Smart Lock Market Size, Share, Trends and Forecast by Lock Type, Communication Protocol, End-User, and Region, 2026-2034

Smart Lock Market Size, Share, Trends & Forecast (2026-2034)

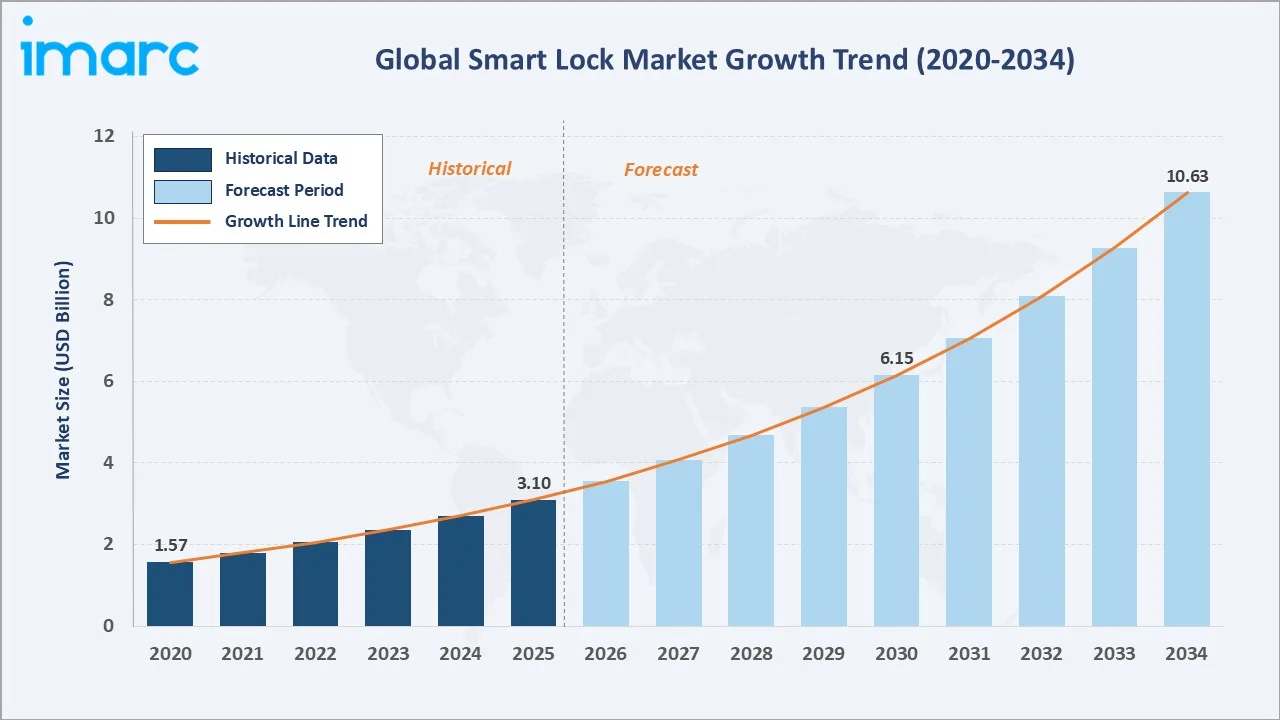

The global smart lock market reached USD 3.10 Billion in 2025 and is projected to reach USD 10.63 Billion by 2034, growing at a CAGR of 14.65% during 2026-2034. Rapid smart home ecosystem adoption, rising security awareness among residential and commercial users, proliferation of IoT connectivity infrastructure, growing demand for contactless and keyless access solutions, and expanding integration with voice assistants and mobile platforms are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.10 Billion |

|

Forecast Market Size (2034) |

USD 10.63 Billion |

|

CAGR (2026-2034) |

14.65% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

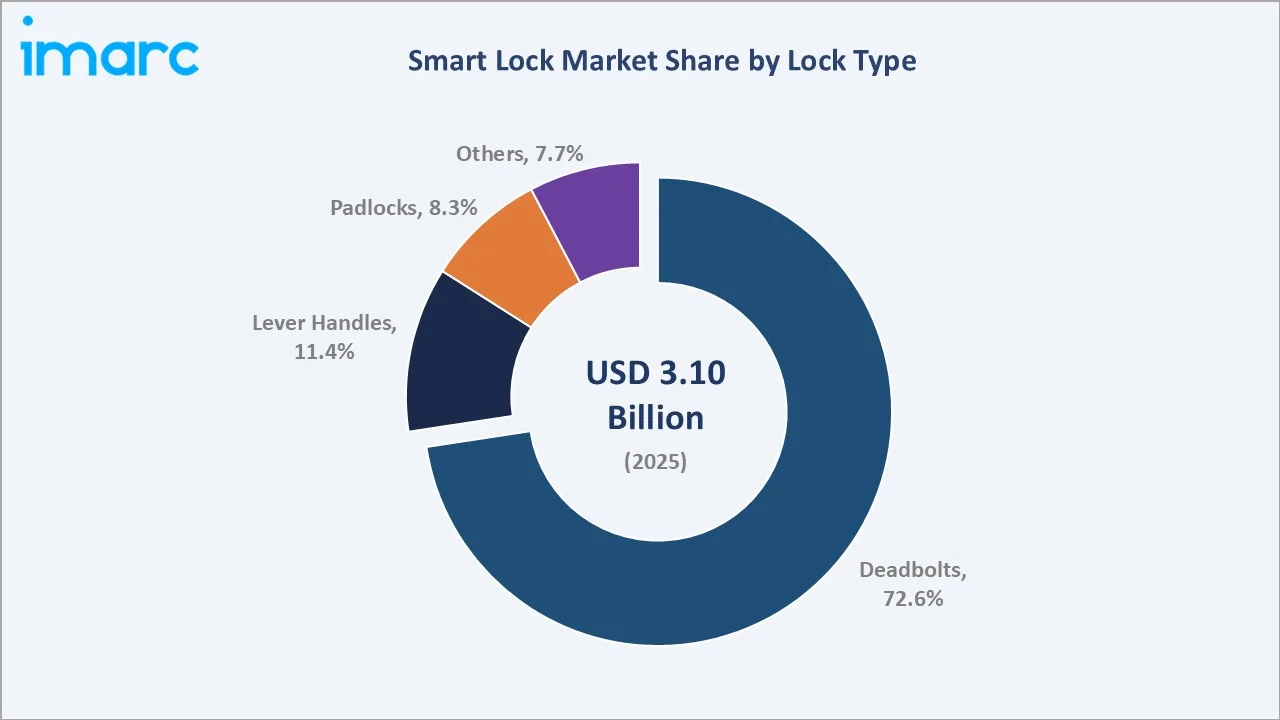

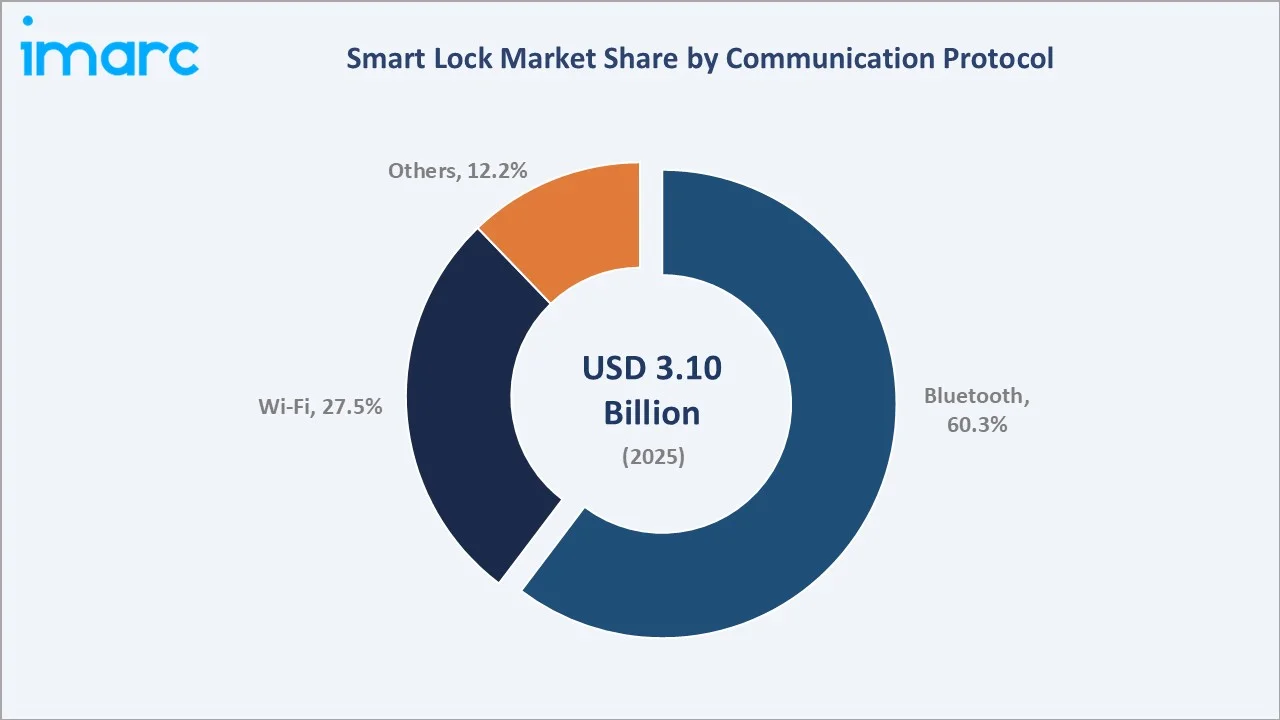

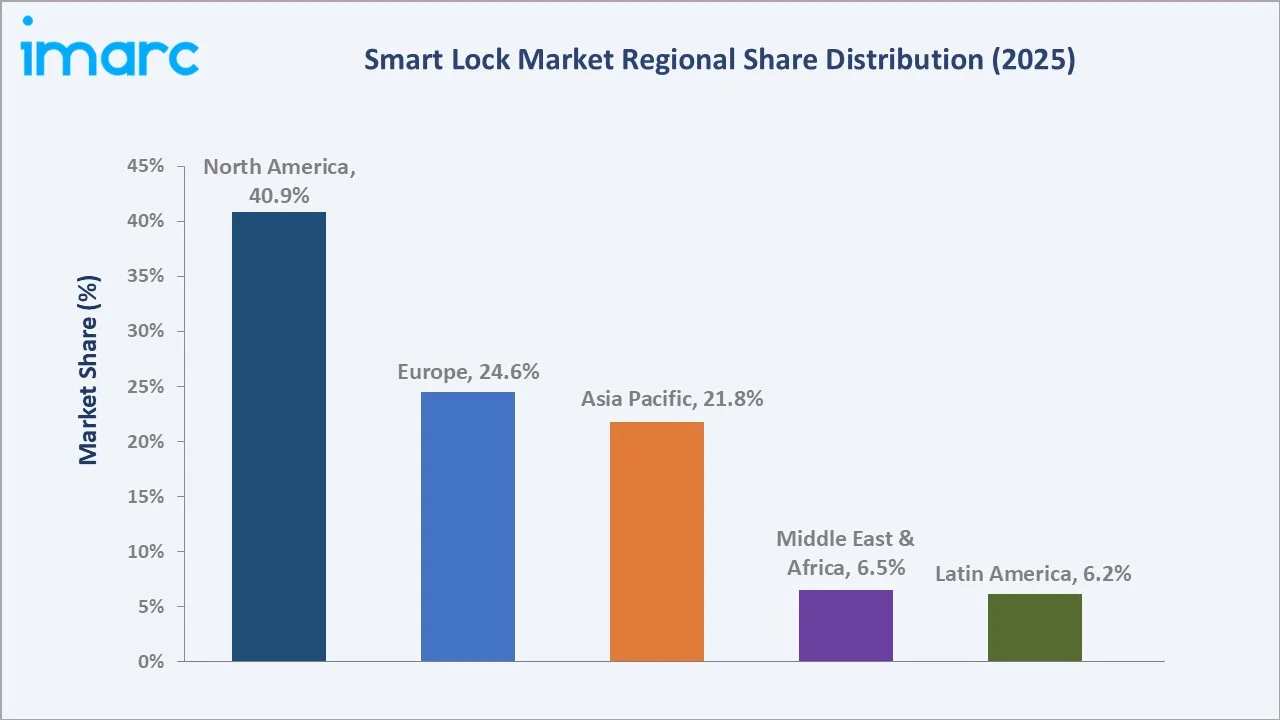

North America leads regionally with a 40.9% share in 2025, driven by high smart home technology adoption rates, mature residential IoT infrastructure, and strong consumer demand for integrated security systems. Deadbolts command the dominant lock type segment at 72.6%, while Bluetooth remains the leading communication protocol at 60.3%.

To get more information on this market, Request Sample

The market grew from USD 1.57 Billion in 2020 to USD 3.10 Billion in 2025, reflecting a historical CAGR of approximately 14.6%. The forecast period 2026–2034 projects accelerating growth anchored by smart home platform proliferation, rising commercial building automation investment, 5G connectivity expansion, and growing consumer preference for remote access management and biometric security solutions.

Executive Summary

The global smart lock market is experiencing high-growth expansion underpinned by converging megatrends in smart home technology, IoT connectivity, and heightened security awareness across both residential and commercial segments. The market reached USD 3.10 Billion in 2025 and is forecast to reach USD 10.63 Billion by 2034 at a CAGR of 14.65%.

Deadbolts dominate the lock type segment with a 72.6% share in 2025, reflecting the critical role of deadbolt-style smart locks in residential front door security, the primary use case driving consumer smart lock adoption. Bluetooth leads communication protocol at 60.3%, driven by its energy efficiency, local connectivity, and seamless smartphone integration.

North America commands the largest regional share at 40.9%, anchored by high smart home technology penetration, strong demand from the residential sector, and well-established distribution ecosystems for smart security products. Key players including ASSA ABLOY, Allegion plc, dormakaba Group, SALTO WECOSYSTEM, and Fortune Brands Innovations are competing through product innovation, AI and biometric integration, and strategic smart home platform partnerships.

Key Market Insights

|

Insight |

Data |

|

Largest Lock Type |

Deadbolts – 72.6% share (2025) |

|

Fastest Growing Type |

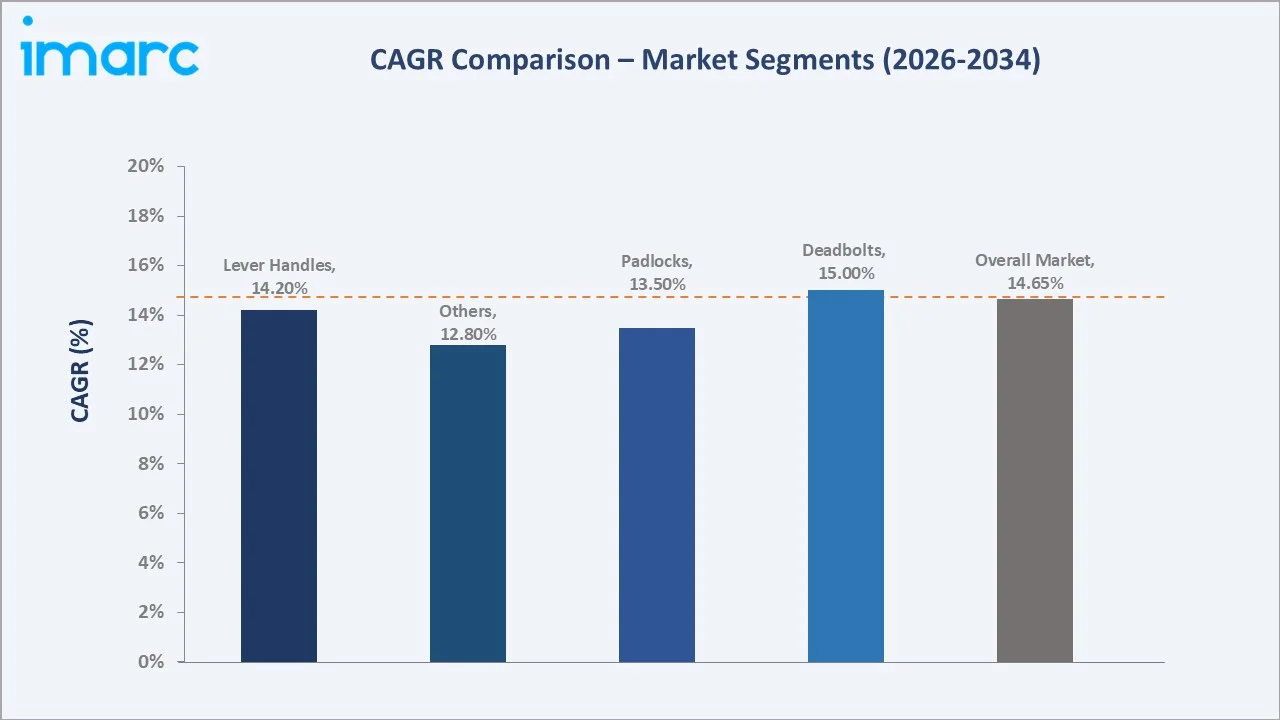

Deadbolts – ~15.0% CAGR (2026-2034) |

|

Leading Protocol |

Bluetooth – 60.3% share (2025) |

|

Fastest Growing Protocol |

Wi-Fi – ~15.5% CAGR (2026-2034) |

|

Leading Region |

North America – 40.9% share (2025) |

|

Top Companies |

ASSA ABLOY, Allegion plc, dormakaba Group, SALTO WECOSYSTEM, and Fortune Brands Innovations |

Key Analytical Observations Supporting the Above Data:

- Deadbolts at 72.6% (2025) reflect the dominant use case of smart locks in residential front door and primary entry point security. Deadbolt-style smart locks represent the market's highest-volume product category, benefiting from direct compatibility with existing standard door hardware and consumer familiarity with deadbolt security standards.

- Bluetooth at 60.3% leads communication protocol due to its energy efficiency, direct smartphone pairing without internet dependency, and strong consumer privacy credentials. Bluetooth Low Energy (BLE)-based smart locks dominate the residential consumer market, offering simple app-based setup and auto-unlock proximity detection features.

- Wi-Fi at 27.5%, growing at ~15.5% CAGR, is the market's fastest-growing protocol segment, driven by demand for remote access management from anywhere without a separate hub device. Wi-Fi-enabled smart locks allow homeowners and property managers to control access remotely, receive real-time activity notifications, and integrate with cloud-based property management systems.

- North America at 40.9% reflects the region's leading smart home technology adoption rate, with approximately 69% of US households owning at least one smart home device in 2025. Strong consumer awareness of home security, mature e-commerce distribution, and active retail presence of smart lock products sustain the region's dominant market position.

Smart Lock Market Overview

Smart locks are electronically controlled locking mechanisms that replace or augment traditional mechanical key-operated locks, providing keyless entry through digital authentication methods including PIN codes, biometric fingerprint or facial recognition, Bluetooth smartphone proximity, Wi-Fi remote access, RFID cards, and voice assistant integration.

The market is driven by the convergence of smart home platform ecosystems, growing consumer awareness of remote access security, and expanding commercial building automation investment by property managers and hospitality operators. The rollout of the Matter smart home interoperability standard in 2022 significantly reduced fragmentation across smart lock platforms, accelerating consumer adoption by enabling cross-platform device compatibility for the first time.

Market Dynamics

To evaluate market opportunities, Request Sample

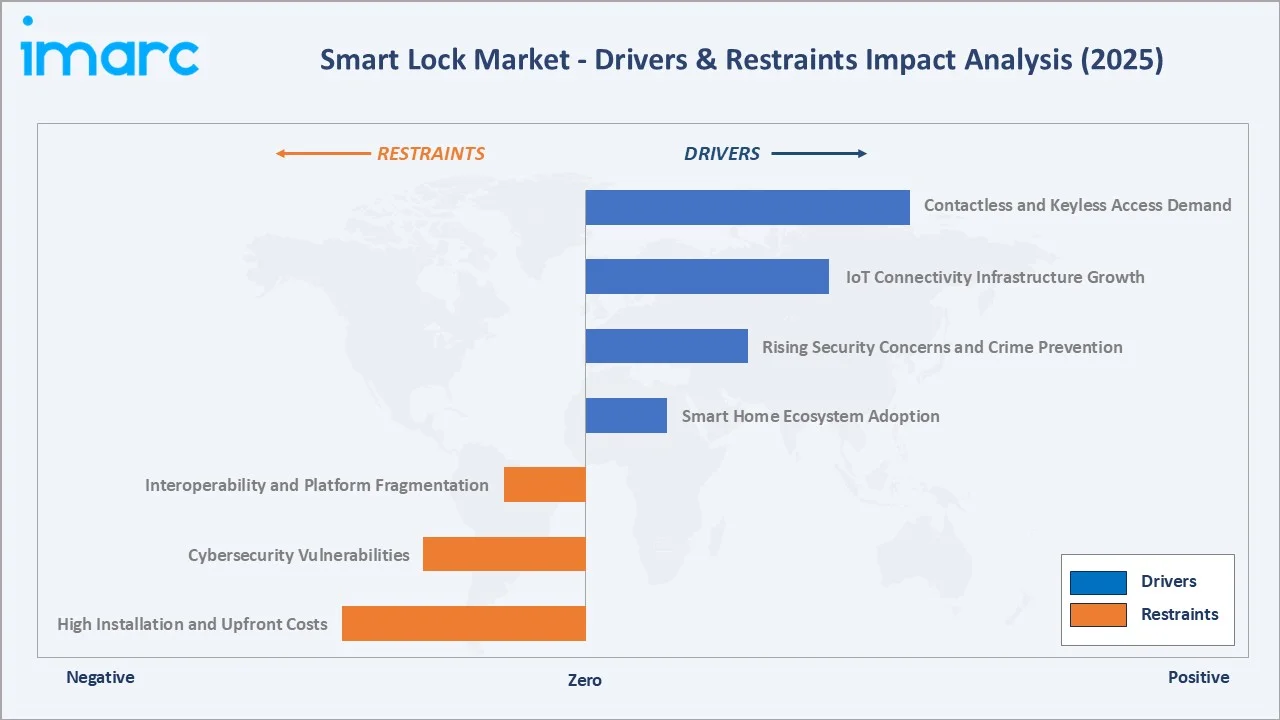

Market Drivers

- Smart Home Ecosystem Adoption: The rapid expansion of smart home platforms including Amazon Alexa, Google Home, Apple HomeKit, and Samsung SmartThings is the primary structural driver of smart lock market growth. Smart locks represent a fundamental smart home entry point, and platform ecosystem expansion directly expands the addressable market for connected security devices.

- Rising Security Concerns and Crime Prevention: Growing urban residential security concerns and increasing commercial property security investment are driving smart lock adoption. Smart locks provide real-time access logging, instant lock/unlock notification, and temporary access code management.

- IoT Connectivity Infrastructure Growth: The global expansion of high-speed internet connectivity, 4G/5G mobile network coverage, and smart home hub proliferation is enabling always-connected smart lock deployments across previously underserved geographies. In Asia Pacific and Latin America, rapidly expanding urban broadband penetration is opening new market segments for Wi-Fi-enabled smart locks with remote access management capabilities.

- Contactless and Keyless Access Demand: The COVID-19 pandemic permanently accelerated consumer and commercial preference for touchless access solutions, establishing contactless entry as a standard expectation in both residential and commercial environments. Hotels, offices, co-working spaces, and rental property platforms are systematically transitioning to keyless entry.

Market Restraints

- High Installation and Upfront Costs: Premium smart lock systems, particularly commercial-grade and multi-door deployments, command significant upfront hardware and installation costs versus conventional mechanical locks. Entry-level consumer smart locks range from USD 100–300, while commercial access control systems scale to several thousand dollars per door.

- Cybersecurity Vulnerabilities: Smart locks' dependence on wireless communication protocols introduces cybersecurity risks including Bluetooth relay attacks, Wi-Fi hacking, and firmware vulnerabilities that can compromise physical security. High-profile smart lock vulnerability disclosures by security researchers create consumer hesitation and increase product development and security certification costs.

- Interoperability and Platform Fragmentation: Despite the Matter 1.0 standard's launch in 2022, ecosystem fragmentation between Apple HomeKit, Amazon Alexa, Google Home, and Samsung SmartThings creates consumer confusion and compatibility concerns that slow replacement purchasing cycles.

Market Opportunities

- Commercial Real Estate and Hospitality Expansion: The commercial real estate sector, encompassing hotels, co-working spaces, student housing, multi-family residential, and healthcare facilities, represents the highest-growth near-term opportunity for smart lock manufacturers.

- AI-Powered Biometric Authentication: Samsung's residential SHP-DP920 biometric smart lock and ASSA ABLOY's iDFlex biometric commercial access control systems demonstrate the market's evolution toward multi-factor authentication as a standard feature in premium smart security products.

Market Challenges

- Battery Life and Power Reliability: Smart locks depend on battery power for wireless connectivity and electronic actuation, creating maintenance challenges in commercial multi-door deployments and consumer anxiety about lockout risk during battery depletion.

- Consumer Resistance to Legacy Lock Replacement: A significant proportion of residential consumers and small commercial operators remain attached to familiar mechanical key security and are reluctant to invest in smart lock upgrades without a compelling security-motivated purchase trigger.

Emerging Market Trends

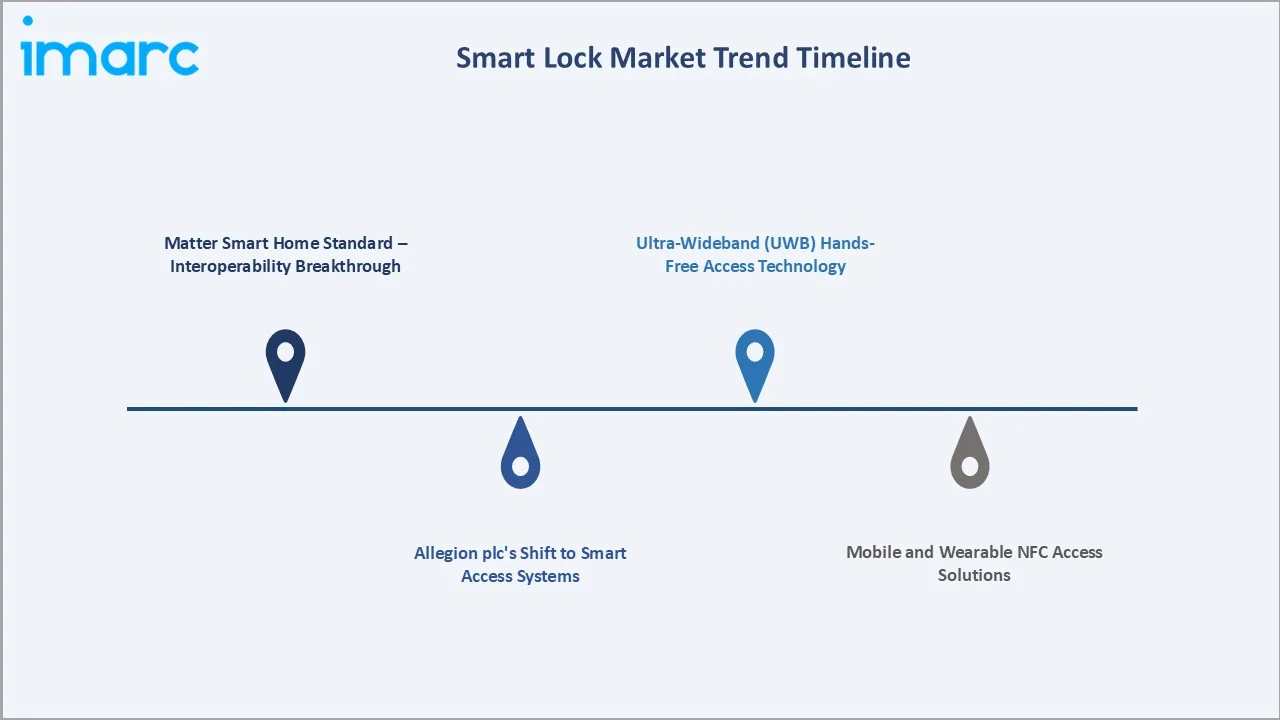

1. Matter Smart Home Standard – Interoperability Breakthrough

The launch of the Matter smart home interoperability standard in late 2022 fundamentally transformed smart lock market dynamics by enabling cross-platform device compatibility. Smart locks supporting Matter can seamlessly integrate with any major smart home platform without proprietary hub requirements, significantly reducing consumer friction and accelerating replacement cycles.

2. Ultra-Wideband (UWB) Hands-Free Access Technology

Ultra-Wideband (UWB) technology is emerging as the next generation of smart lock proximity communication, enabling centimeter-level spatial precision that allows smart locks to detect an authorized user's exact position and automatically unlock only when they are directly at the door. Apple's AirTag-proven UWB ecosystem and Samsung's SmartThings spatial sensing platform are accelerating UWB adoption in premium smart lock products.

3. Mobile and Wearable NFC Access Solutions

According to new research from Parks Associates, 84% of smart lock purchase intenders intending to purchase smart locks are interested in using mobile phones and wearable devices for NFC-based home access, reflecting growing demand for contactless smart home security solutions. The findings highlight increasing adoption of AI-enabled access control, interoperability standards, and integrated smart home ecosystems that combine security, automation, and connected living experiences.

4. Allegion plc's Shift to Smart Access Systems

Allegion plc is accelerating the shift from traditional mechanical doors to smart access systems through connected locks, cloud-based access control, and mobile-enabled entry technologies designed for homes and commercial buildings. The company’s strategy focuses on interoperability, remote access management, and recurring software-driven services as rising demand for smart security solutions reshapes the global access control market.

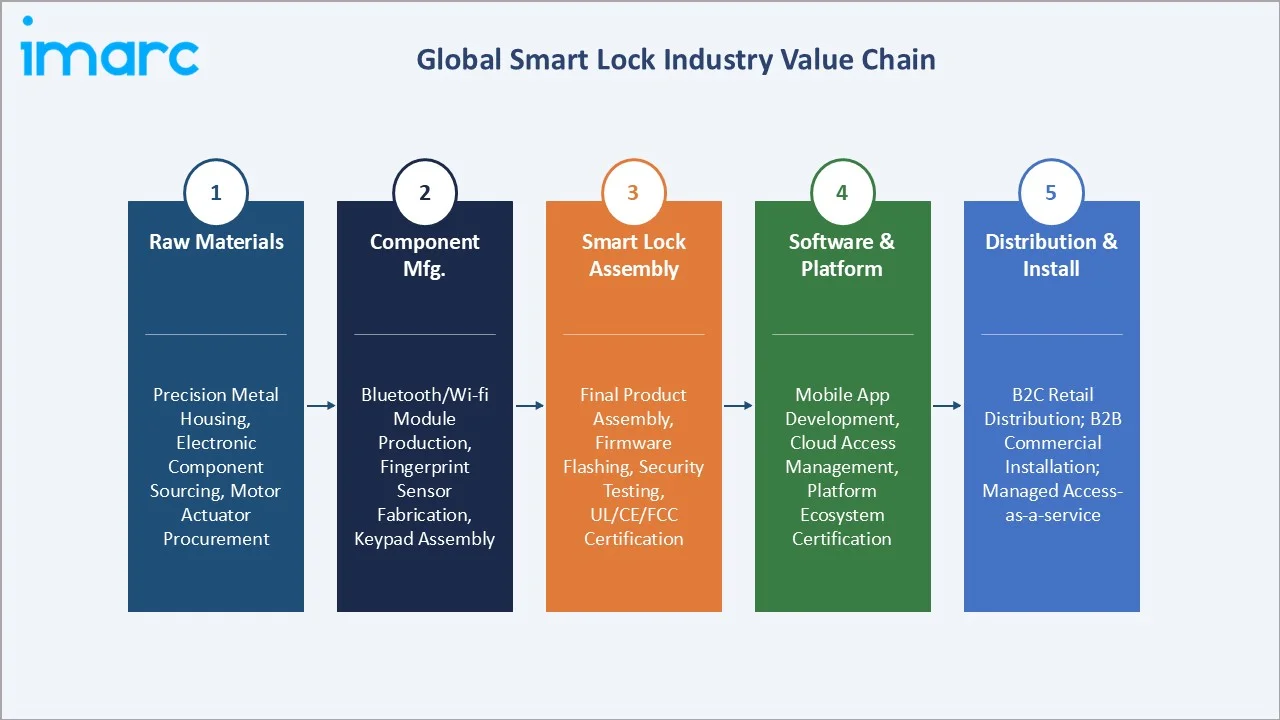

Industry Value Chain Analysis

The smart lock market value chain spans electronic component and raw material sourcing through end-user deployment and managed service operation, with significant value creation at the firmware development, platform integration, and cloud service subscription stages that differentiate digital smart lock products from traditional mechanical security hardware.

|

Stage |

Value-Add Activity |

|

Raw Materials |

Precision metal housing, electronic component sourcing, motor actuator procurement |

|

Component Mfg. |

Bluetooth/Wi-Fi module production, fingerprint sensor fabrication, keypad assembly |

|

Smart Lock Assembly |

Final product assembly, firmware flashing, security testing, UL/CE/FCC certification |

|

Software & Platform |

Mobile app development, cloud access management, platform ecosystem certification |

|

Distribution & Install |

B2C retail distribution; B2B commercial installation; managed access-as-a-service |

Technology Landscape in the Smart Lock Industry

Smart Deadbolts – Residential Security Standard

Smart deadbolts are designed as direct replacements for or upgrades to existing mechanical deadbolt hardware, fitting standard ANSI/BHMA-compliant door preparations without structural modification. Leading smart deadbolt products including the Schlage Encode Plus, Yale Assure Lock 2, and August Wi-Fi Smart Lock represent the market's highest-volume consumer SKUs, available through major retail channels at price points ranging from USD 150–300 per unit.

Smart Lever – Commercial Office and ADA-Compliant Access

Smart lever handles from Allegion's Schlage commercial line and ASSA ABLOY's HID Global provide card reader integration, RFID/NFC credential compatibility, and access control software connectivity for multi-door enterprise deployments. The growing adoption of cloud-based corporate access control systems is driving above-average growth in commercial lever handle smart lock deployments through 2034.

Smart Padlocks – Portable and Industrial Security Applications

Products including the Master Lock Bluetooth Smart Padlock and igloohome smart padlock address use cases where wired or door-integrated locks are impractical, offering keyless access through Bluetooth smartphone apps. The growing logistics and warehouse automation sector, combined with shared mobility and rental equipment applications, is expanding smart padlock adoption in commercial and industrial settings.

Bluetooth vs. Wi-Fi – Competing Protocol Architectures

Bluetooth's 60.3% share reflects its dominance in consumer residential smart locks due to energy efficiency enabling multi-year battery life, simple direct smartphone pairing, and strong consumer privacy through local-only connectivity without cloud dependency. Wi-Fi's 27.5% share and faster ~15.5% CAGR growth reflect commercial and rental property market preference for always-connected remote access management from anywhere without proximity requirement.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Lock Type |

Deadbolts |

72.6% |

2025 |

|

Communication Protocol |

Bluetooth |

60.3% |

2025 |

|

End-User |

🔒 |

🔒 |

2025 |

|

Region |

North America |

40.9% |

2025 |

By Lock Type

Deadbolts dominate the lock type segment with a 72.6% share in 2025. This segment benefits from the fundamental replacement market for the deadbolt-equipped residential doors, representing a massive addressable upgrade market for smart deadbolt products. The standardization of deadbolt form factors and consumer familiarity with deadbolt security standards sustains Deadbolts' structural market dominance across the residential smart lock segment.

To access detailed market analysis, Request Sample

Lever handles at 11.4% serve the commercial and institutional access control segment, while padlocks at 8.3% address portable and industrial security applications. The others segment at 7.7% encompasses mortise locks, rim locks, and specialty format smart locking mechanisms used in architectural applications and high-security commercial environments.

By Communication Protocol

Bluetooth leads the communication protocol segment with a 60.3% share in 2025. Bluetooth Low Energy (BLE) technology enables smart locks to maintain always-on proximity detection and auto-unlock functionality with minimal battery drain, supporting 6–12 month battery lifespans on standard AA batteries.

Wi-Fi at 27.5%, growing at approximately 15.5% CAGR, enables remote access management and real-time notifications without a separate hub device, making it the preferred protocol for short-term rental properties, property management applications, and always-connected commercial deployments. The others segment at 12.2% encompasses Z-Wave, Zigbee, Thread, and UWB protocols serving specific ecosystem and commercial integration requirements.

Regional Market Insights

North America's market leadership (40.9%, 2025) is anchored by the US’s position as the world's most advanced smart home technology consumer market, with an estimated 69% of US households owning at least one smart home device in 2025. The region benefits from mature retail, high consumer awareness of home security solutions, and strong demand from the short-term rental market.

Europe at 24.6% is driven by strong commercial building automation investment, GDPR-influenced consumer preference for local Bluetooth connectivity over cloud-dependent Wi-Fi protocols, and EU-wide smart building energy efficiency mandates requiring integrated access control in new commercial construction.

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

40.9% |

High smart home adoption; strong residential replacement market; Airbnb and short-term rental keyless entry demand |

|

Europe |

24.6% |

GDPR-driven data privacy preference for local Bluetooth protocols; strong commercial building automation investment |

|

Asia Pacific |

21.8% |

Rapid smart apartment adoption; India's expanding residential real estate development; Japan's smart home technology leadership |

|

Middle East & Africa |

6.5% |

Saudi Vision 2030 smart city investments; luxury hospitality sector keyless upgrade programs; rapidly expanding urban residential construction |

|

Latin America |

6.2% |

Growing urban residential security concerns; expanding broadband penetration enabling Wi-Fi smart lock adoption |

Asia Pacific at 21.8% benefits from China's smart apartment development ecosystem, South Korea's advanced smart home infrastructure, and India's rapidly expanding premium residential real estate segment adopting smart access control as a standard amenity.

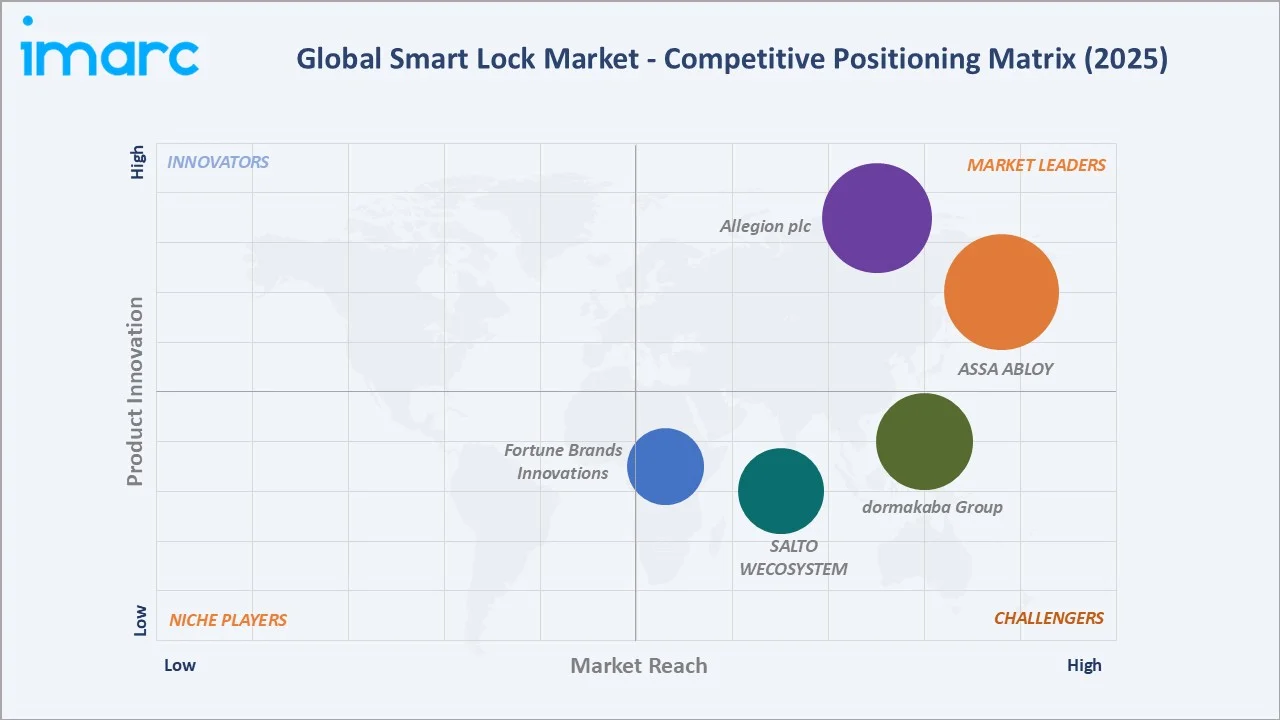

Competitive Landscape

The global smart lock market exhibits moderate concentration, with the top five players (ASSA ABLOY, Allegion plc, dormakaba Group, SALTO WECOSYSTEM, and Fortune Brands Innovations) collectively holding approximately 50–55% of global market revenue in 2025. ASSA ABLOY and Allegion plc jointly lead through comprehensive product portfolios spanning residential to enterprise-grade commercial access control, backed by decades of mechanical lock manufacturing heritage and established global distribution networks.

|

Company Name |

Key Brands |

Market Position |

Core Strength |

|

ASSA ABLOY |

ASSA ABLOY, ACCENTRA, Corbin Russwin, SARGENT, Medeco, among others |

Market Leader |

World's largest lock manufacturer; Matter certification; AI-powered series |

|

Allegion plc |

Schlage, SimonsVoss, CISA, Interflex, Isonas, Zentra, Gatewise, Elatec, Yonomi, among others |

Market Leader |

Enterprise commercial IoT integration; ADA-compliant lever handles |

|

dormakaba Group |

dormakaba |

Strong Challenger |

Global commercial access control leadership; hotel and hospitality master key systems; dormakaba evolo smart platform |

|

SALTO WECOSYSTEM |

Salto, Gantner, Vintia |

Challenger |

Cloud-based commercial access control; hospitality and education sector focus; wireless electronic RFID expertise |

|

Fortune Brands Innovations |

Master Lock, SentrySafe |

Challenger |

Bluetooth smart padlock range; contractor and portable security applications; strong brand recognition |

Market consolidation is accelerating through ASSA ABLOY's ongoing acquisition strategy and Allegion plc's commercial segment platform buildout. The Matter smart home standard is reshaping competitive dynamics by commoditizing basic protocol connectivity and shifting differentiation toward AI features, cybersecurity certifications, and cloud-based access management platform sophistication.

Key Company Profiles

ASSA ABLOY

ASSA ABLOY is the world's largest lock manufacturer and the global leader in access solutions. The company's smart lock division encompasses multiple brands serving institutional and industrial access markets.

- Brand Portfolio: ASSA ABLOY, ACCENTRA, Corbin Russwin, SARGENT, Medeco, among others.

- Recent Developments: In September 2024, ASSA ABLOY acquired Level Lock to strengthen its smart access solutions portfolio with advanced connected lock technologies, digital access platforms, and sleek retrofit smart lock designs. Level’s multifamily platform, known as Level M, operates as a standalone entity under Ambient Property Technologies.

- Strategic Focus: AI-powered security intelligence feature development; cloud-based enterprise access management platform expansion; India and Southeast Asia market entry through smart apartment developer partnerships.

Allegion plc

Allegion plc is a global provider of security products and solutions serving residential, commercial, and institutional markets. Allegion's Schlage brand is the most widely recognized smart lock brand in North America, holding a leading position in both consumer residential and commercial access control segments.

- Brand Portfolio: Schlage, SimonsVoss, CISA, Interflex, Isonas, Zentra, Gatewise, Elatec, Yonomi, among others.

- Recent Developments: In January 2025, Allegion plc showcased new smart lock innovations at CES 2025 through its Schlage brand, including the Schlage Sense Pro Smart Deadbolt and Schlage Arrive Smart WiFi Deadbolt featuring hands-free unlocking, Matter-over-Thread compatibility, and enhanced remote access management.

- Strategic Focus: Matter ecosystem leadership in consumer Schlage product lines; subscription-based cloud access management service development; growing commercial market share in healthcare, education, and multi-family residential through Allegion's Engage cloud platform.

Market Concentration Analysis

The global smart lock market exhibits moderate concentration, with the top five players (ASSA ABLOY, Allegion plc, dormakaba Group, SALTO WECOSYSTEM, and Fortune Brands Innovations) holding approximately 50–55% of market revenue in 2025. ASSA ABLOY's dominant position reflects decades of access control industry consolidation through strategic acquisitions, giving it the broadest product portfolio from consumer residential smart deadbolts to enterprise-grade biometric commercial access systems.

The introduction of the Matter smart home standard is progressively commoditizing basic wireless connectivity features, shifting competitive differentiation toward AI-powered security intelligence, cloud-based access management platform capabilities, cybersecurity certification depth, and the quality of mobile and smart home ecosystem integration.

Investment & Growth Opportunities

Fastest Growing Segments

Wi-Fi communication protocol (~15.5% CAGR), Deadbolts (~15.0% CAGR), and the Asia Pacific region (~18.0% CAGR) represent the highest-growth investment vectors through 2034. The commercial end-user segment is growing at approximately 16.0% CAGR, driven by property management technology investment, smart building mandates, and short-term rental market keyless entry adoption.

Smart Building and Commercial Real Estate Expansion

The global smart building market, projected to exceed USD 570 Billion by 2030, represents the smart lock industry's most significant enterprise opportunity. Property technology (PropTech) investment in access control modernization across commercial office, multi-family residential, healthcare, and student housing verticals is systematically upgrading traditional mechanical lock infrastructure with cloud-based smart access control systems.

Investment and Venture Trends

- Venture capital investment in smart home security startups exceeded USD 2 Billion globally in 2024, with smart lock and access control representing a significant sub-category. AI-powered access control platforms, biometric authentication technology companies, and cloud-based property access management startups are attracting significant Series B and C funding rounds.

- Matter ecosystem certification investment by all major smart lock manufacturers represents a structural market catalyst: as Matter adoption expands the compatible smart home device base to hundreds of millions of households globally, smart lock manufacturers will benefit from a significantly enlarged addressable upgrade market for interoperable smart security products.

Future Market Outlook (2026-2034)

The global smart lock market is positioned for sustained, high-growth expansion through 2034. From USD 3.10 Billion in 2025, the market is projected to reach USD 10.63 Billion by 2034 at a CAGR of 14.65%. This trajectory reflects a market in the middle of its S-curve adoption growth phase, with mainstream consumer adoption accelerating as smart lock price points decline, smart home platform compatibility becomes universal through Matter, and commercial building automation investment creates systematic institutional demand.

The 2026–2034 period will be defined by three structural shifts: the transition of smart locks from standalone devices to integrated AI-powered security intelligence nodes; the expansion of biometric multi-factor authentication from premium to mid-market price segments; and the geographic diversification of demand growth from North American and European early-adopter markets toward high-velocity Asia Pacific, Middle Eastern, and Latin American markets.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 95 industry participants in 2024–2025, including smart lock manufacturers, access control system integrators, residential and commercial property managers, smart home platform developers, IoT chipset suppliers, cybersecurity specialists, and investment analysts covering connected security technology equities across North America, Europe, and Asia Pacific.

Secondary Research

Secondary research encompassed ASSA ABLOY, Allegion plc, and dormakaba Group annual reports; Z-Wave Alliance and Connectivity Standards Alliance (Matter) industry data; NIST smart home cybersecurity guidelines; IHS Markit access control market database; and industry publications including Security Products magazine, Security Info Watch, and Parks Associates smart home consumer research.

Forecasting Models

Market size estimations used top-down and bottom-up modelling incorporating global residential and commercial door hardware installation base data, smart lock penetration rate projections by region, average selling price trajectory analysis, and end-user segment growth rate differentials. A base-case CAGR of 14.65% reflects consensus smart security market growth estimates validated against manufacturer revenue guidance and smart home market research forecasts for 2026–2034.

Smart Lock Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Lock Types Covered | Deadbolts, Lever Handles, Padlocks, Others |

| Communication Protocols Covered | Bluetooth, Wi-Fi, Others |

| End-Users Covered | Commercial, Residential, Institution and Government, Industrial |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | ASSA ABLOY, Allegion plc, dormakaba Group, SALTO WECOSYSTEM, Fortune Brands Innovations, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the smart lock market from 2020-2034.

- The smart lock market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the smart lock industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Smart Lock Market Report

The global smart lock market reached USD 3.10 Billion in 2025 and is projected to reach USD 10.63 Billion by 2034.

The market is expected to grow at a CAGR of 14.65% during 2026-2034, driven by smart home adoption, IoT connectivity expansion, contactless access demand, and commercial building automation investment.

Deadbolts lead with a 72.6% share in 2025, reflecting their role as the primary smart lock form factor for residential front door security and direct compatibility with standard door hardware installations.

Bluetooth leads with a 60.3% share in 2025, driven by energy efficiency enabling multi-year battery life, direct smartphone pairing, and strong consumer privacy credentials in the residential market.

North America leads with a 40.9% share in 2025, anchored by the United States' high smart home adoption rate, mature retail distribution, and strong demand from short-term rental platforms including Airbnb.

Key players include ASSA ABLOY, Allegion plc, dormakaba Group, SALTO WECOSYSTEM, and Fortune Brands Innovations.

Wi-Fi is the fastest-growing protocol at approximately 15.5% CAGR, driven by demand for remote access management without proximity requirement, making it ideal for property managers, short-term rental operators, and commercial deployments requiring always-connected cloud access control.

Key challenges include cybersecurity vulnerabilities in wireless protocols, high upfront costs for commercial deployments, battery life and power reliability concerns, interoperability fragmentation between smart home platforms, and consumer resistance to replacing familiar mechanical locks.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)