Sun Care Products Market Size, Share, Trends and Forecast by Product Type, Product Form, Gender, Distribution Channel, and Region, 2026-2034

Sun Care Products Market Size, Share, Trends & Forecast (2026-2034)

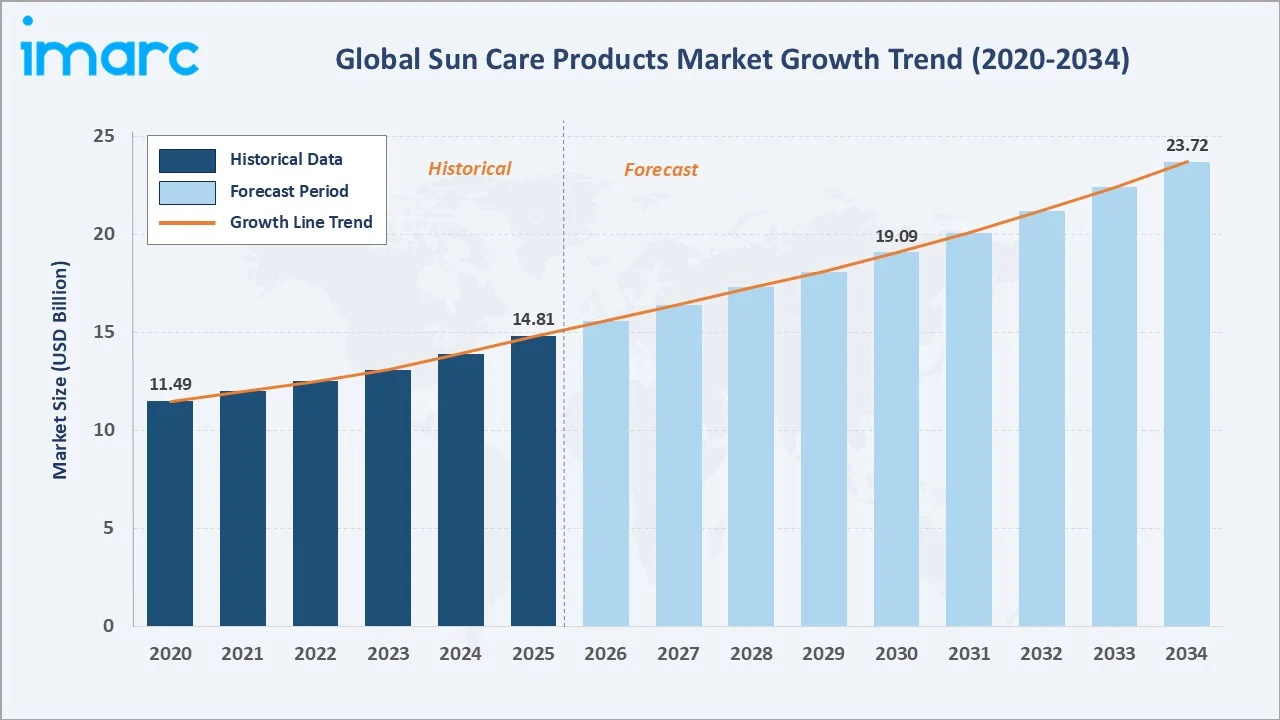

The global sun care products market reached USD 14.81 Billion in 2025 and is projected to reach USD 23.72 Billion by 2034, growing at a CAGR of 5.21% during 2026-2034. The market is driven by rising UV awareness, growing demand for broad-spectrum SPF formulations, premiumization of sun care portfolios, and expanding outdoor recreation globally.

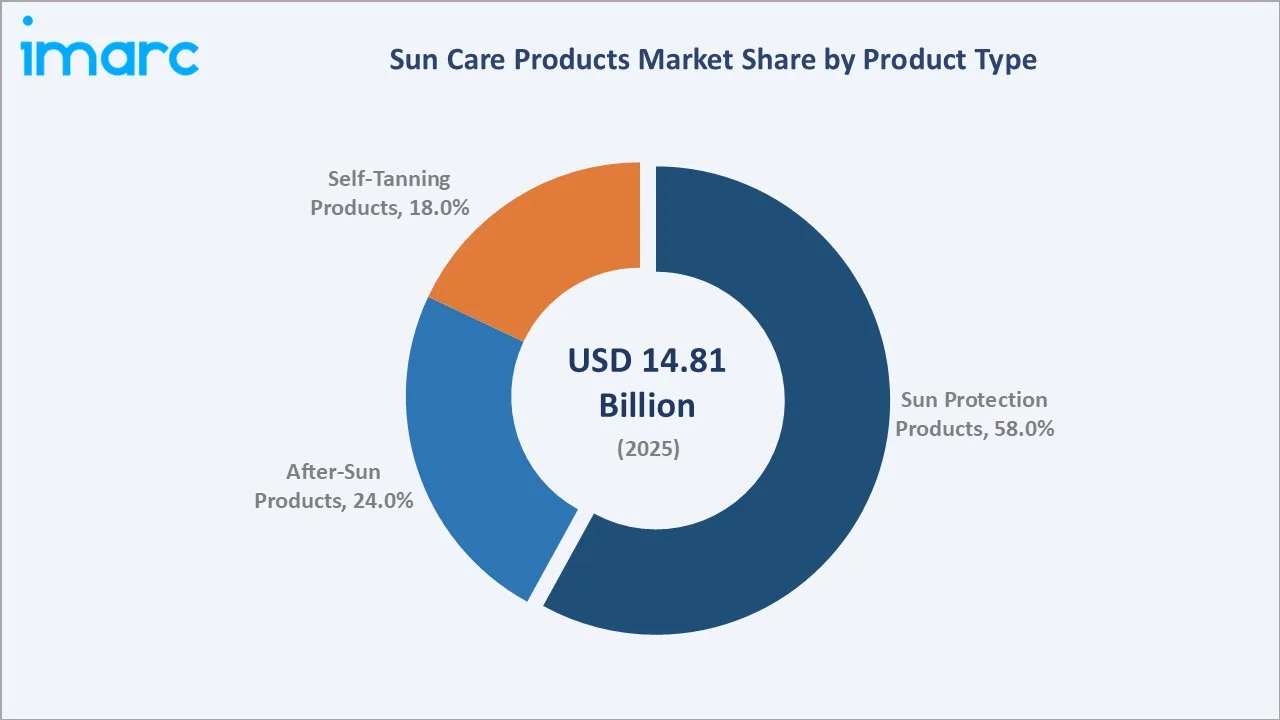

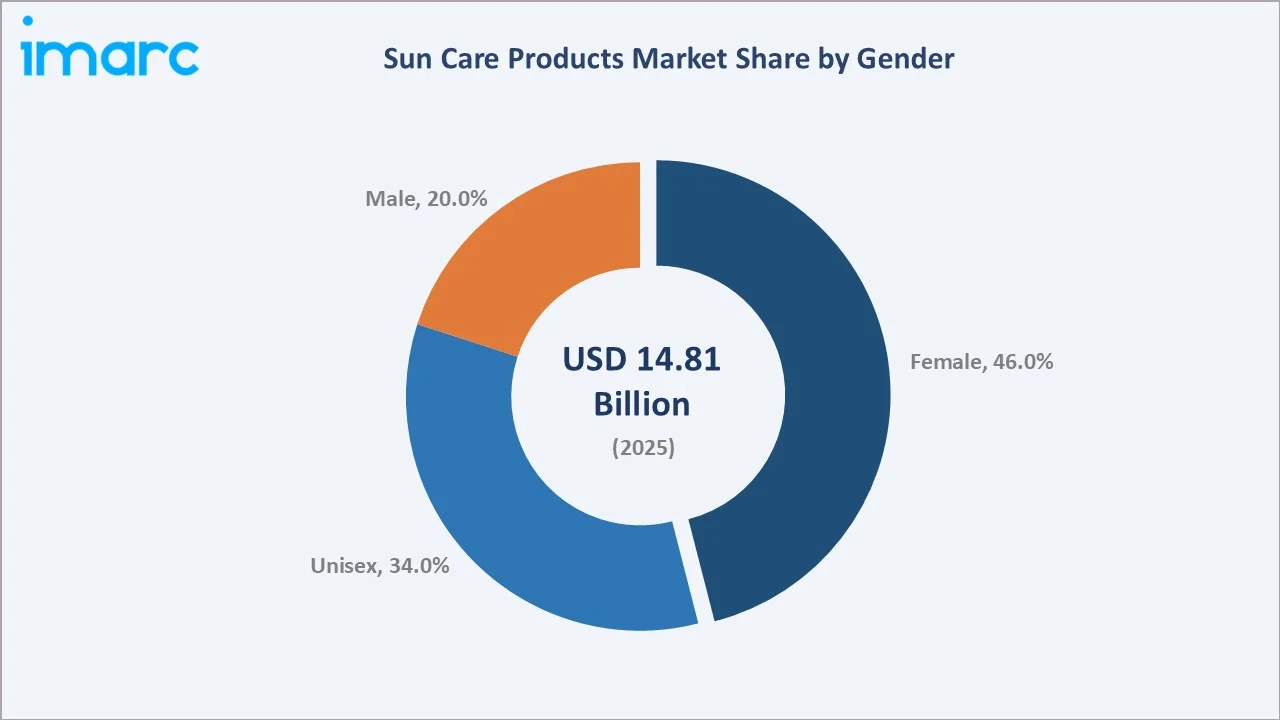

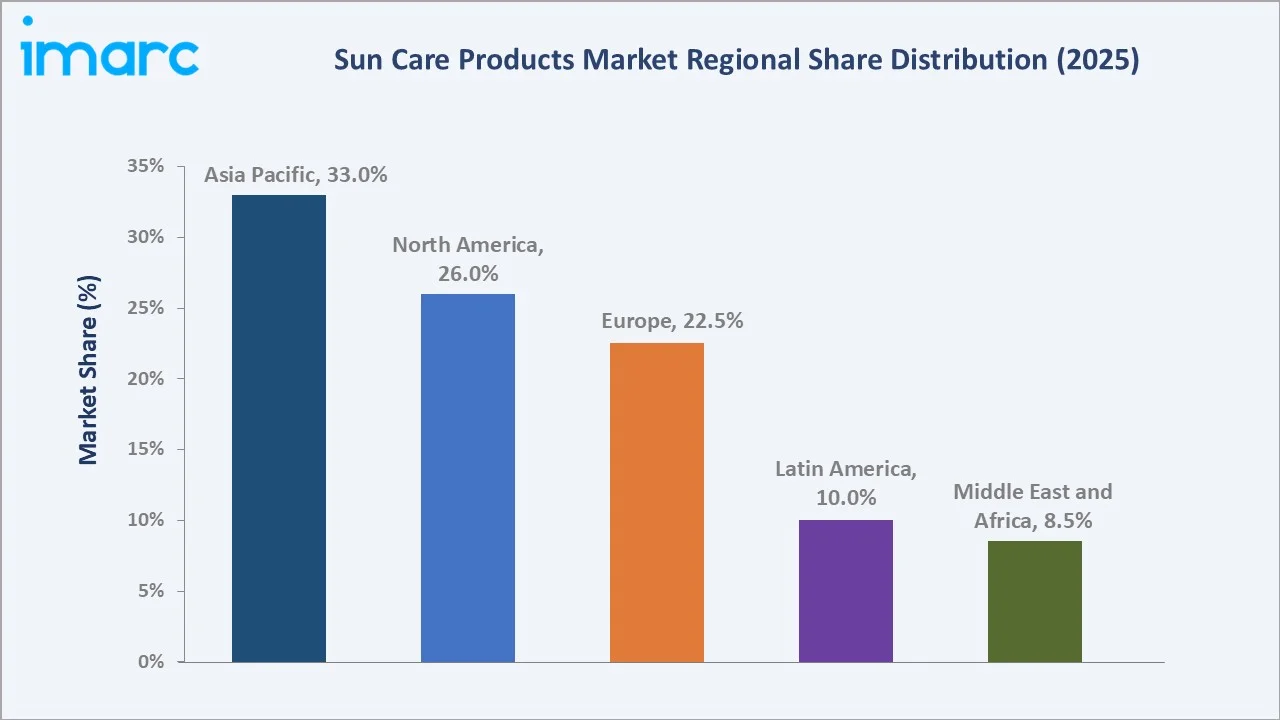

Sun Protection Products dominate at 58.0%. Female consumers lead the gender segment at 46.0%. Asia Pacific commands 33.0% of the global market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 14.81 Billion |

|

Forecast Market Size (2034) |

USD 23.72 Billion |

|

CAGR (2026-2034) |

5.21% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Product Type |

Sun Protection Products (58.0%, 2025) |

|

Dominant Gender Segment |

Female (46.0%, 2025) |

|

Leading Region |

Asia Pacific (33.0%, 2025) |

The market expanded from USD 11.49 Billion in 2020 to USD 14.81 Billion in 2025, anchored at USD 19.09 Billion in 2030, and forecast to reach USD 23.72 Billion by 2034. Growth is underpinned by rising UV-related skin cancer awareness, post-pandemic recovery in outdoor recreation and travel, and accelerating premiumization of SPF-integrated skincare across key consumer markets.

To get more information on this market, Request Sample

Self-Tanning Products grow fastest at ~6.2% CAGR driven by sun-safe bronzing trends. The Male gender segment grows at ~6.0% CAGR through men's grooming expansion. Asia Pacific leads regional CAGR at ~6.1% through South and Southeast Asian market development alongside continued K-beauty and J-beauty sun care innovation.

Executive Summary

The global sun care products market reached USD 14.81 Billion in 2025, representing a mature yet rapidly evolving personal care segment driven by growing UV awareness, cosmetic innovation in SPF, and expanding consumer health consciousness. The market is projected to reach USD 23.72 Billion by 2034.

Sun Protection Products at 58.0% dominate as the most essential category, underpinned by dermatologist recommendations and public health mandates for daily SPF use. Female consumers at 46.0% represent the primary demand base, with Unisex products gaining momentum through gender-neutral marketing. Asia Pacific commands 33.0% of global share, led by high UV-exposure markets in China, Japan, South Korea, and India.

Key Market Insights

|

Insight |

Data |

|

Dominant Product Type |

Sun Protection Products – 58.0% share (2025) |

|

Dominant Gender Segment |

Female – 46.0% market share (2025) |

|

Leading Region |

Asia Pacific – 33.0% market share (2025) |

|

Market Opportunity |

Mineral sunscreens; gender-neutral SPF; tinted sun protection; self-tanning innovation; D2C channel growth |

Key Analytical Observations Supporting The Above Data:

- Sun Protection Products at 58.0%: Dominates through year-round consumer awareness of UV damage, broadened SPF product ranges across mass and premium tiers, and growing integration of SPF into daily skincare routines globally.

- Female Segment at 46.0%: Leads consumption through deeper engagement with skincare regimens, higher awareness of photoaging, and strong adoption of SPF-integrated cosmetics and beauty products across all age groups.

- Asia Pacific at 33.0%: Regional dominance driven by high UV index environments, K-beauty and J-beauty SPF innovation leadership and rising disposable incomes in fast-growing emerging markets.

Sun Care Products Market Overview

The global sun care products market encompasses all topical and cosmetic formulations designed to protect, soothe, or aesthetically enhance skin exposed to sunlight. This includes broad-spectrum sunscreens, SPF moisturizers, after-sun soothing products, and self-tanning formulations across mass, masstige, and premium tiers.

The ecosystem integrates UV filter and raw material suppliers, cosmetic formulators, contract manufacturers, global beauty conglomerates, specialty dermatological brands, pharmacies, specialty retailers, and online platforms. Macroeconomic drivers include rising UV-induced skin cancer incidence, growing outdoor recreation, tourism recovery, and expanding middle-class beauty spending in emerging markets.

Market Dynamics

To evaluate market opportunities, Request Sample

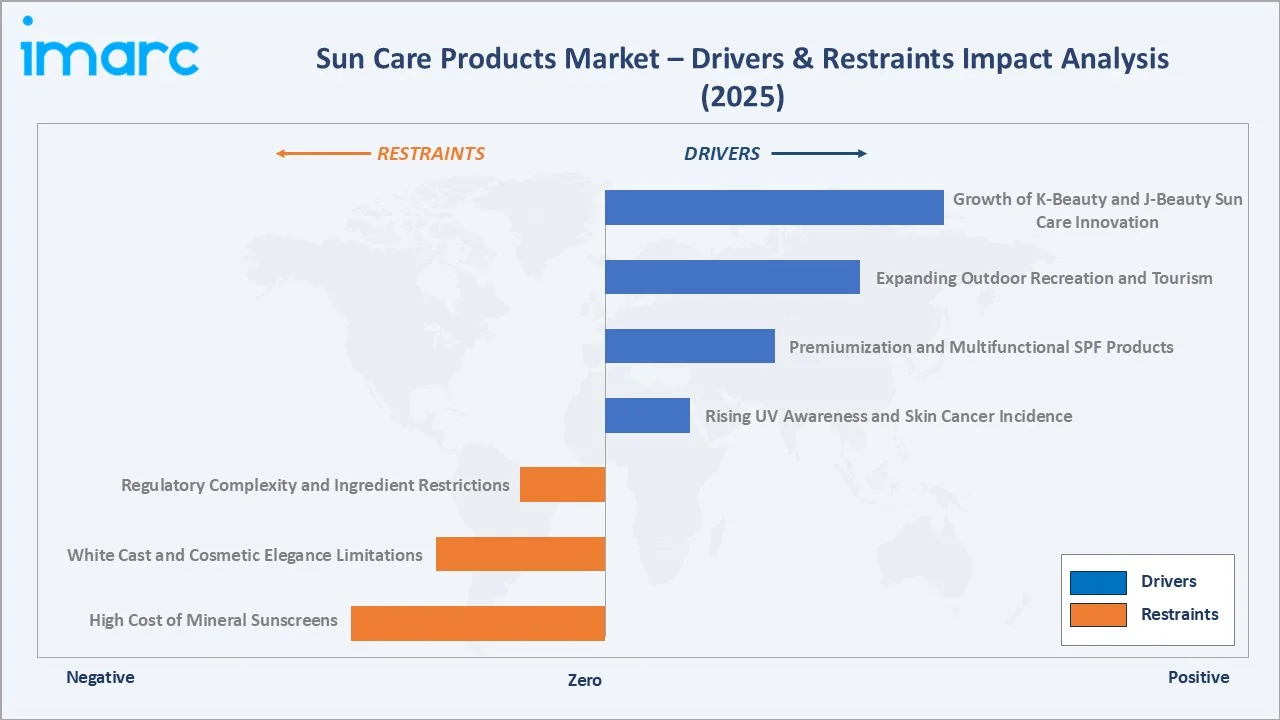

Market Drivers

- Rising UV Awareness and Skin Cancer Incidence: Growing global incidence of melanoma and non-melanoma skin cancers is driving broad-spectrum SPF adoption. Public health campaigns by dermatological associations and WHO UV Index communications are educating consumers on daily SPF use, expanding the addressable sun protection market across all demographics, regions, and age groups.

- Premiumization and Multifunctional SPF Products: Consumer demand for hybrid sun care combining SPF protection with anti-aging, moisturizing, and toning benefits is driving the premium segment. Brands are launching tinted SPF moisturizers, SPF primers, and SPF serums, increasing average selling prices and adoption across diverse consumer groups seeking skin performance and protection together.

- Expanding Outdoor Recreation and Tourism: Global recovery of outdoor leisure, sports, and tourism is boosting seasonal and year-round demand for sun care products. Adventure tourism, beach vacations, and urban outdoor fitness create consistent demand across sun protection, after-sun, and self-tanning categories, with seasonal peaks driving high-volume retail sell-through globally.

- Growth of K-Beauty and J-Beauty Sun Care Innovation: South Korean and Japanese brands are redefining sun care with lightweight SPF formulations featuring hybrid textures, including sunscreen sticks, essences, and cushion compacts. These innovations are gaining global traction and raising consumer expectations for sun care efficacy, skin compatibility, and cosmetic elegance worldwide.

Market Restraints

- High Cost of Mineral Sunscreens: Zinc oxide and titanium dioxide-based mineral sunscreens command significant price premiums over chemical alternatives. High raw material and formulation costs limit accessibility for price-sensitive consumer segments in developing economies, constraining volume growth in mass-market sun protection categories across the Asia Pacific and Latin America.

- White Cast and Cosmetic Elegance Limitations: Traditional mineral sunscreens leave visible white residue on darker skin tones, limiting adoption among significant global consumer demographics. Despite R&D in transparent mineral formulations, cosmetic acceptance remains a commercial barrier, particularly in the Asia Pacific and Latin American markets with diverse skin tone populations.

- Regulatory Complexity and Ingredient Restrictions: Diverging global regulatory frameworks for sunscreen actives create compliance complexity for multinational brands. The US FDA's categorization of several chemical UV filters as requiring additional safety data and EU restrictions on certain sunscreen actives increase formulation costs and limit ingredient choice for global manufacturers.

Market Opportunities

- Mineral Nano-Dispersion and Transparent SPF Technology: Advances in nano-dispersed mineral UV filters enable transparent, cosmetically elegant formulations suitable for all skin tones. These technologies expand mineral sunscreen adoption beyond niche clean beauty consumers into mainstream markets, creating a significant commercial opportunity for brands investing in transparent mineral SPF innovation.

- Self-Tanning Innovation and Sun-Safe Aesthetics: Consumer preference for bronzed aesthetics without UV exposure is driving consistent growth in self-tanning. Advances in DHA delivery, gradual tanning technologies, and natural bronzer formulations are expanding self-tanning accessibility and creating new premium product tiers for brands in this fastest-growing sun care subsegment.

Market Challenges

- Ingredient Safety Scrutiny and Clean Beauty Pressure: Ongoing consumer and regulatory scrutiny of chemical UV filter safety is increasing formulation complexity. Brands must balance efficacy, regulatory compliance, and clean-label consumer demand, requiring sustained R&D investment to maintain product competitiveness across diverging global regulatory frameworks and consumer expectations.

- Seasonal Demand Volatility Affecting Year-Round Revenue: Sun care demand remains heavily skewed toward summer months and holiday travel seasons, creating revenue volatility and inventory management challenges. Encouraging year-round SPF adoption through daily skincare positioning remains a key commercial challenge for the global sun care industry.

Emerging Market Trends

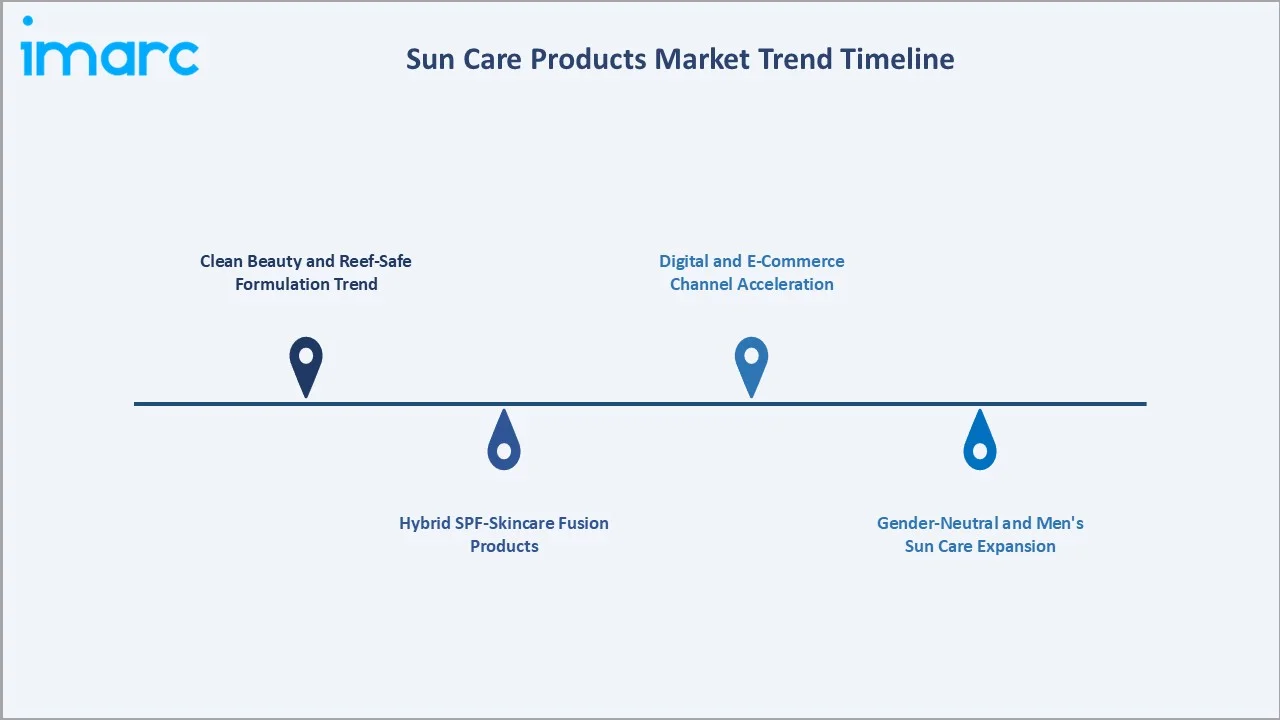

1. Clean Beauty and Reef-Safe Formulation Trend

Consumer and regulatory pressure are driving rapid adoption of reef-safe, biodegradable sunscreen formulations free from oxybenzone, octinoxate, and microplastics. Brands are reformulating with eco-conscious UV filters, natural antioxidants, and sustainable packaging, reshaping the product development roadmap across the industry and creating new premium positioning opportunities globally.

2. Hybrid SPF-Skincare Fusion Products

Integration of SPF into daily skincare products including moisturizers, serums, foundations, and lip care is expanding the sun care category beyond seasonal use. Hybrid SPF-skincare formulations are driving year-round consumer engagement and premiumization, particularly among female consumers investing in comprehensive anti-aging and daily skin protection routines.

3. Gender-Neutral and Men's Sun Care Expansion

The unisex and male sun care segments are growing as gender-neutral marketing, men's grooming trends, and sports-focused SPF products attract new male consumers. SPF-integrated grooming products including moisturizers, lip balms, and post-shave treatments are broadening the market beyond female-dominated consumer demographics into new addressable segments.

4. Digital and E-Commerce Channel Acceleration

Online channels and direct-to-consumer models are enabling indie sun care brands and niche SPF innovators to reach global audiences cost-effectively. Personalization tools, skin type assessments, and subscription-based sun care models are driving customer retention in e-commerce, growing significantly faster than traditional brick-and-mortar retail channels.

Industry Value Chain Analysis

The sun care products value chain integrates raw material and UV filter sourcing, cosmetic formulation and manufacturing, packaging and branding, multi-channel distribution and retail, and after-sales consumer engagement. The commercial architecture is progressively shifting toward D2C and e-commerce as primary growth channels alongside traditional pharmacy and specialty retail.

|

Stage |

Key Activities |

|

Raw Material & UV Filter Sourcing |

Procurement of chemical and mineral UV filters, botanical extracts, emollients, and packaging raw materials from global suppliers |

|

Formulation & Manufacturing |

Development and production of sunscreen, after-sun, and self-tanning formulations, including stability testing, safety assessment, and regulatory compliance |

|

Packaging & Branding |

Primary and secondary packaging design, labelling, regulatory text compliance, and sustainable packaging development for retail and e-commerce channels |

|

Distribution & Retail |

Multi-channel distribution covering supermarkets, pharmacies, specialty beauty retailers, online marketplaces, and direct-to-consumer platforms |

|

After-Sales & Consumer Engagement |

Consumer education, dermatologist partnerships, loyalty programs, digital skin advice tools, and product repurchase facilitation |

The raw material and UV filter sourcing stage is the most commercially sensitive due to regulatory restrictions on certain chemical UV filters and growing demand for natural and mineral alternatives. The distribution and retail stage is experiencing the most rapid structural transformation as brands increasingly invest in D2C and e-commerce to capture higher margins and build direct consumer relationships.

Technology Landscape in the Sun Care Products Industry

Broad-Spectrum UV Filter Technology

Modern broad-spectrum formulations combine UVA and UVB filters to deliver comprehensive photon protection. Advanced encapsulation of chemical UV filters enhances photostability, reduces skin irritation, and improves cosmetic elegance, enabling high-SPF formulations with lightweight, non-greasy textures suitable for daily use across diverse skin types and climates.

Mineral Nano-Dispersion Technology

Nanotechnology-enabled zinc oxide and titanium dioxide dispersions reduce the cosmetic white cast of mineral sunscreens while maintaining UV barrier efficacy. Transparent mineral formulations are expanding adoption among diverse skin tone consumers and supporting growth in the premium clean beauty sun care segment, making mineral SPF commercially viable for mainstream markets.

After-Sun and Skin Recovery Technology

Advanced after-sun formulations incorporate hyaluronic acid, ceramides, aloe vera extracts, and anti-inflammatory actives to accelerate skin recovery and restore barrier function. These technologies drive premiumization in the after-sun category and support year-round product usage beyond peak seasonal sun protection periods.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Sun Protection Products |

58.0% |

2025 |

|

Product Form |

Lotion |

🔒 |

2025 |

|

Gender |

Female |

46.0% |

2025 |

|

Distribution Channel |

Pharmacies and Drug Stores |

🔒 |

2025 |

|

Region |

Asia Pacific |

33.0% |

2025 |

By Product Type

Sun Protection Products lead at 58.0% in 2025, representing the core essential category driven by medical necessity, dermatologist recommendations, and year-round daily-use adoption. This segment encompasses sunscreen lotions, creams, sprays, sticks, and SPF-integrated cosmetics across SPF levels from SPF 15 to SPF 100+.

To access detailed market analysis, Request Sample

After-Sun Products at 24.0% serve the post-exposure recovery market with moisturizing and soothing formulations. Self-Tanning Products at 18.0% represent the fastest-growing subsegment, driven by sun-safe tanning aesthetics, social media beauty trends, and technological advances in streak-free, natural-looking bronze formulations for a broad range of skin tones.

By Gender

Female consumers at 46.0% represent the largest gender segment, driven by higher skincare engagement, greater awareness of photoaging, and strong adoption of SPF as a daily essential. Unisex products at 34.0% reflect gender-neutral marketing and growing male engagement with sun care through sports, outdoor activity, and grooming awareness.

Male consumers at 20.0% represent the fastest-growing gender subsegment as awareness campaigns and men's grooming trends accelerate SPF adoption. The male sun care segment is particularly expanding in North America and Europe through sports-focused SPF positioning and dedicated men's skincare product innovation from both established and indie brands.

Regional Market Insights

|

Region |

Share (2025) |

Key Market Drivers & Characteristics |

|

Asia Pacific |

33.0% |

Driven by high UV index environments, lightweight SPF formulation innovation, rising disposable incomes, and growing skin protection awareness across major economies in the region |

|

North America |

26.0% |

Supported by high UV-related health awareness, strong dermatologist-recommended SPF adoption, premium product penetration, and well-developed retail and e-commerce infrastructure |

|

Europe |

22.5% |

Driven by stringent cosmetic regulations, high UV risk awareness, growing clean beauty and reef-safe sun care demand, and strong preference for sustainable and mineral formulations |

|

Latin America |

10.0% |

Driven by high UV exposure levels, growing middle-class consumer spending, expanding modern retail footprint, and increasing integration of sun care into daily personal care routines |

|

Middle East and Africa |

8.5% |

Emerging with high ambient UV intensity, rising consumer awareness of skin protection, growing beauty and personal care spending, and expanding organised retail infrastructure |

Asia Pacific at 33.0% leads globally through premium sun care consumption growth, lightweight SPF formulation innovation, and rapidly expanding mass-market sun care adoption in high UV intensity markets. North America at 26.0% reflects mature consumer awareness and a strong dermatologist-driven SPF recommendation culture.

Europe at 22.5% benefits from clean beauty regulation convergence and growing demand for sustainable sun care formulations. Latin America and the Middle East and Africa represent high-growth emerging markets, driven by natural UV intensity, expanding modern retail infrastructure, and rising consumer awareness of sun protection benefits.

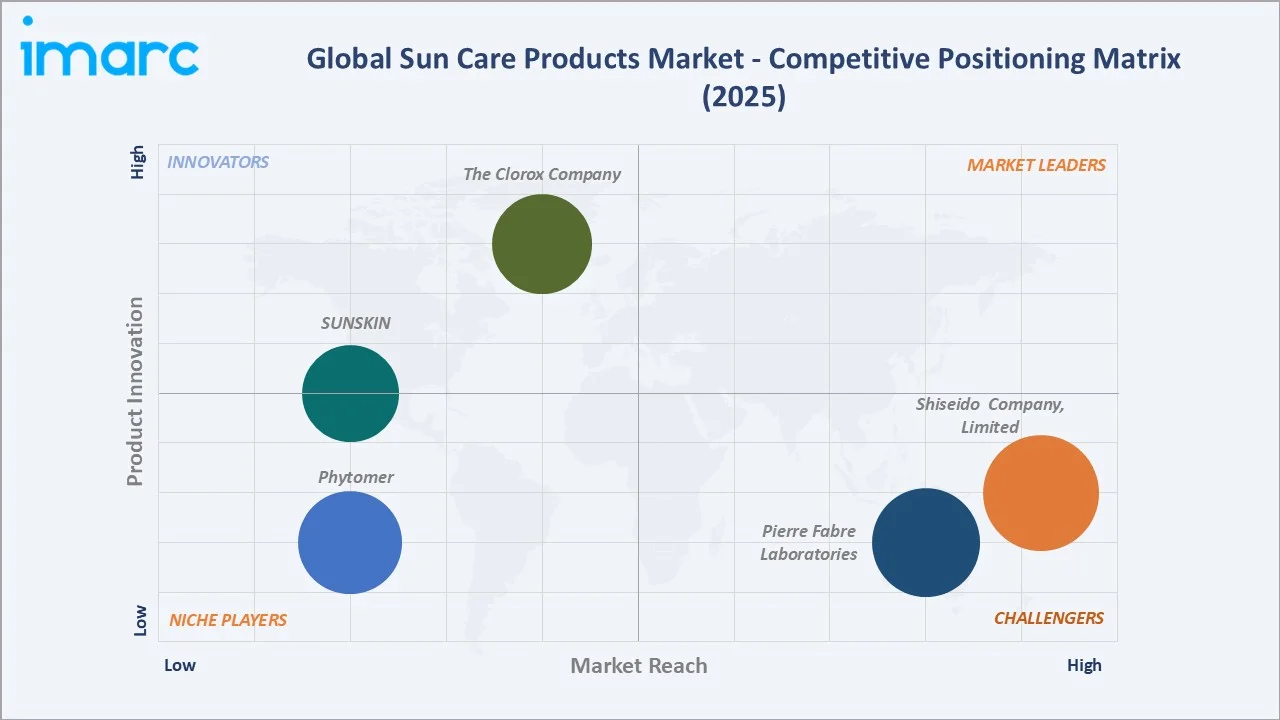

Competitive Landscape

The global sun care products market competitive landscape is moderately concentrated with three distinct competitive tiers: global beauty conglomerates with integrated sun care portfolios, dermatologist-endorsed specialty SPF brands, and regional and mass-market manufacturers serving local consumer preferences.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Shiseido Company, Limited |

Anessa, Perfect Uv Protector S, Shiseido The Perfect Protector Spf 50+ Pa++++ Syncroshield |

Strong Challenger |

Leading innovator in lightweight, high-performance SPF formulations with dominant market presence in Asia Pacific |

|

Pierre Fabre Laboratories |

EAU THERMALE AVÈNE SPF 50+ Spray, A-Derma PROTECT Very High Protection Spray SPF50+, Actine Protetor Solar FPS 30 |

Strong Challenger |

Dermatologist-endorsed SPF portfolio spanning sensitive and medical-grade skin care |

|

Phytomer |

Sun Reset, SunActive |

Niche Player |

Marine biotechnology pioneer specialising in sea-derived active ingredients; sun care combining UV filters with marine anti-aging and repair actives; |

|

The Clorox Company |

Island Getaway SPF 30 Lip Balm, Coco Loco SPF 30 Lip Balm, SPF 30 Sensitive Solutions Calming Day Lotion, Aloe & Coconut Oil After Sun Soother, Aloe After Sun Soother, Beaches & Cream SPF 30 Lip Balm, SPF 30 Renewal Firming Day Lotion |

Specialty Player |

Natural and mineral-focused sun care portfolio positioned for clean beauty consumers seeking reef-safe formulations |

|

SUNSKIN |

Face sunscreen, Face & Body sunscreen, Tinted sunscreen, Spray sunscreen, Lips Protection |

Emerging Player |

South Africa-based specialist sun care brand offering full-spectrum SPF 50 formulations across face, body, tinted, and lip categories; focused on dry-touch, lightweight, skin-sensitive formulations for active and daily use |

Key players include Shiseido Company, Limited, Pierre Fabre Laboratories, Phytomer, The Clorox Company, SUNSKIN, and others.

Key Company Profiles

Shiseido Company, Limited

Shiseido Company is a Japan-based global cosmetics company recognised as a leading innovator in lightweight, high-performance SPF formulations, with its sun care portfolio widely regarded as a benchmark for product elegance and efficacy in Asia Pacific markets.

- Key Products: Anessa, Perfect Uv Protector S, Shiseido The Perfect Protector Spf 50+ Pa++++ Syncroshield

- Strategic Focus: Global expansion of premium sun care formulations, investment in SPF-skincare hybrid product innovation, and integration of digital beauty platforms for personalised sun care recommendations in key growth markets.

Pierre Fabre Laboratories

Pierre Fabre Laboratories is a France-based global healthcare and dermo-cosmetics company, recognised as the world's second-largest dermo-cosmetics manufacturer and ranked No. 2 in sun protection in Europe. Its sun care portfolio, anchored by Eau Thermale Avène and A-Derma, is built on dermatologist-backed photoprotection research and proprietary UV filter innovation.

- Key Products: EAU THERMALE AVÈNE SPF 50+ Spray, A-Derma PROTECT Very High Protection Spray SPF50+, Actine Protetor Solar FPS 30

- Recent Developments: In May 2026, Pierre Fabre invested to expand and modernize its Avène manufacturing facility in southern France, aiming to double annual production capacity. The investment is intended to support growing global demand for Eau Thermale Avène products, particularly in key international markets such as China and the United States.

- Strategic Focus: Expanding dermatologist-endorsed sun care globally through the Avène and A-Derma brand platforms, scaling the patented TriAsorB™ ultra-broad-spectrum filter across new product formats, strengthening US and Asia market presence through regional innovation centres, and deepening the integration of dermo-cosmetic sun care with medical-grade skincare protocols under its "supportive care" strategy.

The Clorox Company

The Clorox Company is a US-based consumer goods corporation headquartered in Oakland, California, with Burt's Bees as its flagship natural personal care brand. Burt's Bees has been active in sun care and is recognised as a leading specialty player in natural, mineral-based, reef-safe sun care formulations positioned for clean beauty consumers.

- Key Products: Island Getaway SPF 30 Lip Balm, Coco Loco SPF 30 Lip Balm, SPF 30 Sensitive Solutions Calming Day Lotion, Aloe & Coconut Oil After Sun Soother, Aloe After Sun Soother, Beaches & Cream SPF 30 Lip Balm, SPF 30 Renewal Firming Day Lotion

- Strategic Focus: Strengthening Burt's Bees' natural and mineral sun care positioning through 100% natural origin, nano-free zinc oxide formulations; expanding reef-safe and ocean-friendly product credentials across the sun care range; driving growth through pharmacy, mass retail, and e-commerce channels; and advancing sustainability goals, including reduced virgin plastic packaging and responsible ingredient sourcing aligned with Clorox's broader ESG commitments.

Market Concentration Analysis

The sun care products market is moderately concentrated, with the top five companies accounting for approximately 45-55% of global sun care revenue. Market leaders maintain their position through dermatological brand credibility, broad retail distribution, and sustained product innovation investment.

Market concentration is gradually declining as indie SPF brands, clean beauty labels, and regional players gain consumer traction through e-commerce and social media-driven brand discovery, reducing barriers to consumer adoption for smaller entrants.

Investment & Growth Opportunities

Highest Growth Segments

Self-Tanning Products (~6.2% CAGR), the male sun care segment (~6.0% CAGR), the Asia Pacific region (~6.1% CAGR), mineral and clean-label SPF formulations, tinted sun protection with makeup functionality, after-sun probiotic and barrier-repair formulations, and SPF-integrated skincare hybrid products represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

Personalised SPF powered by skin AI diagnostics, digital skin tone analysis tools matching consumers to optimal SPF formulations, and subscription-based D2C sun care models represent emerging commercial investment themes. Sustainable packaging innovation and biodegradable UV filter research are increasingly critical for regulatory compliance and ESG-aligned brand strategy.

Investment Themes

- Transparent mineral SPF technology scaling: Mineral UV filter nano-dispersion technology represents the most commercially significant sun care innovation investment, enabling brands to serve reef-safe and clean-label consumer demand across all skin tones with cosmetically elegant, high-performance broad-spectrum sun protection.

- Asia Pacific emerging market expansion: High UV intensity environments, rising disposable incomes, and rapidly growing modern retail and e-commerce penetration across emerging economies in the region offer significant volume growth opportunities for both mass and premium sun care brands through the forecast period.

Future Market Outlook (2026-2034)

The global sun care products market is projected to grow from USD 14.81 Billion in 2025 to USD 23.72 Billion by 2034, delivering a 5.21% CAGR over the forecast period. Sun Protection Products will maintain their dominant market share through daily-use SPF normalisation across global consumer demographics, while Self-Tanning Products will post the fastest category growth driven by sun-safe beauty aesthetics.

Asia Pacific will consolidate its regional leadership through premiumisation in developed markets and mass-market expansion in emerging economies. Clean beauty regulation convergence in Europe and North America will continue reshaping formulation priorities, creating sustained opportunities for mineral SPF innovation, reef-safe certification, and eco-label brand differentiation globally through 2034.

Research Methodology

Primary Research

Primary research comprised structured interviews with 40+ industry stakeholders (2025), including dermatologists, brand R&D managers, cosmetic formulators, retail category managers, and consumer insights professionals across the US, Germany, Japan, China, and Brazil.

Secondary Research

Secondary research encompassed brand annual reports, WHO UV Index and skin cancer incidence data, Cosmetics Europe regulatory guidelines, retail sales data, and industry association publications. Over 50 secondary sources were reviewed for market sizing, segmentation, and competitive benchmarking.

Forecasting Models

Market revenue forecasts developed using a bottom-up model incorporating category-level demand by product type, gender, and region; SPF premiumisation trend adjustments; e-commerce channel growth multipliers; and historical CAGR calibration against 2020-2025 observed market performance data.

Sun Care Products Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types Covered | Sun Protection Products, After-Sun Products, Self-Tanning Products |

| Product Forms Covered | Cream, Gel, Lotion, Wipes, Spray, Others |

| Genders Covered | Female, Male, Unisex |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Specialty Retailers, Pharmacies and Drug Stores, Online Stores, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Shiseido Company Limited, Pierre Fabre Laboratories, Phytomer, The Clorox Company, SUNSKIN, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the sun care products market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global sun care products market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the sun care products industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Sun Care Products Market Report

The global sun care products market reached USD 14.81 Billion in 2025, driven by Sun Protection Products at 58.0%, Female consumers at 46.0% gender segment dominance, and Asia Pacific commanding 33.0% regional market share.

The sun care products market grows at 5.21% CAGR during 2026-2034, reaching USD 23.72 Billion by 2034, driven by clean beauty SPF innovation, self-tanning product growth, and expanding emerging market adoption.

Sun Protection Products lead at 58.0% in 2025, capturing the largest share through daily-use SPF normalisation, dermatologist-driven product adoption, and integration of SPF into mainstream beauty and skincare routines globally.

Female consumers lead at 46.0% in 2025, driven by greater skincare engagement and high adoption of SPF in daily beauty routines. Unisex and male segments are growing as gender-neutral sun care positioning gains consumer acceptance across key markets.

Asia Pacific leads at 33.0% through strong SPF innovation, high UV index markets, and expanding mass-market sun care adoption in rapidly growing consumer economies across the region.

Leading companies include Shiseido Company, Limited, Pierre Fabre Laboratories, Phytomer, The Clorox Company, SUNSKIN, and others.

The sun care products market is projected to reach USD 23.72 Billion by 2034, with mineral and reef-safe SPF innovation, self-tanning product expansion, and Asia Pacific emerging market growth as key structural drivers through the forecast period.

Three priority investment themes: transparent mineral SPF technology scaling for diverse skin tones, Asia Pacific emerging market sun care expansion through affordable and effective formulations, and personalised SPF powered by digital skin diagnostics and subscription-based D2C commerce models.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade