remote areas where clinical facilities remain limited, making self-care solutions particularly valuable for extending medical services to underserved populations and reducing geographic health disparities. Governments are implementing ambitious policies to encourage medical technology innovation through research funding, tax incentives, regulatory streamlining, and support for local manufacturing capabilities to reduce import dependence and create domestic medical device industries. Regional healthcare systems are increasingly incorporating remote monitoring platforms and telehealth consultation services, creating integrated digital ecosystems for self-care device deployment that connect patients, devices, and healthcare providers. In September 2024, Medtronic inaugurated Southeast Asia's first Robotics Experience Studio in Singapore, a state-of-the-art facility that focuses on skill-building in robotic-assisted procedures and artificial intelligence applications, supporting the region's rising demand for precision care and medical technology while strengthening the regional healthcare ecosystem by fostering collaboration between industry, academia, and healthcare providers, providing hands-on training for healthcare professionals, and facilitating access to cutting-edge technologies that improve patient outcomes across Southeast Asia.

Latin America Self-Care Medical Devices Market Analysis

Latin America is embracing self-care medical device technology with growing recognition of its potential to address persistent healthcare accessibility challenges and reduce strain on overburdened public health systems that struggle to meet population needs with limited budgets and resources. The region's healthcare infrastructure varies significantly between countries and within countries, with urban areas generally possessing better access to advanced medical technologies, specialist physicians, and diagnostic facilities compared to rural regions where basic healthcare services remain limited. Economic factors substantially influence adoption patterns, with price-sensitive markets driving particular demand for cost-effective self-monitoring solutions that provide value without premium pricing, while import tariffs and currency fluctuations affect device affordability and market dynamics. Governments are gradually implementing regulatory frameworks that balance essential safety requirements with pragmatic recognition of the need to improve healthcare access, with some countries establishing expedited approval pathways for devices already approved in reference markets.

Middle East and Africa Self-Care Medical Devices Market Analysis

The Middle East and Africa region is experiencing gradual but steady adoption of self-care medical devices, driven by ongoing healthcare infrastructure development, increasing chronic disease prevalence particularly in urban populations, and government initiatives to modernize health systems as components of broader economic development strategies. Gulf Cooperation Council countries including the United Arab Emirates, Saudi Arabia, and Qatar are investing heavily in healthcare technology as central elements of economic diversification strategies that reduce oil dependence and position these nations as regional healthcare hubs. African nations are exploring self-care solutions to extend medical services to remote populations with severely limited clinical access, recognizing that traditional healthcare delivery models cannot economically reach dispersed rural populations.

Competitive Landscape:

Major participants in the market are diligently concentrating on improving product innovation, broadening their digital health platforms, and reinforcing their distribution channels. They are putting resources into research and development to launch sophisticated, easy-to-use devices that offer enhanced accuracy and connectivity capabilities. Strategic alliances and collaborations are being emphasized to incorporate artificial intelligence and data analytics for customized healthcare solutions. Businesses are also broadening their market presence by focusing on emerging areas and modifying their products to cater to various consumer demands. Initiatives aimed at meeting regulatory standards and improving affordability are shaping their competitive approaches. In 2024, Oxymed introduced the SleepEasy Auto CPAP devices in India, which include advanced FlowSens algorithms, CSA detection, and adjustable therapy modes for improved sleep apnea treatment. These CE-certified products merge cost-effectiveness with global standards, highlighting Oxymed's growth in the respiratory care sector.

The report provides a comprehensive analysis of the competitive landscape in the self-care medical devices market with detailed profiles of all major companies, including:

- Johnson & Johnson

- Medtronic

- Abbott Laboratories

- Bayer HealthCare

- Koninklijke Philips

- General Electric Company

- F. Hoffmann-La Roche AG

- ResMed

- Omron Healthcare

- Martifarm, OraSure Technologies

- Baxter

- B. Braun Melsungen

Latest News and Developments:

- September 2024: Mankind Pharma introduces RAPID NEWS self-test kits, addressing critical health challenges like dengue, UTIs, and early menopause in India. These innovative devices empower individuals with private, rapid, and accessible healthcare solutions. Amid rising health concerns, such as 300,000 dengue cases in 2023, timely detection is key to improving outcomes. This launch marks a significant step toward enhancing self-care in healthcare.

- January 2024: OraSure Technologies, Inc., a prominent provider of point-of-care and home diagnostic tests, specimen collection devices, and microbiome laboratory services, announced its leadership in Series B financing and the establishment of strategic distribution agreements with Sapphiros. Sapphiros, specializes in advanced consumer diagnostics, featuring new sample collection methods, next-generation detection systems, computational biology, and printed electronics to enhance diagnostic accessibility.

- October 2025: Outfront Health revealed its official launch, providing a contemporary method for adults to assess vital health indicators - without needing to visit a clinic or lab. The company offers biomarker test kits that enable nearly painless at-home collection through a self-administered device applied to the upper arm. Orders are approved by a licensed healthcare professional, and results undergo safety evaluation by a physician for critical values; a separate physician appointment is not necessary. Findings are provided via a secure online platform that illustrates trends throughout time.

- July 2025: Abhay HealthTech has revealed the growth of its product range to assist India’s transition to consumer-driven and preventive healthcare. The company now provides rapid diagnostic kits, hygiene items, wellness products, and telehealth services, addressing the increasing need for home-based medical solutions.

Self-Care Medical Devices Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Device Types Covered | Self-Monitoring of Blood Glucose (SMBG), PD, Sleep Apnea Devices, Insulin Pumps, Body Temperature Monitors, Inhalers, Pedometers, Blood Pressure Monitors, Nebulizers, Male External Catheters, Holter Monitors, Others |

| End-Users Covered | Geriatric, Pediatrics, Adults, Pregnant Women, Others |

| Distribution Channels Covered | Pharmacies, Online Stores, Supermarkets and Hypermarkets, Others |

| Regions Covered | North America, Europe, Asia Pacific, Middle East and Africa, Latin America |

| Companies Covered | Johnson & Johnson, Medtronic, Abbott Laboratories, Bayer HealthCare, Koninklijke Philips, General Electric Company, F. Hoffmann-La Roche AG, ResMed, Omron Healthcare, Martifarm, OraSure Technologies, Baxter, B. Braun Melsungen, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the self-care medical devices market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global self-care medical devices market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the self-care medical devices industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Self-Care Medical Devices Market Report

The self care medical devices market size reached USD 27.5 Billion in 2025.

The self-care medical devices market is projected to reach a value of USD 45.0 Billion by 2034, exhibiting a CAGR of 5.65% during the forecast period of 2026-2034.

Key factors driving the market include the rising prevalence of chronic diseases like diabetes and hypertension, an aging population, growing health awareness, technological advancements in wearable and AI-driven devices, and the increasing demand for cost-effective, at-home healthcare solutions that reduce reliance on healthcare facilities.

North America dominates the self-care medical devices market in 2025, accounting for a share exceeding 34.7%. This dominance is fueled by advanced healthcare infrastructure, high adoption of innovative technologies, increasing prevalence of chronic diseases, and strong consumer demand for convenient, tech-enabled healthcare solutions.

Some of the major players in the self-care medical devices market include Johnson & Johnson, Medtronic, Abbott Laboratories, Bayer HealthCare, Koninklijke Philips, General Electric Company, F. Hoffmann-La Roche AG, ResMed, Omron Healthcare, Martifarm, OraSure Technologies, Baxter, and B. Braun Melsungen, among others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)