Soft Starter Market Size, Share, Trends and Forecast by Type, Application, End Use Industry, and Region, 2026-2034

Soft Starter Market Size, Share, Trends & Forecast (2026-2034)

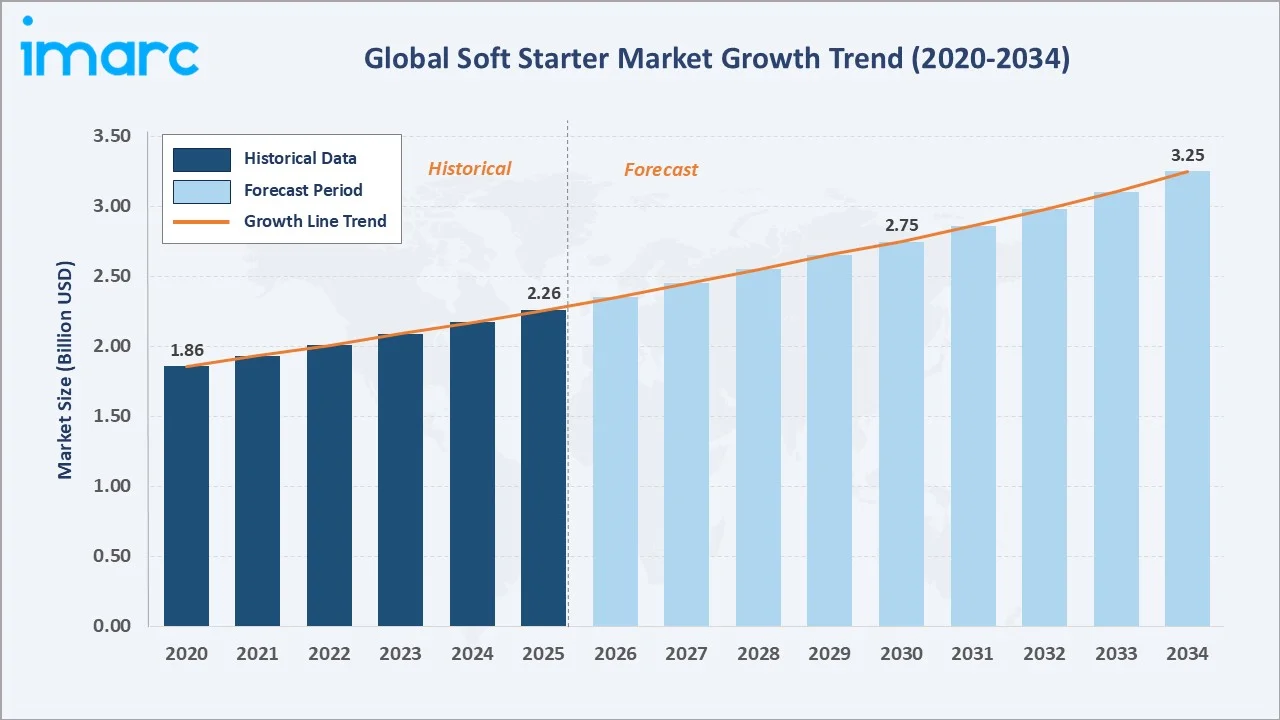

The global soft starter market reached USD 2.26 Billion in 2025 and is projected to reach USD 3.25 Billion by 2034, growing at a CAGR of 4.00% during 2026-2034. Rising demand for motor protection and energy efficiency in industrial applications, expanding oil and gas capital expenditure, and stringent global energy regulations are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.26 Billion |

|

Forecast Market Size (2034) |

USD 3.25 Billion |

|

CAGR (2026-2034) |

4.00% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

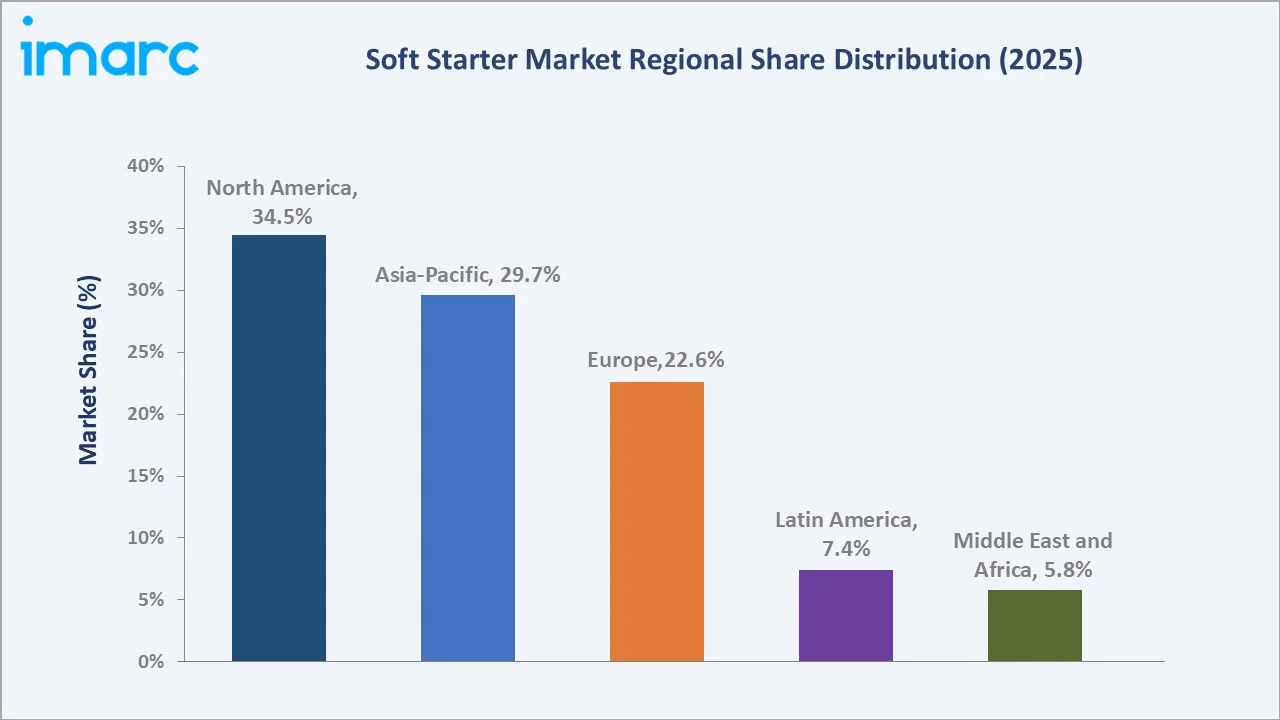

North America leads regionally with a 34.5% market share in 2025, anchored by its large industrial motor installed base, high oil and gas capital expenditure, and stringent energy efficiency regulations. Oil and gas dominate the end use breakdown at 29.3%, while the pumps application segment commands a 46.7% share, reflecting the widespread use of soft starters for controlled pump motor starting in oil and gas and water treatment operations.

To get more information on this market, Request Sample

The soft starter market is driven by three convergent structural forces: global industrial energy efficiency mandates compelling motor control upgrades, sustained oil and gas and mining capital expenditure creating ongoing motor protection demand, and the progressive shift from direct-on-line starters to electronically controlled motor starting solutions across heavy industries worldwide.

Executive Summary

The global soft starter market is experiencing steady growth, supported by the convergence of industrial motor protection requirements, tightening energy efficiency regulations, and sustained capital investment in oil and gas, mining, and power generation infrastructure. The market was valued at USD 2.26 Billion in 2025 and is forecast to reach USD 3.25 Billion by 2034, growing at a CAGR of 4.00%. The ongoing transition from direct-on-line and star-delta starters to electronically controlled soft starters across heavy industry applications is a primary structural market driver.

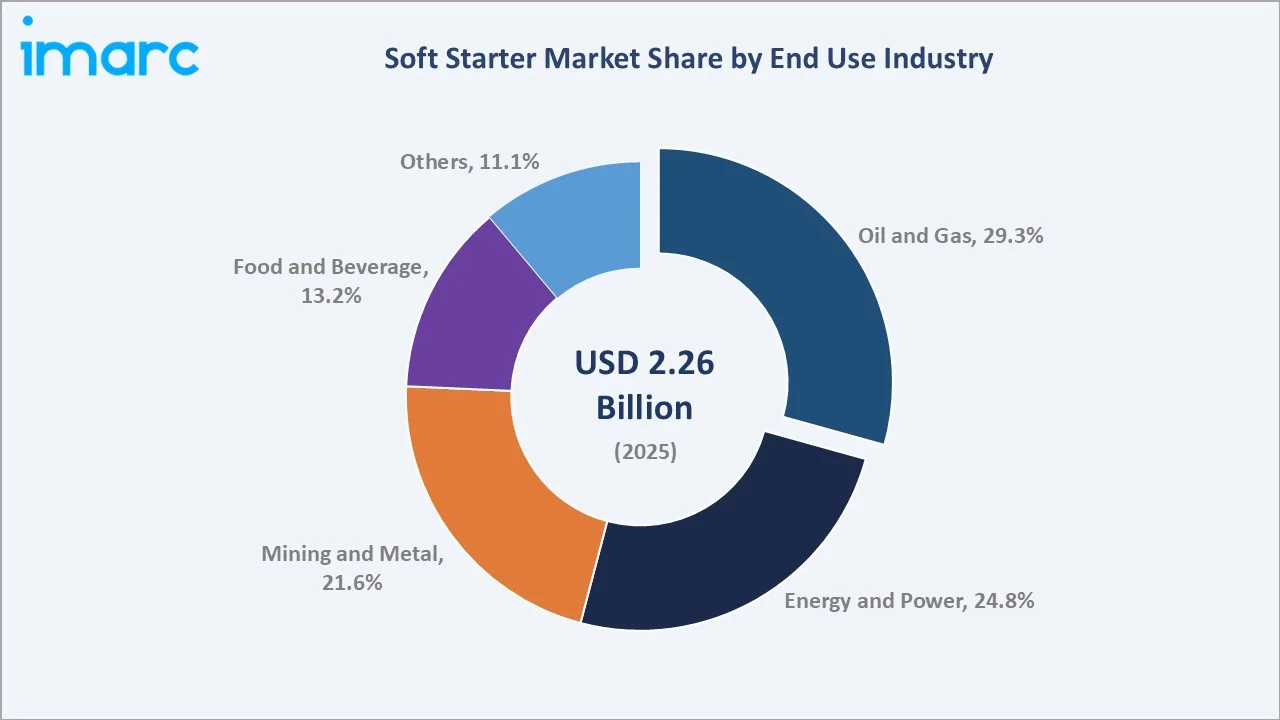

Oil and gas lead the end use segment with a 29.3% share in 2025, driven by the critical need for controlled motor starting in compressor stations, pump systems, and offshore platform motor loads, where mechanical stress reduction directly reduces maintenance costs and extends equipment life. Energy and power follow at 24.8%, reflecting the large motor installed base in power generation facilities, substations, and utility infrastructure. Mining and metal at 21.6% represents the third major end use, with soft starters critical for belt conveyor drives, crusher motors, and slurry pump systems in underground and surface mining operations.

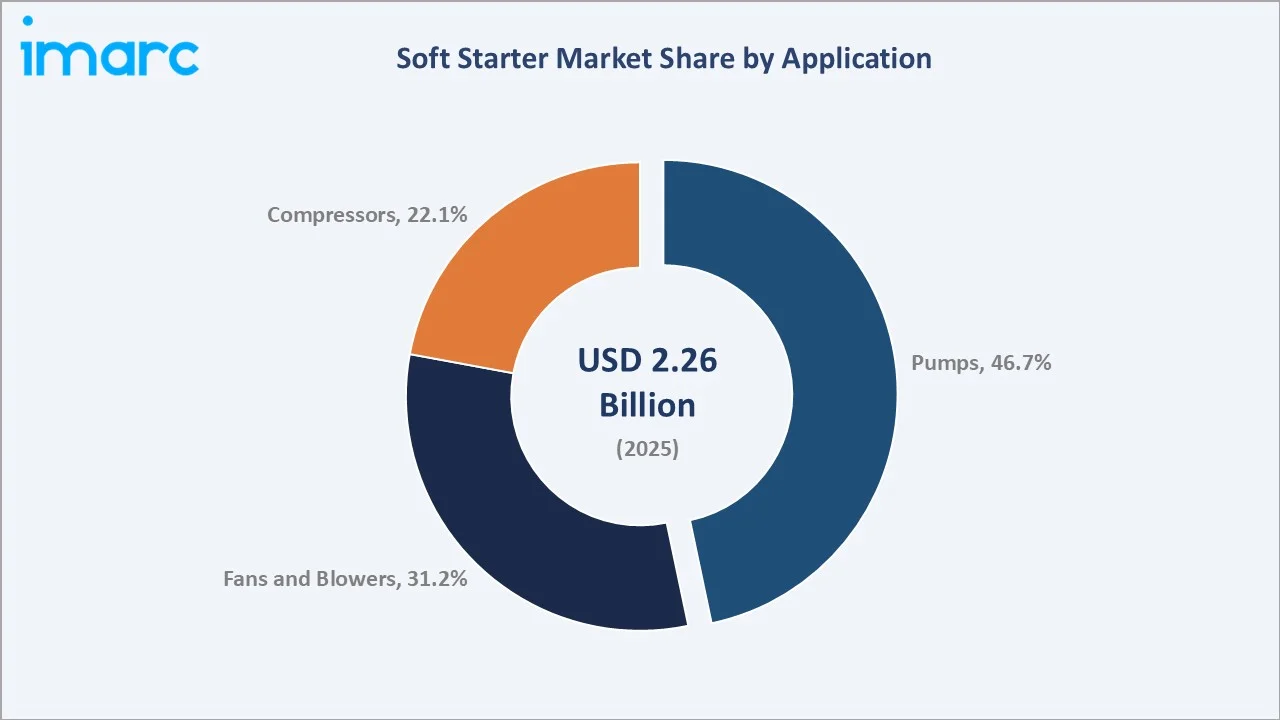

The pumps application segment leads at 46.7%, anchored by the extensive deployment of soft starters for pump motor control in oil and gas, water treatment, and industrial process applications. North America leads regionally at 34.5%, supported by a large industrial motor installed base, high replacement cycle activity, and significant oil and gas capital spending across the Gulf Coast, Permian Basin, and Canadian oil sands. Key players collectively dominate the competitive landscape through product innovation, global service networks, and deep industrial sector relationships.

Key Market Insights

|

Insight |

Data |

|

Largest End Use |

Oil and Gas – 29.3% share (2025) |

|

Fastest Growing End Use |

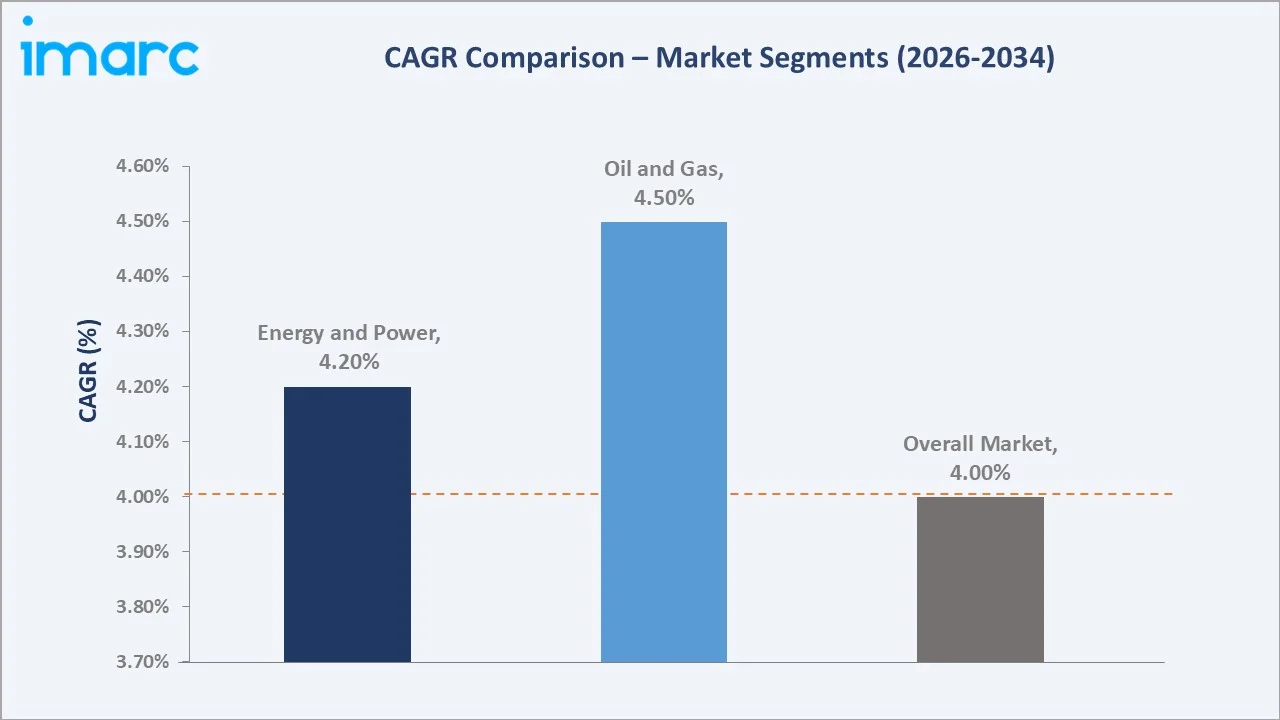

Oil and Gas – ~4.5% CAGR (2026-2034) |

|

Largest Application |

Pumps – 46.7% share (2025) |

|

Fastest Growing Application |

Compressors – ~4.8% CAGR (2026-2034) |

|

Leading Region |

North America – 34.5% share (2025) |

|

Top Companies |

ABB Ltd, Siemens, Schneider Electric SE, Eaton Corporation plc, Rockwell Automation Inc. |

Key Analytical Observations Supporting The Above Data:

- Oil and gas accounts for 29.3% of the global soft starter market in 2025. This dominance reflects the critical importance of controlled motor starting for compressors, pumps, and fans in upstream extraction, midstream pipeline compression, and downstream refinery operations, where mechanical and electrical stress reduction directly reduces unplanned downtime and maintenance costs.

- Pumps represent 46.7% share (2025) of the application segment, reflecting the soft starter’s fundamental role in centrifugal pump applications, where inrush current limitation and gradual speed ramp-up prevent water hammer effects, reduce mechanical seal wear, and extend impeller and piping system life.

- Energy and power at 24.8% (2025) reflects the large motor population in power generation and utility infrastructure. Soft starters enable controlled starting of boiler feed pumps, cooling water pumps, and auxiliary drives in thermal, hydro, and renewable power plants without the electrical stress of direct-on-line starting.

- North America’s 34.5% share (2025) reflects the region’s combination of a large industrial motor installed base with high replacement cycle activity, significant oil and gas capital expenditure, and early adoption of energy efficiency regulations that mandate electronically controlled motor starting solutions.

Soft Starter Market Overview

A soft starter is an electronic device that controls the voltage supplied to an electric motor during the start-up phase, gradually increasing voltage to limit inrush current, reduce mechanical torque shock, and enable smooth motor acceleration. Soft starters are deployed across industrial applications wherever motor starting stress represents a risk to motor longevity, connected equipment, or power network stability. The global market spans low voltage (LV), medium voltage (MV), and high voltage (HV) product categories, with MV soft starters commanding premium pricing and market share in heavy industry applications.

Macroeconomic drivers include IEA projections for global industrial energy consumption growing at more than 3.5% annually on average through this decade, capital flows to the energy sector expected to grow by 5% in 2026, reaching USD 3.4 trillion, and the EU’s Energy Efficiency Directive mandating motor system efficiency improvements across EU member state industrial facilities. These macro forces collectively sustain replacement demand for legacy direct-on-line and star-delta starters across global industrial motor populations.

Market Dynamics

To evaluate market opportunities, Request Sample

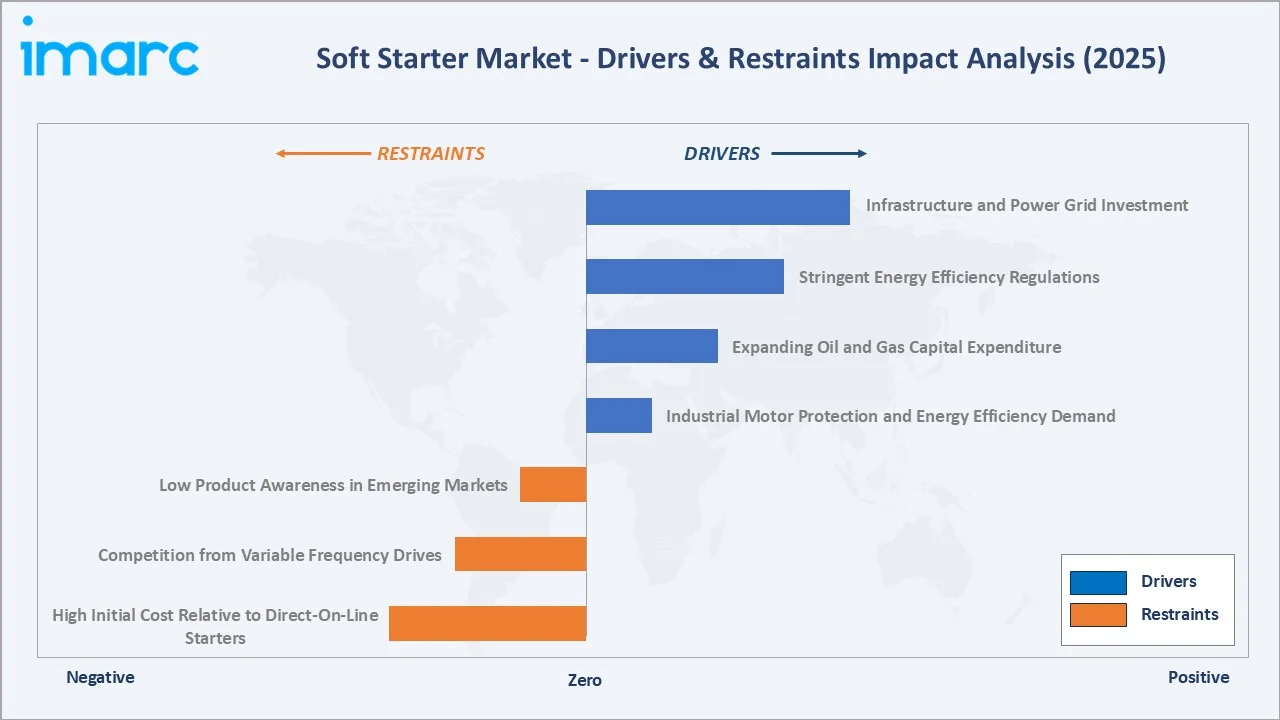

Market Drivers

- Industrial Motor Protection and Energy Efficiency Demand: Soft starters reduce motor inrush current by 30–70% versus direct-on-line starting, by reducing thermal and mechanical stress and thereby extending motor and driven equipment service life. With electric motors accounting for approximately 45% of global electricity consumption, industrial operators face regulatory and cost pressures to deploy electronically controlled starting solutions across their motor fleets.

- Expanding Oil and Gas Capital Expenditure: Although upstream oil spending is declining for a third consecutive year, global investment in natural gas projects is expected to rise by more than 10% this year to USD 330 billion, marking its highest level in a decade, according to the International Energy Agency. New compression stations, pipeline pump systems, and offshore platform motor installations provide sustained soft starter demand across upstream, midstream, and downstream applications.

- Stringent Energy Efficiency Regulations: The EU Energy Efficiency Directive, IEA Net Zero targets, and national energy regulations in North America, China, and India are compelling industrial operators to upgrade legacy starter technology. These mandates create systematic replacement demand for soft starters across ageing industrial motor populations.

- Infrastructure and Power Grid Investment: Global investment in power generation, transmission infrastructure, and water treatment facilities is expanding the addressable base of motor applications requiring soft starters. Renewable energy auxiliary systems, pumped hydro storage, and desalination plants each create new soft starter demand vectors beyond traditional heavy industry.

Market Restraints

- High Initial Cost Relative to Direct-On-Line Starters: Soft starters carry a significant price premium over conventional direct-on-line (DOL) and star-delta starters. In cost-sensitive applications and markets with limited awareness of the total cost of ownership benefits, this premium creates adoption barriers, particularly among SME industrial operators.

- Competition from Variable Frequency Drives: Variable frequency drives (VFDs) offer more comprehensive motor speed and torque control than soft starters, and their cost has declined significantly with Asian manufacturing scale. In applications requiring continuous speed variation, VFDs are preferred over soft starters, limiting the addressable market for soft starter products.

- Low Product Awareness in Emerging Markets: In developing economies across Africa, Southeast Asia, and Latin America, direct-on-line starting remains the dominant motor starting method due to lower initial cost and limited technical expertise. Building market awareness and distribution infrastructure in these markets requires sustained investment from manufacturers.

Market Opportunities

- Predictive Maintenance and IoT Integration: The integration of soft starters with industrial IoT platforms enables real-time motor health monitoring, start event logging, and predictive maintenance alerts. This capability transforms soft starters from passive protective devices into active motor management systems, creating significant product differentiation and value-add opportunities for technology leaders.

- Replacement Demand in Ageing Industrial Installed Base: The global industrial motor installed base includes hundreds of millions of units with legacy direct-on-line starters nearing the end of life. The systematic replacement cycle across oil and gas, mining, and food processing facilities represents a structural demand opportunity independent of capacity expansion cycles.

- Emerging Market Industrial Expansion: Rapid industrialization in India, Indonesia, Vietnam, and Sub-Saharan Africa is creating new motor installation demand that increasingly adopts soft starters from the outset rather than through replacement cycles, representing a growing greenfield market opportunity.

Market Challenges

- Technical Complexity and Installation Expertise Requirements: Soft starter installation, commissioning, and parameter configuration require technical expertise that is not universally available in developing markets. The shortage of qualified electrical engineers and certified installation partners in emerging geographies constrains market penetration below its theoretical addressable scale.

- Semiconductor Supply Chain Volatility: Soft starters are dependent on power semiconductors, thyristors, and microcontrollers whose supply chains experienced significant disruption during 2020–2023. Ongoing semiconductor supply chain concentration risks create cost and availability volatility that challenges manufacturer production planning and pricing stability.

Emerging Market Trends

1. IoT-Enabled Smart Soft Starters

Leading manufacturers are integrating IoT connectivity, onboard diagnostics, and cloud data transmission into next-generation soft starters. Siemens’ SIRIUS 3RW55, Schneider Electric’s Altivar ATS480, and ABB’s PSTX series now offer Modbus, PROFIBUS, EtherNet/IP, and Profinet connectivity, enabling real-time monitoring, remote configuration, and predictive maintenance integration with plant-level MES and SCADA systems. This smart capability is commanding 15–25% price premiums over standard products.

2. Energy Efficiency Regulation-Driven Replacement Cycles

The European Union’s revised Energy Efficiency Directive and the IEA’s Net Zero Industrial Transition requirements are compelling systematic replacement of legacy DOL starters with energy-optimized soft starters and VFDs across EU industrial facilities. Manufacturers are reporting accelerated replacement tender activity in European food and beverage, water treatment, and chemical processing sectors, a trend expected to intensify through 2030 as compliance deadlines approach.

3. Predictive Maintenance Integration

Industrial operators are increasingly requiring soft starters to function as motor condition monitoring nodes within broader predictive maintenance architectures. Soft starters with onboard temperature monitoring, current harmonic analysis, and start event logging are enabling operators to transition from time-based to condition-based maintenance strategies, reducing unplanned downtime in high-criticality pump and compressor applications.

4. Expansion into Renewable Energy Applications

Soft starters are finding new application vectors in renewable energy auxiliary systems, including wind turbine pitch control drives, solar tracking systems, and pumped hydro storage pump-motor units. These applications leverage the soft starter’s core capabilities in a growing market segment that is structurally less dependent on fossil fuel industry capital cycles, providing manufacturers with portfolio diversification opportunities.

Industry Value Chain Analysis

The soft starter value chain spans from raw material and semiconductor supply through component manufacture, product assembly, distribution, industrial installation, and aftermarket service. Each stage is occupied by specialized players, with the manufacturer tier dominated by a small number of large industrial automation groups and a longer tail of regional and application-specific specialists.

|

Stage |

Key Players / Examples |

|

Raw Material & Component Suppliers |

Semiconductor producers, thyristor manufacturers, PCB fabricators, heat sink and enclosure suppliers |

|

Component Manufacturers |

Bypass contactor producers, control board manufacturers, cooling system and firmware developers |

|

Soft Starter Manufacturers |

OEM assemblers integrating hardware and firmware, performing quality and safety certification testing |

|

Distributors & System Integrators |

Value-added resellers, panel builders, OEM machine integrators, and MRO distributors |

|

End-Use Industries |

Oil and gas operators, energy and power utilities, mining operators, food and beverage processors |

|

End Users & Operators |

Plant engineers, facility managers, motor control center operators, and energy efficiency teams |

Technology Landscape in the Soft Starter Industry

Thyristor-Based Power Control

The dominant soft starter technology uses anti-parallel connected thyristors (SCRs) on each motor phase to progressively increase applied voltage during the start-up sequence. Modern thyristor-based soft starters incorporate microprocessor-controlled firing angle algorithms that optimize start ramp profiles for specific motor and load characteristics, enabling precise inrush current limitation and torque control across a wide range of motor sizes and load types.

Digital Communication and Protocol Integration

Contemporary soft starters integrate multiple industrial fieldbus and Ethernet protocols, including Modbus RTU/TCP, PROFIBUS DP, DeviceNet, EtherNet/IP, and PROFINET. This protocol diversity enables seamless integration with legacy and modern PLC-based control architectures, reducing engineering effort and enabling centralized motor management from SCADA and DCS platforms across large industrial facilities.

Advanced Motor Protection Functions

Beyond starting control, modern soft starters incorporate comprehensive motor protection functions including phase imbalance detection, undercurrent and overcurrent protection, thermistor motor temperature monitoring, ground fault detection, and motor stall protection. These integrated protection capabilities reduce the need for separate protective relay devices, lowering total installed cost and simplifying motor control center designs.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

End Use Industry |

Oil and Gas |

29.3% |

2025 |

|

Application |

Pumps |

46.7% |

2025 |

|

Type |

Medium to High Voltage Soft Starter |

🔒 |

2025 |

|

Region |

North America |

34.5% |

2025 |

By End Use Industry

The oil and gas segment leads with a 29.3% share of the global soft starter market in 2025, reflecting the critical importance of controlled motor starting in upstream extraction pump systems, midstream pipeline compressor stations, and downstream refinery process motor loads. The physical consequences of uncontrolled motor starting make soft starters an essential protective investment in oil and gas facilities where unplanned downtime carries significant production and safety costs.

To access detailed market analysis, Request Sample

Energy and power represents 24.8% of the market in 2025, driven by the large motor population in power generation facilities, substations, and utility infrastructure. Mining and metal at 21.6% reflects deployment in belt conveyor drives, crusher motors, and pump systems in surface and underground mining operations. Food and beverage at 13.2% benefits from the hygiene and operational continuity requirements of food processing facilities, where controlled motor starting reduces product quality risks during production line start-up.

By Application

The pumps application segment dominates with a 46.7% share in 2025, representing the largest single motor application in industrial facilities across oil and gas, mining, water treatment, and process industries. Soft starters are particularly well-suited to centrifugal pump applications, where their voltage ramp-up capability prevents water hammer and eliminates the mechanical shock that reduces impeller and seal life in direct-on-line started pump systems.

Fans and blowers represent 31.2% of the application segment in 2025, reflecting the widespread use of soft starters in industrial ventilation, combustion air, and process gas handling fan systems, where torque shock at start-up causes belt and coupling fatigue.

Compressors at 22.1% represent the third major application, with soft starters critical for reciprocating and screw compressor starting across oil and gas, mining, and refrigeration applications, where compressor valve and coupling mechanical stress at full-voltage starting would otherwise limit equipment life.

Regional Market Insights

North America’s dominant position (34.5%, 2025) reflects the region’s combination of a large industrial motor installed base, significant oil and gas capital expenditure, and early adoption of energy efficiency regulations. The United States represents the single largest national market, driven by the Gulf Coast petrochemical complex, Permian Basin oil and gas activity, and the extensive industrial motor installed base across manufacturing, mining, and water utility sectors.

Asia-Pacific, with 29.7% share (2025), is the fastest-growing regional market, driven by China’s continued heavy industrial expansion, India’s infrastructure and manufacturing growth, and the electrification of new industrial capacity across Southeast Asia.

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

34.5% |

Strong industrial base, stringent energy efficiency regulations, high oil and gas capital expenditure, and well-established replacement and upgrade cycles for motor control equipment |

|

Asia-Pacific |

29.7% |

Rapid industrialization, expanding manufacturing capacity, growing energy and power infrastructure investments, and increasing adoption of motor protection technologies in emerging economies |

|

Europe |

22.6% |

Strict energy efficiency directives, large industrial motor installed base, strong demand from the food and beverage and chemical processing sectors, and ongoing plant modernization programs |

|

Latin America |

7.4% |

Growing oil and gas extraction activity, expanding mining operations, increasing industrial infrastructure investment, and rising awareness of motor protection benefits |

|

Middle East and Africa |

5.8% |

Hydrocarbon sector expansion, new power generation infrastructure, increasing adoption of energy management systems, and growth in water treatment and desalination plant installations |

Europe, at 22.6%, is characterized by replacement demand driven by energy efficiency directives, with particularly strong activity in German, French, and Nordic industrial sectors. Latin America at 7.4% and the Middle East and Africa at 5.8% represent smaller but growing markets, driven by oil and gas and mining sector investment in their respective regions.

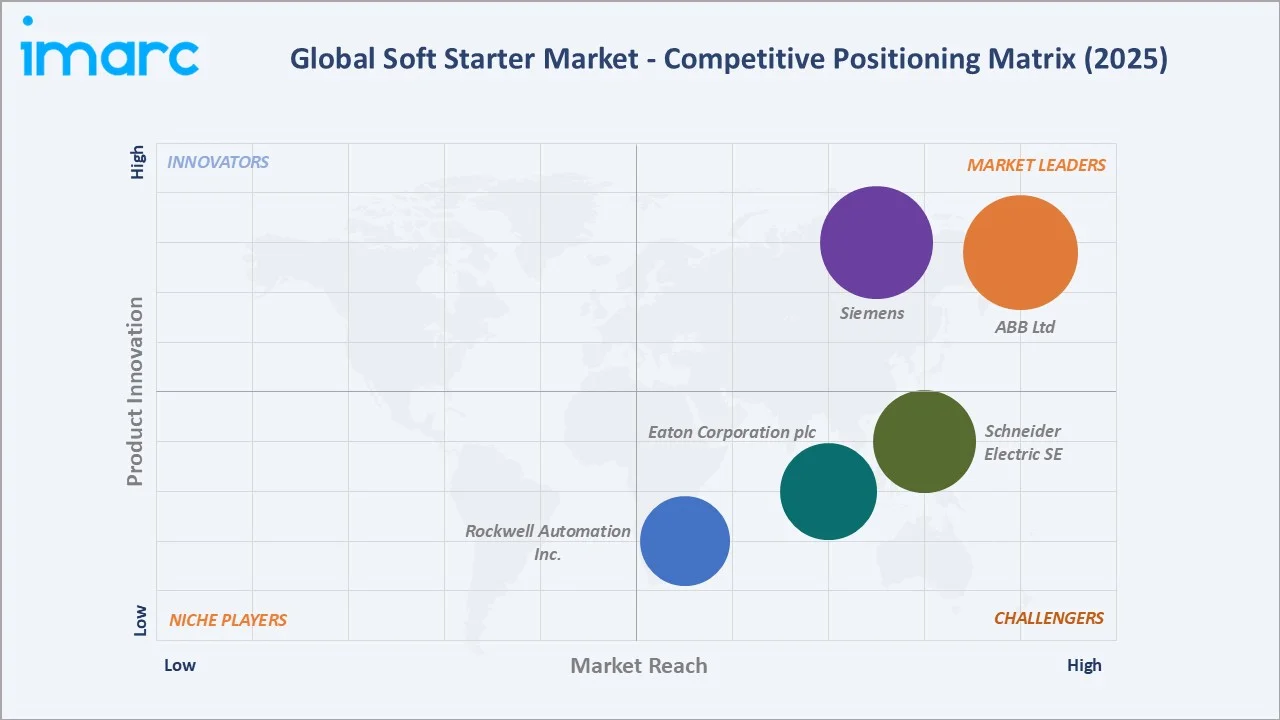

Competitive Landscape

The global soft starter market exhibits moderate-to-high concentration, with the top players collectively accounting for approximately 60–65% of global market revenue in 2025. The remaining market is served by regional specialists, including Carlo Gavazzi Holding AG, CG Power and Industrial Solutions, OMRON Corporation, and SOLCON.

|

Company Name |

Brands/Products |

Market Position |

Core Strength |

|

ABB Ltd |

PSTX Soft Starters, PSE Soft Starters, PSR Soft Starters, PSRC Soft Starters |

Market Leader |

Broad product portfolio, global service network, and strong industrial automation integration capability |

|

Siemens |

SIRIUS 3RW Soft Starters, SIRIUS 3RW5 -Z R11 refurbished soft starter |

Market Leader |

Advanced motor control technology, large installed base, and deep integration with industrial automation systems |

|

Schneider Electric SE |

Altivar Soft Starter ATS490, Altivar Soft Starter ATS430, Altivar Soft Starter ATS130, Altivar Soft Starter ATS480 |

Strong Challenger |

IoT-enabled motor protection, energy management expertise, and an extensive global distribution network |

|

Eaton Corporation plc |

S811+ Soft Starter, DS7 Soft Starter |

Strong Challenger |

Energy-efficient design focus, strong North American presence, and competitive pricing in the low-voltage segment |

|

Rockwell Automation Inc. |

Allen-Bradley SMC-3, SMC Flex, and SMC-50 Soft Starters |

Challenger |

Seamless PLC integration, smart manufacturing positioning, and strong North American factory automation presence |

Leading manufacturers compete primarily on product technology (IoT connectivity, protection function breadth, and energy savings certification), global service network coverage, and total installed cost value propositions targeted at specific end-use segments.

Key Company Profiles

ABB Ltd

ABB Ltd is one of the world’s leading electrification and automation technology companies and one of the global market leaders in soft starters. Its PSTX series represents the company’s flagship product line, combining comprehensive motor protection functions and multi-protocol communication for energy-efficient steady-state operation.

- Product Portfolio: PSE, PSR, PSRC, and PSTX series soft starters spanning 3–2000A, with specialized versions for marine, ATEX hazardous area, and high-ambient-temperature applications.

- Recent Developments: In April 2026, ABB Ltd reported Q1 2026 results, with orders rising 32% year-on-year to a record USD 11.3 billion and revenues increasing 18% to USD 8.73 billion. Operational EBITA reached USD 2.05 billion with a margin of 23.5%, driven by robust demand in electrification, automation, and power grid products.

- Strategic Focus: Digital service platform expansion; growing presence in data center and renewable energy applications; lifecycle management service contracts for large motor populations.

Siemens

Siemens is one of the global industrial automation and electrification leaders whose SIRIUS product family encompasses one of the broadest motor control portfolios in the industry. The SIRIUS 3RW series covers the full soft starter product range from standard to fully integrated smart soft starters.

- Product Portfolio: SIRIUS 3RW30, 3RW40, 3RW50, and 3RW55 series spanning standard to high-feature variants; SIRIUS 3RW5 -Z R11 refurbished soft starter.

- Recent Developments: In March 2026, Siemens launched the circular SIRIUS 3RW5 -Z R11 refurbished soft starter, designed to deliver the same features as a new device with up to 50% lower CO₂ footprint. The product supports sustainable industrial motor control through tested refurbishment, component replacement, full functionality checks, and seamless integration.

- Strategic Focus: TIA Portal integration for seamless engineering workflow; industry-specific solution packages for oil and gas, mining, and water treatment; digital twin capabilities for motor system optimization.

Market Concentration Analysis

The global soft starter market exhibits moderate-to-high concentration at the global level, with the top players accounting for approximately 60–65% of market revenues. The remaining 35–40% is distributed among regional specialists, application-specific manufacturers, and a growing tier of Asian manufacturers competing on price in the standard low-voltage segment.

Consolidation activity has been limited in recent years, with manufacturers preferring organic growth through product line extensions and IIoT platform investments over acquisition. Moreover, the competitive intensity at the standard product tier is increasing as Asian manufacturers expand their global distribution, constraining pricing power for incumbent Western manufacturers in volume segments.

Investment & Growth Opportunities

Fastest Growing Segments

Oil and gas (~4.5% CAGR), compressors (~4.8% CAGR), and renewable energy auxiliary system applications represent the highest-growth investment vectors within the soft starter market through 2034. Aftermarket service contracts and digital monitoring subscriptions are emerging as a recurring revenue opportunity that is growing faster than hardware sales.

Emerging Market Expansion

India, Indonesia, Vietnam, and sub-Saharan Africa represent significant greenfield market opportunities as rapid industrialization installs new motor populations that increasingly adopt soft starters from the outset. Local manufacturing partnerships, targeted channel development, and simplified product variants suited to local technical capability levels are the primary market entry strategies for manufacturers targeting these geographies.

Technology Investment Trends

- IIoT platform investment is accelerating, with leading manufacturers integrating soft starters into broader digital asset management platforms offering subscription-based motor health monitoring, remote diagnostics, and predictive maintenance services that transform the soft starter from a capital purchase into a managed service.

- Energy efficiency certification programs are creating differentiation opportunities for manufacturers whose products can demonstrably contribute to certified system-level efficiency improvements.

- Semiconductor supply chain diversification and regional manufacturing capacity investments are being prioritized by leading manufacturers following the 2020–2023 supply chain disruptions, with nearshoring initiatives planned for North America and Europe.

Future Market Outlook (2026-2034)

The global soft starter market is positioned for steady, sustained growth through 2034. From USD 2.26 Billion in 2025, the market is projected to reach USD 3.25 Billion by 2034, representing total incremental value creation of USD 0.99 Billion at a CAGR of 4.00%. This growth is structurally supported by the global industrial motor installed base replacement cycle, tightening energy efficiency regulation, and the ongoing transition of soft starters from simple motor protection devices to integrated IIoT-enabled motor management systems.

The competitive landscape will continue to bifurcate between a premium tier of IoT-integrated, analytics-enabled smart soft starters and a commoditizing standard product tier. Manufacturers investing in digital service platforms and lifecycle management offerings will sustain higher margins, while those competing solely on hardware price in standard voltage segments will face increasing pressure from Asian manufacturing competition. The transition of soft starters into managed service models through subscription-based motor monitoring represents the most significant structural market evolution anticipated through 2034.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 70 industry participants in 2024–2025, including soft starter manufacturers, motor control system integrators, end-use industry plant engineers, electrical equipment distributors, and industrial automation consultants across North America, Europe, and Asia-Pacific. Expert input validated market sizing, segment growth rates, and regional penetration estimates.

Secondary Research

Secondary research encompassed manufacturer annual reports and investor disclosures, IEA industrial energy consumption statistics, IEEE Transactions on Industrial Electronics publications, EU Energy Efficiency Directive implementation guidelines, NEMA and IEC motor standards documentation, and industry publications including Control Engineering, Plant Engineering, and Drives & Controls.

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting, incorporating global industrial motor population data, soft starter penetration rate modelling by industry and application, replacement cycle duration assumptions, and new installation growth projections. The base-case CAGR of 4.00% reflects consensus estimates validated against manufacturer revenue growth disclosures and industrial capital expenditure projection databases for 2026–2034.

Soft Starter Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Low Voltage Soft Starter, Medium to High Voltage Soft Starter |

| Applications Covered | Pumps, Fans and Blowers, Compressors |

| End Use Industries Covered | Mining and Metal, Food and Beverage, Energy and Power, Oil and Gas, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | ABB Ltd, Siemens, Schneider Electric SE, Eaton Corporation plc, Rockwell Automation Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the soft starter market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global soft starter market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the soft starter industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Soft Starter Market Report

The global soft starter market reached USD 2.26 Billion in 2025 and is projected to reach USD 3.25 Billion by 2034.

The market is expected to grow at a CAGR of 4.00% during 2026-2034, driven by industrial motor protection demand, energy efficiency regulations, oil and gas capital expenditure, and expanding IIoT integration.

North America leads with a 34.5% share in 2025, anchored by its large industrial motor installed base, significant oil and gas capital expenditure, and early adoption of energy efficiency regulations compelling motor control upgrades.

Oil and gas dominate with a 29.3% share in 2025, driven by the critical importance of controlled motor starting for compressors, pumps, and fans in upstream, midstream, and downstream oil and gas operations.

Pumps lead with a 46.7% share in 2025, reflecting the widespread deployment of soft starters in centrifugal pump applications across oil and gas, water treatment, mining, and industrial process sectors.

Some of the key players include ABB Ltd, Siemens, Schneider Electric SE, Eaton Corporation plc, and Rockwell Automation Inc.

Key drivers include industrial motor protection requirements, reducing inrush current and mechanical stress, global energy efficiency regulations, sustained oil and gas capital expenditure, and IIoT integration enabling predictive maintenance value propositions.

Fastest-growing opportunities include IoT-integrated smart soft starter platforms, medium & high voltage applications in oil and gas and mining, and digital subscription-based motor monitoring services transforming hardware into managed service revenue models.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)