South Africa Craft Beer Market Size, Share, Trends and Forecast by Product Type, Age Group, Distribution Channel, and Province, 2026-2034

South Africa Craft Beer Market Overview:

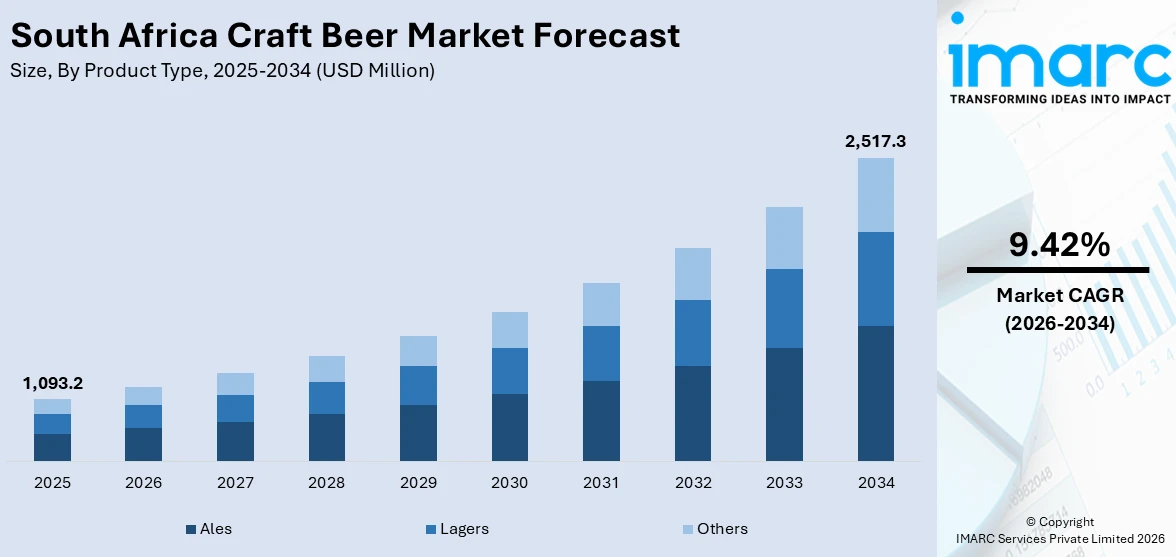

The South Africa craft beer market size reached USD 1,093.2 Million in 2025. Looking forward, the market is expected to reach USD 2,517.3 Million by 2034, exhibiting a growth rate (CAGR) of 9.42% during 2026-2034. The market is expanding steadily, driven by a rise in microbreweries, demand for unique local flavors, and growing interest in artisanal, community-based experiences. Health-conscious options and tourism-focused events are also boosting visibility. These combined trends are contributing to the continued growth of the South Africa craft beer market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 1,093.2 Million |

| Market Forecast in 2034 | USD 2,517.3 Million |

| Market Growth Rate 2026-2034 | 9.42% |

South Africa Craft Beer Market Trends:

Demand for Distinctive Flavors and Local Craftsmanship

South African consumers are increasingly drawn to beers that reflect creativity, authenticity, and regional identity. Unlike mass-produced lagers, craft breweries focus on bold, distinctive flavors using local ingredients like rooibos, fynbos, and indigenous fruits. This commitment to unique taste profiles allows brewers to offer products that are both culturally rooted and innovative. As consumers become more knowledgeable and adventurous, their preference shifts toward small-batch, hand-crafted beers with richer character and complexity. The rise in appreciation for authenticity and traceability has made storytelling and origin key to consumer loyalty. In this environment, quality and craftsmanship are not just selling points—they’re expectations. This evolving palate is helping South African craft brewers carve out a strong niche, while also elevating the image of beer as a premium, artisanal product.

To get more information on this market Request Sample

Growth of Microbreweries and Experiential Consumption

The growth of microbreweries in South Africa has significantly contributed to the craft beer environment. The local microbreweries are attracting community-focused venues with taprooms, beer tastings, and local beer festivals. Another trend has been the adoption of the world of town lively, Cape Town and Johannesburg, as well as growing rural hotspots, have accepted the culture of experience consumption where beer is grouped not only as a product but also as a social image. People are attracted by the opportunity to have direct contact with the brewers, taste exclusive products, and make purchases in local institutions. This direct engagement strengthens brand loyalty and educates drinkers about flavor profiles and brewing methods. Additionally, craft beer tourism is becoming a niche attraction, supporting local economies and increasing visibility. These social and experiential elements are vital to the South Africa craft beer market growth.

Regulatory Support and Shifting Health Preferences

Favorable policy shifts and evolving consumer health consciousness are key enablers of South Africa’s craft beer market growth. Government initiatives, including tax relief and relaxed licensing conditions for small brewers, have made it more feasible for entrepreneurs to enter and compete in the market. This has encouraged innovation and allowed for greater diversity in product offerings. Simultaneously, health-aware consumers are looking for low-alcohol or alcohol-free alternatives that still deliver flavor and quality. Craft brewers are responding with lighter brews, often made from organic or locally sourced ingredients. This dual trend—regulatory encouragement and health-conscious demand—is expanding the appeal of craft beer beyond traditional consumers. By aligning with wellness values and maintaining premium standards, South African brewers are capturing new segments and fostering long-term market resilience.

South Africa Craft Beer Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country and regional levels for 2026-2034. Our report has categorized the market based on product type, age group, and distribution channel.

Product Type Insights:

- Ales

- Lagers

- Others

The report has provided a detailed breakup and analysis of the market based on the product type. This includes ales, lagers, and others.

Age Group Insights:

- 21–35 Years Old

- 40–54 Years Old

- 55 Years and Above

A detailed breakup and analysis of the market based on the age group have also been provided in the report. This includes 21–35 years old, 40–54 years old, and 55 years and above.

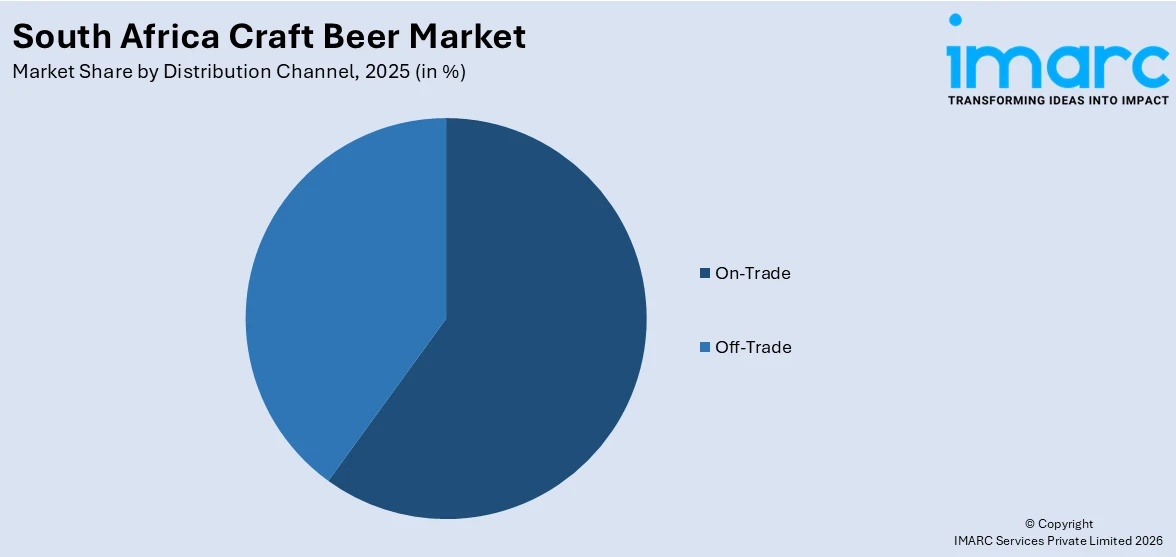

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- On-Trade

- Off-Trade

A detailed breakup and analysis of the market based on the distribution channel have also been provided in the report. This includes on-trade and off-trade.

Province Insights:

- Gauteng

- KwaZulu-Natal

- Western Cape

- Mpumalanga

- Eastern Cape

- Others

The report has also provided a comprehensive analysis of all the major regional markets, which include Gauteng, KwaZulu-Natal, Western Cape, Mpumalanga, Eastern Cape, and others.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

South Africa Craft Beer Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Ales, Lagers, Others |

| Age Groups Covered | 21–35 Years Old, 40–54 Years Old, 55 Years and Above |

| Distribution Channels Covered | On-Trade, Off-Trade |

| Provinces Covered | Gauteng, KwaZulu-Natal, Western Cape, Mpumalanga, Eastern Cape, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the South Africa craft beer market performed so far and how will it perform in the coming years?

- What is the breakup of the South Africa craft beer market on the basis of product type?

- What is the breakup of the South Africa craft beer market on the basis of age group?

- What is the breakup of the South Africa craft beer market on the basis of distribution channel?

- What is the breakup of the South Africa craft beer market on the basis of province?

- What are the various stages in the value chain of the South Africa craft beer market?

- What are the key driving factors and challenges in the South Africa craft beer market?

- What is the structure of the South Africa craft beer market and who are the key players?

- What is the degree of competition in the South Africa craft beer market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the South Africa craft beer market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the South Africa craft beer market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the South Africa craft beer industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade