Smart Water Meter Market Report by Product (Electromagnetic Meter, Ultrasonic Meter, Electromechanical Meter, and Others), Meter Type (Smart Hot-Water Meter, Smart Cold-Water Meter), Configuration Type (Automated Meter Reading (AMR), Advanced Metering Infrastructure (AMI)), Component (Meters & Accessories, IT Solutions, Communication System), Application (Water Utilities, Commercial, Industrial, Residential), and Region 2026-2034

Smart Water Meter Market Size:

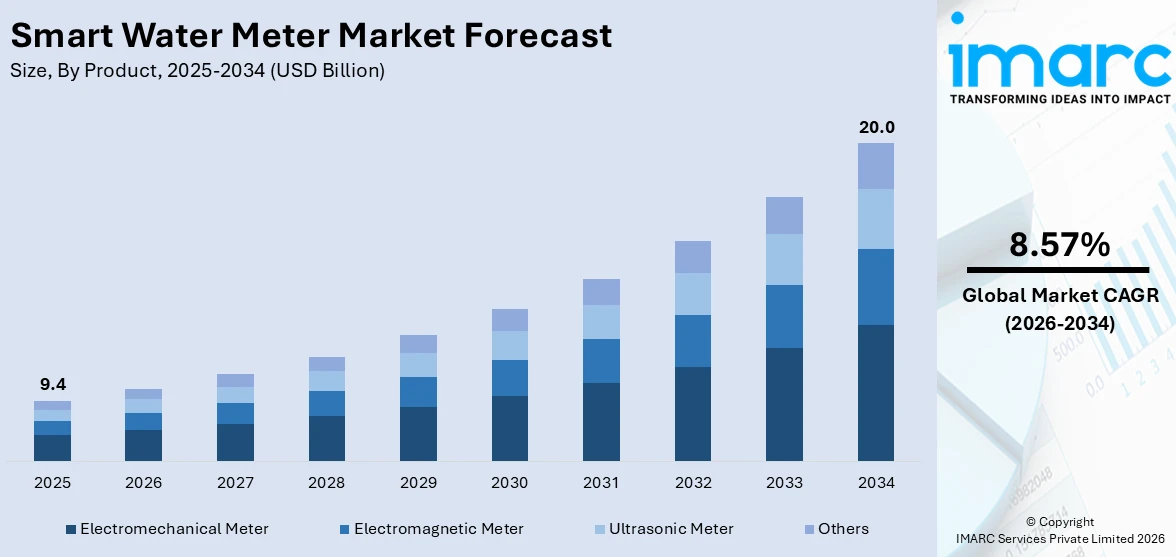

The global smart water meter market size reached USD 9.4 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 20.0 Billion by 2034, exhibiting a growth rate (CAGR) of 8.57% during 2026-2034. The market is experiencing steady growth driven by the growing concerns about water scarcity due to population growth, urbanization, and climate change, regulatory mandates and government policies to promote water conservation, and rising need for efficient water management.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 9.4 Billion |

| Market Forecast in 2034 | USD 20.0 Billion |

| Market Growth Rate 2026-2034 |

8.57%

|

Smart Water Meter Market Analysis:

- Market Growth and Size: The market is witnessing strong growth, driven by the increasing awareness about water conservation, along with the need for efficient water management solutions.

- Technological Advancements: Technological innovations in smart water meters are leading to its increasing adoption. These meters incorporate Internet of Things (IoT) and wireless communication technologies, enabling real-time data collection and remote monitoring.

- Industry Applications: Smart water meters find applications in various sectors, including residential, commercial, and industrial. They are crucial in monitoring water usage across these segments, ensuring efficient resource allocation.

- Geographical Trends: North America leads the market, driven by the aging water infrastructure. However, Asia Pacific is emerging as a fast-growing market, driven by the increasing demand for efficient water management.

- Competitive Landscape: Key players in the market are actively investing in research and development (R&D) activities to enhance their product offerings. They are focusing on developing advanced metering technologies that provide higher accuracy, greater reliability, and improved data communication capabilities.

- Challenges and Opportunities: While the market faces challenges, such as high initial costs and the need for retrofitting existing infrastructure, it also encounters opportunities in offering cost-effective solutions, addressing water conservation goals, and expanding market reach.

- Future Outlook: The future of the smart water meter market looks promising, with sustained growth anticipated. As environmental concerns are increasing, smart water meters will continue to play a pivotal role in efficient water management and conservation efforts globally.

To get more information on this market Request Sample

Smart Water Meter Market Trends:

Growing water scarcity concerns

Water scarcity is a pressing global issue due to population growth, urbanization, and climate change. This concern is a significant driver for the smart water meter market. Smart water meters provide a solution to efficiently manage and conserve water resources. By offering real-time data on water consumption and leak detection, they empower utilities and consumers to take proactive measures to reduce water wastage. Governments and regulatory bodies worldwide are increasingly advocating for the adoption of smart water meters to address water scarcity challenges. This, in turn, is propelling the growth of the market, especially in regions prone to water shortages, as it aligns with sustainability goals and promotes responsible water management practices. As water scarcity is increasing, the demand for smart water meters is rising, making them a vital tool in ensuring sustainable water usage.

Regulatory mandates for water conservation

Regulatory mandates and government policies aimed at promoting water conservation play a crucial role in driving the smart water meter market. Many countries and regions are implementing strict regulations to monitor and reduce water consumption, especially in urban areas facing water stress. Smart water meters enable compliance with these regulations by providing accurate and timely data on water usage. They also facilitate fair billing practices, as consumers are billed based on their actual consumption, discouraging wasteful usage. In response to these regulatory pressures, utilities and municipalities are increasingly adopting smart water metering solutions to ensure compliance, avoid penalties, and demonstrate their commitment to sustainable water management. In addition, the need for regulatory compliance and the drive toward responsible water usage is impelling the growth of the market.

Efficient water management for utilities

The need for efficient water management is catalyzing the demand for smart water meters, particularly for water utilities and municipalities. Smart water meters offer utilities a powerful tool to optimize their operations and resources. These meters provide real-time data on water consumption, enabling utilities to detect leaks, identify unusual usage patterns, and plan maintenance more effectively. This leads to reduced water losses, lower operational costs, and improved service reliability. Additionally, the data collected by smart water meters can be used for demand forecasting, infrastructure planning, and informed decision-making. As utilities are striving to provide reliable water services while minimizing waste and operational expenses, the adoption of smart water meters is becoming increasingly appealing. Thus, the pursuit of efficient water management is bolstering the growth of the market.

Environmental sustainability initiatives

Environmental sustainability initiatives, both from public and private sectors, are driving the adoption of smart water meters. As people are becoming more conscious of environmental issues, there is a growing emphasis on reducing water wastage and conserving this precious resource. Smart water meters play a pivotal role in achieving these sustainability goals. They enable consumers to monitor their water usage in real-time, promoting conscious consumption and reducing water wastage. Additionally, by swiftly detecting leaks and irregularities, smart water meters prevent water loss, which aligns with sustainability objectives.

Smart Water Meter Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on product, meter type, configuration type, component, and application.

Breakup by Product:

- Electromagnetic Meter

- Ultrasonic Meter

- Electromechanical Meter

- Others

Electromechanical meter accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the product. This includes electromagnetic meter, ultrasonic meter, electromechanical meter, and others. According to the report, electromechanical meter represented the largest segment as these traditional meters are evolving to incorporate smart features, such as automated data collection and remote monitoring. They use mechanical components to measure water flow, making them robust and reliable. Their widespread use in existing infrastructure and their gradual transition to smart technology contribute to their dominance in the market. They are often preferred for retrofitting older water meter systems, ensuring compatibility and ease of integration with legacy systems.

Electromagnetic meters are a significant segment in the smart water meter market. These meters utilize the principles of electromagnetic induction to measure water flow accurately. They are known for their durability and reliability in various operating conditions. Electromagnetic meters are often preferred for industrial and commercial applications where precise measurement and longevity are crucial.

Ultrasonic meters are gaining traction in the smart water meter market due to their non-intrusive and highly accurate measurement capabilities. These meters use ultrasonic sound waves to determine water flow rates. They are known for their versatility, as they can be used for both residential and commercial purposes.

