Southeast Asia Cloud Computing Market Size, Share, Trends and Forecast by Service, Workload, Deployment Mode, Organization Size, Vertical, and Country, 2026-2034

Southeast Asia Cloud Computing Market Size, Share, Trends & Forecast (2026-2034)

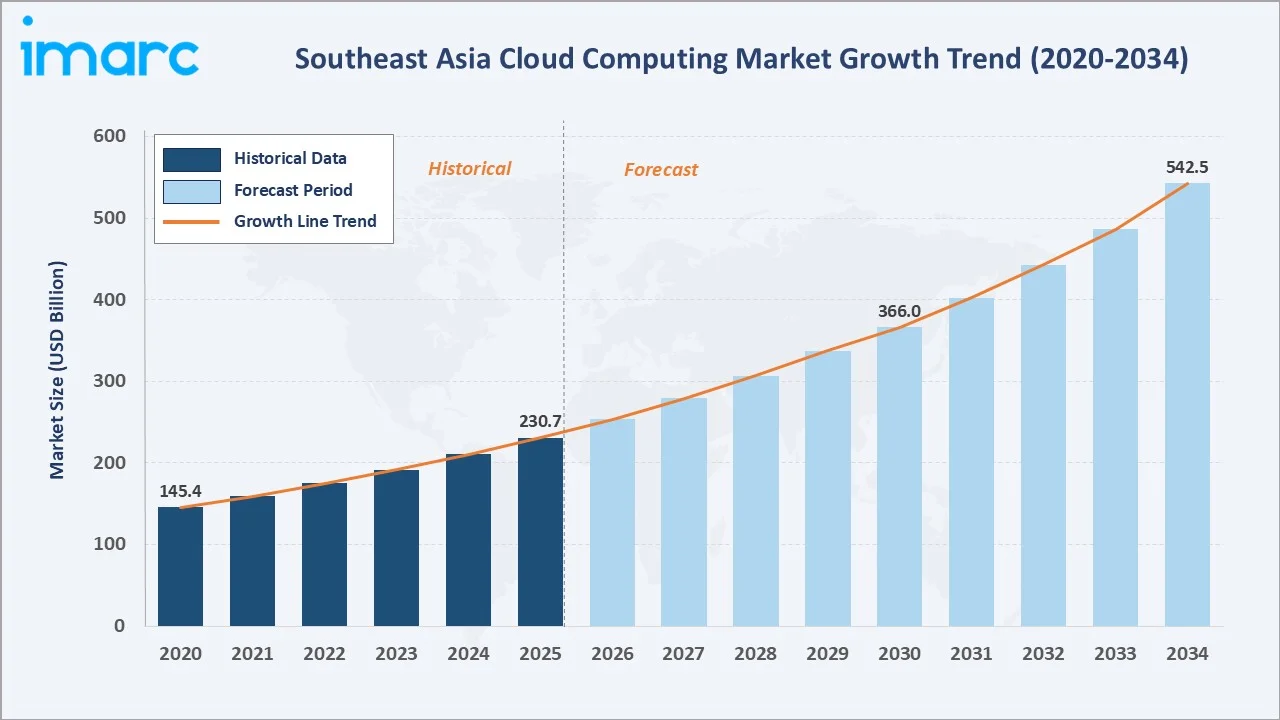

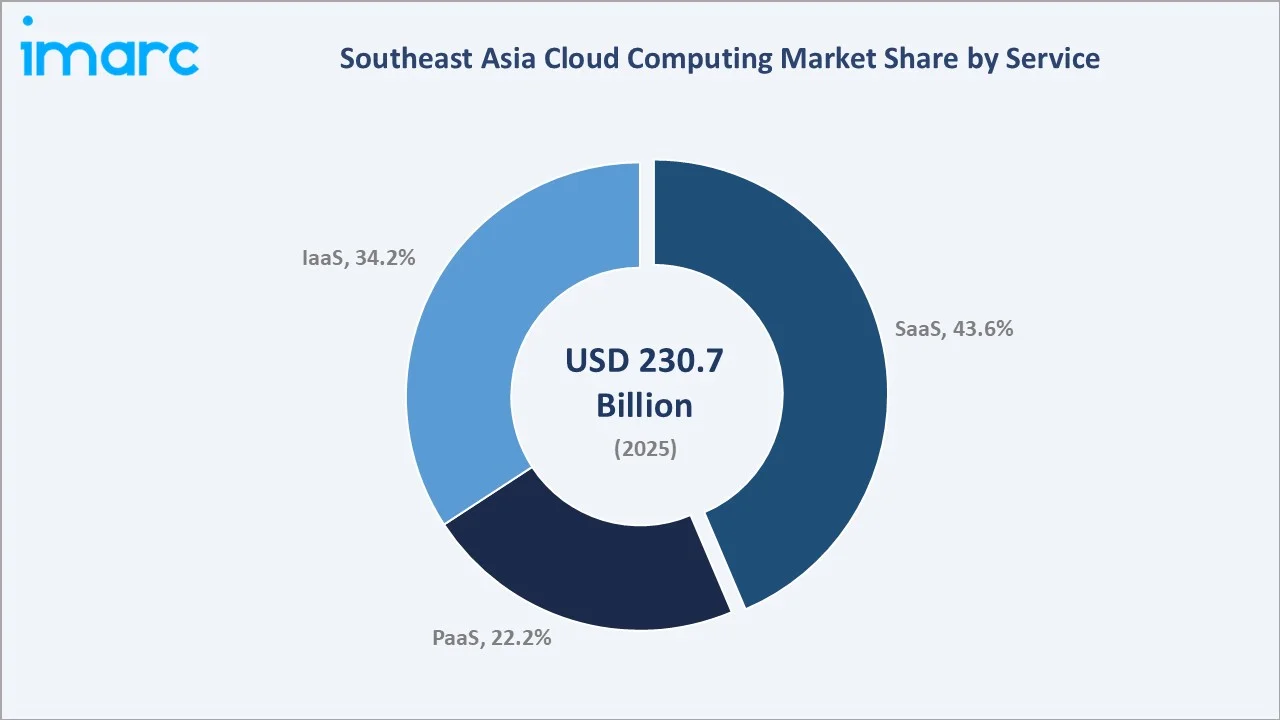

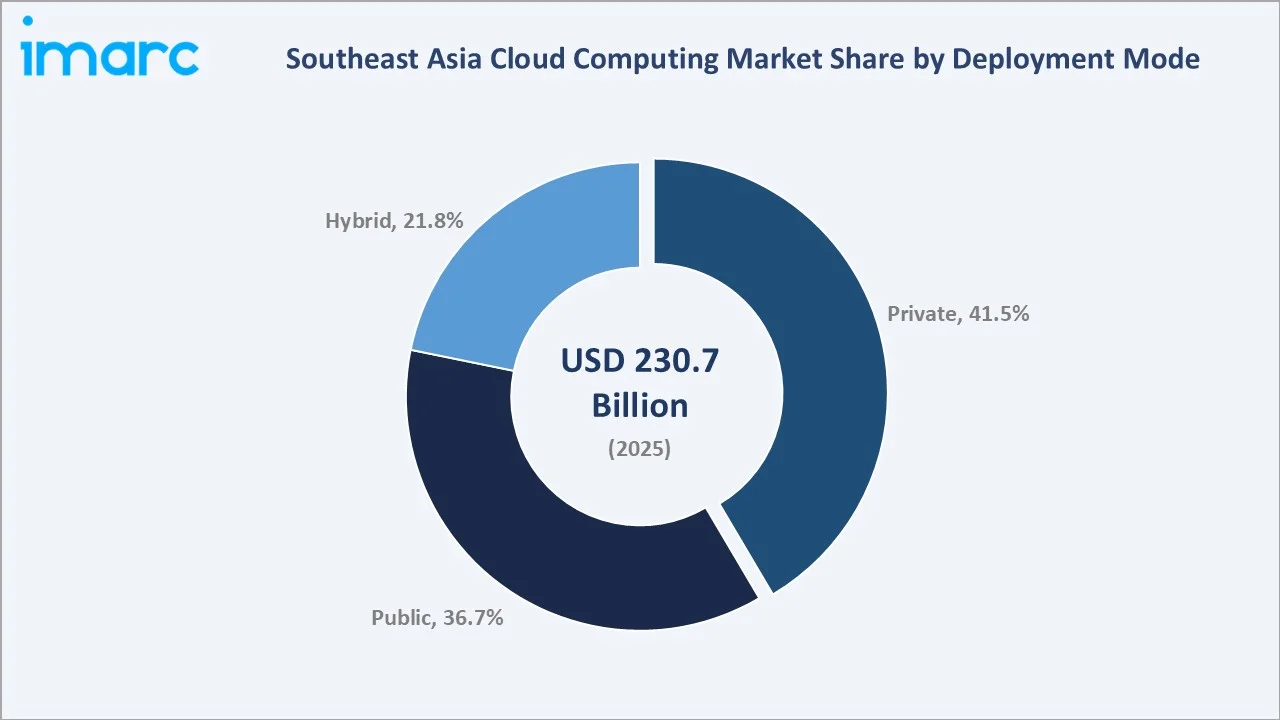

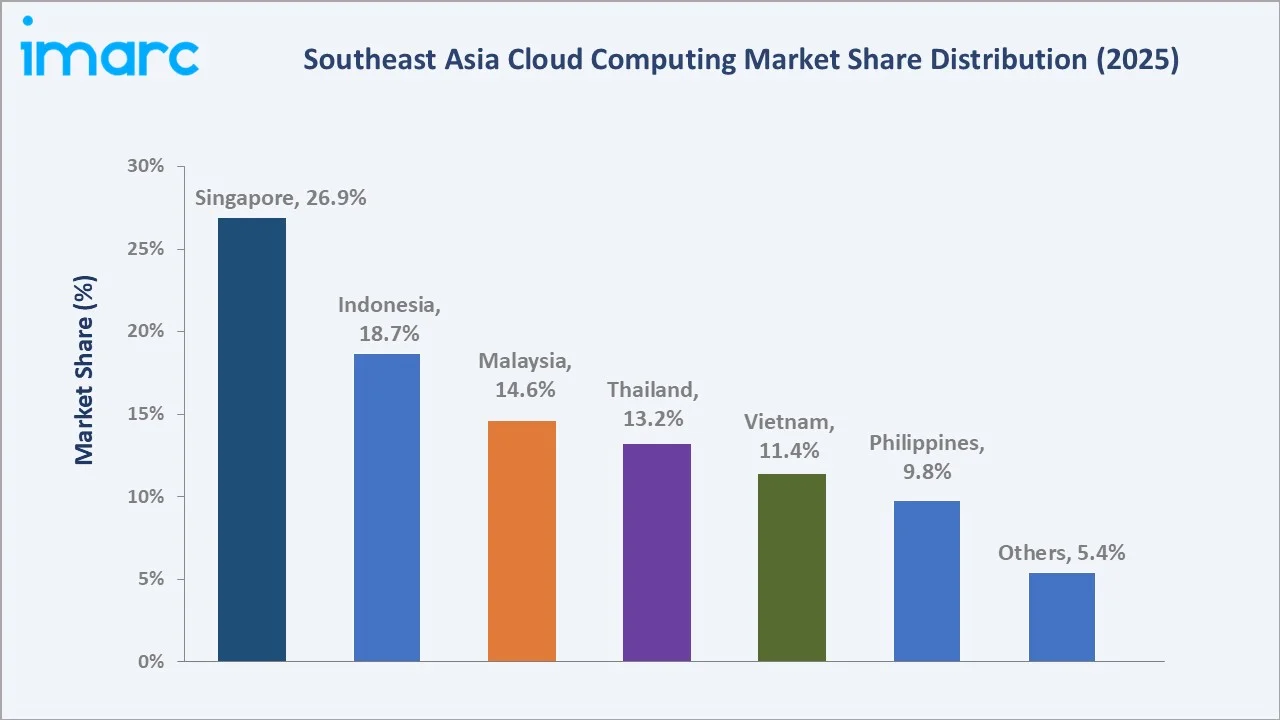

The Southeast Asia cloud computing market reached USD 230.7 Billion in 2025 and is projected to reach USD 542.5 Billion by 2034, growing at a CAGR of 9.67% during 2026-2034. Southeast Asia's digital economy targeting USD 1 Trillion by 2030, hyperscaler data center investments across SEA countries, generative AI workload adoption, government digitalization mandates, and the region's digitally connected population drive the market's robust growth. SaaS leads service type at 43.6%. Private cloud dominates deployment at 41.5%. Singapore commands 26.9% of market revenues.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 230.7 Billion |

|

Forecast Market Size (2034) |

USD 542.5 Billion |

|

CAGR (2026-2034) |

9.67% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Service |

SaaS (43.6%, 2025) |

|

Dominant Deployment Mode |

Private Cloud (41.5%, 2025) |

|

Leading Country |

Singapore (26.9%, 2025) |

The market expanded from USD 145.4 Billion in 2020 to USD 230.7 Billion in 2025, anchored at USD 366.0 Billion in 2030, and forecast to reach USD 542.5 Billion by 2034. The COVID-19 pandemic was the market's defining inflection event, forcing SEA businesses to digitize workflows, serve customers remotely, and operate distributed teams through cloud infrastructure virtually overnight, accelerating cloud adoption.

To get more information on this market, Request Sample

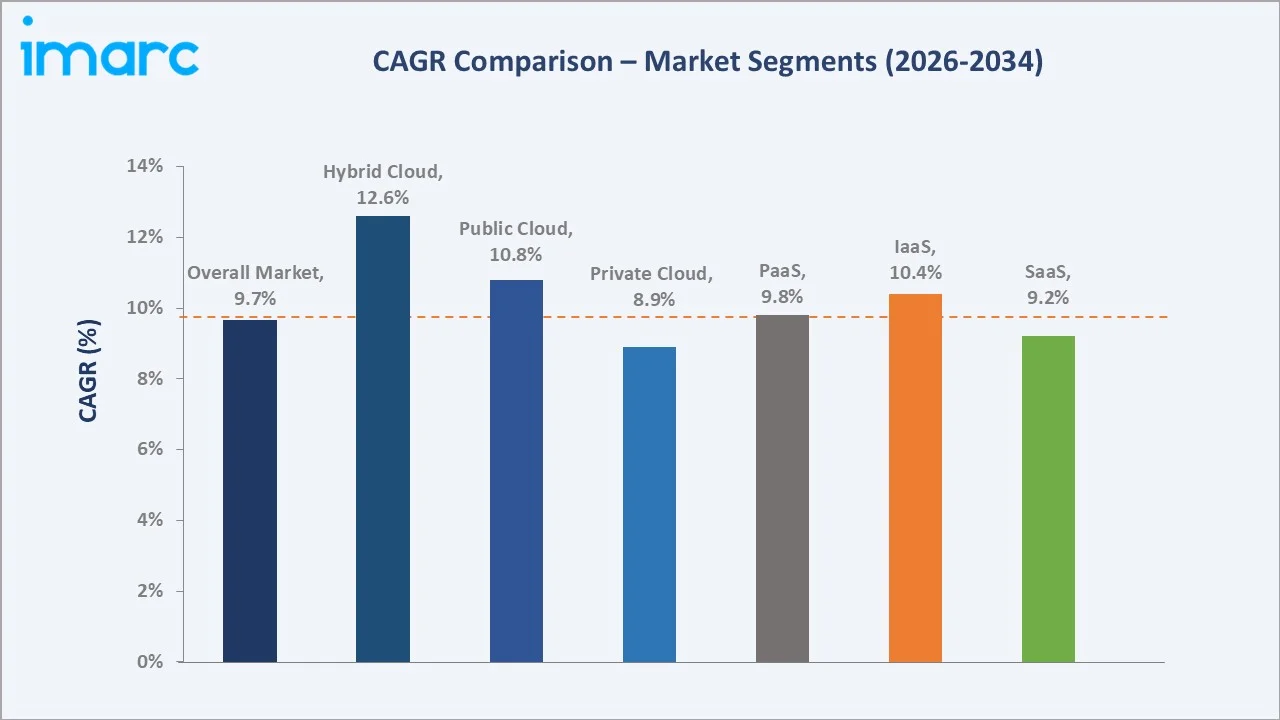

IaaS grows fastest at ~10.4% CAGR (2026-2034) as AI and ML workloads requiring GPU computing infrastructure, hyperscaler data center expansion across SEA countries, and SEA enterprises' cloud-first infrastructure strategy generate unprecedented IaaS consumption. Hybrid cloud grows fastest among deployment modes at ~12.6% CAGR as regulated industries (banking, healthcare, government) adopt hybrid architectures combining private cloud data sovereignty with public cloud scalability.

Executive Summary

The Southeast Asia cloud computing market reached USD 230.7 Billion in 2025, establishing the region as one of the Asia Pacific's largest cloud markets and one of the world's highest-growth major cloud geographies. Southeast Asia's cloud market occupies a unique structural position. The market is projected to reach USD 542.5 Billion by 2034 at 9.67% CAGR.

SaaS at 43.6% leads in Southeast Asia's businesses, from Singapore's multinational headquarters to Indonesia's 65 million MSMEs, which adopt cloud-delivered software for CRM, ERP, HR, collaboration, and industry-specific applications. Private cloud at 41.5% reflects SEA's regulatory environment, where financial sector cloud guidelines in Singapore, Indonesia, Malaysia, and Thailand require controlled data environments for sensitive financial workloads. Singapore, at 26.9%, leads through unrivalled hyperscaler infrastructure density and government cloud leadership.

Key Market Insights

|

Insight |

Data |

|

Dominant Service |

SaaS - 43.6% revenue share (2025) |

|

Dominant Deployment Mode |

Private - 41.5% market share (2025) |

|

Leading Country |

Singapore - 26.9% market share (2025) |

Key Analytical Observations Supporting the above data:

- SaaS at 43.6% reflecting SEA's SaaS-first cloud adoption pattern, where businesses bypass on-premise software for cloud-delivered applications: Southeast Asia's businesses lack the IT infrastructure and specialized IT talent required to self-manage on-premise software. SaaS eliminates this barrier, enabling an SME to deploy CRM without any server infrastructure investment.

- Private Cloud at 41.5% anchored by SEA financial sector's regulatory-compliant cloud requirements and government data sovereignty mandates: Southeast Asia's financial services regulators have collectively issued cloud outsourcing frameworks requiring banks to maintain control over sensitive customer data, operational systems, and regulatory reporting infrastructure.

- Singapore at 26.9% through unmatched hyperscaler density and Asia's most mature cloud regulatory framework: Singapore's cloud market per-capita intensity exceeds any comparable geography globally, represents 6x the per-capita cloud consumption of any other SEA country and nearly doubles Hong Kong's equivalent density.

Southeast Asia Cloud Computing Market Overview

Southeast Asia's cloud computing market encompasses all cloud service delivery models, SaaS (cloud-delivered software applications), IaaS (virtualized computing, storage, and networking infrastructure), and PaaS (cloud-based application development platforms and middleware), across three deployment architectures (public cloud, private cloud, and hybrid cloud). The market spans six primary SEA economies (Singapore, Indonesia, Malaysia, Thailand, Vietnam, Philippines) and four smaller markets (Brunei, Cambodia, Laos, Myanmar). Cloud computing has become the foundational infrastructure of Southeast Asia's digital economy, representing the digital infrastructure layer enabling the region's economic transformation.

The ecosystem integrates global hyperscalers, Chinese technology challengers, traditional enterprise technology vendors evolving cloud offerings, regional telecommunications companies building cloud businesses, managed service providers, and a vibrant regional SaaS ecosystem. Macroeconomic factors include rapid digitalization, expanding internet penetration, rising AI and data-intensive workloads, and strong GDP growth.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

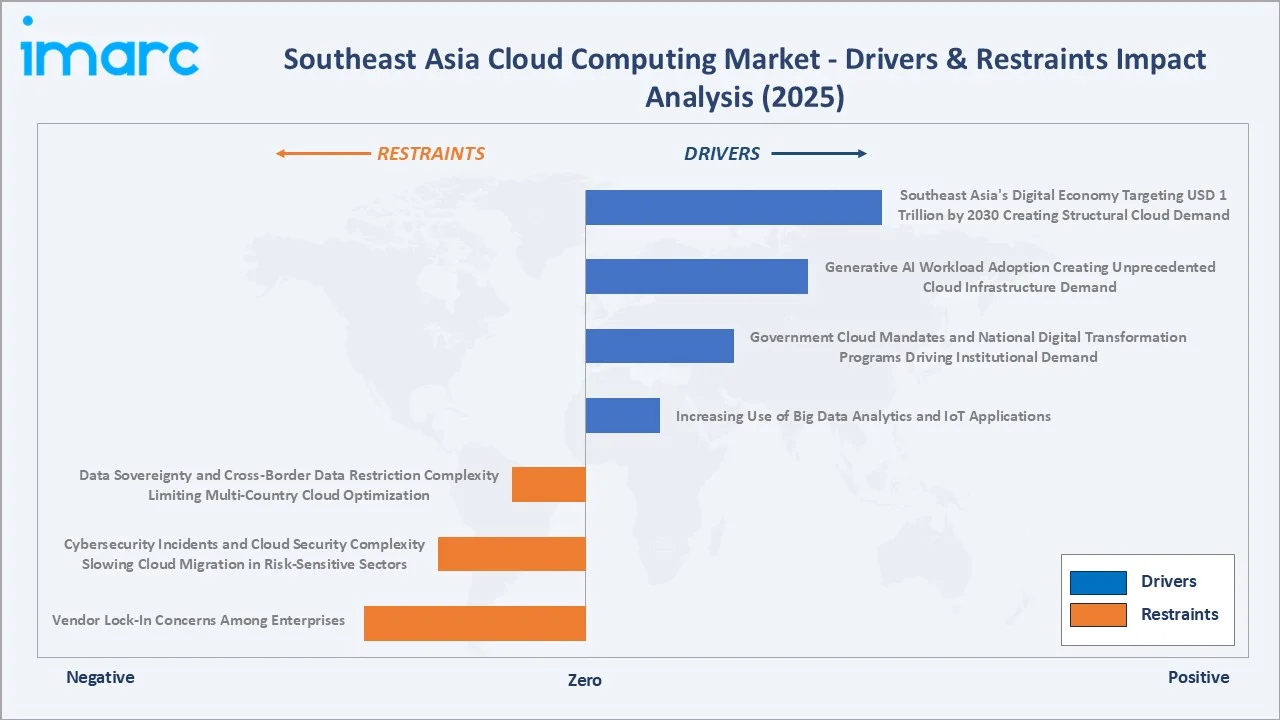

- Southeast Asia's Digital Economy Targeting USD 1 Trillion by 2030 Creating Structural Cloud Demand: Southeast Asia’s ambition to build a digital economy valued at around USD 1 trillion by 2030 is accelerating investments in cloud infrastructure, AI platforms, digital payments, e-commerce, and enterprise software ecosystems. The rapid expansion of digital businesses, online services, and data-driven operations across ASEAN countries is creating sustained demand for scalable public, private, and hybrid cloud solutions to support regional digital transformation initiatives.

- Generative AI Workload Adoption Creating Unprecedented Cloud Infrastructure Demand: The rapid adoption of generative AI applications across Southeast Asia is significantly increasing demand for high-performance cloud infrastructure, GPU-powered computing, and scalable data storage solutions. Enterprises are increasingly relying on cloud platforms to deploy AI models, automate operations, and process large datasets, encouraging hyperscalers and regional providers to expand data center capacity and AI-ready cloud services across ASEAN markets.

- Government Cloud Mandates and National Digital Transformation Programs Driving Institutional Demand: Government-led cloud-first policies and national digital transformation programs across Southeast Asia are accelerating cloud adoption among public sector institutions, healthcare systems, education networks, and state-owned enterprises. Initiatives focused on smart cities, digital governance, cybersecurity modernization, and e-government services are creating long-term institutional demand for secure and scalable cloud computing infrastructure across the region.

Market Restraints

- Data Sovereignty and Cross-Border Data Restriction Complexity Limiting Multi-Country Cloud Optimization: Southeast Asia's regulatory heterogeneity creates significant cloud architecture complexity for regional enterprises. A regional retailer operating in all major SEA markets requires separate data compliance architectures, preventing the single-region cloud optimization that a purely commercial analysis would recommend. This regulatory fragmentation adds 15-25% to SEA enterprise cloud architecture costs versus a hypothetical unrestricted deployment.

- Cybersecurity Incidents and Cloud Security Complexity Slowing Cloud Migration in Risk-Sensitive Sectors: Southeast Asia experienced the highest rate of ransomware attacks with over 135,000 ransomware attacks detected in 2024, with major incidents in Indonesia, where 57,554 attacks were detected. These incidents have reinforced government reluctance toward complete public cloud dependency and accelerated private cloud and hybrid cloud investment by governments previously planning full public cloud migration.

Market Opportunities

- AI Cloud Services Creating New Premium Market Tier Above Commodity IaaS/SaaS Pricing: Generative AI cloud services command price premiums over equivalent non-AI cloud compute. For SEA hyperscalers with existing IaaS/SaaS market positions, AI service layer adoption from current customers represents a significant ARPU (Average Revenue Per User) expansion opportunity without requiring customer acquisition.

- ASEAN Digital Economy Integration Creating Cross-Border Cloud Opportunity: ASEAN's progressive digital economic integration creates structural demand for cloud infrastructure spanning multiple SEA jurisdictions. An ASEAN-compliant cloud platform capable of managing data residency, regulatory compliance, and local language support across all ASEAN member states from a single management console represents a product opportunity no vendor has yet comprehensively delivered.

Market Challenges

- Concentrated Hyperscaler Market Power Creating Vendor Lock-In Concern for SEA Enterprises: The dominance of a few global hyperscale cloud providers in Southeast Asia is increasing vendor lock-in risks, making it difficult for enterprises to migrate workloads, maintain interoperability, or negotiate favorable pricing structures. Heavy dependence on proprietary cloud ecosystems can also limit operational flexibility, increase long-term switching costs, and create data sovereignty and compliance concerns for regional businesses.

- Power Infrastructure Constraints Limiting Data Center Expansion in Indonesia, Vietnam, and the Philippines: Southeast Asia's data center expansion is increasingly constrained by power infrastructure limitations rather than land or capital availability. Singapore imposed a three-year data center moratorium specifically due to power consumption concerns, and remaining approvals require Power Usage Effectiveness (PUE).

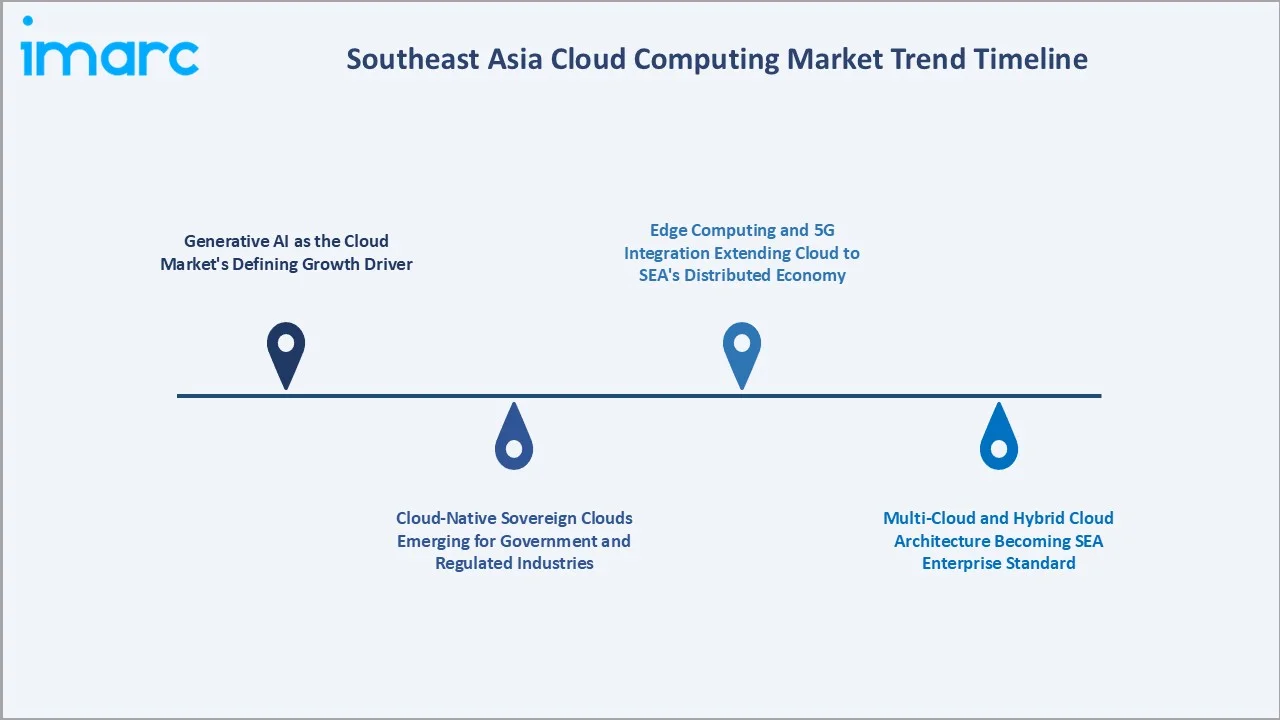

Emerging Market Trends

1. Generative AI as the Cloud Market's Defining Growth Driver

Generative AI is emerging as a defining growth trend as enterprises increasingly adopt AI-powered automation, customer analytics, and content generation tools that require scalable cloud infrastructure and high-performance GPU computing. Major hyperscalers such as Microsoft Azure, Amazon Web Services (AWS), and Google Cloud are expanding AI-ready cloud and data center investments across Singapore, Malaysia, Indonesia, and Thailand to support rising regional AI workloads and enterprise adoption.

2. Cloud-Native Sovereign Clouds Emerging for Government and Regulated Industries

Cloud-native sovereign clouds are becoming an important trend as governments and regulated sectors seek greater control over sensitive data, digital sovereignty, and compliance with local cybersecurity regulations. Telecom operators globally are increasingly prioritizing investments in AI infrastructure, and Asia Pacific companies are following the same path, with Singtel emerging as a leading player aiming to become a major Singapore provider of AI infrastructure and sovereign cloud services. The company adopted its AI-focused cloud strategy well before the recent surge in demand for sovereign cloud solutions, and recent market developments have reinforced the effectiveness of this approach.

3. Multi-Cloud and Hybrid Cloud Architecture Becoming SEA Enterprise Standard

Multi-cloud and hybrid cloud architecture is becoming a standard enterprise strategy as organizations seek greater flexibility, improved cybersecurity, and reduced dependence on a single cloud provider. Enterprises in sectors such as banking, telecom, retail, and manufacturing are increasingly combining public cloud, private cloud, and on-premises infrastructure to optimize workloads, meet data localization requirements, and enhance business continuity across ASEAN markets.

4. Edge Computing and 5G Integration Extending Cloud to SEA's Distributed Economy

The integration of edge computing with expanding 5G networks is emerging as a key trend in the Southeast Asia cloud computing market by enabling low-latency data processing and real-time application performance across distributed economies. Industries such as smart manufacturing, logistics, autonomous systems, gaming, and digital retail are increasingly adopting edge-enabled cloud infrastructure to support IoT devices, AI workloads, and faster regional connectivity across ASEAN countries.

Industry Value Chain Analysis

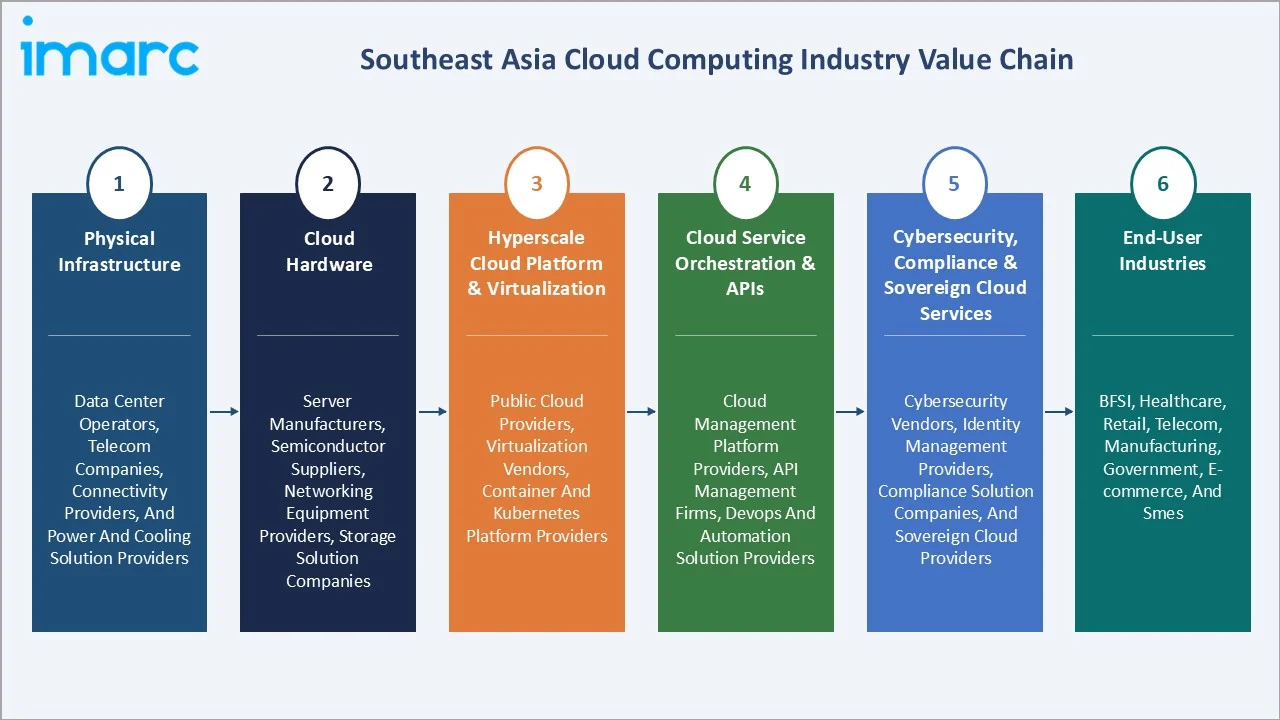

Southeast Asia's cloud value chain integrates physical data center infrastructure, hyperscale virtualization platforms, cloud service orchestration and APIs, ISV and managed service provider solution delivery, enterprise deployment and migration services, and end-user consumption and optimization. Hyperscalers capture 50-60% of value chain revenue through infrastructure ownership and platform services; SaaS vendors capture 25-30% through application software licensing; MSPs and consulting firms capture 10-15% through deployment and managed services; regional telcos capture 5-8% through domestic cloud platforms and connectivity.

|

Stage |

Key Participants |

|

Physical Infrastructure |

Data center operators, telecom companies, connectivity providers, and power and cooling solution providers |

|

Cloud Hardware |

Server manufacturers, semiconductor suppliers, networking equipment providers, storage solution companies |

|

Hyperscale Cloud Platform & Virtualization |

Public cloud providers, virtualization vendors, container and Kubernetes platform providers |

|

Cloud Service Orchestration & APIs |

Cloud management platform providers, API management firms, DevOps and automation solution providers |

|

Cybersecurity, Compliance & Sovereign Cloud Services |

Cybersecurity vendors, identity management providers, compliance solution companies, and sovereign cloud providers |

|

End-User Industries |

BFSI, healthcare, retail, telecom, manufacturing, government, e-commerce, and SMEs |

The managed service provider and ISV delivery tier is experiencing significant disruption as AI automation reduces the implementation labor previously required for cloud migration and management.

Technology Landscape in the Southeast Asia Cloud Computing Industry

AI and Machine Learning Cloud Infrastructure

AI and machine learning cloud infrastructure are rising demand for GPU-powered computing, high-performance data processing, and scalable AI model training platforms. Cloud providers are expanding AI-ready data centers, advanced analytics capabilities, and generative AI services to support enterprises across finance, healthcare, retail, and manufacturing. In March 2025, Oracle Corporation announced the establishment of an AI Centre of Excellence in Singapore aimed at supporting organizations in adapting to rapid AI advancements. The center will function as a regional hub for innovation, collaboration, and AI expertise, helping accelerate AI adoption and digital transformation initiatives across Southeast Asia.

Kubernetes and Cloud-Native Application Architecture

Kubernetes and cloud-native application architecture enable enterprises to build scalable, flexible, and containerized digital applications. Organizations are increasingly adopting microservices, container orchestration, and DevOps-driven deployment models to improve operational agility, application portability, and multi-cloud management. This trend is accelerating demand for automated cloud infrastructure, platform engineering, and cloud-native security solutions across Southeast Asian markets.

Zero Trust Security Architecture for SEA Cloud Environments

Zero Trust security architecture is emerging as enterprises strengthen cybersecurity frameworks amid rising cloud adoption and cyber threats. Organizations are increasingly implementing identity-based access controls, continuous authentication, endpoint verification, and data encryption to secure hybrid and multi-cloud environments. The growing focus on regulatory compliance, data sovereignty, and remote workforce security is further accelerating investments in Zero Trust cloud security solutions across ASEAN markets.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Service |

Software as a Service (SaaS) |

43.6% |

2025 |

|

Workload |

🔒 |

🔒 |

2025 |

|

Deployment Mode |

Private |

41.5% |

2025 |

|

Organization Size |

🔒 |

🔒 |

2025 |

|

Vertical |

🔒 |

🔒 |

2025 |

|

Country |

Singapore |

26.9% |

2025 |

By Service

SaaS leads at 43.6% market share (2025). The rapid adoption of cloud-based business applications for customer relationship management, enterprise collaboration, accounting, and human resource management among enterprises and SMEs is driving the segment growth. Its lower upfront costs, easy scalability, and growing demand for remote and digital workplace solutions continue to strengthen SaaS adoption across ASEAN countries.

To access detailed market analysis, Request Sample

IaaS at 34.2% grows fastest at ~10.4% CAGR, encompassing virtual compute, cloud storage, virtual networking, and specialized infrastructure. PaaS at 22.2% covers database services, container platforms, serverless, and developer platforms that SEA's development-intensive digital economy heavily consumes.

By Deployment Mode

Private cloud leads at 41.5% market share (2025). Private cloud in SEA encompasses government-dedicated cloud environments, financial institution cloud environments, and enterprise on-premise virtualized infrastructure. The regulatory environment across SEA's financial sector and government IT is the primary private cloud demand driver, creating a structurally large private cloud market that will not be displaced by public cloud advocacy regardless of technology efficiency arguments.

Public cloud at 36.7% grows at ~10.8% CAGR as SEA's digital economy and enterprise workloads adopt hyperscaler public cloud for its unmatched service breadth, global scale, and AI capability density. Hybrid cloud at 21.8% grows fastest at ~12.6% CAGR as SEA enterprises implement hybrid architectures connecting on-premise and private cloud with public cloud services.

Regional Market Insights

|

Country |

Share (2025) |

Key Cloud Growth Drivers & Characteristics |

|

Singapore |

26.9% |

Advanced digital infrastructure, strong data center ecosystem, supportive government policies, and position as a regional cloud hub for hyperscalers and multinational enterprises. |

|

Indonesia |

18.7% |

Driven by rapid digitalization, expanding e-commerce activities, growing startup ecosystems, rising internet penetration, and increasing enterprise cloud adoption. |

|

Malaysia |

14.6% |

Supported by digital economy initiatives, increasing investments in hyperscale data centers, expanding enterprise cloud migration, and favorable infrastructure development. |

|

Thailand |

13.2% |

Smart manufacturing adoption, digital transformation programs, expansion of 5G infrastructure, and increasing cloud utilization among enterprises and SMEs. |

|

Vietnam |

11.4% |

Supported by strong technology sector growth, rising digital businesses, expanding fintech adoption, and increasing government-led digital transformation initiatives. |

|

Philippines |

9.8% |

Expanding BPO operations, increasing remote workforce requirements, digital banking growth, and rising adoption of SaaS and hybrid cloud solutions. |

|

Others |

5.4% |

Experiencing gradual cloud adoption driven by improving internet infrastructure, digital government initiatives, SME digitalization, and rising mobile connectivity. |

Singapore's 26.9% cloud market share. The country benefits from supportive government digitalization policies, high enterprise cloud adoption, robust cybersecurity frameworks, and the presence of major global cloud providers and AI infrastructure investments. Its strategic geographic location and stable regulatory environment further strengthen its role as a regional cloud and data management center for ASEAN markets.

Indonesia's 18.7% is growing fastest. The hyperscaler tripling in Indonesia created simultaneous cloud regions in a single year. Vietnam, at 11.4%, is SEA's fastest-growing cloud market by CAGR from 2020-2025 as Vietnam's technology export economy and digital services economy generate enterprise-quality cloud demand. The Philippines, at 9.8%, is uniquely driven by the BPO sector cloud requirements, making Philippine cloud adoption more enterprise-B2B than the consumer-digital-economy-led patterns of Indonesia and Vietnam.

