Solar Module Market Report by Technology (Crystalline Silicon, Thin Film), Connectivity (On-grid, Off-grid), Mounting (Ground Mounted, Roof Top), End User (Residential, Commercial, Utility), and Region 2026-2034

Market Overview:

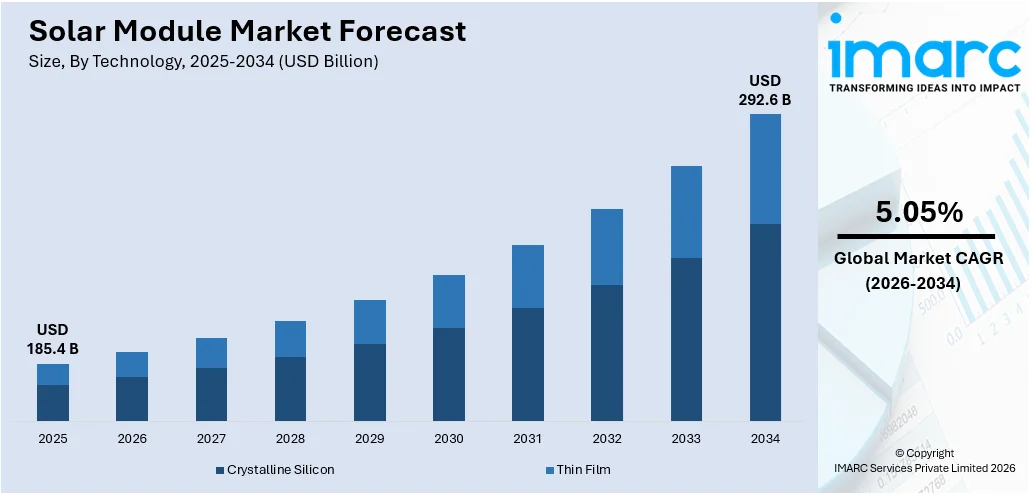

The global solar module market size reached USD 185.4 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 292.6 Billion by 2034, exhibiting a growth rate (CAGR) of 5.05% during 2026-2034. The increasing agricultural integration, the rapid residential growth, the rising innovative business models, the intense competition among solar manufacturers, the escalating improvements in solar module efficiency and durability, and the increasing mandates for renewable energy integration are some of the factors propelling the market.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 185.4 Billion |

| Market Forecast in 2034 | USD 292.6 Billion |

| Market Growth Rate 2026-2034 | 5.05% |

A solar module, also known as a solar panel, is a device that converts sunlight into electricity using photovoltaic cells. These cells are made from semiconductor materials like silicon, which absorb photons from sunlight and release electrons, generating an electric current. Solar modules consist of multiple solar cells connected in a circuit and enclosed in a protective casing. They are essential components of solar energy systems for residential, commercial, or industrial applications. They provide a clean and renewable source of electricity, contributing to reduced greenhouse gas emissions and a more sustainable energy future. The efficiency of a solar module is measured by its ability to convert sunlight into usable electricity. Advances in technology have led to improved efficiency and affordability of solar modules over the years. As solar energy continues to gain popularity, innovations in solar module design and manufacturing are shaping a promising path toward greater adoption and integration into various aspects of our lives.

To get more information on this market Request Sample

The global market is majorly driven by the increasing energy demand. In line with this, the rising awareness of climate change encourages the adoption of clean energy solutions, significantly contributing to the market. Furthermore, subsidies, tax credits, and grants make solar installations more attractive, positively influencing the market. Apart from this, technological advancements and economies of scale are lowering solar module production costs, catalyzing the market. Moreover, the higher conversion rates of sunlight into electricity make solar modules more appealing, propelling their demand. Besides, the solar module growth contributes to employment opportunities in manufacturing, installation, and maintenance, strengthening the market. Additionally, the growing urban populations drive the need for distributed energy solutions, stimulating the market. Other factors driving the market include rapid technological innovations, the global energy transition, advances in battery technology, and favorable policies and regulations.

Solar Module Market Trends/Drivers:

Increasing infrastructure development

The increasing infrastructure development is favorably impacting the market. As countries invest in expanding their energy networks and enhancing power distribution systems, the demand for solar modules rises in tandem. Solar installations require new transmission lines, substations, and storage facilities, stimulating the growth of the renewable energy sector and associated infrastructure projects. Moreover, the integration of solar energy into existing grids requires advancements in smart grid technology, making solar modules an essential component of modernizing energy infrastructure. This synergy between solar energy expansion and infrastructure development creates a positive feedback loop, where the growth of one sector accelerates progress in the other.

Rising energy transition policies by governments worldwide

The global rise in energy transition policies enforced by governments is creating a positive outlook for the market. With a growing emphasis on reducing carbon emissions and shifting towards renewable sources, these policies encourage the adoption of solar energy as a vital component of clean energy portfolios. Governments are setting ambitious targets for renewable energy adoption, creating a strong market demand for solar modules. Subsidies, incentives, and regulations promoting renewable energy further enhance the attractiveness of solar installations. As a result, solar module manufacturers experience increased orders and investments, accelerating innovation and economies of scale. The alignment between government policies and market growth cultivates an environment where solar modules play a crucial role in achieving sustainability goals. This trend positions the solar module market as a focal point of economic growth and environmental transformation in the energy sector.

Growing integration with IoT, AI, and smart grids

The growing integration of solar modules with IoT (Internet of Things), AI (Artificial Intelligence), and smart grids is a key driver of the market expansion. This integration enhances the efficiency and effectiveness of solar energy systems. IoT allows for real-time monitoring and control of solar installations, optimizing energy production and maintenance. AI algorithms can predict solar output, manage energy storage, and even forecast maintenance needs, making solar power more reliable. Additionally, integration with smart grids enables better energy supply and demand synchronization, improving grid stability and resilience. As industries and utilities increasingly adopt these technologies, the demand for technologically advanced solar modules rises. This trend stimulates innovation in both the solar and technology sectors, propelling the growth of the solar module market by providing sophisticated solutions that align with modern energy needs and infrastructure.

Solar Module Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global solar module market report, along with forecasts at the global, regional and country levels from 2026-2034. Our report has categorized the market based on the technology, connectivity, mounting, and end user.

Breakup by Technology:

- Crystalline Silicon

- Monocrystalline

- Polycrystalline

- Thin Film

- Cadmium Telluride (CdTe)

- Amorphous Silicon (a-Si)

- Copper Indium Gallium Diselenide (CIGS)

Crystalline Silicon dominates the market

The report has provided a detailed breakup and analysis of the market based on technology. This includes crystalline silicon (Monocrystalline and Polycrystalline) and thin film (Cadmium Telluride (CdTe), Amorphous Silicon (a-Si), and Copper Indium Gallium Diselenide (CIGS)). According to the report, crystalline silicon represented the largest segment.

Crystalline silicon technology, comprising monocrystalline and polycrystalline panels, contributes to the market growth due to its efficiency, reliability, and continuous improvements. These panels offer higher energy conversion rates and longer lifespans, making them a preferred choice for residential, commercial, and industrial applications. The ongoing innovation in crystalline silicon technology enhances efficiency while reducing production costs, thus bolstering its adoption.

Furthermore, thin film technology, including amorphous silicon, cadmium telluride, and copper indium gallium selenide panels, offers flexibility, lightweight design, and lower production costs. This makes Thin Film modules suitable for unconventional applications, such as building-integrated photovoltaics and large-scale installations in areas with limited space. The technology's potential for customization and adaptability to various surfaces opens up new opportunities.

Breakup by Connectivity:

- On-Grid

- Off-Grid

On-grid dominates the market

The report has provided a detailed breakup and analysis of the market based on connectivity. This includes on-grid and off-grid. According to the report, on-grid represented the largest segment.

On-grid solar systems are directly connected to the utility grid, allowing excess energy generated by solar modules to be fed back into the grid. This integration promotes the efficient use of solar power and enables users to earn incentives through net metering or feed-in tariffs. As more regions adopt favorable policies for grid-connected systems, the demand for on-grid solar modules rises.

On the other hand, off-grid solar systems cater to remote or isolated locations where traditional power infrastructure is unavailable or expensive to implement. These systems rely on solar modules and energy storage solutions, such as batteries. Off-grid solar modules provide vital electricity access to rural areas, powering homes, schools, healthcare facilities, and small businesses. The technology's capability to empower communities without access to centralized electricity grids fosters market growth by tapping into previously underserved segments.

Breakup by Mounting:

- Ground Mounted

- Roof Top

Ground mounted dominates the market

The report has provided a detailed breakup and analysis of the market based on mounting. This includes ground mounted and roof top. According to the report, ground mounted represented the largest segment.

Ground-mounted solar installations effectively harness solar energy in open spaces like fields or unused land. These systems can be designed for utility-scale projects, enabling the generation of significant amounts of electricity. As renewable energy goals become more ambitious, the demand for ground-mounted solar installations increases, leading to market growth.

Rooftop solar installations, on the other hand, cater to residential, commercial, and industrial buildings, where available space on rooftops is utilized to generate clean energy. The adoption of rooftop solar systems is rising due to incentives, reduced energy bills, and increased environmental awareness. As urban areas become denser, rooftop installations present a viable means to maximize energy production while minimizing land usage.

Breakup by End User:

Access the comprehensive market breakdown Request Sample

- Residential

- Commercial

- Utility

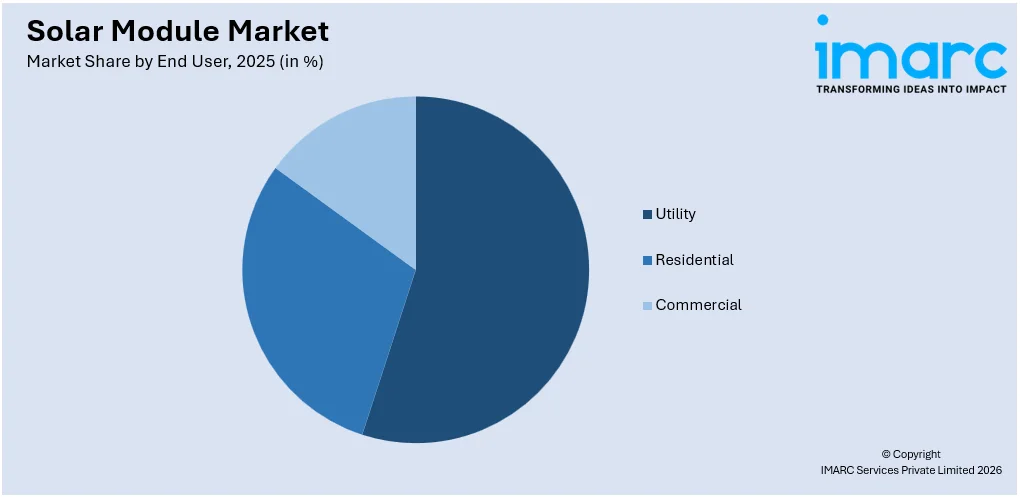

Utility dominates the market

The report has provided a detailed breakup and analysis of the market based on end user. This includes residential, commercial, and utility. According to the report, utility represented the largest segment.

Utility solar installations empower homeowners to generate clean energy, reducing reliance on traditional power sources and lowering electricity bills. As renewable energy gains popularity, increased awareness of environmental benefits and potential savings encourages to adopt solar modules. Government incentives and financing options stimulate utility solar growth, contributing to the market's expansion.

Solar modules are also being rapidly integrated into businesses, offices, and industrial complexes in the commercial sector. Companies are driven by environmental consciousness and the opportunity to cut operational costs and improve their sustainability profile. As corporate social responsibility gains prominence, businesses are investing in solar installations as a strategic move to showcase their commitment to clean energy and reduce their carbon footprint.

Breakup by Region:

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

Asia Pacific exhibits a clear dominance, accounting for the largest market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Europe (Germany, France, the United Kingdom, Italy, Spain, and others); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, Asia Pacific accounted for the largest market share.

In Asia Pacific, numerous policies promoting renewable energy adoption and advancements in solar technology have catalyzed significant growth in the solar module market. The region has seen substantial investments in solar installations across residential, commercial, and utility-scale projects. Net metering, federal tax incentives, and state-level initiatives encourage solar adoption, driving market expansion.

Furthermore, Europe has also emerged as a leader in renewable energy deployment, driven by aggressive climate targets and supportive policies. Several countries have well-established solar markets driven by feed-in tariffs and comprehensive energy strategies. Europe's commitment to sustainability and clean energy and technological innovations have fostered consistent growth in the solar module sector.

Competitive Landscape:

Top companies are bolstering the market growth through innovation, scale, and influence. These industry leaders invest heavily in research and development, constantly improving the efficiency and performance of solar modules. They drive economies of scale in manufacturing, reducing costs and making solar installations more accessible. Additionally, these companies establish strategic partnerships, ensuring widespread distribution and installation networks. Their strong brand reputation and quality assurance inspire consumer confidence, further accelerating adoption. Furthermore, their involvement in large-scale projects and partnerships with governments and corporations propel solar energy into mainstream awareness. By pushing technological boundaries, expanding global reach, and spearheading industry trends, these top solar module companies are meeting market demands and shaping the trajectory of the entire renewable energy sector.

The report has provided a comprehensive analysis of the competitive landscape in the solar module market. Detailed profiles of all major companies have also been provided.

- Canadian Solar

- DelSolar Co. Ltd.

- First Solar Inc.

- GCL System Integration Technology Co. Ltd.

- Hanwha Group

- JinkoSolar Holding Co. Ltd.

- Kyocera Corporation

- REC Solar Holdings AS (Reliance New Energy Solar Limited)

- The Solaria Corporation

- Trina Solar Co. Ltd.

Solar Module Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Technologies Covered |

|

| Connectivities Covered | On-grid, Off-grid |

| Mountings Covered | Ground Mounted, Roof Top |

| End Users Covered | Residential, Commercial, Utility |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Canadian Solar, DelSolar Co. Ltd., First Solar Inc., GCL System Integration Technology Co. Ltd., Hanwha Group, JinkoSolar Holding Co. Ltd., Kyocera Corporation, REC Solar Holdings AS (Reliance New Energy Solar Limited), The Solaria Corporation, Trina Solar Co. Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the global solar module market performed so far, and how will it perform in the coming years?

- What are the drivers, restraints, and opportunities in the global solar module market?

- What is the impact of each driver, restraint, and opportunity on the global solar module market?

- What are the key regional markets?

- Which countries represent the most attractive solar module market?

- What is the breakup of the market based on the technology?

- Which is the most attractive technology in the global solar module market?

- What is the breakup of the market based on the connectivity?

- Which is the most attractive connectivity in the global solar module market?

- What is the breakup of the market based on the mounting?

- Which is the most attractive mounting in the global solar module market?

- What is the breakup of the market based on the end user?

- Which is the most attractive end user in the global solar module market?

- What is the competitive structure of the global solar module market?

- Who are the key players/companies in the global solar module market?

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the solar module market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global solar module market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the solar module industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)