Breakup by Meter Type:

- Smart Hot-Water Meter

- Smart Cold-Water Meter

Smart cold-water meter holds the largest share in the industry

A detailed breakup and analysis of the market based on the meter type have also been provided in the report. This includes smart hot-water meter and smart cold-water meter. According to the report, smart cold-water meter accounted for the largest market share.

Smart cold-water meters are widely used to measure the consumption of cold water in residential, commercial, and industrial settings. They form the backbone of water management systems, enabling accurate billing, leak detection, and water conservation. They are known for their versatility and ability to integrate seamlessly into existing water infrastructure. Their widespread adoption is driven by the need for efficient water resource management, compliance with regulations, and the desire to reduce water wastage.

Smart hot-water meters are a crucial segment in the smart water meter market. These meters are designed specifically to measure the consumption of hot water in residential and commercial settings. They play a vital role in tracking and managing energy consumption for heating purposes. Smart hot-water meters provide real-time data on hot water usage, helping consumers make informed decisions about energy conservation and efficiency.

Breakup by Configuration Type:

- Automated Meter Reading (AMR)

- Advanced Metering Infrastructure (AMI)

Automated meter reading (AMR) represents the leading market segment

The report has provided a detailed breakup and analysis of the market based on the configuration type. This includes automated meter reading (AMR) and advanced metering infrastructure (AMI). According to the report, automated meter reading (AMR) represented the largest segment.

AMR systems enable the collection of consumption data from smart water meters at regular intervals without the need for real-time communication. This data is typically retrieved periodically by meter readers using specialized equipment. AMR systems are valued for their cost-effectiveness and reliability, making them a preferred choice for utilities, especially in areas with stable and well-established meter-reading processes. They provide the benefits of improved billing accuracy and reduced manual reading efforts.

AMI systems enable real-time, two-way communication between smart meters and utilities. They provide a continuous flow of data, allowing utilities to monitor water consumption, detect leaks, and respond to issues promptly. AMI systems offer a higher level of data granularity and enable remote control of meters. While AMI systems offer advanced features and greater control, they typically involve a higher initial investment.

Breakup by Component:

- Meters & Accessories

- IT Solutions

- Communication System

Meters and accessories represent the leading market segment

The report has provided a detailed breakup and analysis of the market based on the component. This includes meters and accessories, IT solutions, and communication system. According to the report, meters and accessories represented the largest segment.

The meters and accessories segment encompasses the physical smart water meters themselves, as well as the associated accessories, such as installation kits, data loggers, and sensors. This segment is critical as it constitutes the core hardware responsible for accurately measuring water consumption. The reliability, accuracy, and durability of these meters are paramount for utilities and consumers. As smart water meter adoption is growing, the demand for high-quality meters and accessories is rising, making this segment a key driver in the market.

IT solutions play a vital role in the smart water meter market, offering software and data management tools that enable utilities to collect, process, and analyze the data generated by smart meters. These solutions often include data analytics, billing and invoicing software, and customer engagement platforms.

The communication system segment encompasses the infrastructure and technologies that enable smart meters to transmit data to utilities and other stakeholders. This includes various communication protocols, networks, and data concentrators.

Breakup by Application:

Access the comprehensive market breakdown Request Sample

- Water Utilities

- Commercial

- Industrial

- Residential

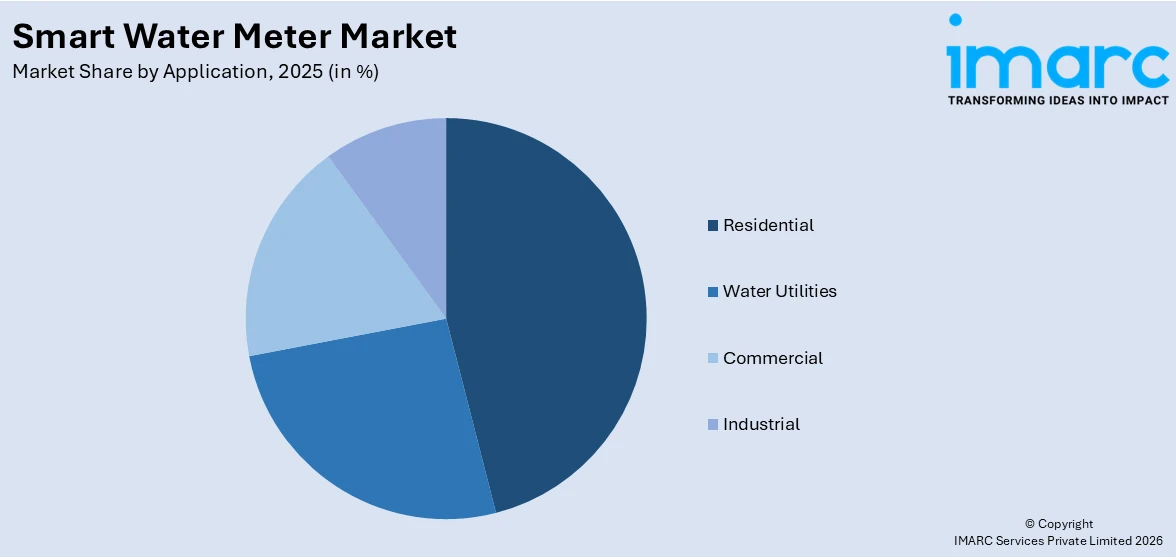

Residential represents the leading market segment

The report has provided a detailed breakup and analysis of the market based on the application. This includes water utilities, commercial, industrial, and residential. According to the report, residential represented the largest segment.

Smart water meters in residential settings allow homeowners and property managers to monitor their water consumption, detect leaks, and optimize water usage. They are instrumental in promoting water conservation, reducing water bills, and ensuring accurate billing. The ease of installation and user-friendly interfaces make smart water meters accessible to a wide range of residential consumers, contributing to their dominance in this segment.

The commercial sector represents a substantial portion of the smart water meter market. Businesses and commercial properties require accurate measurement of water consumption for billing, operational efficiency, and sustainability efforts. Smart water meters in commercial applications provide real-time data, allowing businesses to track water usage patterns and identify opportunities for efficiency improvements.

The industrial sector utilizes smart water meters for monitoring large-scale water consumption in manufacturing processes, cooling systems, and other industrial applications. These meters play a critical role in optimizing water usage, reducing waste, and ensuring compliance with environmental regulations. The industrial segment benefits from the precision and data capabilities offered by smart water meters to enhance resource management and operational efficiency.

Water utilities are another key segment in the smart water meter market. Smart water meters enable utilities to efficiently manage their water distribution networks, detect leaks, and reduce non-revenue water losses. They also facilitate remote meter reading, which streamlines billing processes and reduces operational costs. Water utilities rely on these meters to improve overall system performance and provide better services to their customers.

Breakup by Region:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America leads the market, accounting for the largest smart water meter market share

The market research report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, North America accounted for the largest market share.

North America comprises the United States and Canada, is witnessing significant adoption of smart water meters due to the aging water infrastructure, a growing focus on water conservation, and the need for accurate billing. Regulatory pressures and initiatives to modernize water management are driving the adoption of smart water metering solutions.

The Asia Pacific region is experiencing rapid growth in the smart water meter market. Factors, such as urbanization, population growth, and the increasing demand for efficient water management are driving the adoption of smart water meters in countries like China, India, and Japan.

Europe is a significant segment in the smart water meter market, known for its focus on environmental sustainability and water conservation. European countries have been proactive in adopting smart water meters to promote responsible water usage, reduce water wastage, and achieve regulatory compliance.

Latin America is witnessing steady growth in the adoption of smart water meters. The region faces water supply challenges, making efficient water management crucial. Countries like Brazil and Mexico are investing in modernizing their water infrastructure, including the implementation of smart water meters.

The Middle East and Africa region are gradually embracing smart water meters to address water scarcity issues and improve water distribution efficiency. Countries like the United Arab Emirates, South Africa, and Saudi Arabia are investing in smart water metering solutions to optimize water usage and reduce non-revenue water losses.

Leading Key Players in the Smart Water Meter Industry:

Key players in the market are actively investing in research and development (R&D) activities to enhance their product offerings. They are focusing on developing advanced metering technologies that provide higher accuracy, greater reliability, and improved data communication capabilities. Additionally, these companies are working on user-friendly interfaces and data analytics tools to empower consumers and utilities with valuable insights into water consumption patterns. Furthermore, there is a growing emphasis on ensuring the cybersecurity of smart water metering systems to protect against potential cyber threats. Companies are also expanding their global presence through strategic partnerships and acquisitions, aiming to tap into emerging markets where smart water meter adoption is on the rise. Overall, key players are committed to innovation, sustainability, and providing comprehensive solutions to address the evolving needs of the smart water meter market.

The market research report has provided a comprehensive analysis of the competitive landscape. Detailed profiles of all major companies have also been provided. Some of the key players in the market include:

- Arad Group

- Badger Meter

- Bmeters Srl

- Diehl Stiftung & Co. KG

- Honeywell International Inc.

- Itron Inc.

- Kamstrup

- Landis+Gyr

- Maddalena Spa

- Neptune Technology Group Inc.

- WAVIoT

- Xylem

- ZENNER International GmbH & Co. KG

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

Latest News:

- May 2, 2022: Badger Meter has announced that its ModMAG® M2000 Electromagnetic flow meter is available with BACnet MS/TP communication protocol. The M2000 meter has also completed rigorous testing for the BACnet Testing Laboratories (BTL) Certification Program, assuring seamless integration with building management systems (BMS). The M2000 meter is the first full-bore inline electromagnetic meter to achieve BTL Certification.

- December 1, 2021: Diehl Stiftung & Co. KG helped the Maltese utility Water Services Corporation (WSC) to reduce non-revenue water and overcome the challenges of low flow rates and high levels of limescale.

Smart Water Meter Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Products Covered | Electromagnetic Meter, Ultrasonic Meter, Electromechanical Meter, Others |

| Meter Types Covered | Smart Hot-Water Meter, Smart Cold-Water Meter |

| Configuration Types Covered | Automated Meter Reading (AMR), Advanced Metering Infrastructure (AMI) |

| Components Covered | Meters & Accessories, IT Solutions, Communication System |

| Applications Covered | Water Utilities, Commercial, Industrial, Residential |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Arad Group, Badger Meter, Bmeters Srl, Diehl Stiftung & Co. KG, Honeywell International Inc., Itron Inc., Kamstrup, Landis+Gyr, Maddalena Spa, Neptune Technology Group Inc., WAVIoT, Xylem, ZENNER International GmbH & Co. KG, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the smart water meter market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global smart water meter market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the smart water meter industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Smart Water Meter Market Report

The global smart water meter market was valued at USD 9.4 Billion in 2025.

We expect the global smart water meter market to exhibit a CAGR of 8.57% during 2026-2034.

The rising consumer awareness towards various associated benefits of smart water meters, such as reducing the overall labor cost, keeping track of the exact usage of water, offering a relatively more accurate billing with the ability to detect thefts, etc., is primarily driving the global smart water meter market.

The sudden outbreak of the COVID-19 pandemic had led to the implementation of stringent lockdown regulations across several nations, resulting in the temporary closure of numerous manufacturing units for smart water meters.

Based on the product, the global smart water meter market can be segmented into electromagnetic meter, ultrasonic meter, electromechanical meter, and others. Among these, electromechanical meter currently holds the majority of the total market share.

Based on the meter type, the global smart water meter market has been divided into smart hot-water meter and smart cold-water meter. Currently, smart cold-water meter exhibits a clear dominance in the market.

Based on the configuration type, the global smart water meter market can be categorized into Automated Meter Reading (AMR) and Advanced Metering Infrastructure (AMI), where Automated Meter Reading (AMR) currently accounts for the majority of the global market share.

Based on the component, the global smart water meter market has been segregated into meters & accessories, IT solutions, and communication system. Currently, meters & accessories hold the largest market share.

Based on the application, the global smart water meter market can be bifurcated into water utilities, commercial, industrial, and residential. Among these, the residential sector exhibits a clear dominance in the market.

On a regional level, the market has been classified into North America, Asia-Pacific, Europe, Latin America, and Middle East and Africa, where North America currently dominates the global market.

Some of the major players in the global smart water meter market include Arad Group, Badger Meter, Bmeters Srl, Diehl Stiftung & Co. KG, Honeywell International Inc., Itron Inc., Kamstrup, Landis+Gyr, Maddalena Spa, Neptune Technology Group Inc., WAVIoT, Xylem, ZENNER International GmbH & Co. KG, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)