Set-Top Box Market Size, Share, Trends and Forecast by Type, Resolution, End User, Service Type, Distribution, and Region 2026-2034

Global Set-Top Box Market Size, Share, Trends & Forecast (2026-2034)

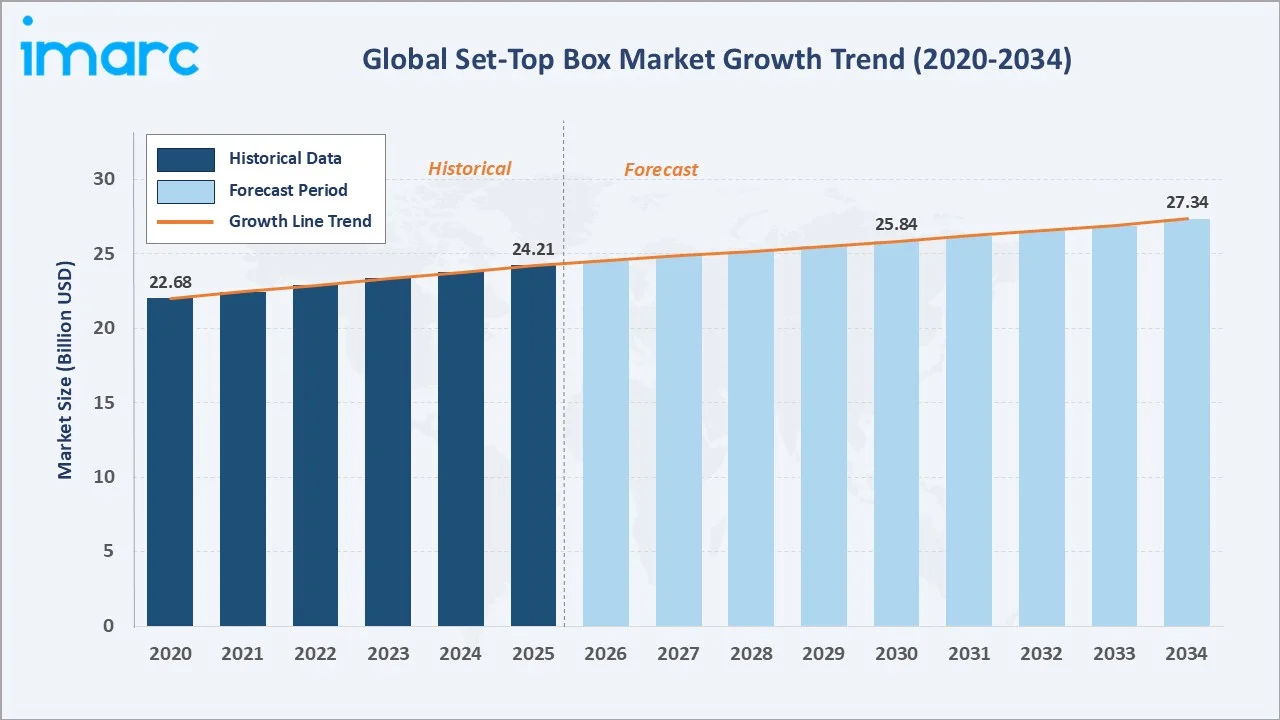

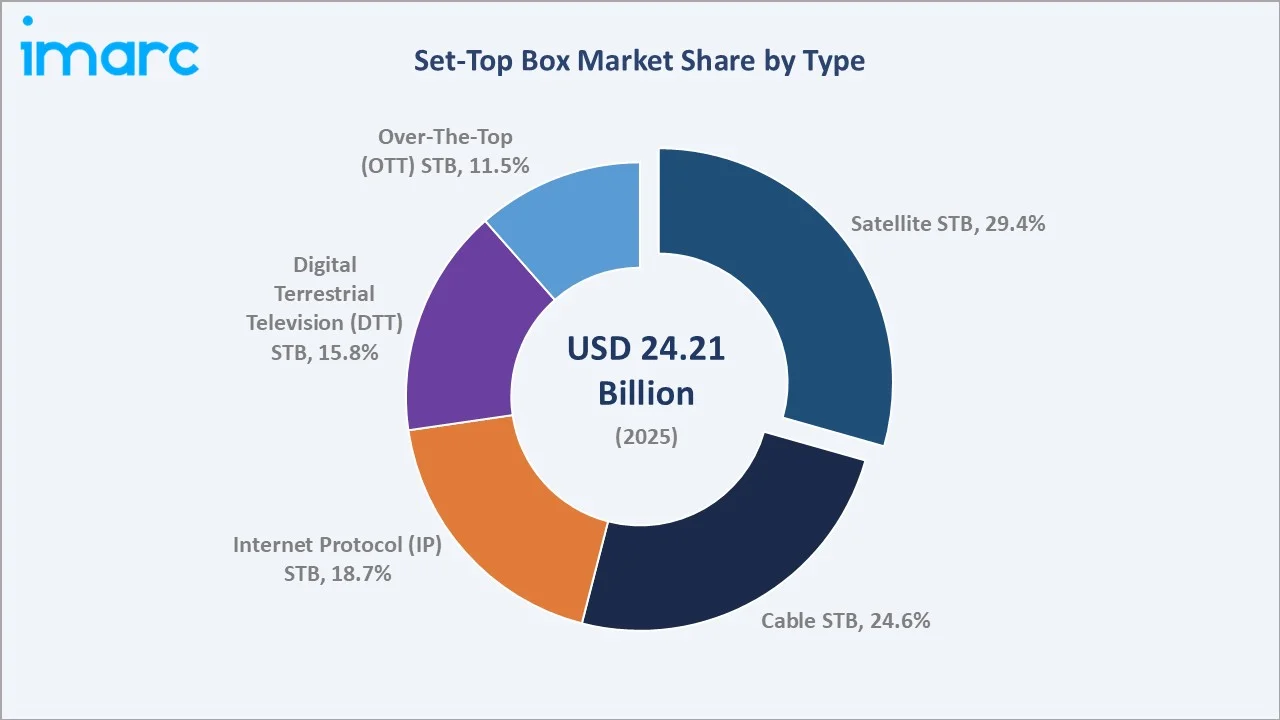

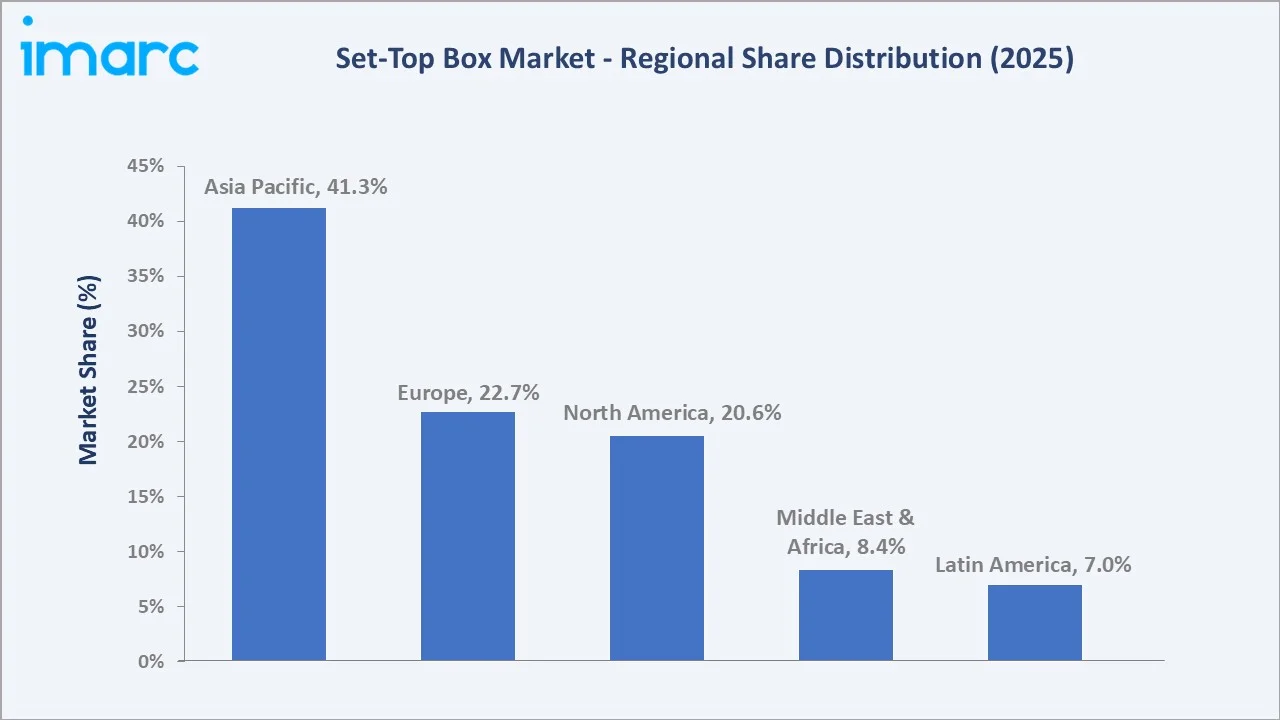

The global set-top box market size was valued at USD 24.21 Billion in 2025 and is projected to reach USD 27.34 Billion by 2034, exhibiting a CAGR of 1.31% during the forecast period 2026-2034. Growth is driven by sustained pay-TV penetration in emerging economies, rising demand for hybrid OTT-enabled boxes, the progressive migration from analogue cable to IP-based delivery, and accelerating 4K/8K UHD upgrades across operator deployments. Asia Pacific leads the global market with a 41.3% revenue share in 2025, driven by India's DTH expansion and China's IPTV base. Satellite STBs remain the largest segment at 29.4%, while OTT STBs grow fastest on streaming platform integration and Android TV adoption across telco operators.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 24.21 Billion |

|

Forecast Market Size (2034) |

USD 27.34 Billion |

|

CAGR (2026-2034) |

1.31% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (41.3% share, 2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~2.1%) |

|

Leading Type Segment |

Satellite STB (29.4%, 2025) |

|

Leading Distribution Channel |

Offline Distribution (68.5%, 2025) |

The global set-top box market growth trajectory from 2020 through 2034 reflects steady historical expansion giving way to a measured forecast curve shaped by hybrid OTT integration, premium 4K/8K unit mix-up, and ongoing emerging-market pay-TV adoption.

To get more information on this market, Request Sample

Segment-level CAGR comparisons highlight OTT STB and Internet Protocol (IP) STB as the two fastest-growing sub-categories within the global set-top box industry analysis through 2034.

Executive Summary

The global set-top box market is undergoing a measured structural transition driven by the convergence of pay-TV modernisation, OTT streaming adoption, and ultra-high-definition content delivery. Valued at USD 24.21 Billion in 2025, the market is forecast to reach USD 27.34 Billion by 2034 at a CAGR of 1.31%. Global pay-TV households exceeded 1 billion in 2024, with cable and satellite platforms still serving the majority, even as hybrid OTT-enabled boxes gain momentum in developed markets.

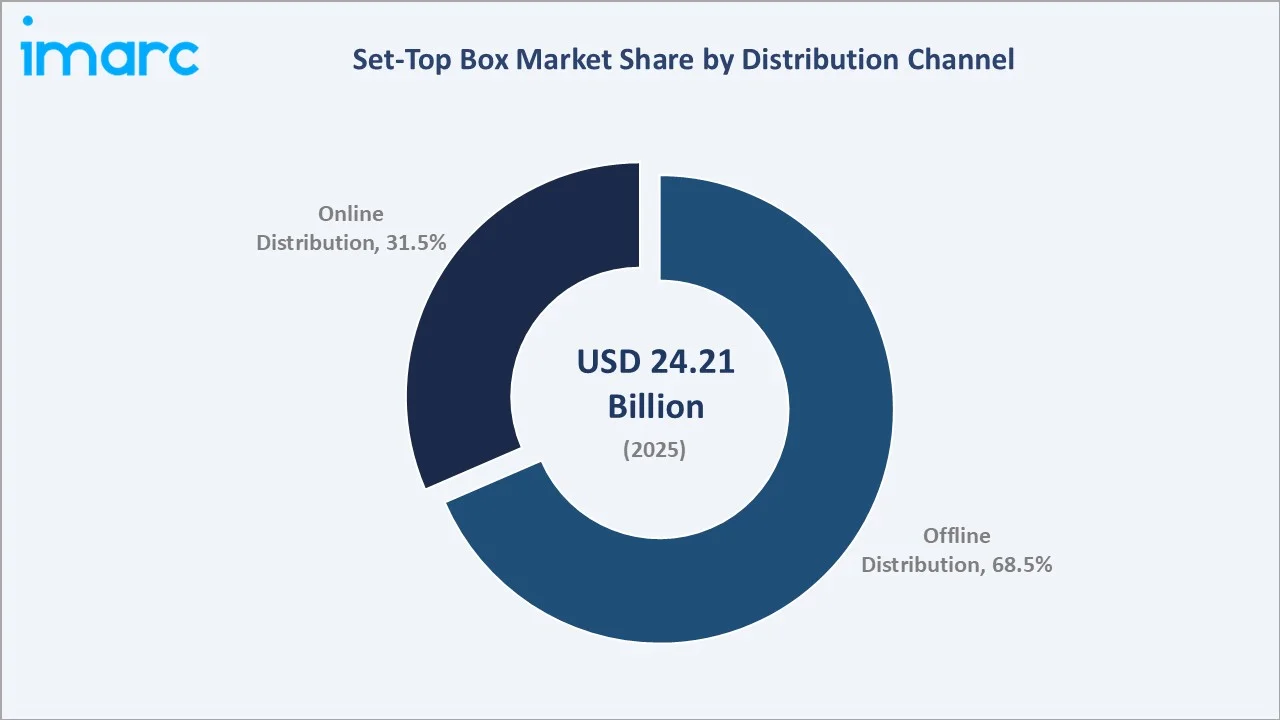

Satellite STB commands the dominant type share at 29.4% in 2025, followed by Cable STB at 24.6%, driven by entrenched DTH ecosystems across India, Brazil, and Sub-Saharan Africa. Internet Protocol (IP) STBs at 18.7% represent the fastest-scaling traditional delivery format as telco operators migrate subscribers to fibre-based video. Offline Distribution leads at 68.5% of 2025 revenue, reflecting operator-bundled deployment, while Online Distribution at 31.5% grows faster through e-commerce and direct-to-consumer OTT hardware sales.

Asia Pacific dominates with a 41.3% global revenue share in 2025, led by India's 65+ million pay-TV subscriber base, China's IPTV household leadership, and Southeast Asia's hybrid STB adoption. Europe holds 22.7% and North America 20.6%, both characterised by mature cable bases transitioning toward OTT-integrated hardware and IP delivery.

Key Market Insights

|

Insight |

Data |

|

Largest Type Segment |

Satellite STB – 29.4% share (2025) |

|

Leading Distribution Channel |

Offline – 68.5% share (2025) |

|

Leading Region |

Asia Pacific – 41.3% revenue share (2025) |

|

Second Region |

Europe – 22.7% revenue share (2025) |

|

Top Companies |

CommScope Technologies LLC, Vantiva, Humax Co., Ltd., Sagemcom, Huawei Technologies Co., Ltd. |

Key Analytical Observations Supporting the Above Data:

- Satellite STB's 29.4% dominance in 2025 reflects the enduring DTH subscriber base across India, Brazil, and MENA, where satellite remains the most reliable pay-TV medium for regions with inconsistent terrestrial broadband.

- Offline Distribution leads at 68.5% in 2025, driven by operator-led bundling where STBs ship installed with pay-TV subscriptions. Online Distribution at 31.5% is gaining on direct-to-consumer OTT hardware sales via Amazon, Flipkart, and JD.com.

- Asia Pacific's 41.3% global dominance in 2025 reflects India's DD Free Dish 45+ million reach, China's 400+ million IPTV households, and ASEAN's rapid hybrid OTT-STB adoption across Indonesia, Vietnam, and the Philippines.

Global Set-Top Box Market Overview

Set-top boxes are consumer electronics devices that decode and deliver digital broadcast, IP, and streaming video signals to television displays. They incorporate tuners, conditional access modules, middleware operating systems, and increasingly hybrid OTT application layers that aggregate linear and on-demand content. Modern STBs integrate 4K/8K UHD decoding, Dolby Atmos audio, AI voice search, and smart-home hub functionality.

Applications span residential pay-TV delivery, hospitality in-room entertainment, commercial digital signage, and educational content distribution, with the residential segment accounting for the vast majority of shipments.

Macroeconomic enablers include 1+ billion global pay-TV households (2024), rising disposable incomes in emerging Asia and Africa, and the accelerating deployment of 4K-capable broadcast infrastructure by national public broadcasters and pay-TV operators worldwide.

