South East Asia Food Packaging Market Size, Share, Trends and Forecast by Packaging Type, Application, and Country, 2026-2034

South East Asia Food Packaging Market Summary:

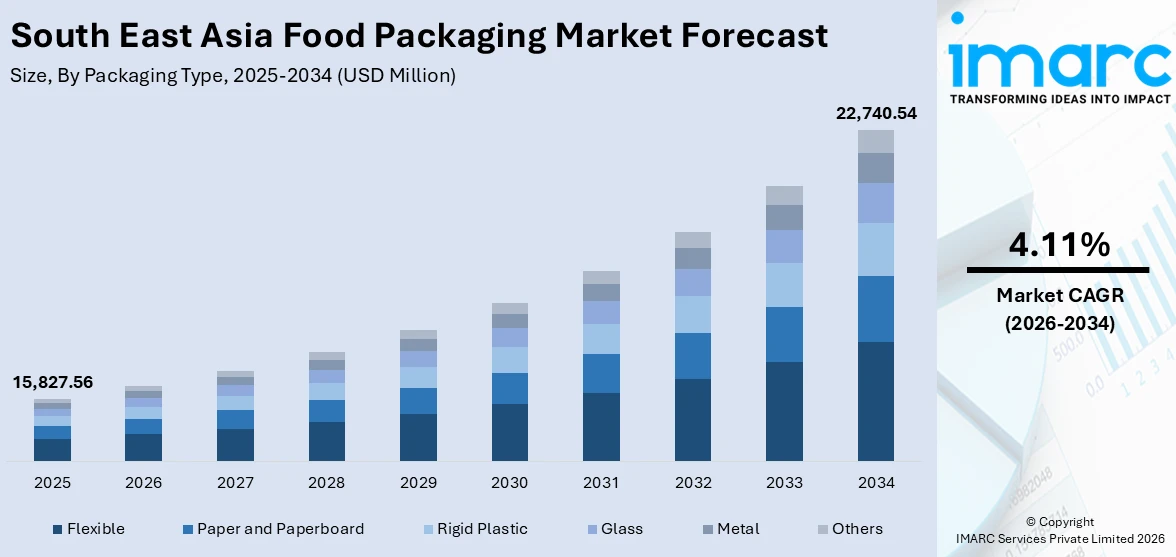

The South East Asia food packaging market size was valued at USD 15,827.56 Million in 2025 and is projected to reach USD 22,740.54 Million by 2034, growing at a compound annual growth rate of 4.11% from 2026-2034.

As modern retail formats spread throughout urban areas and governments fortify regulatory frameworks for sustainable packaging, the food packaging market in South East Asia is growing. Adoption of recyclable materials and circular economy principles is fueled by growing environmental consciousness. The quality of food preservation is being improved by developments in barrier coatings, smart labeling technologies, and temperature-controlled solutions, establishing the area as a quickly developing market for cutting-edge packaging technology.

Key Takeaways and Insights:

- By Packaging Type: Flexible dominates the market with a share of 30% in 2025, owing to its lightweight characteristics, cost-effectiveness, and versatility across diverse food applications, enabling efficient transportation and extended shelf life for packaged goods.

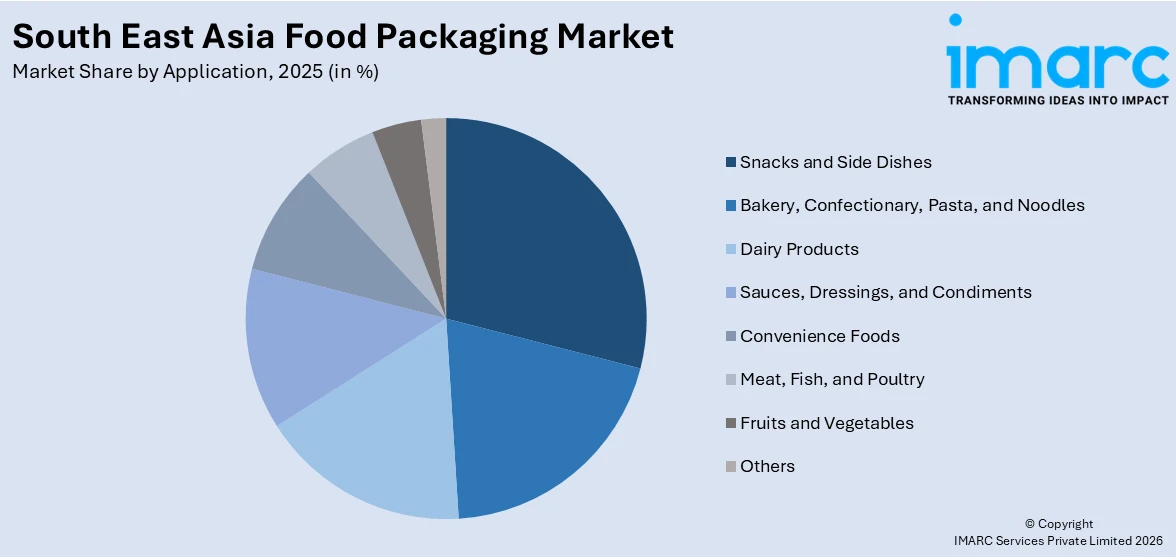

- By Application: Snacks and side dishes lead the market with a share of 18% in 2025, reflecting the increasing urban consumption patterns, on-the-go eating habits, and expanding convenience food categories across Southeast Asian metropolitan areas.

- Key Players: By increasing production capacity, making investments in innovative sustainable materials, and fortifying distribution networks, major companies propel the food packaging industry in South East Asia. In addition to supporting food safety and quality preservation across a variety of applications, their emphasis on regulatory compliance, cutting-edge barrier technologies, and collaborations with food makers speeds up market penetration. Some of the key players operating in the market include Foil Packaging Thailand Inc., HPI Resources Berhad (Oji Paper Asia Sdn. Bhd.), Huhtamaki Group, PT Primajaya Eratama, SCG Packaging Public Company Limited, and South East Packaging Industry Co. Ltd.

To get more information on this market Request Sample

With Indonesia and Thailand recording high urban population shares that allow increased access to contemporary retail formats and e-commerce platforms, the South East Asia food packaging market is expanding rapidly as urbanization reaches new heights. The demand for premium packaging solutions is being driven by rising disposable incomes in Malaysia, Indonesia, and Vietnam, which are increasing consumer spending power for convenience and branded foods. Regulatory developments are transforming the competitive landscape, with Indonesia implementing the National Standard SNI 8218:2024 for paperboard packaging in July 2025, requiring compliance with strength, chemical migration, and hygienic processing standards. Singapore passed its Food Safety and Security Bill in January 2025, establishing comprehensive oversight of food-contact materials and mandating Extended Producer Responsibility reporting for packaging producers. Thailand banned plastic waste imports in January 2025 to encourage domestic recycling infrastructure development. These policy initiatives are compelling manufacturers to accelerate investments in recyclable, biodegradable, and circular packaging alternatives while enhancing food safety protocols across the regional supply chain.

South East Asia Food Packaging Market Trends:

Growing Adoption of Sustainable Packaging Materials

Due to legal requirements and growing consumer awareness of environmental issues, South East Asian countries are moving toward eco-friendly packaging options. Extended Producer Responsibility initiatives, which mandate that brands handle and recycle post-consumer packaging materials, are being implemented by governments around the region. Innovative reusable cold-chain containers and cutting-edge packaging technologies are being introduced via industry partnerships, improving temperature management and greatly lowering environmental impact. These programs encourage manufacturers to invest in biodegradable materials, recyclable laminates, and compostable substitutes by raising industry awareness and bringing packaging design into line with the ideals of the circular economy. The change is a reflection of the increased dedication to sustainable practices in packaging supply chains and food distribution networks.

Expansion of E-Commerce and Ready-to-Eat Food Packaging

As online food delivery and sales platforms increase exponentially, digital commerce penetration is changing packaging needs throughout Southeast Asia. Single-serve, portable, and convenience-focused package forms that guarantee freshness, portability, and simplicity of use during transit are becoming more and more popular among urban customers. Robust, transit-safe packaging that satisfies logistics needs, branding standards, and extended shelf-life requirements is essential for the growth of contemporary retail chains and online grocery platforms. In the food and beverage industry, modified environment packaging technologies are becoming more popular. They support the region's changing consumption habits by improving product preservation while maintaining quality throughout distribution channels.

Integration of Smart and Active Packaging Technologies

Southeast Asian food packaging manufacturers are incorporating intelligent solutions including QR codes, RFID tags, freshness indicators, and IoT-enabled monitoring systems that enhance traceability, food safety, and shelf-life management. These innovations provide transparency throughout the supply chain while enabling consumers to access product authenticity information and nutritional data through digital interfaces. In September 2025, Unilever and SCG Chemicals launched ASEAN's first food-grade recycled packaging for Knorr Professional, developed using advanced recycling technology to produce circular resins safe for food contact, marking a milestone in sustainable packaging innovation. The integration of smart labels and active barrier systems supports temperature monitoring, contamination detection, and product integrity verification across distribution networks.

Market Outlook 2026-2034:

The South East Asia food packaging market is positioned for sustained expansion as regional economies advance infrastructure development and consumer spending patterns evolve. Government commitments to sustainable packaging standards, coupled with rising export growth for processed foods, are creating favorable conditions for market advancement. Indonesia announced plans to invest approximately USD 22 Billion in agricultural and food processing infrastructure in late 2025, while logistics providers expand cold-chain and temperature-controlled networks across Indonesia, Malaysia, Singapore, and the Philippines. The market generated a revenue of USD 15,827.56 Million in 2025 and is projected to reach a revenue of USD 22,740.54 Million by 2034, growing at a compound annual growth rate of 4.11% from 2026-2034. These developments will strengthen processed food production capabilities, improve supply-chain efficiency, and drive sustained demand for innovative, sustainable, and high-performance packaging solutions that meet international trade standards across Southeast Asia.

South East Asia Food Packaging Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

| Packaging Type | Flexible | 30% |

| Application | Snacks and Side Dishes | 18% |

Packaging Type Insights:

- Flexible

- Paper and Paperboard

- Rigid Plastic

- Glass

- Metal

- Others

Flexible dominates with a market share of 30% of the total South East Asia food packaging market in 2025.

Flexible packaging leads the market thanks to its exceptional adaptability, low weight, and affordability for a variety of food applications. Manufacturers can use less material thanks to the format while yet preserving the protective barrier qualities that prolong the shelf life of perishable goods. Its versatility in terms of sizes, forms, and closure systems facilitates effective storage and transportation optimization, reducing supply chain logistics expenses. The industry gains from ongoing advancements in bio-based materials that tackle sustainability issues, recyclable laminates, and multilayer films. Flexible-format pouches, bags, and wraps offer convenience features like portion control, resealable closures, and aesthetic appeal through superior printing capabilities that improve brand distinctiveness on store shelves.

Growing consumer preference for on-the-go consumption and single-serve portions drives demand for flexible packaging across snack foods, beverages, and ready-to-eat meals. E-commerce expansion requires puncture-resistant and lightweight packaging solutions that withstand shipping pressures while minimizing volumetric weight pricing, making flexible formats particularly suitable for direct-to-consumer delivery models. The format's compatibility with Modified Atmosphere Packaging technologies enables oxygen barrier control and freshness preservation without refrigeration requirements. In June 2025, SCG Packaging Public Company Limited completed the acquisition of Duy Tan Plastic Manufacturing JSC, Vietnam's leading rigid-plastic packaging firm, expanding its footprint across flexible and rigid formats throughout ASEAN markets. Manufacturers continue advancing down-gauging techniques that reduce material thickness while preserving or improving performance characteristics, supporting environmental sustainability objectives alongside cost reduction initiatives across the regional market.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Bakery, Confectionary, Pasta, and Noodles

- Dairy Products

- Sauces, Dressings, and Condiments

- Snacks and Side Dishes

- Convenience Foods

- Meat, Fish, and Poultry

- Fruits and Vegetables

- Others

Snacks and side dishes lead with a share of 18% of the total South East Asia food packaging market in 2025.

Accelerated urbanization, rising disposable incomes, and changing consumption patterns in Southeast Asian cities have led to a major market presence for snacks and side dishes. Busy urban lives promote packaged snack categories including chips, crackers, almonds, dried fruits, and savory accompaniments by driving demand for quick, easy-to-consume food options that require little preparation time. With doughnuts, muffins, pastries, and international snack variants becoming more popular alongside local goods, the industry benefits from Western culinary influences entering traditional markets. Packaging specifications provide a strong emphasis on barrier protection against light, air, and moisture exposure while preserving the flavor, crispness, and freshness of products throughout long shelf lives.

Flexible packaging formats that offer portion control, visual transparency, and convenience features that appeal to younger consumers and working professionals, such as stand-up pouches, flow-wrap films, and reclosable bags, are given priority by manufacturers. Larger family-size formats accommodate household bulk purchase inclinations, while single-serve packaging advances cater to individual consumption situations. The rise of the regional processed food sector is indicative of strong consumer demand for packaged snack foods, which is being bolstered by an increase in exports. While e-commerce platforms allow direct consumer access across urban and semi-urban regions, the increasing presence of modern retail outlets, supermarkets, and convenience stores offers improved distribution channels for packaged snacks, bolstering the demand for packaging solutions that are sustainable, appealing, and transit safe.

Country Insights:

- Indonesia

- Thailand

- Singapore

- Philippines

- Vietnam

- Malaysia

- Others

Indonesia's sizable population, growing middle class, and increasing rates of urbanization all contribute to the country's emergence as a major market for packaged food items. Packaging requirements for a variety of categories are strengthened by the nation's expanding contemporary retail infrastructure and rising consumer expenditure on convenience foods. Favorable conditions for the growth of the packaging business are created by government programs that encourage investments in food processing and the development of export markets. Strategic geographic placement within ASEAN trade networks and the availability of a wealth of raw materials help manufacturers maintain competitive production costs while successfully catering to regional markets.

Thailand's well-established food processing industry, export-focused manufacturing capacity, and sophisticated logistics infrastructure all contribute to its significant market position. With significant expenditures in sustainable material development and packaging technologies, the country functions as a regional center for food product manufacture. The demand for portion-controlled packaging, take-out containers, and convenient formats is driven by the growing foodservice and tourism industries. The implementation of recyclable and biodegradable packaging options across the supply chain is accelerated by Thailand's dedication to environmental sustainability, which is demonstrated by the country's total prohibition on the importation of plastic garbage in January 2025.

Strict food safety laws, widespread use of cutting-edge technology, and sophisticated consumer tastes define Singapore as a highly developed market. The city-state's extensive Food Safety and Security Bill requires Extended Producer Responsibility reporting from packaging manufacturers and imposes strict control on materials that come into contact with food. The demand for luxury packaging solutions, creative formats, and sustainable materials is supported by Singapore's completely urbanized population, high disposable incomes, and global dining culture. Through established distribution networks, the country acts as a regional trial ground for novel packaging technologies, smart labels, and active packaging systems that subsequently spread throughout Southeast Asian markets.

The Philippines has growing market potential due to the country's rapid population expansion, rising urbanization, and robust demand for packaged foods in urban areas. The nation's sizable consumer base and rising purchasing power enable a range of packaging needs, from premium to low-cost categories. Creation of an Extended Producer Initiatives for the circular economy and responsibility programs promote the use of sustainable packaging while addressing environmental issues. In metropolitan areas, the need for single-use packaging, take-out containers, and portion-controlled formats is driven by the growth of the foodservice industry, quick-service restaurants, and convenience store networks.

Vietnam's market is growing quickly thanks to its growing urban population, economic development, and growing integration into international trade networks. Competitive manufacturing costs, advancing infrastructure, and advantageous trade agreements that promote export competitiveness all assist the nation's food processing industry. The need for dependable packaging solutions that adhere to international standards is driven by growing consumer awareness of food safety and quality. Investments in ecologically friendly packaging materials and circular economy activities are encouraged across the value chain by the government's emphasis on sustainable development, which is represented in the Environmental Protection Law that enforces eco-labels and reduction objectives.

Malaysia demonstrates steady market advancement through balanced economic growth, diverse food manufacturing capabilities, and strategic positioning within Halal certification networks that enable access to global Muslim consumer markets. The nation's Roadmap Towards Zero Single-Use Plastics 2018-2030 emphasizes biodegradable and compostable alternatives while discouraging single-use plastic consumption at public venues. Growing middle-class populations and increasing health consciousness support demand for quality packaging that preserves nutritional value and extends product freshness. Modern retail expansion, coupled with e-commerce growth, creates opportunities for innovative packaging formats that address changing shopping behaviors.

Market Dynamics:

Growth Drivers:

Why is the South East Asia Food Packaging Market Growing?

Rapid Urbanization and Changing Consumer Lifestyles

Southeast Asia's urban population is experiencing significant expansion, with increasing proportions of residents living in cities that support greater access to modern retail formats, supermarkets, and e-commerce platforms that primarily distribute packaged and processed food products. Urban lifestyles increasingly favor convenience, time-saving solutions, and ready-to-eat options that require minimal preparation, driving demand for portion-controlled packaging, resealable closures, and single-serve formats. Rising disposable incomes across the region strengthen consumer purchasing power, enabling transitions from traditional loose foods toward branded, hygienically packaged alternatives. Improving living standards support increased expenditure on packaged convenience foods. Working professionals, dual-income households, and expanding middle-class populations prioritize food safety, quality assurance, and extended shelf life that modern packaging technologies provide, fundamentally reshaping consumption patterns and distribution channels throughout Southeast Asian markets.

Regulatory Support for Sustainable Packaging and Food Safety Standards

Government authorities across Southeast Asia are implementing comprehensive regulatory frameworks that promote sustainable packaging practices while strengthening food safety oversight. Regional countries have established mandatory national standards for paper and cardboard primary food packaging, setting requirements for strength, chemical migration limits, and hygienic processing that align with international standards and improve export competitiveness. Governments are passing legislation that provides legal foundations for regulating food-contact materials, enabling future bans on hazardous substances and mandating Extended Producer Responsibility reporting for packaging producers. National authorities are advancing regulations for food-contact paper packaging with strict controls on chemical treatments and new labeling requirements. Updated guidelines permit recycled materials in food packaging, supporting circular economy development while addressing post-consumer plastic waste challenges. These regulatory initiatives encourage manufacturers to invest in recyclable materials, biodegradable alternatives, and circular packaging solutions that meet compliance requirements while reducing environmental impact. Harmonization efforts within regional frameworks are creating more uniform standards to facilitate trade, promote best practices, and ensure consistency in packaging safety and sustainability across member nations.

Expansion of Modern Retail Infrastructure and E-Commerce Platforms

Southeast Asia's retail landscape is transforming through rapid expansion of modern trade formats, organized supermarket chains, and digital commerce platforms that fundamentally alter packaging requirements and distribution logistics. E-commerce food sales continue growing substantially, fueled by rising smartphone penetration, improving internet connectivity, and growing consumer confidence in online purchasing. Digital platforms enable direct-to-consumer models that require transit-safe, lightweight, and visually appealing packaging capable of withstanding multiple handling touchpoints throughout delivery networks. Modern retail outlets demand standardized packaging dimensions, shelf-ready formats, and barcode integration that support efficient inventory management and automated replenishment systems. Cold-chain infrastructure investments by logistics providers are expanding temperature-controlled networks across the region, enabling distribution of perishable products that require specialized packaging solutions maintaining freshness and safety throughout transportation. The proliferation of convenience stores, quick-service restaurants, and foodservice chains drives demand for single-serve packaging, take-away containers, and portion-controlled formats designed for on-the-go consumption. Export growth further reinforces packaging demand, highlighting the importance of compliant, high-quality packaging in enabling international trade competitiveness.

Market Restraints:

What Challenges the South East Asia Food Packaging Market is Facing?

Higher Costs of Sustainable Packaging Materials

Sustainable packaging alternatives including biodegradable films, compostable pouches, and recyclable laminates command premium pricing compared to conventional plastic materials, creating cost barriers particularly for small and medium enterprises operating on tight profit margins. Bio-based plastics such as Polylactic Acid, Polyhydroxyalkanoates, and plant-derived materials require specialized production processes and limited manufacturing scale, resulting in elevated raw material expenses. Despite long-term environmental benefits and regulatory advantages, many manufacturers hesitate to transition from established conventional packaging due to immediate financial constraints and uncertain return on investment timelines. The price differential discourages widespread adoption among budget-conscious producers serving price-sensitive consumer segments across emerging Southeast Asian economies.

Complex and Evolving Regulatory Compliance Requirements

Manufacturers face challenges navigating diverse and frequently changing packaging regulations across multiple Southeast Asian jurisdictions, each implementing distinct timelines, technical specifications, and compliance procedures. Indonesia's mandatory SNI 8218:2024 standard, Singapore's comprehensive Food Safety and Security Bill, and Thailand's emerging food-contact paper regulations create fragmented compliance landscapes requiring significant administrative resources and technical expertise. Companies operating across borders must simultaneously meet varying migration limits, testing protocols, declaration of conformity requirements, and Extended Producer Responsibility obligations that differ by country. Smaller enterprises often lack the technical capabilities and financial resources to conduct extensive testing, maintain documentation systems, and adapt production processes to meet evolving regulatory demands. The transition periods between regulation announcements and enforcement deadlines can create operational uncertainties, production disruptions, and inventory obsolescence risks for non-compliant packaging materials.

Limited Recycling Infrastructure and Collection Systems

Despite advancing Extended Producer Responsibility programs and circular economy initiatives, many Southeast Asian markets continue facing insufficient recycling infrastructure, particularly in rural and semi-urban areas where waste collection systems remain informal or underdeveloped. Limited post-consumer plastic recovery rates reduce the availability of recycled materials for food-grade packaging applications, forcing manufacturers to rely on virgin resins and limiting circular economy progress. Thailand's complete ban on plastic waste imports from January 2025 eliminated a key source of recycled PET flakes and recycled polyethylene pellets, causing PET flake prices to rise. Small and medium enterprises often revert to virgin resin usage when recycled materials become unavailable or prohibitively expensive, undermining sustainability commitments and green marketing claims throughout the packaging supply chain.

Competitive Landscape:

The South East Asia food packaging market demonstrates moderate fragmentation with regional manufacturers and global corporations competing through capacity expansion, technological innovation, and sustainability initiatives. Leading players are strengthening their market positions by investing in production facilities, acquiring local competitors, and developing strategic partnerships with food and beverage manufacturers. Companies focus on differentiating through sustainable packaging portfolios, advanced barrier technologies, and customized solutions that meet specific application requirements across bakery, dairy, snacks, and convenience food categories. Competitive strategies emphasize vertical integration, with major manufacturers controlling upstream resin production, paper mills, and converting capabilities to deliver comprehensive packaging solutions. Firms are enhancing research and development efforts to create recyclable mono-material laminates, biodegradable films, and active packaging systems incorporating freshness indicators and smart labels. Collaboration with raw material suppliers enables faster time-to-market for Extended Producer Responsibility-compliant packaging that meets evolving regulatory standards. Market participants are expanding geographic footprints across ASEAN nations through greenfield investments, mergers and acquisitions, and distribution network strengthening to capture growth opportunities in emerging economies.

Some of the key players include:

- Foil Packaging Thailand Inc.

- HPI Resources Berhad (Oji Paper Asia Sdn. Bhd.)

- Huhtamaki Group

- PT Primajaya Eratama

- SCG Packaging Public Company Limited

- South East Packaging Industry Co. Ltd.

South East Asia Food Packaging Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Packaging Types Covered | Flexible, Paper and Paperboard, Rigid Plastic, Glass, Metal, Others |

| Applications Covered | Bakery, Confectionary, Pasta, and Noodles, Dairy Products, Sauces, Dressings, and Condiments, Snacks and Side Dishes, Convenience Foods, Meat, Fish, and Poultry, Fruits and Vegetables, Others |

| Countries Covered | Indonesia, Thailand, Singapore, Philippines, Vietnam, Malaysia, Others |

| Companies Covered | Foil Packaging Thailand Inc., HPI Resources Berhad (Oji Paper Asia Sdn. Bhd.), Huhtamaki Group, PT Primajaya Eratama, SCG Packaging Public Company Limited, South East Packaging Industry Co. Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the South East Asia Food Packaging Market Research Report Report

The South East Asia food packaging market size was valued at USD 15,827.56 Million in 2025.

The South East Asia food packaging market is expected to grow at a compound annual growth rate of 4.11% from 2026-2034 to reach USD 22,740.54 Million by 2034.

Flexible packaging dominated the market with a share of 30%, driven by its lightweight characteristics, cost-effectiveness, and versatility across diverse food applications, enabling efficient transportation and extended shelf life while supporting innovations in multilayer films and recyclable laminates that address sustainability concerns throughout the regional market.

Key factors driving the South East Asia food packaging market include rapid urbanization and changing consumer lifestyles, regulatory support for sustainable packaging and food safety standards, expansion of modern retail infrastructure and e-commerce platforms, rising disposable incomes, and investments in cold-chain logistics and processing infrastructure across the region.

Major challenges include higher costs of sustainable packaging materials compared to conventional alternatives, complex and evolving regulatory compliance requirements across multiple jurisdictions, limited recycling infrastructure and collection systems particularly in rural areas, and supply chain constraints affecting availability of recycled materials for food-grade applications.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)