South East Asia Seafood Market Size, Share, Trends and Forecast by Type, Form, Distribution Channel, and Country 2026-2034

South East Asia Seafood Market Size and Share:

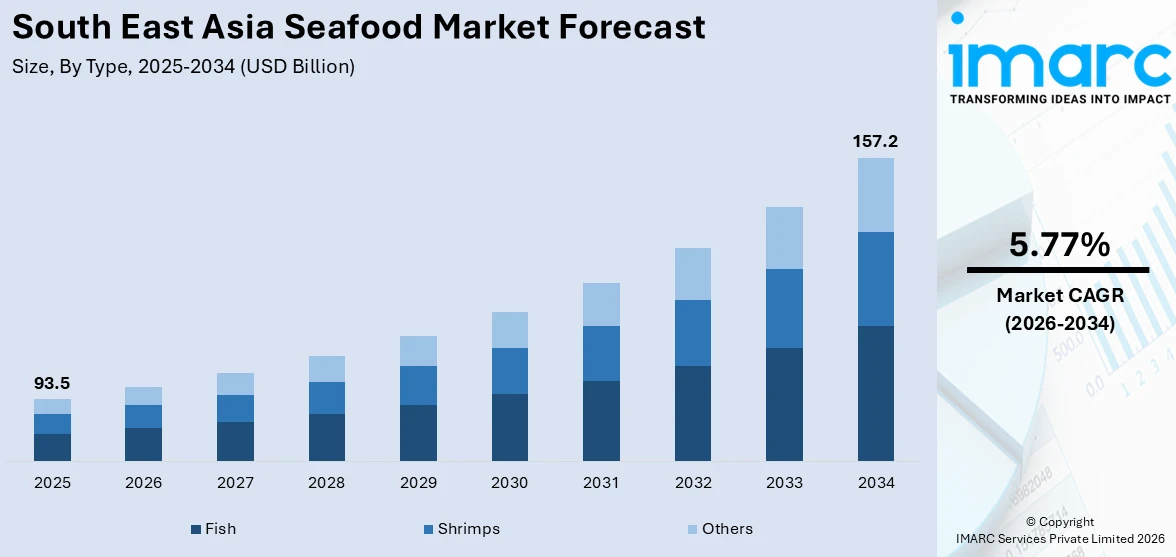

The South East Asia seafood market size was valued at USD 93.5 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 157.2 Billion by 2034, exhibiting a CAGR of 5.77% during 2026-2034. Indonesia currently dominates the market, holding a significant market share of over 45.0% in 2024. The nation's vast archipelago, extensive coastlines, and vibrant marine ecosystem position it firmly as a market leader. Its fishery and aquaculture at an industrial scale serve regional and global demands, positioning the country as a lead actor in South East Asia seafood market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 93.5 Billion |

| Market Forecast in 2034 | USD 157.2 Billion |

| Market Growth Rate 2026-2034 | 5.77% |

The Southeast Asia seafood market is being driven by a combination of population growth, rising incomes, and shifting dietary patterns. For instance, as per industry reports, Southeast Asia is undergoing swift urban growth, with nearly half of its population currently residing in cities. This upward trend is projected to persist, with around 70 million more people anticipated to move into urban areas across the region by 2025. As urbanization accelerates in the region, consumers are switching more and more towards protein diets, with seafood being a popular choice due to its nutritional and cultural popularity. Seafood plays a key role in traditional diets in nations like Thailand, Vietnam, Indonesia, and the Philippines, underpinning demand. Moreover, the growing middle class is driving increased demand for superior-quality, fresh, and value-added seafood products, thereby propelling the South East Asia seafood market growth. Governments also are making investments in sustainable aquaculture and fisheries development, with partnerships at the regional level promoting traceability, food safety, and international competitiveness. Expansion in exports, especially to China, the United States, and Europe, is also prompting local producers to enhance processing and cold-chain facilities.