Market Dynamics

To evaluate market opportunities, Request Sample

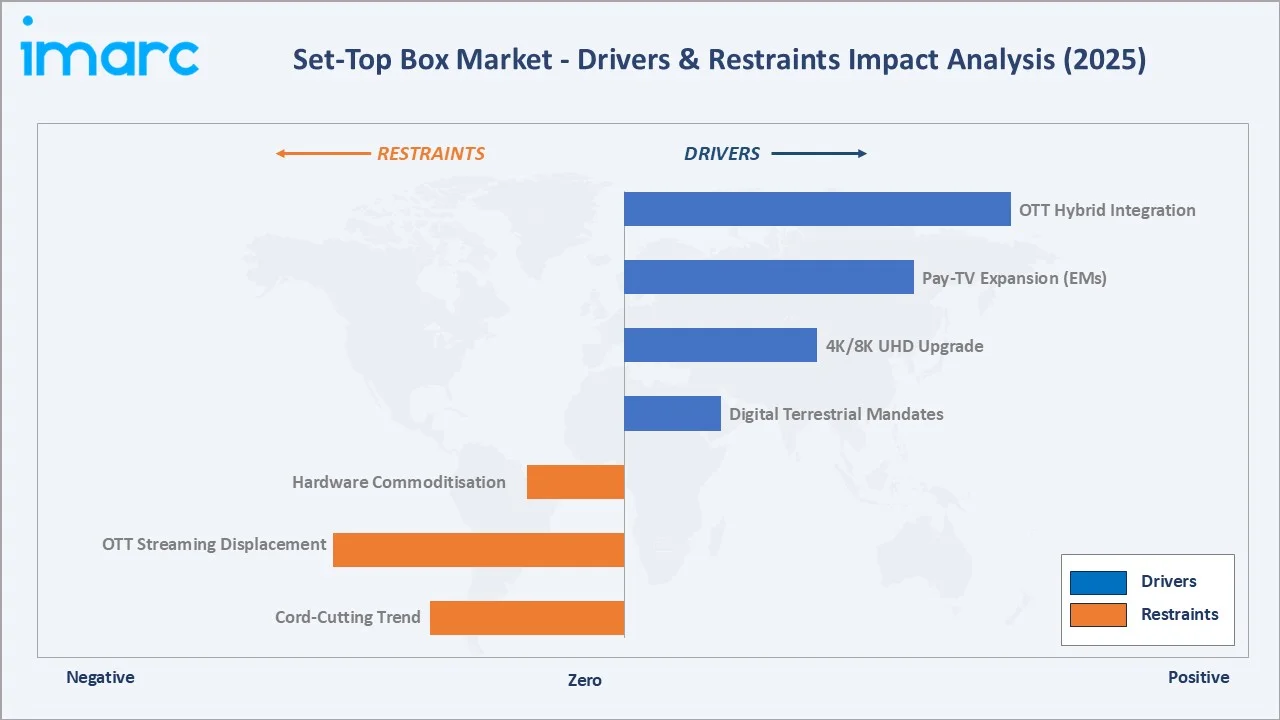

Market Drivers

- Pay-TV Expansion in Emerging Economies: India, Indonesia, Nigeria, and Brazil continue adding first-time pay-TV households at ~20 million net additions per year, with satellite and cable STBs forming the entry-level hardware platform for new subscribers.

- Hybrid OTT-STB Integration: Operators are rapidly replacing legacy boxes with Android TV-powered hybrid devices that combine linear broadcast with Netflix, Prime, and Disney+ app access. Comcast XClass TV, Sky Stream, and Airtel Xstream are reference deployments.

- 4K and 8K UHD Transition: Global 4K-capable STB shipments exceeded 110 million units in 2024, driven by sports broadcasts, UHD linear channels, and streaming UHD tiers. 8K-ready STBs are beginning mass deployment in Japan and South Korea from 2025 onwards.

Market Restraints

- OTT Streaming Displacement: Direct-to-consumer streaming via smart TVs, streaming sticks, and mobile devices is progressively cannibalising traditional STB demand in developed markets, with US pay-TV penetration falling below 60% of households in 2024.

- Hardware Commoditisation: STB average selling prices have declined 18-22% cumulatively since 2020, owing to standardised chipset platforms (Broadcom, MediaTek, Amlogic) and intense OEM competition, squeezing manufacturer margins.

Market Opportunities

- Android TV and Google TV OEM Partnerships: Android TV-certified STB deployments by telcos create recurring software, app-store, and advertising revenue streams beyond the one-time hardware sale, fundamentally reshaping operator economics.

- Voice-Enabled AI Assistants: Integration of Alexa, Google Assistant, and operator-branded voice engines into STB remotes is unlocking premium SKU differentiation and driving measurable 15-25% increases in content discovery and subscriber engagement metrics.

- Commercial & Hospitality Segment: Hotel chains, cruise lines, and healthcare facilities represent a growing underpenetrated STB replacement cycle, with an estimated 40+ million commercial screens targeted for upgrades through 2030.

Market Challenges

- Regional Standards Fragmentation: DVB-S2X, ATSC 3.0, ISDB-T, DTMB, and CAS fragmentation means OEMs must maintain 8+ platform variants, inflating certification costs and lengthening time-to-market for global product platforms.

- Content Piracy and Illicit STBs: Grey-market Android STBs with pre-loaded unauthorised streaming apps are eroding the legitimate operator-branded STB market in Southeast Asia, the Middle East, and parts of Europe.

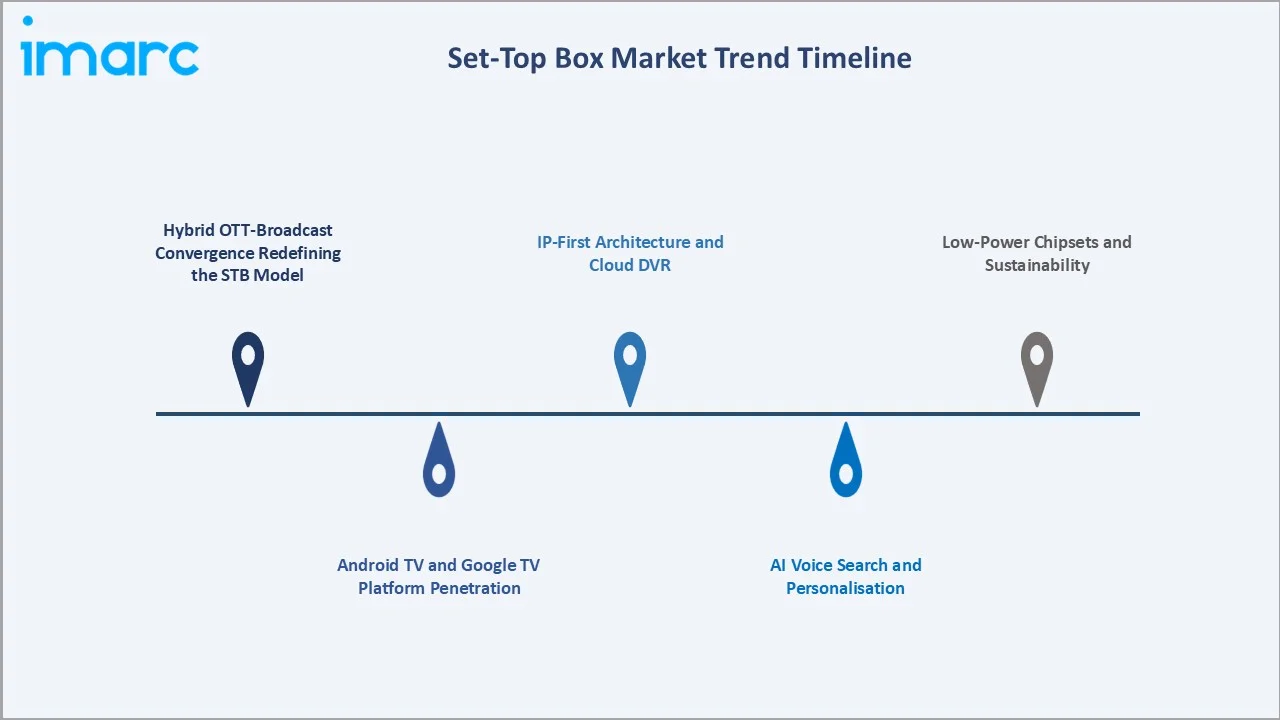

Emerging Market Trends

1. Hybrid OTT-Broadcast Convergence Redefining the STB Model

STBs are evolving from single-purpose tuners to unified content aggregators. Sky Stream, Orange TV Box, and Tata Play Binge demonstrate that operator-led aggregation is becoming the core differentiator, with nearly 70% of new STB launches in 2024-2025 being hybrid-capable.

2. Android TV and Google TV Platform Penetration

Android TV and Google TV have become the leading operator platforms, powering more than 200 million certified devices globally. The OS enables a shared app ecosystem, faster time-to-market, and over-the-air updates that legacy proprietary middleware cannot match.

3. AI Voice Search and Personalisation

Voice remotes and conversational search are shifting from premium to mainstream STB SKUs. Operators such as Comcast, Sky, and Rogers have deployed voice-first experiences that drive measurable 15-25% uplifts in content discovery and engagement time.

4. IP-First Architecture and Cloud DVR

Cable and telco operators are replacing on-device DVRs with cloud-based recording, reducing STB bill-of-materials while enabling multi-screen playback. Xfinity Flex and Altice One are reference cloud-first STB deployments.

5. Low-Power Chipsets and Sustainability

Regulatory pressure (EU Ecodesign, US ENERGY STAR) and operator cost discipline are driving the adoption of sub-5W standby chipsets and recycled-plastic enclosures, with VANTIVA and Sagemcom announcing carbon-neutral STB lines through 2027.

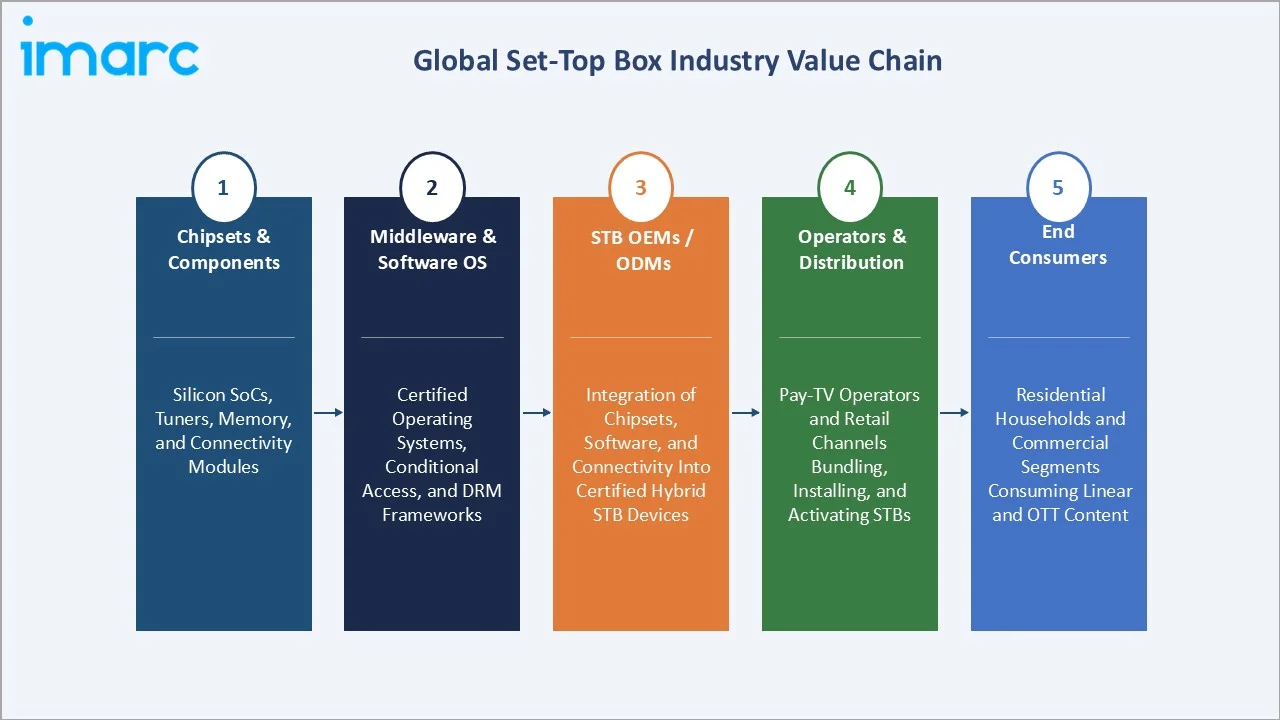

Industry Value Chain Analysis

The set-top box value chain spans five integrated stages from semiconductor component supply through end-consumer delivery. Each stage presents distinct competitive dynamics, margin profiles, and technology investment requirements, and dominant players at each tier are shifting as Android TV standardisation reshapes supplier economics.

|

Stage |

Role in the Value Chain |

|

Chipsets & Components |

Silicon SoCs, tuners, memory, and connectivity modules form the hardware foundation of every STB. |

|

Middleware & Software OS |

Certified operating systems, conditional access, and DRM frameworks enabling secure content delivery. |

|

STB OEMs / ODMs |

Integration of chipsets, software, and connectivity into certified turnkey hybrid STB devices. |

|

Operators & Distribution |

Pay-TV operators and retail channels are bundling, installing, and activating STBs for end users. |

|

End Consumers |

Residential households and commercial segments are consuming linear, on-demand, and OTT content. |

Tier-1 STB OEMs occupy a pivotal position in the value chain, consolidating chipsets, middleware, conditional access, and connectivity into certified turnkey platforms for pay-TV operators. However, the rise of operator-owned Android TV specifications is progressively shifting value upstream toward platform software vendors and downstream toward service operators.

Technology Landscape in the Set-Top Box Industry

Decoding Architecture: 4K, 8K, and HDR

Modern STBs integrate HEVC/H.265 and increasingly AV1 video decoders supporting 4K HDR10, Dolby Vision, and HLG formats. 4K-capable STB shipments surpassed 110 million units in 2024, with 8K-ready units beginning commercial deployment through NHK Japan and KT Korea.

Operating Systems and Middleware

Android TV and Google TV power over 200 million certified devices globally. RDK (Reference Design Kit), backed by Comcast and Liberty Global, remains the dominant open-source platform for cable operators, while Linux-based proprietary stacks continue to power high-end hybrid STBs.

Connectivity and Smart Integration

Wi-Fi 6E and Wi-Fi 7 adoption is accelerating in premium STBs to support simultaneous 4K streaming and whole-home mesh networking. Bluetooth 5.3, Thread, and Matter protocols are increasingly integrated, positioning the STB as a smart-home hub led by Comcast X1 and Sky Glass.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Type | Satellite STB |

29.4% |

2025 |

| Resolution | HD (High Definition) |

🔒 |

2025 |

| End User | Residential |

🔒 |

2025 |

| Service Type | PayTV |

🔒 |

2025 |

| Distribution | Offline Distribution |

68.5% |

2025 |

|

Region |

Asia Pacific |

41.3% |

2025 |

By Type

Satellite STB commands a 29.4% majority share in 2025, reflecting the entrenched DTH ecosystem across India, Brazil, and MENA. Cable STB at 24.6% holds strong in North America and Europe, although it faces structural cord-cutting pressure with ~6-7% annual US subscriber attrition.

To access detailed market analysis, Request Sample

Internet Protocol (IP) STB at 18.7% in 2025 is the fastest-scaling traditional delivery format, aligned with global FTTH deployment exceeding 1.3 billion homes passed by 2024. Digital Terrestrial Television (DTT) STB at 15.8% remains relevant in free-to-air Africa, Southeast Asia, and select European markets undergoing ASO transitions. Over-The-Top (OTT) STB at 11.5% is the highest-CAGR category at ~4.8% through 2034, driven by Android TV, Roku, and Apple TV.

By Distribution Channel

Offline Distribution dominates at 68.5% in 2025, reflecting the operator-led channel where STBs ship bundled with pay-TV subscriptions via installer networks, retail partners, and direct sales forces. Emerging-market cable and satellite operators rely almost exclusively on this channel.

Online Distribution at 31.5% in 2025 is the fastest-growing channel at ~3.4% CAGR through 2034, driven by e-commerce expansion (Amazon, JD.com, Flipkart) and direct-to-consumer OTT hardware sales (Roku, Google, Fire TV, Xiaomi Mi Box). The shift toward consumer-owned retail STBs is the primary growth vector in developed markets.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

41.3% |

India DTH + FTTH, China IPTV, ASEAN hybrid OTT-STB adoption |

|

Europe |

22.7% |

Android TV hybrid refresh, EU Ecodesign mandates, Sky/Orange rollouts |

|

North America |

20.6% |

Operator streaming STBs (Xfinity Flex, Xumo), IP migration |

|

Middle East & Africa |

8.4% |

Satellite DTH dominance, DVB-T2 ASO migrations, Saudi media |

|

Latin America |

7.0% |

Brazilian DTH base, Mexican IPTV rollout, mid-range OTT STB growth |

Asia Pacific commands a 41.3% global revenue share in 2025, the most dominant regional position in the global set-top box market. India (65+ million pay-TV subscribers) and China (400+ million IPTV households) form the volume backbone, while Indonesia, Vietnam, and the Philippines drive incremental DTH and hybrid OTT-STB demand across the region.

Europe at 22.7% in 2025 is anchored by Sky Group, Vodafone, Deutsche Telekom, and Orange, all actively replacing legacy boxes with Android TV and IP-first hybrid STBs under EU Ecodesign mandates. North America, at 20.6%, is characterised by structural cord-cutting and the shift toward operator-branded streaming STBs such as Xfinity Flex, Charter Xumo, and Verizon Stream TV. Middle East & Africa (8.4%) is led by Saudi Arabia, the UAE, and South Africa, where beIN, OSN, and DStv continue satellite-first deployments. Latin America (7.0%) is anchored by Brazil and Mexico, with SKY Brasil, Claro, and Izzi Telecom driving operator-led STB demand.

Competitive Landscape

|

Company Name |

Key Brand / Offerings |

Market Position |

Core Strength |

|

CommScope Technologies LLC |

CommScope Solutions |

Leader |

Pay-TV hybrid STBs, cable MSO relationships |

|

Vantiva |

Connected Home |

Leader |

Hybrid Android TV, carbon-neutral lines |

|

Humax Co., Ltd. |

Humax |

Leader |

DTH satellite STBs, European retail presence |

|

Sagemcom |

IP/DVB-T2 Ultra HD Set-top Box |

Challenger |

Android TV for telcos, eco-designed STBs |

|

Huawei Technologies Co., Ltd. |

CloudLink Box 200 |

Challenger |

Telco IPTV globally, Android TV, 4K/8K chips |

|

ZTE Corporation |

Android TV STB, Retail STB |

Challenger |

Low-cost IPTV STBs, emerging-market telcos |

|

Echostar Corporation |

dish |

Emerging |

DISH Network ecosystem, satellite DVR tech |

The set-top box competitive landscape is shaped by a handful of global Tier-1 OEMs serving pay-TV operators, alongside consumer electronics giants driving the OTT streaming-box segment. Chinese OEMs — Skyworth, Huawei, and ZTE — have emerged as aggressive challengers in both operator-led and retail channels, applying pricing pressure on European and Korean incumbents.

Key Company Profiles

CommScope Technologies LLC

CommScope Technologies LLC's product portfolio spans DOCSIS gateways, voice-enabled 4K STBs, and Android TV-certified hybrid devices.

- Product & Platform Portfolio: DCX series cable STBs, VIP hybrid IP boxes, VIP5002W voice 4K STB, Ruckus-integrated gateways, cloud-connected services.

- Recent Developments: In September 2025, CommScope and Comcast Accelerate Rollout of DOCSIS 4.0 Amplifiers.

- Strategic Focus: CommScope Technologies LLC concentrates on cable operator 10G migration, voice-first user experience, and tight integration between broadband gateway and video hardware. CommScope's platform software investments are positioning the brand for the Android TV-dominated next cycle.

Vantiva

Vantiva SA is a French multinational corporation that provides technology products and services for the communication, media, and entertainment industries.

- Product & Platform Portfolio: Android TV STBs, hybrid IP-DVB devices, fibre-optic gateways, carbon-neutral STB lines, Smart Home / CPE integration suite.

- Recent Developments: In April 2024, Vantiva announced that it has sold 22 million set-top boxes (STBs) powered by Android TVTM to date, strengthening its 25% market share as of the end of 2023 according to the latest Omdia STB 3Q23 report.

- Strategic Focus: VANTIVA prioritises Android TV platform leadership for telco customers, sustainability differentiation through carbon-neutral lines, and cross-sell between STB and broadband gateway product lines for integrated telco deployments.

Humax Co., Ltd.

Humax is a Korean consumer electronics manufacturer specialising in satellite, cable, and hybrid STBs, with strong retail presence in Europe, MENA, and Asia Pacific. The company's Aura Android TV and H-Series product lines anchor its premium European retail position.

- Product & Platform Portfolio: Humax HDR FVP series (UK DTT), Aura Android TV hybrid, NanoStream 4K, H3 operator-branded STBs, HMS middleware stack.

- Recent Developments: Humax launched the Aura EZ 4K set-top box in February 2026, featuring built-in Freely (UK), 4K HDR10+ support, and up to 2TB storage for 1,000 hours of recordings. This new Freeview Play recorder enables viewing over 75,000 hours of on-demand content and simultaneous recording of four channels while watching a fifth.

- Strategic Focus: Humax focuses on European DTH and DTT retail leadership, Android TV premium tier positioning, and hospitality sector expansion through operator-agnostic hybrid platforms.

Market Concentration Analysis

The global set-top box market exhibits moderate-to-high concentration among the top Tier-1 OEMs, with CommScope Technologies LLC, Vantiva, Humax Co., Ltd., Sagemcom, and Huawei Technologies Co., Ltd. collectively accounting for approximately 42-48% of global unit shipments in 2025. The remainder is fragmented across Chinese challengers, regional ODMs, and OTT streaming-box specialists.

The global set-top box market is experiencing a bifurcated structural dynamic. At the operator-hardware end, consolidation is occurring: complex hybrid STB architectures require sustained platform investment that only the largest OEMs can support, effectively excluding mid-size suppliers from flagship operator programmes.

