Smart Grid Market Report by Component (Software, Hardware, Services), End-User (Residential, Commercial, Industrial), and Region 2026-2034

Smart Grid Market Size:

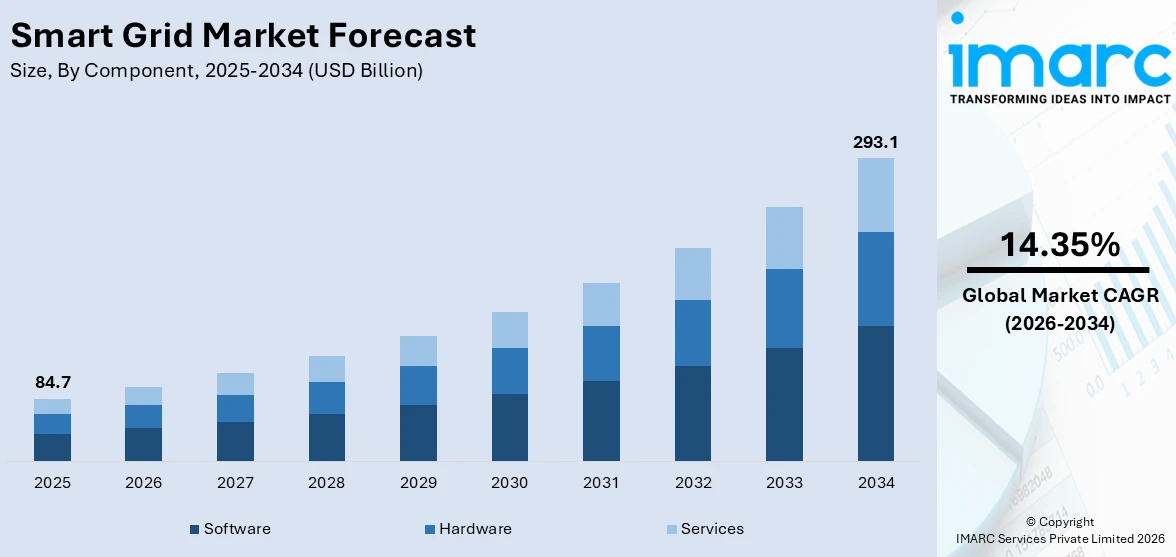

The global smart grid market size reached USD 84.7 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 293.1 Billion by 2034, exhibiting a growth rate (CAGR) of 14.35% during 2026-2034. The increasing energy efficiency demands, advancements in information communication and technology (ICT), the implementation of supportive government policies, escalating carbon emission reduction efforts, growing consumer demand for reliable power, and enhanced grid security are some of the factors accelerating the market growth.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 84.7 Billion |

| Market Forecast in 2034 | USD 293.1 Billion |

| Market Growth Rate 2026-2034 |

14.35%

|

Smart Grid Market Analysis:

- Market Growth and Size: The global smart grid market is experiencing significant growth, driven by increased investments in renewable energy, urbanization, and modernization of aging grid infrastructures. This growth is further fueled by the rising energy demands across the globe and the shift towards sustainable energy practices.

- Major Market Drivers: The smart grid market is propelled by key drivers, such as increasing electric vehicle (EV) adoption, escalating demand for grid stability in extreme weather, and evolving consumer expectations for interactive services. Additionally, increased focus on reducing power theft, growth in home energy management systems, and burgeoning investments in smart city infrastructure are supporting the market growth. Besides this, the emergence of smart homes and the development of battery storage technologies indicate a multifaceted growth trajectory for the smart grid sector.

- Technological Advancements: Technological advancements are at the core of the smart grid market's evolution. Developments in artificial intelligence (AI), machine learning (ML), and the Internet of Things (IoT) have significantly enhanced grid automation and management capabilities. Furthermore, innovations in communication technologies have improved the connectivity and responsiveness of smart grids, enabling more efficient and reliable energy distribution and management.

- Industry Applications: Smart Grids are widely applied in utility-scale electricity distribution, enabling better load management, fault detection, and response to changing energy demands. Moreover, they are essential in developing smart cities, providing the infrastructure for efficient energy management and supporting EV charging networks.

- Key Market Trends: The smart grid market is characterized by emerging trends, such as an increased focus on consumer engagement and interactive technologies, growing adoption of cloud-based solutions for grid management, and the rise of edge computing in grid operations. This is further supported by the development of microgrids for localized energy distribution, integration of blockchain for secure transactions, and growing emphasis on predictive maintenance. Furthermore, the expansion of 5G technology enhancing grid communication, increased use of drones for grid inspection, and growing focus on sustainability are other key market trends.

