Soda Ash Market Size, Share, Trends and Forecast by Application and Region, 2026-2034

Global Soda Ash Market Size, Share, Trends & Forecast (2026-2034)

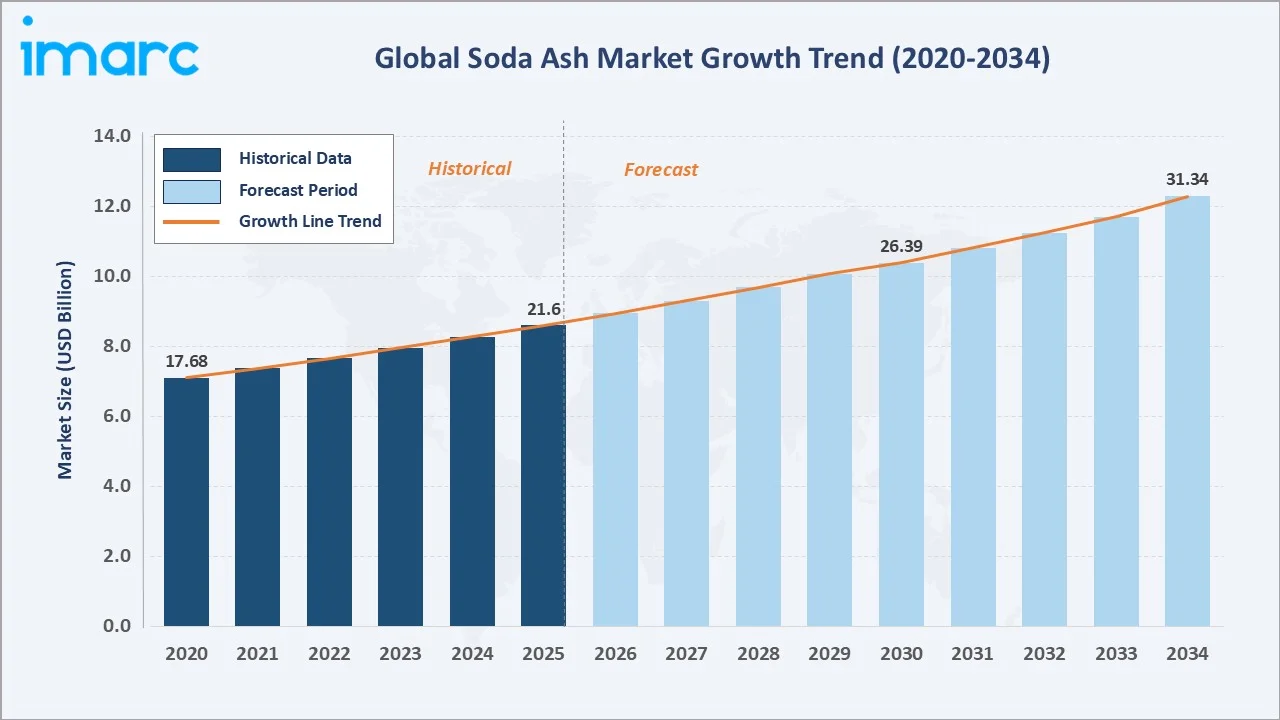

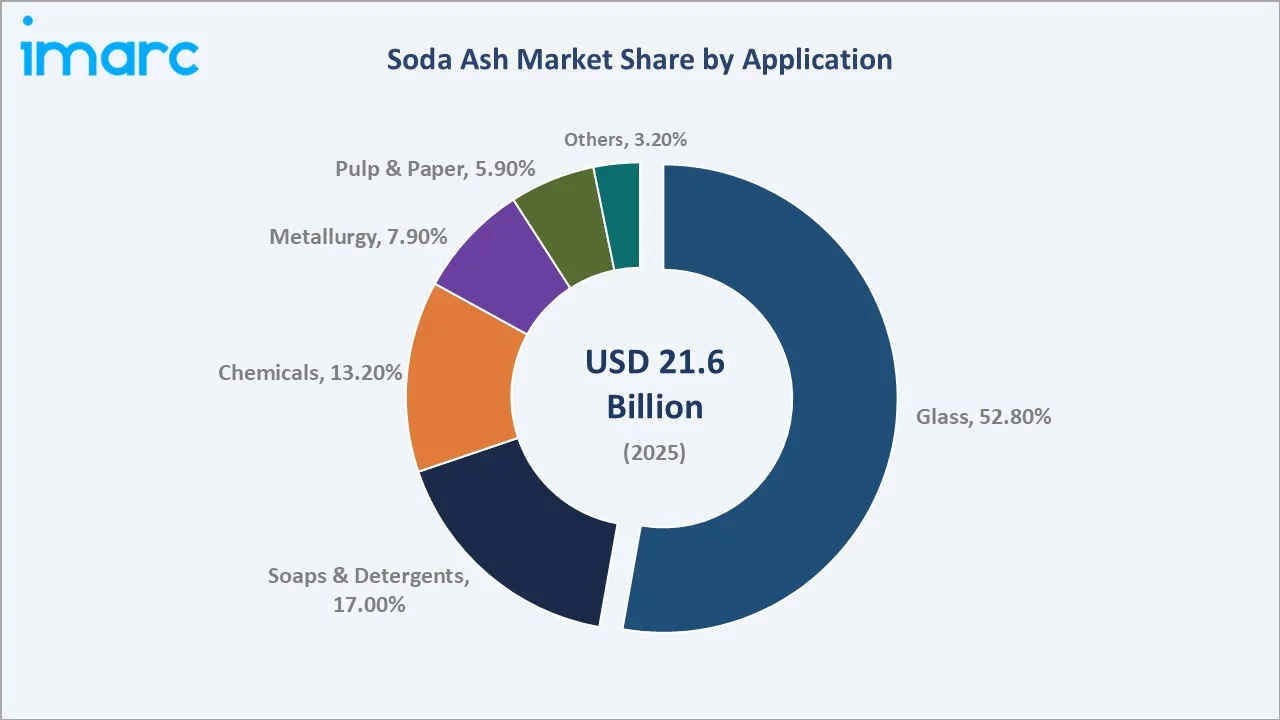

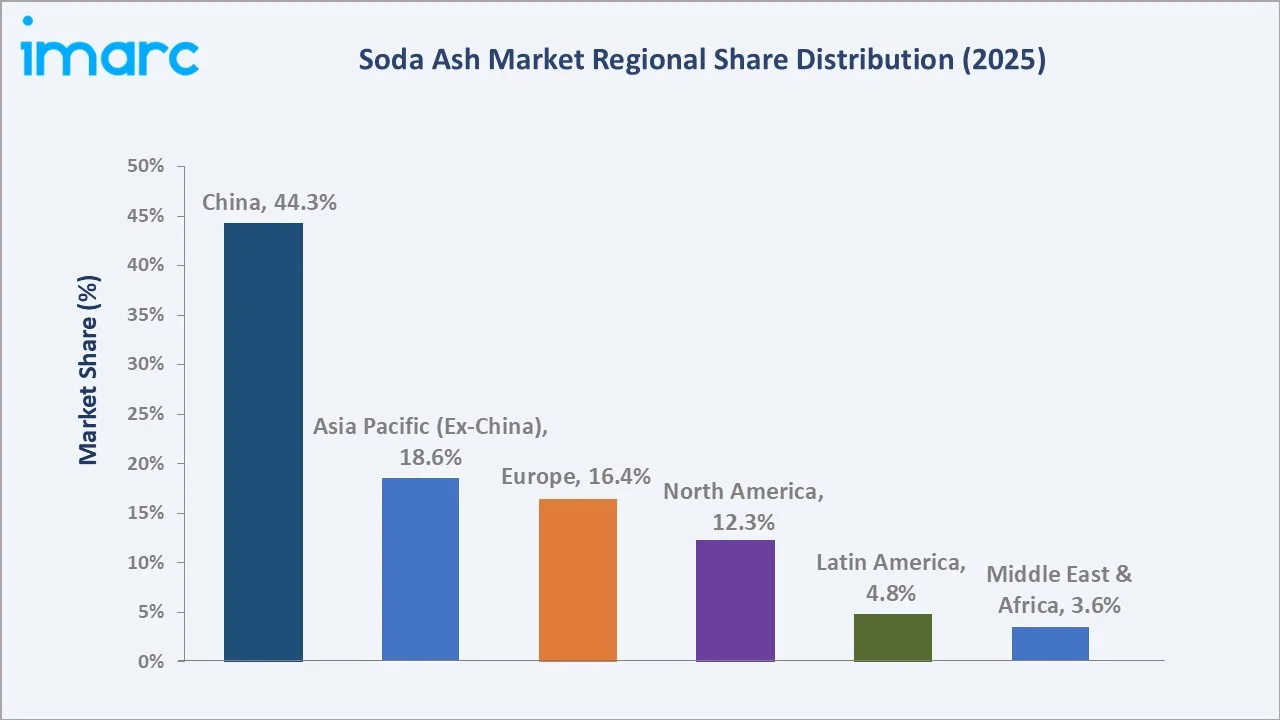

The global soda ash market reached a value of USD 21.6 Billion in 2025 and is projected to reach USD 31.3 Billion by 2034, exhibiting a CAGR of 4.09% during the forecast period (2026-2034). Market growth is primarily driven by escalating utilization in glass manufacturing for construction and automotive sectors, rising wastewater treatment applications, expanding chemical processing demand, and the emerging link to lithium carbonate production for EV battery supply chains. China dominates the global market with a 44.3% share in 2025, backed by the world's largest Solvay process and Hou process manufacturing capacity. Glass manufacturing leads application demand at 52.8% (2025), followed by soaps and detergents (17.0%) and chemicals (13.2%). The market is forecast to reach USD 26.4 Billion by 2030.

Market Snapshot

|

Metric |

Value |

|

Market Size (2020) |

USD 17.7 Billion |

|

Market Size (2025) |

USD 21.6 Billion |

|

Market Size (2030) |

USD 26.4 Billion |

|

Forecast Market Size (2034) |

USD 31.3 Billion |

|

CAGR (2026-2034) |

4.09% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Region |

China (44.3%, 2025) |

|

Second-Largest Region |

Asia Pacific Ex-China (18.6%, 2025) |

|

Leading Application |

Glass Manufacturing (52.8%, 2025) |

|

Second Application |

Soaps & Detergents (17.0%, 2025) |

From USD 17.7 Billion in 2020 to USD 21.6 Billion in 2025, the soda ash market delivered a 22% historical value increase, demonstrating robust demand resilience across construction, chemical, and consumer goods end-markets. The forecast addition of USD 9.7 Billion through 2034 reflects the structural importance of soda ash across multiple industrial verticals.

To get more information on this market, Request Sample

The 4.09% CAGR through 2034 reflects a market in steady structural expansion, with above-average growth in solar glass and EV battery-linked lithium carbonate applications accelerating from 2026 onward.

Executive Summary

The global soda ash (sodium carbonate, Na2CO3) market reached USD 21.6 Billion in 2025, sustained by its irreplaceable role as a primary raw material in glass manufacturing, detergents, chemical processing, metallurgy, and pulp and paper production. The market is forecast to reach USD 31.3 Billion by 2034 at a CAGR of 4.09%, crossing USD 26.4 Billion by 2030. China's 44.3% market dominance (2025) reflects its world-leading soda ash production capacity, concentrated particularly in Shandong,

Glass manufacturing’s 52.8% application dominance (2025) is underpinned by rising urbanization-driven construction activity, automotive glass demand, and crucially, the rapid scale-up of solar photovoltaic (PV) panel production requiring ultra-clear flat glass. Europe (16.4%), North America (12.3%), Latin America (4.8%), and the Middle East and Africa (3.6%) complete the regional picture.

Key Market Insights

|

Insight |

Data |

|

Dominant Application |

Glass Manufacturing – 52.8% (2025) |

|

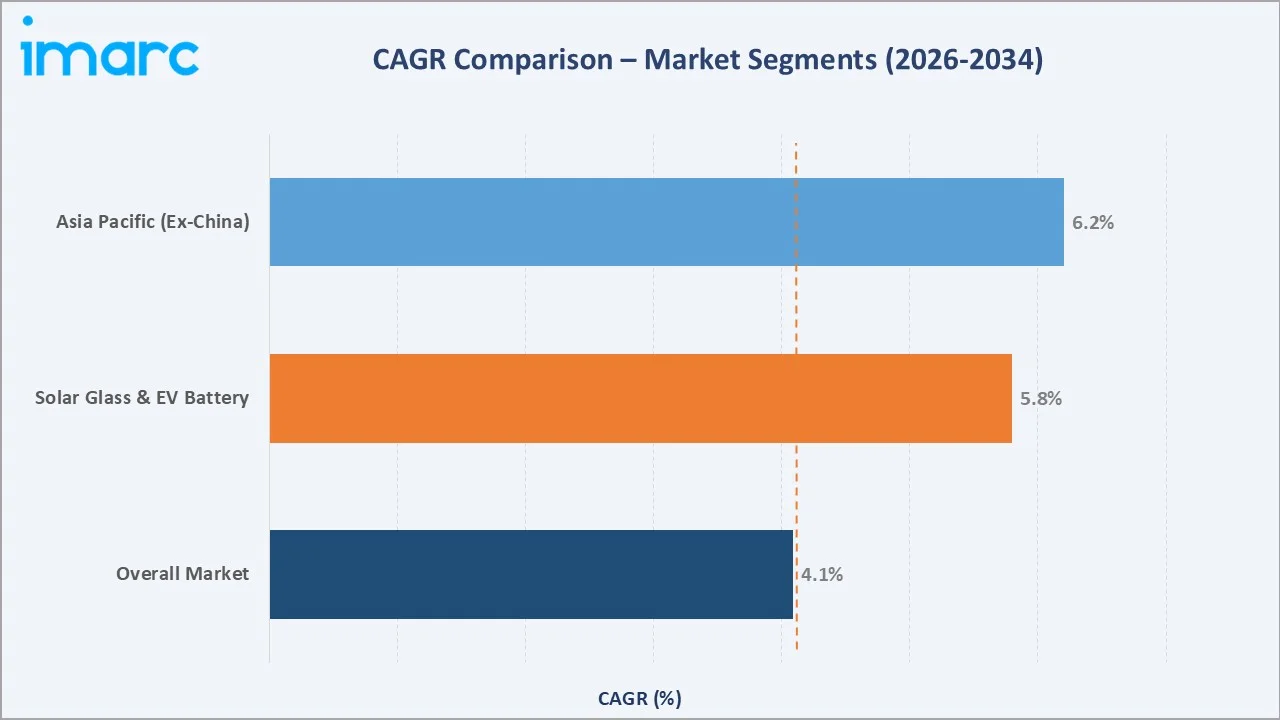

Fastest Growing Application |

Solar Glass & EV Battery (Li-Carbonate) – ~5.8% CAGR |

|

Dominant Region |

China – 44.3% (2025) |

|

Second-Largest Region |

Asia Pacific (Ex-China) – 18.6% (2025) |

|

Leading Production Method |

Solvay Process (synthetic) – ~42% of global capacity |

|

Major Capacity Expansion |

PT Pupuk Indonesia – 300,000 tons/year (announced March 2024) |

|

Top Companies |

Solvay, Ciner, Tata Chemicals, GHCL |

Key analytical observations supporting the above data:

- Glass manufacturing’s 52.8% share (2025) encompasses flat glass for construction and automotive (the largest sub-segment), container glass for food and beverage packaging, specialty glass for solar panels, and fiberglass for composites and insulation, each representing distinct demand growth drivers.

- China's 44.3% dominance reflects its status as both the world's largest soda ash producer and consumer, with Chinese domestic capacity exceeding 35 million metric tons annually. China's glass, detergent, and chemical manufacturing industries are simultaneously the world's largest consumers of soda ash across all major application categories.

- Europe's 16.4% share is sustained by its significant flat glass, container glass, and specialty glass manufacturing base, with major soda ash producers including Solvay, and GHCL, supplying regional glass and chemical industries.

Global Market Overview

Soda ash (sodium carbonate, Na2CO3) is one of the world's most foundational industrial chemicals, used as a raw material, processing agent, and pH regulator across over a dozen major industry verticals. It is produced commercially through two primary routes: the synthetic Solvay process (using limestone and salt brine, accounting for approximately 70% of global capacity) and natural trona mining (primarily in Wyoming, USA, and sub-Saharan Africa). China additionally employs the Hou process, a modified Solvay variant, at significant scale. As of 2025, global soda ash market was valued at USD 21.6 Billion. The main source of natural soda ash is bedded trona brines, which are mined for roughly 47 billion tonnes worldwide. The chemical's unique alkaline buffering properties, glass-forming chemistry, and affordability make it irreplaceable in glass manufacturing, detergent formulation, chemical synthesis, water treatment, pulp delignification, and metallurgical flux applications. Infrastructure investments, urbanization, solar energy expansion, and EV battery supply chain development are collectively creating structural demand tailwinds that underpin the market's projected 4.09% CAGR through 2034.

Market Dynamics

To evaluate market opportunities, Request Sample

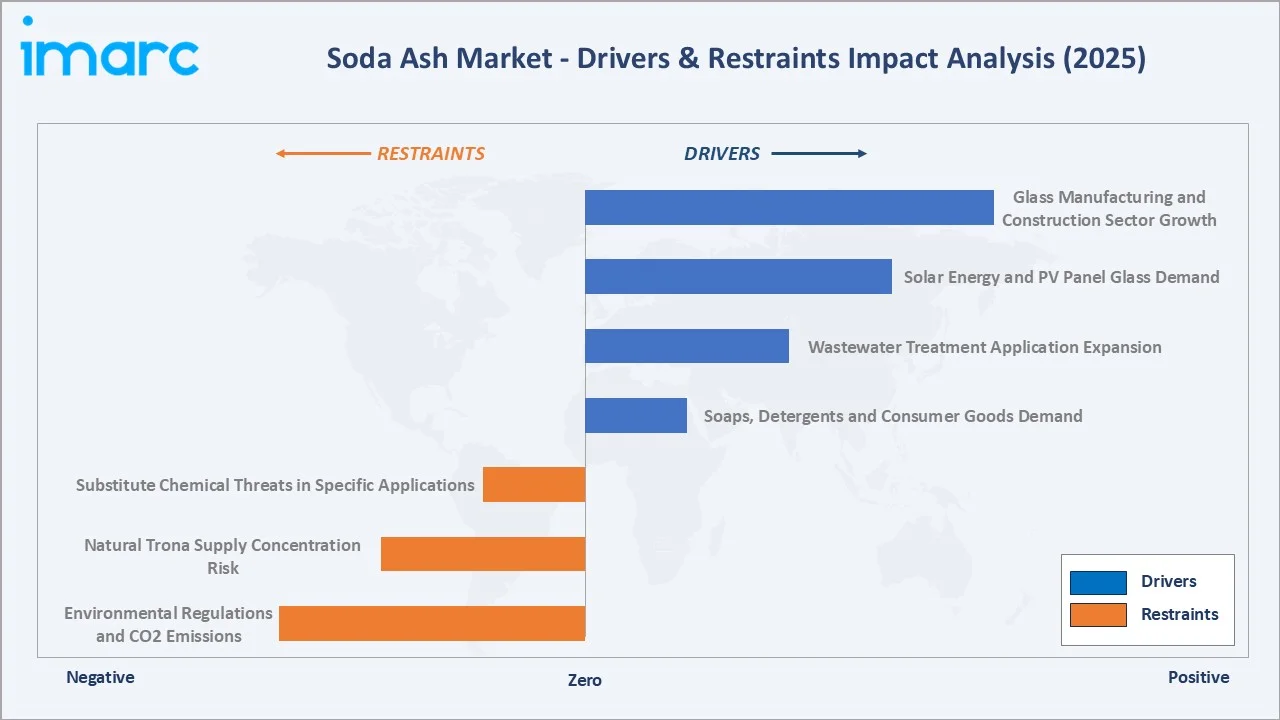

Market Drivers

- Glass Manufacturing and Construction Sector Growth: Soda ash is an irreplaceable flux in glass manufacturing, lowering the melting point of silica and enabling efficient glass formation. Global construction output reached approximately USD 13 Trillion in 2023 (7% of global GDP), driving sustained demand for flat glass in facades, windows, and interior applications.

- Solar Energy and PV Panel Glass Demand: The global solar photovoltaic industry is creating significant new demand for ultra-clear, iron-reduced flat glass, a high-soda-ash-intensity product. Solar PV installations grew at over 37% annually in 2023–2024, with global cumulative installed capacity exceeding 2,000 GW.

- Wastewater Treatment Application Expansion: Soda ash's ability to regulate pH levels and precipitate heavy metals makes it a key chemical in municipal and industrial wastewater treatment. The approximately 113 billion m³ of untreated wastewater globally released in 2022 reflects a massive unmet treatment infrastructure gap, and government regulatory pressure is driving investment in new treatment facilities across Asia, Africa, and Latin America.

- Soaps, Detergents and Consumer Goods Demand: Soda ash is a key alkaline builder in laundry detergent formulations, maintaining washing solution pH and enhancing cleaning agent effectiveness. Unilever's April 2024 launch of Wonder Wash, designed for 15-minute wash cycles meeting growing consumer preference for short wash settings, exemplifies continued product innovation that sustains soda ash consumption in the detergent supply chain.

Market Restraints

- Environmental Regulations and CO2 Emissions: The Solvay process for soda ash production is energy-intensive and generates significant CO2 emissions, approximately 0.4–0.5 metric tons of CO2 per metric ton of soda ash produced. Increasing carbon pricing and emissions regulations in the EU and increasingly in Asia are creating cost headwinds for synthetic soda ash producers and incentivizing investment in process decarbonization, which requires significant capital expenditure.

- Natural Trona Supply Concentration Risk: The most cost-effective and environmentally favorable soda ash production method, natural trona mining is geographically concentrated, primarily in Wyoming, USA, and the Lagash Lake region of sub-Saharan Africa.

- Substitute Chemical Threats in Specific Applications: In some applications, soda ash faces competition from substitute chemicals. Caustic soda (sodium hydroxide) can replace soda ash in certain pH adjustment and chemical synthesis applications. In detergents, zeolites and polycarboxylates are increasingly used as soda ash substitutes in premium formulations targeting environmentally sensitive markets.

Market Opportunities

- Emerging Economy Import Substitution Capacity: Nations with significant soda ash import dependency, including Indonesia (nearly 1 million tons/year fully imported), India, and various African countries represent major investment opportunities for domestic production capacity development. PT Pupuk Indonesia's announced 300,000 ton/year capacity in East Java and East Kalimantan (March 2024) exemplifies the import substitution trend that will create substantial new regional capacity through 2034.

- Green and Low-Carbon Soda Ash Production: Carbon capture and utilization (CCU) integration into Solvay process plants, solar-powered process energy, and electrolytic production methods are emerging as differentiated, premium-priced product opportunities. European and North American industrial buyers under scope 3 emissions reporting obligations are willing to pay premiums for certified low-carbon soda ash.

- Specialty and High-Purity Soda Ash for Advanced Applications: High-purity soda ash grades for pharmaceutical applications, food additive uses (E500 designation), and specialty glass manufacturing for electronics and optical applications command significant price premiums over standard commodity grades.

Market Challenges

- Energy Cost Exposure: Soda ash production is highly energy-intensive, with energy accounting for 25–40% of total production cost. Volatility in natural gas, coal, and electricity prices, the primary energy inputs for Solvay process production, creates significant margin uncertainty for producers without long-term energy supply contracts or captive energy generation.

- Transportation and Logistics Cost Structure: Soda ash is a bulk commodity with relatively low value-to-weight ratio, making transportation costs a significant component of delivered price, particularly for landlocked or import-dependent markets. Ocean freight rate volatility creates procurement cost uncertainty for import-dependent consumers in Asia, Africa, and Latin America.

- Quality Consistency Requirements for Glass Industry: The flat glass industry, the largest soda ash consumer, requires highly consistent chemical purity and particle size distribution to ensure furnace performance and glass quality. Producers supplying the premium flat glass sector must maintain strict quality management systems and traceability documentation, creating barriers for new market entrants.

Emerging Market Trends

The global soda ash market is being reshaped by five converging trends spanning energy transition demand creation, environmental compliance requirements, capacity expansion in import-dependent emerging markets, and digital manufacturing efficiency improvements through 2034.

1. Solar Energy Glass Demand as a Structural Growth Catalyst

The global solar energy buildout is creating a powerful and growing new demand vector for soda ash through ultra-clear, low-iron flat glass production for photovoltaic panels. With solar PV installations growing at 35–45% annually, and each GW of solar capacity requiring significant amount of soda ash-derived flat glass as it comprises of nearly 70% of the PV, the solar energy transition is becoming one of the most significant new structural demand drivers for soda ash globally. This trend positions soda ash as an indirect but essential enabler of the global decarbonization agenda.

2. EV Battery Supply Chain Integration: Lithium Carbonate Link

The electrochemical conversion of lithium chloride (extracted from salt flats and brine deposits) to battery-grade lithium carbonate uses soda ash (sodium carbonate) as a key precipitation reagent. As global EV production scales toward 30 million vehicles annually by 2027, the lithium carbonate demand cascade creates a material, high-growth new consumption vector for soda ash that is largely independent of traditional glass and detergent market cycles.

3. Import Substitution Capacity Development in Asia and Africa

Historically import-dependent nations are accelerating domestic soda ash capacity development to reduce supply chain vulnerability and capture manufacturing value. Indonesia's PT Pupuk Indonesia announced 300,000 ton/year capacity across two facilities in 2024. India's GHCL, Tata Chemicals, and Nirma collectively represent a growing domestic production base serving India's significant soda ash deficit. Sub-Saharan Africa's trona deposits in Ethiopia and Kenya are attracting investment for natural soda ash production targeting regional demand growth.

4. Wastewater Treatment Infrastructure Expansion

The global water stress crisis and stricter municipal wastewater discharge regulations are driving significant investment in treatment facility construction, particularly across Asia Pacific, Africa, and Latin America. Soda ash is used for pH neutralization, heavy metal precipitation, and biological treatment support across municipal and industrial wastewater applications. The WHO/UN target of universal access to safely managed sanitation by 2030, while unlikely to be fully achieved is driving sustained public and private investment in treatment infrastructure that directly expands soda ash procurement volumes.

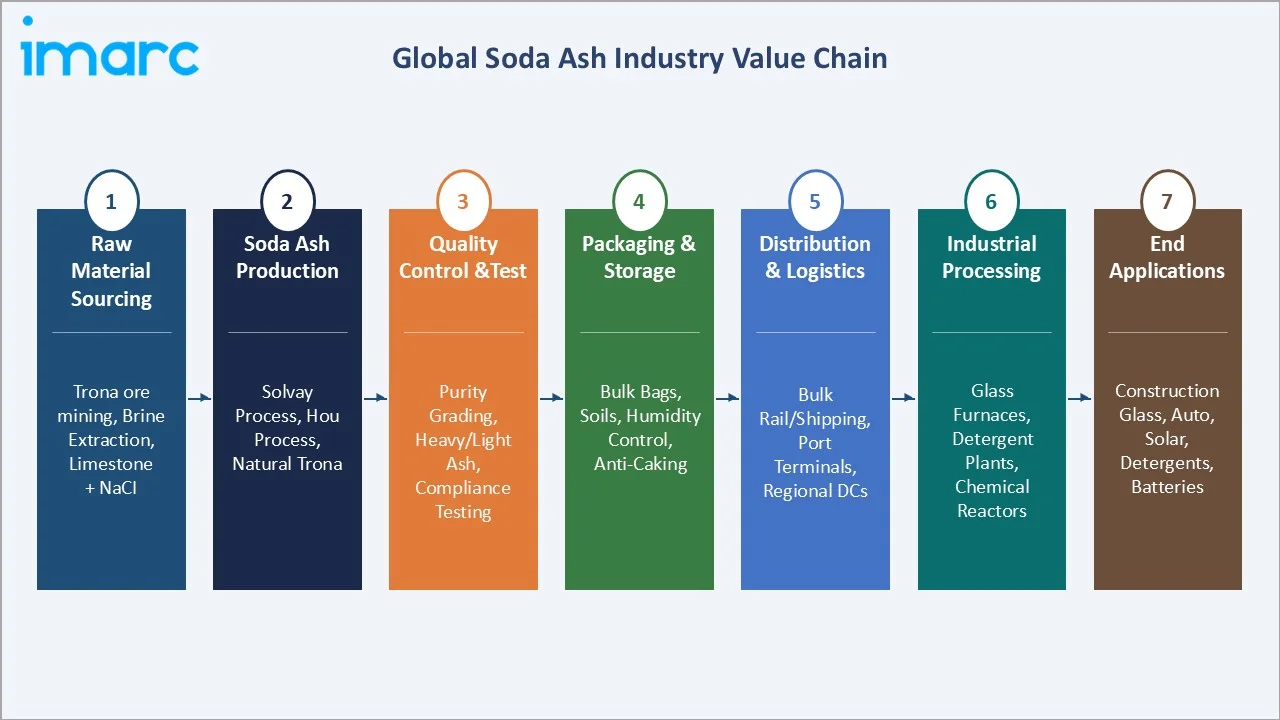

Industry Value Chain Analysis

The soda ash industry value chain spans seven interconnected stages from raw material extraction through to end-application processing. The relative efficiency, cost structure, and environmental footprint of each stage varies significantly depending on whether production is based on the synthetic Solvay process, the Hou process, or natural trona mining.

|

Stage |

Key Activities |

Representative Players |

|

Raw Material Sourcing |

Trona ore mining, salt and limestone quarrying, brine extraction from saline lakes |

Ciner (trona), natural brine processors in Chile/Bolivia |

|

Soda Ash Production |

Solvay process, Hou process, natural trona calcination, electrolytic methods |

Solvay S.A., GHCL, Tata Chemicals, Chinese producers |

|

Quality Control & Grading |

Purity testing (light/dense ash), particle size analysis, trace contaminant removal |

Third-party certification labs, producer in-house QC facilities |

|

Packaging & Storage |

Bulk silo storage, 1-ton big bags, anti-caking treatment, humidity-controlled warehousing |

Specialized bulk chemical packaging providers, producer logistics |

|

Distribution & Logistics |

Bulk rail and maritime shipping, port terminal handling, regional distribution centers |

Bulk chemical logistics companies, port operators, regional distributors |

|

Industrial Processing |

Integration into glass furnace batches, detergent manufacturing lines, chemical reactors |

Owens Corning (glass), Unilever (detergents), BASF (chemicals), water utilities |

|

End Applications |

Flat glass, container glass, solar glass, laundry detergents, lithium carbonate, water treatment |

Construction companies, automotive OEMs, solar developers, municipalities |

The production stage is the most capital-intensive and strategically significant in the soda ash value chain. A world-scale Solvay process soda ash plant requires investment of USD 300–500 Million and operates optimally at 500,000–1,000,000 metric tons per year capacity.

Technology Landscape in the Soda Ash Industry

Solvay Process – Dominant Synthetic Production

The Solvay ammonia-soda process remains the dominant global production technology, accounting for approximately 50% of global soda ash capacity. Developed in 1861, the process converts salt brine (NaCl) and limestone (CaCO3) into sodium carbonate using ammonia as a carrier, producing calcium chloride as a by-product. Modern Solvay plants achieve heat recovery efficiencies of 80–90% and incorporate continuous process monitoring and automation.

Hou Process – China's Modified Approach

The Hou Process, developed by Chinese chemist Hou Debang, combines ammonia-soda and ammonium-salt production in a more resource-efficient dual-product system. This process dominates Chinese synthetic soda ash production. Its advantage over the standard Solvay process is more complete utilization of salt and generation of ammonium chloride fertilizer as a co-product, improving overall process economics in regions with high agricultural fertilizer demand.

Natural Trona Mining – Cost-Competitive USA and Africa

Natural trona (Na3H(CO3)2·2H2O) mining and calcination is the most cost-effective and lowest-carbon-footprint production method, concentrated in Wyoming's Green River Basin (USA) and emerging operations in sub-Saharan Africa. The Green River Basin contains the world's largest known trona deposits, estimated at nearly 127 billion metric tons. Natural soda ash production avoids the energy-intensive chemical conversion steps of synthetic processes, resulting in approximately 40% lower CO2 emissions per ton and significantly lower production cost versus standard Solvay process plants.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Application |

Glass |

52.8% |

2025 |

|

Region |

China |

44.3% |

2025 |

By Application

The soda ash market is segmented across six primary application categories, each with distinct demand growth drivers, geographic concentration, and competitive dynamics:

To access detailed market analysis, Request Sample

Glass manufacturing’s 52.8% application dominance reflects soda ash's irreplaceable role as a flux that reduces silica's melting point from approximately 1,720°C to 1000°C, dramatically reducing the energy required for glass production. This fundamental chemistry ensures that soda ash cannot be substituted in glass manufacturing without fundamental reformulation of glass batch composition, providing structural demand security for the application segment.

Regional Market Insights

The global soda ash market is geographically concentrated to an exceptional degree, with China alone accounting for 44.3% of global market value in 2025. This concentration reflects China's simultaneous dominance in both soda ash production capacity and consumption across glass, detergent, and chemical applications.

|

Region |

Share (2025) |

Key Drivers |

Major Players |

| China | 44.3% | World's largest glass, detergent, and chemical producer; abundant salt/coal feedstock for Solvay/Hou process | Multiple large-scale Chinese SOE and private soda ash producers in Shandong, Sichuan, Qinghai |

| Asia Pacific (Ex-China) | 18.6% | India infrastructure growth, Indonesia import substitution, Southeast Asia consumer goods expansion | Tata Chemicals, GHCL, Nirma (India); emerging Indonesian capacity |

| Europe | 16.4% | Flat glass for construction, automotive specialty glass, REACH-compliant detergents | Solvay (Belgium), Sisecam (Turkey), BASF (Germany) |

| North America | 12.3% | Natural trona dominance, glass container demand, construction flat glass | Ciner (USA) |

| Latin America | 4.8% | Brazil construction boom, detergent industry, chemical processing growth | Imports dominant; emerging capacity from regional chemical investments |

|

Middle East & Africa |

3.6% | Natural trona potential (Kenya/Ethiopia), Qatar/UAE chemical industry, import-based consumption | Imports dominant; East Africa trona development projects in progress |

China's 44.3% market dominance (2025) creates both global market opportunity and supply concentration risk. Chinese soda ash exports influence global commodity prices significantly, when Chinese domestic demand contracts or production exceeds domestic consumption, Chinese export volumes increase and depress global market prices.

Competitive Landscape

The global soda ash market is moderately concentrated at the large-scale production tier, with the top five producers, Solvay S.A., Ciner Group, and Tata Chemicals, accounting for approximately 20–25% of global production capacity outside China. Within China, production is distributed across numerous large state-owned and private chemical companies, with no single entity commanding dominant market share.

| Company Name | HQ | Market Position | Primary Strategy |

|---|---|---|---|

| Solvay S.A. | Brussels, Belgium | Global Leader – Synthetic Production | Green soda ash (CarbonSafe), EU market dominance, premium specialty grades, decarbonization R&D |

| Tata Chemicals | Mumbai, India | Leader – Asia (India/UK/Kenya) | India, UK, Kenya production diversification, specialty grades, sustainability programs |

| Ciner Group | Istanbul, Turkey | Leader – Trona (Turkey/USA) | Turkish trona reserves exploitation, US operations via Ciner Wyoming, export focus |

| GHCL Limited | Ahmedabad, India | Established – India | India's largest synthetic soda ash, glass and detergent sector supply, cost optimization |

| Nirma Limited | Ahmedabad, India | Established – India | Vertically integrated detergent-to-soda ash, low-cost Indian market supply |

| Tokuyama Corporation | Yamaguchi, Japan | Challenger – Japan/Asia | High-purity specialty soda ash, pharmaceutical and electronics glass applications |

Solvay S.A. maintains global technological leadership through its proprietary Solvay process and ongoing investment in CarbonSafe CO2 capture, positioning it as the premium-grade and sustainability-credentialed supplier for European glass and chemical industry buyers operating under scope 3 emissions reporting requirements. U.S. natural trona producers (Ciner) compete primarily on production cost, leveraging the world's lowest-cost natural soda ash deposit to supply both domestic and export markets.

Key Company Profiles

Solvay S.A.

Solvay S.A. is the inventor of the commercial ammonia-soda process and the world's leading synthetic soda ash producer outside China, with production facilities in Belgium, Germany, France, Bulgaria, the USA, and Brazil. Annual soda ash revenues exceed USD 4.97 Billion.

- Product Portfolio: Dense and light soda ash grades, sodium bicarbonate, sodium silicate, premium specialty grades for electronics and pharmaceutical applications.

- Recent Developments: Advanced CarbonSafe CO2 capture and utilization program at European plants; issued green bond for soda ash decarbonization investment; expanded US soda ash capacity via Wyoming operations.

- Strategic Focus: Process decarbonization (CarbonSafe), green soda ash premium positioning, specialty grade expansion for electronics and pharmaceutical sectors, and European market supply security.

Ciner Group

Ciner Group is a leading global soda ash producer with significant natural trona operations in Turkey (one of the world's largest trona reserves outside the USA) and the United States (Ciner Wyoming). Combined capacity exceeds 2.5 million metric tons annually.

- Product Portfolio: Natural soda ash (dense and light), sodium bicarbonate, with Turkey operations serving European glass and detergent industries and US operations serving North American markets.

- Recent Developments: Continued capacity expansion at both Turkish and Wyoming operations; pursued European and Asian export growth strategies; advanced sustainability certification for low-carbon natural ash.

- Strategic Focus: Global trona-based production scale, export diversification, European market supply security, and cost-competitive positioning against Chinese synthetic producers.

Tata Chemicals Limited

Tata Chemicals is one of the world's most geographically diversified soda ash producers, operating Solvay process plants in India (Mithapur, Gujarat), the United Kingdom (Northwich, Cheshire), and Kenya (Magadi, natural trona).

- Product Portfolio: Dense and light soda ash, sodium bicarbonate, vacuum evaporated salt, food-grade sodium bicarbonate, and natural soda ash from Kenya's Magadi operations.

- Recent Developments: Advanced India capacity expansion to meet growing domestic glass and detergent demand; launched Tata Chemicals sustainability program targeting net-zero production by 2045.

- Strategic Focus: India and Asia Pacific market growth, production diversification across synthetic and natural methods, specialty grade development, and sustainability leadership in the Indian chemical industry.

GHCL Limited

GHCL Limited is India's largest soda ash manufacturer, operating a major Solvay process plant in Sutrapada, Gujarat, with annual capacity exceeding 1.2 million metric tons. GHCL is a primary supplier to India's glass, detergent, and chemical industries.

- Product Portfolio: Dense soda ash, light soda ash, vacuum salt, and chemical-grade sodium bicarbonate for Indian and export markets.

- Recent Developments: Ongoing capacity optimization and energy efficiency improvement programs at Sutrapada facility; expanded export volumes to Southeast Asian and Middle Eastern markets.

- Strategic Focus: India market supply dominance, cost leadership through process optimization, capacity expansion aligned with India's growing glass and infrastructure demand, and export market development.

Market Concentration Analysis

The global soda ash market exhibits a distinctive two-tier concentration structure. Outside China, the market is moderately concentrated, the top five non-Chinese producers (Solvay, Ciner, Tata Chemicals, GHCL) account for approximately more than half of non-Chinese production capacity. Within China, the market is highly fragmented, with over 30 active producers operating at various scales, though the top 10 Chinese producers collectively represent approximately 70% of Chinese capacity.

The natural trona production base is geographically highly concentrated Green River Basin, Wyoming is the largest global natural trona production capacity, creating supply chain concentration risk for buyers seeking sustainable or natural-origin soda ash. Turkey's Beypazari trona deposit (operated by Ciner and other producers) and Kenya's Lake Magadi (operated by Tata Chemicals) provide the principal diversification from the Wyoming concentration. M&A activity in the soda ash sector has been modest but strategically significant.

Investment & Growth Opportunities

Fastest Growing Application Segments

Solar glass, lithium carbonate production for EV batteries, and industrial wastewater treatment represent the highest-growth investment vectors in the global soda ash market through 2034. These segments collectively represent an incremental demand by 2034.

Emerging Market Capacity Investment

Indonesia's announced 300,000 ton/year domestic capacity plans (PT Pupuk Indonesia, 2024) represents the archetype of emerging market import substitution investment opportunity. India's growing soda ash consumption deficit – with domestic demand growing at approximately 7–8% annually ahead of production capacity expansion – is attracting significant foreign direct investment in new Solvay process capacity. East Africa's trona deposits represent a multi-billion dollar greenfield investment opportunity for both natural soda ash production and regional industrial chemical supply.

Technology and Green Production Investment

- Electrolytic soda ash production using renewable electricity represents a next-generation low-carbon production pathway attracting pilot-scale investment from chemical companies in renewable-energy-abundant regions including Chile, Morocco, and the Gulf states.

- Lithium carbonate production capacity investments in Chile, Argentina, and Australia are creating co-located soda ash procurement demand, incentivizing proximity production capacity investment to reduce logistics costs in the battery supply chain.

- Digital process optimization platforms for Solvay process energy management, using AI-driven heat integration, predictive maintenance, and real-time purity control are achieving 10–15% energy intensity reductions, representing significant investment ROI at current energy prices.

Future Market Outlook (2026-2034)

The global soda ash market is entering a decade of above-historical-average growth, driven by the structural convergence of construction and urbanization demand, solar energy transition glass requirements, and the EV battery supply chain's emerging link to soda ash through lithium carbonate production.

The energy transition will be the most consequential structural factor reshaping soda ash demand through 2034. Solar PV deployment growth, accelerating across Asia, Europe, the Middle East, and the Americas is creating unprecedented new demand for ultra-clear flat glass that directly drives premium-grade soda ash consumption. Simultaneously, the lithium carbonate supply chain's scale-up for EV batteries is creating a new high-growth, price-premium application for soda ash that did not exist at material scale prior to 2020.

Research Methodology

Primary Research

Primary research for this report included structured interviews with over 140 industry participants in 2024–2025, comprising soda ash producers, glass and detergent manufacturers, chemical distributors, water treatment operators, and industry analysts across China, Europe, North America, India, and the Middle East.

Secondary Research

Secondary research encompassed comprehensive review of company annual reports, IHS Markit chemical industry databases, USGS Mineral Commodity Summaries, CEFIC (European Chemical Industry Council) data, trade publications (ICIS Chemical Business, Chemical & Engineering News), and government industrial statistics from China's National Bureau of Statistics, EU Eurostat, and USDA. Over 280 secondary sources were reviewed and validated.

Forecasting Models

Market size estimations and growth projections were derived using a combination of bottom-up production capacity and utilization modeling and top-down end-market demand analysis, incorporating glass production forecasts, detergent consumption projections, EV battery supply chain lithium carbonate demand models, and wastewater treatment infrastructure investment plans by region. Scenario analysis was performed across base, optimistic, and conservative cases.

Soda Ash Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD, Million Tons |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Applications Covered | Glass, Soaps and detergents, Chemicals, Metallurgy, Pulp and paper, and Others |

| Regions Covered | China, Asia Pacific (Excluding China), Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Solvay S.A., Tata Chemicals, Ciner Group, GHCL Limited, Nirma Limited, Tokuyama Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the soda ash market from 2020-2034.

- The soda ash market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the soda ash industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Soda Ash Market Report

The global soda ash market was valued at USD 21.6 Billion in 2025 and is projected to reach USD 31.3 Billion by 2034, growing at a CAGR of 4.09%.

The market is forecast to grow at a CAGR of 4.09% during 2026-2034, driven by glass manufacturing expansion, solar energy transition glass demand, wastewater treatment growth, and emerging EV battery supply chain applications.

China dominates with a 44.3% market share in 2025, backed by world-leading production capacity across Solvay and Hou process facilities, and simultaneous dominance in soda ash-consuming industries including glass, detergents, and chemicals.

Glass manufacturing leads with a 52.8% share in 2025, encompassing flat glass for construction and automotive, container glass, solar PV panel glass, and specialty glass applications.

Key drivers include glass demand from construction and automotive sectors, solar PV glass expansion, wastewater treatment infrastructure investment, soaps and detergent consumption in developing markets, and lithium carbonate production for EV batteries.

Solar PV installations require ultra-clear flat glass, consuming significant amount of soda ash per GW of solar capacity deployed. This creates a powerful, structurally growing new demand vector for soda ash as a key enabler of the global decarbonization transition.

Soda ash (sodium carbonate) is used as a precipitation reagent in lithium carbonate production from brine sources, lithium carbonate is the key cathode material precursor for lithium-ion EV batteries. As EV production scales, lithium carbonate demand grows proportionally, creating a material new high-growth application for soda ash.

Leading companies include Solvay S.A., Tata Chemicals, Ciner Group, GHCL Limited, Nirma Limited, Tokuyama Corporation, etc.

The global soda ash market is projected to reach USD 26.4 Billion by 2030, reflecting steady compound growth from the 2025 base at the market's 4.09% CAGR.

Natural soda ash is mined from trona deposits and processed through calcination, primarily in Wyoming (USA), Turkey, and Kenya. Synthetic soda ash is produced via the Solvay or Hou chemical process. Natural soda ash has 40% lower CO2 emissions and 30–40% lower production cost, while synthetic production is more geographically distributable.

Key opportunities include import substitution capacity in Indonesia and India, East Africa trona deposit development, green/low-carbon soda ash production technology investment, EV battery supply chain proximity production, and solar glass-driven capacity expansion in Asia Pacific.

Key challenges include rising carbon pricing on energy-intensive Solvay process production, natural trona supply geographic concentration, transportation cost sensitivity as a bulk commodity, substitute chemicals in niche applications, and Chinese export volume influence on global pricing.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)