Skin Care Products Market Size, Share, Trends and Forecast by Product Type, Ingredient, Gender, Distribution Channel, and Region, 2026-2034

Skin Care Products Market Size, Share, Trends & Forecast (2026-2034)

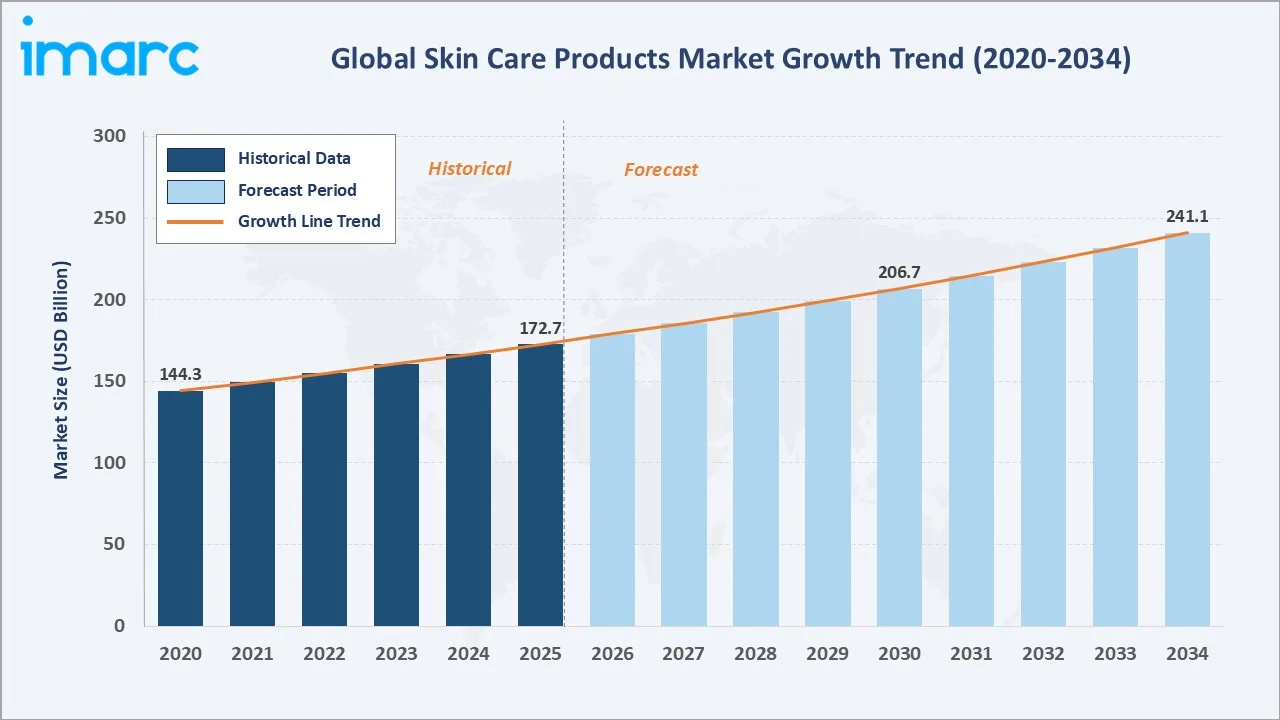

The global skin care products market reached USD 172.7 Billion in 2025 and is projected to reach USD 241.1 Billion by 2034, growing at a CAGR of 3.66% during 2026-2034. Rising health and wellness consciousness, accelerating premiumization and anti-aging demand, expanding e-commerce and direct-to-consumer channels, clean beauty and natural ingredient trends, and growing male grooming adoption are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 172.7 Billion |

|

Forecast Market Size (2034) |

USD 241.1 Billion |

|

CAGR (2026-2034) |

3.66% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

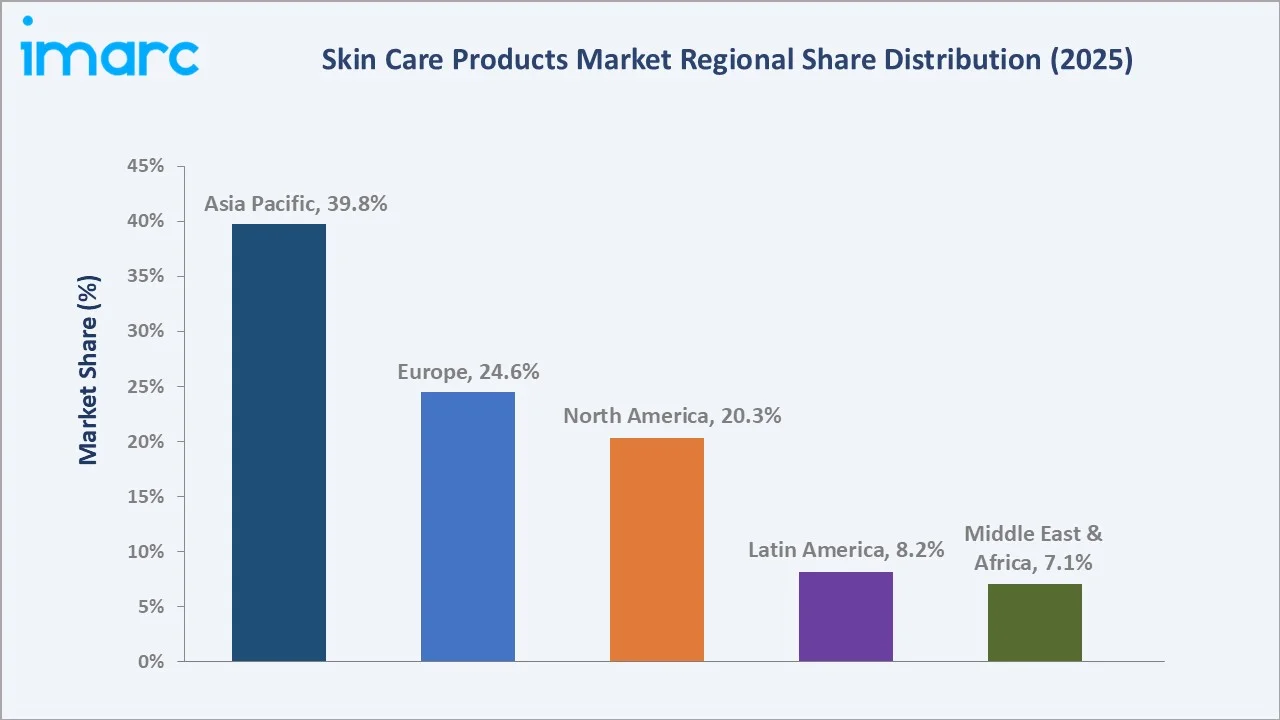

Asia Pacific leads regionally with a 39.8% share in 2025, anchored by China, Japan, and South Korea's dominant consumption and rapidly expanding demand across India and Southeast Asia. Chemical ingredients account for 63.5% of the ingredient breakdown, while female consumers represent 62.4% of the gender segment, reflecting the structurally female-skewed historical consumption base.

To get more information on this market, Request Sample

The market grew from USD 144.3 Billion in 2020 to USD 172.7 Billion in 2025, reflecting a historical CAGR of approximately 3.66%. The forecast period is supported by sustained premiumization, accelerating natural and clean beauty adoption, expansion of e-commerce and D2C channels, and rising male and unisex segment consumption. The market reaches USD 206.7 Billion by 2030 before expanding to USD 241.1 Billion by 2034.

Executive Summary

The global skin care products market is experiencing steady expansion driven by converging consumer trends in health and wellness, anti-aging demand, premium skin care adoption, clean beauty and natural ingredient preferences, and the rising prominence of male grooming. The market reached USD 172.7 Billion in 2025 and is forecast to reach USD 241.1 Billion by 2034, growing at a CAGR of 3.66%.

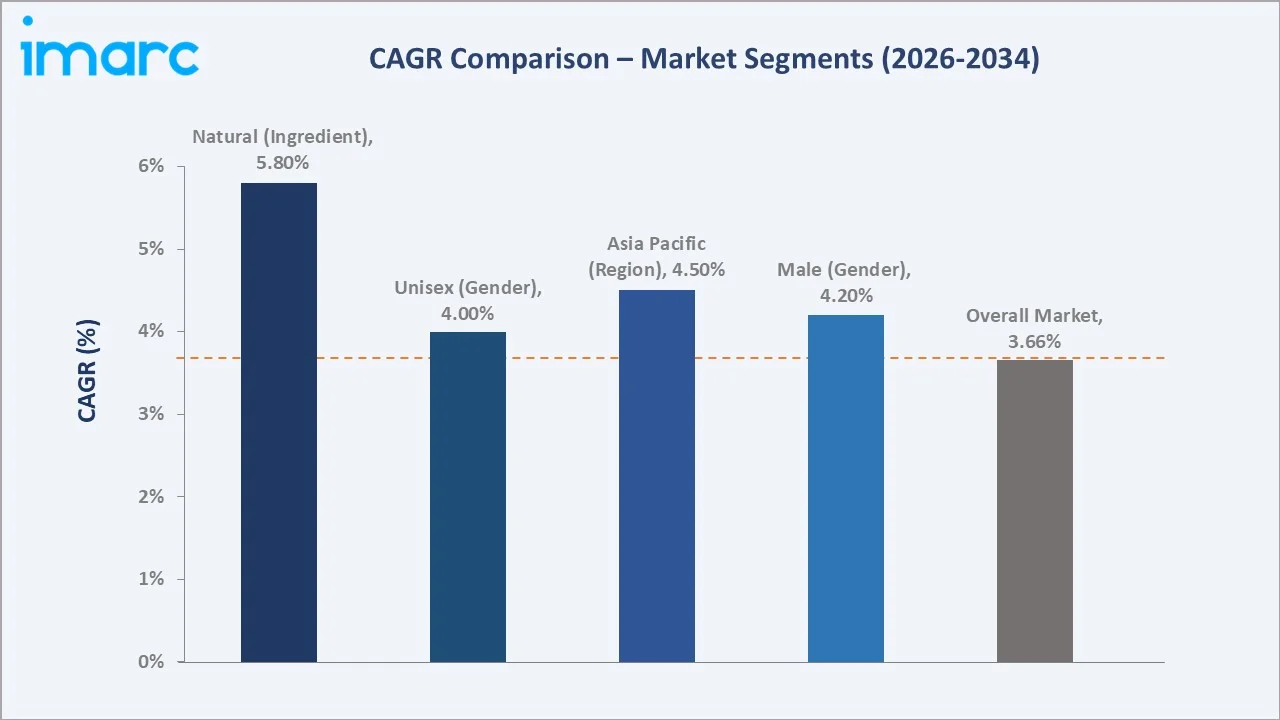

Chemical-based ingredients dominate the ingredient segment with a 63.5% share in 2025, reflecting their efficacy advantages in active dermatological formulations such as retinoids, peptides, hyaluronic acid synthetics, and proven anti-aging compounds. Natural ingredients at 36.5% represent the fastest-growing ingredient sub-segment at approximately 5.8% CAGR, driven by clean beauty trends, plant-based actives, and consumer demand for botanical and bio-derived formulations.

Female consumers command the largest gender share at 62.4%, reflecting the historically female-skewed consumption base. Male grooming at 21.3% is the fastest-growing gender segment at approximately 4.2% CAGR, supported by L'Oréal Men Expert, Nivea Men, and emerging D2C male skin care lines. Asia Pacific commands 39.8% of the regional share and is the fastest-growing region at approximately 4.5% CAGR.

Key Market Insights

|

Insight |

Data |

|

Largest Ingredient Segment |

Chemical – 63.5% share (2025) |

|

Fastest Growing Ingredient |

Natural – ~5.8% CAGR (2026-2034) |

|

Largest Gender Segment |

Female – 62.4% share (2025) |

|

Fastest Growing Gender |

Male – ~4.2% CAGR (2026-2034) |

|

Leading Region |

Asia Pacific – 39.8% share (2025) |

|

Top Companies |

L’OREAL S.A., The Estée Lauder Companies, Unilever, Procter & Gamble, and Shiseido Company, Limited |

Key Analytical Observations Supporting the Above Data:

- Chemical-based ingredients at 63.5% (2025) reflect the structural importance of clinically proven actives including retinoids, peptides, niacinamide, AHAs/BHAs, and hyaluronic acid in anti-aging, brightening, and dermatological skin care.

- Natural ingredients at 36.5% (2025), growing at approximately 5.8% CAGR, represent the highest-growth ingredient sub-segment, driven by clean beauty trends, plant-based actives, and rising consumer demand for botanical, vegan, and bio-derived formulations.

- Female consumers at 62.4% (2025) reflect the historically female-skewed skin care consumption base. Male grooming at 21.3% is the fastest-growing gender segment at approximately 4.2% CAGR, supported by L'Oréal Men Expert, Nivea Men, Bulldog, and emerging direct-to-consumer male skin care lines.

- Asia Pacific's 39.8% share (2025) is structurally anchored by China (growing exports of cosmetics in 2025), Japan (premium and K-beauty influence), and South Korea (K-beauty global export hub). India, Southeast Asia, and emerging Asia represent the fastest-growing within Asia Pacific, contributing to the region's ~4.5% CAGR.

Skin Care Products Market Overview

Skin care products encompass a broad range of formulations including face creams, body lotions, serums, cleansers, masks, sunscreens, and treatment products designed for cleansing, moisturizing, protecting, and treating the skin. The global skin care products market spans chemical and natural ingredient categories, multiple gender segments, and a diversified distribution landscape spanning supermarkets, beauty parlors, multi-branded retail, online platforms, exclusive retail, and salons.

The market is shaped by three structural forces: rising global health, wellness, and beauty consciousness, with skin care consumption increasingly viewed as part of holistic self-care; digital transformation of beauty retail through e-commerce, social media-driven discovery, and direct-to-consumer brand emergence; and consumer-led ingredient sophistication, with shoppers increasingly informed about active ingredients, formulation science, and sustainability credentials.

Market Dynamics

To evaluate market opportunities, Request Sample

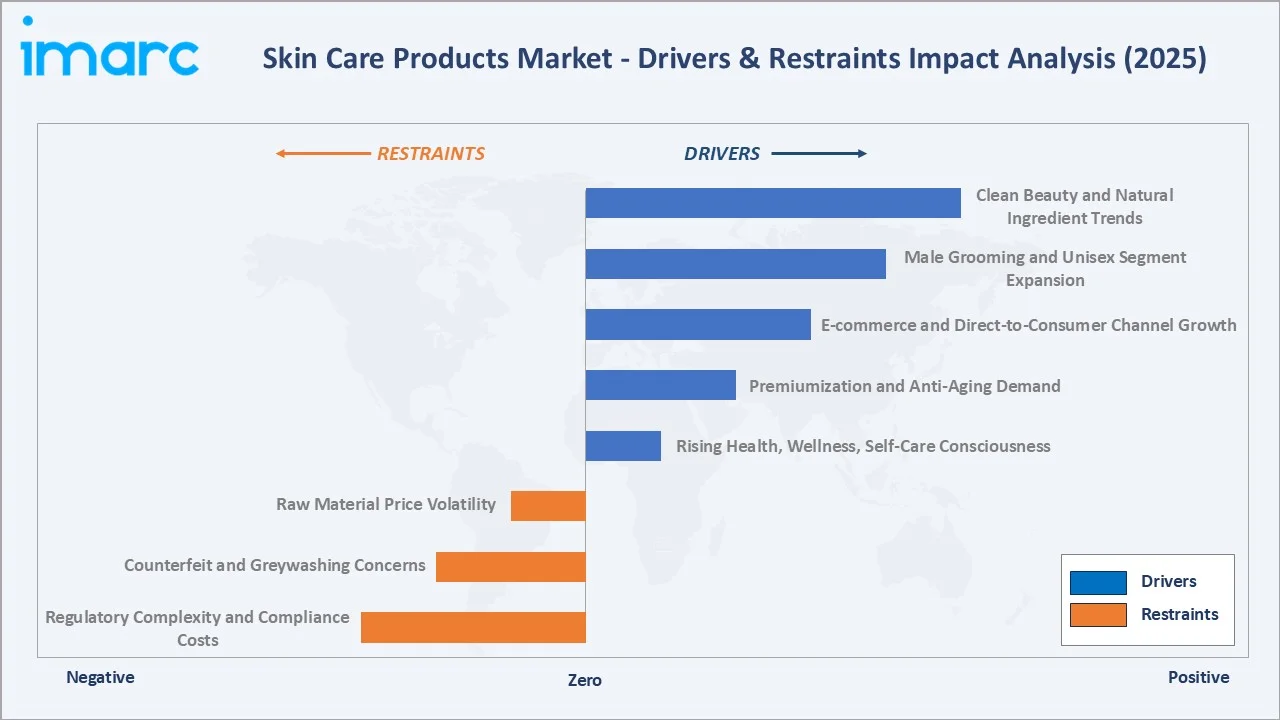

Market Drivers

- Rising Health, Wellness, and Self-Care Consciousness: Consumer interest in holistic self-care has elevated skin care from a beauty product to a wellness staple. Social media-driven education around active ingredients, SPF, and routine-building accelerates daily skin care adoption across age groups.

- Premiumization and Anti-Aging Demand: Aging consumers in mature markets and aspirational premium consumption in emerging markets are driving trade-up to premium and prestige skin care. Anti-aging serums, retinoid treatments, and peptide-rich formulations command 3–5× the price of mass-market equivalents.

- E-commerce and Direct-to-Consumer Channel Growth: Online channels are expanding rapidly through D2C premium brands, Amazon's beauty category, China's Tmall and JD platforms, and social commerce. Online platforms enable ingredient education and personalized recommendations.

- Male Grooming and Unisex Segment Expansion: Male grooming is among the fastest-growing segments, supported by L'Oréal Men Expert, Nivea Men, Bulldog, and Lumin. Gen Z's gender-fluid approach is also expanding the unisex segment via brands such as Aesop and Kiehl's.

- Clean Beauty and Natural Ingredient Trends: Consumer preference for natural, organic, vegan, and clean-label skin care is driving rapid growth in plant-based actives, botanical extracts, and bio-derived ingredients.

Market Restraints

- Regulatory Complexity and Compliance Costs: Skin care ingredient regulations across the EU, US FDA, China NMPA, and other jurisdictions impose registration, testing, and labeling requirements that increase product development cycles and costs, particularly for novel actives and natural ingredients.

- Counterfeit and Greywashing Concerns: Counterfeit premium skin care, particularly in e-commerce and emerging markets, undermines brand equity and consumer trust. Greenwashing claims around clean beauty without verified substantiation create regulatory and reputational risks.

- Raw Material Price Volatility: Active ingredients including hyaluronic acid, peptides, retinoids, and specialty botanicals face price volatility driven by supply concentration, regulatory restrictions, and climate-driven agricultural inputs. Packaging material cost inflation also pressures margins.

Market Opportunities

- Personalized Skin Care and AI Diagnostics: AI-powered skin diagnostics, personalized formulation services, and DNA-based skin care recommendations represent emerging high-margin opportunities. Brands including L'Oréal ModiFace and Estée Lauder's Le Labo customization are pioneering this segment.

- India and Emerging Asia Expansion: India's per-capita skin care consumption remains a fraction of mature-market levels, indicating significant structural growth headroom. South Korea-style K-beauty is also driving Southeast Asian and global consumer interest in trend-driven product launches.

Market Challenges

- Market Saturation in Developed Regions: North America and Western Europe face mature-market saturation with limited unit volume growth, requiring brands to compete on premiumization, innovation, and consumer engagement rather than category expansion.

- Sustainability and Packaging Pressures: Consumer and regulatory demand for sustainable, refillable, and low-plastic packaging requires significant reformulation and supply-chain investment by established players.

Emerging Market Trends

1. Clean Beauty and Bio-Based Ingredient Innovation

Clean beauty has evolved from niche trend to mainstream consumer expectation. Bio-fermented hyaluronic acid, plant-derived squalane, bakuchiol, and probiotics are scaling rapidly. Leading brands are reformulating to remove parabens, sulfates, and synthetic fragrances, with EU Cosmetics Regulation and California's Toxic-Free Cosmetics Act reinforcing the shift.

2. K-Beauty and Cross-Cultural Beauty Influences

K-beauty's global influence continues with multi-step routines, sheet masks, snail mucin, and centella-based products becoming mainstream. Korean indie brands and global majors with Korean R&D operations are setting trends that propagate across Asia Pacific, North America, and Europe.

3. Personalized Skin Care and AI Diagnostics

AI-powered skin analysis (L'Oréal ModiFace), personalized formulation services (Curology), and DNA-based recommendations are scaling. These technologies enable brands to capture data-driven loyalty and command premium pricing for customized formulations.

4. Sustainable and Refillable Packaging

Refillable formats, post-consumer recycled plastics, glass alternatives, and biodegradable packaging are scaling across premium and mass-market tiers. L'Oréal unveiled its 2030 sustainability targets with a strong focus on packaging, aiming to ensure that all plastic packaging is refillable, reusable, recyclable, or compostable, driving systematic packaging redesign across its skin care portfolios.

Industry Value Chain Analysis

The skin care products value chain spans raw material and active ingredient supply through downstream retail and consumer engagement, with significant value creation at the formulation R&D, brand marketing, and retail merchandising stages. Premium brand equity, ingredient innovation, and consumer relationships drive differential margin across mass-market versus prestige tiers.

|

Stage |

Key Players / Examples |

|

Raw Material & Ingredients |

Global specialty chemical suppliers; active ingredient innovators; biotechnology and fermentation-based ingredient houses |

|

Formulation & R&D |

In-house R&D divisions of major beauty conglomerates; specialized cosmetic science labs; clinical and dermatological testing partners |

|

Manufacturing & Filling |

Brand-owned manufacturing facilities; contract manufacturers and CDMOs; specialist filling and packaging operators |

|

Branding & Marketing |

Global FMCG and beauty conglomerates; pure-play prestige beauty houses; dermatological skin care brand owners |

|

Distribution & Retail |

Beauty specialty retailers; pharmacy and drugstore chains; mass-market supermarkets and hypermarkets; e-commerce and digital marketplaces |

Technology Landscape in the Skin Care Products Industry

Active Ingredient Formulation and Encapsulation

Advanced delivery systems including liposomes, nanoemulsions, and polymeric microcapsules enable controlled release and improved bioavailability of active ingredients such as retinoids, vitamin C, and peptides. Leading ingredient suppliers operate dedicated personal care innovation centers serving global skin care formulators.

Clean Beauty and Bio-Based Ingredient Technology

Biotechnology platforms producing fermented hyaluronic acid, plant-cell-cultured actives, and biosynthetic squalane are scaling. Companies such as Geltor and Evolva supply major brands transitioning to clean-beauty positioning.

Personalized Skin Care and AI Diagnostics

AI-powered skin analysis platforms (L'Oréal ModiFace) deploy computer vision to assess skin condition and recommend products. DNA-based personalized skin care and AI-formulated custom skin care represent the emerging personalization frontier.

Sustainable and Refillable Packaging Innovation

Refillable packaging systems, post-consumer recycled plastic adoption, mono-material packaging for recyclability, and biodegradable packaging materials are scaling across skin care. Major brands have committed to 50–100% sustainable packaging by 2030, driving systematic packaging innovation.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Ingredient |

Chemical |

63.5% |

2025 |

|

Gender |

Female |

62.4% |

2025 |

|

Product Type |

🔒 |

🔒 |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

Region |

Asia Pacific |

39.8% |

2025 |

By Ingredient

Chemical ingredients dominate the ingredient segment with a 63.5% share in 2025. This category includes synthetic actives such as retinoids, peptides, niacinamide, hyaluronic acid synthetics, AHAs/BHAs, and proven anti-aging compounds. Chemical formulations dominate premium dermatologist-recommended and prestige segments where clinical efficacy substantiation is critical.

To access detailed market analysis, Request Sample

Natural ingredients at 36.5% represent the fastest-growing ingredient sub-segment at approximately 5.8% CAGR, driven by clean beauty trends, plant-based actives, and consumer demand for botanical, vegan, and bio-derived formulations. Brands including The Body Shop, L'Occitane, Origins, Burt's Bees, and emerging clean-beauty entrants anchor this segment, alongside major brand portfolios pivoting to natural sub-lines.

By Gender

Female consumers command a 62.4% share in 2025, reflecting the historically female-skewed skin care consumption base across mass and premium tiers. Brands such as L'Oréal Paris, Estée Lauder, Olay, Clinique, Lancôme, and Shiseido are predominantly female-targeted, supported by extensive female-focused advertising, retail merchandising, and digital engagement.

Male grooming at 21.3% is the fastest-growing gender segment at approximately 4.2% CAGR, supported by L'Oréal Men Expert, Nivea Men, Bulldog, Lumin, and direct-to-consumer male skin care brands. Unisex at 16.3% reflects Gen Z's gender-fluid approach to beauty, with brands such as Aesop, Le Labo, and Kiehl's positioned across genders.

Regional Market Insights

Asia Pacific's market leadership (39.8%, 2025) reflects China’s increased cosmetics exports by 11.7% year-on-year during the first eight months of 2025, Japan's premium skin care tradition, and South Korea's role as a global K-beauty innovation hub. India, Indonesia, Vietnam, and Thailand are the fastest-growing within Asia Pacific, contributing to the region's overall 4.5% CAGR.

Europe at 24.6% maintains its position as a premium and prestige consumer market, anchored by L'Oréal Paris, Lancôme, Vichy, and La Roche-Posay. EU Cosmetics Regulation reinforces European leadership in clean beauty and dermatological skin care. North America at 20.3% commands strong premium consumption, with Sephora and Ulta Beauty driving the prestige retail channel.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

39.8% |

Dominant China, Japan, South Korea consumption base; K-beauty global influence; rapidly expanding India, Southeast Asia premium segment; rising middle-class skin care adoption |

|

Europe |

24.6% |

Mature premium and prestige consumer base; French luxury heritage; strong dermatological pharmacy channel; clean beauty regulatory leadership |

|

North America |

20.3% |

Strong premium and prestige consumer base; emerging D2C and clean beauty disruptor brands; expanding male grooming segment |

|

Latin America |

8.2% |

Brazilian direct-selling tradition; growing premium consumer base in Mexico and Argentina; rising e-commerce penetration |

|

Middle East & Africa |

7.1% |

GCC premium consumption growth; expanding urban affluent middle class; rising sun-care and anti-aging demand in climate-affected markets |

Competitive Landscape

The global skin care products market exhibits moderate concentration, with the top five players (L’OREAL S.A., The Estée Lauder Companies, Unilever, Procter & Gamble, and Shiseido Company, Limited) collectively holding approximately 40–45% of global market revenue in 2025.

|

Company Name |

Brand Name / Portfolio |

Market Position |

Core Strength |

|

L’OREAL S.A. |

L'Oréal Paris, Lancôme, Kiehl's, La Roche-Posay, Vichy, Garnier, CeraVe, Helena Rubinstein, SkinCeuticals, Aesop |

Market Leader |

World's largest beauty company; full mass-to-prestige portfolio; R&D and innovation leadership |

|

The Estée Lauder Companies |

Estée Lauder, Clinique, La Mer, Origins |

Market Leader |

Prestige skin care leader; multi-brand premium portfolio; strong department store and travel retail |

|

Unilever |

Dove, Vaseline, Dermalogica, Dove Men+Care, Paula's Choice, POND’S SKIN INSTITUTE |

Market Leader |

Mass-market and prestige skin care; global distribution scale; sustainability and clean beauty pivot |

|

Procter & Gamble |

Olay, SK-II |

Market Leader |

Mass-market Olay dominance; consumer science depth |

|

Shiseido Company, Limited |

Shiseido, Clé de Peau Beauté |

Strong Challenger |

Japanese skin care heritage; prestige and luxury positioning; Asia Pacific stronghold |

L’OREAL S.A. leads through its multi-tier brand portfolio spanning mass-market (L'Oréal Paris, Garnier) to prestige (Lancôme, Kiehl's, La Roche-Posay), while The Estée Lauder Companies, Shiseido Company, Limited, and Unilever compete through differentiated portfolios.

Key Company Profiles

L'ORÉAL S.A.

L'ORÉAL S.A. is the world's largest beauty and personal care company, with a multi-tier brand portfolio spanning mass-market, dermatological, professional, and luxury skin care across more than 150 countries.

- Brand Portfolio: L'Oréal Paris, Lancôme, Kiehl's, La Roche-Posay, Vichy, Garnier, CeraVe[PS5.1], Helena Rubinstein, SkinCeuticals, and Aesop.

- Recent Developments: In April 2026, L'Oréal partnered with Institut Pasteur to advance skin health science through joint research on skin biomarkers, microbiome, and immunity. The collaboration aims to accelerate the discovery of new biological targets and develop next-generation active ingredients for advanced skin care solutions.

- Strategic Focus: Multi-tier brand portfolio leadership; AI and personalization; green sciences and clean beauty pivot; emerging-market expansion.

The Estée Lauder Companies

The Estée Lauder Companies is a global prestige beauty leader with a multi-brand portfolio focused on premium and luxury skin care. The company operates through department stores, specialty retailers, and travel retail.

- Brand Portfolio: Estée Lauder, Clinique, La Mer, The Ordinary, and Origins.

- Recent Developments: In April 2026, The Estée Lauder Companies announced a minority investment in luxury clinical skin care brand 111SKIN to strengthen its science-driven skin care portfolio. The partnership aims to expand 111SKIN’s global presence while leveraging its NAC Y2 technology and treatment-inspired skin care expertise.

- Strategic Focus: Prestige skin care leadership; luxury positioning through La Mer and Clinique; Asia Pacific expansion; digital and D2C investment.

Unilever

Unilever is a leading global FMCG company with substantial skin care presence across mass-market and prestige tiers through its Beauty & Wellbeing division.

- Brand Portfolio: Dove, Vaseline, Dermalogica, Dove Men+Care, Paula's Choice, and POND’S SKIN INSTITUTE.

- Recent Developments: In April 2025, Unilever, via its Indian subsidiary, Hindustan Unilever Limited (HUL), acquired a 90.5% stake in premium beauty brand Minimalist (owned by Uprising Science Private Limited) to strengthen its beauty & wellbeing, including skin care portfolio.

- Strategic Focus: Mass-market scale leadership; premiumization through prestige acquisitions; sustainability; emerging-market growth.

Market Concentration Analysis

The global skin care products market exhibits moderate concentration, with the top five players holding approximately 40–45% of revenue in 2025. The next tier includes other emerging players, collectively accounting for an additional 18–22% of share. The remaining market is fragmented across regional players, indie clean beauty brands, K-beauty disruptors, and private-label products.

Consolidation patterns are concentrated around prestige brand acquisitions, D2C disruptor acquisitions, and clean-beauty pivots. Established players invest in AI personalization, sustainable packaging, and ingredient innovation to differentiate offerings, while emerging D2C and indie brands disrupt premium and clean segments. K-beauty contract manufacturers enable rapid product innovation across the industry.

Investment & Growth Opportunities

Fastest Growing Segments

Natural ingredients (~5.8% CAGR), Asia Pacific consumption (~4.5% CAGR), male grooming (~4.2% CAGR), and premium/prestige skin care (~5% CAGR) represent the highest-growth investment vectors through 2034. Together, these subcategories address a combined incremental addressable opportunity of approximately USD 35 Billion by 2034.

Emerging Market Expansion

India, Indonesia, Vietnam, Thailand, and the GCC represent the highest-growth emerging skin care markets. Per-capita consumption gaps versus mature markets indicate substantial structural growth potential as urban affluent consumers adopt premium skin care routines and Western and K-beauty trends propagate.

Premium and Innovation Investment

- Clean beauty and natural ingredient innovation, with bio-fermented hyaluronic acid, plant-cell-cultured actives, and biosynthetic squalane representing the highest-growth ingredient categories.

- AI-powered personalization and DNA-based skin care are emerging premium segments commanding price premiums and supporting brand differentiation.

- Direct-to-consumer brands such as The Ordinary, Glow Recipe, and emerging clean-beauty disruptors demonstrate the viability of digital-first premium positioning.

Future Market Outlook (2026-2034)

The global skin care products market is positioned for steady expansion through 2034. From USD 172.7 Billion in 2025, the market is projected to reach USD 241.1 Billion by 2034, representing incremental value creation of USD 68.4 Billion at a CAGR of 3.66%. This trajectory is underpinned by sustained Asia Pacific consumption, mature-market premiumization, clean-beauty mainstreaming, and rising male and unisex segment adoption.

Three structural shifts will define 2026–2034: the accelerating mainstreaming of clean beauty and natural ingredients across mass-market and prestige tiers; rapid scale-up of AI-powered personalization and D2C channels; and the consolidation of prestige brand portfolios through M&A by L'Oréal, Estée Lauder, Unilever, and P&G targeting emerging premium and clean disruptors.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 110 industry participants in 2024–2025, including skin care brand executives, ingredient suppliers, contract manufacturers, retail buyers (Sephora, Ulta, Boots), dermatologists, and beauty consumers across China, Japan, South Korea, France, the US, India, and the UK. Expert input validated market sizing, segment shares, and regional consumption patterns.

Secondary Research

Secondary research encompassed L’OREAL S.A., The Estée Lauder Companies, Unilever, Procter & Gamble, and Shiseido Company, Limited annual reports; Euromonitor and NielsenIQ retail audit data; EU CosIng database; US FDA cosmetics regulatory documents; and industry publications (WWD Beauty Inc., Cosmetics Business, Beauty Packaging).

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting, incorporating global skin care consumption data, regional and demographic trends, segment-level price evolution, and channel-mix transitions. A base-case CAGR of 3.66% reflects consensus estimates validated against company revenue disclosures, retail audit data, and historical consumption growth patterns from FY2020 to FY2025.

Skin Care Products Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered |

|

| Ingredients Covered | Chemical, Natural |

| Genders Covered | Male, Female, Unisex |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Beauty Parlours and Salons, Multi Branded Retail Stores, Online, Exclusive Retail Stores, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | L’OREAL S.A., The Estée Lauder Companies, Unilever, Procter & Gamble, Shiseido Company, Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the skin care products market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global skin care products market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the skin care products industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Skin Care Products Market Report

The global skin care products market reached USD 172.7 Billion in 2025 and is projected to reach USD 241.1 Billion by 2034.

The market is expected to grow at a CAGR of 3.66% during 2026-2034, driven by health and wellness consciousness, premiumization, e-commerce expansion, male grooming growth, and clean-beauty trends.

Asia Pacific leads with a 39.8% share in 2025, anchored by China, Japan, and South Korea consumption and rapidly expanding India and Southeast Asia demand.

Chemical-based ingredients dominate with a 63.5% share in 2025, driven by clinically proven actives including retinoids, peptides, niacinamide, and hyaluronic acid synthetics.

Female consumers hold the largest share at 62.4%, reflecting the historically female-skewed skin care consumption base.

Key players include L’OREAL S.A., The Estée Lauder Companies, Unilever, Procter & Gamble, and Shiseido Company, Limited.

Natural ingredients are growing at approximately 5.8% CAGR driven by clean-beauty trends, consumer demand for plant-based actives, regulatory pressure on synthetics, and rising preference for botanical, vegan, and bio-derived formulations.

Key challenges include regulatory complexity across EU, US FDA, and China NMPA jurisdictions, counterfeit and greywashing concerns, raw material price volatility, market saturation in developed regions, and sustainability and packaging pressures.

Natural and clean-beauty ingredients, AI-powered personalization, male grooming, India and Southeast Asia expansion, D2C premium brands, and sustainable refillable packaging represent the highest-growth investment opportunities.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)