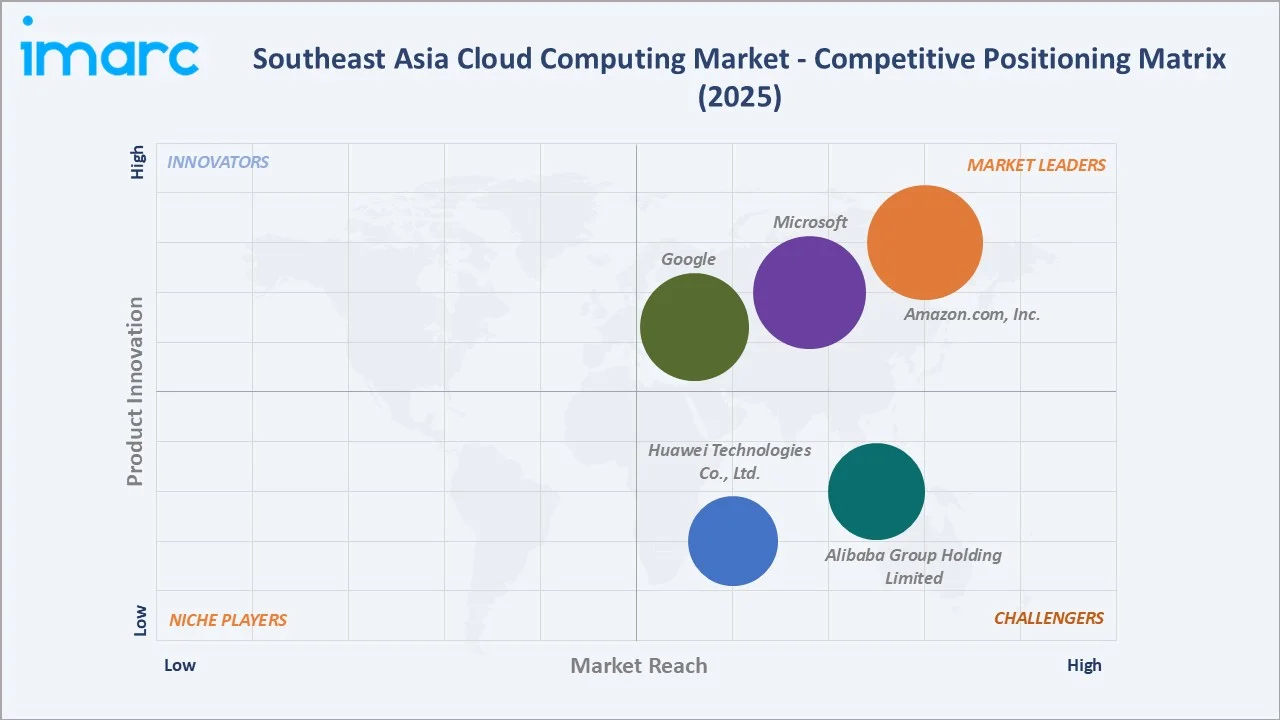

Competitive Landscape

Southeast Asia's cloud computing market is highly concentrated at the hyperscaler level. This concentration is higher than comparable markets due to hyperscalers' first-mover regional data center advantages. Once enterprises commit workloads to a regional cloud region, switching costs create sticky customer relationships.

|

Company Name |

Platform |

Market Position |

Core Strength |

|

Amazon.com, Inc. |

Amazon Web Services (AWS) |

Market Leader |

AWS is designed for security, protecting even the most sensitive workloads, such as government, financial services, and healthcare |

|

Microsoft |

Microsoft Azure |

Market Leader |

From datacenters to silicon, Azure delivers infrastructure at a global scale with more regions than any other cloud provider. |

|

|

Google Cloud |

Market Leader |

Google Cloud helps organizations build a new way forward in an increasingly AI-driven world. |

|

Alibaba Group Holding Limited |

Alibaba Cloud |

Strong Challenger |

Alibaba Cloud for AI Builders is shaping the future and Enterprises scaling AI securely. |

|

Huawei Technologies Co., Ltd. |

Huawei Cloud |

Strong Challenger |

Huawei Cloud is known for its high- performance, highly available, energy‑efficient, and open AI infrastructure |

The competitive landscape is being actively reshaped by AI differentiation, creating meaningful AI product differentiation that enterprise AI buyers use to select primary cloud providers and regional telco cloud platforms competing in government cloud, where local regulatory relationships and national data sovereignty credentials provide structural advantages over global hyperscalers.

Key Company Profiles

Amazon.com, Inc.

Amazon.com, Inc., known for its Amazon Web Services, is Southeast Asia's largest cloud provider by revenue and infrastructure scale, operating three dedicated cloud regions and is adding more.

- Platform: Amazon Web Services (AWS).

- Recent Developments: In June 2025, Amazon Web Services (AWS) launched its first Asia Pacific AWS Innovation Hub in Singapore, creating an interactive facility where business leaders can explore AWS, Amazon technologies, and partner-led cloud solutions across multiple real-world use cases. The center is designed to support enterprise digital transformation by providing practical cloud adoption strategies and customized innovation roadmaps powered by AWS’s Vision Builder platform.

- Strategic Focus: Expanding hyperscale cloud infrastructure, AI-ready data centers, enterprise digital transformation services, and sovereign cloud capabilities across Southeast Asia.

Microsoft

Microsoft, with its Azure platform, is Southeast Asia's most enterprise-penetrated cloud provider, leveraging Microsoft's existing enterprise software relationships to convert on-premise workloads to Azure cloud.

- Platform: Microsoft Azure

- Recent Developments: In April 2026, Microsoft launched Microsoft Fabric Go Local in Singapore to address data residency and compliance requirements for government and regulated sector workloads, alongside the introduction of Windows 365 Link devices that enable secure remote access to Cloud PCs.

- Strategic Focus: Expanding AI-powered cloud services, sovereign cloud infrastructure, enterprise digital transformation, and secure hybrid cloud solutions across Southeast Asia.

Market Concentration Analysis

Southeast Asia's cloud market is highly concentrated, with the top 3 players (Amazon, Microsoft, and Google) commanding approximately 55-60% of total market revenues, with Alibaba Cloud adding 8-10% for a combined Big Four cloud market share of 63-70%. This concentration exceeds US market concentration due to hyperscalers' compounding first-mover advantages in SEA, early regional data center investment creates lock-in for regional enterprises, and each enterprise customer's workload migration creates a network of system integrators, consultants, and ISVs building around that customer's chosen platform, reinforcing platform adoption momentum.

Regional differentiation in cloud concentration is notable; Singapore is the most concentrated, while Vietnam and Indonesia show more balanced competition as domestic providers and Huawei Cloud compete with hyperscalers for government and SOE cloud mandates. The Philippines' concentration is unique. Concentration is expected to slightly decrease through 2034 as Huawei Cloud's government cloud wins create systematic first-mover positions in Indonesia, Malaysia, Vietnam, and Thailand government sectors; regional telcos create protected domestic cloud segments through regulatory preference; and the AI model layer introduces new competitive dynamics as open-source AI models reduce enterprise AI provider dependency on hyperscaler proprietary AI APIs.

Investment & Growth Opportunities

Fastest Growing Segments

Hybrid cloud deployment (~12.6% CAGR), IaaS service (~10.4% CAGR), public cloud deployment (~10.8% CAGR), AI/ML cloud services (~35%+ CAGR from 2022 base), PaaS (~9.8% CAGR), and the Vietnam country market (~15-18% CAGR) represent Southeast Asia's highest-growth cloud investment vectors through 2034.

Emerging Market Opportunities

Vietnam's cloud market represents SEA's most disproportionate growth opportunity relative to its current market share. Vietnam's population, GDP growth, world-leading manufacturing export orientation, and technology sector ambition create the structural prerequisites for cloud market growth that will likely see Vietnam challenge the Philippines for SEA's 5th-largest cloud market position by 2030. Investors establishing cloud infrastructure or SaaS businesses in Vietnam in 2026-2028 will benefit from first-mover advantages in a market at the early exponential phase of cloud adoption.

Investment Themes

- Sovereign cloud and government cloud platform development for SEA national AI strategies: Singapore, Indonesia, Malaysia, Thailand, and Vietnam are each developing national AI strategies requiring dedicated AI computing infrastructure. Investors supporting national AI cloud infrastructure development can capture a structurally protected government cloud segment growing at 20-25% annually, with long-term government contracts providing revenue certainty unavailable in commercial cloud markets.

- Multi-cloud management and FinOps services for SEA's growing cloud spending optimization market: As SEA enterprises' cloud spending grows from 2025 baseline to 2034 projections, the inefficiency embedded in first-generation cloud deployments becomes increasingly costly. Regional MSPs developing differentiated FinOps capabilities for SEA's unique multi-cloud regulatory environment can command significant engagement fees from large enterprise clients seeking to rationalize growing cloud budgets.

Future Market Outlook (2026-2034)

The Southeast Asia cloud computing market is projected to grow from USD 230.7 Billion in 2025 to USD 542.5 Billion by 2034, delivering a 9.67% CAGR and 135% market expansion over the forecast period. The market's anchor value of USD 366.0 Billion in 2030 represents a Southeast Asian cloud ecosystem where generative AI has become embedded in all enterprise cloud deployments, hybrid and multi-cloud architectures have become the standard for regulated industries, and at least 3 SEA countries (Singapore, Indonesia, Malaysia) have achieved cloud penetration rates comparable to middle-income developed market benchmarks. The transition from infrastructure-led cloud growth to intelligence-led cloud growth is the fundamental market transition defining the 2025-2034 forecast period.

Three structural forces define Southeast Asia's cloud market growth with high certainty through 2034: SEA's digital economy growth to USD 1 Trillion (2030) requires proportional cloud infrastructure scaling, with AI-native digital economy applications requiring 3-5x cloud spend per unit of economic output versus traditional digital economy applications; hyperscaler data center investment commitments creating irreversible infrastructure capacity that generates self-fulfilling enterprise cloud adoption through availability, performance, compliance certifications, and price reductions that competitive infrastructure supply enables; and government digital transformation across SEA citizens creating sovereign cloud demand that grows structurally independent of private sector economic cycles.

Research Methodology

Primary Research

Primary research comprised structured interviews with 70+ industry stakeholders (2025), including Cloud Architecture leads from AWS SEA, Microsoft Azure SEA, Google Cloud SEA, Alibaba Cloud SEA, and Huawei Cloud SEA; CTO and CIO executives from DBS Bank, GRAB, Sea Limited, Tokopedia, Gojek, and GovTech Singapore; cloud practice directors; enterprise technology directors from major SEA banks, telcos, and manufacturing conglomerates; and startup technology founders from 30+ SEA cloud-native companies across Singapore, Indonesia, Malaysia, Thailand, Vietnam, and the Philippines.

Secondary Research

Secondary research encompassed AWS, Microsoft, Google, and Alibaba annual reports and investor presentations (2023-2025), IDC Asia Pacific Cloud Computing Market Report 2025, Gartner Magic Quadrant for Cloud Infrastructure and Platform Services 2025, Google SEA 2024 report, IMDA Singapore Data Center Road Map 2025, ASEAN Digital Integration Framework monitoring reports, national digital economy strategy documents, World Bank Southeast Asia Digital Economy Report 2025, and company-specific press releases and investor communications for all 12 profiled companies. Over 110 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using bottom-up service type and deployment mode models calibrated against IDC SEA quarterly cloud tracker data, Gartner cloud revenue databases, hyperscaler annual report geographic revenue disclosures, and IMDA SEA cloud spending survey data. Key inputs include SEA GDP growth projections, digital economy GMV projections, hyperscaler data center investment commitment timelines, AI workload cloud spending growth multipliers from NVIDIA and McKinsey AI infrastructure research, and SEA enterprise cloud adoption rate progression models based on analogous market developments in Australia and South Korea.

Southeast Asia Cloud Computing Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Segment Coverage |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Service | Infrastructure as a Service (IaaS), Platform as a Service (PaaS), Software as a Service (SaaS) |

| Workload | Application Development and Testing, Business Analytics, Data Storage, Backup and Disaster Recovery, Integration and Orchestration, Collaboration and Content Management, Others |

| Deployment Mode | Public, Private, Hybrid |

| Organization Size | Large Enterprise, Small and Medium Enterprise |

| Vertical | BFSI, IT and Telecom, Retail and Consumer Goods, Energy and Utilities, Healthcare, Media and Entertainment, Government and Public Sector, Others |

| Countries Covered | Indonesia, Philippines, Vietnam, Malaysia, Singapore, Thailand, Others |

| Companies Covered | Amazon.com, Inc., Microsoft, Google, Alibaba Group Holding Limited, Huawei Technologies Co., Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Southeast Asia Cloud Computing Market Report

The Southeast Asia cloud computing market reached USD 230.7 Billion in 2025, driven by SEA's digital economy, hyperscaler data center investments across SEA countries, COVID-accelerated enterprise cloud migration, government digitalization mandates, and the digital economy ecosystem generating cloud-native infrastructure demand.

The market grows at 9.67% CAGR during 2026-2034, reaching USD 542.5 Billion by 2034, driven by SEA's digital economy targeting USD 1 Trillion by 2030, generative AI workload adoption creating premium cloud demand, hybrid cloud maturation in regulated industries, Indonesia and Vietnam's rapidly growing cloud markets, and ASEAN DEFA simplifying cross-border cloud service delivery.

SaaS leads at 43.6% through Microsoft 365, Google Workspace, Salesforce, and SAP cloud adoption.

Private cloud leads at 41.5% through SEA's regulatory-driven financial sector and government sovereign cloud mandates.

Singapore leads at 26.9% through unmatched hyperscaler density, government Smart Nation cloud-first mandates, and MNC regional headquarters consuming Singapore cloud regions for ASEAN-wide operations.

Leading companies include Amazon.com, Inc., Microsoft, Google, Alibaba Group Holding Limited, and Huawei Technologies Co., Ltd., among others.

The market is projected to reach approximately USD 366.0 Billion by 2030, with AI cloud services overtaking traditional SaaS as the growth, hybrid cloud becoming the default architecture for SEA-regulated industries, and Vietnam emerging as the fastest-growing cloud market.

GenAI is creating a new premium cloud service layer commanding 3-8x price premiums over commodity IaaS. Azure OpenAI, AWS cloud, and other cloud platforms are driving 30-40% increases for existing enterprise cloud customers.

Three priority opportunities: national AI cloud infrastructure development; vertical SaaS for SEA's underserved manufacturing, agriculture, and healthcare sectors; and multi-cloud FinOps services capturing SEA enterprises' estimated 30-35% cloud overspend.

Vietnam has the highest CAGR growth potential given its combination of population, world-leading manufacturing FDI, domestic tech sector ambition, IT engineers target by 2030, and current cloud penetration significantly below peers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade