South East Asia Data Center Market Size, Share, Trends and Forecast by Component, Type, Enterprise Size, End User, and Country, 2026-2034

South East Asia Data Center Market Size, Share, Trends & Forecast (2026-2034)

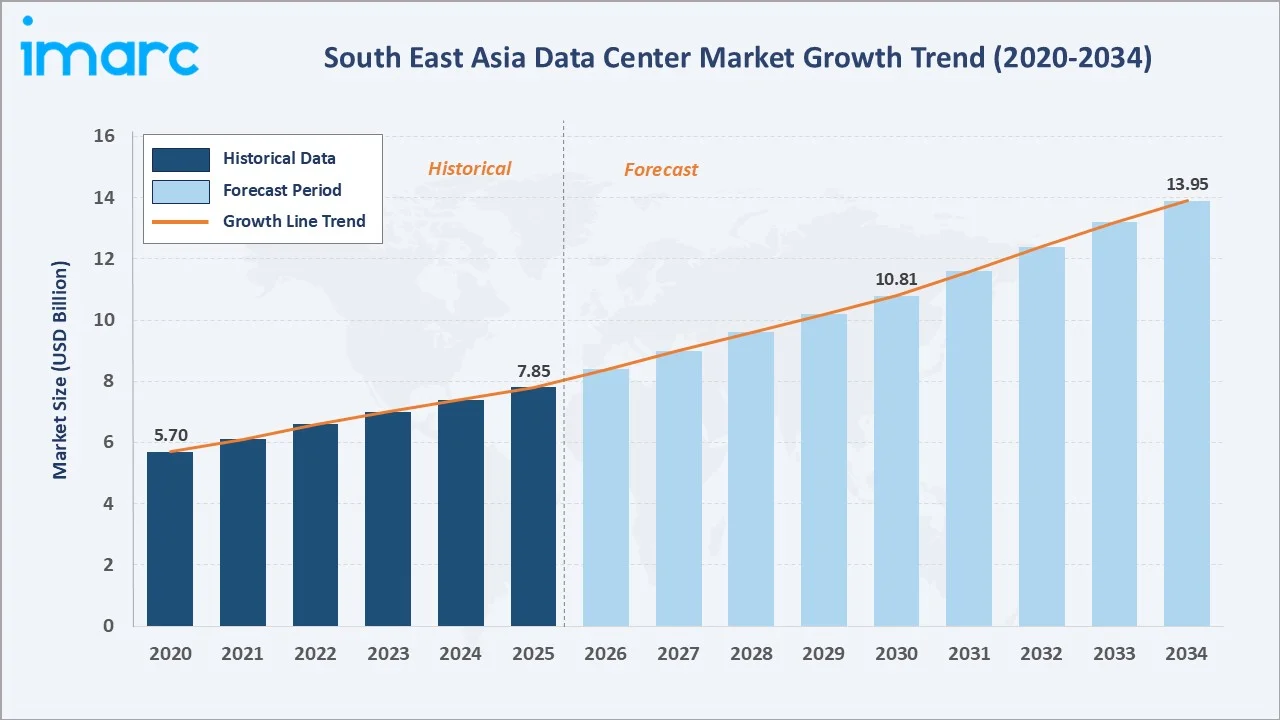

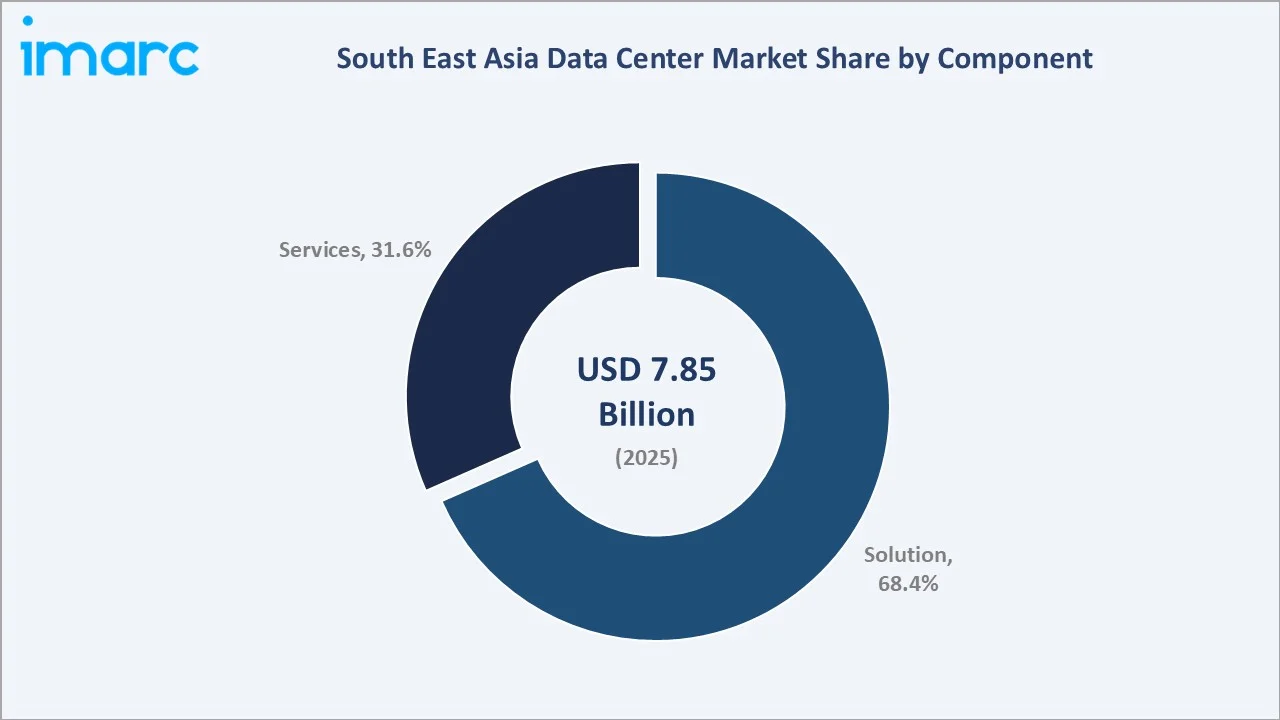

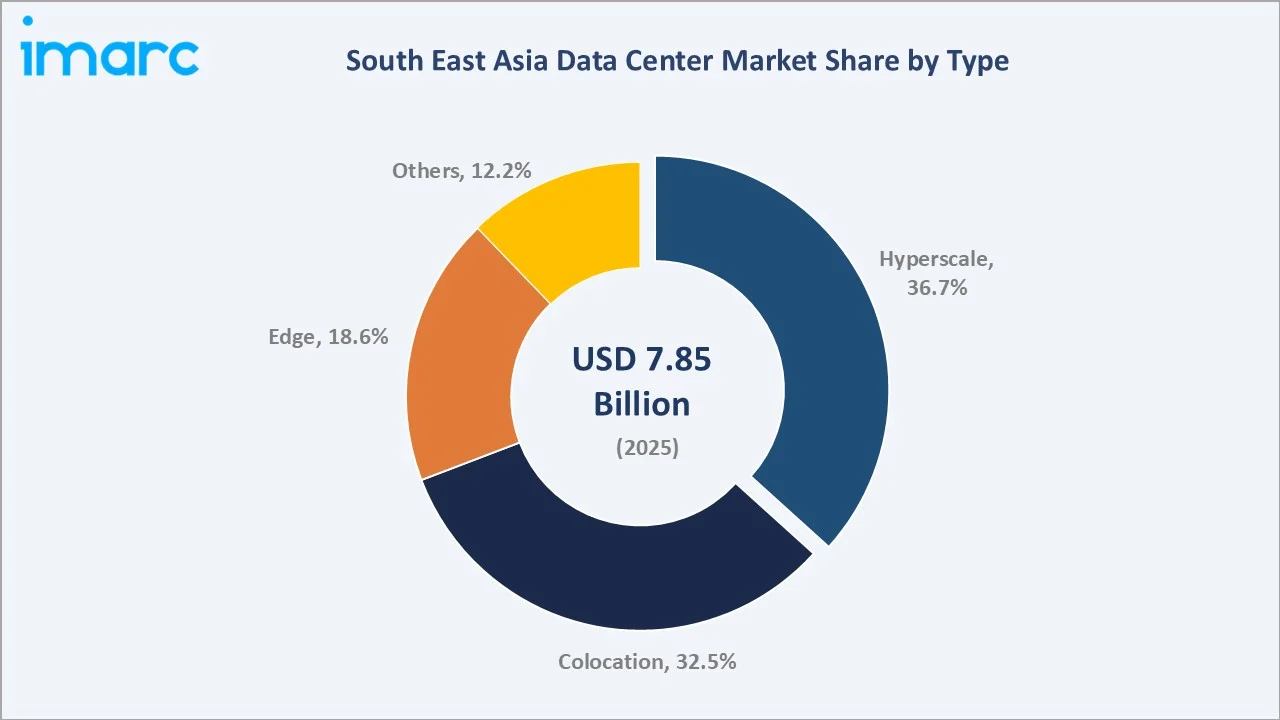

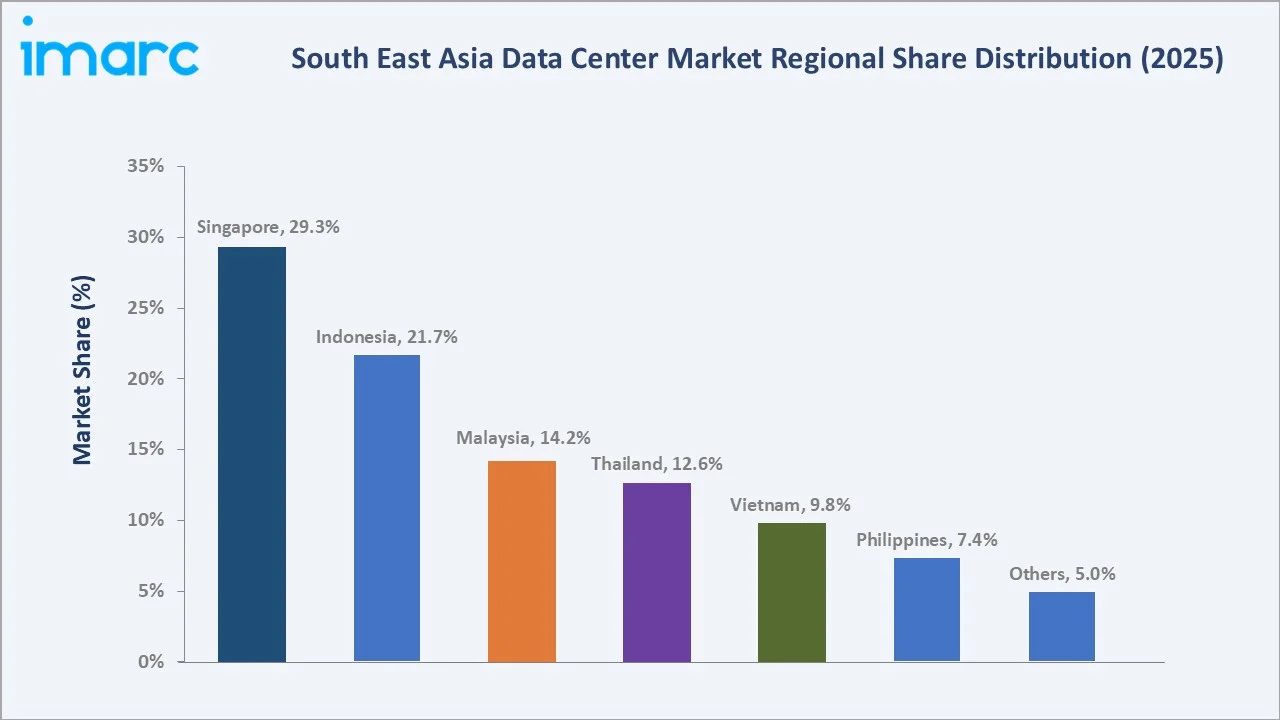

The South East Asia data center market reached USD 7.85 Billion in 2025 and is projected to reach USD 13.95 Billion by 2034, growing at a CAGR of 6.60% during 2026-2034. Southeast Asia's digital economy targeting USD 1 Trillion by 2030, generative AI GPU workload demand, government data sovereignty mandates creating localized demand, and digitally connected consumers anchor the market's robust growth. Solution dominates at 68.4%. Hyperscale leads at 36.7%. Singapore commands 29.3% of the regional market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 7.85 Billion |

|

Forecast Market Size (2034) |

USD 13.95 Billion |

|

CAGR (2026-2034) |

6.60% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Component |

Solution (68.4%, 2025) |

|

Dominant Type |

Hyperscale (36.7%, 2025) |

|

Leading Country |

Singapore (29.3%, 2025) |

The market expanded from USD 5.70 Billion in 2020 to USD 7.85 Billion in 2025, anchored at USD 10.81 Billion in 2030, and forecast to reach USD 13.95 Billion by 2034. COVID-19 was the market's defining catalyst, accelerating digital adoption by consumers, enterprises, and governments, who migrated operations to cloud-based platforms simultaneously, creating unprecedented data center demand that has sustained well beyond the pandemic through structural behavioral and enterprise IT architecture changes favoring cloud-first deployments over on-premises infrastructure.

To get more information on this market, Request Sample

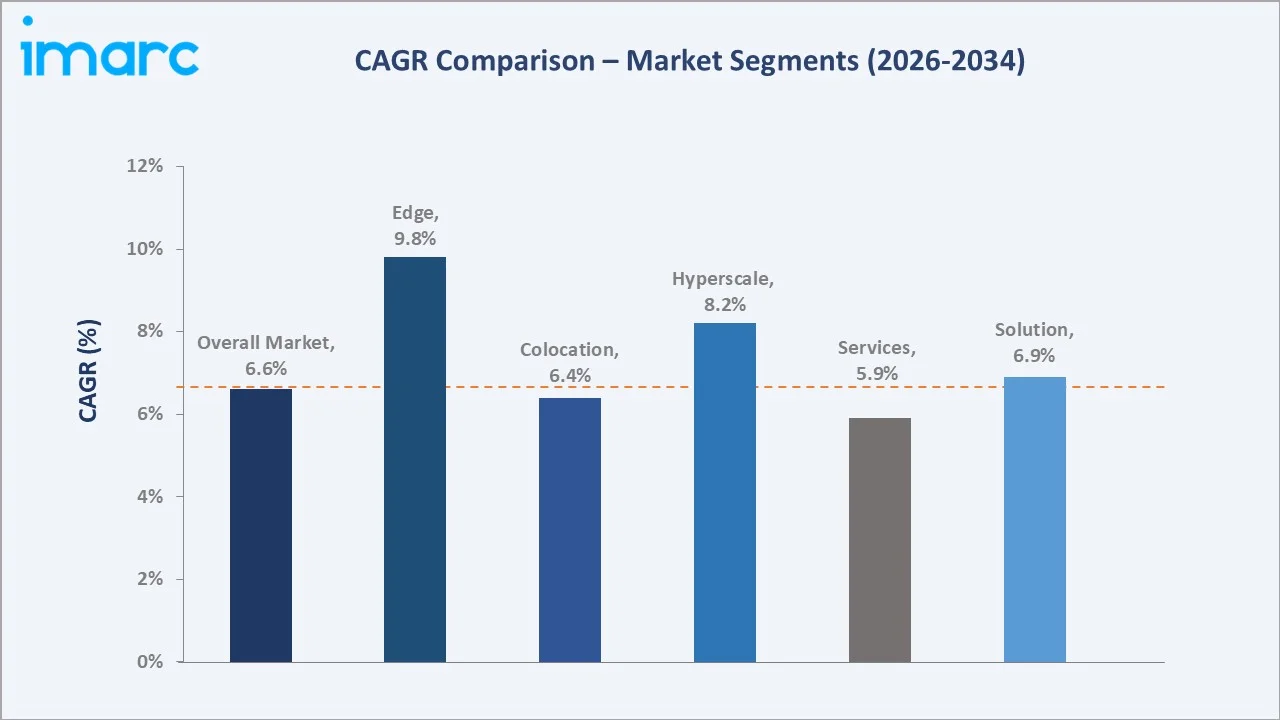

Edge data centers grow fastest at ~9.8% CAGR as 5G network rollout across Singapore, Indonesia, Malaysia, Thailand, and Vietnam creates connectivity infrastructure enabling ultra-low latency applications requiring data processing within less time rather than central data centers. Solution component grows at ~6.9% CAGR driven by hyperscaler hardware investment.

Executive Summary

The South East Asia data center market reached USD 7.85 Billion in 2025, representing one of the world's fastest-growing digital infrastructure markets and the most strategically contested data center geography in the Asia Pacific. Southeast Asia's data center ecosystem sits at the convergence of three global macro trends: the hyperscaler cloud expansion race to establish regional dominance; the artificial intelligence infrastructure buildout requiring GPU clusters most cost-effectively deployed in purpose-built data centers with high-density cooling and renewable energy access; and data sovereignty regulation across all major SEA nations requiring in-country data storage that mandates new data center construction even for workloads that would otherwise be centralized in Singapore. The market is projected to reach USD 13.95 Billion by 2034 at 6.60% CAGR.

Solution at 68.4% dominates as data center hardware investment constitutes the largest capital expenditure component of data center construction. Hyperscale at 36.7% leads the type segment as AWS, Microsoft Azure, Google Cloud, and Alibaba Cloud construct purpose-built campus facilities across Singapore, Indonesia, Malaysia, Thailand, and the Philippines to serve the region's cloud-first enterprise market. Singapore, at 29.3%, leads as ASEAN's technology hub.

Key Market Insights

|

Insight |

Data |

|

Dominant Component |

Solution - 68.4% share (2025) |

|

Dominant Type |

Hyperscale - 36.7% market share (2025) |

|

Leading Country |

Singapore - 29.3% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- Solution at 68.4% reflecting the capital-intensive nature of data center hardware in a market building new capacity from the ground up: Southeast Asia's data center market is predominantly in the construction and capacity expansion phase, with national hyperscalers collectively building new capacity across SEA, each requiring high solution investments.

- Hyperscale at 36.7% anchored by cloud investment across the six primary SEA data center markets: The hyperscale segment's leading share reflects the scale of AWS, Microsoft, Google, and Alibaba's regional infrastructure investment.

- Singapore at 29.3% reflecting structural advantages that sustain hyperscaler preference despite moratorium and land constraints: Despite facing land scarcity, Singapore retains its leading share through continued expansion of existing campus facilities within approved footprints.

South East Asia Data Center Market Overview

The Southeast Asia data center market encompasses all commercial data center infrastructure providing space, power, cooling, and connectivity for IT equipment across colocation, hyperscale, edge, and enterprise-owned categories. The market spans the ASEAN region's six primary digital economies: Singapore as the established hub, Indonesia as the largest emerging market, Malaysia as the hyperscale challenger, Thailand as the mainland SEA gateway, Vietnam as the fastest-growing frontier, and the Philippines as the BPO-driven demand anchor.

The ecosystem integrates global hyperscalers, specialized data center REITs and developers, technology infrastructure suppliers, connectivity providers operating subsea cables connecting SEA hubs, professional services firms for data center engineering, and government digital agencies. Macroeconomic factors include rapid digitalization, rising internet and smartphone penetration, expanding cloud adoption, and strong growth in AI, e-commerce, fintech, and streaming services.

Market Dynamics

To evaluate market opportunities, Request Sample

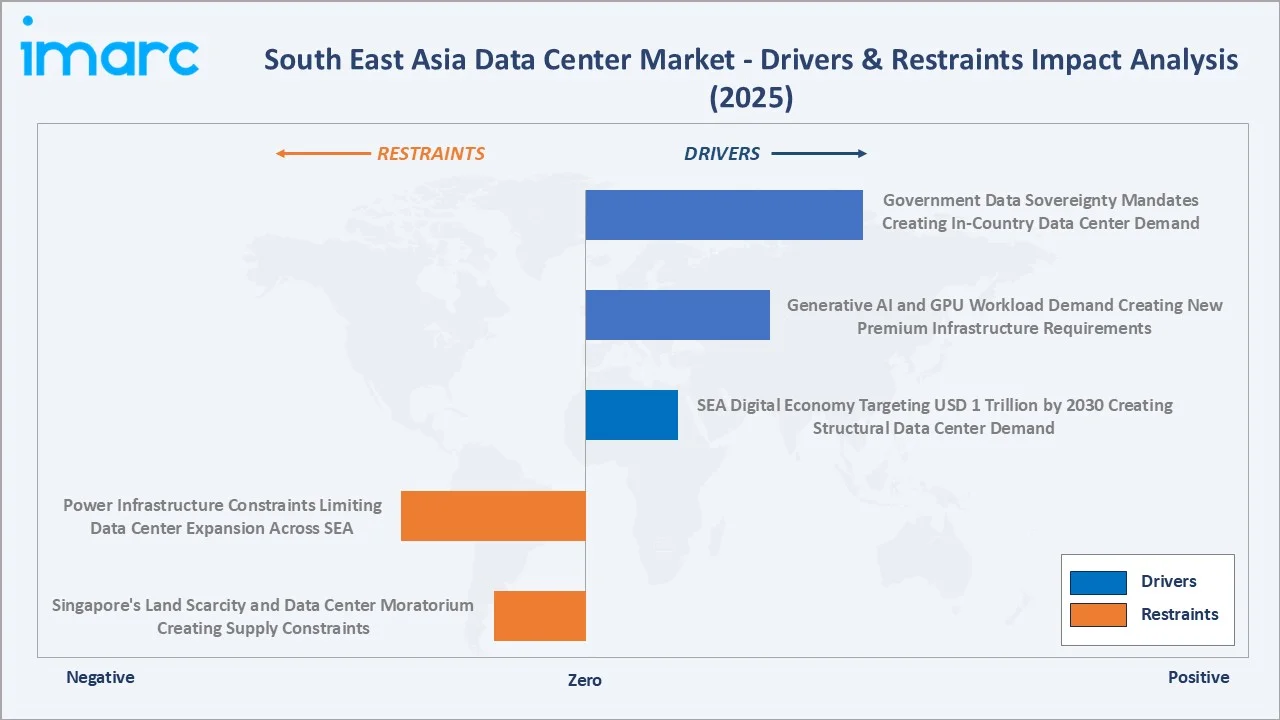

Market Drivers

- SEA Digital Economy Targeting USD 1 Trillion by 2030, Creating Structural Data Center Demand: Southeast Asia’s push toward building a digital economy valued at nearly USD 1 trillion by 2030 is creating strong long-term demand for data center infrastructure across the region. Rapid growth in cloud computing, e-commerce, AI workloads, digital payments, streaming platforms, and enterprise digital transformation is increasing the need for large-scale data storage and processing capacity. This expansion is encouraging hyperscale operators, colocation providers, and global technology firms to invest heavily in regional data center development.

- Generative AI and GPU Workload Demand Creating New Premium Infrastructure Requirements: GenAI infrastructure has created a new data center specification category requiring advanced liquid cooling and power densities previously unseen in commercial colocation. AWS, Microsoft Azure, Google Cloud, and specialized AI infrastructure providers are constructing dedicated GPU data centers in Singapore and Malaysia to serve the AI startup ecosystem and enterprise AI adoption.

- Government Data Sovereignty Mandates Creating In-Country Data Center Demand: Government data sovereignty mandates across Southeast Asia are driving demand by requiring sensitive public, financial, and enterprise data to be stored and processed locally. Regulations related to cybersecurity, digital governance, and personal data protection are encouraging enterprises and cloud providers to establish regional hosting infrastructure within national borders. These policies are accelerating investments in hyperscale and colocation facilities across key markets such as Singapore, Indonesia, Malaysia, Thailand, and Vietnam.

Market Restraints

- Power Infrastructure Constraints Limiting Data Center Expansion in Indonesia, Vietnam, and the Philippines: Limited electricity generation capacity, grid instability, and delays in transmission infrastructure development are creating operational challenges for large-scale facility deployments across several Southeast Asian countries. Rising power demand from hyperscale operators is increasing pressure on national utilities, leading to concerns regarding reliable energy availability and project approval timelines. High dependence on fossil-fuel-based grids and insufficient renewable integration are also affecting long-term sustainability and expansion plans for operators in the region.

- Singapore's Land Scarcity and Data Center Moratorium Legacy Creating Supply Constraints: Singapore's limited 728 sq.km. land area restricts large-scale data center construction, increasing land acquisition costs and limiting future capacity expansion opportunities in the regional market. While existing campus expansions continue, new entrant data center developers face long approval timelines with uncertain outcomes.

Market Opportunities

- Johor Bahru-Batam-Bintan Cluster as Singapore's Cost-Effective Extension Market: Malaysia's Johor Bahru and Indonesia's Batam, which is near Singapore, offer Singapore-equivalent fiber connectivity at 60-70% lower land and power costs, enabling data center economics impossible within Singapore's constrained market.

- Green Data Center Certification Creating Premium Revenue Tier: Hyperscaler sustainability commitments require their data center providers to achieve specific renewable energy and efficiency standards. Data centers achieving Tier III+ certification with high renewable energy supply command premium pricing versus non-certified equivalents in Singapore and Malaysia's competitive colocation markets, creating revenue incentive for green infrastructure investment that aligns with hyperscaler procurement requirements.

Market Challenges

- Multi-Country Regulatory Compliance Creating Operational Complexity for Regional Operators: A data center operator with facilities across Singapore, Indonesia, Malaysia, Thailand, Vietnam, and the Philippines must comply with 6 different data protection laws, 6 different telecommunications regulations, 6 different building and fire safety codes, and multiple sector-specific regulations for BFSI clients. This regulatory matrix adds 2-3 months per country to new data center commissioning timelines and high ongoing compliance costs for large operators, creating structural advantages for large operators with scale to amortize compliance costs across large revenue bases.

- Subsea Cable Capacity Constraints Creating Latency and Bandwidth Challenges for Edge Markets: Southeast Asia's international connectivity depends on active subsea cable systems converging on Singapore. Secondary SEA markets face cable capacity constraints, with Vietnam's international bandwidth experiencing congestion events following damage to the Asia Pacific Gateway cable, causing a 30-50% international bandwidth reduction for weeks.

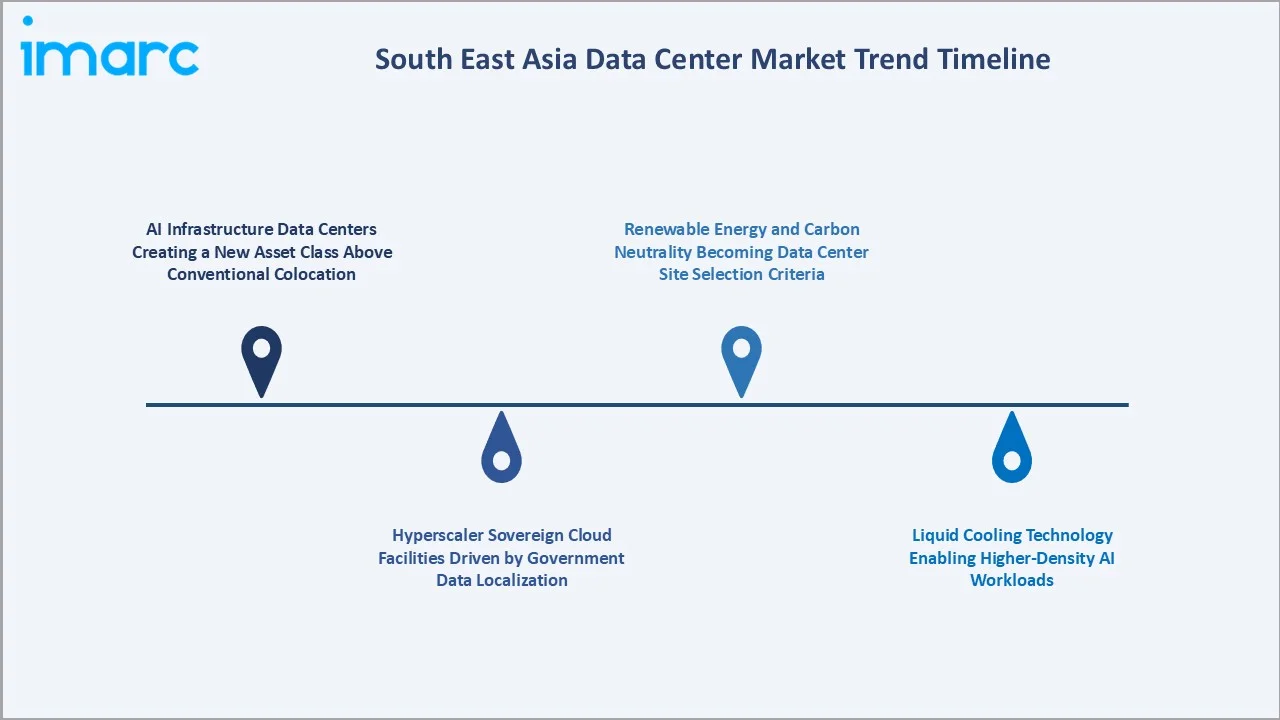

Emerging Market Trends

1. AI Infrastructure Data Centers Creating a New Asset Class Above Conventional Colocation

AI infrastructure data centers are emerging as a premium asset class in Southeast Asia due to rising demand for high-density computing, GPU clusters, liquid cooling systems, and low-latency AI processing capabilities. In April 2026, ST Telemedia Global Data Centres partnered with SuperX AI Technology to establish an AI Innovation Center in Singapore focused on accelerating enterprise AI adoption by overcoming infrastructure limitations. Situated at STT GDC’s Singapore 5 facility, the center offers a dedicated platform for enterprises to scale AI initiatives from pilot testing to full production deployment.

2. Hyperscaler Sovereign Cloud Facilities Driven by Government Data Localization

Hyperscaler sovereign cloud facilities are emerging rapidly as governments strengthen data localization, cybersecurity, and digital sovereignty regulations. Global cloud providers are increasingly establishing country-specific cloud and data center infrastructure to comply with local data storage and processing requirements. This trend is driving partnerships between hyperscalers, telecom operators, and regional data center providers to develop secure, compliant, and low-latency cloud environments for enterprises and public sector organizations.

3. Liquid Cooling Technology Enabling Higher-Density AI Workloads

Liquid cooling technology supports high-density AI and accelerated computing workloads with greater thermal efficiency. Compared to traditional air-cooling systems, liquid cooling enables operators to manage rising rack power densities while reducing energy consumption and cooling costs. The technology is gaining adoption among hyperscale and AI-focused facilities seeking improved performance, sustainability, and operational reliability.

4. Renewable Energy and Carbon Neutrality Becoming Data Center Site Selection Criteria

Renewable energy availability and carbon neutrality goals are becoming critical site selection factors for data center investments across Southeast Asia. Hyperscale operators and colocation providers are increasingly prioritizing locations with access to clean energy, stable power infrastructure, and supportive sustainability policies to meet corporate ESG commitments. This trend is encouraging greater integration of solar, wind, hydropower, and energy-efficient technologies into new data center developments across the region.

Industry Value Chain Analysis

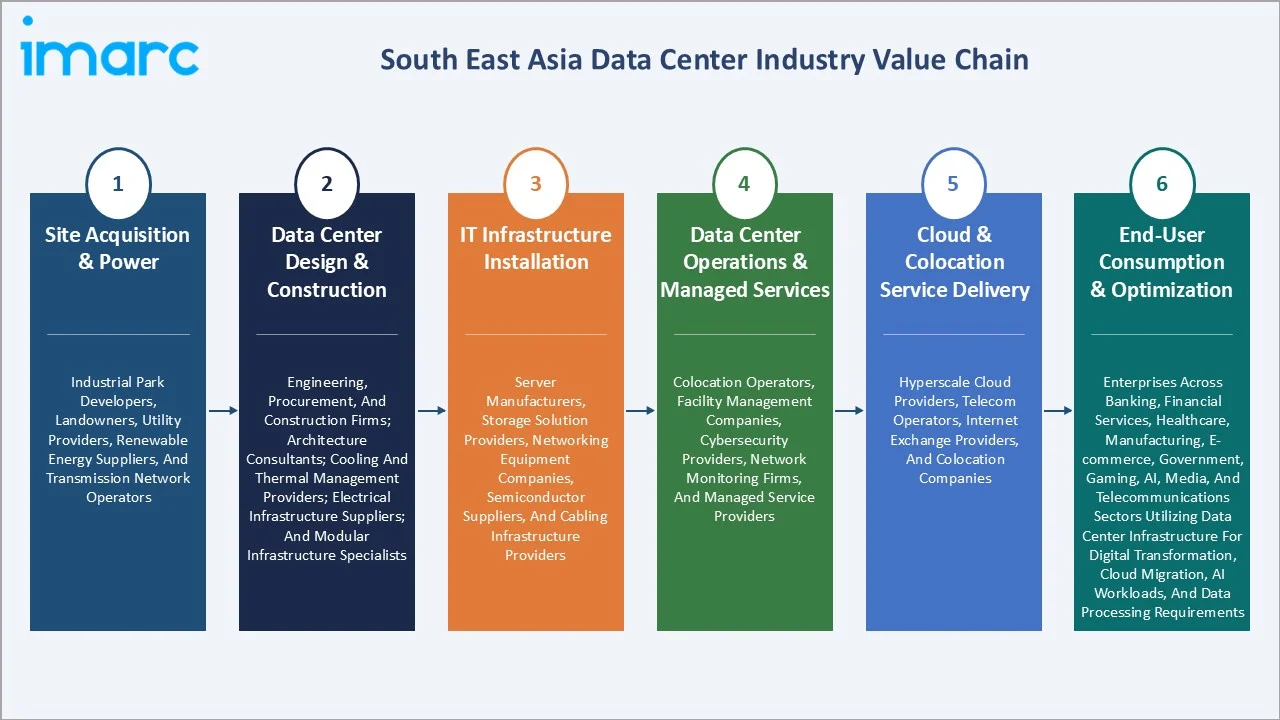

South East Asia's data center value chain integrates site acquisition and power procurement, physical data center design and construction, IT hardware installation, ongoing operations and managed services, cloud and colocation service delivery, and end-user consumption. Facility operators earn colocation revenue of USD 8-20/kW/month for standard space and USD 20-40/kW/month for high-density AI clusters. Construction contractors earn AUD 500,000-2 Million per MW of new capacity built. IT hardware manufacturers earn product margins of 20-35% on data center hardware. Managed service providers earn 15-25% margins on managed hosting services delivered above physical colocation.

|

Stage |

Key Participants |

|

Site Acquisition & Power |

Industrial park developers, landowners, utility providers, renewable energy suppliers, and transmission network operators. |

|

Data Center Design & Construction |

Engineering, procurement, and construction firms; architecture consultants; cooling and thermal management providers; electrical infrastructure suppliers; and modular infrastructure specialists. |

|

IT Infrastructure Installation |

Server manufacturers, storage solution providers, networking equipment companies, semiconductor suppliers, and cabling infrastructure providers. |

|

Data Center Operations & Managed Services |

Colocation operators, facility management companies, cybersecurity providers, network monitoring firms, and managed service providers. |

|

Cloud & Colocation Service Delivery |

Hyperscale cloud providers, telecom operators, internet exchange providers, and colocation companies. |

|

End-User Consumption & Optimization |

Enterprises across banking, financial services, healthcare, manufacturing, e-commerce, government, gaming, AI, media, and telecommunications sectors utilizing data center infrastructure for digital transformation, cloud migration, AI workloads, and data processing requirements. |

The cloud and colocation service delivery tier is the value chain's highest revenue concentration point. AWS, Microsoft Azure, and Google Cloud represent 50%+ of the data center market's total revenue from a single tier. This concentration demonstrates that cloud services revenue dwarfs the physical infrastructure revenue in the market's current development phase, implying that the physical data center market will grow proportionally to cloud services adoption even as cloud services revenue grows faster than infrastructure revenue per unit.

Technology Landscape in the South East Asia Data Center Industry

Power Infrastructure and UPS Systems

Advanced power infrastructure and UPS systems are ensuring uninterrupted operations and improving energy reliability for high-density computing environments. Operators are increasingly deploying modular UPS systems, lithium-ion battery backup solutions, intelligent power distribution units, and redundant power architectures to minimize downtime risks. These technologies are also supporting hyperscale expansion, AI workloads, and energy-efficient facility operations across the region.

Cooling Technology for Tropical Climate Data Centers

Southeast Asia's tropical climate at 28-35 degrees Celsius ambient and 70-90% relative humidity creates unique cooling challenges, increasing cooling energy's share of total data center power to 35-45% versus 25-30% in temperate climates. In November 2023, a new facility aimed at accelerating the testing and adoption of sustainable cooling technologies for data centers in tropical environments was officially launched at the National University of Singapore (NUS). Known as the Sustainable Tropical Data Centre Testbed (STDCT), the full-scale living laboratory supports a national research initiative led by NUS and Nanyang Technological University in collaboration with industry stakeholders, with a focus on advancing innovative cooling solutions and sustainability standards for tropical-climate data centers.

Network Connectivity and Internet Exchange Infrastructure

Network connectivity and internet exchange infrastructure enable low-latency data transmission and high-speed regional connectivity. Growing investments in submarine cables, fiber-optic networks, carrier-neutral facilities, and internet exchange points are improving cross-border data flow and cloud service performance. These technologies are supporting hyperscale expansion, AI applications, digital services, and rising enterprise demand for reliable connectivity across the region.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

Solution |

68.4% |

2025 |

|

Type |

Hyperscale |

36.7% |

2025 |

|

Enterprise Size |

🔒 |

🔒 |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Country |

Singapore |

29.3% |

2025 |

By Component

Solution leads at 68.4% market share (2025). The solution component encompasses all physical data center infrastructure: IT hardware including servers, storage, and networking equipment; power infrastructure including UPS, generators, PDUs, and transformers; cooling systems including CRAC/CRAH units, cooling towers, chillers, and liquid cooling; physical security; and the data center facility structure itself.

To access detailed market analysis, Request Sample

Services at 31.6% encompasses managed hosting, professional services including design consulting and migration, facility management, and IT support. Services grow at ~5.9% CAGR as the market transitions from the construction phase to the operations phase over the forecast period.

By Type

Hyperscale leads at 36.7% market share (2025). Hyperscale data centers are purpose-built facilities of 20-1,000 MW designed for a single or a few anchor tenants, typically cloud providers. AWS's Singapore, Microsoft Azure's Singapore, and Google Cloud's Singapore collectively represent high hyperscale infrastructure investment in SEA. Each hyperscale campus generates high annual revenue from the cloud services it enables, captured by the hyperscaler operating its cloud services.

Colocation at 32.5% is the revenue model for charging enterprise and cloud customers for dedicated space, power, cooling, and connectivity within shared facilities. Edge at 18.6% grows fastest at ~9.8% CAGR through 5G enablement and digital economy geographic expansion beyond Tier-1 SEA cities. Others at 12.2% covers enterprise-owned private data centers, government data centers, and hosted dedicated server environments.

Regional Market Insights

|

Country |

Share (2025) |

Key Data Center Growth Drivers & Characteristics |

|

Singapore |

29.3% |

Advanced digital infrastructure, strong international connectivity, stable regulatory environment, and presence of major hyperscale cloud providers. |

|

Indonesia |

21.7% |

Driven by its large population base, rapid internet penetration, expanding digital economy, and rising cloud adoption among enterprises and government institutions. |

|

Malaysia |

14.2% |

Supported by lower operating costs, improving power infrastructure, government incentives, and proximity to Singapore. |

|

Thailand |

12.6% |

Supported by rising enterprise digital transformation, smart city initiatives, cloud computing adoption, and government-led digital economy development programs. |

|

Vietnam |

9.8% |

Increasing digital service consumption, rising internet users, expanding manufacturing activity, and supportive government digitalization policies. |

|

Philippines |

7.4% |

Driven by growing demand for cloud services, business process outsourcing operations, digital banking, and rising internet usage. |

|

Others |

5.0% |

Other Southeast Asian markets are gradually expanding their data center infrastructure through growing digital economy initiatives, improving connectivity, rising enterprise cloud adoption, and increasing investments in localized data storage capabilities. |

Singapore's 29.3% leadership despite representing less land area and its population reflects the extraordinary revenue density of the world's most connected city-state's data center ecosystem. Singapore's internet exchange processes more traffic than any other Asian exchange point outside Japan, its colocation premium at USD 15-25/kW/month exceeds comparable APAC facilities by 20-40%, and its hyperscaler investment density committed by AWS, Microsoft, Google, and Alibaba combined creates Asia's highest absolute data center investment concentration per square kilometer.

Indonesia's 21.7% and its structural growth trajectory make it the market's most important long-term growth opportunity. Malaysia's 14.2% understates its strategic importance given Johor's emergence as the region's primary hyperscale campus zone. Vietnam's 9.8% represents the fastest per-capita growth trajectory. Thailand's 12.6% reflects active data center investment promotion, and the Philippines' 7.4% anchors its BPO-sector-driven demand model.

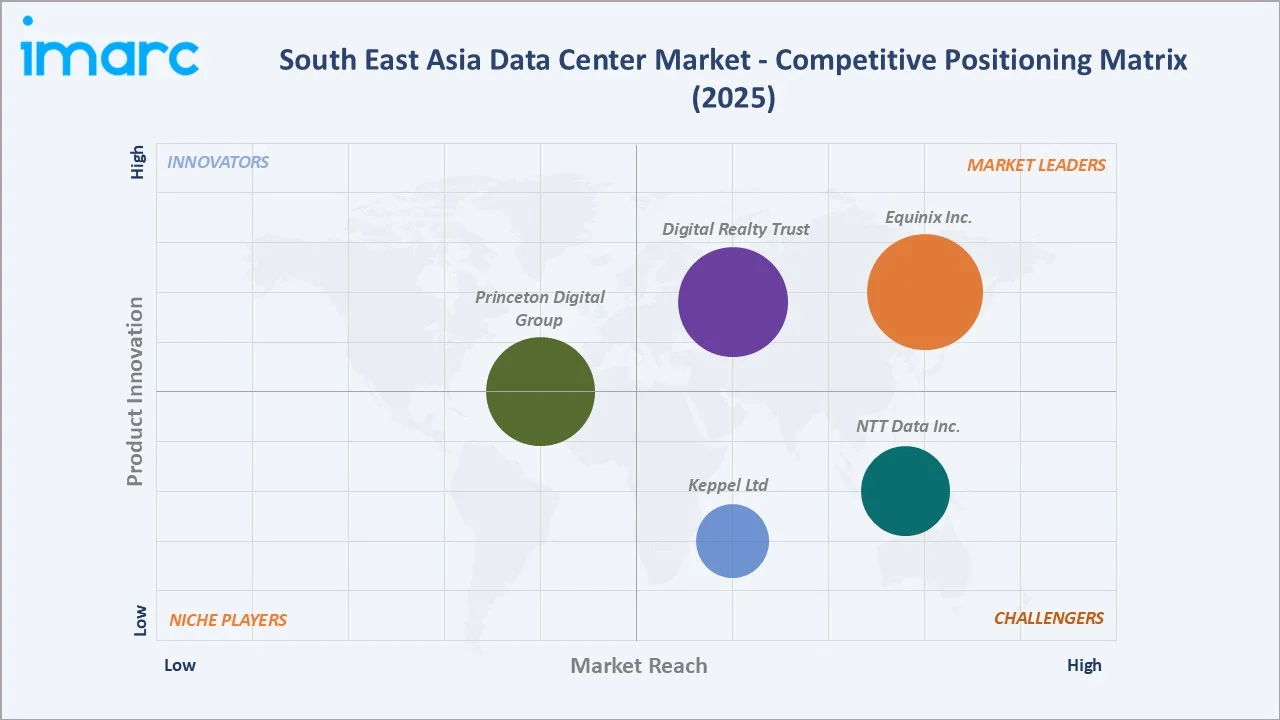

Competitive Landscape

Southeast Asia's data center market exhibits a bifurcated competitive structure: high concentration among global colocation REITs with Equinix and Digital Realty together commanding 25-30% of colocation revenue, and moderate concentration among hyperscale campus developers, including NTT Data Inc., Keppel, Princeton Digital, and others competing for hyperscaler anchor tenants.

|

Company Name |

Data Center Facilities |

Market Position |

Core Strength |

|

Equinix Inc. |

SG1-SG5 (Singapore), JK1 (Indonesia), Johor, Kuala Lumpur (Malaysia), Manila (Philippines) |

Market Leader |

Equinix colocation brings AI within milliseconds of the data, so performance stays high, and latency stays low. |

|

Digital Realty Trust |

Jakarta CGK10, Jakarta CGK11, Singapore SIN10, Singapore SIN11, Singapore SIN12 |

Market Leader |

Backed by long-standing expertise, future-forward design, and a global partner ecosystem, Digital Realty accelerate innovation across industries. |

|

NTT Data Inc. |

Jakarta 2, Jakarta 3, Cyberjaya 4, Cyberjaya 5, Serangoon, Bangkok 1, Bangkok 2, Ho Chi Minh City 1 |

Strong Challenger |

NTT Data offer local-to-global data center expertise, aligned with their connected platform of AI-ready data centers to create solutions that enable clients to seamlessly scale their digital businesses, anywhere and anytime. |

|

Keppel Ltd |

Keppel DC Singapore 1 to 8, IndoKeppel Data Centre 1, Keppel DC Johor 1 |

Strong Challenger |

Keppel is a trusted partner delivering wholesale, build-to-suit and hyperscale facilities for the IT workloads of leading cloud and digital enterprises. |

|

Princeton Digital Group |

Singapore - SG1, SG3, Johor - JH1, Johor - JH2, Greater Jakarta - JC1, JC2 |

Established Player |

Leading Pan-Asia data center platform with scalable, sustainable and standardized AI-ready infrastructure |

The competitive landscape is being reshaped by Chinese capital backing new entrants competing with US REITs for the same hyperscaler anchor tenant relationships; national operators leveraging government relationships to win sovereign cloud contracts unavailable to international operators; and the Johor-Batam cluster's emergence, creating a new competitive arena where all major operators simultaneously seek to establish first-mover advantage in Asia's most dynamic new hyperscale market.

Key Company Profiles

Equinix Inc.

Equinix is the world's largest data center company by revenue and market capitalization, operating as a data center REIT with a huge number of facilities globally.

- Data Center Facilities: SG1-SG5 (Singapore), JK1 (Indonesia), Johor, Kuala Lumpur (Malaysia), Manila (Philippines).

- Recent Developments: In November 2024, Equinix announced its sixth data center in Singapore, which will be built with an initial investment of USD260 million. This new facility, set to open in Q1 2027, will offer 20MW of power upon completion.

- Strategic Focus: Expanding carrier-neutral colocation, interconnection, and hyperscale-ready digital infrastructure capabilities to support rising cloud, AI, and enterprise connectivity demand across Southeast Asia.

Digital Realty Trust

Digital Realty Trust is one of the world's largest data center REITs, operating as a global data center platform serving enterprise customers across metro markets with colocation, hyperscale, and interconnection services.

- SEA Facilities: Jakarta CGK10, Jakarta CGK11, Singapore SIN10, Singapore SIN11, Singapore SIN12.

- Recent Developments: In April 2026, Digital Realty is targeting nearly S$7 billion of total investment in Singapore, reinforcing the market's critical role as an AI infrastructure hub for the Asia Pacific, with more than S$4.3 billion planned for new data center developments, building on existing investments.

- Strategic Focus: Focused on expanding hyperscale and colocation data center capacity, strengthening regional interconnection ecosystems, and supporting cloud and AI-driven digital infrastructure demand across Southeast Asia.

Market Concentration Analysis

South East Asia's data center market exhibits moderate concentration at the operator level with high concentration in specific submarkets. In Singapore colocation, Equinix and Digital Realty together command approximately 35-40% of commercial colocation revenue, with NTT Data Inc., Keppel, and Princeton sharing the remaining 60-65%. In hyperscale, AWS, Microsoft Azure, and Google Cloud together account for 70-75% of hyperscale cloud services revenue, though their physical infrastructure is increasingly built through third-party campus developers.

Concentration dynamics are shifting as the Johor-Batam cluster emerges. First-mover operators in Johor with Microsoft, GDS, and Vantage making early campus commitments, and in Batam with PDG, Vantage, and Bridge having first operational facilities, are establishing hyperscaler anchor tenant relationships that create self-reinforcing position advantages. Late entrants to the Johor-Batam market will face higher land costs, longer timelines to operational status, and hyperscaler preference for incumbent operators with an operational track record, suggesting that the 2024-2026 window is the critical period for establishing a competitive position in SEA's next-generation hyperscale cluster.

Investment & Growth Opportunities

Fastest Growing Segments

Edge data centers at ~9.8% CAGR, hyperscale type at ~8.2% CAGR, solution component at ~6.9% CAGR, AI GPU cluster colocation at estimated 30%+ CAGR from small base, Vietnam country market at ~12-15% CAGR from strong digital economy and data localization drivers, and Johor-Batam cluster at 100%+ CAGR from near-zero 2022 base through 2028 represent Southeast Asia's highest-growth data center investment vectors.

Emerging Market Opportunities

Vietnam's data center market represents the most significant greenfield investment opportunity in SEA for 2026-2034, with a high population, 16%+ annual digital economy growth, mandatory government data localization, and current data center penetration at 30-40% of comparable markets, including Malaysia and Thailand. Vietnam offers first-mover advantages for operators establishing Tier III+ certified facilities in Ho Chi Minh City and Hanoi before the market's hyperscale phase accelerates.

Investment Themes

- Hyperscale campus development in Johor-Batam cluster: First-mover operators securing 100-500 MW land parcels with power PPAs and fiber connectivity in Johor Bahru and Batam Island between 2025 and 2027 will capture the hyperscaler anchor tenant relationships that generate 10-15 year revenue certainty.

- Edge data center network development for 5G-enabled SEA cities: Deploying distributed edge data center nodes of 1-5 MW per site within 10 km of population centers in Indonesia's cities including Surabaya, Bandung, and Medan; Thailand's regional cities including Chiang Mai, Phuket, and Khon Kaen; and Vietnam's secondary cities including Da Nang and Can Tho enables edge compute-as-a-service for 5G enterprise applications at USD 20-50/kW versus colocation's USD 8-15/kW for urban premium locations.

Future Market Outlook (2026-2034)

The South East Asia data center market is projected to grow from USD 7.85 Billion in 2025 to USD 13.95 Billion by 2034, delivering a 6.60% CAGR over the forecast period. The market's anchor value of USD 10.81 Billion in 2030 represents a data center industry where the Johor-Batam cluster has emerged as a genuine hyperscale hub rivaling Singapore's existing footprint, AI GPU clusters constitute 15-20% of total data center revenue at premium pricing, and sovereign cloud mandates in Indonesia, Vietnam, Malaysia, and Thailand have created structured institutional data center demand supplementing commercial cloud adoption. The geographic center of gravity of SEA data center investment will have shifted significantly southward from Singapore toward Johor, Batam, and Indonesia's Java island corridor by 2030.

Three structural forces define Southeast Asia's data center market growth through 2034 with high confidence: SEA's digital economy growing to USD 1 Trillion by 2030 requires proportional data center capacity scaling with AI-native applications consuming 3-5x more data center capacity per unit of economic output than previous-generation digital applications; the hyperscaler investment wave's second and third phases with AWS, Microsoft, and Google each announcing multi-country SEA investment programs annually creates physical infrastructure at a pace limited by construction timelines and power utility connections rather than commercial demand; and regulatory data sovereignty requirements in major SEA markets ensure that data center demand is structurally protected from geographic consolidation, sustaining market growth in Vietnam, Indonesia, Thailand, Malaysia, and Philippines independently of Singapore's supply and cost constraints.

Research Methodology

Primary Research

Primary research comprised structured interviews with 65+ industry stakeholders in 2025, including VP Sales and Regional Directors; enterprise IT directors from major SEA BFSI; Singapore IMDA, Indonesia Kominfo, Malaysia MDEC, and Thailand DEPA digital infrastructure program officials; and subsea cable operators providing connectivity intelligence.

Secondary Research

Secondary research encompassed IMDA Singapore Data Center Road Map 2020-2025 and Update 2023; Indonesia Ministry of Communication PDN Program reports; MDEC Malaysia Data Center Policy Framework 2023; Gartner Magic Quadrant for Data Center Outsourcing APAC 2025; IDC Asia Pacific Data Center Market Tracker Q4 2025; JLL Data Center Perspectives Asia Pacific 2025; e-Conomy SEA 2024; company annual reports and investor presentations; Uptime Institute Annual Data Center Survey 2025; and individual country-level data center regulation reviews. Over 90 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using bottom-up component and type models calibrated against IDC Asia Pacific quarterly data center market tracker, Gartner's data center outsourcing revenue database, hyperscaler annual report geographic revenue disclosures, and operator-disclosed capacity figures. Key inputs include SEA GDP growth by country from the IMF World Economic Outlook 2025, digital economy scenario models, hyperscaler SEA investment commitments from public announcements, data localization regulation enforcement timelines by country, AI workload infrastructure spend growth projections from IDC AI market model, and 5G coverage expansion schedules from GSMA Intelligence SEA 5G forecast for edge data center demand modeling.

South East Asia Data Center Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Components Covered | Solution, Services |

| Types Covered | Colocation, Hyperscale, Edge, Others |

| Enterprise Sizes Covered | Large Enterprises, Small and Medium-sized Enterprises |

| End Users Covered | BFSI, IT and Telecom, Government, Energy and Utilities, Others |

| Countries Covered | Indonesia, Thailand, Singapore, Philippines, Vietnam, Malaysia, Others |

| Companies Covered | Equinix Inc., Digital Realty Trust, NTT Data Inc., Keppel Ltd, Princeton Digital Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the South East Asia data center market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the South East Asia data center market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the South East Asia data center industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the South East Asia Data Center Market Report

The South East Asia data center market reached USD 7.85 Billion in 2025, driven by hyperscaler investments across SEA nations, government data sovereignty mandates in Indonesia, Vietnam, Malaysia, and Thailand, the generative AI GPU infrastructure buildout creating premium data center demand, 5G network rollout enabling edge data center adoption, and SEA's digital economy growth.

The market grows at 6.60% CAGR during 2026-2034, reaching USD 13.95 Billion by 2034, driven by the Johor-Batam cluster emerging as a hyperscale hub, AI GPU cluster revenue premium, Indonesia's PDN sovereign cloud program, Vietnam's digital economy acceleration, SEA's digital economy reaching USD 1 Trillion by 2030, and 5G-enabled edge data center proliferation across all primary SEA markets.

Solution leads at 68.4% through server hardware, power infrastructure, cooling systems, and physical facility construction, representing the capital-intensive base of data center capacity expansion across SEA's new capacity additions.

Hyperscale leads at 36.7% through AWS, Microsoft Azure, and Google Cloud's purpose-built campus investments.

Singapore leads at 29.3%, anchored by Equinix SG1-SG5, AWS ap-southeast-1, Microsoft Azure Southeast Asia, Google Cloud Singapore, and Alibaba Cloud APAC HQ.

Leading companies include Equinix Inc., Digital Realty Trust, NTT Data Inc., Keppel Ltd, and Princeton Digital Group, among others.

The market is projected to reach approximately USD 10.81 Billion by 2030, with the Johor-Batam cluster, Vietnam emerging as SEA's fourth-largest data center market, Indonesia's PDN sovereign cloud deploying government-certified capacity, and hyperscale type exceeding 40% of market share as AWS, Azure, and Google complete their second-wave SEA regional launches.

Generative AI is creating a new premium data center tier requiring 30-100 kW per rack GPU density versus 5-15 kW standard, direct liquid cooling, and InfiniBand interconnect, commanding USD 20-40/kW pricing versus USD 8-15/kW for standard colocation.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)