- Geographical Trends: Currently, North America leads the smart grid market, primarily due to the early adoption of smart grid technologies, strong government support, and significant investments in grid modernization. The region's focus on renewable energy integration and energy efficiency drives its market dominance. However, Asia-Pacific is rapidly emerging as a key market, with countries like China and India investing heavily in smart grid technologies to meet their growing energy demands and environmental goals.

- Competitive Landscape: The smart grid market is highly competitive, with a mix of established players and emerging startups. Competition is driven by technological innovation, strategic partnerships, and geographic expansion. The leading companies are constantly evolving, offering advanced solutions to meet the growing and changing demands of the smart grid market.

- Challenges and Opportunities: The smart grid market faces challenges like high initial investment costs, cybersecurity threats, and the need for skilled workforce and standardization. However, these challenges present opportunities for innovation and development. Opportunities lie in developing cost-effective solutions, enhancing cybersecurity measures, training skilled personnel, and establishing global standards. Furthermore, the growing emphasis on sustainability and renewable energy presents significant opportunities for smart grid expansion and development.

To get more information on this market Request Sample

Smart Grid Market Trends:

Growing demand for energy efficiency

The increasing need for energy efficiency in electricity supply systems is a primary driver of the global smart grid market. Traditional power grids often suffer from significant energy losses during transmission and distribution, primarily due to outdated infrastructure and a lack of real-time monitoring capabilities. Smart grids address these inefficiencies through advanced technologies like smart meters and grid automation, which enable better control and optimization of electricity flow. This results in reduced energy wastage, more efficient use of resources, and lower operational costs. Additionally, smart grids facilitate demand response programs, allowing for more effective load management and further contributing to energy savings.

Integration of renewable energy sources

Smart grids are instrumental in integrating renewable energy sources like wind and solar power into our electricity systems. These renewable sources are known for their variable and less predictable energy output compared to traditional energy sources. Traditional power grids often struggle to handle these fluctuations effectively. Smart grids, with their advanced technology, provide a more dynamic and responsive infrastructure, enabling better management and distribution of the variable energy produced by renewable sources. This enhanced capability is essential for incorporating a higher proportion of renewable energy into our electricity networks, supporting a transition to more sustainable energy practices. Smart grids, however, are equipped with advanced technology that can better manage and balance these fluctuations. They allow for real-time monitoring and control of energy production and distribution, ensuring a stable and reliable power supply. This integration is essential for transitioning to more sustainable energy systems and reducing reliance on fossil fuels. Furthermore, smart grids can support distributed generation, where energy is produced closer to where it is used, reducing transmission losses and further promoting the use of renewables.

Advancements in information and communication technology (ICT)

ICT advancements are a fundamental driver in the evolution and implementation of smart grids. The incorporation of modern ICT into grid infrastructure allows for the real-time collection, analysis, and management of vast amounts of data. This data is crucial for the efficient operation of smart grids, enabling predictive maintenance, better load management, and quick response to power outages or other issues. Technologies such as AI and machine learning (ML) further enhance the capabilities of smart grids, allowing for more sophisticated data analysis and decision-making. These advancements not only improve the efficiency and reliability of the power supply but also pave the way for innovative applications and services in energy management.

Government policies and regulations

Government policies and regulations significantly influence the development and deployment of smart grids. Many governments around the world have recognized the potential of smart grids in achieving energy efficiency, reducing carbon emissions, and transitioning to renewable energy sources. As a result, they have implemented policies and regulations that promote and sometimes mandate the adoption of smart grid technologies. These can include financial incentives, subsidies, and regulatory frameworks that encourage investment and innovation in this sector. For instance, policies mandating the installation of smart meters in homes and businesses have been instrumental in driving the growth of smart grids. Government initiatives also play a vital role in setting standards and protocols for smart grid interoperability and security, ensuring a cohesive and secure development of the smart grid infrastructure.

Smart Grid Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global and regional levels for 2026-2034. Our report has categorized the market based on component and end-user.

Breakup by Component:

- Software

- Advanced Metering Infrastructure

- Smart Grid Distribution Management

- Smart Grid Network Management

- Substation Automation

- Others

- Hardware

- Sensor

- Programmable Logic Controller

- AMI Metre

- Networking Hardware

- Others

- Services

- Consulting

- Support and Maintenance

- Deployment and Integration

Software accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the component. This includes software (advanced metering infrastructure, smart grid distribution management, smart grid network management, substation automation, others), hardware (sensor, programmable logic controller, AMI metre, networking hardware, others), and services (consulting, support and maintenance, deployment and integration). According to the report, software represented the largest segment.

The software segment of the smart grid market is driven by the increasing need for efficient grid management and data analytics. As grids become more complex with the integration of various energy sources, the demand for sophisticated software solutions for grid management, data analysis, and predictive maintenance is growing. These solutions enable utilities to optimize energy distribution, integrate renewable resources effectively, and enhance customer engagement through real-time data insights. Additionally, the adoption of cloud computing, AI, and IoT in smart grid applications further propels the software segment, offering advanced capabilities for real-time monitoring, control, and decision-making processes in grid operations.

The hardware segment is driven by the increasing requirement for robust and advanced infrastructure in smart grids. This includes the need for smart meters, sensors, and control devices that facilitate real-time monitoring and energy management. The integration of renewable energy sources into the grid necessitates the development of sophisticated hardware capable of handling variable energy inputs and ensuring grid stability. Moreover, advancements in communication technologies are crucial for the hardware segment, as they enable the seamless transmission of data between various grid components.

The services segment is driven by the increasing demand for professional and managed services in the implementation and maintenance of smart grids. This includes consultation, installation, support, and maintenance services that are crucial for the successful deployment and operation of smart grids. The complexity of smart grid systems requires specialized expertise, driving demand for skilled professionals capable of managing these sophisticated networks. Furthermore, as cybersecurity becomes a major concern, the demand for security services is also rising, ensuring the protection of sensitive data and infrastructure.

Breakup by End User:

Access the comprehensive market breakdown Request Sample

- Residential

- Commercial

- Industrial

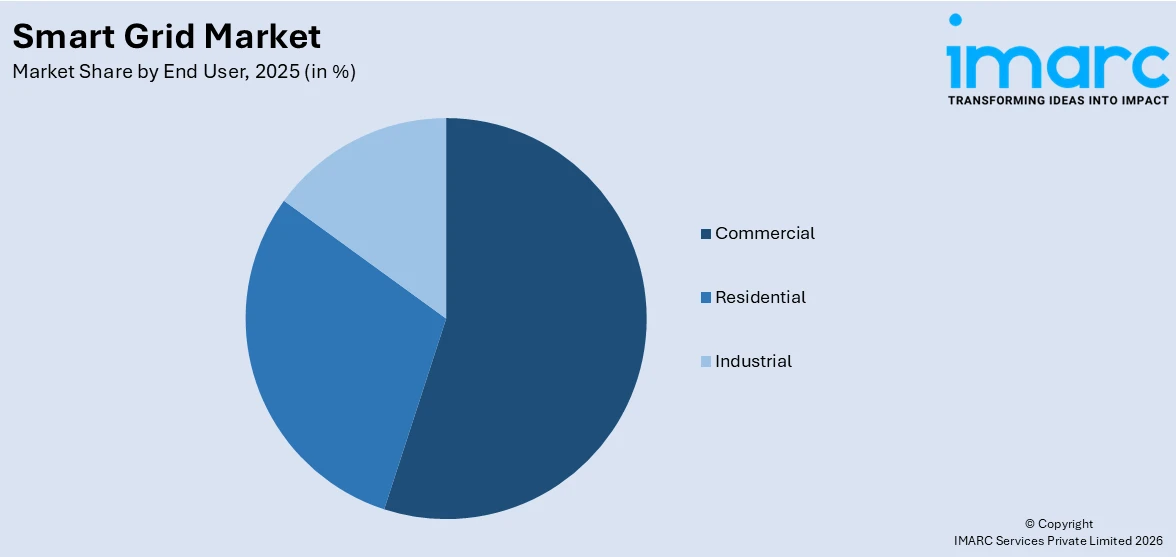

Commercial accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the end user. This includes residential, commercial, and industrial. According to the report, commercial represented the largest segment.

The commercial segment is driven by the increasing need for reliable and efficient energy management in businesses and public facilities. Commercial buildings, including offices, shopping centers, and hospitals, are adopting smart grid technologies to reduce operational costs, ensure consistent power supply, and enhance their sustainability practices. The commercial sector is also influenced by regulatory pressures to reduce carbon footprints and by incentives for using renewable energy sources. Furthermore, the adoption of advanced metering infrastructure and energy management systems in commercial buildings for better load management and predictive maintenance is fueling the market growth in this segment.

The residential segment is driven by the increasing demand for energy-efficient and cost-saving solutions, such as smart meters and home energy management systems. Homeowners are becoming more aware of the benefits of energy conservation and are adopting smart grid technologies to optimize electricity usage, reduce bills, and contribute to environmental sustainability. Additionally, the growing trend of smart homes, equipped with IoT devices that require efficient energy management, is propelling the residential smart grid market.

The industrial segment is driven by the increasing emphasis on industrial automation and the need for robust energy management systems. Large-scale industries, such as manufacturing and processing plants, require a steady and reliable energy supply to maintain continuous operations. Smart grid technologies in these settings help in optimizing energy use, reducing downtime, and improving overall operational efficiency. Additionally, the industrial segment is benefiting from the implementation of demand response programs and advanced grid analytics to manage high energy demands and reduce costs.

Breakup by Region:

- Asia Pacific

- Europe

- North America

- Middle East and Africa

- Latin America

North America leads the market, accounting for the largest smart grid market share

The market research report has also provided a comprehensive analysis of all the major regional markets, which include Asia Pacific, Europe, North America, Middle East and Africa, and Latin America. According to the report, North America accounted for the largest market share.

North America's smart grid market is driven by the need to modernize aging electricity infrastructure and the increasing adoption of renewable energy sources. The region has a strong regulatory framework supporting the development of smart grids, including incentives and policies encouraging the deployment of smart technologies. There is also a growing demand for improved grid reliability and efficiency, particularly in the face of extreme weather events. Moreover, the high penetration of advanced metering infrastructure and the push for energy independence further stimulate the market in the region.

The Asia Pacific’s smart grid market is driven by the increasing demand for energy due to rapid urbanization and industrialization, especially in emerging economies like China and India. Governments in this region are actively promoting smart grid technologies to enhance energy efficiency and integrate renewable energy sources. Significant investments in upgrading aging infrastructure and the growing emphasis on reducing carbon emissions further fueling the market.

The European market is driven by the increasing focus on renewable energy integration and energy efficiency mandates. Europe's commitment to meet stringent climate goals has led to the adoption of smart grid technologies for better energy management and reduced carbon footprint. The region benefits from strong government support and favorable policies, along with high consumer awareness about energy conservation.

The Middle East and Africa region is driven by the increasing demand for reliable and efficient energy supply, especially in rapidly urbanizing areas. Governments in this region are investing in smart grid technologies to improve energy distribution and manage the growing demand.

Latin America's smart grid market is driven by the increasing need for energy efficiency and reliable electricity supply in the face of growing urbanization. Governments in the region are investing in smart grid infrastructure to improve the management of energy resources and reduce technical losses in electricity distribution. Additionally, the need to modernize aging power infrastructure and the potential for reducing electricity theft are significant drivers of the smart grid market in Latin America.

Leading Key Players in the Smart Grid Industry:

Key players in the smart grid market are actively engaging in a range of strategic initiatives to strengthen their market position and respond to the evolving demands of this dynamic sector. They are heavily investing in research and development (R&D) to innovate and improve smart grid technologies, such as advanced metering infrastructure, grid automation, and energy storage systems. These companies are also forming strategic partnerships and collaborations with technology firms, governments, and utility companies to expand their reach and expertise. Another significant focus is on integrating renewable energy sources with the existing grid infrastructure, aiming to enhance sustainability and efficiency. Additionally, they are developing more secure and resilient grid systems to address the growing concerns over cybersecurity threats. To cater to the diverse global market, these players are tailoring their solutions to meet regional needs and regulations, ensuring compliance and maximizing market penetration.

The market research report has provided a comprehensive analysis of the competitive landscape. Detailed profiles of all major companies have also been provided. Some of the key players in the market include:

- ABB Ltd.

- Cisco Systems Inc.

- Eaton

- Fujitsu Limited

- GE Vernova, Inc

- Honeywell International Inc.

- International Business Machines Corporation

- Schneider Electric SE

- Siemens AG

- Wipro Limited

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

Latest News:

- In June 2022: Cisco unveiled new cloud management capabilities to provide a more unified IT experience. This included cloud management for Cisco Catalyst, giving customers the option to bring the simplicity of the Meraki Cloud to their existing Catalyst deployments.

- In January 2022: Siemens AG is focusing on integrating renewable energy into the power grid, as highlighted in their "Grid Edge" initiative. This approach emphasizes the coupling of decentralized power grids with advanced technologies to facilitate energy transition and decarbonization.

- In October 2022: Eaton announced the launch of its new advanced energy storage system, the EnergyAware UPS. This innovative system is designed to help customers reduce energy costs and improve power reliability by intelligently storing and deploying energy during peak demand periods. It integrates seamlessly with Eaton's existing power management solutions.

Smart Grid Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered |

|

| End-Users Covered | Residential, Commercial, Industrial |

| Regions Covered | Asia Pacific, Europe, North America, Middle East and Africa, Latin America |

| Companies Covered | ABB Ltd., Cisco Systems Inc., Eaton, Fujitsu Limited, GE Vernova, Inc, Honeywell International Inc., International Business Machines Corporation, Schneider Electric SE, Siemens AG, Wipro Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the global smart grid market performed so far, and how will it perform in the coming years?

- What are the drivers, restraints, and opportunities in the global smart grid market?

- What is the impact of each driver, restraint, and opportunity on the global smart grid market?

- What are the key regional markets?

- Which countries represent the most attractive smart grid market?

- What is the breakup of the market based on the component?

- Which is the most attractive component in the smart grid market?

- What is the breakup of the market based on end-user?

- Which is the most attractive end-user in the smart grid market?

- What is the competitive structure of the market?

- Who are the key players/companies in the global smart grid market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the smart grid market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global smart grid market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the smart grid industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)