Simultaneously, the OTT streaming-box retail segment is fragmenting further with Amazon Fire TV, Roku, Google Chromecast, and Xiaomi Mi Box competing on retail channels. Chinese OEMs' domestic market strength and export competitiveness are creating pricing pressure on European and Korean incumbents in emerging Africa, Southeast Asia, and Latin America deployments.

Investment & Growth Opportunities

Fastest-Growing Segments

OTT STB is the highest-growth type sub-segment at ~4.8% CAGR through 2034, powered by Android TV, Roku, and Apple TV proliferation and operator white-label streaming devices. Internet Protocol (IP) STB follows at ~3.9% CAGR, aligned with global FTTH rollouts exceeding 1.3 billion homes passed by 2024.

Emerging Market Expansion

India, Indonesia, Nigeria, and Vietnam represent the highest-potential growth markets, with combined net additions of ~20 million pay-TV households annually. DTH and hybrid OTT STBs are the primary hardware beneficiaries of these subscriber additions through 2030.

Venture & Private Investment Trends

Notable transactions include CommScope's portfolio optimisation, VANTIVA's post-spin capital raises, and venture rounds in Android TV-certified ODMs such as Skyworth Coocaa and Kaonmedia. Streaming-box specialists, including Roku and Xiaomi, continue attracting public equity flows tied to OTT adoption narratives.

Future Market Outlook (2026-2034)

The global set-top box market forecast projects measured value expansion from USD 24.21 Billion in 2025 to USD 27.34 Billion by 2034 at a CAGR of 1.31%. The modest growth rate reflects the mature state of the traditional STB industry, offset by hybrid OTT-STB upgrades, emerging-market penetration, and premium 4K/8K unit mix-up through the forecast period.

Two structural dynamics are most likely to reshape the market through 2034. First, the cable-to-IP migration in North America and Europe will progressively displace legacy cable STBs with IP-first hybrid Android TV devices. Second, the streaming-box retail channel will continue to decouple from pay-TV operators, with Amazon, Google, Roku, and Xiaomi capturing the bulk of incremental OTT volume.

By 2034, the set-top box industry is forecast to have completed much of its transition from a hardware-centric pay-TV accessory market to a platform-enabled hybrid aggregation ecosystem. Competitive differentiation will centre on Android TV certification, voice-AI integration, sustainability credentials, and operator cloud-service integration.

Research Methodology

Primary Research

Primary research encompassed over 45 structured interviews conducted in 2024-2025 with set-top box industry stakeholders, including STB OEM product directors, pay-TV operator hardware procurement leads, semiconductor business unit managers, middleware and CAS platform heads, and streaming-service device partnership teams. Primary insights validated market sizing, segmentation estimates, technology adoption timelines, and competitive dynamics.

Secondary Research

Secondary sources include ITU pay-TV data, GSMA Intelligence, Dataxis pay-TV reports, Omdia Set-Top Box tracker, Digital TV Research, company annual reports and investor materials, trade publications including Rapid TV News, Advanced Television, and Broadband TV News, and national regulator publications from TRAI, FCC, Ofcom, and ANATEL.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down (pay-TV households × ARPU) and bottom-up (unit shipment × ASP) models, incorporating GDP growth, broadband penetration, and household income indices. Scenario analysis (base, optimistic, and conservative cases) was performed to account for cord-cutting and OTT substitution sensitivities.

Set-Top Box Market Report Scope

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Cable STB, Satellite STB, Digital Terrestrial Television (DTT) STB, Internet Protocol (IP) STB, Over-The-Top (OTT) STB |

| Resolutions Covered | HD (High Definition), SD (Standard Definition), UHD (Ultra-High Definition) |

| End-Users Covered | Residential, Commercial |

| Service Types Covered | PayTV, Free-to-Air |

| Distributions Covered | Online Distribution, Offline Distribution |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | CommScope Technologies LLC, Vantiva, Humax Co., Ltd., Sagemcom, Huawei Technologies Co., Ltd., ZTE Corporation, Echostar Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the set-top box market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global set-top box market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the set-top box industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Set-Top Box Market Report

The global set-top box market was valued at USD 24.21 Billion in 2025, driven by emerging-market pay-TV expansion and hybrid OTT-STB adoption across the Asia Pacific and Europe.

The market is projected to reach USD 27.34 Billion by 2034, growing at a CAGR of 1.31% during 2026-2034, driven by OTT hybrid integration, 4K UHD upgrades, and IP migration.

Satellite STB leads with a 29.4% share in 2025, driven by the entrenched DTH ecosystem across India, Brazil, MENA, and Sub-Saharan Africa, where terrestrial broadband remains limited.

Offline Distribution dominates with a 68.5% share in 2025, reflecting the operator-led channel where STBs ship bundled with pay-TV subscriptions via installer networks.

Asia Pacific leads with a 41.3% share in 2025, driven by India's DTH scale, China's IPTV household base, and Southeast Asia's rapid hybrid OTT-STB adoption trend.

Key drivers include emerging-market pay-TV additions (20M annual), hybrid OTT-STB integration, 4K/8K UHD transition, DTT mandates, and operator replacement refresh cycles.

OTT STB is the fastest-growing at ~4.8% CAGR through 2034, driven by Android TV, Roku, and Apple TV proliferation and operator white-label streaming boxes.

Leading companies include CommScope Technologies LLC, Vantiva, Humax Co., Ltd., Sagemcom, Huawei Technologies Co., Ltd., ZTE Corporation, and Echostar Corporation.

OTT streaming is cannibalising traditional STB demand in developed markets, while simultaneously driving new demand for hybrid Android TV and operator-branded streaming devices.

Android TV powers over 200 million certified STBs globally, enabling shared app ecosystems, faster time-to-market, and over-the-air software updates for telco operators.

The outlook is one of modest, platform-led growth. Value is migrating from hardware to software, services, and operator-integrated user experience layers through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade