Southeast Asia Semiconductor Market Size, Share, Trends and Forecast by Components, Material Used, End User, and Country, 2026-2034

Southeast Asia Semiconductor Market Size, Share, Trends & Forecast (2026-2034)

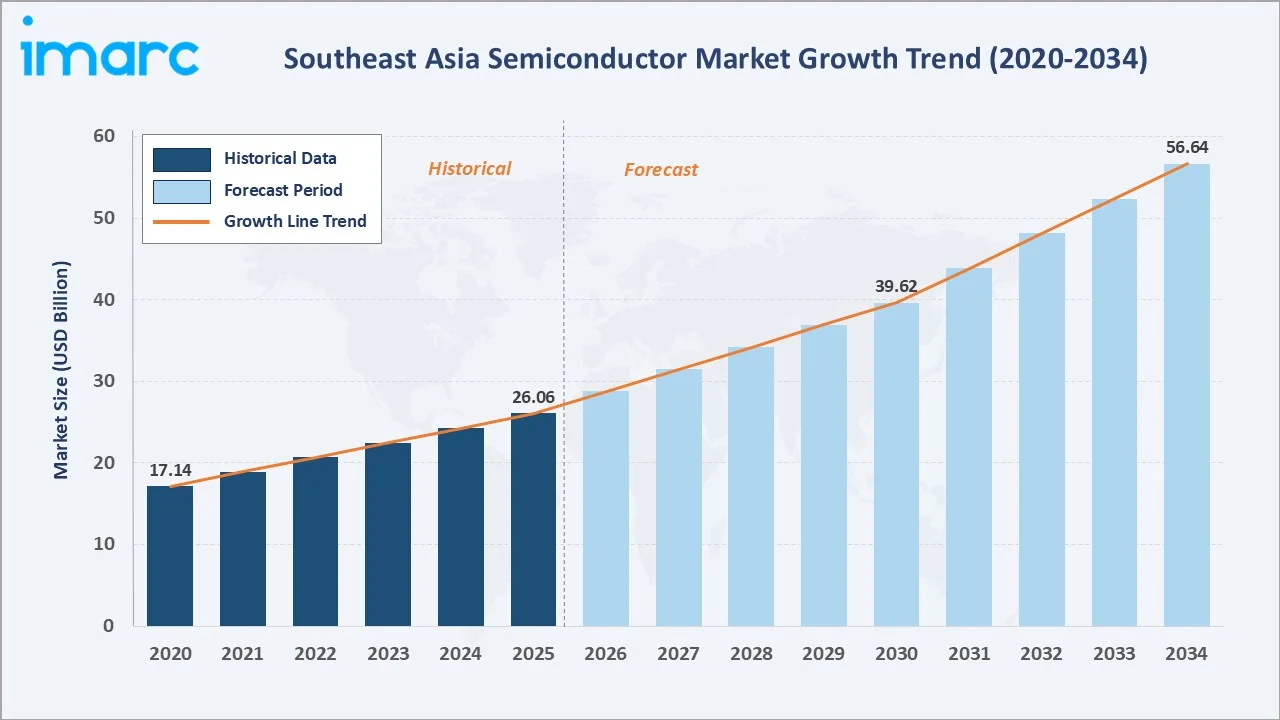

The Southeast Asia semiconductor market reached USD 26.06 Billion in 2025 and is projected to reach USD 56.64 Billion by 2034, growing at a CAGR of 8.74% during 2026-2034. The US-China geopolitical semiconductor supply chain reconfiguration, driving SEA fab investment, EV power electronics surge with Thailand aims for EVs to account for 30% of its total vehicle production by 2030, creating unprecedented SiC demand, AI and data center GPU supply chain localization, and ASEAN governments' national semiconductor strategies collectively anchor the market's robust growth. Silicon Carbide leads the material type at 28.5%. Consumer electronics dominate the end user at 26.8%. Singapore commands 27.9% of regional market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 26.06 Billion |

|

Forecast Market Size (2034) |

USD 56.64 Billion |

|

CAGR (2026-2034) |

8.74% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Material |

Silicon Carbide (28.5%, 2025) |

|

Dominant End User |

Consumer Electronics (26.8%, 2025) |

|

Leading Country |

Singapore (27.9%, 2025) |

The market expanded from USD 17.14 Billion in 2020 to USD 26.06 Billion in 2025, anchored at USD 39.62 Billion in 2030, and forecast to reach USD 56.64 Billion by 2034. The 2020 COVID-19 semiconductor shortage validated SEA's critical position in the global semiconductor supply chain and accelerated government and private sector investment in supply chain resilience that has characterized the 2022-2025 investment boom.

To get more information on this market, Request Sample

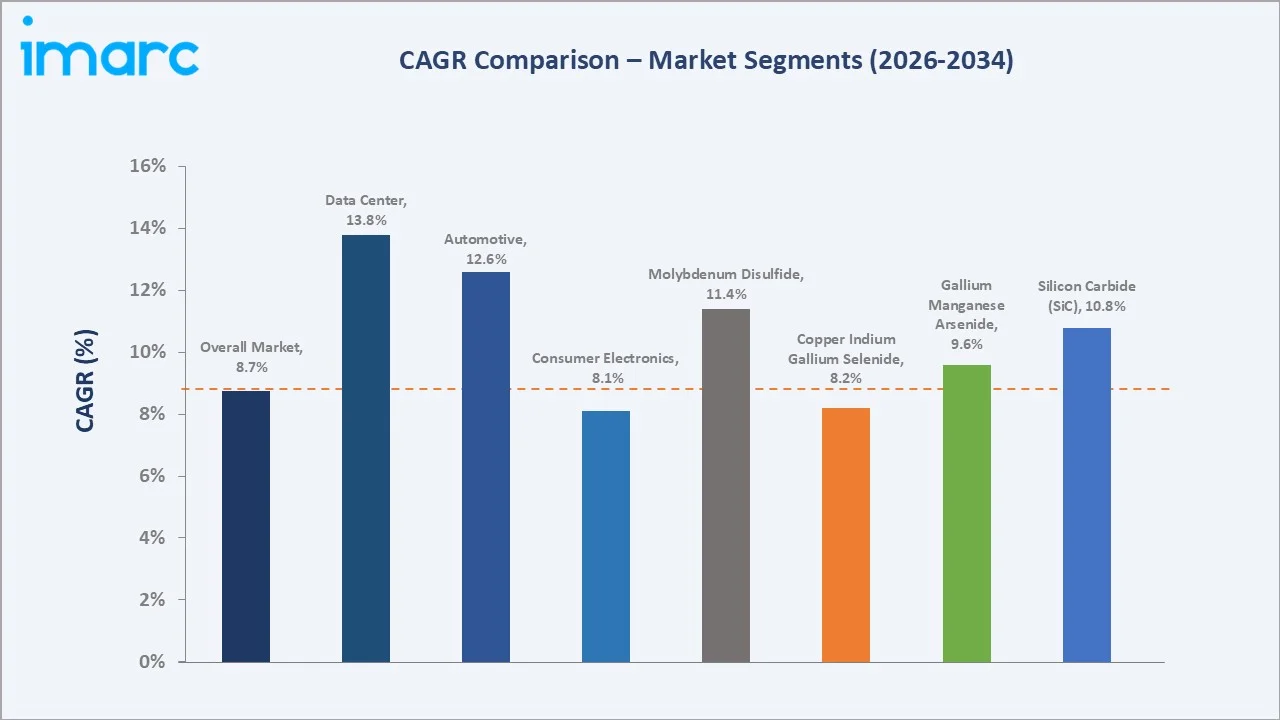

Molybdenum disulfide grows fastest at ~11.4% CAGR as this 2D transition metal dichalcogenide material enables sub-3nm transistors beyond silicon's physical scaling limits, with foundry research from TSMC Singapore R&D and GlobalFoundries' Singapore-based materials research positioning SEA at the frontier of post-silicon materials. Data center grows fastest among end users at ~13.8% CAGR as SEA hyperscaler investment drives semiconductor demand for server processors.

Executive Summary

The Southeast Asia semiconductor market reached USD 26.06 Billion in 2025, establishing SEA as the world's most strategically important semiconductor manufacturing geography outside Taiwan, South Korea, and the United States. Southeast Asia's semiconductor ecosystem spans raw material processing, wafer fabrication, back-end OSAT assembly and test, and IC design. The market is projected to reach USD 56.64 Billion by 2034 at 8.74% CAGR.

Silicon carbide at 28.5% leads as the semiconductor material most transformed by the EV revolution. Consumer electronics at 26.8% reflects SEA's established role as the world's primary semiconductor back-end supply chain for consumer products. Singapore, at 27.9%, leads through its concentration of wafer fabrication, IC design, and semiconductor trade functions.

Key Market Insights

|

Insight |

Data |

|

Dominant Material Used |

Silicon Carbide - 28.5% share (2025) |

|

Dominant End User |

Consumer Electronics - 26.8% market share (2025) |

|

Leading Country |

Singapore - 27.9% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- Silicon Carbide at 28.5% reflecting SEA's strategic position in the global EV power semiconductor supply chain: SiC-based power devices have emerged as the defining semiconductor technology of the EV transition. Each EV requires USD 600-1,200 in SiC content, versus USD 100-200 for conventional ICE vehicles.

- Consumer electronics at 26.8% reflecting SEA's position as the world's primary back-end semiconductor supply chain for global brands: Every iPhone, Samsung Galaxy, and Dell laptop contains semiconductors assembled in Southeast Asia. Apple's supply chain concentration creates annual semiconductor processing of USD 8-10 Billion attributable to Apple's devices alone.

- Singapore at 27.9% through its unique combination of wafer fabrication, IC design, and semiconductor trade: Singapore's semiconductor market revenue concentration exceeds its manufacturing employment share because Singapore captures the highest value-added functions.

Southeast Asia Semiconductor Market Overview

The Southeast Asia semiconductor market encompasses the design, fabrication, packaging, testing, and distribution of semiconductor integrated circuits, discrete devices, and optoelectronics across the ASEAN region. SEA's semiconductor industry operates across four distinct functional tiers: wafer fabrication in Singapore, Malaysia, and Thailand; OSAT back-end assembly and test in Malaysia, Philippines, Thailand, and Vietnam; IC design centered in Singapore with secondary hubs in Malaysia and Vietnam; and distribution and trade centered in Singapore as the primary semiconductor trading hub for APAC.

The ecosystem integrates multinational semiconductor companies' SEA operations as fabrication and back-end anchors, locally-listed OSAT champions in Malaysia and Singapore, and government investment agencies driving capacity expansion. Macroeconomic factors include rapid digitalization, expanding electronics manufacturing, rising EV and AI adoption, and increasing demand for consumer electronics and data center infrastructure.

Market Dynamics

To evaluate market opportunities, Request Sample

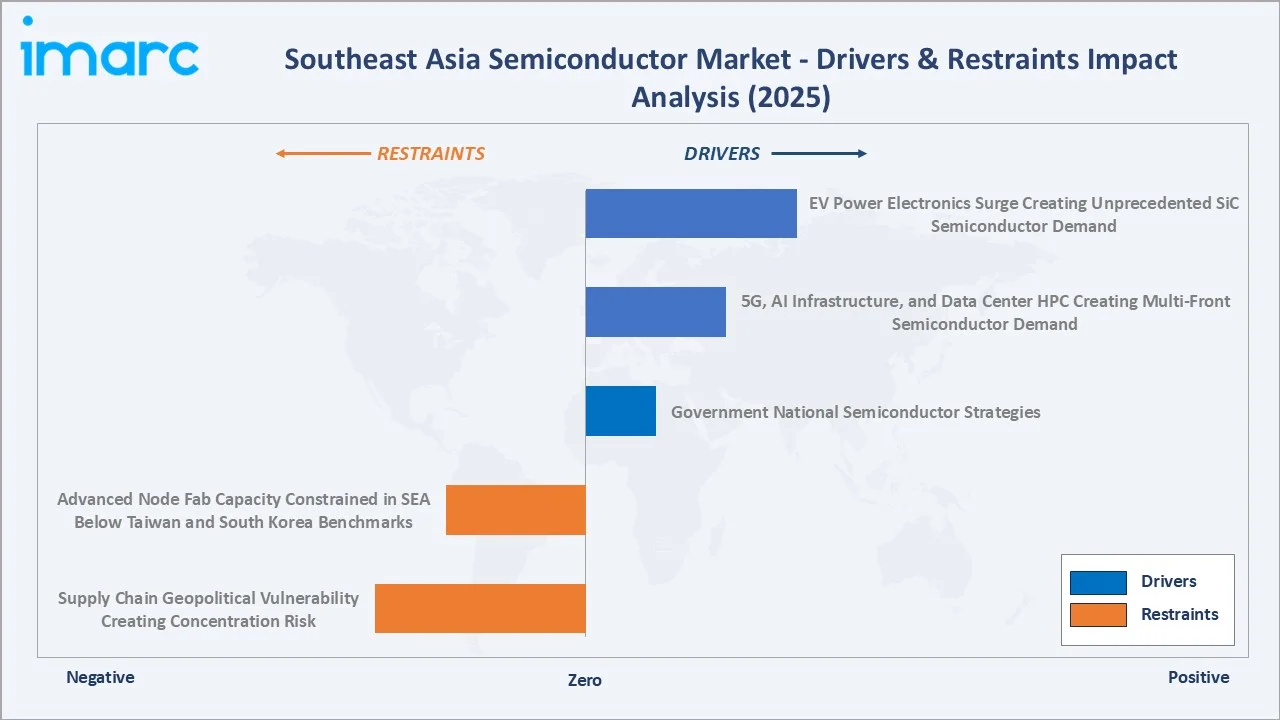

Market Drivers

- EV Power Electronics Surge Creating Unprecedented SiC Semiconductor Demand: In Singapore, electric vehicles (EVs) accounted for 57.6% of the 13,322 new cars registered in the first three months of 2026. The rapid growth of electric vehicle production is increasing demand for silicon carbide (SiC) semiconductors used in EV powertrains, fast-charging systems, and battery management applications.

- 5G, AI Infrastructure, and Data Center HPC Creating Multi-Front Semiconductor Demand: The expansion of 5G networks, AI infrastructure, and hyperscale data centers across Southeast Asia is significantly increasing demand for advanced semiconductors such as processors, GPUs, memory chips, and networking components. Growing investments in cloud computing, AI model training, and high-performance computing facilities are accelerating semiconductor consumption across telecommunications, enterprise, and digital infrastructure applications.

- Government National Semiconductor Strategies: Every primary SEA semiconductor economy has launched a national semiconductor strategy with significant public investment. In Singapore, EDB secured S$14.2 billion in Fixed Asset Investments and S$8.9 billion in Total Business Expenditure, with the investments expected to create 15,700 jobs and generate S$18 billion in value-added contribution over the next five years. Thailand's BOI offers 8-year tax holidays. Collectively deploying government support, these programs multiply private sector investment by creating the total investment pipeline characterizing SEA's semiconductor boom.

Market Restraints

- Advanced Node Fab Capacity Constrained in SEA Below Taiwan and South Korea Benchmarks: Southeast Asia's semiconductor manufacturing is concentrated in mature nodes and back-end OSAT rather than the advanced nodes commanding the highest semiconductor value. The absence of leading-edge logic fab capacity means SEA misses the highest-value semiconductor content in AI GPUs and smartphone SoCs manufactured outside SEA.

- Supply Chain Geopolitical Vulnerability Creating Concentration Risk: SEA's supply chain depends on US semiconductor equipment, including Japanese chemicals, where suppliers hold 60-80% global market share, and Taiwanese wafer supply, creating multiple chokepoints where geopolitical events could disrupt SEA manufacturing.

Market Opportunities

- Advanced Packaging Creating New SEA Market Segment: The semiconductor industry's response to end-of-Moore's-Law is heterogeneous integration, combining chiplets in a single package using interposer and stacking techniques requiring sophisticated back-end expertise precisely suited to SEA's OSAT strengths.

- Vietnam Emerging as SEA's Fastest-Growing Semiconductor Manufacturing Economy: Vietnam's competitive manufacturing costs 30-40% below Malaysia, US strategic partnership commitments, Samsung and Intel anchor tenant validation, and the government's semiconductor engineer development target create conditions for Vietnam to capture 15-20% of new SEA semiconductor OSAT investment through 2034.

Market Challenges

- China's Domestic Semiconductor Investment Creating Competitive Pressure on SEA OSAT Economics: China's national semiconductor program is developing domestic OSAT capacity that competes directly with Malaysia, Philippines, and Thailand's back-end manufacturing cost base. Chinese OSAT operations benefit from subsidized land, energy, and capital costs, enabling pricing 10-20% below comparable SEA OSAT facilities for commodity packaging.

- Semiconductor Cycle Volatility Creating Investment Uncertainty for SEA Capacity Expansion: The semiconductor industry's boom-bust cycle creates persistent uncertainty for long-horizon capacity investment decisions. The 3-5 year lead times for advanced packaging and SiC fab investment require committing capital when short-term revenue visibility is poor, affecting private OSAT companies more severely than multinational semiconductor companies with diversified revenue bases.

Emerging Market Trends

1. Silicon Carbide Manufacturing Cluster Forming in Malaysia's Kedah State

Malaysia’s Kedah state is emerging as a major silicon carbide (SiC) semiconductor manufacturing cluster due to increasing investments and facilities in power electronics and EV-related chip production. In August 2024, Infineon Technologies launched the first phase of its new Malaysia facility, which is set to become the world’s largest and most competitive 200-mm silicon carbide (SiC) power semiconductor fab, supporting growing global demand driven by decarbonization efforts.

2. OSAT Advanced Packaging Transition Reshaping SEA's Back-End Semiconductor Industry

The transition toward advanced outsourced semiconductor assembly and testing (OSAT) packaging technologies is reshaping Southeast Asia’s back-end semiconductor industry as demand grows for AI, high-performance computing, and advanced consumer electronics chips. Companies across Malaysia, Singapore, Vietnam, and Thailand are investing in technologies such as 2.5D/3D packaging, chiplet integration, and heterogeneous packaging to support next-generation semiconductor performance requirements. This shift is strengthening the region’s competitiveness in the global semiconductor value chain beyond traditional assembly and testing operations.

3. Compound Semiconductor Materials Displacing Silicon in Premium Applications

Compound semiconductor materials such as silicon carbide (SiC) and gallium nitride (GaN) are increasingly replacing traditional silicon in premium applications requiring higher efficiency, faster switching speeds, and better thermal performance. Rising demand from electric vehicles, renewable energy systems, AI infrastructure, and advanced industrial electronics is accelerating investment in compound semiconductor manufacturing across Southeast Asia. This trend is strengthening the region’s role in next-generation power and high-performance semiconductor technologies.

4. Vietnam's Semiconductor Talent Development Creating ASEAN's Next Major Design Economy

Vietnam is emerging as a key semiconductor design and engineering hub in Southeast Asia through aggressive investments in semiconductor talent development, technical education, and international industry partnerships. Government-backed initiatives and collaborations with global chip companies are expanding the country’s skilled workforce in chip design, testing, and embedded engineering. This growing talent ecosystem is positioning Vietnam as ASEAN’s next major semiconductor design economy alongside its expanding electronics manufacturing base.

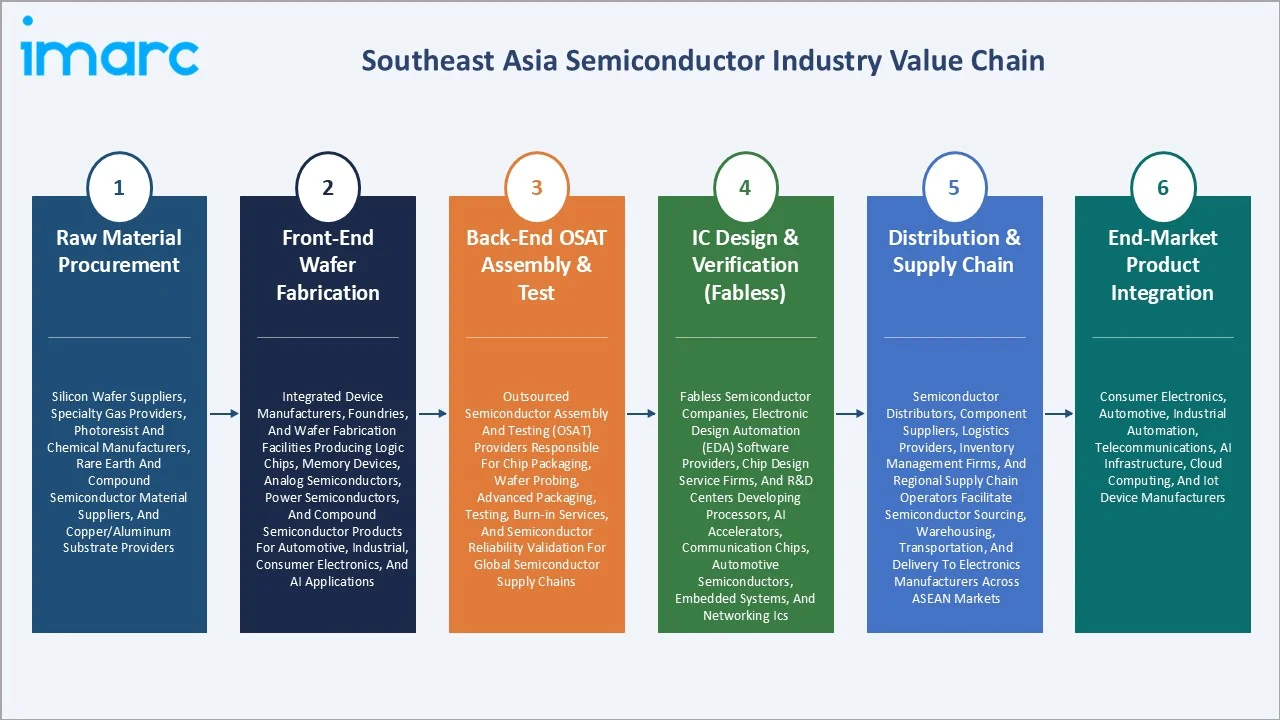

Industry Value Chain Analysis

Southeast Asia's semiconductor value chain integrates raw material procurement, front-end wafer fabrication, back-end OSAT assembly and test, IC design and verification, distribution and supply chain, and end-market product integration. Front-end wafer fabrication generates the highest per-unit revenue and captures 40-50% of chip manufacturing value, though SEA remains primarily a mature-node fab geography.

|

Stage |

Key Participants |

|

Raw Material Procurement |

Silicon wafer suppliers, specialty gas providers, photoresist and chemical manufacturers, rare earth and compound semiconductor material suppliers, and copper/aluminum substrate providers. |

|

Front-End Wafer Fabrication |

Integrated device manufacturers, foundries, and wafer fabrication facilities producing logic chips, memory devices, analog semiconductors, power semiconductors, and compound semiconductor products for automotive, industrial, consumer electronics, and AI applications. |

|

Back-End OSAT Assembly & Test |

Outsourced semiconductor assembly and testing (OSAT) providers responsible for chip packaging, wafer probing, advanced packaging, testing, burn-in services, and semiconductor reliability validation for global semiconductor supply chains. |

|

IC Design & Verification (Fabless) |

Fabless semiconductor companies, electronic design automation (EDA) software providers, chip design service firms, and R&D centers developing processors, AI accelerators, communication chips, automotive semiconductors, embedded systems, and networking ICs. |

|

Distribution & Supply Chain |

Semiconductor distributors, component suppliers, logistics providers, inventory management firms, and regional supply chain operators facilitate semiconductor sourcing, warehousing, transportation, and delivery to electronics manufacturers across ASEAN markets. |

|

End-Market Product Integration |

Consumer electronics, automotive, industrial automation, telecommunications, AI infrastructure, cloud computing, and IoT device manufacturers. |

The distribution and supply chain tier anchored in Singapore's free port status generates approximately USD 3-4 Billion in annual distribution revenue from Singapore's semiconductor trading activities. Singapore's semiconductor distribution industry benefits from a zero-tariff semiconductor import-export policy, sophisticated trade finance ecosystem, and Changi Airport logistics enabling just-in-time semiconductor delivery to Southeast Asia's manufacturing customers within 24-48 hours of order placement.

Technology Landscape in the Southeast Asia Semiconductor Industry

Silicon Carbide (SiC) Wafer Fabrication Technology

Silicon carbide (SiC) wafer fabrication technology is emerging rapidly in Southeast Asia as demand grows for high-efficiency power semiconductors used in electric vehicles, renewable energy systems, industrial automation, and AI infrastructure. In June 2025, Singapore’s Agency for Science, Technology and Research (A*STAR) launched the world’s first 200mm industrial-grade open R&D silicon carbide (SiC) production line through its Institute of Microelectronics (IME). The facility integrates the full SiC development process from material growth and defect analysis to device fabrication and testing to reduce technology costs, address industry skill gaps, and accelerate commercialization for applications such as electric vehicles, power grids, and data centers.

Advanced Packaging Technology

Advanced packaging technologies such as 2.5D, 3D IC, and Fan-Out Wafer Level Packaging (FOWLP) are emerging due to rising demand for AI chips, high-performance computing, and advanced mobile devices. Semiconductor companies across Malaysia, Singapore, and Vietnam are investing in next-generation packaging capabilities to improve chip performance, power efficiency, and miniaturization. These technologies are enabling higher chip density and faster data processing for applications in AI, automotive electronics, and cloud infrastructure.

Compound Semiconductor Process Technology

Compound semiconductor process technologies based on materials such as silicon carbide (SiC) and gallium nitride (GaN) are emerging rapidly due to growing demand for high-performance and energy-efficient semiconductor devices. These technologies are increasingly used in electric vehicles, renewable energy systems, 5G infrastructure, industrial automation, and AI data centers because of their superior thermal conductivity and high-voltage performance. Regional investments in advanced fabrication, R&D facilities, and power electronics manufacturing are strengthening Southeast Asia’s position in the global compound semiconductor ecosystem.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

🔒 |

🔒 |

2025 |

|

Material Used |

Silicon Carbide |

28.5% |

2025 |

|

End User |

Consumer Electronics |

26.8% |

2025 |

|

Country |

Singapore |

27.9% |

2025 |

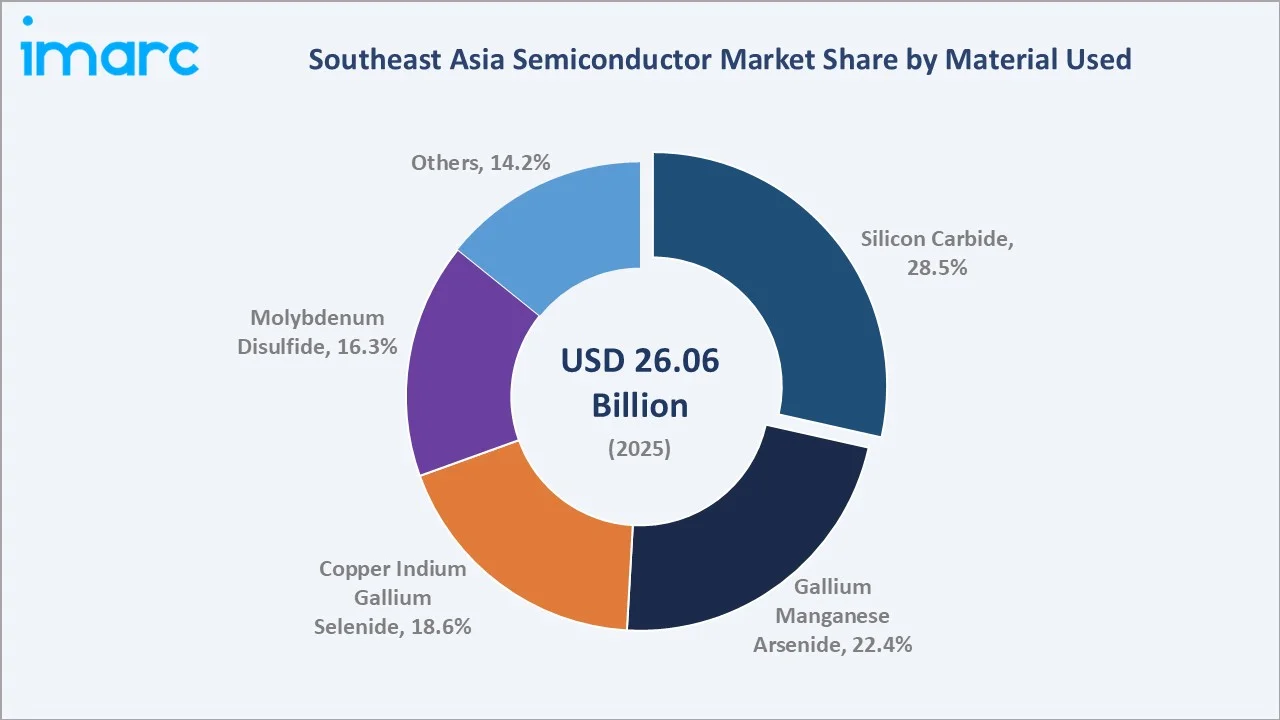

By Material Used

Silicon Carbide leads at 28.5% market share (2025). SiC's dominance reflects Malaysia's strategic positioning in the EV power semiconductor supply chain, making Malaysia the world's emerging SiC manufacturing capital. SiC semiconductor demand is projected to grow, driven purely by EV adoption, with SEA's manufacturing share among the world's most concentrated in any technology transition.

To access detailed market analysis, Request Sample

Gallium manganese arsenide at 22.4% encompasses the compound semiconductor materials underlying SEA's RF semiconductor industry, dominated by MMIC chip manufacturing for 5G smartphones in Malaysia. Copper indium gallium selenide at 18.6% covers thin-film photovoltaic semiconductor manufacturing in Malaysia and Thailand, serving the region's growing solar energy sector. Molybdenum disulfide at 16.3% grows fastest at ~11.4% CAGR through 2D material research commercialization and early production in Singapore and Malaysia. Others at 14.2% encompasses conventional silicon, germanium, and specialty III-V materials.

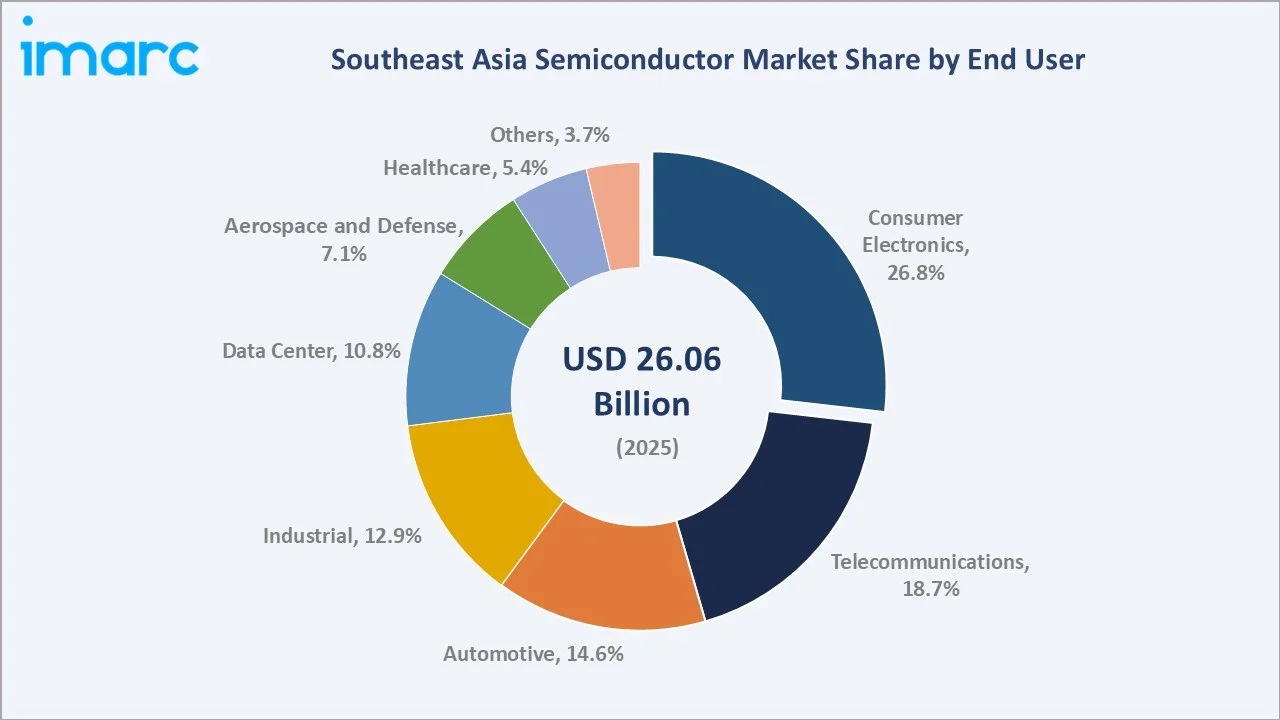

By End User

Consumer electronics lead at 26.8% market share (2025). SEA's back-end OSAT infrastructure is globally dominant for consumer electronics semiconductor supply, with every major consumer electronics OEM's semiconductor supply chain passing through Malaysia, the Philippines, or Thailand's OSAT facilities. Telecommunications at 18.7% reflects 5G network deployment, semiconductor demand and smartphone RF chip manufacturing in Malaysia. Automotive at 14.6% grows at ~12.6% CAGR driven by Thailand's automotive electronics manufacturing and Malaysia's EV power semiconductor production.

Industrial at 12.9% serves SEA's factory automation, motor drive, and power conversion markets, growing with Industry 4.0 adoption. Data center at 10.8% grows fastest at ~13.8% CAGR as SEA hyperscaler investment creates adjacent semiconductor manufacturing demand. Aerospace and defense at 7.1% is anchored by Singapore's defense-qualified mature-node fab. Healthcare at 5.4% and others at 3.7% round out the end-user landscape.

Regional Market Insights

|

Country |

Share (2025) |

Key Semiconductor Growth Drivers & Characteristics |

|

Singapore |

27.9% |

Supported by advanced wafer fabrication capabilities, strong R&D infrastructure, and a highly skilled engineering workforce. |

|

Malaysia |

19.6% |

Driven by its strong electronics manufacturing ecosystem, advanced packaging and testing capabilities, and increasing foreign direct investment. |

|

Thailand |

15.8% |

Benefiting from rising automotive electronics production, EV ecosystem development, industrial automation adoption, and expanding electronics manufacturing activities. |

|

Vietnam |

12.4% |

Expanding rapidly due to increasing electronics exports, rising foreign investments, growing semiconductor talent development initiatives, and strengthening manufacturing capabilities. |

|

Philippines |

9.6% |

Supported by its established semiconductor assembly and testing industry, skilled labor availability, and strong export-oriented electronics manufacturing sector. |

|

Indonesia |

8.7% |

Driven by rising consumer electronics demand, industrial digitalization, EV battery ecosystem development, and increasing investments in local electronics manufacturing infrastructure. |

|

Others |

6.0% |

Other Southeast Asian countries are gradually strengthening semiconductor ecosystems through electronics manufacturing expansion, industrial modernization, digital infrastructure investments, and growing participation in regional semiconductor supply chains. |

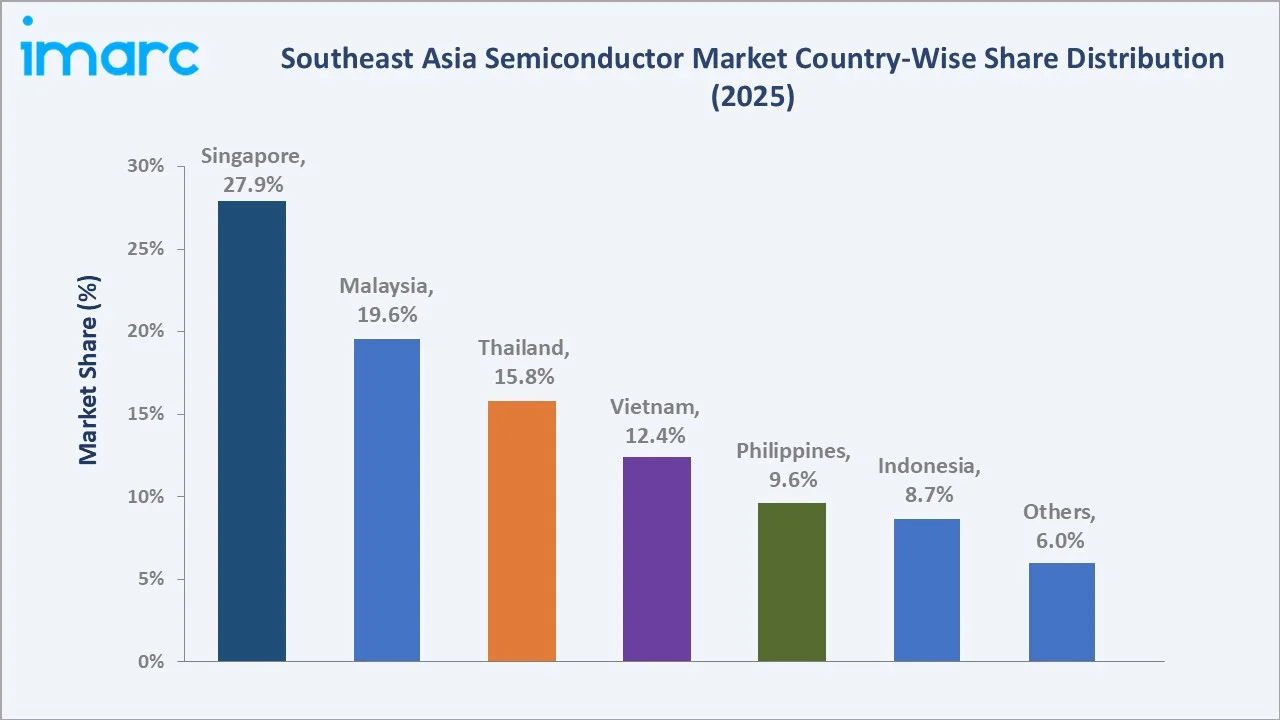

Singapore's 27.9% market leadership, despite a modest manufacturing employee base versus Malaysia, reflects the revenue concentration from wafer fabrication and IC design activities. The IC design intellectual property embedded in Singapore's design center outputs generates license revenue and design service income, creating Singapore's premium position in the SEA semiconductor value hierarchy.

Malaysia's 19.6% represents the manufacturing engine with the region's largest semiconductor workforce and the most significant near-term capacity expansion. Thailand's 15.8% anchors automotive semiconductor manufacturing. Vietnam's 12.4% is growing fastest as Intel's established presence and Samsung's supply chain requirements attract additional OSAT investment. The Philippines' 9.6% reflects historical back-end manufacturing strength, while Indonesia's 8.7% is growing from its Batam-based electronics manufacturing base.

Competitive Landscape

Southeast Asia's semiconductor competitive landscape is dominated by multinational semiconductor companies' SEA subsidiaries and manufacturing operations, with a secondary tier of locally-listed OSAT companies in Malaysia and Singapore that have developed world-class back-end packaging capabilities serving global semiconductor supply chains. The competitive dynamics are shaped by customer concentration and technology differentiation, with advanced packaging capability increasingly separating premium-margin operators from commodity packaging competitors.

|

Company Name |

Products |

Market Position |

Core Strength |

|

Infineon Technologies AG |

Battery management ICs, Evaluation Boards, Memories, Microcontroller, Power |

Market Leader |

Infineon is a world leader in semiconductor solutions |

|

STMicroelectronics |

Diodes and rectifiers, Imaging and photonics solutions, Interfaces and transceivers, Memories, MEMS and sensors, Microcontrollers & microprocessors |

Strong Challenger |

ST’s Singapore manufacturing sites are home to its largest front-end manufacturing and electrical wafer sort (EWS) facilities. |

|

NXP Semiconductors |

Arm Microcontrollers, Arm Processors, Battery Management, Interfaces, Power Drivers |

Established Player |

NXP advances technology through a global reach, and the company’s presence in Singapore focuses on design, supply, sales and technical support. |

|

Inari Amertron Berhad |

Wafer Processing |

Established Player |

As a leading Outsourced Semiconductor Assembly and Test (OSAT) player in the semiconductor industry, Inari is committed to bringing the best quality products and services to the customers. |

The competitive landscape is evolving as advanced packaging and SiC manufacturing create new competitive frontiers where SEA operators can differentiate beyond commodity services.

Key Company Profiles

Infineon Technologies AG

Infineon Technologies represents the most strategically critical foreign semiconductor investment in Southeast Asia for the EV transition.

- Product Portfolio: Battery management ICs, Evaluation Boards, Memories, Microcontroller, Power.

- Recent Development: In August 2025, Infineon Technologies AG completed its acquisition of Marvell Technology’s Automotive Ethernet business after first announcing the deal in April 2025 and securing all required regulatory approvals. Through this acquisition, Infineon aims to strengthen its capabilities in software-defined vehicle technologies and expand its leadership position in automotive microcontroller solutions.

- Strategic Focus: Focused on expanding power semiconductor, silicon carbide (SiC), automotive electronics, and energy-efficient chip manufacturing capabilities across Southeast Asia to support EVs, renewable energy, AI infrastructure, and industrial automation demand.

STMicroelectronics

ST’s Singapore manufacturing sites are home to the company’s largest front-end manufacturing and electrical wafer sort (EWS) facilities. They also house packaging R&D activities. The site in Ang Mo Kio, established in 1984, was the first front-end wafer fab in Singapore.

- Product Portfolio: Diodes and rectifiers, Imaging and photonics solutions, Interfaces and transceivers, Memories, MEMS and sensors, Microcontrollers & microprocessors.

- Recent Developments: In May 2025, STMicroelectronics, in collaboration with the A*STAR Institute of Microelectronics and ULVAC, announced the expansion of the “Lab-in-Fab” (LiF) in Singapore.

- Strategic Focus: Focuses on strengthening semiconductor manufacturing resilience, expanding chip production, and supporting industrial automation and smart device ecosystems across Southeast Asia.

Market Concentration Analysis

Southeast Asia's semiconductor market exhibits high concentration at the technology segment level, with wafer fabrication dominated by 4-5 companies, while OSAT is more fragmented with 50+ operators across Malaysia, Philippines, Thailand, and Vietnam. The multinational company dominance collectively commanding 30-35% of SEA semiconductor revenue reflects the capital-intensive nature of semiconductor manufacturing, where barriers to entry require billion-dollar fabrication investments. Locally-listed OSAT companies collectively hold 8-12% of SEA semiconductor revenue, a concentration that understates their strategic importance as the only publicly-traded pure-play SEA semiconductor companies providing institutional investors direct access to SEA semiconductor market exposure.

Investment & Growth Opportunities

Highest Growth Investment Areas

SiC wafer fabrication in Malaysia's Kedah cluster at ~10.8% CAGR for the SiC segment, advanced packaging including 2.5D and 3D IC in Penang and Singapore at ~25%+ CAGR for advanced packaging revenue, data center semiconductor at ~13.8% CAGR, Vietnam OSAT expansion at ~20%+ CAGR from small base, automotive semiconductor at ~12.6% CAGR, and compound semiconductor including GaN for 5G and GaAs for IoT at ~10%+ CAGR represent SEA's highest-return semiconductor investment vectors through 2034.

Emerging Investment Opportunities

Indonesia's semiconductor manufacturing entry represents the most significant greenfield investment opportunity in the Southeast Asia semiconductor industry through 2034. With the world's 4th-largest population, a national semiconductor strategy targeting SiC substrate manufacturing, US-Indonesia Comprehensive Strategic Partnership semiconductor cooperation, and Batam's existing electronics manufacturing infrastructure, Indonesia is positioned to capture 5-10% of new SEA semiconductor OSAT investment through 2034, growing its market share from 8.7% toward 12-15%.

Investment Themes

- Advanced packaging capability development for fabless semiconductor companies: The advanced packaging market projected for SEA by 2030 requires OSAT companies investing now in 2.5D interposer assembly, fan-out WLP, and heterogeneous integration capabilities. Fabless semiconductor companies are actively seeking non-TSMC advanced packaging partners in SEA, creating direct commercial demand for OSAT companies investing in CoWoS-equivalent process technology.

- Vietnam semiconductor talent and infrastructure development: Vietnam's semiconductor engineer development program and government investment incentives create a 5-10 year window to establish IC design and OSAT operations ahead of market competition.

Future Market Outlook (2026-2034)

The Southeast Asia semiconductor market is projected to grow from USD 26.06 Billion in 2025 to USD 56.64 Billion by 2034, delivering an 8.74% CAGR over the forecast period. The market's anchor value of USD 39.62 Billion in 2030 represents a semiconductor industry where the SiC mega-fab has transformed Malaysia into the world's SiC production capital, Intel Penang's advanced packaging transition has established SEA's first global center of excellence for chiplet-based heterogeneous integration, and Vietnam's semiconductor industry has crossed the USD 8-10 Billion annual revenue threshold establishing it as Asia's fourth major semiconductor manufacturing economy.

Three structural forces define Southeast Asia's semiconductor market growth through 2034 with high certainty: the EV power electronics revolution driving SiC semiconductor demand; the US-China geopolitical semiconductor supply chain restructuring directing new semiconductor capacity investment to ASEAN allies through friend-shoring policies that make ASEAN semiconductor investment simultaneously commercially attractive and geopolitically incentivized; and the advanced packaging technology transition enabling SEA's OSAT industry to capture dramatically higher per-package revenue from chiplet integration, 2.5D interposers, and 3D IC stacking that are the semiconductor industry's primary scaling technology for AI, HPC, and 5G applications through 2034.

Research Methodology

Primary Research

Primary research comprised structured interviews with 60+ industry stakeholders (2025), including VP Manufacturing and Operations from Intel Malaysia, Infineon Malaysia, STMicroelectronics Thailand, ON Semiconductor Malaysia, Texas Instruments Philippines, and NXP Semiconductors Singapore; OSAT company CEOs; EDB Singapore, MIDA Malaysia, BOI Thailand, and DOST Philippines semiconductor investment promotion officials; semiconductor equipment suppliers including ASML Singapore and Applied Materials Malaysia providing capacity investment intelligence; and semiconductor industry association executives from MSPA Malaysia Semiconductor Industry Association, SEIPI Philippines, and SEMI Southeast Asia.

Secondary Research

Secondary research encompassed Malaysia Investment Development Authority MIDA semiconductor investment statistics 2024; EDB Singapore semiconductor sector data 2024; BOI Thailand Electronics Industry statistics 2024; SEMI Southeast Asia market data quarterly reports; Gartner Semiconductor Revenue Forecast Q4 2025; OMDIA power semiconductor market report 2025; company annual reports; IDC semiconductor market tracker Asia Pacific Q4 2025; and US Commerce Department CHIPS Act guardrail regulation analysis. Over 80 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using bottom-up material type x end-user models calibrated against SEMI's North America and Japan semiconductor equipment billings data as a leading indicator of SEA fab investment, individual company revenue guidance for SEA operations, MIDA Malaysia-approved manufacturing licenses for semiconductor projects, and end-market demand models. Key inputs include S-curve adoption models for SiC in EV applications, CAGR extrapolation for compound semiconductor materials, regression analysis of SEA semiconductor market growth versus regional electronics export growth, and Wolfspeed and Infineon production ramp trajectory models for SiC supply projections.

Southeast Asia Semiconductor Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Components Covered | Memory Devices, Logic Devices, Analog IC, MPU, Discrete Power Devices, MCU, Sensors, Others |

| Materials Used Covered | Silicon Carbide, Gallium Manganese Arsenide, Copper Indium Gallium Selenide, Molybdenum Disulfide, Others |

| End Users Covered | Automotive, Industrial, Data Center, Telecommunication, Consumer Electronics, Aerospace and Defense, Healthcare, Others |

| Countries Covered | Indonesia, Thailand, Singapore, Philippines, Vietnam, Malaysia, Others |

| Companies Covered | Infineon Technologies AG, STMicroelectronics, NXP Semiconductors, Inari Amertron Berhad, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Southeast Asia semiconductor market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Southeast Asia semiconductor market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Southeast Asia semiconductor industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Southeast Asia Semiconductor Market Report

The Southeast Asia semiconductor market reached USD 26.06 Billion in 2025, driven by Malaysia's SiC wafer fabrication and OSAT leadership, Singapore's IC design and specialty fab functions, Intel Penang's advanced packaging transition, and the US-China friend-shoring supply chain reconfiguration directing USD 60+ Billion in semiconductor investment to ASEAN allies.

The market grows at 8.74% CAGR during 2026-2034, reaching USD 56.64 Billion by 2034, driven by EV SiC power semiconductor surge, SiC mega-fab volume production commencing 2027-2028, Intel Penang advanced packaging for external customers, Vietnam's semiconductor industry scaling, advanced packaging 2.5D/3D IC technology transition, and US-ASEAN semiconductor supply chain partnership institutionalization.

Silicon Carbide leads at 28.5% through Malaysia's Infineon Kulim SiC fab, Wolfspeed's under-construction Kulim mega-fab, and ON Semiconductor's Selangor SiC production.

Consumer electronics lead at 26.8% through Malaysia and the Philippines' back-end OSAT for iPhone, Samsung, and Dell supply chains.

Singapore leads at 27.9% through Micron's 300mm DRAM fab, GlobalFoundries Singapore mature-node foundry, Siltronic 300mm silicon wafer fab, and the highest concentration of IC design centers generating premium revenue per unit versus volume manufacturing.

Leading companies include Infineon Technologies AG, STMicroelectronics, NXP Semiconductors, and Inari Amertron Berhad, among others.

The market is projected to reach approximately USD 39.62 Billion by 2030, with SiC mega-fab commencing volume production, reshaping global SiC supply, Intel Penang advanced packaging opening for external IFS customers, Vietnam's semiconductor industry crossing USD 8-10 Billion revenue, and advanced packaging revenue crossing USD 5 Billion annually from Penang-Singapore-Thailand OSAT cluster.

Singapore serves as SEA's semiconductor intellectual capital hosting wafer fabrication including Micron 300mm DRAM and GlobalFoundries mature-node, IC design centers with 20+ multinational design houses, semiconductor distribution hub, and research institutions at A*STAR and NUS, generating 200+ MoS2 papers annually.

Three priority opportunities: SiC power semiconductor manufacturing in Malaysia's Kedah SiC cluster creating USD 2-3 Billion annual revenue ecosystem opportunity for substrate suppliers, specialty chemical vendors, and SiC-process OSAT operators; advanced packaging capability development for fabless customers requiring non-TSMC 2.5D/3D IC integration with USD 10B+ market by 2030; and Vietnam semiconductor design and OSAT infrastructure establishment capturing first-mover advantages before government talent pipeline reaches scale by 2028-2030.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)