Skid Steer Loader Market Size, Share, Trends and Forecast by Operating Capacity, Power Train, End Use, and Region, 2026-2034

Skid Steer Loader Market Size and Share:

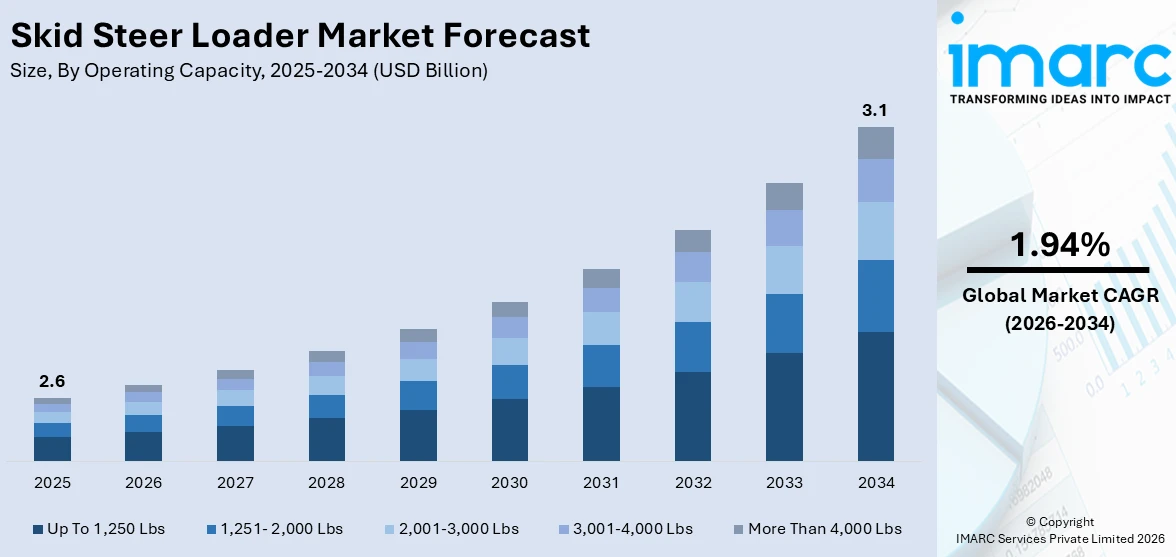

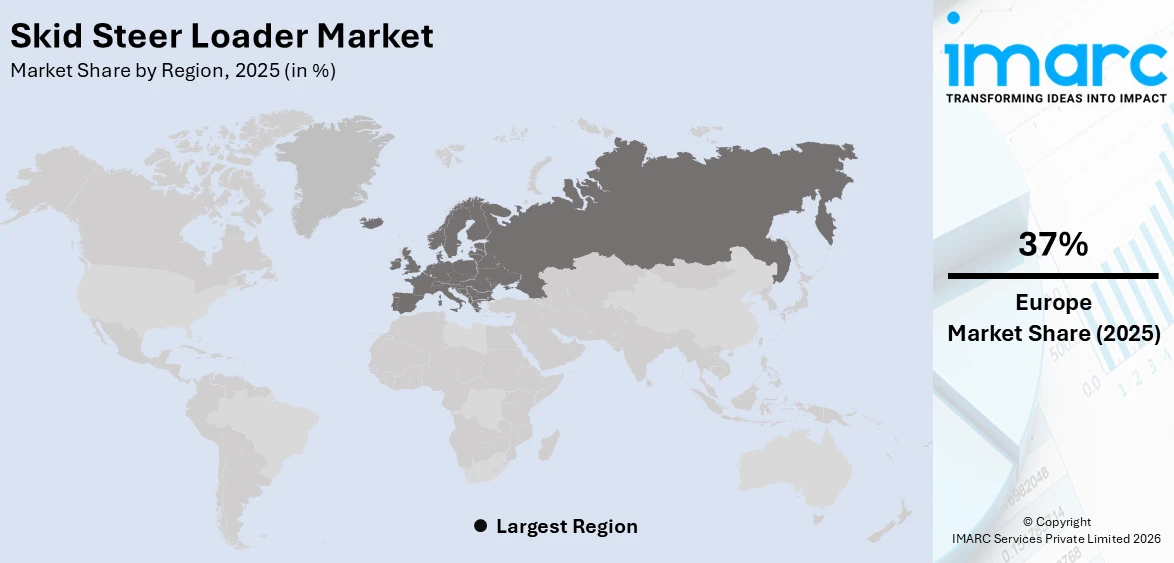

The global skid steer loader market size was valued at USD 2.6 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 3.1 Billion by 2034, exhibiting a CAGR of 1.94% from 2026-2034. Europe currently dominates the market, holding a market share of 37% in 2025. The region benefits from advanced construction standards, strong government investment in infrastructure modernization, and the widespread adoption of compact machinery across residential and commercial building projects, supported by strict emission norms driving demand for efficient equipment, thereby influencing the skid steer loader market share.

The global skid steer loader market is being driven by the escalating demand for compact and versatile construction equipment across both developed and developing economies. Rapid urbanization, coupled with an increasing number of infrastructure development projects encompassing highways, bridges, airports, and residential complexes, is propelling the need for maneuverable machinery that can operate efficiently in confined spaces. Furthermore, the growing mechanization of agriculture and landscaping activities is augmenting market expansion, as skid steer loaders offer multifunctional capabilities through diverse attachment options, including trenchers, augers, and grapples. The rising preference for rental and leasing models among small- and medium-sized contractors is further broadening market access by reducing upfront capital expenditure. Additionally, advancements in hydraulic systems, enhanced fuel efficiency, and improved operator comfort features are making these machines increasingly attractive, thereby contributing to the skid steer loader market growth.

The United States has emerged as a major region in the skid steer loader market owing to many factors. The country's robust construction activity, bolstered by federal investment in public infrastructure, transportation networks, and energy systems, is generating sustained demand for compact construction equipment. The Infrastructure Investment and Jobs Act continues to support a pipeline of highway, bridge, and water utility projects, directly increasing deployment of versatile earthmoving machinery. According to the US Census Bureau, public construction spending in the United States reached approximately USD 516.8 billion in 2025, representing a 3.6% increase compared to the prior year, thereby reinforcing demand for equipment across road building and municipal development projects. Moreover, the expanding adoption of skid steer loaders in residential landscaping, snow removal, and agricultural operations is strengthening equipment utilization beyond traditional construction applications, creating a broad base of end users across the nation.

To get more information on this market Request Sample

Skid Steer Loader Market Trends:

Growing Electrification of Equipment

The increasing shift toward electric and hybrid models represents a significant development in the skid steer loader market. Manufacturers are introducing battery-powered variants that deliver zero tailpipe emissions, lower noise levels, and reduced maintenance requirements compared to conventional diesel-hydraulic counterparts. These electric loaders are particularly suited for indoor applications, urban job sites, and environmentally sensitive areas where air quality and noise regulations are stringent. Advanced lithium-ion battery technology is enabling longer operational runtimes and faster charging cycles, improving the practical viability of electric equipment for daily commercial use. For instance, in February 2025, Tobroco-Giant, a Netherlands-based manufacturer of compact machinery, officially entered the electric equipment segment with the launch of two fully electric skid steer loaders, the GS900E wheeled model and the GS950TE tracked model. These models are built on the same platform as their combustion engine counterparts, aiming to deliver robust performance alongside environmental benefits.

Integration of Telematics and Smart Controls

The integration of telematics, automation, and intelligent control systems is transforming operational efficiency and fleet management in the skid steer loader market. Modern skid steer loaders are increasingly equipped with GPS tracking, remote diagnostics, real-time performance monitoring, and predictive maintenance capabilities that enable operators and fleet managers to optimize machine utilization and minimize downtime. Self-leveling loader arms, automated bucket functions, and customizable joystick controls are enhancing precision and reducing operator fatigue, particularly on repetitive tasks. These technological advancements are appealing to contractors who prioritize productivity gains and data-driven decision-making. For instance, in September 2025, Caterpillar Inc. launched eight new next-generation skid steer loader and compact track loader models, including the Cat 250, 260, 270, and 270 XE, featuring upgraded engine power, enhanced stability, and closed-center auxiliary hydraulics at 3,500 psi, representing a ground-up redesign to improve performance and technology integration. These developments are indicative of the positive skid steer loader market outlook.

Expanding Applications in Diverse Sectors

The widening range of applications beyond traditional construction is driving diversified demand for skid steer loaders across agriculture, landscaping, warehousing, and municipal services. The availability of over 100 different attachment types, including pallet forks, snowblowers, cold planers, and tree cutters, allows a single machine to replace multiple pieces of specialized equipment, enhancing cost efficiency and operational versatility for end users. This multifunctionality is particularly attractive to small- and medium-scale contractors and farm operators who require adaptable solutions for varied tasks. The agriculture sector is witnessing growing adoption for tasks such as feed handling, barn cleaning, and land preparation. For instance, according to the Indian government, India's National Infrastructure Pipeline targets USD 1.4 trillion in capital expenditure, creating a substantial base of demand for compact machinery. This expanding application scope is supporting the skid steer loader market forecast.

Skid Steer Loader Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global skid steer loader market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on operating capacity, power train, and end use.

Analysis by Operating Capacity:

- Up To 1,250 Lbs

- 1,251- 2,000 Lbs

- 2,001-3,000 Lbs

- 3,001-4,000 Lbs

- More Than 4,000 Lbs

Up To 1,250 Lbs holds 30% of the market share. Skid steer loaders with an operating capacity of up to 1,250 lbs are specifically designed for light-duty tasks, making them highly suitable for residential construction, small-scale landscaping, and limited agricultural operations. Their compact dimensions and lightweight build allow these machines to navigate tight spaces, narrow pathways, and indoor environments with exceptional maneuverability. These loaders consume less fuel and are easier to transport between job sites compared to larger models, reducing operational costs for small contractors and independent operators. Moreover, the relatively lower purchase and rental costs within this operating capacity segment make these machines more accessible to a broader range of end users, including small and mid-sized contractors. Growing investments in infrastructure, particularly in smart and sustainable construction initiatives across Europe, are further supporting demand for compact equipment. Their affordability, versatility, and suitability for confined urban job sites position them as practical solutions for modern construction requirements.

Analysis by Power Train:

- Electric

- Conventional

Conventional leads the market with a share of 85%. Conventional diesel-powered skid steer loaders continue to dominate the market, driven by their proven reliability, high power output, and extensive refueling infrastructure across both urban and remote job sites. Diesel engines provide better torque and maintain performance at full load, and it is essential in demanding operations like excavation, material handling, and site grading. The geographical presence of diesel fuel all over the world ensures that operations are not interrupted in the various geographical locations. Fleet operators and contractors prefer to use traditional models because they are less expensive to purchase, they have developed maintenance networks and are familiar with how they operate. Also, the further development of engine technology has provided better fuel economy, reduced the number of particulates, and allowed equipment manufacturers to comply with the stricter environmental requirements. Across the European construction sector, updated machinery regulations have introduced revised safety and sustainability requirements, prompting manufacturers to incorporate cleaner engines, advanced emission control systems, and improved operational safeguards. These regulatory developments are accelerating the transition toward more environmentally responsible and compliant construction equipment across the region.

Analysis by End Use:

Access the comprehensive market breakdown Request Sample

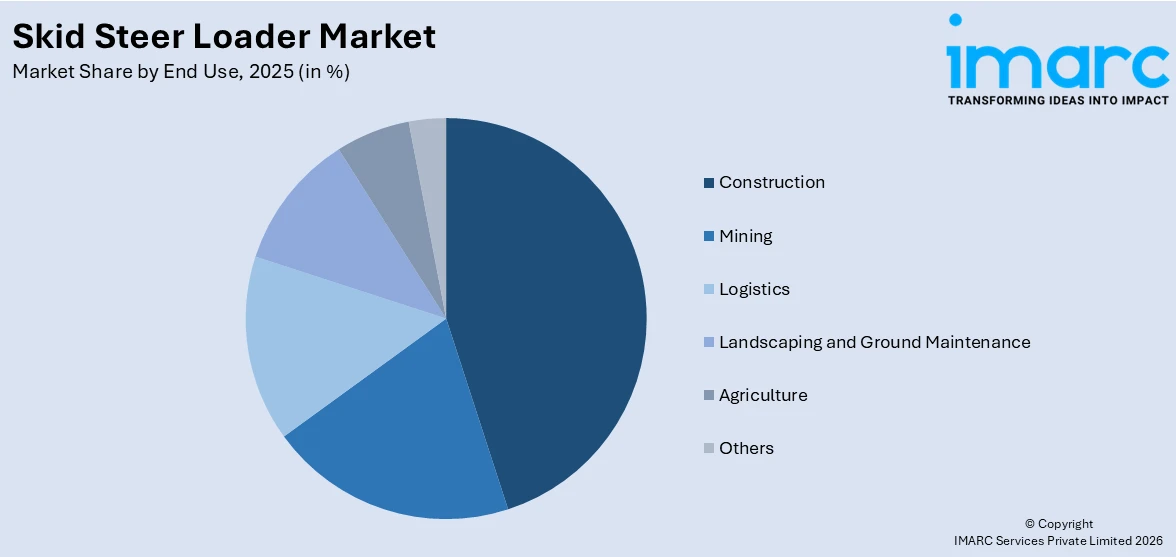

- Construction

- Mining

- Logistics

- Landscaping and Ground Maintenance

- Agriculture

- Others

Construction dominates the market, with a share of 45%. The construction sector accounts for the largest share of the skid steer loader market demand, driven by the versatility of these machines for site preparation, excavation, grading, demolition, and material handling. Skid steer loaders are also highly valued on construction sites due to their small footprint, which allows them to be used in congested urban locations and areas that may be inaccessible to large equipment. Demand among construction end users is being maintained by the continuous growth of residential, commercial, and public infrastructure projects in the world. Also, the ability to quickly change attachments such as buckets, breakers, and cement mixers will increase productivity and minimise the need for numerous specialised machines on a single project. For instance, according to Germany's Federal Transport Infrastructure Plan, the government has earmarked significant investment toward upgrading road, rail, and waterway infrastructure through 2030, supporting sustained equipment demand.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

Europe, accounting for 37% of the share, enjoys the leading position in the market. The region's dominance is underpinned by substantial government investment in infrastructure modernization, stringent environmental regulations encouraging adoption of advanced and energy-efficient machinery, and a mature construction equipment rental market that facilitates widespread equipment access. The European Union's Trans-European Transport Network initiative and Recovery and Resilience Facility funds are channeling significant capital into cross-border connectivity projects, housing developments, and green building programs across major economies including Germany, France, and the United Kingdom. Additionally, the region's emphasis on sustainable construction practices and low-emission zones in urban areas is accelerating demand for compact, fuel-efficient, and increasingly electric equipment. For instance, Europe's equipment rental sector generated approximately EUR 33.9 billion in revenue during 2025, with Germany, France, and the United Kingdom collectively accounting for nearly 60% of this market, reflecting strong equipment utilization across the region.

Key Regional Takeaways:

North America Skid Steer Loader Market Analysis

The North American skid steer loader market is supported by extensive infrastructure development programs, a well-established equipment rental industry, and strong demand from the construction, agriculture, and landscaping sectors. The region benefits from a highly mechanized construction environment where contractors routinely deploy compact equipment to maximize efficiency on diverse project types, ranging from highway rehabilitation to residential site preparation. Federal investment programs, particularly the Infrastructure Investment and Jobs Act, which allocated USD 550 billion for transportation infrastructure, broadband expansion, and energy systems, continue to provide a robust project pipeline driving equipment utilization. Additionally, the growing trend of equipment rental over ownership among small and mid-sized contractors is broadening market access and supporting higher fleet turnover rates. Technological advancements, including telematics-enabled fleet management and improved hydraulic systems, are further enhancing machine productivity and appeal. The expanding use of skid steer loaders for snow removal, municipal maintenance, and waste management applications also contributes to year-round equipment demand across the region, supporting steady skid steer loader market trends.

United States Skid Steer Loader Market Analysis

The United States represents a key contributor to the skid steer loader market within North America, driven by the scale of its construction industry, agricultural mechanization, and robust infrastructure investment programs. The country's diverse end-use landscape, spanning residential and commercial construction, road building, landscaping, agriculture, and municipal services, ensures consistent demand across multiple application segments throughout the year. Federal programs and state-level infrastructure initiatives are generating a sustained pipeline of projects that require compact, versatile earthmoving equipment. The rapid expansion of data center construction and renewable energy installations is creating new demand avenues for compact loaders on specialized job sites. Furthermore, the growing adoption of electric and hybrid models in environmentally sensitive urban areas is shaping equipment procurement decisions among forward-looking contractors. For instance, in April 2024, FIRSTGREEN Industries launched ROCKEAT, a new line of electric, cabinless skid steer loaders. Featuring a low-clearance design, 360-degree camera system, and remote operation, the machines are built to improve safety and efficiency in mining, construction, and other hazardous environments.

Europe Skid Steer Loader Market Analysis

Europe holds the leading position in the global skid steer loader market, supported by advanced construction standards, strong government investment in infrastructure modernization, and a mature equipment rental ecosystem. The European Union's commitment to sustainable development, through initiatives such as the European Green Deal and the Trans-European Transport Network, is channeling substantial capital into transportation, housing, and green building projects across the continent. Strict emission regulations, including Stage V compliance requirements and emerging municipal zero-emission mandates, are encouraging adoption of cleaner, more efficient equipment, including electric and hybrid models. Countries including Germany, France, and the United Kingdom serve as key demand centers, collectively driving significant equipment procurement and rental activity. Urban redevelopment programs and housing construction initiatives are further boosting demand for compact machinery that can operate efficiently in space-constrained environments. For instance, according to Eurostat, construction activities accounted for approximately 9% of the European Union's GDP, highlighting the sector's significance and its sustained demand for specialized equipment.

Asia-Pacific Skid Steer Loader Market Analysis

The Asia-Pacific region is experiencing accelerating demand for skid steer loaders, propelled by rapid urbanization, large-scale infrastructure development, and increasing agricultural mechanization across key economies. Countries such as China and India are making substantial investments in transportation networks, smart city development, and industrial corridors that necessitate versatile compact equipment. Government-backed initiatives, including China's Belt and Road Initiative and India's Bharatmala highway program, are creating extensive construction activity that drives equipment demand. The growing rental market in the region is also improving equipment accessibility for smaller operators. For instance, in June 2024, CASE Construction Equipment introduced its domestically manufactured Skid Steer Loader (SSL) to the Indian market, produced at its advanced facility in Pithampur, Madhya Pradesh. The company had earlier announced the launch of the indigenously developed model during the previous edition of CII EXCON, marking the expansion of its product portfolio in India.

Latin America Skid Steer Loader Market Analysis

The Latin American skid steer loader market is witnessing gradual expansion, driven by infrastructure development programs, urban expansion, and growing construction activity in key economies such as Brazil and Mexico. Government investment in transportation, energy, and housing projects is supporting demand for compact construction equipment across the region. The increasing mechanization of agricultural operations and expansion of mining activities are further contributing to market growth. For instance, Brazil's national infrastructure program has prioritized investment in road construction and port modernization, with federal highway investment reaching approximately BRL 30 billion in 2025, creating opportunities for compact equipment deployment across diverse projects.

Middle East and Africa Skid Steer Loader Market Analysis

The Middle East and Africa region is experiencing growing demand for skid steer loaders, supported by large-scale infrastructure projects, urban development initiatives, and expanding construction activity in key economies. State-backed economic diversification initiatives, especially across the Gulf Cooperation Council nations, are stimulating increased capital allocation toward residential, commercial, and transport infrastructure developments. Saudi Arabia's Vision 2030 and the UAE's urban master plans are generating significant construction activity that requires versatile compact equipment. For instance, according to industry reports, the GCC construction equipment market size reached USD 4.8 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 10.0 Billion by 2033, exhibiting a growth rate (CAGR) of 7.7% during 2025-2033, indicating robust equipment demand growth across the region.

Competitive Landscape:

The competitive landscape of the global skid steer loader market is characterized by the presence of several established players who are actively pursuing strategies including product innovation, strategic acquisitions, geographic expansion, and technology integration to strengthen their market positions. Leading manufacturers are investing in the development of next-generation models featuring enhanced engine performance, advanced telematics systems, improved operator comfort, and electric powertrain options to address evolving customer requirements and regulatory standards. The market is witnessing consolidation activity as companies seek to expand their product portfolios and geographic reach. Equipment rental companies are also playing an increasingly influential role in shaping purchasing and technology adoption trends. Additionally, players are focusing on aftermarket services, digital fleet management solutions, and customized attachment offerings to differentiate themselves and build long-term customer relationships.

The report provides a comprehensive analysis of the competitive landscape in the skid steer loader market with detailed profiles of all major companies, including:

- The Volvo Group

- Yanmar Power Technology Co. Ltd.

- Doosan Infracore Co. Ltd.

- Caterpillar Inc.

- CNH Industrial N.V.

- Deere & Company

- J C Bamford Excavators Ltd

- Komatsu Ltd.

- Kubota Corporation

- Wacker Neuson SE

Latest News and Developments:

- In December 2025, Doosan Bobcat Inc. entered advanced discussions regarding the possible acquisition of a majority stake in Wacker Neuson SE, a German manufacturer of light and compact construction equipment. The proposed transaction involves the acquisition of approximately 63% of Wacker Neuson's share capital from major shareholders, followed by a public all-cash takeover offer to remaining shareholders. The deal, if completed, would significantly expand Doosan Bobcat's presence in Europe and broaden its compact equipment product portfolio.

- In February 2025, Komatsu unveiled two additions to its compact equipment lineup: a newly developed 4-tonne skid steer loader and a 5-tonne compact track loader at Bauma 2025, the renowned international trade fair for construction and infrastructure. As a prominent global producer of construction and mining machinery, the company introduced these models to strengthen its presence in the compact equipment segment and address evolving job-site requirements.

Skid Steer Loader Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Operating Capacities Covered | Up To 1,250 Lbs, 1,251- 2,000 Lbs, 2,001-3,000 Lbs, 3,001-4,000 Lbs, More Than 4,000 Lbs |

| Power Trains Covered | Electric, Conventional |

| End Uses Covered | Construction, Mining, Logistics, Landscaping and Ground Maintenance, Agriculture, Others |

| Regions Covered | North America, Asia Pacific, Europe, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, China, Japan, India, South Korea, Australia, Indonesia, Germany, France, United Kingdom, Italy, Spain, Russia, Brazil, Mexico |

| Companies Covered | The Volvo Group, Yanmar Power Technology Co. Ltd., Doosan Infracore Co. Ltd., Caterpillar Inc., CNH Industrial N.V., Deere & Company, J C Bamford Excavators Ltd, Komatsu Ltd., Kubota Corporation, Wacker Neuson SE, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the skid steer loader market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global skid steer loader market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the skid steer loader industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Skid Steer Loader Market Report

The skid steer loader market was valued at USD 2.6 Billion in 2025.

The skid steer loader market is projected to exhibit a CAGR of 1.94% during 2026-2034, reaching a value of USD 3.1 Billion by 2034.

Key factors driving the skid steer loader market include the rising demand for compact and versatile construction equipment, rapid urbanization and expanding infrastructure development globally, increasing mechanization in agriculture and landscaping, the growing trend toward equipment rental models, and technological advancements in engine efficiency, telematics, and electric powertrains.

Europe currently dominates the skid steer loader market, accounting for a share of 37%. The region's leading position is driven by substantial government investment in infrastructure modernization, stringent environmental regulations promoting efficient machinery, and a mature equipment rental ecosystem.

Some of the major players in the skid steer loader market include The Volvo Group, Yanmar Power Technology Co. Ltd., Doosan Infracore Co. Ltd., Caterpillar Inc., CNH Industrial N.V., Deere & Company, J C Bamford Excavators Ltd, Komatsu Ltd., Kubota Corporation, Wacker Neuson SE, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)