Spoolable Pipes Market Size, Share, Trends and Forecast by Matrix Type, Reinforcement Type, Application, Sales Channel, and Region, 2026-2034

Spoolable Pipes Market Size and Share:

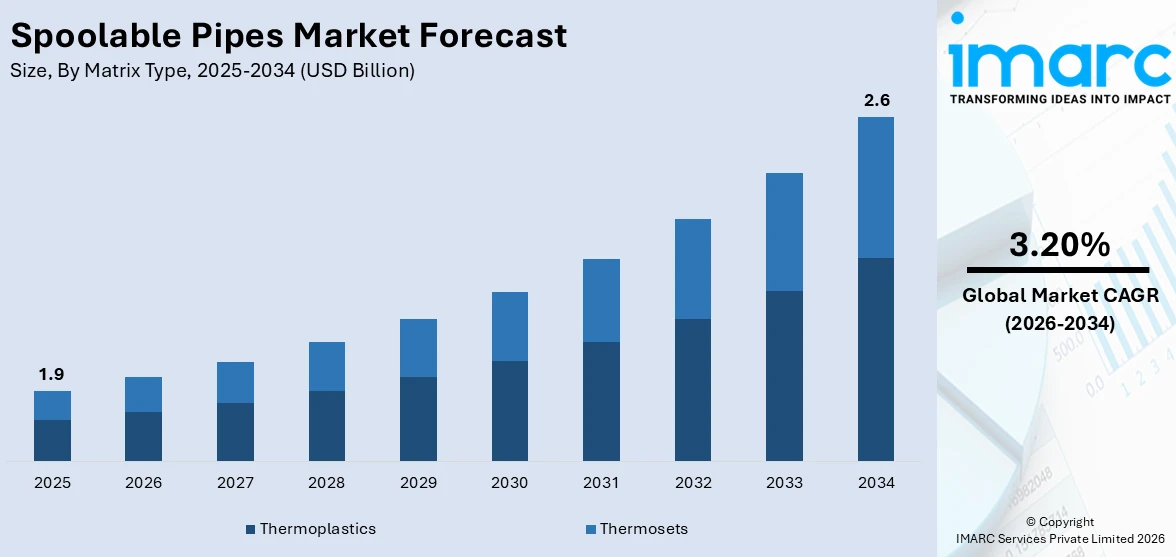

The global spoolable pipes market size was valued at USD 1.9 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 2.6 Billion by 2034, exhibiting a CAGR of 3.20% during 2026-2034. North America currently dominates the market, holding a significant market share of around 33.1% in 2025. The market is driven by rising demand from the oil and gas industry due to their flexibility, corrosion resistance, and cost-effectiveness in high-pressure applications. Increasing infrastructure development, especially in remote and harsh environments, supports adoption across water distribution, chemical transport, and mining sectors. Growing focus on reducing installation time, maintenance costs, and environmental impact are some of the key factors augmenting spoolable pipes market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 1.9 Billion |

|

Market Forecast in 2034

|

USD 2.6 Billion |

| Market Growth Rate 2026-2034 | 3.20% |

The market growth is fueled by the increasing need for economical and efficient fluid transportation, especially in remote and hostile environments. Expansion in the oil and gas industry is increasing the demand for spoolable pipes, as they are extensively favored due to their flexibility and simplicity of installation. According to industry reports, global oil supply grew by 240 kb/d in February 2025 to 103.3 mb/d in March 2025. This increase further underscores the need for effective pipeline solutions, particularly in remote or difficult environments. Moreover, advances in material technology have resulted in the creation of stronger and more corrosion-resistant pipes, making them perform better and last longer. The transition towards sustainable and environmentally friendly options in industrial uses also supports the use of spoolable pipes across different industries. In addition, the capability of spoolable pipes to resist tough conditions, such as extreme pressure and temperature, further enhances the spoolable pipes market outlook.

To get more information on this market Request Sample

In the United States, the demand for spoolable pipes is mainly driven by the growth of the country's energy network, including the expansion of renewable energy infrastructure. According to industry reports, the United States remains a major investor in oil and gas and accounts for 15% of global investments in renewable energy. With the U.S. moving towards cleaner sources of energy, spoolable pipes are being used more and more for the transportation of geothermal and biogas, in addition to conventional fossil fuels. Besides this, the potential of spoolable pipes to be quickly deployed in extreme locations like offshore installations and outlying areas contributes to market growth in America. In addition, the focus on minimizing downtime operations and enhancing security levels in the sector further catalyzes the uptake of spoolable pipes, thereby entrenching them in new-age infrastructure works.

Spoolable Pipes Market Trends:

Liquid Fuels Production Growth Driving Long-Distance Flowline Demand

The expansion of liquid fuels production, particularly from tight oil, oil sands, and enhanced oil recovery (EOR) operations, is increasing demand for flexible, durable pipeline infrastructure. According to an industry report, the production of liquid fuels is expected to rise by 1.3 Million b/d in 2025 and 1.2 Million b/d in 2026. In response, energy operators are increasingly turning to spoolable pipes due to their superior corrosion resistance, mechanical flexibility, and ease of installation across long distances and complex terrains. These pipes are adopted in both upstream and midstream environments to replace or supplement conventional steel pipelines, particularly in regions where logistical constraints or cost limitations hinder traditional infrastructure. Additionally, their ability to withstand cyclic loading and temperature fluctuations supports deployment in variable terrains and climates. This, in turn, is contributing to the spoolable pipes market growth. With international oil companies investing in modular production facilities and satellite well pads, the need for quickly deployable, jointless flowlines is intensifying, positioning spoolable pipes at the forefront of liquid transport innovations.

Shift Toward Hydrogen and CO2 Transport Applications

As energy transition efforts accelerate, spoolable pipes are increasingly evaluated and deployed for transporting hydrogen and carbon dioxide in midstream infrastructure. These gases present specific technical challenges, hydrogen’s small molecular size and high diffusivity raise permeation risks in conventional steel pipelines, especially under elevated pressures, while supercritical CO₂ used in carbon capture and storage (CCS) demands materials with high chemical resistance and resistance to crack propagation. As per industry reports, in the United States, approximately 68 Million Tons of CO₂ are transported annually through 50 pipelines covering about 5,000 miles as of 2023, positioning pipelines as the dominant mode of CO₂ transport. As CCS projects expand and new carbon hubs are established, the need for materials capable of accommodating corrosive or high-pressure gases is accelerating the transition to advanced spoolable pipe systems. Thermoplastic composite pipes (TCPs) and other reinforced spoolable solutions are gaining traction due to their impermeability, corrosion resistance, and fatigue endurance, making them suitable for long-distance CO₂ pipelines and hydrogen blending networks. Industry players are also investing in material compatibility studies and certification protocols to ensure compliance with evolving international hydrogen and CO₂ transport standards. These spoolable pipes market trends are likely to redefine future pipeline specifications as demand shifts from hydrocarbons to alternative energy vectors.

Increasing Utilization in Mining for Slurry and Dewatering Applications

Spoolable pipes are gaining prominence in the mining sector due to their performance advantages in abrasive and corrosive fluid handling. They are increasingly deployed for transporting mineral slurries, managing tailings, and executing pit dewatering activities. These operations require piping systems that can endure high solids content, pressure variations, and chemical exposure, conditions where traditional steel pipes often fail or incur high maintenance costs. Spoolable pipes made from reinforced thermoplastics or composites offer a corrosion-resistant, flexible, and low-maintenance alternative. As per industry reports, as of FY24 (provisional), there were an estimated 2,036 reported mines in India, with 795 of those being for metallic minerals and 1,241 for non-metallic minerals. The scale and diversity of mining activities across such operations generate continuous demand for adaptable, easily deployable piping systems. As mechanization and water management practices intensify in both private and public sector mines, spoolable pipes are increasingly viewed as a cost-effective infrastructure investments that reduce operational disruptions and enhance fluid transport efficiency.

Spoolable Pipes Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global spoolable pipes market, along with forecasts at the global, regional, and country levels from 2026-2034. The market has been categorized based on matrix type, reinforcement type, application, and sales channel.

Analysis by Matrix Type:

- Thermoplastics

- Thermosets

Thermoplastics leads the market with around 92.6% of market share in 2025. Thermoplastics are known for their special blend of flexibility, chemical resistance, and toughness. As a matrix material, thermoplastics offer the strength required for spoolable composite pipes for oil and gas, water supply, and other industrial uses. Thermoplastics are different from thermosets as they can be melted and reformed, which makes them simpler to process and repair. Their resistance to corrosive conditions, high pressure, and temperature variation makes them suitable for carrying a vast variety of fluids. Moreover, thermoplastics help in achieving the lightness of spoolable pipes, making it simpler to transport them and easier to install them at a faster rate in comparison to steel pipes. As the demand for cost-effective and efficient pipeline solutions increases, thermoplastics become more prominent in enriching the performance, durability, and sustainability of spoolable piping systems.

Analysis by Reinforcement Type:

- Glass Fiber-Reinforced Spoolable Pipe

- Carbon Fiber-Reinforced Spoolable Pipe

- Steel-Reinforced Spoolable Pipe

- Others

Glass fiber-reinforced spoolable pipes lead the market with around 61.4% of market share in 2025 due to their affordability, flexibility, and corrosion resistance. These pipes are extensively applied in low to medium pressure environments, particularly in the oil and gas sector for water injection, gas gathering, and flowlines. Glass fiber's non-metallic character causes these pipes to be corrosion-resistant to external and internal attack, keeping costs of maintenance lower and increasing working life. Furthermore, their lighter construction enables greater ease of transport and installation, leading to the overall cost of installation being less than that of conventional steel pipes. These qualities have ensured that glass fiber-reinforced pipes are an operator's choice for tough and cost-effective solutions in demanding environments that are not extremely challenging regarding pressure or mechanical stress.

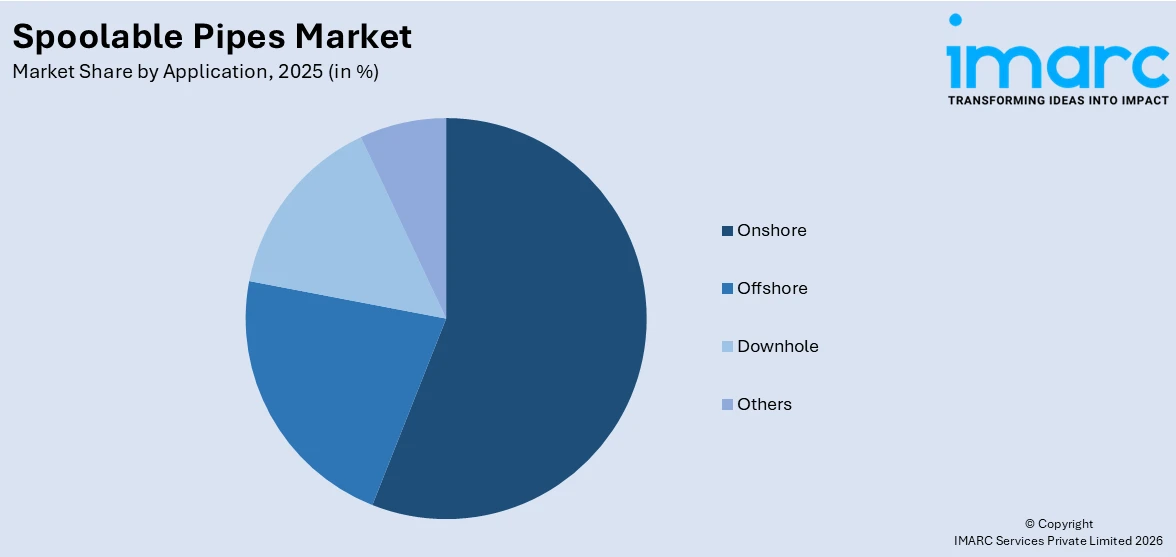

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Onshore

- Offshore

- Downhole

- Others

Onshore leads the market with around 56.0% of market share in 2025. Onshore plays a vital role, especially within the oil and gas sector. Spoolable pipes are used extensively for transporting crude oil, natural gas, and other liquids from production points to processing plants. Their ease of installation, corrosion resistance, and flexibility make them ideal for onshore conditions, where terrain variation and operational efficiency are critical. They have several benefits over steel pipes, including lower weight, lower transportation and installation costs, and greater durability. They are resistant to corrosion, fatigue, and environmental stresses, which lowers the maintenance costs and enhances operating safety. With the increasing demand for energy, the onshore segment continues to be a driving factor for spoolable pipes market growth, since they offer a cost-efficient and durable option for pipeline transportation requirements.

Analysis by Sales Channel:

- Direct Sales

- Distributors

Direct sales lead the market with around 83.6% of market share in 2025. It allows manufacturers to establish closer relationships with end-users and offer tailored solutions. Through this channel, companies can gain valuable insights into customer requirements, project specifications, and performance feedback, which can inform product development and support services. Direct sales are especially prominent in large-scale industrial projects such as oil and gas operations, mining, and municipal infrastructure, where technical precision and after-sales support are critical. This channel also enables manufacturers to control pricing, delivery schedules, and quality assurance more effectively. As a result, direct sales are often preferred for high-value, customized projects where close coordination between supplier and buyer is essential for the success of the deployment and long-term system performance.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2025, North America accounted for the largest market share of over 33.1%, driven largely by its robust oil and gas sector and infrastructure growth. The region's growing need for pipeline solutions is due to the immense exploration and production processes, especially in the shale gas fields. The demand for spoolable pipes in North America is due to their capacity to address the demands of fluid transportation under different pressure conditions. Thus, spoolable pipes find significant applications in the oil and gas, water distribution, and chemical industries. The United States is a significant region in the regional market, due to vast pipeline networks and ongoing investment in energy infrastructure. Canada also fuels market expansion with increasing demand for spoolable pipes across diverse industrial applications. The region's emphasis on low-cost, high-durability, and easy-to-install options guarantees that spoolable pipes will continue to be a preferred option in North America's pipeline projects.

Key Regional Takeaways:

United States Spoolable Pipes Market Analysis

In 2025, the United States holds a substantial share of around 81.30% of the market share in North America. The region is witnessing increased demand for spoolable pipes driven by growing investment in infrastructure development across multiple sectors. For instance, in a series of bills passed by Congress, over USD 1.2 Trillion will be spent between 2021 and 2030 to modernize aging U.S. infrastructure. Expansion in construction, urban development, and pipeline rehabilitation is pushing the need for lightweight, corrosion-resistant, and flexible pipe systems. As infrastructure ages, replacement and upgrades using modern materials like spoolable pipes are becoming standard practice, reducing installation time and costs. Public and private investments in infrastructure modernization are amplifying the requirement for efficient piping systems. Spoolable pipes offer benefits such as durability, high pressure handling, and easy deployment, making them well-suited for water systems, gas distribution, and industrial applications. Increasing focus on sustainable materials and reduced environmental footprint also supports spoolable pipe demand, aligning with green infrastructure goals and long-term resilience in United States infrastructure projects.

Asia-Pacific Spoolable Pipes Market Analysis

Asia-Pacific is seeing strong growth in spoolable pipes adoption due to expanding water distribution and water treatment initiatives across urban and rural areas. According to Ministry of Commerce and Industry, India, 565 investment projects in the water treatment plants subsector in India are worth USD 60.43 Billion. Rapid population growth and industrialization are driving governments and utilities to enhance water infrastructure efficiency and coverage. Spoolable pipes provide an ideal solution for water-related networks due to their flexibility, corrosion resistance, and quick installation, especially in regions with difficult terrain. The push for modernizing outdated water distribution systems and improving wastewater treatment facilities is accelerating deployment. Environmental concerns and stricter water regulations are compelling stakeholders to adopt advanced piping systems to minimize leakages and contamination risks. Spoolable pipes are increasingly favored in both municipal and industrial water management projects, contributing to safer, cleaner, and more efficient water distribution and treatment in Asia-Pacific.

Europe Spoolable Pipes Market Analysis

Europe is experiencing heightened adoption of spoolable pipes supported by growing transportation of refined and crude petroleum fuels through safer and more efficient pipeline systems. According to reports, in 2022, the European Union's reliance on imports for all of its petroleum products and crude oil rose to a new all-time high of 97.7%. Aging infrastructure and the need for corrosion-resistant materials in hydrocarbon transportation have driven the transition to composite and flexible pipe technologies. Spoolable pipes are well-suited for oil and fuel transfer due to their high chemical resistance, reduced maintenance needs, and ability to withstand harsh operating conditions. Regulatory emphasis on pipeline safety and operational reliability is further promoting these solutions. As transportation networks for refined and crude petroleum fuels expand and diversify, spoolable pipes offer faster installation and adaptability in various terrain and pressure scenarios. Their usage is becoming central to pipeline refurbishment, capacity expansion, and new petroleum logistics projects across Europe’s energy corridors.

Latin America Spoolable Pipes Market Analysis

Latin America is witnessing rising demand for spoolable pipes in response to growing mining activities across the region. According to industry reports, mining has contributed between 13% and 19% of foreign direct investment into Latin America in the past. As mining operations expand, there is increasing requirement for durable, corrosion-resistant piping solutions to handle abrasive materials and fluids. Spoolable pipes provide the strength, flexibility, and rapid deployment necessary for remote and challenging mining environments. Their lightweight nature also reduces logistics costs, which makes them ideal for use in large-scale mineral extraction and transport systems in Latin America.

Middle East and Africa Spoolable Pipes Market Analysis

Middle East and Africa are adopting spoolable pipes at a greater pace due to growing oil and gas projects requiring efficient and cost-effective pipeline solutions. According to industry reports, during the period 2024-2028, a total of 668 oil and gas projects are expected to commence operations in the Middle East. In addition to this, the region’s focus on expanding upstream and midstream infrastructure is driving the need for high-performance pipes that reduce installation time and maintenance costs. Moreover, spoolable pipes, with their corrosion resistance and flexibility, are increasingly preferred in harsh desert and offshore conditions prevalent in Middle East and Africa, which is also a significant growth-inducing factor for the market.

Competitive Landscape:

The market is characterized by dynamic and intense competition driven by increasing demand across oil and gas, water management, and industrial sectors. Moreover, continual improvements in composite materials, durability of products, and cost-effectiveness mainly define market competition. Market leaders distinguish themselves based on advancements in pipe design, pressure resistance, and corrosion resistance. According to the spoolable pipes market forecast, the sector is anticipated to witness steady expansion, driven by increasing need for lightweight, flexible, and corrosion-resistant piping solutions. Compliance with regulations and environmental sustainability are increasingly becoming essential drivers of market positioning. The industry experiences robust engagement by incumbent manufacturers and niche players alike, launching niche solutions. Regional demand is not uniform, as growth in North America, the Middle East, and Asia-Pacific is prominent, driven by infrastructure spending and oil exploration. Also, strategic partnerships, technological integration, and expansion into untapped markets are common competitive tactics.

The report provides a comprehensive analysis of the competitive landscape in the spoolable pipes market with detailed profiles of all major companies, including:

- Baker Hughes Company

- FlexSteel Pipeline Technologies Inc.

- Future Pipe Industries

- Hebei Heng An Tai Pipeline Co. Ltd

- Magma Global Ltd. (TechnipFMC plc)

- NOV Inc.

- Pipelife International Gmbh (Wienerberger AG)

- Shawcor Ltd.

- Smartpipe Technologies

- Strohm B.V.

Latest News and Developments:

- April 2025: Axiom Investors LLC DE increased its holdings in Cactus, Inc. by 30,851 shares during the fourth quarter, bringing its total ownership to 149,317 shares valued at USD 8.71 Million. The investment move reflected rising institutional interest in Cactus, which operates in pressure control and spoolable pipes technologies. Despite the share acquisition, Cactus stock fell 6.5% to USD 37.97, following mixed earnings results and a lowered price target from Barclays.

- April 2025: Bryce Point Capital LLC invested USD 443,000 in Cactus, Inc. by acquiring 7,586 shares during the fourth quarter. Cactus, known for its pressure control solutions and spoolable pipes, attracted additional institutional interest, including Vanguard and JPMorgan. The company last reported quarterly revenue of USD 272.12 Million and maintained a strong market presence in spoolable technologies across the U.S. and international markets.

- November 2024: Nutrien, a Canadian fertilizer producer, upgraded the brine transfer line at its Rocanville potash facility in Saskatchewan by replacing welded steel with a steel-reinforced, high-density polyethylene (HDPE) composite pipe. For the project, FlexSteel provided 3,937 feet (1,200 meters) of 10-inch MXL spoolable steel-reinforced composite piping. As per API Specification 15S, the new design can handle pressures of up to 1,500 psi, meeting high-pressure requirements. The overall longevity and effectiveness of the facility are intended to be enhanced by this improvement.

Spoolable Pipes Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Matrix Types Covered | Thermoplastics, Thermosets |

| Reinforcement Types Covered | Glass Fiber-Reinforced Spoolable Pipe, Carbon Fiber-Reinforced Spoolable Pipe, Steel-Reinforced Spoolable Pipe, Others |

| Applications Covered | Onshore, Offshore, Downhole, Others |

| Sales Channels Covered | Direct Sales, Distributors |

| Region Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Baker Hughes Company, FlexSteel Pipeline Technologies Inc., Future Pipe Industries, Hebei Heng An Tai Pipeline Co. Ltd, Magma Global Ltd. (TechnipFMC plc), NOV Inc., Pipelife International Gmbh (Wienerberger AG), Shawcor Ltd., Smartpipe Technologies and Strohm B.V. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the spoolable pipes market from 2020-2034.

- The spoolable pipes market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the spoolable pipes industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The spoolable pipes market was valued at USD 1.9 Billion in 2025.

The spoolable pipes market is projected to exhibit a CAGR of 3.20% during 2026-2034, reaching a value of USD 2.6 Billion by 2034.

The market is driven by the growing demand for cost-effective and corrosion-resistant piping solutions in oil and gas and chemical sectors, increased shale gas exploration, expanding offshore operations, quicker installation timelines, rising replacement of steel pipelines, and supportive government investments in energy infrastructure and pipeline rehabilitation.

North America currently dominates the market with a market share of 33.1%. The dominance is fueled by the region’s booming shale gas industry, extensive pipeline network upgrades, rising adoption of composite pipes for onshore and offshore applications, strong presence of key manufacturers, and favorable regulatory frameworks supporting advanced piping materials.

Some of the major players in the spoolable pipes market include Baker Hughes Company, FlexSteel Pipeline Technologies Inc., Future Pipe Industries, Hebei Heng An Tai Pipeline Co. Ltd, Magma Global Ltd. (TechnipFMC plc), NOV Inc., Pipelife International Gmbh (Wienerberger AG), Shawcor Ltd., and Smartpipe Technologies and Strohm B.V., among others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)