Surrogacy Market Size, Share, Trends and Forecast by Type, Technology, Service Provider, and Region 2026-2034

Surrogacy Market Size, Share, Trends & Forecast (2026-2034)

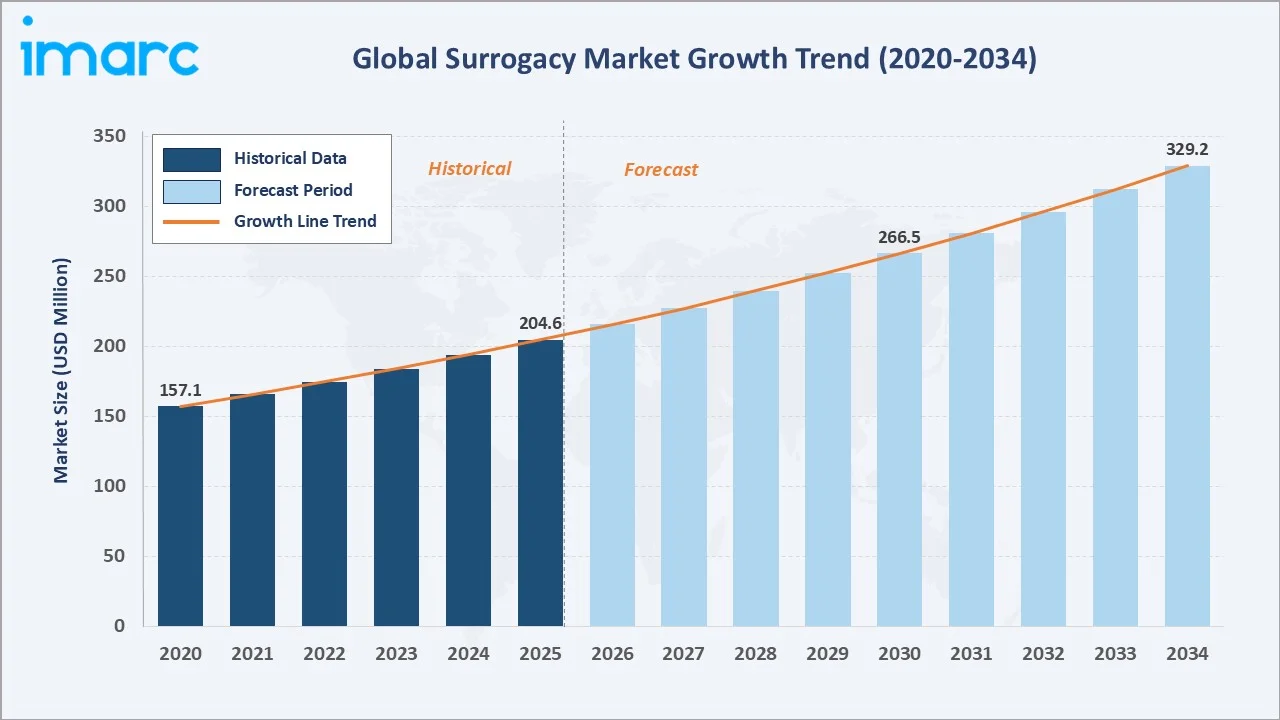

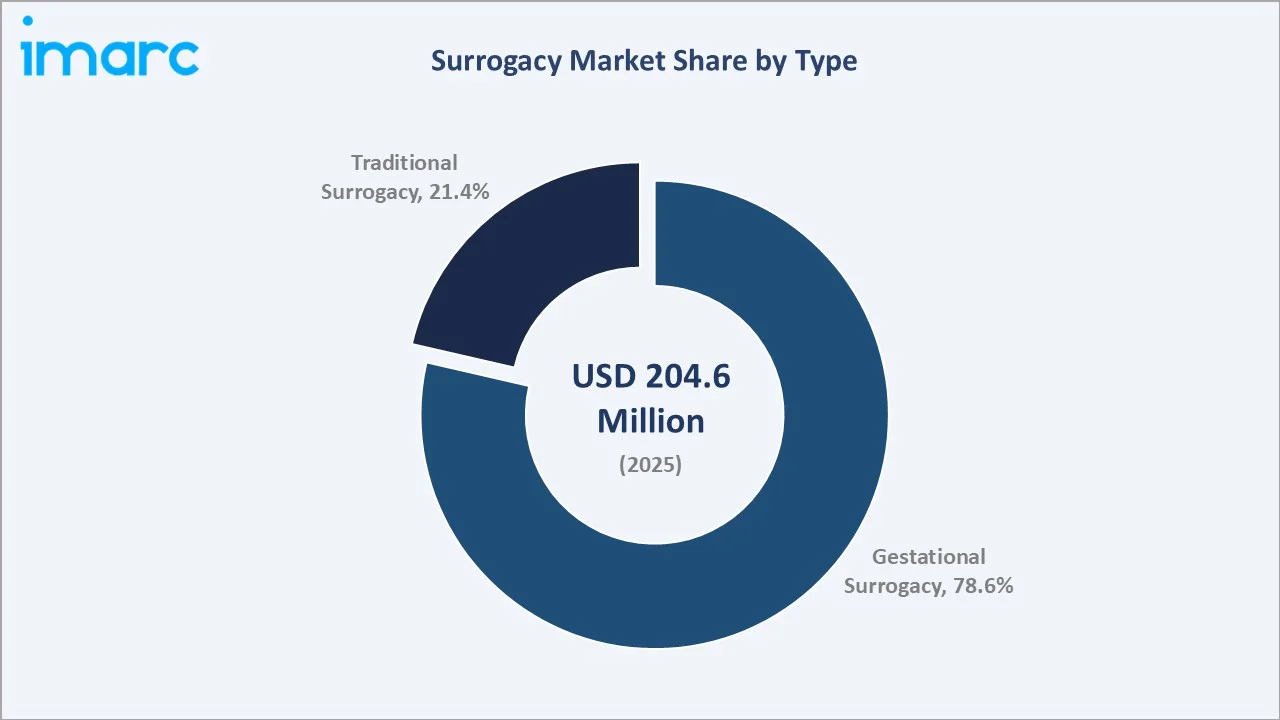

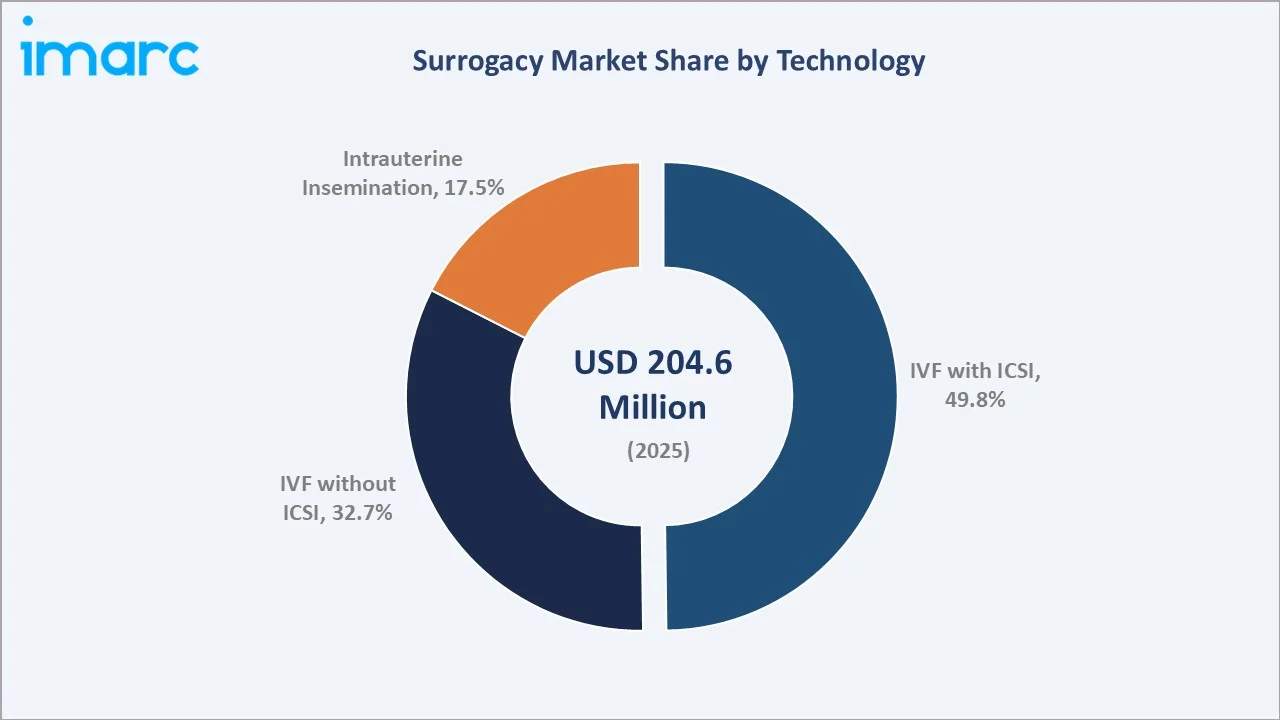

The global surrogacy market reached USD 204.6 Million in 2025 and is projected to reach USD 329.2 Million by 2034, growing at a CAGR of 5.43% during 2026-2034. Rising infertility rates, growing LGBTQ+ family-building demand, expanding fertility tourism, advancements in assisted reproductive technologies (ART), and increasing societal acceptance of surrogacy as a family-building pathway are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 204.6 Million |

|

Forecast Market Size (2034) |

USD 329.2 Million |

|

CAGR (2026-2034) |

5.43% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

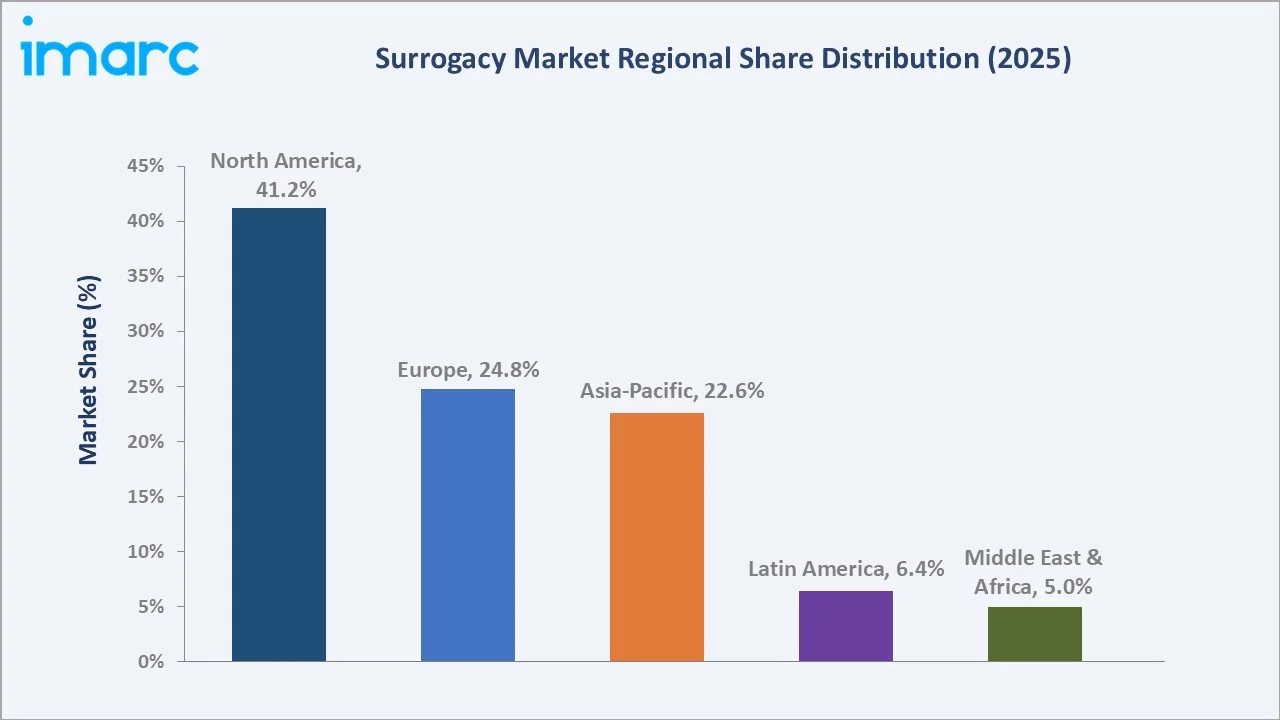

North America leads regionally with a 41.2% share in 2025, anchored by the United States’ permissive legal environment, advanced fertility clinic infrastructure, and established surrogacy agency ecosystem. Gestational surrogacy commands the dominant type segment at 78.6%, while IVF with ICSI leads the technology segment at 49.8%.

To get more information on this market, Request Sample

The global surrogacy market is driven by three structural forces: the rising prevalence of infertility and delayed parenthood in developed economies; the increasing legal recognition and societal normalization of gestational surrogacy in key markets; and the growing availability of lower-cost international surrogacy destinations through fertility tourism corridors. These forces collectively sustain a 5.43% CAGR through 2034.

Executive Summary

The global surrogacy market is experiencing steady growth underpinned by demographic, technological, and legal tailwinds. Valued at USD 204.6 Million in 2025, the market is forecast to reach USD 329.2 Million by 2034 at a CAGR of 5.43%. The persistent global infertility burden (WHO estimate: 17.5% of adults affected), the expanding LGBTQ+ family-building cohort, and IVF technology advances that have raised clinical pregnancy success rates per transfer cycle in leading clinics are the primary structural drivers.

Gestational surrogacy dominates at 78.6%, reflecting its clinical and legal advantages over traditional surrogacy: the surrogate carries no genetic relationship to the child, significantly reducing legal and emotional complexity for all parties. IVF with ICSI leads the technology segment at 49.8%, driven by its higher fertilization success rates, particularly in cases of male-factor infertility. North America commands 41.2% of the global market, anchored by the United States’ state-level legal frameworks in California, Nevada, and Washington that provide clear, enforceable surrogacy contracts and pre-birth orders.

Key players including Kindbody, Pinnacle Fertility, ConceiveAbilities, Surrogacy Is, and Golden Surrogacy are competing through service integration, technology-enabled care models, and international market expansion. In March 2026, Kindbody partnered with Future Family to expand nationwide access to fertility care by offering flexible financing solutions, dedicated financial specialists, and RN care coaches for patients undergoing treatments such as IVF, IUI, egg freezing, and genetic testing.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Gestational Surrogacy – 78.6% share (2025) |

|

Fastest Growing Type |

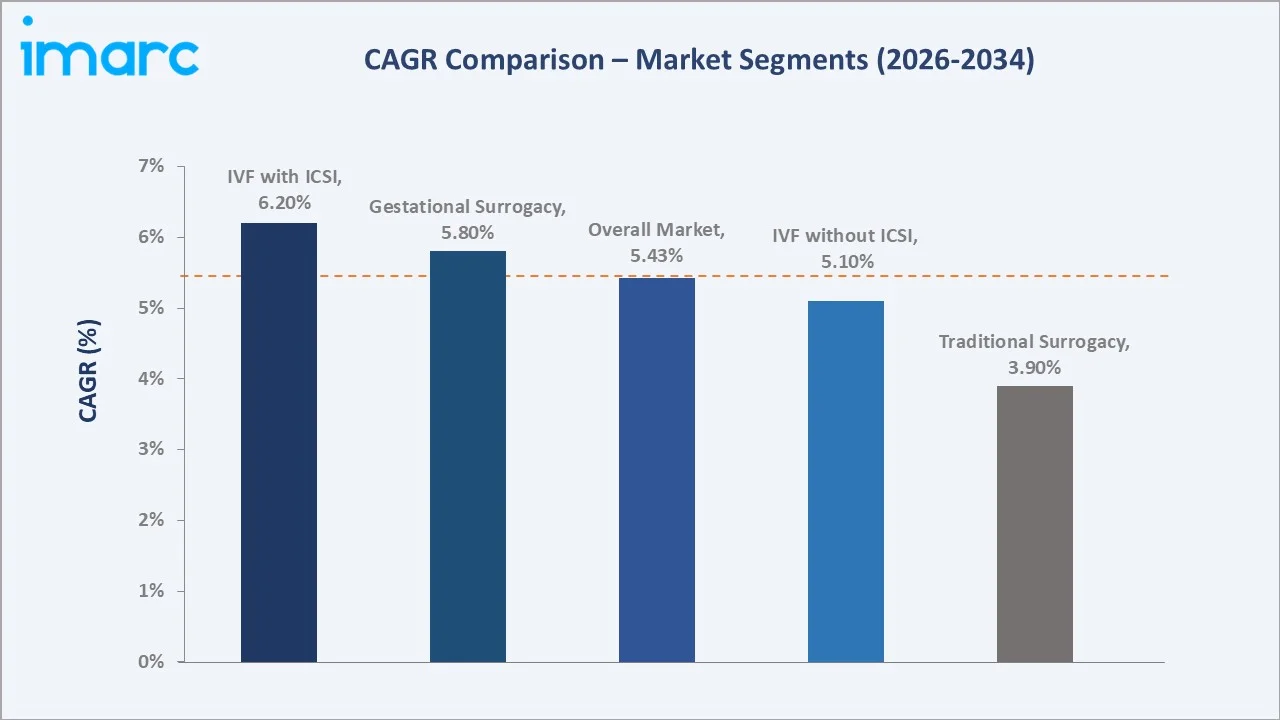

Gestational Surrogacy – ~5.8% CAGR (2026-2034) |

|

Leading Technology |

IVF with ICSI – 49.8% share (2025) |

|

Fastest Growing Technology |

IVF with ICSI – ~6.2% CAGR (2026-2034) |

|

Leading Region |

North America – 41.2% share (2025) |

|

Top Companies |

Kindbody, Pinnacle Fertility, ConceiveAbilities, Surrogacy Is, Golden Surrogacy |

Key Analytical Observations Supporting the Above Data:

- Gestational Surrogacy at 78.6% (2025) reflects the medical and legal preference for IVF-based gestational arrangements over traditional surrogacy. In gestational surrogacy, the surrogate is not genetically related to the child, reducing legal risk and emotional complexity. Most jurisdictions that have legalized surrogacy, including the US, UK, Canada, and Greece, explicitly regulate or prefer gestational arrangements.

- IVF with ICSI at 49.8% (2025) reflects its clinical superiority in fertilization success, particularly for male-factor infertility cases that represent 30–50% of infertility diagnoses in intended parent couples. ICSI’s single-sperm injection technique achieves fertilization rates of 70–80% versus 50–60% for conventional IVF, making it the preferred technology for surrogacy cycles where embryo quality is critical.

- North America at 41.2% (2025) is anchored by California, Nevada, and Washington’s fertility-friendly legal frameworks that provide enforceable pre-birth orders recognizing intended parents as legal parents before birth. The US surrogacy industry is a mature ecosystem of fertility clinics, surrogacy agencies, reproductive law firms, and mental health counsellors with standardized operational protocols.

- Fertility tourism driving Asia-Pacific's 22.6% share (2025) reflects cross-border demand from European and East Asian intended parents accessing more affordable surrogacy in Georgia, Ukraine, and select markets with favorable frameworks, with Asia-Pacific growing at approximately 7.1% CAGR through 2034.

Surrogacy Market Overview

Surrogacy is an assisted reproductive arrangement in which a woman (the surrogate) carries and delivers a child on behalf of another individual or couple (the intended parents). Two primary forms exist: gestational surrogacy, where the surrogate has no genetic connection to the child (embryo created via IVF from intended parents' or donor gametes), and traditional surrogacy, where the surrogate is also the genetic mother (inseminated with intended father's or donor sperm via IUI or IVF).

The regulatory and ethical landscape varies significantly across regions. The US maintains the most permissive and commercially developed surrogacy framework, while the UK allows only altruistic surrogacy without agency fees. Canada permits altruistic surrogacy with legal expenses reimbursement. Key European destinations including Greece, Georgia, and Ukraine offer internationally accessible gestational surrogacy with legal protections. India banned commercial surrogacy for international intended parents in 2022.

Market Dynamics

To evaluate market opportunities, Request Sample

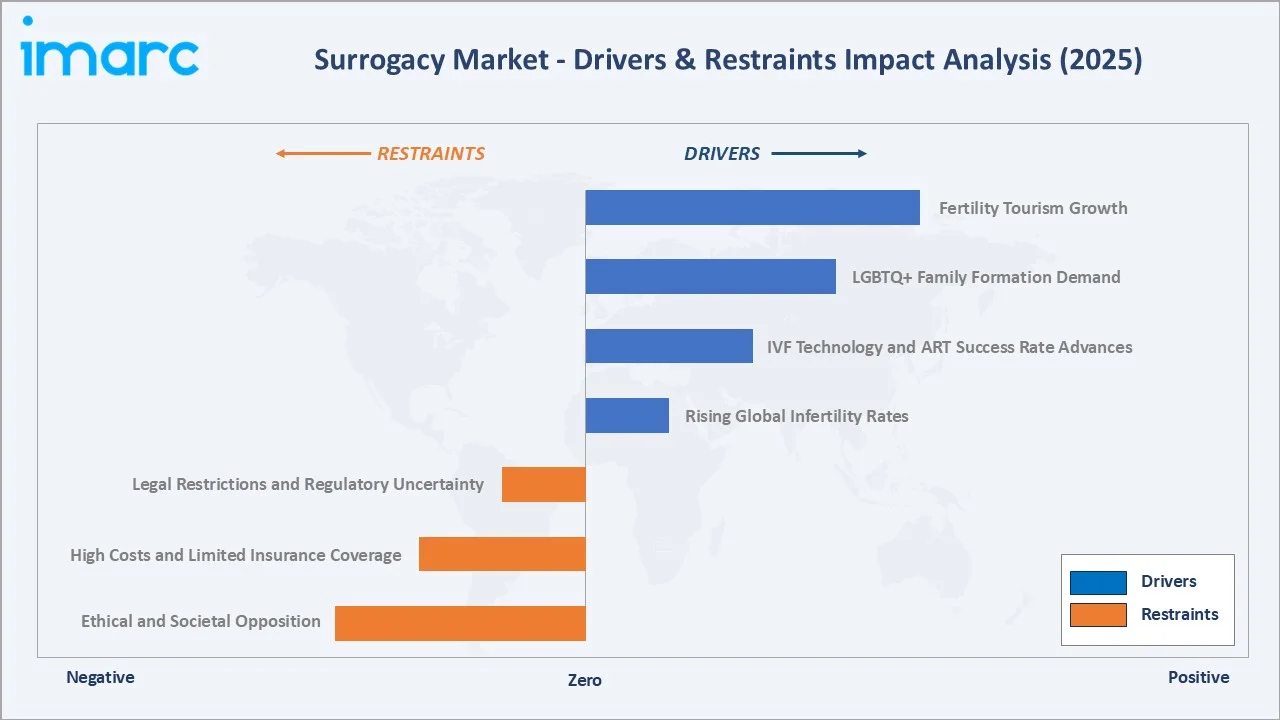

Market Drivers

- Rising Global Infertility Rates: The WHO estimates that approximately 17.5% of the adult global population, around 1 in 6 individuals, experience infertility. Surrogacy is increasingly positioned as the definitive solution for women with uterine conditions (Mayer-Rokitansky-Kuster-Hauser syndrome, Asherman syndrome, and hysterectomy) and recurrent pregnancy loss.

- IVF Technology and ART Success Rate Advances: ICSI, blastocyst culture, time-lapse embryo monitoring, and preimplantation genetic testing (PGT) have collectively raised clinical pregnancy rates per IVF transfer cycle. PGT-A (aneuploidy testing) reduces miscarriage risk by half, making gestational surrogacy cycles more predictable and commercially viable.

- LGBTQ+ Family Formation Demand: Growing social acceptance, legalization of same-sex marriage in 39 countries, and expanding LGBTQ+ adoption of parenthood are creating a structurally new demand cohort for gestational surrogacy. In the US, LGBTQ+ couples represent a high number of intended parents in surrogacy arrangements, with this trend growing as fertility benefit coverage in corporate America expands to cover same-sex couples.

- Fertility Tourism Growth: Cross-border surrogacy is expanding as intended parents in restrictive jurisdictions (Germany, France, Italy, Spain) travel to permissive destinations (US, Canada, Georgia, Greece) for surrogacy services. Cost differentials of USD 120,000–USD 200,000+ (US) versus USD 18,000–USD 30,000 (India) are driving cost-sensitive demand toward lower-cost markets with adequate legal frameworks.

Market Restraints

- Legal Restrictions and Regulatory Uncertainty: Surrogacy remains legally prohibited or unregulated in Germany, France, Italy, Spain, China, and much of the Middle East. India's Surrogacy (Regulation) Act, 2021 (effective 2022) banned commercial surrogacy for foreign nationals, significantly restricting a previously major cross-border destination. Varying legal frameworks create compliance complexity for international agencies and fertility clinics.

- High Costs and Limited Insurance Coverage: Commercial gestational surrogacy in the United States costs USD 80,000–150,000 for intended parents, encompassing agency fees, surrogate compensation, legal fees, and IVF cycles. At present, 25 U.S. states and Washington, D.C. mandate private insurance coverage for fertility care, and surrogacy-specific coverage remains limited, creating significant financial barriers for middle-income intended parents.

- Ethical and Societal Opposition: Concerns around commodification of reproduction, exploitation of economically vulnerable surrogate carriers, and the psychological welfare of children born through surrogacy continue to generate policy opposition in several jurisdictions. The Hague Conference on Private International Law has been developing an international surrogacy convention since 2011, reflecting ongoing global uncertainty about the ethical framework for commercial arrangements.

Market Opportunities

- Employer Fertility Benefit Expansion: Kindbody expanded its reproductive care offerings by acquiring Chicago-based surrogacy agency Alternative Reproductive Resources (ARR), bringing gestational surrogacy services in-house through its KindEOS division. According to the Society for Human Resource Management 2025 Employee Benefits Survey, an equal share of employers, accounting for 24%, provide coverage for both IVF procedures and non-IVF infertility treatments.

- AI-Assisted IVF and Digital Care Platforms: AI embryo selection, digital surrogate monitoring platforms, and telemedicine-enabled care coordination are reducing cost and improving success rates in surrogacy cycles. Fertility technology investment and AI tools that reduce the number of IVF cycles needed per successful birth directly lower the cost barrier for intended parents.

Market Challenges

- Surrogate Supply Constraints: The number of qualified women willing to serve as gestational carriers is limited by stringent medical, psychological, and lifestyle screening criteria. Worldwide, approximately 20,000–30,000 surrogate births take place annually, with 4–12 months of matching time.

- Complex Multi-Jurisdictional Legal Compliance: International surrogacy arrangements require compliance across the intended parents’ home country, the country where the surrogate resides, and immigration law regarding the child’s citizenship. Cases of stateless children resulting from surrogacy arrangements in countries with jus sanguinis citizenship laws underscore the legal complexity that deters some intended parents from pursuing international surrogacy.

Emerging Market Trends

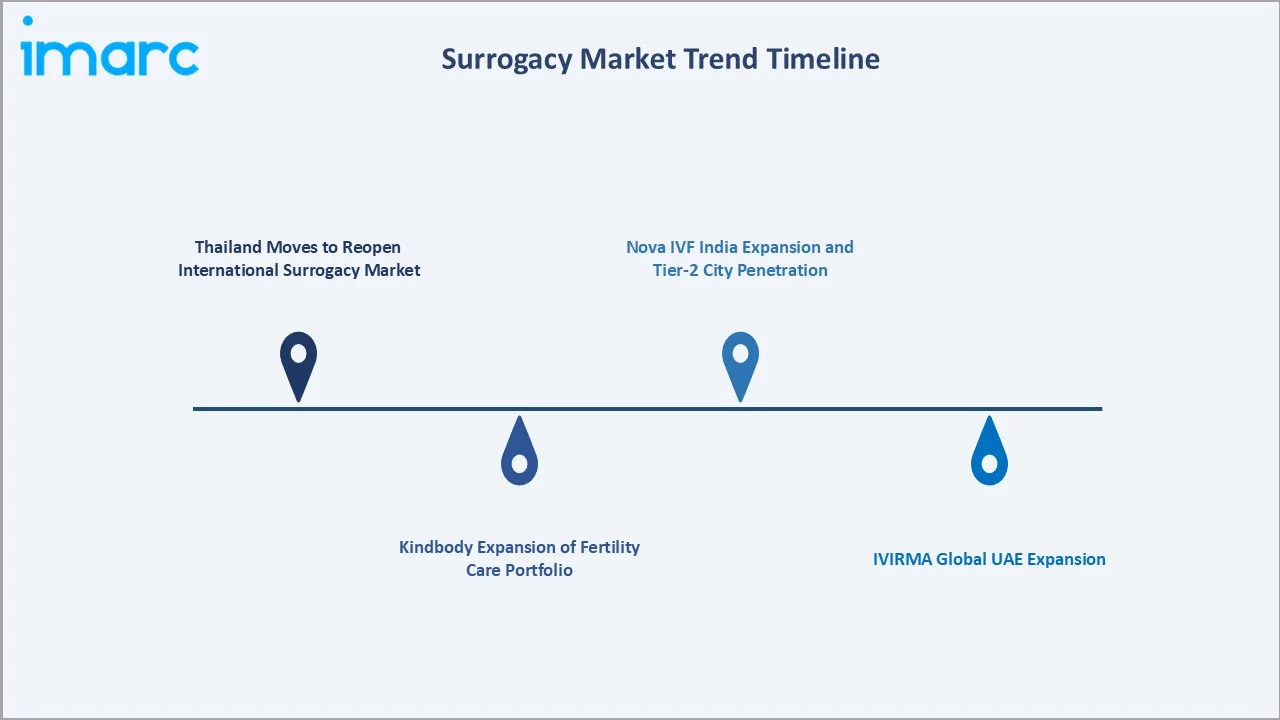

1. Thailand Moves to Reopen International Surrogacy Market

In March 2026, Thailand is preparing to reopen international surrogacy after nearly a decade-long ban, with proposed regulations allowing legally married foreign couples, including same-sex couples, to pursue surrogacy under stricter government oversight. The move aims to revive the country’s assisted reproductive technology sector while strengthening protections against human trafficking and unethical surrogacy practices.

2. Kindbody Expansion of Fertility Care Portfolio

Kindbody expanded its fertility care portfolio by acquiring Chicago-based surrogacy agency Alternative Reproductive Resources (ARR), integrating gestational surrogacy services into its KindEOS platform. The acquisition strengthened Kindbody’s end-to-end reproductive care model by combining fertility treatment, donor services, and surrogacy support under a single network to improve care coordination and patient outcomes.

3. IVIRMA Global UAE Expansion

In July 2025, IVIRMA Global announced the acquisition of ART Fertility Clinics' operations in the UAE and Saudi Arabia, targeting rising demand from Gulf Cooperation Council nationals seeking advanced reproductive care and surrogacy consultation services. This acquisition reflects the broader trend of leading fertility clinic networks moving into the Middle East, where rising per-capita incomes, increasing infertility awareness, and a growing expatriate population are creating new demand for premium IVF and surrogacy services.

4. Nova IVF India Expansion and Tier-2 City Penetration

In July 2025, Nova IVF Fertility opened its 100th fertility center in Jammu, expanding its nationwide network across 63 Indian cities to improve access to ethical and standardized fertility care, particularly in tier 2 and tier 3 regions. While India's Surrogacy (Regulation) Act, 2021 (effective 2022), restricts commercial surrogacy for foreigners, domestic altruistic surrogacy and IVF services represent a high-growth segment, with Nova IVF’s expansion directly addressing the substantial unmet fertility treatment demand in smaller Indian cities.

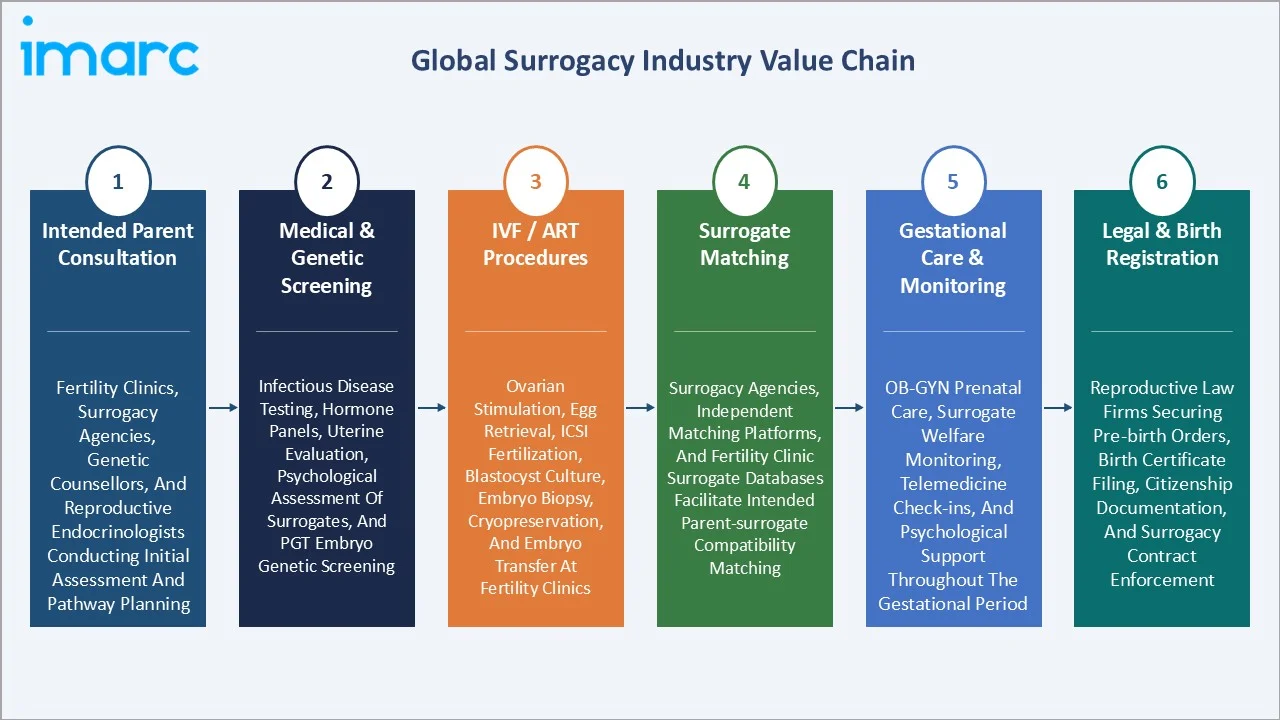

Industry Value Chain Analysis

The surrogacy value chain spans initial intended parent consultation through post-birth legal registration, involving a multi-disciplinary ecosystem of fertility clinics, surrogacy agencies, legal specialists, and psychological counsellors.

|

Stage |

Key Participants / Activities |

|

Intended Parent Consultation |

Fertility clinics, surrogacy agencies, genetic counsellors, and reproductive endocrinologists conducting initial assessment and pathway planning. |

|

Medical & Genetic Screening |

Infectious disease testing, hormone panels, uterine evaluation, psychological assessment of surrogates, and PGT embryo genetic screening |

|

IVF / ART Procedures |

Ovarian stimulation, egg retrieval, ICSI fertilization, blastocyst culture, embryo biopsy, cryopreservation, and embryo transfer at fertility clinics |

|

Surrogate Matching |

Surrogacy agencies, independent matching platforms, and fertility clinic surrogate databases facilitating intended parent-surrogate compatibility matching |

|

Gestational Care & Monitoring |

OB-GYN prenatal care, surrogate welfare monitoring, telemedicine check-ins, and psychological support throughout the gestational period |

|

Legal & Birth Registration |

Reproductive law firms securing pre-birth orders, birth certificate filing, citizenship documentation, and surrogacy contract enforcement |

Technology Landscape in the Surrogacy Industry

IVF with ICSI (Intracytoplasmic Sperm Injection)

IVF with ICSI is the dominant technology at 49.8% market share, particularly relevant in surrogacy given the high incidence of male-factor infertility in intended parent couples. ICSI achieves fertilization rates of 70–80% per mature egg by directly injecting a single sperm into the egg cytoplasm, compared to 50–60% for conventional IVF insemination. The procedure is performed by embryologists using micromanipulation equipment and is standard practice in leading fertility clinics in North America, Europe, and Asia-Pacific.

IVF without ICSI (Conventional IVF)

Conventional IVF at 32.7% market share involves co-incubation of eggs and sperm in culture media, suitable for couples without severe male-factor infertility. Technological advances in culture media formulations, time-lapse embryo imaging systems, and blastocyst culture extending to day 5–6 have improved conventional IVF success rates, making it the preferred option for younger intended parent couples with no significant fertility compromise beyond uterine factors requiring a surrogate.

Intrauterine Insemination

Intrauterine Insemination at 17.5% market share is primarily used in traditional surrogacy arrangements, where processed sperm is directly inserted into the surrogate’s uterus at the time of ovulation. It is the lowest-cost ART procedure and is appropriate where the surrogate’s own eggs are used (traditional surrogacy). Its clinical success rate per cycle is lower (10–20% per cycle) than IVF, but its simplicity, lower cost, and minimal clinical intervention requirements make it applicable in specific traditional surrogacy arrangements.

Preimplantation Genetic Testing and Embryo Selection Technology

PGT-A (aneuploidy screening) and PGT-M (monogenic disease testing) represent advanced embryo selection technologies that are increasingly standard in gestational surrogacy cycles. By identifying chromosomally normal embryos before transfer, PGT-A reduces miscarriage rates by half and improves pregnancy rates per transfer by 10-20 percentage points, directly improving the clinical reliability and commercial predictability of surrogacy arrangements.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Gestational Surrogacy |

78.6% |

2025 |

|

Technology |

IVF with ICSI |

49.8% |

2025 |

|

Service Provider |

🔒 |

🔒 |

2025 |

|

Region |

North America |

41.2% |

2025 |

By Type

Gestational surrogacy dominates the type segment with a 78.6% share in 2025. In gestational surrogacy, the surrogate carries an embryo created from the intended parents’ own gametes or donor eggs/sperm via IVF, with no genetic relationship between the surrogate and the child. This distinction eliminates the most complex legal and emotional risks associated with traditional surrogacy.

To access detailed market analysis, Request Sample

Traditional surrogacy at 21.4% represents arrangements where the surrogate is also the genetic mother, with insemination achieved via IUI or IVF using intended father’s or donor sperm. While legally simpler to execute medically, traditional surrogacy creates parental rights complications requiring additional legal steps in most jurisdictions.

By Technology

IVF with ICSI leads the technology segment at 49.8%, reflecting the high proportion of intended parent couples presenting with male-factor infertility or age-related egg quality issues requiring microinjection techniques for reliable fertilization. ICSI's higher fertilization success rate, combined with blastocyst culture and PGT-A embryo selection, creates the most clinically reliable pathway for gestational surrogacy cycles at leading fertility centers.

IVF without ICSI at 32.7% represents conventional IVF cycles used where sperm quality is adequate for natural fertilization. Intrauterine Insemination at 17.5% is primarily deployed in traditional surrogacy arrangements or in cases where cervical or mild male-factor infertility is the primary diagnosis. IVF with ICSI is the fastest-growing technology segment at ~6.2% CAGR, driven by its adoption in LGBTQ+ male intended parent cycles and single-father-by-choice arrangements.

Regional Market Insights

North America’s leadership at 41.2% in 2025 reflects the US’ position as the world’s most developed and commercially active surrogacy market. Multiple US states provide comprehensive legal frameworks, including pre-birth orders, gestational carrier agreements, and parentage establishment that protect all parties, making the US the default destination for international intended parents.

Europe at 24.8% is a diverse market with highly heterogeneous national policies. Greece, as the first European country to legalize altruistic surrogacy for foreigners, has emerged as the preferred destination for European intended parents unable to pursue surrogacy domestically. Ukraine, historically a major commercial surrogacy destination, has seen market disruption from geopolitical developments, accelerating demand diversification toward Georgia and Portugal.

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

41.2% |

Advanced fertility clinic infrastructure, employer fertility benefit expansion, and high LGBTQ+ family-building demand |

|

Europe |

24.8% |

Greece and Ukraine as accessible surrogacy destinations; UK Law Commission reform discussions; growing cross-border demand from Germany, France, and Italy |

|

Asia-Pacific |

22.6% |

Expanding fertility tourism in Georgia and select markets; domestic IVF growth in India and Australia; rising infertility awareness in Japan, South Korea, and China. |

|

Latin America |

6.4% |

Mexico and Colombia as emerging destinations for affordable cross-border surrogacy; growing domestic demand from rising middle-class fertility awareness |

|

Middle East & Africa |

5.0% |

UAE and Israel emerging as regional fertility hubs; Israel's 2021 LGBTQ+ surrogacy ruling expanding the domestic addressable market |

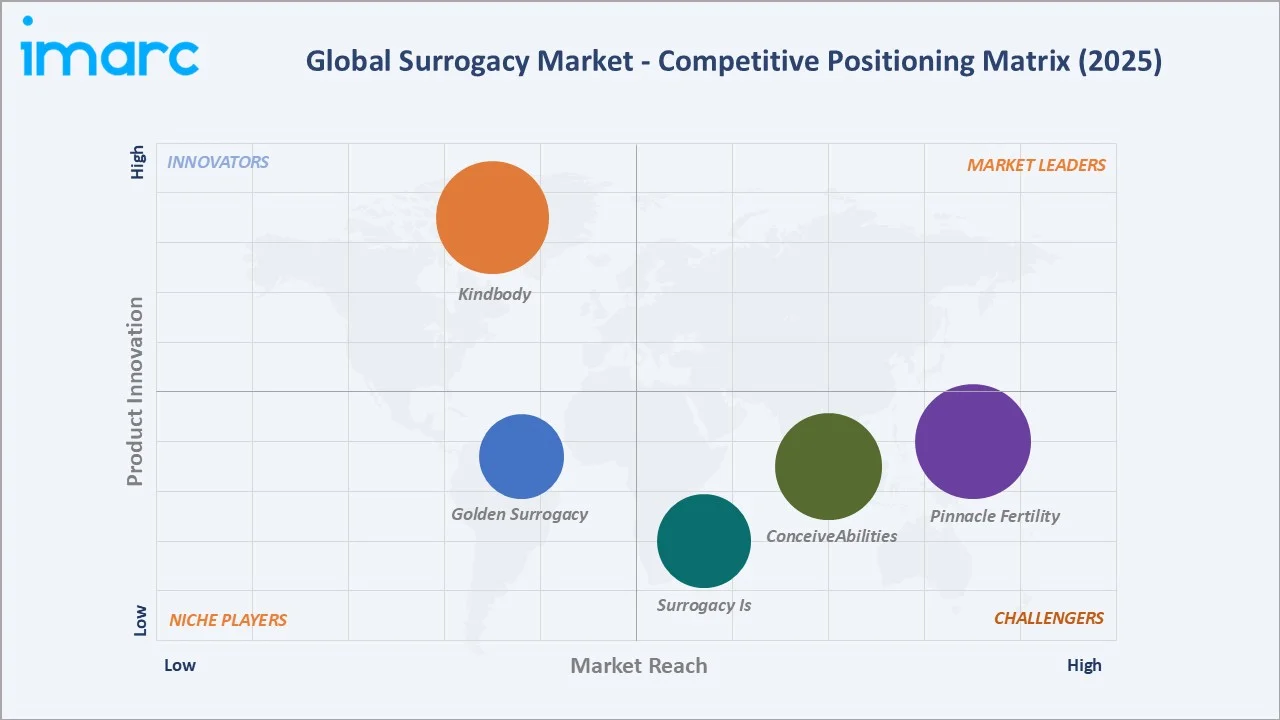

Competitive Landscape

The global surrogacy market is fragmented, with no single entity commanding more than 10–15% of global market revenue. The competitive landscape encompasses fertility clinic networks, dedicated surrogacy agencies, and integrated fertility service providers that combine clinical IVF services with agency-style surrogate matching and legal coordination.

|

Company Name |

Brand/Program |

Market Position |

Core Strength |

|

Kindbody |

KindEOS surrogacy program |

Innovator |

Tech-enabled patient experience; LGBTQ+ inclusive care; Alternative Reproductive Resources acquisition |

|

Pinnacle Fertility |

Pinnacle Surrogacy |

Strong Challenger |

Comprehensive agency services; international expansion; LGBTQ+ services |

|

ConceiveAbilities |

ConceiveAbilities, Surrogacy Advocate Program |

Strong Challenger |

LGBTQ+ and same-sex family advocacy; multiple US locations |

|

Surrogacy Is |

Surrogacy Is |

Challenger |

Surrogate-first advocacy model; referral platform |

|

Golden Surrogacy |

Golden Surrogacy |

Niche Player |

Illinois-based surrogacy agency; 99% surrogate clinic approval rate; strong LGBTQ+ focus |

The market is also witnessing rising investments in AI-enabled embryo selection, personalized fertility care, and cross-border surrogacy services, while evolving regulations in countries such as the US and Thailand continue to reshape competitive dynamics and international patient flows.

Key Company Profiles

Kindbody

Kindbody is a technology-enabled fertility and family-building company that integrates fertility clinic services with digital health platforms and a consumer-friendly brand experience.

- Product Portfolio: KindEOS surrogacy program

- Recent Developments: In February 2026, Kindbody launched a next-generation fertility platform integrating AI-driven intelligence, advanced clinical care, and virtual support services to improve reproductive health outcomes while lowering costs for employers and patients.

- Strategic Focus: Technology platform development for patient navigation; LGBTQ+ market leadership; surrogacy-to-birth integrated service model via ARR.

Pinnacle Fertility

Pinnacle Fertility provides non-clinical administrative and operational support to an expanding network of independent fertility clinics and reproductive specialists, currently spanning multiple fertility clinics in the US led by renowned reproductive specialists, with its own in-house surrogacy programs.

- Product Portfolio: Pinnacle Surrogacy (an in-house surrogate matching and case management program)

- Recent Developments: In May 2026, Pinnacle Fertility joined its network Genesis Fertility to expand its reproductive care presence across New York. As part of the deal, Genesis Fertility was rebranded as Pinnacle Fertility New York, strengthening Pinnacle’s nationwide fertility clinic and embryology lab network while enhancing access to integrated fertility and surrogacy services.

- Strategic Focus: LGBTQ+ inclusive family-building services across all clinic locations; technology partnerships with TMRW Life Sciences for cryogenic embryo storage management; insurance navigation and employer benefits channel development through PatientFi and financial counselling integration.

Market Concentration Analysis

The global surrogacy market is highly fragmented. No single entity captures more than 10–15% of the global market, and the competitive landscape comprises hundreds of regional fertility clinics, specialized surrogacy agencies, and multi-specialty reproductive health companies. Consolidation is occurring primarily through fertility clinic network M&A as private equity-backed roll-up strategies seek to capture the high-value IVF and surrogacy clinical segment.

The agency segment, comprising ConceiveAbilities and dozens of regional operators, remains independently fragmented, as the personalized, high-touch nature of surrogacy matching and support creates barriers to commodification. The most significant consolidation trend is fertility clinics acquiring or integrating agency capabilities, creating vertically integrated entities that capture margin across the entire surrogacy value chain.

Investment & Growth Opportunities

Fastest Growing Segments

IVF with ICSI (~6.2% CAGR), Gestational Surrogacy (~5.8% CAGR), and Asia-Pacific region (~7.1% CAGR) represent the highest-growth investment vectors through 2034. The Asia-Pacific opportunity, anchored by Georgia’s and select emerging markets’ legal frameworks, represents the largest geographic growth increment in the forecast period as European intended parents diversify destination options.

Employer Fertility Benefits as a Distribution Channel

Corporate America’s expanding fertility benefit coverage creates an estimated USD 40–60 Billion total addressable market for fertility services including surrogacy in the US alone by 2030. Technology-enabled benefit platforms are the distribution gateway, with surrogacy coverage representing the highest-value benefit tier. This channel bypasses traditional direct-to-consumer marketing costs and improves intended parent ability-to-pay.

Venture and Institutional Investment Trends

- Global fertility technology investment exceeded USD 1.5 Billion in 2024, including AI embryo selection tools, digital patient platforms, and clinic networks, all of which directly support the surrogacy market infrastructure.

- Private equity roll-up strategies targeting IVF clinic networks in the US, Australia, and Europe are creating larger, better-capitalized entities capable of investing in surrogacy program development, digital care platforms, and international market entry.

Future Market Outlook (2026-2034)

The global surrogacy market is positioned for steady, sustained growth through 2034. From USD 204.6 Million in 2025, the market is projected to reach USD 329.2 Million by 2034 at a CAGR of 5.43%. This trajectory reflects a market in which structural demand (infertility, LGBTQ+ family-building, single parenthood) is growing faster than legal access is expanding, maintaining a supply-constrained market dynamic that sustains pricing power and service quality in established markets like the United States.

The 2026–2034 period will be defined by three structural shifts: the expansion of legally permissive surrogacy destinations in Europe and Asia-Pacific; the integration of employer fertility benefit coverage as a mainstream distribution channel; and the improvement of IVF success rates through AI and genomic technologies that reduce cycle numbers and associated costs. These shifts will collectively expand the addressable market while improving service accessibility for intended parents across income brackets.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 80 industry participants in 2024–2025, including fertility clinic directors, surrogacy agency coordinators, reproductive lawyers, intended parents, gestational surrogates, and healthcare policy specialists across North America, Europe, and Asia-Pacific.

Secondary Research

Secondary research encompassed company annual reports, CDC ART Success Rates data, Society for Assisted Reproductive Technology (SART) national cycle data, WHO reproductive health publications, and industry publications including RESOLVE (National Infertility Association) and Fertility and Sterility journal.

Forecasting Models

Market size estimations used top-down and bottom-up modelling, incorporating global IVF cycle volumes, surrogacy arrangement completion rates, average revenue per arrangement, and regional legal access expansion projections. A base-case CAGR of 5.43% reflects conservative assumptions about legal framework pace of evolution and excludes scenarios of major regulatory expansion.

Surrogacy Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Gestational Surrogacy, Traditional Surrogacy |

| Technologies Covered | IVF with ICSI, IVF without ICSI, Intrauterine Insemination |

| Service Providers Covered | Hospitals, Fertility Clinics, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Kindbody, Pinnacle Fertility, ConceiveAbilities, Surrogacy Is, Golden Surrogacy, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the surrogacy market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global surrogacy market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the surrogacy industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Surrogacy Market Report

The global surrogacy market reached USD 204.6 Million in 2025 and is projected to reach USD 329.2 Million by 2034.

The market is expected to grow at a CAGR of 5.43% during the forecast period of 2026-2034.

Gestational surrogacy dominates with a 78.6% market share in 2025, reflecting its legal and clinical advantages over traditional surrogacy, including the absence of a genetic relationship between surrogate and child.

IVF with ICSI is the largest technology with 49.8% share in 2025, driven by its superior fertilization success rates, growing use in LGBTQ+ male-intended-parent cycles, and integration with PGT embryo selection.

North America leads with a 41.2% regional share in 2025, anchored by US state-level legal frameworks that provide comprehensive legal protection for all surrogacy parties and the world's most developed fertility clinic and agency ecosystem.

Key players include Kindbody, Pinnacle Fertility, ConceiveAbilities, Surrogacy Is, and Golden Surrogacy.

Primary drivers include rising global infertility rates, IVF technology advances improving success rates, LGBTQ+ family formation demand, fertility tourism growth, and expanding employer fertility benefit coverage.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)