Smart Card Market Size, Share, Trends and Forecast by Type, Component, Application, End User, and Region, 2026-2034

Global Smart Card Market Size, Share, Trends & Forecast (2026-2034)

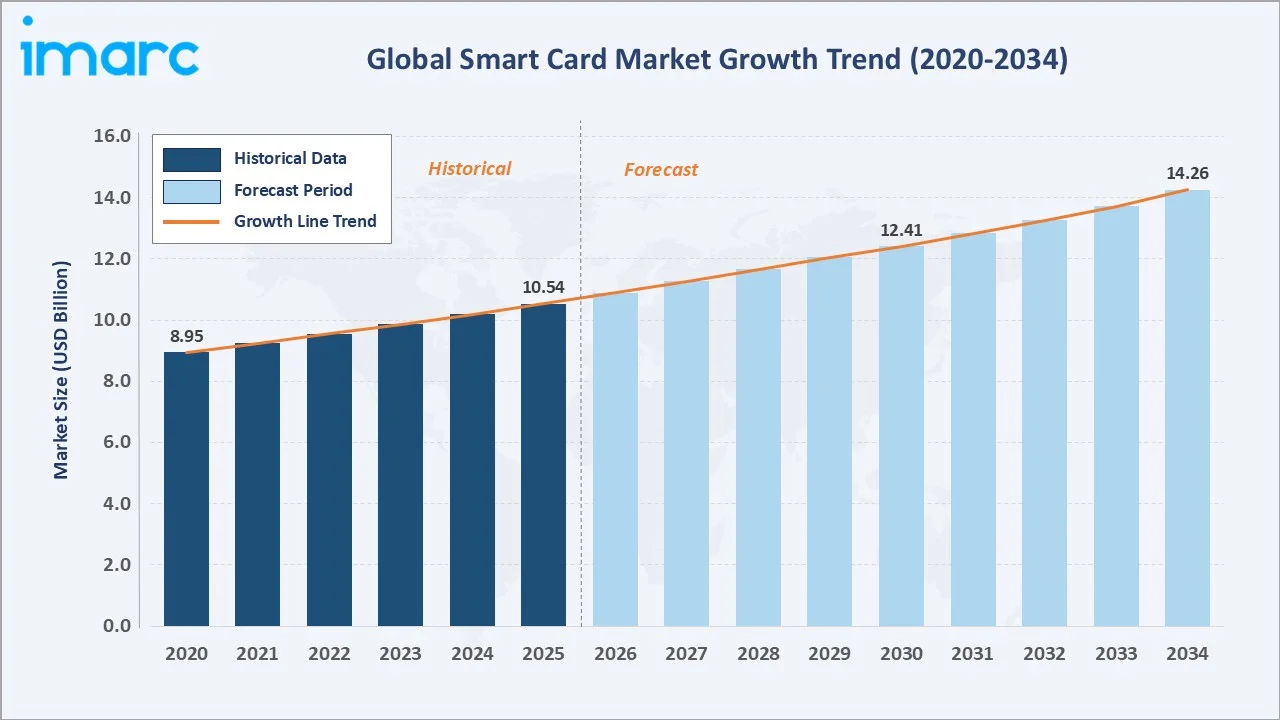

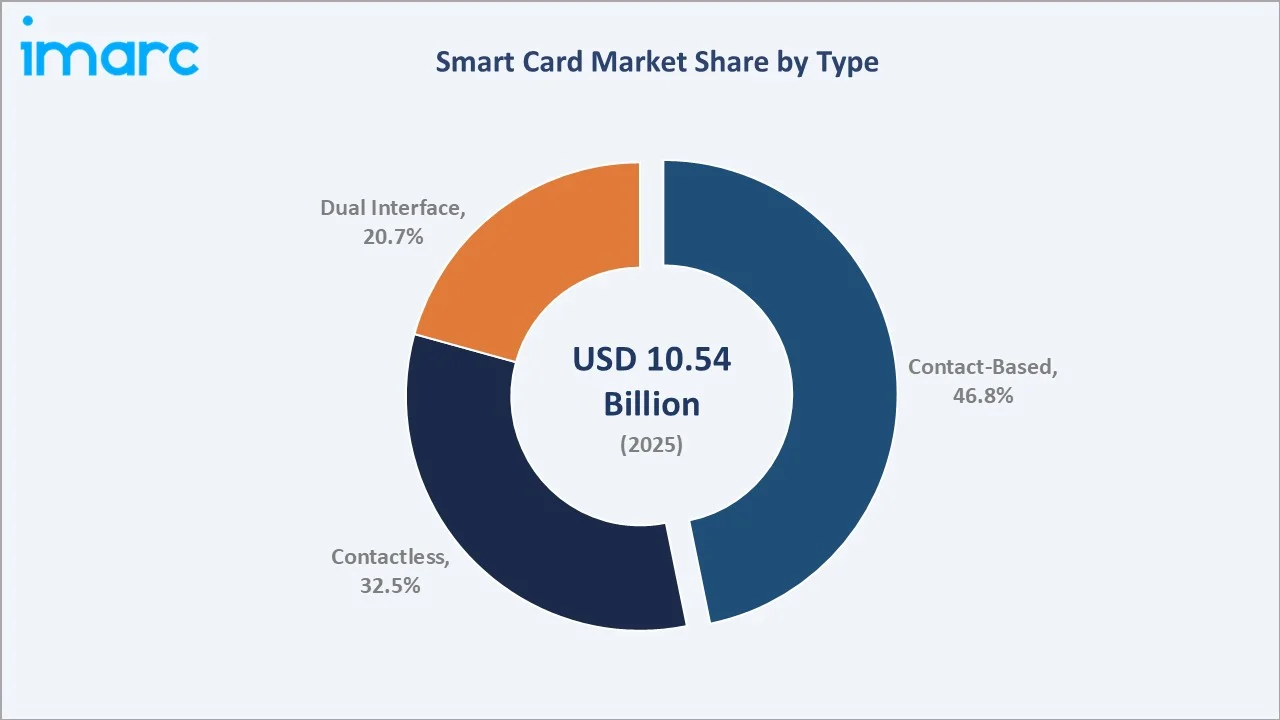

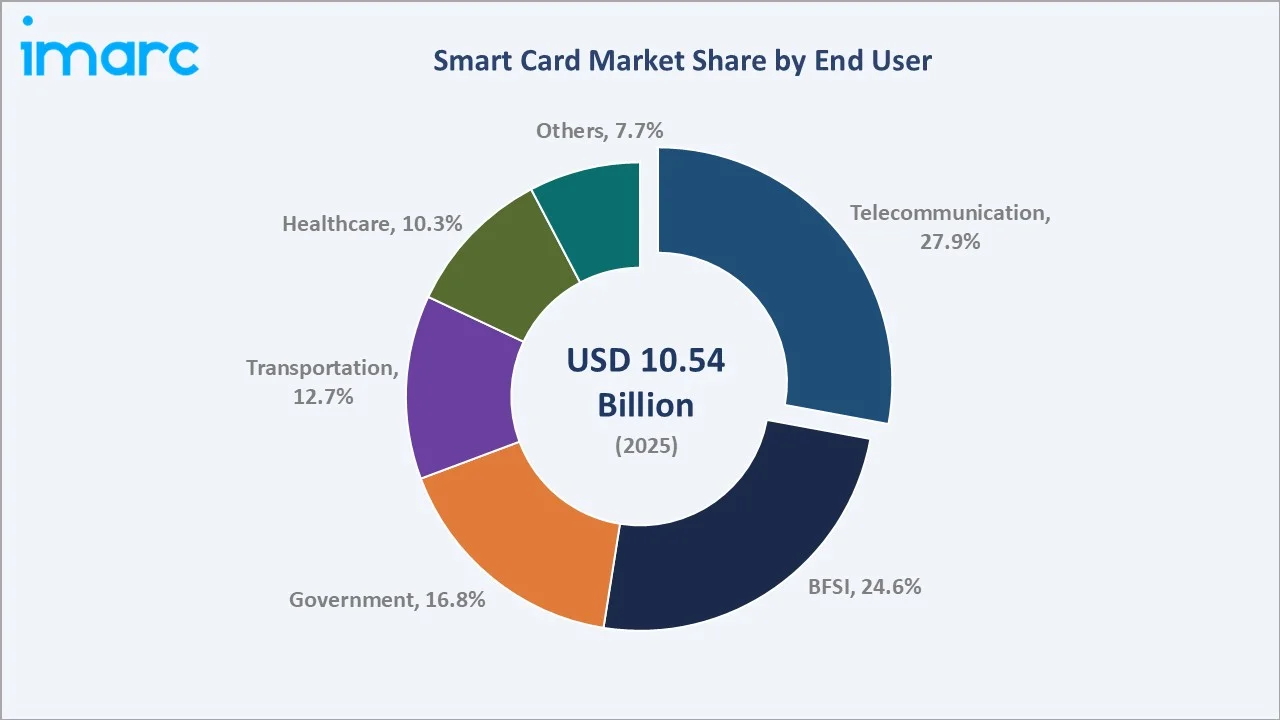

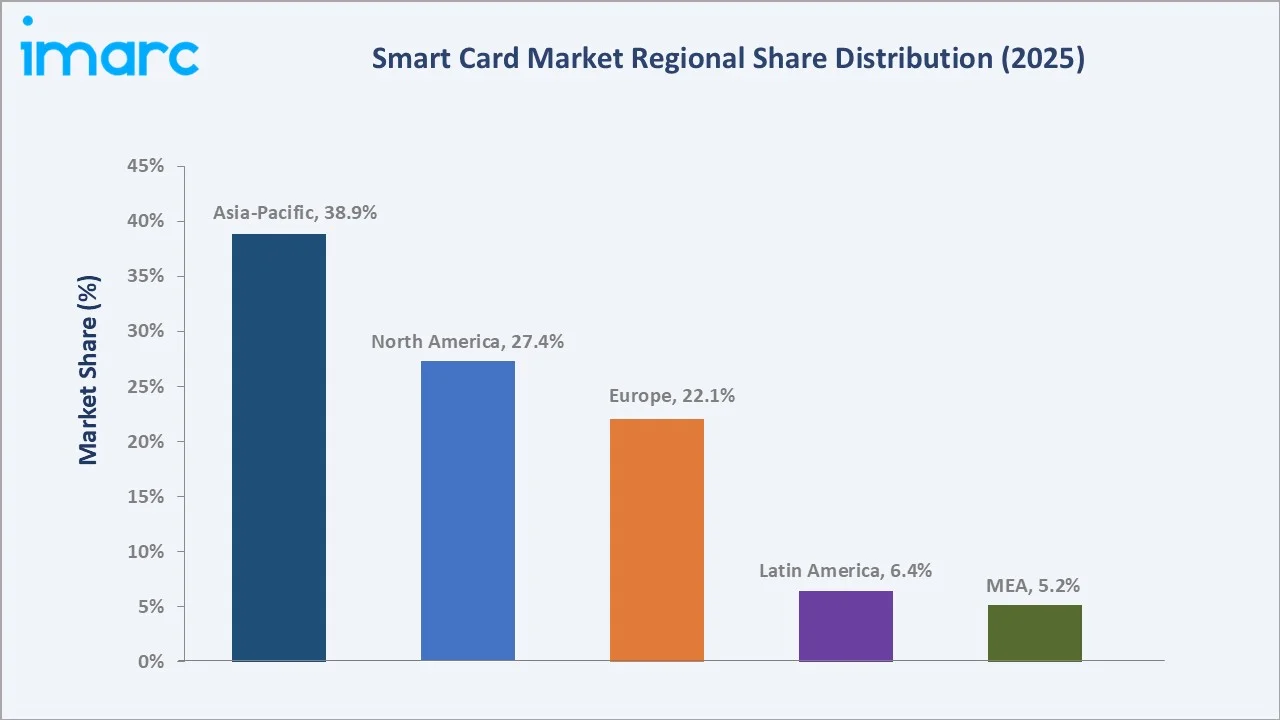

The global smart card market size was valued at USD 10.54 Billion in 2025 and is projected to reach USD 14.26 Billion by 2034, exhibiting a CAGR of 3.32% during the forecast period 2026-2034. Rising adoption of digital payment infrastructure, expanding government e-ID programs, and the proliferation of NFC-enabled contactless transactions are primary growth catalysts. Contact-Based cards lead with a 46.8% share in 2025, while Telecommunication dominates the end-user segment at 27.9%. Asia-Pacific commands 38.9% of global revenue, consolidating its position as the world's largest regional market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2020) |

USD 8.95 Billion |

|

Market Size (2025) |

USD 10.54 Billion |

|

Forecast Market Size (2030) |

USD 12.41 Billion |

|

Forecast Market Size (2034) |

USD 14.26 Billion |

|

CAGR (2026-2034) |

3.32% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia-Pacific (38.9% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific |

|

Leading Type |

Contact-Based (46.8%, 2025) |

|

Leading End User |

Telecommunication (27.9%, 2025) |

The chart highlights global smart card market growth from 2020–2034, showing historical expansion and future gains driven by contactless payments, digital identity adoption, and 5G SIM growth.

To get more information on this market, Request Sample

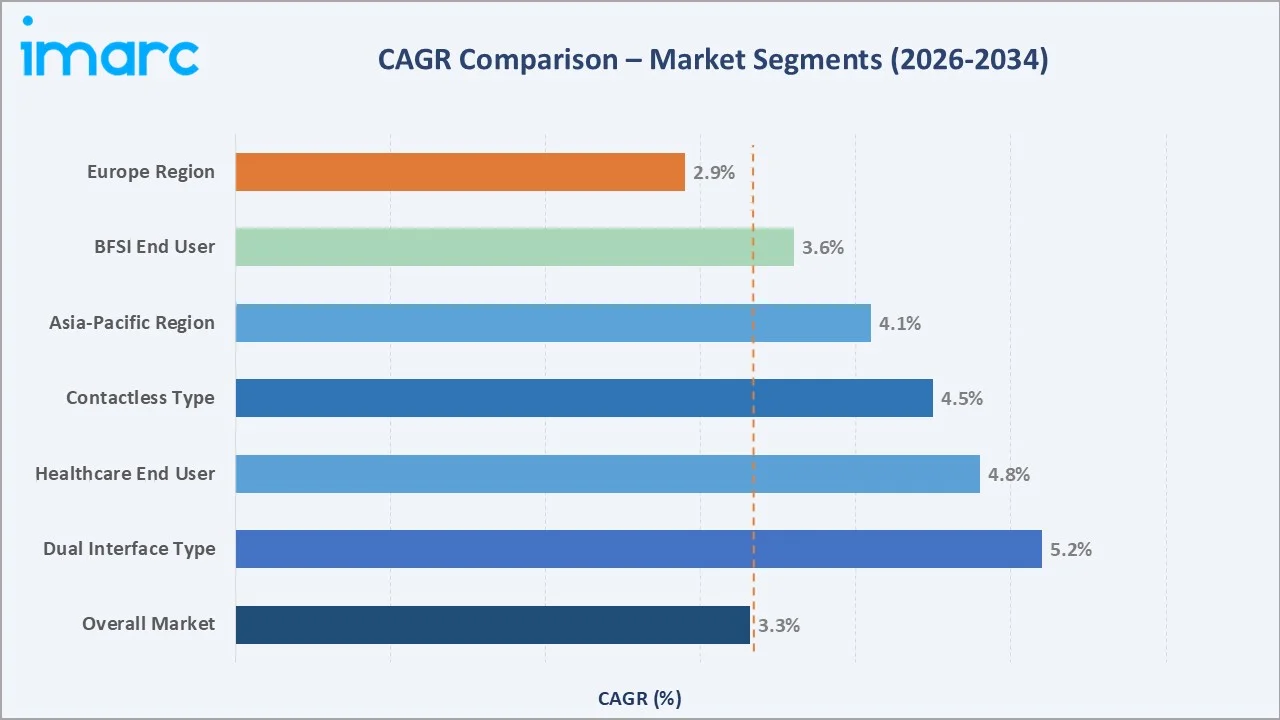

CAGR comparison shows Dual Interface cards and Healthcare as the fastest-growing segments in the global smart card market through 2034.

Executive Summary

The global smart card market is undergoing a measured but resilient expansion, propelled by the twin forces of digital financial inclusion and government-led identity modernization. Valued at USD 10.54 Billion in 2025, the market is forecast to reach USD 14.26 Billion by 2034 at a CAGR of 3.32%. According to the World Bank, over 1.4 billion adults remained unbanked in 2024, and national programs in South Asia, Africa, and Southeast Asia are deploying smart-card-based national ID and payment systems as foundational financial inclusion tools, creating a structural long-term demand pipeline.

Contact-Based cards retain a 46.8% majority in 2025, underpinned by EMV chip-and-PIN banking card standards mandated by payment networks in over 80 countries. Contactless cards at 32.5% in 2025 represent the fastest-growing type segment – Mastercard reported that over 75% of its global in-person transactions were contactless in 2025. Dual Interface cards at 20.7% are gaining traction as banks issue single cards combining EMV contact and NFC contactless functionality to future-proof their card portfolios.

Telecommunication leads end-user demand at 27.9% in 2025, driven by global SIM card deployment where 5G rollout is creating an upgrade cycle from 4G SIM to 5G-compatible UICC. BFSI at 24.6% remains the second-largest end user, driven by EMV migration completion in developing markets and the shift toward premium metal card issuance in North America and Europe. Asia-Pacific dominates geographically at 38.9%, driven by China's Union Pay network, India's Aadhaar biometric ID card program, and South Korea's advanced transit card infrastructure.

Key Market Insights

|

Insight |

Data |

|

Largest Type Segment |

Contact-Based – 46.8% share (2025) |

|

Fastest Growing Type |

Dual Interface – ~5.2% CAGR (2026-2034) |

|

Leading End User |

Telecommunication – 27.9% share (2025) |

|

Fastest Growing End User |

Healthcare – ~4.8% CAGR (2026-2034) |

|

Leading Region |

Asia-Pacific – 38.9% revenue share (2025) |

|

Top Companies |

Thales Group, IDEMIA, G+D, HID Global, Sony |

|

Market Opportunity |

Healthcare smart cards for patient ID & EHR access |

Key Analytical Observations Supporting The Above Data:

- Contact-Based cards' 46.8% dominance in 2025 reflects EMV chip adoption, driven by Visa, Mastercard, and American Express liability-shift programs, has expanded to more than 80 countries globally.

- Contactless card adoption is accelerating rapidly – EMVCo reports that over 96% of global card-present transactions now use EMV technology, with contactless payments continuing to grow rapidly worldwide.

- Dual Interface cards accounted for 20.7% share in 2025 and are gaining strong traction as issuers increasingly adopt single-card solutions supporting both contact and contactless transactions.

- Telecommunication's 27.9% end-user dominance is directly tied to global 5G rollout – GSMA Intelligence projects 5.6 billion 5G connections worldwide by 2030, each requiring a compatible UICC or eSIM card.

- Healthcare smart cards are growing rapidly, driven by national EHR programs in Germany, France, and South Korea mandating health card issuance.

- Asia-Pacific's 38.9% market share reflects India's Aadhaar program linking 1.3 billion citizens to biometric smart ID infrastructure, alongside China's 2nd-generation Resident Identity Card (RIC) rollout.

Global Smart Card Market Overview

Smart cards are pocket-sized cards embedded with microprocessor or memory chips that securely store and process data for authentication, identification, payments, and data exchange. The ecosystem includes semiconductor suppliers, card manufacturers, personalization providers, software vendors, terminal manufacturers, and end-user industries such as banking, telecom, government, healthcare, and transportation.

Smart cards are widely used in payments, SIM cards, national IDs, e-passports, transit, healthcare, and access control. Market growth is driven by digital payments, government digitization, and 5G expansion, with global card networks processing 687.19 billion transactions in 2023.

Market Dynamics

To evaluate market opportunities, Request Sample

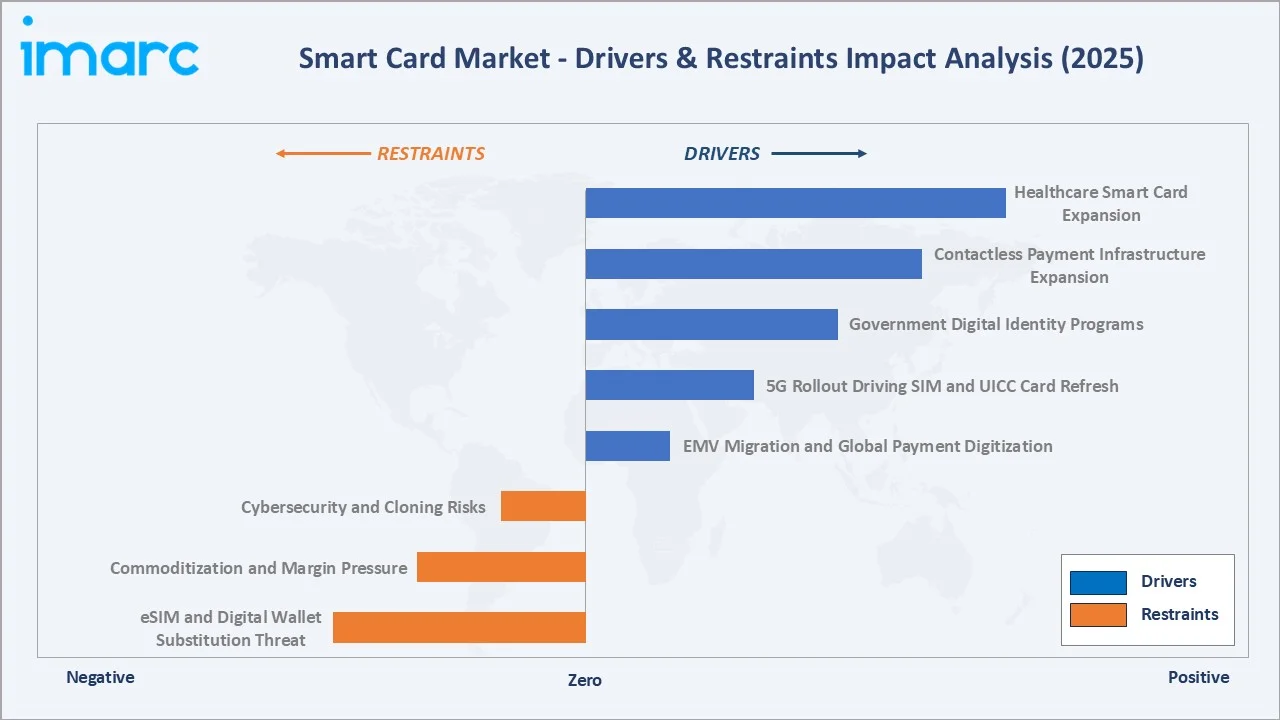

Market Drivers

- EMV Migration and Global Payment Digitization: EMVCo reports that EMV chip transactions reached 96% of global card-present transactions in 2023, anchoring contact-based card demand in financial services globally.

- 5G Rollout Driving SIM and UICC Card Refresh: GSMA Intelligence projects 5.6 billion 5G connections by 2030. Each 5G subscriber requires a 5G-compatible UICC or eSIM, creating a sustained replacement cycle for telecommunication smart cards.

- Government Digital Identity Programs: The EU Digital Identity Wallet initiative targeting 80% of EU citizens by 2030 and India's Aadhaar biometric ID program linked to 1.3 billion residents are generating large-scale government smart card procurement programs.

- Contactless Payment Infrastructure Expansion: Mastercard reported over 75% of in-person transactions were contactless in 2025. NFC terminal penetration is driving demand for contactless and dual-interface card issuance by banks globally.

Market Restraints

- eSIM and Digital Wallet Substitution Threat: Apple Pay, Google Wallet, and eSIM adoption are reducing physical card and SIM issuance in premium smartphones, particularly in North America and Europe, as device-based payments continue gaining share in contactless transactions.

- Commoditization and Margin Pressure: Contact-based and standard SIM cards face strong price competition, particularly from Asian manufacturers, pressuring margins in high-volume, standardized smart card segments.

- Cybersecurity and Cloning Risks: Advanced SIM-swapping attacks and contactless skimming techniques pose persistent threats to consumer trust in smart card security, requiring continuous security protocol upgrades that add to manufacturer R&D costs.

Market Opportunities

- Healthcare Smart Card Expansion: Germany’s eGK, France’s Carte Vitale, and South Korea’s health cards, alongside emerging Middle East and Southeast Asia deployments, represent significant underpenetrated opportunities driven by national digital healthcare initiatives.

- Biometric Smart Card Integration: Biometric payment cards with fingerprint authentication are entering commercial deployment following Visa and Mastercard certifications, but adoption remains limited, creating significant future scaling opportunities.

- Transit and Multi-Application Cards: Urban transit smart card programs, including India’s National Common Mobility Card, are expanding across emerging markets, enabling multi-application cards integrating transit, payments, and public service access.

Market Challenges

- Semiconductor Supply Chain Concentration: Smart card IC supply is concentrated among NXP, Infineon, and STMicroelectronics, creating procurement risks for card manufacturers due to geopolitical tensions and dependence on a limited supplier base.

- Regulatory Compliance Complexity: GDPR, India’s Digital Personal Data Protection Act (2023), and China’s PIPL create fragmented compliance requirements, complicating cross-border data management for global smart card operators handling cardholder information.

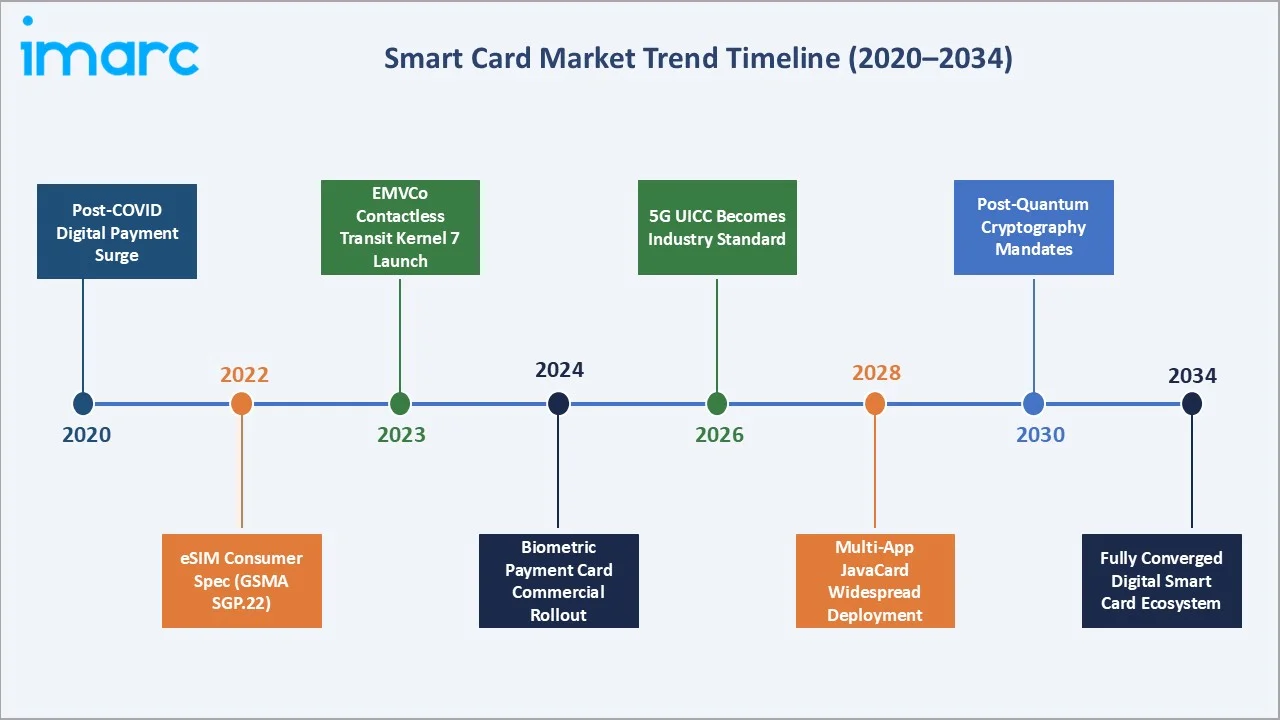

Emerging Market Trends

1. Biometric Authentication Integration in Payment Cards

Fingerprint-enabled payment cards are moving from pilots to early commercial deployment, with banks like BNP Paribas issuing biometric cards. Limited adoption and premium positioning create a new high-value segment within the smart card market.

2. eSIM and iSIM Convergence with Traditional Smart Cards

eSIM adoption is accelerating, with over 500 million units shipped in 2024. This shift is pushing telecom operators from physical SIM volumes toward higher-value eSIM provisioning and platform-based services.

3. Government e-ID and e-Passport Modernization

ICAO-compliant e-passports are deployed in over 140 countries, while the EU Digital Identity Wallet targeting 80% adoption by 2030 is driving demand for multi-application national eID platforms.

4. Contactless EMV and Open-Loop Transit Integration

Open-loop transit systems are expanding globally. London processes over 3 million contactless journeys daily, while New York, Singapore, and Sydney are adopting similar models, increasing demand for dual-interface payment cards.

5. Multi-Application JavaCard Platform Adoption

JavaCard-based multi-application smart cards are gaining traction in Asia-Pacific government programs. Malaysia’s MyKad combines national ID, driving license, health data, and e-wallet functions, serving as a leading multi-application smart card deployment.

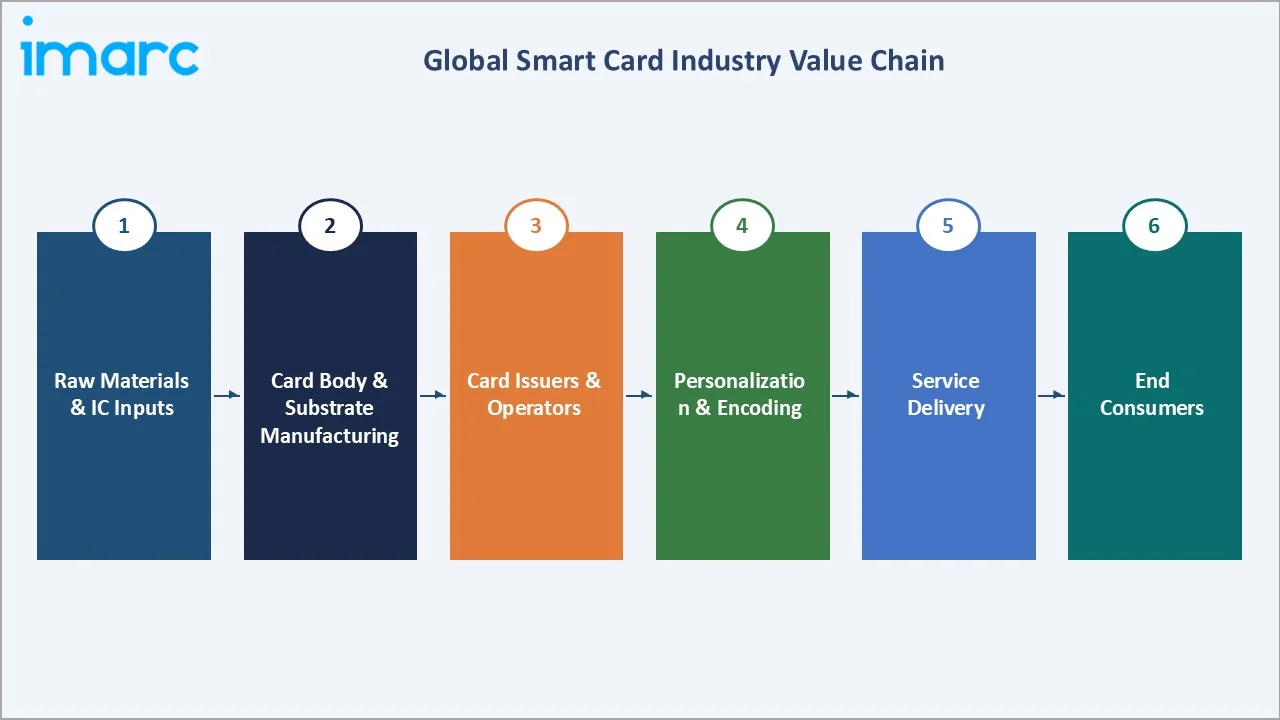

Industry Value Chain Analysis

The smart card value chain spans semiconductor fabrication, chip design, card manufacturing, personalization, issuance, and lifecycle management, with each stage characterized by distinct competitive dynamics, margins, and technology investment requirements.

|

Stage |

Key Players / Examples |

|

Semiconductor & IC Supply |

NXP Semiconductors, Infineon Technologies, STMicroelectronics, Samsung Semiconductors |

|

Card Body & Substrate Manufacturing |

Giesecke+Devrient (G+D), Thales Group, IDEMIA, Eastcompeace |

|

Chip Embedding & Lamination |

Mühlbauer Group, Atlantic Zeiser |

|

Personalization & Encoding |

Entrust, IDEMIA, HID Global, CardLogix Corporation |

|

Distribution & System Integration |

Banking card networks (Visa/Mastercard), MNO distribution channels, system integrators |

|

End Consumers |

Bank cardholders, mobile subscribers, government ID holders, transit commuters, healthcare patients |

IC suppliers such as NXP, Infineon, and STMicroelectronics hold higher margins due to patented secure-element chips and certified security standards, while card manufacturers face pricing pressure but retain value through personalization and compliance capabilities.

Technology Landscape in the Smart Card Industry

Secure Element and Chip Architecture

Secure elements are tamper-resistant chips enabling smart card security, typically certified at EAL5+ or higher. NXP SmartMX/MIFARE and Infineon SLE platforms dominate global EMV, government ID, and transit smart card chip deployments.

Near Field Communication (NFC) and Contactless Technology

ISO/IEC 14443 enables 13.56 MHz contactless smart card communication with data rates up to 848 Kbps, supporting fast transit transactions, while EMV contactless kernel standards enable global open-loop transit deployments.

eSIM and Remote SIM Provisioning (RSP)

GSMA SGP.22 and SGP.32 enable remote SIM provisioning via SM-DP+ infrastructure, allowing over-the-air profile activation. This shift from physical SIMs is creating a growing platform services ecosystem.

Biometric Integration

Fingerprint payment cards embed sensors and store biometric templates securely on-card using match-on-card processing. Based on ISO/IEC 19794-2 standards, Visa and Mastercard programs are enabling commercial biometric card deployments.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Contact-Based |

46.8% |

2025 |

|

Component |

🔒 |

🔒 |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

End User |

Telecommunication |

27.9% |

2025 |

|

Region |

Asia-Pacific |

38.9% |

2025 |

By Type

Contact-based smart cards account for a significant share in 2025, supported by EMV chip-and-PIN security and strong adoption in banking and government ID applications where physical contact enhances protection against remote interception

To access detailed market analysis, Request Sample

Contactless cards held 32.5% share in 2025, driven by expanding NFC payment infrastructure. Dual-interface cards accounted for 20.7%, gaining adoption as issuers standardize single-card solutions to support both contact and contactless payments while reducing operational complexity.

By End User

Telecommunication led smart card demand with 27.9% share in 2025, driven by SIM deployments and 5G upgrades. BFSI accounted for 24.6%, supported by sustained EMV card issuance and growing premium banking card adoption across developing markets. Both segments continue to drive large-scale smart card deployment globally.

Government accounted for 16.8% share in 2025, driven by national ID, e-passport, and digital identity programs. Transportation held 12.7% through transit and vehicle smart cards, while Healthcare represented 10.3%, supported by expanding digital health and insurance card initiatives across global markets.

Regional Market Insights

|

Region |

Share (2025) |

Key Drivers |

Major Companies |

|

Asia-Pacific |

38.9% |

China Union Pay, India Aadhaar, 5G SIM rollout, transit smart card programs |

Eastcompeace, CPI Card Group, local SIM suppliers |

|

North America |

27.4% |

EMV migration completion, premium metal card growth, contactless transit |

HID Global, Entrust, CPI Card Group, Identiv |

|

Europe |

22.1% |

EU Digital Identity Wallet, GDPR-compliant ID programs, e-health card mandates |

Thales Group, G+D, IDEMIA, Infineon |

|

Latin America |

6.4% |

Bancarization drives (Brazil, Mexico), government ID programs |

Valid S.A., Thales, local distributors |

|

Middle East & Africa |

5.2% |

GCC national ID programs, SIM-based mobile money (M-Pesa ecosystem) |

G+D, IDEMIA, regional integrators |

Asia-Pacific's 38.9% dominance in 2025 reflects a convergence of three structural demand factors: China's Union Pay network with over 9.4 billion cards in circulation (2024), India's PMJDY financial inclusion scheme driving new bank account and debit card issuance to over 530 million beneficiaries, and South Korea’s T-money and Cashbee systems process tens of millions of NFC transit transactions daily, highlighting one of the world’s most advanced contactless transit infrastructures.

North America held 27.4% share in 2025, supported by mature EMV adoption and premium card demand. The region is shifting toward high-value segments such as metal and biometric cards. U.S. EMV adoption exceeded 93% of card-present transactions by 2024, reflecting widespread chip deployment and sustained growth in premium offerings.

Europe held 22.1% share in 2025, driven by GDPR compliance, EU Digital Identity initiatives, and established national eID programs. Germany’s eGK rollout covering 73 million statutory insurance members by 2022 represents one of the largest health smart card deployments, supporting continued demand for secure, multi-application identity and healthcare smart cards across Europe.

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

Thales Group |

SafeNet IDPrime / IDCore |

Leader |

SIM/UICC, banking cards, e-passport, multi-vertical global platform |

|

IDEMIA |

ID-One™ / IDEMIA Augmented Identity |

Leader |

Biometric smart cards, government ID, eSIM management platform |

|

Giesecke+Devrient GmbH |

G+D Mobile Security / G+D ePayments |

Leader |

SIM cards, eSIM, payment cards, security technology |

|

HID Global Corporation |

Seos® / Crescendo® |

Leader |

Physical access control, government ID, enterprise credentialing |

|

Sony Corporation |

FeliCa |

Challenger |

Transit smart cards (FeliCa NFC standard), Asia-Pacific leadership |

|

Avio Smart Market Stack Ltd. |

AVIO Smart Cards |

Challenger |

RFID and smart card solutions, emerging market penetration |

|

CardLogix Corporation |

M.O.S.T. Card® / Toolz™ |

Emerging |

Specialty smart cards, high-security government applications |

|

dzcard (Toppan Security subsidiary) |

dzcard / dzign |

Emerging |

Loyalty, prepaid, and financial smart cards for regional markets |

The global smart card market features a concentrated group of multinational leaders with strong security capabilities, alongside regional specialists and emerging players competing across banking, telecom, and government applications.

Key Company Profiles

Thales Group

Thales Group, headquartered in Paris, France, is a global leader in aerospace, defense, and digital identity solutions. Following its 2019 acquisition of Gemalto, the company expanded its smart card portfolio across SIM cards, EMV payment cards, e-passports, and digital identity solutions, operating through its Digital Identity & Security division for governments, banks, and telecom operators worldwide.

- Product Portfolio: Thales SIM/UICC and eSIM platforms, EMV payment cards, biometric passport chips, government identity solutions, SafeNet identity and data protection.

- Recent Developments: In 2025, Thales introduced MultiApp 5.2 Premium PQC, a post-quantum cryptography-enabled smart identity card certified by France’s cybersecurity agency. In January 2026, Thales partnered with Ubiqu to develop secure storage infrastructure for EU Digital Identity Wallets.

- Strategic Focus: Thales focuses on integrating physical smart cards with digital identity solutions, using secure hardware to support digital wallets and eSIM platforms, while investing in post-quantum cryptography for next-generation identity documents.

IDEMIA

IDEMIA, headquartered in Courbevoie, France, is a global provider of augmented identity and secure smart card technologies for government, banking, and telecom industries. The company was formed in 2017 through the merger of Oberthur Technologies and Safran Identity & Security (Morpho).

- Product Portfolio: Financial EMV cards, biometric payment cards, eSIM management (M2M and consumer), government eID documents, e-passports, biometric access control, and MorphoWave™ contactless fingerprint.

- Recent Developments: In July 2025, IDEMIA launched its ID-One PIV® 243 smart cards, which were added to the U.S. General Services Administration (GSA) Approved Products List after achieving NIST FIPS 140-3 Level 2 certification. In January 2025, IDEMIA introduced smartphone enrollment capability for its F.CODE biometric payment cards, enabling users to register fingerprints using mobile devices.

- Strategic Focus: IDEMIA focuses on integrating physical smart cards with digital identity platforms. Its eSIM solutions support 200+ mobile operators, while biometric capabilities across payments, government ID, and access control drive differentiation.

Giesecke+Devrient GmbH (G+D)

Giesecke+Devrient (G+D), headquartered in Munich, Germany, is a global security technology provider specializing in smart cards, SIM/eSIM, payment solutions, and secure identity systems. The company operates through Mobile Security, Banking & Payment, and Currency Technology divisions.

- Product Portfolio: SIM/UICC cards, eSIM (M2M and consumer), EMV payment cards, metal payment cards, e-passport chips, G+D Convego payment platform.

- Recent Developments: In FY 2025, G+D reported record order intake of €3.6 billion, driven largely by digital security, payment cards, and SIM/eSIM technologies. In April 2025, G+D became the first company to achieve GSMA eUICC security certification for IoT eSIM products.

- Strategic Focus: G+D focuses on integrating SIM and eSIM services, expanding SM-DP+ subscription management revenue, and advancing digital cash and CBDC pilot programs within its currency technology division.

HID Global Corporation

HID Global, headquartered in Austin, Texas, USA, is a subsidiary of ASSA ABLOY and a leading provider of secure identity, smart card credentials, and access control solutions. The company serves enterprises, governments, and financial institutions globally.

- Product Portfolio: HID Crescendo smart card access credentials, SEOS mobile access, HID Fargo card printers and personalization systems, OMNIKEY readers, government PIV/CAC credentials, iCLASS RFID cards.

- Recent Developments: In March 2026, HID launched Converged Credentials, a unified platform combining, Physical smart cards, Mobile credentials, and Digital identity management. In October 2025, HID acquired IDmelon to enhance smart card authentication, enabling physical access cards and mobile devices to function as FIDO security keys.

- Strategic Focus: HID focuses on converging physical access and digital identity, shifting toward mobile and cloud-based credentials while maintaining leadership in enterprise and government smart card access solutions.

Market Concentration Analysis

The global smart card market shows moderate-to-high concentration at the premium tier, with Thales, IDEMIA, and G+D collectively accounting for about 40–48% of global revenue in 2025, based on digital identity segment revenues and analyst estimates.

The smart card market shows bifurcated concentration. High-security government and financial cards are dominated by top players due to certifications, R&D capabilities, and long-term contracts. In contrast, standard SIM and commodity cards are more fragmented, with Chinese firms such as Eastcompeace, Hengbao, and Watchdata competing aggressively on pricing.

Premium identity and security segments have seen major consolidation, led by Thales’ acquisition of Gemalto (2019) and IDEMIA’s formation via the OT-Safran merger (2017). Further consolidation is expected as rising digital identity platform investments exceed the capabilities of smaller, single-vertical card manufacturers.

Investment & Growth Opportunities

Fastest-Growing Segments

Healthcare smart cards are expanding, driven by Germany’s 73 million insured population under the EHR mandate, alongside France, South Korea, and Southeast Asia deployments. Dual-interface payment cards are also growing as issuers standardize contact and contactless functionality.

Emerging Market Expansion

Sub-Saharan Africa remains underpenetrated, with hundreds of millions of mobile money users led by platforms such as M-Pesa, Airtel Money, and MTN Mobile Money, while the region accounts for over 50% of global mobile money accounts, according to GSMA. Meanwhile, India’s National Common Mobility Card (NCMC) is expanding across metro and bus networks under the One Nation One Card initiative.

Venture & Private Investment Trends

Biometric payment innovators like Fingerprint Cards AB and IDEX Biometrics are attracting investment for fingerprint-on-card technology. Additionally, National Institute of Standards and Technology 2024 post-quantum cryptography standards are driving funding for PQC-resistant secure elements and upgrades to long-lifecycle government smart card programs.

Future Market Outlook (2026–2034)

The global smart card market is projected to grow from USD 10.54 billion in 2025 to USD 14.26 billion by 2034, supported by stable demand across financial services, telecom, government, healthcare, and transportation sectors. Despite moderate growth, three key technology transitions are expected to shape market expansion through 2034.

The shift to eSIM and iSIM is reducing physical SIM demand in premium markets while increasing software-based revenue through SM-DP+ platforms, with Thales, IDEMIA, and G+D investing in this transition. Meanwhile, biometric smart cards are emerging as a premium segment, with higher-priced biometric payment cards supporting overall market value growth.

By 2034, smart cards are expected to evolve from single-function cards to multi-application platforms integrating digital identity, payments, transit, and healthcare credentials. Countries with advanced national ID systems such as Estonia, Germany, Singapore, and South Korea are already demonstrating this convergence, shaping future government smart card deployments globally.

Research Methodology

Primary Research

Primary research encompassed over 45 structured interviews conducted in 2024–2025 with smart card industry stakeholders including product directors at card manufacturers, bank card program managers at leading financial institutions, government eID program directors, telecom procurement executives, and transit authority technology officers. Primary insights validated market sizing, segmentation estimates, technology adoption timelines, and competitive positioning assessments.

Secondary Research

Secondary sources include EMVCo transaction data and EMV deployment statistics, GSMA Intelligence connected device reports, World Bank Global Findex Database 2024, Bank for International Settlements payment statistics, ICAO travel document deployment data, Eurostat digital public services adoption data, company annual reports, and trade publications including Smart Card Alliance journals, CardTechnology Magazine, and NFC World.

Forecasting Models

Market estimates combined top-down and bottom-up models using shipment volumes, pricing, and penetration rates, alongside GDP growth, digital payments adoption, government programs, and SIM refresh cycles, with scenario analysis applied to address eSIM adoption uncertainty.

Smart Card Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Contact-Based, Contactless, Dual Interface |

| Components Covered | Memory Based, Microcontroller Based, Magnetic Stripes |

| Applications Covered | Payment Transactions, ID Verification, Access Control |

| End Users Covered | BFSI, Telecommunication, Healthcare, Government, Transportation, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Thales Group, IDEMIA, Giesecke+Devrient GmbH, HID Global Corporation, Sony Corporation, Avio Smart Market Stack Ltd., CardLogix Corporation, dzcard (Toppan Security subsidiary), etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the smart card market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global smart card market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the smart card industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Smart Card Market Report

The global smart card market was valued at USD 10.54 Billion in 2025, driven by EMV payment card issuance, 5G SIM card rollout, and government digital identity program expansion worldwide.

The market is projected to reach USD 14.26 Billion by 2034, growing at a CAGR of 3.32% during 2026-2034, driven by contactless payment adoption, healthcare e-card mandates, and biometric card integration.

Contact-Based smart cards lead with a 46.8% share in 2025, anchored by global EMV chip-and-PIN standards mandated by Visa, Mastercard, and American Express across 80+ countries for payment card security.

Dual Interface cards are the fastest-growing type at ~5.2% CAGR, as banks globally standardize on combined contact and contactless card bodies, reducing issuance complexity and reissuance operational costs.

Telecommunication leads at 27.9% in 2025, driven by global SIM card volumes and 5G UICC upgrade cycles. GSMA projects 5.9 billion 5G connections by 2030, sustaining SIM card replacement demand.

Asia-Pacific dominates at 38.9% in 2025, led by China's Union Pay network of 9.5 billion cards, India's Aadhaar and PMJDY programs, and South Korea's advanced transit smart card infrastructure.

Key drivers include EMV payment card mandates, 5G SIM refresh cycles, government e-ID and e-passport programs, contactless NFC payment adoption, and healthcare EHR card mandates across Europe and Asia.

Leading companies include Thales Group, IDEMIA, Giesecke+Devrient GmbH, HID Global Corporation, Sony Corporation, Avio Smart Market Stack Ltd., CardLogix Corporation, and dzcard (Toppan Security subsidiary).

eSIM is reshaping the telecom SIM segment – physical SIM volume is declining in premium markets while eSIM management platform revenues grow. Over 1 billion eSIM-capable devices shipped globally in 2024.

Biometric payment cards embed a fingerprint sensor on the card surface, storing the cardholder template on-card without external transmission. Standard Bank and BNP Paribas have commercially deployed biometric Visa cards.

Healthcare smart cards store encrypted patient identity and insurance data, enabling secure EHR access. Germany's eGK health card program covers 73 million insured citizens, the world's largest single-country health card program.

Sub-Saharan Africa's mobile money ecosystem (600 million subscribers), India's National Common Mobility Card rollout across 25 cities, and Latin American bancarization programs represent significant underpenetrated growth opportunities.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade