South Korea Luxury Fashion Market Size, Share, Trends and Forecast by Product Type, Distribution Channel, End User, and Region, 2026-2034

South Korea Luxury Fashion Market Size, Share, Trends & Forecast (2026-2034)

The South Korea luxury fashion market was valued at USD 4.93 Billion in 2025 and is projected to reach USD 6.23 Billion by 2034, exhibiting a CAGR of 2.49% during 2026-2034. Rising affluence among Korean consumers, the soft-power influence of K-pop and K-drama brand placements, expanding flagship boutiques in Seoul, and surging inbound luxury tourism activities are the primary drivers shaping market growth. In April 2023, Louis Vuitton staged its first-ever Pre-Fall womenswear runway show on Seoul's Jamsugyo Bridge in partnership with the Korea Tourism Organization, underlining the strategic importance of Korean luxury fashion industry.

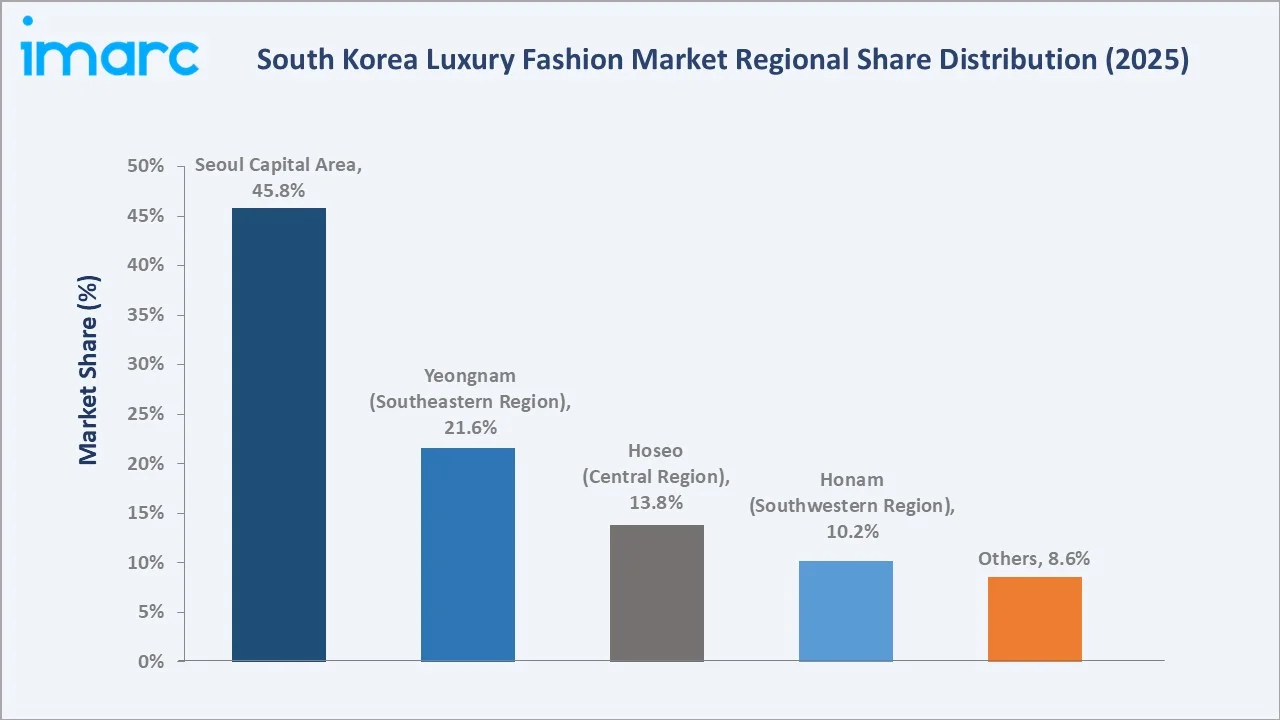

Store-based leads the distribution channel segment at 64.7%, clothing and apparel dominates the product type segment at 52.4%, and Seoul Capital Area commands 45.8% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 4.93 Billion |

|

Forecast Market Size (2034) |

USD 6.23 Billion |

|

CAGR (2026-2034) |

2.49% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Seoul Capital Area (45.8%, 2025) |

|

Fastest Growing Region |

Yeongnam (Southeastern Region) (21.6%, 2025) |

|

Leading Distribution Channel |

Store-Based (64.7%, 2025) |

|

Leading Product Type |

Clothing and Apparel (52.4%, 2025) |

The South Korea luxury fashion market expanded from USD 4.36 Billion in 2020 to USD 4.93 Billion in 2025, supported by rising consumer confidence, increasing premium spend, and a strong return of duty-free traffic. Anchored at USD 5.58 Billion in 2030, the forecast to USD 6.23 Billion by 2034 reflects sustained demand for premium apparel, accessories, and footwear.

To get more information on this market, Request Sample

CAGR trajectories across distribution channel and product type sub-segments show non-store based and accessories expanding faster than the overall 2.49% market CAGR, driven by digital luxury platforms and rising demand for entry-luxury items.

Executive Summary

The South Korea luxury fashion market is on a steady growth path from USD 4.36 Billion in 2020 to USD 6.23 Billion by 2034. Luxury fashion has matured from a status-driven purchase into a daily-wear category for affluent Korean consumers. Strong brand heritage, premium retail experiences, and celebrity-led marketing continue to shape consumer choice. Department-store concessions remain dominant, while online luxury platforms gain share rapidly among younger shoppers.

Store-based dominates the distribution channel segment at 64.7% in 2025, supported by deep department-store networks operated by big brands and increasing tourism activities. According to the Korea Tourism Organization, 16.37 Million foreign visitors came to the country in 2024, marking a 50% increase compared to 2023. Clothing and apparel lead the product type segment at 52.4%, fueled by demand for ready-to-wear, outerwear, and seasonal collections. Seoul Capital Area commands 45.8%, anchored by Cheongdam-dong, Apgujeong, and Gangnam luxury corridors.

Key Market Insights

|

Insight |

Data |

|

Leading Distribution Channel |

Store-Based - 64.7% share (2025) |

|

Second Distribution Channel |

Non-Store Based - 35.3% share (2025) |

|

Leading Product Type |

Clothing and Apparel - 52.4% share (2025) |

|

Second Product Type |

Accessories - 28.6% share (2025) |

|

Leading Region |

Seoul Capital Area - 45.8% share (2025) |

|

Fastest Growing Region |

Yeongnam (Southeastern Region) - 21.6% share (2025) |

|

Top Companies |

Kering, Hermès, Prada S.P.A., Compagnie Financière Richemont SA, Giorgio Armani S.p.A., Ralph Lauren |

Key Analytical Observations Expanding on the Data Above:

- Store-based dominance at 64.7% reflects the central role of premium department stores and standalone flagship boutiques across major Korean cities. Curated in-store experiences, personal shopper services, and exclusive product launches continue to attract high-spending consumers.

- Non-store based share at 35.3% is rising through brand e-commerce sites, premium online platforms, and luxury verticals. Mobile-first browsing and same-day delivery support steady channel migration among younger buyers.

- Clothing and apparel leadership at 52.4% is supported by demand for ready-to-wear, outerwear, and seasonal collections. Brand collaborations with Korean celebrities further fuel category visibility and aspirational purchases.

- Accessories at 28.6% is sustained by strong demand for handbags, small leather goods, and fine jewelry. In 2023, disposable personal income in South Korea rose to 2438286.40 KRW Billion, supporting premium gifting and self-purchase behavior.

- Seoul Capital Area at 45.8% dominates owing to high concentrations of high-net-worth individuals (HNWIs), premium tourism flows, and dense luxury retail clusters in Cheongdam, Apgujeong, and Hannam-dong. Mature retail infrastructure further supports sustained brand investment.

South Korea Luxury Fashion Market Overview

The South Korea luxury fashion market covers premium and high-end clothing, accessories, and footwear sold under globally recognized brand houses through both physical and digital channels. The category caters to affluent consumers, premium tourists, and an expanding base of aspirational young buyers across major metropolitan centers.

The ecosystem integrates global brand houses, design and manufacturing partners, importers, department store operators, premium online platforms, certification bodies, and resale players, together supporting the end-to-end flow from atelier to consumer across South Korea.

Market Dynamics

To evaluate market opportunities, Request Sample

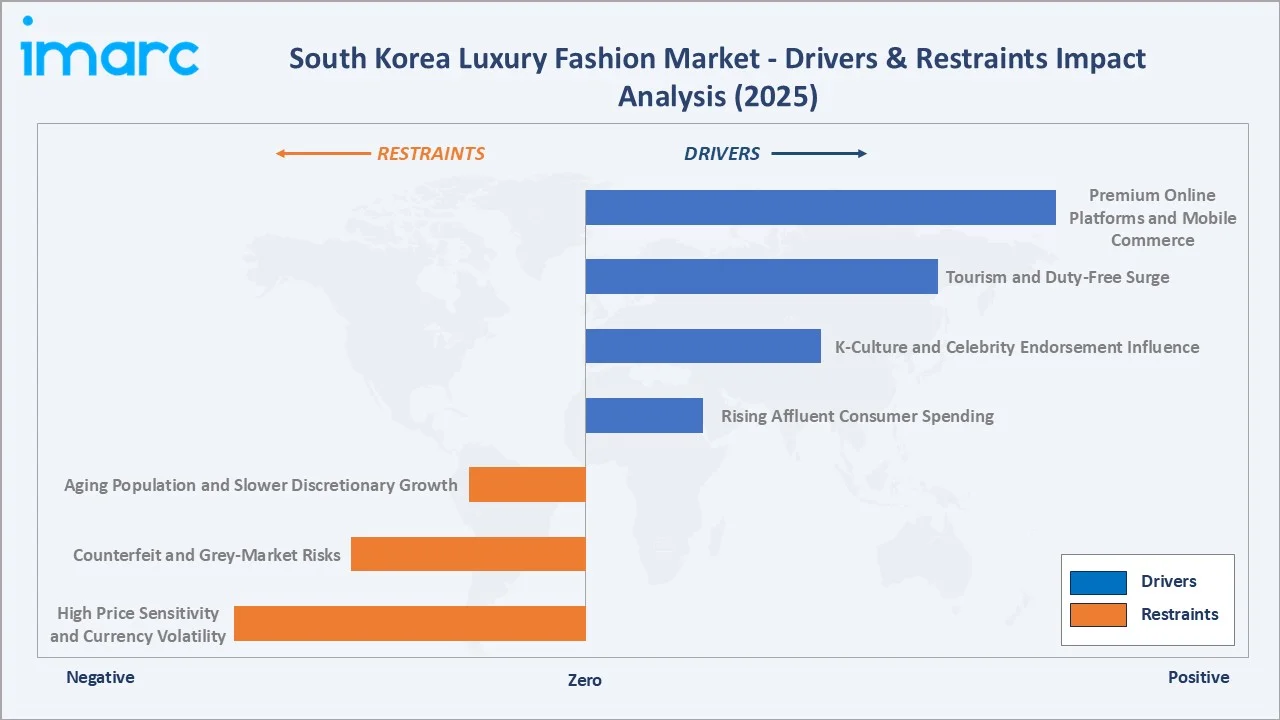

Market Drivers

- Rising Affluent Consumer Spending: Growing wealth among South Korea's HNWI and upper-middle class households continues to support premium fashion demand. Consumers increasingly view luxury purchases as everyday lifestyle items rather than occasional indulgences.

- K-Culture and Celebrity Endorsement Influence: Strong global influence of K-pop and K-drama drives brand visibility through ambassadorships and product placements. Korean celebrities frequently shape demand for specific brands and seasonal collections across both domestic and overseas consumers.

- Tourism and Duty-Free Surge: Rising international tourist arrivals are fueling duty-free and travel-retail luxury sales in South Korea. As per IMARC Group, the South Korea tourism market is set to attain USD 20,659.9 Million by 2034. Chinese, Japanese, and Southeast Asian travelers remain major consumers in airport and downtown duty-free outlets, supporting strong demand for premium beauty, fashion, and luxury products.

- Premium Online Platforms and Mobile Commerce: Online platforms are reshaping luxury distribution by bringing authenticated products, curated launches, and instant logistics to younger digital-first consumers across South Korea.

Market Restraints

- High Price Sensitivity and Currency Volatility: Fluctuations in the Korean won against the euro and US dollar can sharply raise local retail prices, creating short-term affordability barriers. Frequent price hikes by global brands have also fueled consumer pushback and slower repeat purchases.

- Counterfeit and Grey-Market Risks: In 2025, the Korea Customs Service confiscated 117,000 fake items of Korean-brand products, with cosmetics making up 41,903 items, or 35.9%, the highest proportion of all categories. Counterfeit risks weigh on brand value and consumer trust.

- Aging Population and Slower Discretionary Growth: A rapidly aging demographic profile and rising household debt pressure discretionary spending. Future growth depends on attracting younger shoppers and converting aspirational buyers into long-term luxury consumers.

Market Opportunities

- Expansion of Premium Resale and Pre-Owned Channels: Rising consumer comfort with authenticated pre-owned luxury opens new revenue streams. Platforms offering certification and buyback services can capture younger, value-conscious buyers without diluting brand prestige.

- Personalization, Bespoke, and Made-to-Order Services: Affluent Korean consumers show strong interest in monogramming, custom leather goods, and made-to-order tailoring. Bespoke offerings strengthen brand loyalty and command premium margins over standard ready-to-wear lines.

Market Challenges

- Channel Conflict Between Department Stores and Online Platforms: Tension between traditional retail concessions and fast-growing digital channels creates pricing transparency challenges and margin pressure. Brands must carefully balance partnerships across both physical and online ecosystems.

- Sustainability and ESG Compliance Pressure: Korean consumers, especially younger buyers, increasingly evaluate brands on sustainability, materials sourcing, and supply-chain ethics. Failing to demonstrate progress on ESG metrics can hurt brand perception and long-term demand.

Emerging Market Trends

1. Rise of K-Luxury and Local Designer Partnerships

Global luxury houses are increasingly collaborating with Korean designers, artists, and celebrities to localize collections and campaigns. These partnerships enhance cultural relevance and help brands deepen ties with K-pop and K-drama-driven youth audiences.

2. Premium Online Platforms and Digital Luxury

Authenticated online platforms are reshaping luxury distribution in South Korea, offering curated launches, certification, and rapid delivery. Mobile-first browsing, livestream commerce, and AI-driven recommendations are accelerating channel migration among younger buyers.

3. Sustainable Materials and Circular Luxury

Korean shoppers are showing rising preference for recycled leather, traceable supply chains, and certified eco-friendly fabrics. Luxury brands are increasingly incorporating sustainability-focused collections and transparent sourcing practices to strengthen consumer trust and align with evolving environmental expectations.

4. Growth of Resale and Vintage Luxury

Pre-owned and vintage luxury is gaining mainstream appeal among Gen Z and Millennials. Authenticated resale platforms and dedicated vintage boutiques are expanding choice, improving accessibility, and reinforcing the long-term value perception of premium brands.

5. Digital Fashion, NFTs, and Metaverse Integration

Leading luxury houses are exploring digital wearables, NFT collectibles, and metaverse-based brand experiences. Korea's tech-forward consumer base and strong gaming culture provide a fertile testing ground for next-generation luxury engagement formats.

Industry Value Chain Analysis

The South Korea luxury fashion value chain spans six stages from raw material supply to end use and lifecycle. Brand and marketing, along with distribution and retail, capture the highest value-add, while certification and resale players generate complementary downstream advantages in this brand-driven category.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Suppliers of premium leather, fabrics, metals, and precious materials, along with upstream sourcing partners supporting luxury-grade inputs |

|

Design & Production |

Couture houses, ateliers, and OEM manufacturers specializing in high-end ready-to-wear, accessories, and footwear collections |

|

Brand & Marketing |

Global luxury brand owners managing brand positioning, creative direction, advertising, and celebrity partnerships across key markets |

|

Compliance & Certification |

Standards, quality protocols, import authorities, and regulatory frameworks governing luxury imports and IP protection in South Korea |

|

Distribution & Retail |

Department store operators, flagship boutiques, duty-free outlets, and premium online platforms serving end consumers |

|

End Use & Lifecycle |

Domestic and tourist consumers, alongside resale, repair, and vintage players supporting long-term product lifecycles |

Vertically integrated houses, which manage design, sourcing, and retail in-house, achieve superior brand control and pricing power versus smaller players relying on third-party distribution partners across South Korea.

Technology Landscape in the South Korea Luxury Fashion Industry

Materials Innovation

Luxury brands are introducing sustainable and high-performance materials, such as recycled leather, bio-based fibers, and traceable textiles. These advancements support ESG goals while preserving the quality and craftsmanship expected from premium fashion houses.

Digital Authentication and Anti-Counterfeit Tech

Blockchain-based authentication, NFC tags, and digital product passports are increasingly used to verify originality, ownership history, and supply-chain transparency. Such technologies strengthen consumer trust and reduce exposure to counterfeit risks in resale markets.

Smart Retail and Omnichannel Experiences

Flagship stores in Cheongdam and Hannam-dong increasingly integrate digital styling tools, augmented reality (AR) mirrors, and clienteling apps. These tools enable personalized in-store journeys and seamless integration with online ordering, wish lists, and post-purchase services.

AI, Data Analytics, and Personalization

Luxury players are deploying AI-driven analytics for demand forecasting, customer segmentation, and tailored marketing. Personalized recommendations, curated drops, and dynamic merchandising are improving conversion rates and average ticket size across both physical and digital channels.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Clothing and Apparel |

52.4% |

2025 |

|

Distribution Channel |

Store-Based |

64.7% |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Region |

Seoul Capital Area |

45.8% |

2025 |

By Distribution Channel

Store-based commands a 64.7% majority share in 2025, driven by deep department-store penetration, alongside dedicated flagship boutiques in premium Seoul corridors. In-store experiences, personal advisors, and exclusive product launches continue to anchor consumer loyalty.

To access detailed market analysis, Request Sample

Non-store based at 35.3% in 2025 is rising rapidly through brand e-commerce, authenticated luxury platforms, and mobile shopping apps. Digital-first consumers are increasingly comfortable with online luxury purchases, supported by certification, secure logistics, and instant customer service.

By Product Type

Clothing and apparel dominate with 52.4% share in 2025, supported by demand for ready-to-wear, outerwear, knitwear, and seasonal collections. Frequent K-celebrity placements and seasonal capsule drops further reinforce category visibility and aspirational buying.

Accessories prevail in the secondary segment, with 28.6% share, driven by high-margin handbags, small leather goods, fine jewelry, and watches. Entry-luxury items, such as wallets, card holders, and scarves, attract aspirational buyers and first-time luxury consumers.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Seoul Capital Area |

45.8% |

Concentrated HNWI population, dense luxury retail corridors, mature tourism infrastructure, and strong premium consumer base |

|

Yeongnam (Southeastern Region) |

21.6% |

Expanding affluent middle class, rising premium retail footprint, and growing demand from major industrial and port cities |

|

Hoseo (Central Region) |

13.8% |

Rapid urbanization in emerging cities, expanding shopping infrastructure, and increasing penetration of premium brands beyond Seoul |

|

Honam (Southwestern Region) |

10.2% |

Steady growth in disposable incomes, regional tourism flows, and gradual expansion of luxury distribution networks |

|

Others |

8.6% |

Niche premium demand in smaller cities, tourism-led travel-retail purchases, and rising e-commerce penetration |

Seoul Capital Area at 45.8% in 2025 leads the market, anchored by Cheongdam-dong, Apgujeong, Hannam-dong, and Gangnam luxury corridors. Strong HNWI density, deep tourism flows, and concentrated brand investment continue to support sustained leadership in luxury retail.

Yeongnam (Southeastern Region) at 21.6% is supported by Busan, Daegu, and Ulsan, which combine strong industrial wealth with growing premium retail. Rising premium concessions and improving infrastructure are gradually expanding the local luxury consumer base.

Competitive Landscape

The South Korea luxury fashion market is moderately concentrated, with global luxury conglomerates dominating premium positioning, brand experiences, and flagship retail presence, while regional and specialist houses serve niche segments. Strong brand equity, controlled distribution, and integrated marketing form the key competitive moats.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Kering |

Gucci, Saint Laurent, Bottega Veneta, Balenciaga |

Leader |

Multi-brand luxury house; strong creative direction; premium retail footprint |

|

Hermès |

Hermès |

Leader |

Heritage craftsmanship; controlled distribution; high pricing power |

|

Prada S.P.A. |

Prada, Miu Miu, Versace |

Challenger |

Design-led positioning; expanding retail footprint; broad category mix |

|

Compagnie Financière Richemont SA |

Cartier, Van Cleef & Arpels |

Challenger |

Strong accessories and watch portfolio; selective luxury retail strategy |

|

Giorgio Armani S.p.A. |

Emporio Armani, Armani Exchange, Giorgio Armani |

Challenger |

Italian heritage; multi-tier brand strategy; broad lifestyle portfolio |

|

Ralph Lauren |

Purple Label, Polo Ralph Lauren |

Emerging |

American lifestyle luxury; broad apparel mix; strong department-store footprint |

Key players include Kering, Hermès, Prada S.P.A., Compagnie Financière Richemont SA, Giorgio Armani S.p.A., and Ralph Lauren, among others.

Key Company Profiles

Hermès

Hermès is a heritage French luxury house known for its iconic leather goods, ready-to-wear, silk products, and accessories, with a strong and selective retail footprint across major South Korean cities.

- Product Portfolio: Birkin and Kelly handbags, ready-to-wear collections, silk scarves and ties, footwear, jewelry, watches, and home and lifestyle products.

- Recent Developments: The brand has continued to invest in elevated retail experiences and exclusive boutiques across South Korea, while expanding waitlists for its hero leather goods, reflecting strong sustained demand from local and tourist clientele.

- Strategic Focus: Controlled production, selective distribution, deep artisan craftsmanship, and disciplined pricing power across heritage product lines and quietly expanding ready-to-wear collections.

Prada S.P.A.

Prada S.P.A. is an Italian luxury fashion group with a growing multi-brand portfolio and a strong retail footprint in South Korea through flagship boutiques and department-store concessions across Seoul and major regional cities.

- Product Portfolio: Prada ready-to-wear, leather goods, and footwear; Miu Miu fashion and accessories; Versace ready-to-wear, accessories, and footwear.

- Recent Developments: On 2 December 2025, Prada S.P.A. completed the acquisition of Versace from Capri Holdings for an enterprise value of EUR 1.25 Billion, returning the iconic house to Italian ownership and significantly expanding the group's brand portfolio.

- Strategic Focus: Integrating Versace into the group, scaling Miu Miu momentum, expanding flagship retail in South Korea, and reinforcing Italian design heritage across its multi-brand luxury portfolio.

Ralph Lauren

Ralph Lauren is an American lifestyle luxury group with a multi-tier brand portfolio, a strong department-store footprint, and standalone boutiques across South Korea catering to a broad spectrum of premium consumers.

- Product Portfolio: Purple Label highest-tier luxury menswear and tailoring; Polo Ralph Lauren ready-to-wear, accessories, and footwear.

- Recent Developments: In November 2025, Ralph Lauren staged 'Ralph Lauren Christmas' holiday pop-ups in Seoul as part of a global activation that also covered Tokyo, Los Angeles, and London, reinforcing the brand's seasonal engagement with Korean consumers.

- Strategic Focus: Elevating brand positioning, expanding higher-margin Purple Label and luxury categories, and strengthening department-store and direct-to-consumer presence across South Korea.

Market Concentration Analysis

The South Korea luxury fashion market is moderately concentrated, with the top six luxury houses (Kering, Hermès, Prada S.P.A., Compagnie Financière Richemont SA, Giorgio Armani S.p.A., and Ralph Lauren) estimated to hold a significant share of branded luxury fashion sales in 2025, driven by their flagship presence and strong department-store partnerships.

Barriers to entry include high brand-building costs, exclusive distribution agreements with major department stores, premium retail real estate scarcity in Seoul corridors, and the long timeline required to establish authentic luxury heritage, all of which favor incumbent global houses with deep capital and brand equity.

Consolidation is gradually accelerating through portfolio acquisitions, multi-brand house strategies, and the integration of premium accessory and beauty lines. Scale advantages in marketing, retail technology, and supply chain are further reinforcing the competitive position of established players in South Korea.

Investment & Growth Opportunities

Fastest-Growing Segments

Non-store based at 35.3% expands faster than the overall 2.49% market CAGR through 2034, driven by digital luxury platforms, mobile commerce, and authenticated resale channels. Accessories at 28.6% is the fastest-growing product type category as entry-luxury demand expands among younger buyers.

Emerging Sub-Markets

Yeongnam (Southeastern Region) at 21.6% is among the highest-growth regional clusters, with Busan and Daegu leading new openings. Hoseo (Central Region) and Honam (Southwestern Region) represent the largest untapped opportunities as rising disposable incomes and improving infrastructure unlock incremental luxury demand.