To get more information on this market Request Sample

Technological advancements in aquaculture and processing are another major driver of the market. The adoption of precision aquaculture tools—such as IoT-based water quality monitors, automated feeding systems, and disease control technologies is improving yield and reducing operational costs. These innovations are being supported by regional initiatives to ensure responsible sourcing, biodiversity conservation, and reduction of bycatch. Additionally, the rising popularity of e-commerce and cold-chain logistics improvements have enhanced market accessibility, enabling small and mid-sized producers to reach broader urban and international consumer bases. Health-conscious consumers are also seeking sustainable and certified seafood, pushing the industry to adopt eco-labeling and compliance with international sustainability standards. With efforts to harmonize regulatory frameworks and boost cross-border trade, the South East Asia seafood market outlook is expected to remain strong, signaling a promising trajectory for regional growth.

South East Asia Seafood Market Trends:

Strong Cultural Demand and Nutritional Awareness Fueling Regional Consumption

Southeast Asia’s seafood market is significantly driven by the region’s deep-rooted cultural and culinary reliance on marine products, especially in coastal and riverine communities. Countries like Indonesia, Thailand, and Vietnam not only have strong seafood traditions, but also some of the highest per capita fish consumption rates globally. As per industry standards, per capita fish and seafood consumption is projected to reach 21.4 kg by the end of 2030. Asia remains the leading consumer, accounting for 72% of the world’s total fish consumption. This cultural connection continues to support consistent demand across rural and urban areas. Moreover, as awareness of seafood’s nutritional benefits—such as high protein content, omega-3 fatty acids, and low saturated fats—continues to grow, more health-conscious consumers are incorporating fish and shellfish into their diets. This intersection of tradition and health is expected to sustain market growth, especially as younger consumers balance heritage preferences with modern wellness goals. Local cuisines, social behavior, and dietary norms will remain critical demand drivers in this high-consumption region.

Sustainability and Governance Advancements Driving Long-Term Market Viability

A key growth driver in Southeast Asia’s seafood market is the increasing emphasis on sustainability, traceability, and regulatory support from both governments and major industry players. Reflecting broader South East Asia seafood market trends, initiatives like FAO’s IFish project in Indonesia (2017–2024) which managed over 11,800 sq. km of ecosystems and trained over 10,500 locals highlight the region’s proactive shift toward sustainable inland fisheries. Similarly, private sector leadership, such as Thai Union’s sourcing of 85% of its tuna from responsible fisheries and monitoring 90% of its vessels by 2023, demonstrates tangible progress. These efforts align with the SeaChange 2030 program’s ambitious goals for emissions reduction and ecosystem restoration. As global buyers increasingly demand certified, eco-labeled, and ethically sourced seafood, Southeast Asia’s commitment to these market trends strengthens its competitiveness and positions the region as a responsible global seafood supplier.

South East Asia Seafood Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the South East Asia seafood market, along with forecast at the regional and country levels from 2026-2034. The market has been categorized based on type, form, and distribution channel.

Analysis by Type:

- Fish

- Shrimps

- Others

Fish stands as the largest type in 2024, holding around 61.5% of the market. As per South East Asia seafood market forecast, this can be attributed to a confluence of factors, including the region's extensive coastlines and diverse aquatic ecosystems that provide an abundant supply of various fish species. As a dietary staple, fish is a primary and often affordable protein source for a large population. Southeast Asian cuisine features a rich variety of fish-based dishes, further fueling demand. Additionally, a well-established fishing industry, including both capture fisheries and aquaculture, ensures a consistent supply for both domestic consumption and export.

Analysis by Form:

Access the comprehensive market breakdown Request Sample

- Fresh/Chilled

- Frozen/Canned

- Processed

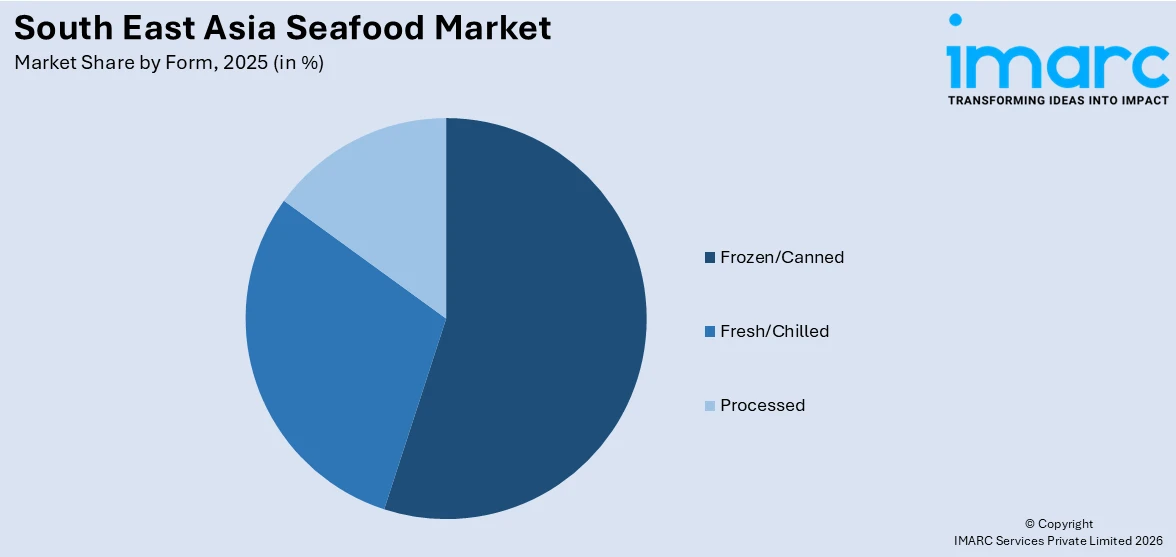

Frozen/canned leads the market in 2024. Frozen and canned seafood hold a significant share of the Southeast Asian market due to several factors. These preservation methods address the challenges of distributing perishable goods in a tropical climate with diverse infrastructure. Frozen seafood offers extended shelf life, preserving freshness and nutritional value, while canned seafood provides even greater convenience and longer storage. This appeals to busy consumers and areas with limited access to fresh supplies. Additionally, these forms facilitate efficient transportation and reduce waste, supporting both domestic and export markets.

Analysis by Distribution Channel:

- Off Trade

- On Trade

On trade leads the market with around 58.9% of market share in 2024. The on-trade sector, encompassing restaurants and foodservice establishments, plays a crucial role in shaping the Southeast Asian seafood market. The region's rich and diverse culinary landscape, combined with a strong culture of dining out, fuels significant demand for seafood within this channel. From casual eateries to high-end restaurants, seafood is a prominent feature on menus, driving consumption and influencing market trends. The on-trade sector's demand for a variety of seafood products, both local and imported, impacts sourcing, distribution, and pricing within the market.

Country Analysis:

- Indonesia

- Thailand

- Singapore

- Philippines

- Vietnam

- Malaysia

- Others

In 2024, Indonesia accounted for the largest market share of over 45.0%. The country holds a prominent position in the Southeast Asian seafood market, driven by its unique geographical advantages and robust industry. As an archipelagic nation with vast coastlines, Indonesia possesses abundant marine resources and a diverse array of seafood products. The country's extensive fishing industry, encompassing both wild-caught and aquaculture sectors, contributes significantly to its leading role. Indonesia's large population and growing economy fuel domestic demand, while its strategic location facilitates exports to regional and global markets. Government initiatives promoting sustainable fishing practices and investments in seafood processing infrastructure further solidify its dominance. The country's rich maritime heritage and culinary traditions also play a vital role in shaping its dynamic seafood market. For instance, in February 2025, JALA and Konservasi Indonesia launched the Climate Smart Shrimp Farming (CSSF) initiative in Donggala, Central Sulawesi. Integrating shrimp farming with mangrove restoration, the project aims to boost productivity, reduce environmental impact, and support local livelihoods through sustainable aquaculture practices on a 10-hectare site.

Competitive Landscape:

The Southeast Asian seafood market presents a dynamic competitive landscape, shaped by a diverse array of participants ranging from small-scale local fishermen to large multinational corporations. For instance, at the 2024 Seafood Expo Asia, Asia-based seafood start-ups drew significant investor attention. Indonesia’s eFishery became the industry’s latest unicorn, while other firms like Captain Fresh and FreshToHome attracted major funding. Six emerging companies pitched sustainable, tech-driven aquaculture solutions to investors, emphasizing strong returns and ESG impact. Notably, Singapore’s Agrata and Indonesia’s Living Seas Aquafeeds showcased innovations in mud crab farming and premium aquafeeds, underscoring Asia’s growing role in shaping the future of sustainable seafood production and aquaculture innovation. Key factors influencing this landscape include the substantial production capabilities of countries like Indonesia, Thailand, and Vietnam, which dictate supply dynamics, and the critical role of efficient distribution networks, encompassing both traditional markets and modern retail channels, in ensuring market accessibility. Moreover, the region's rich biodiversity contributes to a wide variety of available seafood products, further intensifying competition within the market.

The report provides a comprehensive analysis of the competitive landscape in the South East Asia seafood market with detailed profiles of all major companies, including:

- Thai Union Group PCL

- PT Aneka Tuna Indonesia

- Regal Springs Indonesia

- Seafresh Industry Public Company Limited

Latest News and Developments:

- March 2025: Minh Phu Seafood Corporation, a major Vietnamese seafood exporter, joined the Seafood Task Force (STF), reinforcing its commitment to sustainability, supply chain transparency, and innovation. With a global presence and over 15,000 employees, Minh Phu aims to implement eco-friendly practices and support ethical seafood production. The STF works to improve global tuna and shrimp supply chains, emphasizing traceability and social responsibility. Minh Phu's membership strengthens Vietnam’s role in promoting sustainable seafood across Southeast Asia.

- February 2025: Willcom and Sanyo Foods announced the full launch of their oyster business in Vietnam, targeting 100 metric tons of production. The initiative reportedly marks Japan’s first business venture using frozen Vietnamese oysters.

- May 2024: Malaysian seafood company Fusipim launched its new Fish Sausage in cheese and original flavors, made from wild threadfin breams. Introduced at FHA-Food & Beverage 2024 in April, the product offers a seafood alternative to traditional meats.

South East Asia Seafood Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Fish, Shrimps, Others |

| Forms Covered | Fresh/Chilled, Frozen/Canned, Processed |

| Distribution Channels Covered | Off Trade, On Trade |

| Countries Covered | Indonesia, Thailand, Singapore, Philippines, Vietnam, Malaysia, Others |

| Companies Covered | Thai Union Group PCL, PT Aneka Tuna Indonesia, Regal Springs Indonesia, Seafresh Industry Public Company Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the South East Asia seafood market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the South East Asia seafood market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the South East Asia seafood industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the South East Asia Seafood Market Report

The South East Asia seafood market was valued at USD 93.5 Billion in 2025.

The South East Asia seafood market is projected to exhibit a CAGR of 5.77% during 2026-2034, reaching a value of USD 157.2 Billion by 2034.

Key factors driving the South East Asia seafood market include rising demand for sustainable and traceable products, supportive government regulations, technological innovation in aquaculture, and strong export potential. Growing environmental awareness, improved supply chain transparency, and investments from both public and private sectors further strengthen the region’s seafood industry growth.

In 2024, Indonesia dominated the South East Asia seafood market, accounting for the largest market share of 45.0%, with growth driven by strong aquaculture development, government support, and sustainable fishing initiatives. Investments in cold chain logistics, digital traceability systems, and export-oriented production further boosted growth, positioning Indonesia as a key player in the regional and global seafood trade.

Some of the major players in the South East Asia seafood market include Thai Union Group PCL, PT Aneka Tuna Indonesia, Regal Springs Indonesia, Seafresh Industry Public Company Limited, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)