Stout Market Size, Share, Trends and Forecast by Distribution Channel and Region, 2026-2034

Stout Market Size, Share, Trends & Forecast (2026-2034)

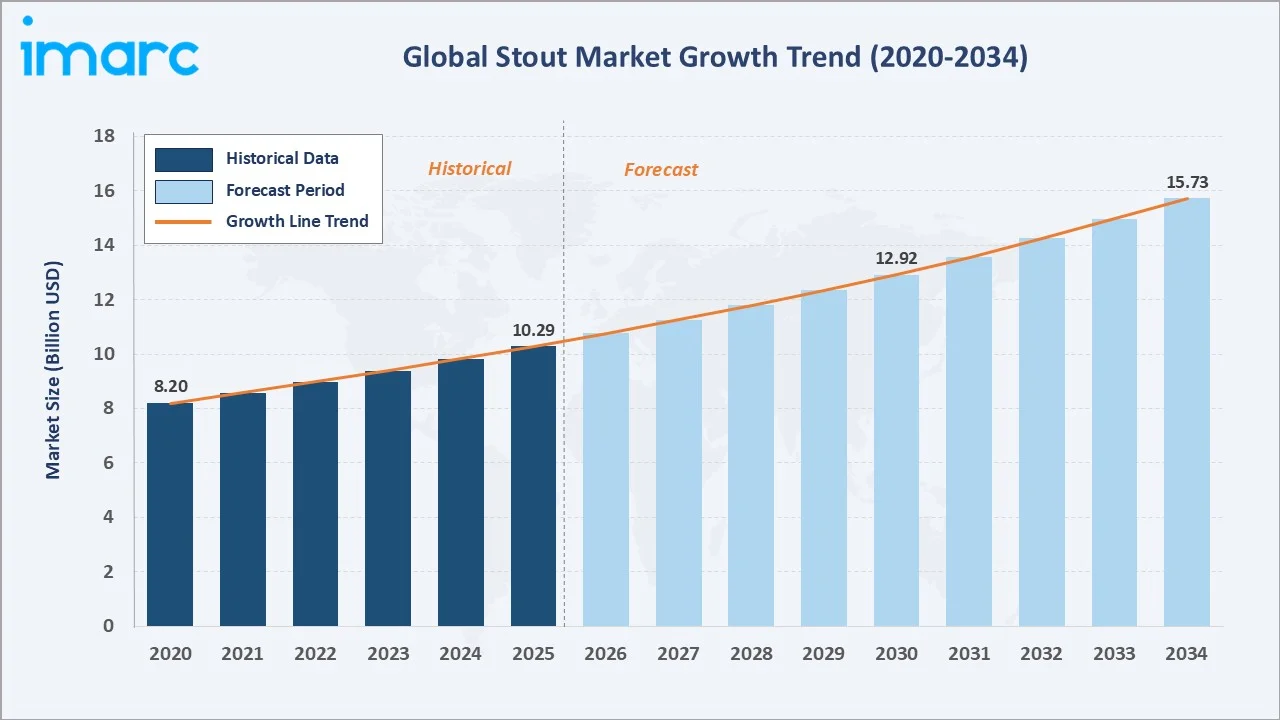

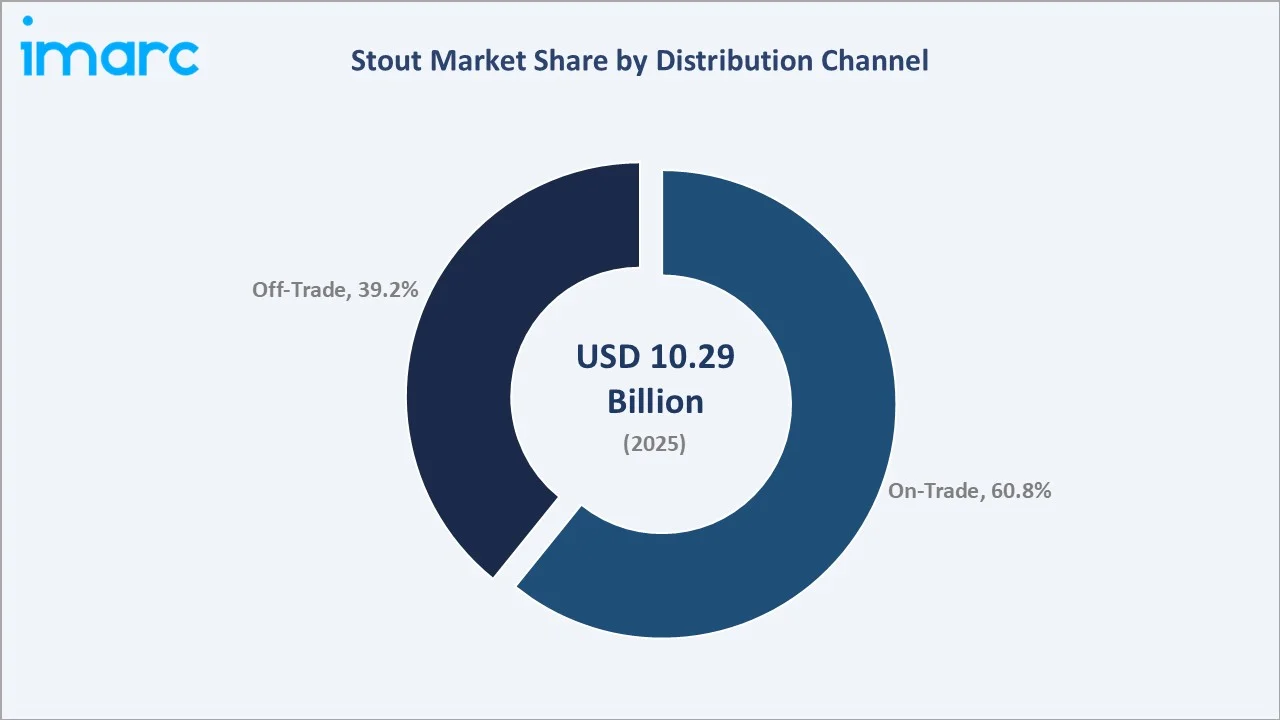

The global stout market reached USD 10.29 Billion in 2025 and is projected to reach USD 15.73 Billion by 2034, growing at a CAGR of 4.65% during 2026-2034. A robust on-trade culture, premiumization of beer portfolios, and the global craft stout movement are the primary growth engines.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 10.29 Billion |

|

Forecast Market Size (2034) |

USD 15.73 Billion |

|

CAGR (2026-2034) |

4.65% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

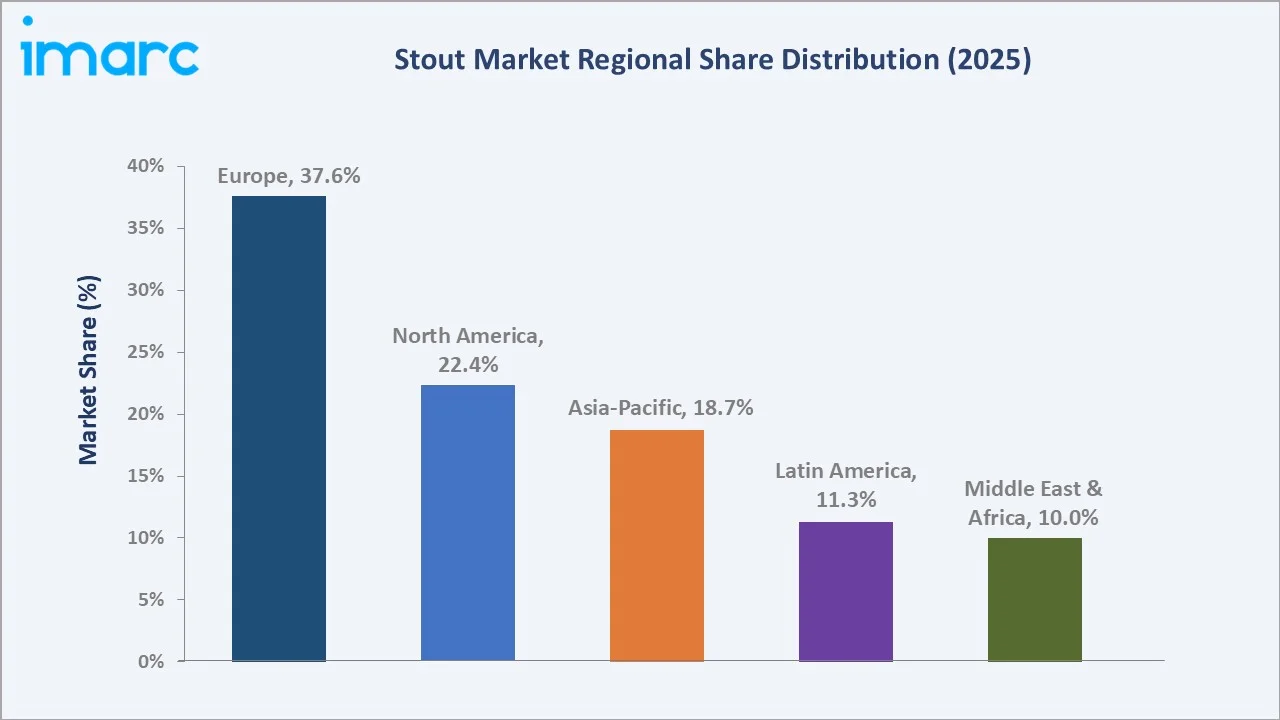

Largest Region |

Europe (37.6% share, 2025) |

|

Fastest Growing Region |

North America |

Europe dominates, holding a 37.6% market share in 2025, while On-Trade distribution leads channel demand at 60.8%. Guinness, produced by Diageo, remains the world's best-selling stout with annual sales exceeding 1.8 billion pints. Stout offers a distinctive sensory profile - characterized by roasted malt, creamy head retention, and nitrogen-infused texture - that differentiates it from lighter beer styles and sustains a loyal global consumer base.

To get more information on this market, Request Sample

With applications spanning pub culture, casual dining, and premium off-trade retail, the stout market is set to expand steadily, supported by innovation in nitro-pouring technology, low-alcohol variants, and category diversification into flavored stout sub-segments.

Executive Summary

The global stout market is on a sustained growth trajectory, driven by deepening on-trade consumption, rising craft beer culture, and expanding premium import markets across Asia-Pacific and North America. The market reached USD 10.29 Billion in 2025 and is forecast to exceed USD 15.73 Billion by 2034, at a CAGR of 4.65%.

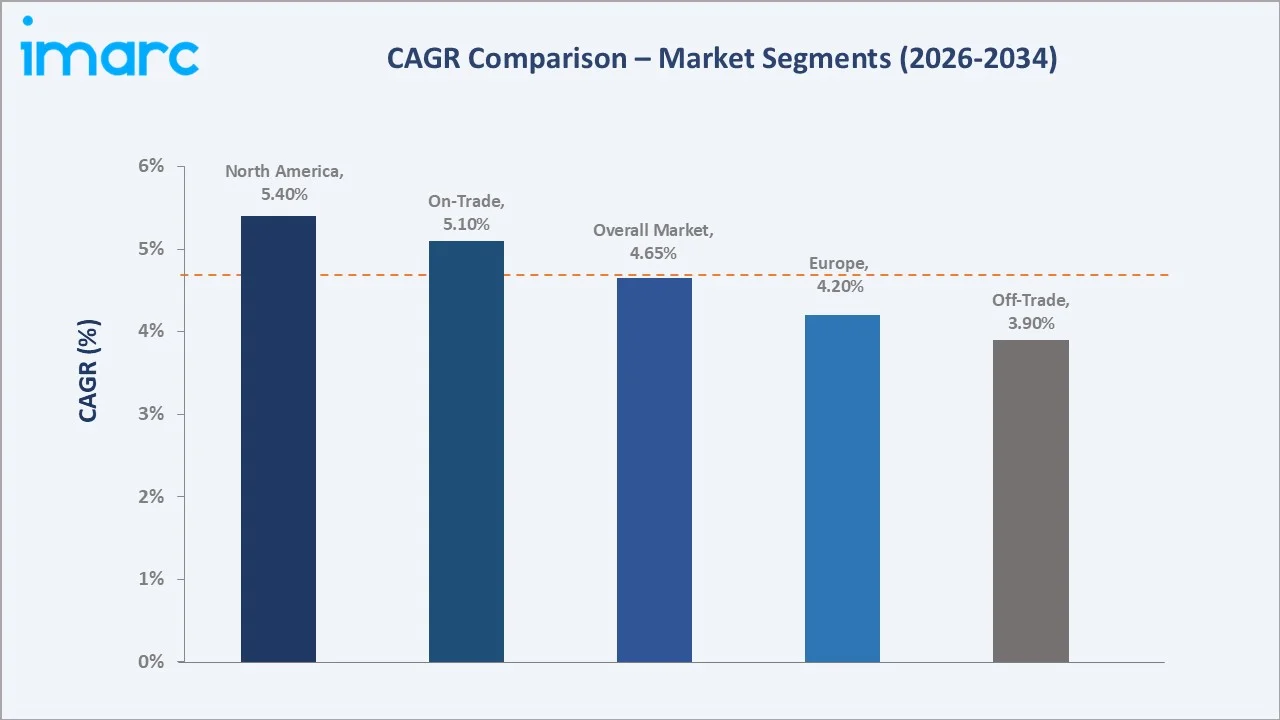

Europe leads globally with a 37.6% share in 2025, anchored by Irish and British stout traditions. Guinness alone serves approximately 100 million glasses daily. North America, at 22.4%, is the most dynamic growth market, craft stout producers and nitro-beer innovations are rapidly expanding the category beyond its traditional Irish-immigrant consumer base.

On-Trade channels dominate at 60.8% as stout's draft and nitrogen-poured formats remain most impactful in live venues. HEINEKEN's Murphy's and Beamish brands maintain a strong Irish regional presence, while Boston Beer Company and Left Hand Brewing lead craft stout innovation in the United States. Premiumization and category innovation - including flavored stouts, pastry stouts, and low-ABV variants - are catalyzing volume growth beyond core demographics.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Channel) |

On-Trade – 60.8% share (2025) |

|

Largest Region |

Europe – 37.6% share (2025) |

|

Fastest Growing Region |

North America (premiumization + craft surge) |

|

Top Companies |

Diageo, HEINEKEN N.V., Carlsberg Breweries A/S, The Boston Beer Company, and Left Hand Brewing Company |

|

Market Opportunity |

The premium and craft stout segment is projected to reach USD 3.5 billion by 2034 |

Key Analytical Observations Supporting the Above Data:

- On-Trade accounts for 60.8% of the stout market in 2025, reflecting the inherently social consumption occasion of draft stout in pubs, bars, and restaurants globally.

- Europe holds 37.6% of the global market in 2025, led by Ireland, the United Kingdom, Germany, and France, all supported by strong beer tourism and pub licensing infrastructure.

- North America is the fastest-growing regional market, driven by the craft beer revolution, with over 9,861 craft breweries operated in the U.S. in 2024, including 2,034 microbreweries and 3,948 taproom breweries, with stout among the top-five most-produced craft styles.

- Premium import stout volumes in Asia-Pacific grew 12.3% year-on-year in 2024, with South Korea and Japan as primary destinations for Guinness and craft stout imports.

- The low-alcohol and no-alcohol stout sub-segment is gaining traction with Guinness 0.0 becoming one of the fastest-growing no/low beer products in the UK market in 2023.

Global Stout Market Overview

Stout is a dark, top-fermented ale characterized by the use of roasted barley or malted barley, giving it a distinctive deep color, creamy texture, and complex flavor profile with notes of coffee, chocolate, and caramel. Originally developed in the British Isles in the 18th century, stout has grown from a regional specialty into a globally consumed beer style with a dedicated following.

The stout ecosystem spans raw material sourcing, particularly specialist malts and hops, through large-scale brewing operations, global distribution networks, and ultimately on-trade and off-trade retail. Macroeconomic trends, including rising disposable incomes, expanding middle-class populations in Asia and Africa, and a global appreciation for authentic, heritage beer styles, are primary growth catalysts.

Market Dynamics

To evaluate market opportunities, Request Sample

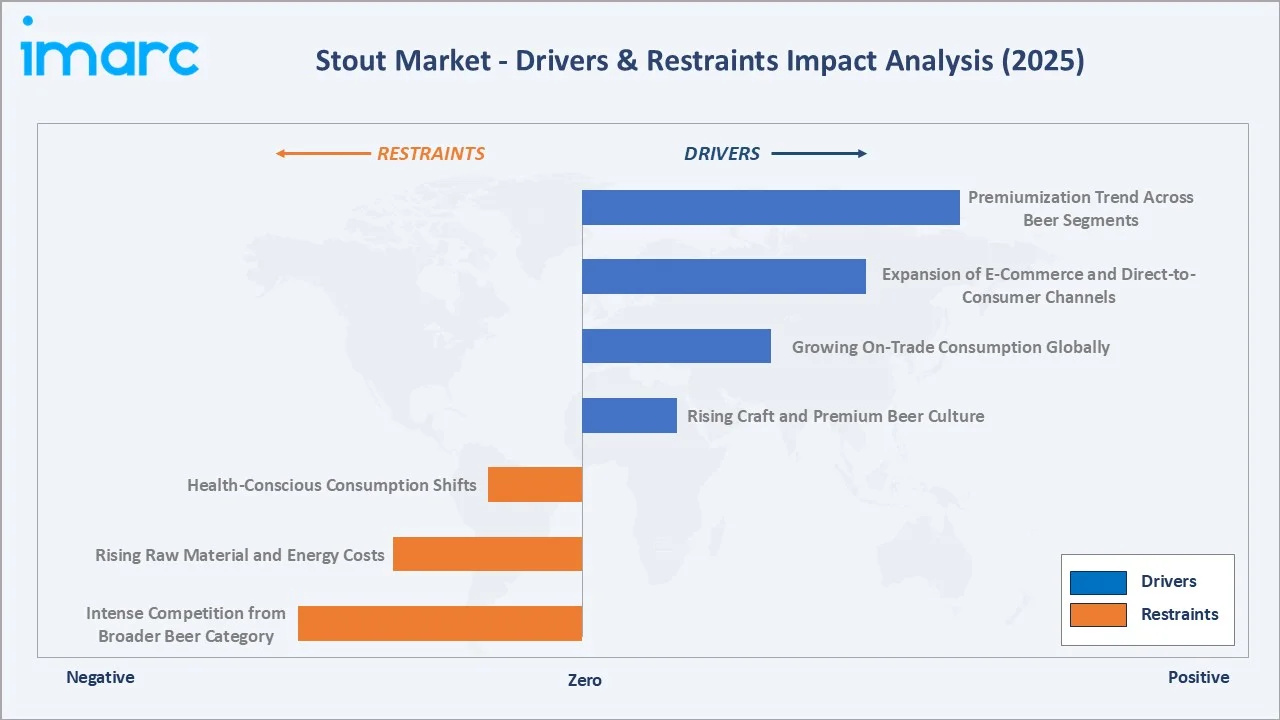

Market Drivers

- Rising Craft and Premium Beer Culture: The global craft beer market reached USD 155.1 billion in 2025, with stout consistently ranking among the top-five craft styles. Independent breweries are reimagining stout through barrel-aged variants, pastry stouts, and tropical fruit-infused editions, attracting younger demographics previously disengaged from the category.

- Growing On-Trade Consumption Globally: For instance, the Indian pub, bar, café, and lounge (PBCL) market size was valued at USD 2.8 billion in 2024. Stout benefits disproportionately from on-trade recovery as its nitrogen-poured draft format and ritualistic two-part serve make on-trade venues the optimal consumption occasion.

- Expansion of E-Commerce and Direct-to-Consumer Beer Channels: Growth in the online alcohol market in the UK is expected to decline by 3.2% as more consumers shift back to pubs, bars, and restaurants. Platforms such as Beer52, Craft Beer & Co., and direct brewery webshops are expanding stout's geographic reach into markets previously inaccessible.

- Premiumization Trend Across Beer Segments: Consumer willingness to pay a 30-50% price premium for craft or heritage beer brands accelerated in 2023-2024, with stout positioned as a premium, complex product. Guinness's Foreign Extra Stout retails at approximately 35% above standard lager price points in Southeast Asian markets.

Market Restraints

- Health-Conscious Consumption Shifts: A report by the Food Institute highlighted that health and wellness have become primary drivers for reducing alcohol consumption among adults, with motivations including improving health (47%), managing weight (38%), lowering disease risk (25%), and avoiding hangovers (23%).

- Rising Raw Material and Energy Costs: Roasted barley and specialty malt prices rose 18% between 2022 and 2024, driven by European supply disruptions and energy cost inflation in malting operations. Brewery energy costs increased 32% during 2021-2023, placing margin pressure on smaller craft producers.

- Intense Competition from Broader Beer Category: Stout competes within a crowded beer market against lager (which holds over 90% of global volume), IPA, sour ales, and hybrid styles. Category fragmentation limits consumer purchase frequency for any single style, constraining Stout's volume ceiling in non-core markets.

Market Opportunities

- Low-Alcohol and No-Alcohol Stout Innovation: 53% of all Guinness deliveries across the UK now comprise Guinness 0.0, the zero-alcohol variant introduced in 2021. Investment in dealcoholizing technology and yeast strain innovation is opening a new addressable market of health-conscious beer drinkers.

- Asia-Pacific Market Expansion: Global beer consumption reached around 194.1 billion liters, reflecting a modest year-on-year growth of 0.5%, according to Kirin Holdings Company, Limited. The increase was largely supported by strong growth in India (+14.6%), Russia (+9.0%), and Thailand (+5.8%).

- Flavor Innovation and Sub-Category Diversification: The pastry stout sub-segment, characterized by adjunct additions of vanilla, lactose, chocolate, and fruit, grew 45% in the North American craft sector in 2023-2024.

Market Challenges

- Regulatory Complexity Across Jurisdictions: Alcohol labelling, advertising restrictions, and import duties vary significantly across the 150+ countries where stout is distributed. The EU's new mandatory ingredient labelling requirements, effective 2025, add compliance costs estimated at EUR 1,200–5,000 per SKU for craft exporters.

- Nitrogen Dispense Infrastructure Dependency: Authentic stout presentation requires nitrogen mixed gas systems (typically 70% N2 / 30% CO2), which are not universally available in emerging market on-trade venues. This limits stout's penetration in bar and restaurant settings outside established beer markets.

Emerging Market Trends

1. Craft Stout Resurgence and Innovation

The craft brewing movement catalyzed a stout renaissance from 2020 onward. U.S. craft stout production volumes grew 22% between 2020 and 2024, outpacing the broader craft beer category growth of 17%. Barrel-aged imperial stouts now command retail prices of USD 15-40 per 330ml bottle, establishing stout as a premium collector's item.

2. Premiumization and Heritage Brand Investment

Diageo opened a £73 million Guinness Open Gate Brewery in London’s Covent Garden in December 2025, signaling premium category commitment. Heritage narratives, production provenance, historical brewing methods, and cultural storytelling are central to stout marketing strategies, resonating with consumers seeking authenticity behind their beer choices.

3. On-Trade Recovery and Experience-Driven Consumption

Post-pandemic on-trade recovery has been particularly strong for stout, a style intrinsically associated with pub and social settings. The UK's pub market generated GBP 24.1 billion in sales in 2024, with dark ales and stout gaining share as consumers trade up from standard lager during out-of-home occasions.

4. Export Market Development

Guinness export volumes grew significantly in 2023, with Africa (particularly Nigeria and Cameroon) and Asia-Pacific contributing disproportionately to growth. Nigeria is now the second-largest Guinness market globally after the UK, with local production catering to West African demand while premium imports target bar and restaurant channels in Southeast Asia.

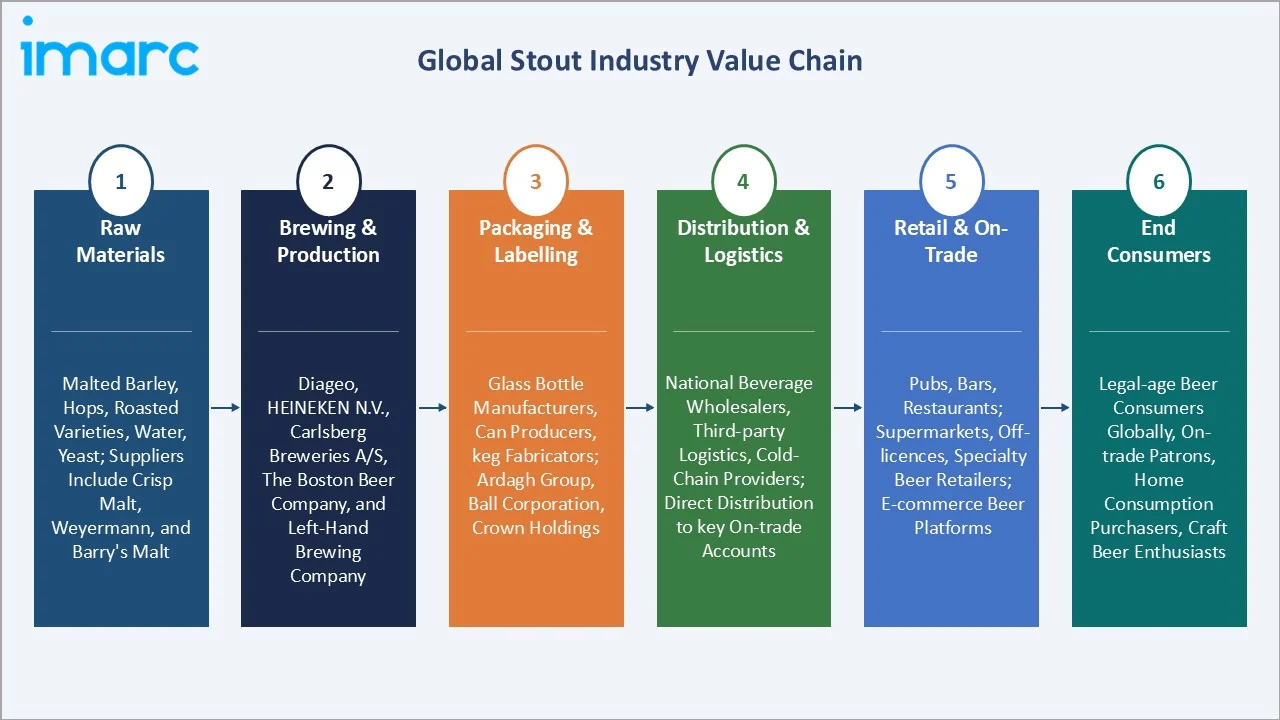

Industry Value Chain Analysis

The stout value chain spans specialist raw material sourcing through globally coordinated brewing and distribution, with each stage characterized by strong vertical integration among leading players and significant regional variation in the off-trade and on-trade delivery infrastructure.

|

Stage |

Key Players / Examples |

|

Raw Materials |

Malted barley, hops (particularly roasted varieties), water, yeast; Suppliers include Crisp Malt, Weyermann, and Barry's Malt |

|

Brewing & Production |

Diageo, HEINEKEN N.V., Carlsberg Breweries A/S, The Boston Beer Company, and Left Hand Brewing Company |

|

Packaging & Labelling |

Glass bottle manufacturers, can producers, keg fabricators, Ardagh Group, Ball Corporation, Crown Holdings. |

|

Distribution & Logistics |

National beverage wholesalers, third-party logistics, cold-chain providers; Direct distribution to key on-trade accounts |

|

Retail & On-Trade |

Pubs, bars, restaurants; Supermarkets, off-licences, specialty beer retailers; E-commerce beer platforms |

|

End Consumers |

Legal-age beer consumers globally, on-trade patrons, home consumption purchasers, craft beer enthusiasts |

Technology Landscape in the Stout Industry

Nitrogen Infusion and Dispensing Innovation

Widget technology, plastic nitrogen-releasing devices inside cans, was pioneered by Guinness in 1989 and remains a key differentiator for stout in the off-trade segment. Next-generation nitro technology, including Guinness Nitrosurge (launched 2021), uses ultrasonic technology to create a draught-like pour from a standard can, addressing the draft quality gap in home consumption settings.

Low-Alcohol and Dealcoholisation Technology

Cold dealcoholizing processes and advanced yeast strains capable of producing minimal alcohol during fermentation are enabling the production of flavor-authentic low-ABV stouts. Vacuum distillation and spinning cone column technology preserve volatile aroma compounds, maintaining stout's characteristic roasty, chocolatey profile at 0.0-0.5% ABV.

Sustainable Brewing Practices

In May 2024, Diageo announced a planned investment of over €100 million to decarbonize the historic Guinness brewery at St. James’s Gate in Dublin, aiming to achieve net-zero carbon emissions by 2030. The initiative will eliminate fossil fuels in brewing, cut emissions by over 90%, and improve water efficiency by 30%, positioning the site among the world’s most sustainable breweries.

Digital and Data-Driven Brewing

Predictive quality analytics and IoT-enabled fermentation monitoring systems are being deployed across large-scale stout breweries to ensure batch-to-batch consistency. AB InBev's PureDraught technology uses cloud-connected tap systems to monitor keg consumption, temperature, and pour quality in real-time, improving on-trade stout quality and reducing waste by up to 15%.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Distribution Channel |

On-trade |

60.8% |

2025 |

|

Region |

Europe |

37.6% |

2025 |

By Distribution Channel

On-Trade dominates the distribution channel segment with a 60.8% share in 2025 (approximately USD 6.26 billion). This dominance reflects stout's intrinsic association with the pub experience, its nitrogen-poured draft format, ritualistic two-part serve, and temperature requirements, making on-trade venues the optimal consumption occasion.

To access detailed market analysis, Request Sample

Off-Trade holds a 39.2% share, growing as nitro-widget can technology, Guinness Nitrosurge, and take-home multi-packs bring closer-to-draft quality to home settings. Supermarket and off-licence channels account for approximately 28% of total stout sales, while e-commerce and direct-to-consumer platforms represent the fastest-growing sub-channel at an estimated 18% CAGR within the off-trade segment.

Regional Market Insights

Europe's market leadership (37.6%, 2025) reflects centuries of stout brewing heritage. Ireland's St. James's Gate Brewery produces more than 7 million hectolitres of beer annually, with stout accounting for slightly over 70% of total output. The UK's Campaign for Real Ale (CAMRA) network of over 170,000 members continues to champion real ale and craft stout, maintaining category awareness and on-trade presence across 47,000+ UK pubs.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Europe |

37.6% |

Pub culture, craft growth, and premium stout demand |

|

North America |

22.4% |

Craft beer movement, premiumization, import growth |

|

Asia-Pacific |

18.7% |

Rising disposable income, Western beer adoption |

|

Latin America |

11.3% |

Beer culture expansion, growing middle class |

|

Middle East & Africa |

10.0% |

Diaspora consumption, tourist venues |

North America (22.4%) is the highest-growth region. The 2025 Beer Serves America study found that the industry supports over 2.42 million jobs in the United States and contributes more than USD 471 billion to the national economy. Left Hand Brewing's Milk Stout Nitro is among the top-five bestselling craft dark beers nationally, demonstrating mainstream viability for craft stout beyond enthusiast consumers.

Competitive Landscape

The global stout market exhibits moderate-to-high concentration at the premium end, anchored by Diageo's Guinness brand, which alone commands an estimated 45-50% of total global stout volume. The top five players, Diageo, HEINEKEN N.V., Carlsberg Breweries A/S, The Boston Beer Company, and Left Hand Brewing Company, collectively hold approximately 60-65% of the premium stout market revenue in 2025.

|

Company Name |

Brand/Product Name |

Market Position |

Core Strength |

|

Diageo |

Guinness |

Market Leader |

World's top stout brand; 150+ country distribution |

|

HEINEKEN N.V. |

Murphy's |

Strong Challenger |

Irish stout heritage; European pub network |

|

Carlsberg Breweries A/S |

Connor's Stout Porter, Danish Royal Stout |

Strong Challenger |

Growing premium portfolio; Asian expansion |

|

The Boston Beer Company |

Samuel Adams |

Challenger |

Craft leadership in North America |

|

Left Hand Brewing Co. |

Nitro range |

Niche Player |

Nitro stout pioneer; craft market specialist |

Key Company Profiles

Diageo

Diageo is a British multinational alcoholic beverages company headquartered in London and the owner of Guinness, the world's best-selling stout brand. Guinness serves over 10 million pints daily across various markets.

- Product Portfolio: Guinness Draught, Guinness Foreign Extra Stout, Guinness Extra Stout, Guinness 0.0, Guinness Nitrosurge.

- Recent Developments: In December 2025, Diageo opened a Guinness Open Gate Brewery in London, creating a dedicated stout-focused destination that enhances consumer engagement through immersive experiences, tastings, and hospitality offerings.

- Strategic Focus: Premiumization, no/low alcohol expansion, Africa market deepening, and sustainable brewing operations.

HEINEKEN N.V.

HEINEKEN N.V. is a Dutch multinational brewing company and the owner of Murphy's Irish Stout and Beamish Stout, two of Ireland's most historically significant stout brands. HEINEKEN operates multiple breweries, providing global distribution leverage for its stout portfolio.

- Product Portfolio: Murphy's Irish Stout, Beamish Stout, and select dark and specialty ales across regional portfolios.

- Recent Developments: In November 2024, Heineken Cambodia launched ABC Smooth Stout, combining the brand’s 30-year premium stout heritage with a smoother, more accessible taste to appeal to both loyal consumers and new drinkers.

- Strategic Focus: Heritage brand revival, Irish cultural identity marketing, and on-trade relationship strengthening in European markets.

Market Concentration Analysis

The global stout market exhibits high concentration at the brand level, with Diageo's Guinness commanding an estimated 45-50% of total stout volume globally, making it among the most concentrated single-brand categories in the global beer industry. The top five players, Diageo, HEINEKEN N.V., Carlsberg Breweries A/S, The Boston Beer Company, and Left Hand Brewing Company, collectively hold approximately 60-65% of the premium stout market revenue in 2025.

However, significant fragmentation exists below the top tier. An estimated 8,000+ craft breweries globally produce at least one stout variant, representing a long tail of value-added, premium products that aggregate to approximately 18-22% of total market revenue. Regional stout producers in Africa (particularly Nigeria's Star Stout and Tanzania's Kilimanjaro Dark) add further complexity to the competitive map.

Consolidation activity is limited in the stout segment specifically, though broader beer market M&A remains active. Craft brewery acquisitions by global majors, such as AB InBev's craft M&A program, have occasionally included stout-specialist producers, but independent craft stout brands continue to generate premium pricing power that incentivizes independent ownership.

Investment & Growth Opportunities

Fastest Growing Segments

No/low alcohol stout (estimated CAGR 12.4%), premium craft and imperial stout (9.8% CAGR), and nitro-technology off-trade formats (7.2% CAGR) represent the three highest-growth investment vectors through 2034. Together, these niches address a total addressable market of approximately USD 2.8 billion by 2030.

Emerging Market Expansion

Sub-Saharan Africa and South/Southeast Asia collectively represent an incremental USD 1.1 Billion stout opportunity by 2034. Guinness's existing African infrastructure - operating breweries in Nigeria, Ghana, Kenya, and Cameroon - provides a blueprint for local production to serve domestic demand while premium imports serve hospitality channels.

Venture and Institutional Investment Trends

- Key investment themes include nitro-dispensing technology, sustainability in brewing (renewable energy, water recycling), and direct-to-consumer e-commerce platforms for premium craft stout.

- Private equity interest in regional craft breweries with stout-led portfolios is growing, with deal activity focused on brands commanding retail price premiums of 40%+ over category average.

- Export-oriented microbrewery investment in North America is accelerating, targeting European and Asian markets where imported stout commands significant premiums.

Future Market Outlook (2026-2034)

The global stout market is positioned for broad-based, sustained growth through 2034. From a base of USD 10.29 Billion in 2025, the market is projected to reach USD 15.73 Billion by 2034, representing total incremental value creation of approximately USD 5.44 Billion over the forecast decade.

The structural macro-themes will define the market's long-term trajectory. First, the continued global craft beer movement will sustain premiumization, driving average selling price per liter upward even as volumes grow modestly. Second, on-trade recovery and experience-driven consumption will support draft stout's dominance as consumers prioritize quality out-of-home occasions.

Technological advances in nitrogen infusion, sustainability practices in large-scale brewing, and data-driven quality management will reshape competitive advantage. Brands that successfully position stout within health-conscious, sustainability-aware, and experiential consumer frameworks will disproportionately benefit from the market's evolution through 2034.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 130 industry participants in 2024–2025, including stout brand managers, pub operators, wholesale distributors, retail buyers, and independent craft brewery owners across Europe, North America, Asia-Pacific, and Africa.

Secondary Research

Secondary research encompassed a systematic review of company annual reports, HMRC alcohol duty statistics, Euromonitor Passport data, IWSR Drinks Market Analysis, trade publications (The Morning Advertiser, Beer Today, Craft Beer & Brewing), and publicly available financial disclosures. Over 230 secondary sources were reviewed and cross-triangulated.

Forecasting Models

Market size estimations and growth projections were derived using top-down and bottom-up forecasting methodologies, incorporating per-capita beer consumption indices, on-trade vs. off-trade volume splits, and historical market evolution across comparable dark beer categories. A base-case CAGR of 4.65% reflects consensus analyst estimates validated against reported brewer revenue growth rates.

Stout Market Report Scope

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Distribution Channels Covered | On-Trade, Off-Trade |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Diageo, HEINEKEN N.V., Carlsberg Breweries A/S, The Boston Beer Company, Left Hand Brewing Co., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the stout market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global stout market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the stout industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Stout Market Report

The global stout market reached USD 10.29 Billion in 2025 and is forecast to reach USD 15.73 Billion by 2034.

The stout market is projected to grow at a CAGR of 4.65% during the forecast period 2026-2034.

Europe leads with a 37.6% share in 2025, driven by Ireland, the UK, Germany, and a deep-rooted pub culture.

On-Trade channels dominate with a 60.8% market share in 2025, reflecting stout's intrinsic association with pub and bar consumption.

Key players include Diageo, HEINEKEN N.V., Carlsberg Breweries A/S, The Boston Beer Company, and Left Hand Brewing Company.

Growth is driven by the craft beer movement, premiumization trends, on-trade recovery, and rising premium import demand in the Asia-Pacific.

Guinness, owned by Diageo, is the world's best-selling stout, serving over 10 million pints daily across 150+ countries.

Guinness 0.0, launched in 2021, rapidly captured a significant UK no/low beer share. The segment is expanding at approximately 12.4% CAGR.

Key challenges include health-conscious consumption shifts, reducing alcohol intake, rising raw material costs, and regulatory complexity across markets.

The global stout market is projected to reach approximately USD 12.92 billion in 2030, based on a 4.65% CAGR from 2025.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)