Venture & Investment Trends

Investment is concentrated in authenticated luxury resale platforms, AI-powered personalization engines, digital authentication technologies, and omnichannel retail infrastructure. Capital is also flowing into sustainability initiatives, traceable supply chains, and premium online platforms tailored to the Korean consumer.

Future Market Outlook (2026-2034)

The South Korea luxury fashion market is forecast to expand from USD 4.93 Billion in 2025 to USD 6.23 Billion by 2034 at a CAGR of 2.49%, adding roughly USD 1.30 Billion in incremental annual market value across the forecast period.

Four forces will shape the market through 2034: deeper digital luxury commerce; rising K-culture-driven brand demand; growth of authenticated resale and circular luxury; and a stronger pivot toward sustainable materials and traceable supply chains across all categories.

By 2034, online luxury channels are expected to account for a meaningfully larger share of premium fashion purchases. Resale and pre-owned luxury, sustainable product lines, and bespoke services are also set to play a more prominent role in the overall consumer journey.

Research Methodology

Primary Research

Primary research included structured interviews with senior brand managers at luxury fashion houses, executives of leading Korean department stores, premium online platform leaders, duty-free retail operators, and end consumers, validating market sizing, channel mix, regional demand patterns, and category-level dynamics.

Secondary Research

Secondary sources included Korea Tourism Organization data, Korea Customs Service publications, Statistics Korea releases, annual reports of listed luxury groups, investor presentations, central bank statistics, industry association data, and curated trade press covering the global and Korean luxury fashion industry.

Forecasting Models

Market forecasts used top-down and bottom-up models combining HNWI growth rates, consumer expenditure shares, inbound tourism flows, channel-level penetration, and category-level pricing. Scenario analysis addressed currency, tourism, and regulatory variation across the forecast horizon.

South Korea Luxury Fashion Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types Covered |

|

| Distribution Channels Covered | Store-Based, Non-Store Based |

| End Users Covered | Men, Women, Unisex |

| Regions Covered | Seoul Capital Area, Yeongnam (Southeastern Region), Honam (Southwestern Region), Hoseo (Central Region), Others |

| Companies Covered | Kering, Hermès, Prada S.P.A., Compagnie Financière Richemont SA, Giorgio Armani S.p.A., Ralph Lauren, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the South Korea luxury fashion market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the South Korea luxury fashion market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the South Korea luxury fashion industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the South Korea Luxury Fashion Market Report

The South Korea luxury fashion market was valued at USD 4.93 Billion in 2025, supported by affluent consumer spending, K-culture-driven demand, and recovering inbound luxury tourism.

The market is projected to grow at a CAGR of 2.49% from 2026 to 2034, reaching USD 6.23 Billion, supported by online luxury platforms, accessories demand, and growing premium retail penetration.

Store-based leads at 64.7% in 2025, anchored by increasing number of department stores and flagship boutiques. Non-store based at 35.3% is expanding faster through digital platforms.

Clothing and apparel dominate at 52.4% in 2025, driven by ready-to-wear, outerwear, and seasonal collections. Accessories at 28.6% follow, supported by demand for handbags and small leather goods.

Seoul Capital Area commands 45.8% in 2025, led by Cheongdam, Apgujeong, and Gangnam luxury corridors, supported by HNWI density, tourism flows, and dense premium retail clusters.

Leading players include Kering, Hermès, Prada S.P.A., Compagnie Financière Richemont SA, Giorgio Armani S.p.A., and Ralph Lauren, among others.

Authenticated luxury platforms, mobile-first shopping habits, fast delivery, and Gen Z preference for digital discovery are driving the rapid migration of luxury purchases to online channels in South Korea.

K-pop and K-drama stars frequently act as brand ambassadors, shaping product visibility, cultural relevance, and aspirational demand for global luxury brands among both domestic and overseas Korean consumers.

Inbound tourism supports duty-free and travel-retail luxury sales, with Chinese, Japanese, and Southeast Asian visitors driving significant demand for premium apparel, handbags, and accessories across Korean outlets.

Rising consumer focus on responsible materials, traceable supply chains, and circular luxury is pushing brands toward sustainable design, recycled inputs, and authenticated resale partnerships within the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)