Stainless Steel Market Size, Share, Trends and Forecast by Product, Grade, Application, and Region, 2026-2034

Stainless Steel Market Size and Share:

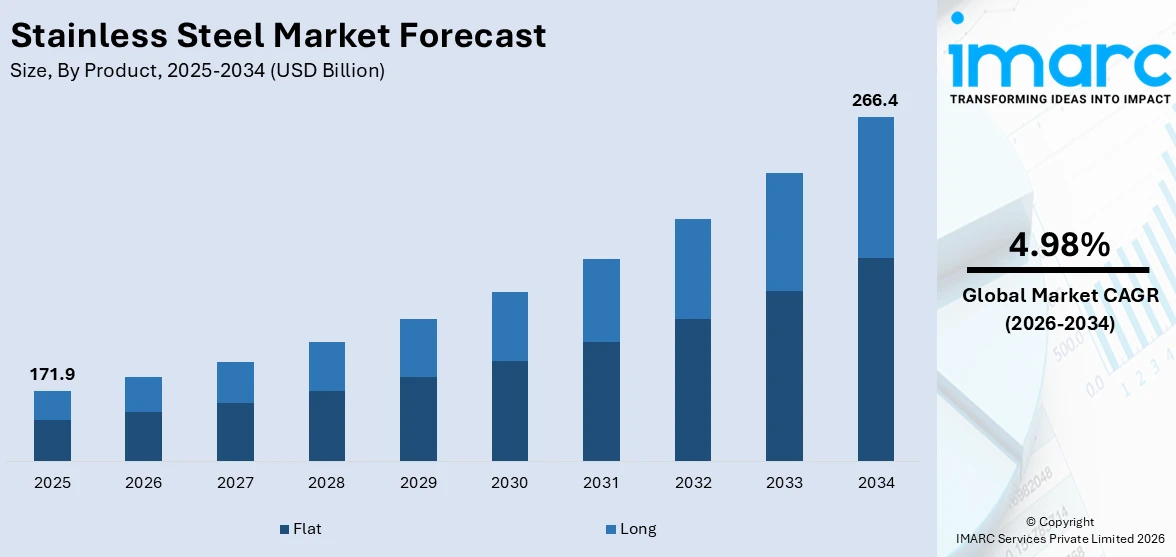

The global stainless steel market size was valued at USD 171.9 Billion in 2025. The market is expected to reach USD 266.4 Billion by 2034, exhibiting a CAGR of 4.98% during 2026-2034. Asia Pacific currently dominates the market, holding a significant market share in 2025. The market is propelled by sectors like automotive, construction, and manufacturing, which depend on strength, durability, and corrosion resistance, given heightened demand. Moreover, accelerated urbanization coupled with infrastructure expansion schemes throughout developing economies has stimulated the need for stainless steel within transportation as well as building materials usage. Furthermore, the heightened emphasis on conservation and technological improvements additionally strengthens manufacturing operations, thereby augmenting stainless steel market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 171.9 Billion |

| Market Forecast in 2034 | USD 266.4 Billion |

| Market Growth Rate 2026-2034 | 4.98% |

The market is witnessing massive growth due to its augmented use in various sectors like aerospace, energy, and consumer goods. Additionally, the growth in renewable energy projects like wind and solar power has also augmented the demand for stainless steel components employed in such technologies. Significantly, in 2024, international investment in clean energy totaled USD 2 Trillion, reflecting an almost 70 percent growth over the last ten years. Furthermore, the continued trend of automation and digitalization of the manufacturing process has also triggered innovation in stainless steel production, enhancing its characteristics and making it more diverse for use in high-tech applications. Furthermore, the increase in international trade agreements has increased the demand for stainless steel worldwide, making more opportunities available in the global market.

To get more information on this market Request Sample

In the United States, the market is especially affected by the robust demand from the automotive sector. The corrosion and lightweight nature of stainless steel make it suitable for vehicle body components, leading to extensive usage. Industry reports indicates that U.S. new-car sales experienced an increase in 2024, fueled by restocked inventories, improved manufacturer incentives, and increasing demand for hybrid cars, boosting overall sales to near 16 million units. In addition, the emphasis of the U.S. government on sustainability and strict environmental regulations has sped up the utilization of stainless steel in green and energy-efficient technologies, which is one of the emerging stainless steel market trends. Infrastructure growth, such as roads, bridges, and urban development projects, is also a prime driver, demanding large amounts of stainless steel for building and repair. The robust manufacturing sector, coupled with ongoing technological innovations in the production processes, contributes significantly to the market's expansion in the region.

Stainless Steel Market Trends:

Growing Demand From Construction And Infrastructure Projects

Increasing demand from construction and infrastructure projects is creating the need for durable, corrosion-resistant, and low-maintenance materials. Stainless steel is widely used in bridges, buildings, roofing, cladding, and structural components due to its strength and long service life. As urbanization and government-led infrastructure development are accelerating, the requirement for high-quality materials that can withstand harsh environmental conditions is rising. Stainless steel’s aesthetic appeal, recyclability, and ease of fabrication make it ideal for modern construction needs. Projects such as airports, metro systems, highways, and smart cities incorporate stainless steel in various applications to ensure safety, longevity, and sustainability. Its ability to support both functional and design elements enhances its value in large-scale developments, driving consistent demand and making it a key material in the thriving building construction and infrastructure sector. As per an industry report, the global buildings construction market is set to attain USD 10.5 Trillion by 2033, exhibiting a growth rate (CAGR) of 4.9% during 2025-2033.

Increasing Vehicle Production

Rising vehicle production is positively influencing the stainless steel market growth. According to reports, total production of passenger vehicles, commercial vehicles, three-wheelers, two-wheelers, and quadricycles from April to June 2025 amounted to 7,660,225 units. Stainless steel is widely used in exhaust systems, fuel tanks, structural frames, and trim parts due to its corrosion resistance, resilience, and capacity to endure elevated temperatures. As more vehicles are manufactured to meet increasing domestic and global transportation needs, the adoption of stainless steel is rising proportionally. Automakers also focus on improving vehicle efficiency, safety, and sustainability, and stainless steel plays a key role in achieving these goals. Its recyclability and compatibility with electric vehicle (EV) designs further enhance its relevance. With the expansion of passenger and commercial vehicle production, the automotive industry continues to be a major driver of stainless-steel demand, supporting the overall growth of the market.

Rising Use In The Oil And Gas Industry

Stainless steel is essential in the construction of pipelines, storage tanks, valves, offshore platforms, and drilling equipment due to its strength, corrosion resistance, and long service life. As exploration and production activities are expanding in both onshore and offshore fields, especially in deep-water and harsh environments, the requirement for durable and reliable materials is growing. Stainless steel’s ability to maintain structural integrity under harsh operating conditions makes it ideal for critical oil and gas infrastructure. Additionally, the desire for higher operational efficiency and safety is further increase adoption, which further enhances stainless steel market outlook. With ongoing oil and gas demand and new field developments, the oil and gas sector continue to significantly contribute to the broadening of the stainless steel market. According to reports, the global oil usage was expected to rise by 720 kb/d in 2025.

Stainless Steel Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global stainless-steel market, along with forecasts at the global, regional, and country levels from 2026-2034. The market has been categorized based on product, grade, and application.

Analysis by Product:

- Flat

- Long

Flat leads the market in 2025 due to its applicability across various industries. Its smooth, uniform surface and excellent corrosion resistance make it perfect for applications in construction, automobile panels, kitchen appliance parts, and equipment in industries. The adaptability of the product enables it to be rolled into sheets, coils, and plates of different thicknesses to suit varied engineering and designing needs. Flat stainless steel is also at the forefront of infrastructure growth, especially in city construction projects, due to its strength combined with beauty. Its higher durability and lower maintenance requirements increase the life of end products and hence make it the choice for manufacturers looking to achieve long-lasting performance. Besides, the capacity to manufacture flat stainless steel in specialized forms, like high-strength or heat-resistant types, further underscores its strategic value in technological and industrial developments.

Analysis by Grade:

- 200 Series

- 300 Series

- 400 Series

- Duplex Series

- Others

300 series leads the market in 2025. This grade boasts an excellent balance of corrosion resistance, strength, and flexibility. Renowned for its austenitic structure, this grade offers excellent formability and weldability, making it suitable for a wide range of industrial and commercial applications. It is widely used in kitchen equipment, chemical processing, architectural structures, and medical instruments, where durability and hygiene are critical. The 300 series is particularly valued for its resistance to oxidation and acidic environments, ensuring long-term performance with minimal maintenance. Its versatility on both flat and long products further adds to its market value, as producers can utilize it on sheets, coils, bars, and tubes. Its consistency in harsh conditions, added to its visual appeal, further solidifies its value as a benchmark product in stainless steel production, improving innovation and addressing the changing needs of contemporary industries.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

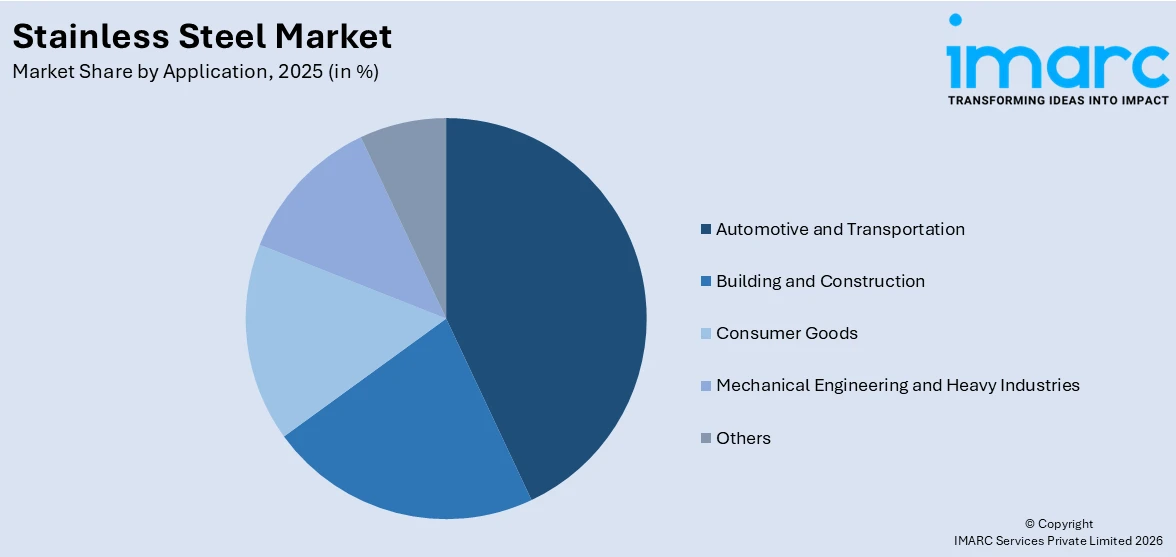

- Automotive and Transportation

- Building and Construction

- Consumer Goods

- Mechanical Engineering and Heavy Industries

- Others

Stainless steel is a critical component in the automotive and transportation industry due to its durability, corrosion resistance, and strength. It is extensively applied in exhaust systems, chassis, fuel tanks, and decorative trims of various components to improve both performance and lifespan. Its capacity to deal with high temperatures and withstand chemicals makes it perfect for use in cars and transportation infrastructure. Moreover, stainless steel helps in optimizing weight and compliance with safety regulations, while facilitating environmentally friendly usage through recyclability. Its multi-functional nature allows manufacturers to achieve demanding design and regulatory requirements, making it a critical material in the current automotive and transportation sectors.

In the construction and building industry, stainless steel is appreciated for its longevity, looks, and corrosion resistance. It is widely used in structural frameworks, roofing, cladding, facades, and architectural fittings, providing functionality and good looks. The strength of the material provides leeway for creative design solutions with safety and longevity. Its resistance to severe environmental conditions and low maintenance needs extends the life of structures, especially in urban and coastal regions. Stainless steel also aids in sustainable construction since it is highly recyclable, a factor that makes it a widely accepted choice for new construction work requiring both performance and environmental awareness.

Stainless steel is central to the consumer goods market due to its cleanliness, longevity, and flexibility of design applications. Stainless steel can be found across kitchen equipment, cookware, cutlery, and personal care appliances, where anti-corrosion and cleanability are essential. The material's clean appearance, along with its strength, makes it possible to create fashion-oriented yet durable products that consumers demand. Stainless steel also facilitates product design innovation, allowing manufacturers to create functional and ergonomic products. Its recyclability is also consistent with increasing consumer demand for sustainable products, making it crucial in the market as a trusted and eco-friendly material for daily use.

Regional Analysis:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2025, Asia Pacific accounted for the largest market share. The market is driven by industrialization, urbanization, and infrastructure growth. The region's strong manufacturing foundation, especially in construction, automotive, and consumer durables industries, drives steady demand for stainless steel across various applications. Its strategic significance is further supported by access to raw materials and skilled manpower, facilitating cost-effective production and competitive prices. Asia Pacific is also a main center of technological innovation in stainless steel processing, as producers emphasize high-quality, niche grades to suit changing industry demands. The region's rising urban population and increased industrial production drive the market significantly and make it an essential driver of global consumption and supply. Therefore, the Asia Pacific is both a key demand hub and a strategic production hub, driving trends and affecting the competitive landscapes of the market globally

Key Regional Takeaways:

United States Stainless Steel Market Analysis

United States is witnessing rising stainless-steel adoption driven by growing investment in the automotive sector. For instance, GM plans to invest USD 4 Billion in its U.S. manufacturing plants. Increased vehicle production, coupled with stringent fuel efficiency standards, has prompted manufacturers to opt for durable and lightweight materials, accelerating stainless steel demand. Ongoing technological innovations in automotive components are further supporting this shift. Investment in electric and hybrid vehicles is also reinforcing material choices, with stainless steel offering corrosion resistance and strength. Additionally, the expanding infrastructure to support mobility has created new opportunities in chassis, exhaust, and structural parts. As automotive sector investment deepens, stainless steel usage across supply chains continues to expand.

Asia Pacific Stainless Steel Market Analysis

Asia-Pacific continues to record strong stainless-steel adoption supported by growing construction activities like smart cities. For instance, as of May 2025, a total of 7,555 smart city projects, accounting for 94% of the total 8,067 projects, have been completed in India. Urban transformation projects and infrastructure development have increased demand for corrosion-resistant and aesthetically appealing materials. Stainless steel is widely used in architectural elements, roofing, facades, water supply systems, and public transit systems due to its long service life and low maintenance needs. Rapid industrialization and modernization have encouraged governments and private developers to invest in sustainable building solutions. Smart city initiatives across the region are pushing for intelligent, energy-efficient structures where stainless-steel applications are integral.

Europe Stainless Steel Market Analysis

Europe is experiencing increased stainless-steel adoption due to growing adoption of renewable energy. According to the International Energy Agency, the European Union (EU) has increased its commitment to clean energy, with investment reaching almost USD 390 Billion in 2025. As countries shift towards wind, solar, and hydropower sources, the demand for durable and corrosion-resistant materials is rising. Stainless steel plays a key role in wind turbine components, solar panel mounts, energy storage units, and heat exchangers used in geothermal and biomass systems. With energy efficiency and sustainability becoming central to energy policies, stainless steel’s recyclability and low environmental impact enhance its appeal. Renewable energy projects in coastal and offshore environments further require materials that withstand harsh conditions, making stainless steel an optimal choice.

Latin America Stainless Steel Market Analysis

Latin America is observing increasing vehicle ownership due to growing urbanization and growing disposable income. For instance, as of 2025, the average annual salary in Brazil is approximately BRL 40,200, equivalent to around USD 7,025.63 per year. Expanding urban populations and improved living standards are stimulating demand for personal mobility solutions which in turn favors the market. Rising middle-class consumption and infrastructure development are also contributing to higher automotive sales further contributing to the steel demand.

Middle East and Africa Stainless Steel Market Analysis

Middle East and Africa are seeing higher stainless-steel adoption due to growing oil and gas industries and projects. According to an industry report, the Middle East is poised to invest approximately USD 130 billion in oil and gas supply in 2025, representing around 15% of the global total. Ongoing upstream and downstream activities, pipeline installations, and refinery expansions require corrosion-resistant and durable materials. Stainless steel’s mechanical strength and heat tolerance make it suitable for demanding oil and gas environments across the region which in turn has been a significant driving factor.

Competitive Landscape:

The competitive environment is marked by stiff competition, with producers striving to innovate products, contain costs, and penetrate emerging markets in a bid to capture market share. In addition, dominant players are investing more in sophisticated production technologies to optimize efficiency, increase quality, and minimize environmental footprint, in response to tougher sustainability regulations. Furthermore, strategic initiatives like joint ventures, capacity expansions, and mergers are common to enhance supply chains and increase geographic presence. Product differentiation, especially in corrosion-resistant and high-grade stainless steel, is an essential competitive advantage. According to the stainless steel market forecast, the market is expected to grow at a steady rate, driven by increasing demand across the industrial, construction, and automotive sectors. Besides this, firms are also focusing on sustainability and recycling efforts to address changing customer demands and differentiated regulatory standards. The rising trend of digitalization and intelligent manufacturing is also driving competitive strategies, which help firms to streamline processes and react quickly to changing market conditions.

The report provides a comprehensive analysis of the competitive landscape in the stainless steel market with detailed profiles of all major companies, including:

- Acerinox S.A.

- Aperam S.A.

- ArcelorMittal S.A.

- Baosteel Group

- JFE Steel Corporation (JFE Holdings Inc.)

- Jindal Stainless Limited

- Nippon Steel Corporation

- Outokumpu Oyj

- POSCO Products

- thyssenkrupp Stainless GmbH (ThyssenKrupp AG)

- Yieh United Steel Corp.

Latest News and Developments:

- June 2025: Cleveland-Cliffs Inc. commissioned its USD 150 Million Vertical Stainless Bright Anneal Line at Coshocton Works, revolutionizing stainless steel production for automotive and appliance sectors using a 100% hydrogen atmosphere that replaced acid-based methods and enhanced sustainability.

- May 2025: Venus Pipes & Tubes announced that it obtained a Letter of Intent from a prominent integrated power plant equipment manufacturer in India to supply stainless steel seamless boiler tubes valued at INR 190 Crore. These seamless boiler tubes made of stainless steel were utilized in various supercritical and subcritical thermal power projects.

- May 2025: Jindal Stainless was in talks with the Maharashtra state government to secure a land lot for its planned INR 40,000-crore stainless steel production plant. The facility would possess an overall melting capacity of 4 Million Tons annually and would be built in stages.

- April 2025: Bansal Wire Industries, a prominent local manufacturer of stainless steel, launched its expanded stainless steel wire production facility in Dadri, Uttar Pradesh. Following this expansion, the plant’s production capacity for stainless steel wire grew from 2.2 lakh metric Tons per annum (MTPA) to 3.6 Lakh MTPA. This positioned it as the largest site for stainless steel wire production in the nation at one location. The firm invested around INR 550 Crore to facilitate this increase in capacity.

- March 2025: Jindal Stainless Ltd (JSL), a leading stainless-steel producer, declared that it would invest INR 700 Crore in decarbonization initiatives as part of its strategy to achieve net-zero emissions by 2050. The funding would cover the upcoming five years and aim at numerous environmentally friendly initiatives, such as waste management and the employment of carbon capture technologies. Jindal Stainless maintained a significant presence in local and global markets, promoting advancements and innovations in stainless steel uses while aiding in India’s industrial development.

Stainless Steel Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Flat, Long |

| Grades Covered | 200 Series, 300 Series, 400 Series, Duplex Series, Others |

| Applications Covered | Automotive and Transportation, Building and Construction, Consumer Goods, Mechanical Engineering and Heavy Industries, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Acerinox S.A., Aperam S.A., ArcelorMittal S.A., Baosteel Group, JFE Steel Corporation (JFE Holdings Inc.), Jindal Stainless Limited, Nippon Steel Corporation, Outokumpu Oyj, POSCO Products, thyssenkrupp Stainless GmbH (ThyssenKrupp AG), Yieh United Steel Corp., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the stainless steel market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global stainless steel market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the stainless steel industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Stainless Steel Market Report

Stainless steel market was valued at USD 171.9 Billion in 2025.

Stainless steel market is projected to exhibit a CAGR of 4.98% during 2026-2034, reaching a value of USD 266.4 Billion by 2034.

The market is driven by increased industrialization, growing construction and automotive sectors, rising demand for durable and corrosion-resistant materials, and technological advancements in manufacturing processes. Additionally, the shift toward sustainable solutions, such as recycling and energy-efficient production, is further fueling market growth.

Asia Pacific currently dominates the stainless steel market in 2025, driven by the rapid industrialization, urbanization, and high demand from the automotive, construction, and manufacturing industries. Countries like China and India contribute significantly to market growth, with expanding infrastructure, a strong manufacturing base, and increasing investment in infrastructure projects.

Some of the major players in the stainless steel market include Acerinox S.A., Aperam S.A., ArcelorMittal S.A., Baosteel Group, JFE Steel Corporation (JFE Holdings Inc.), Jindal Stainless Limited, Nippon Steel Corporation, Outokumpu Oyj, POSCO Products, thyssenkrupp Stainless GmbH (ThyssenKrupp AG), Yieh United Steel Corp., among others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)