Synthetic Rubber Market Size, Share, Trends and Forecast by Type, Form, Application, and Region, 2026-2034

Global Synthetic Rubber Market Size, Share, Trends & Forecast (2026-2034)

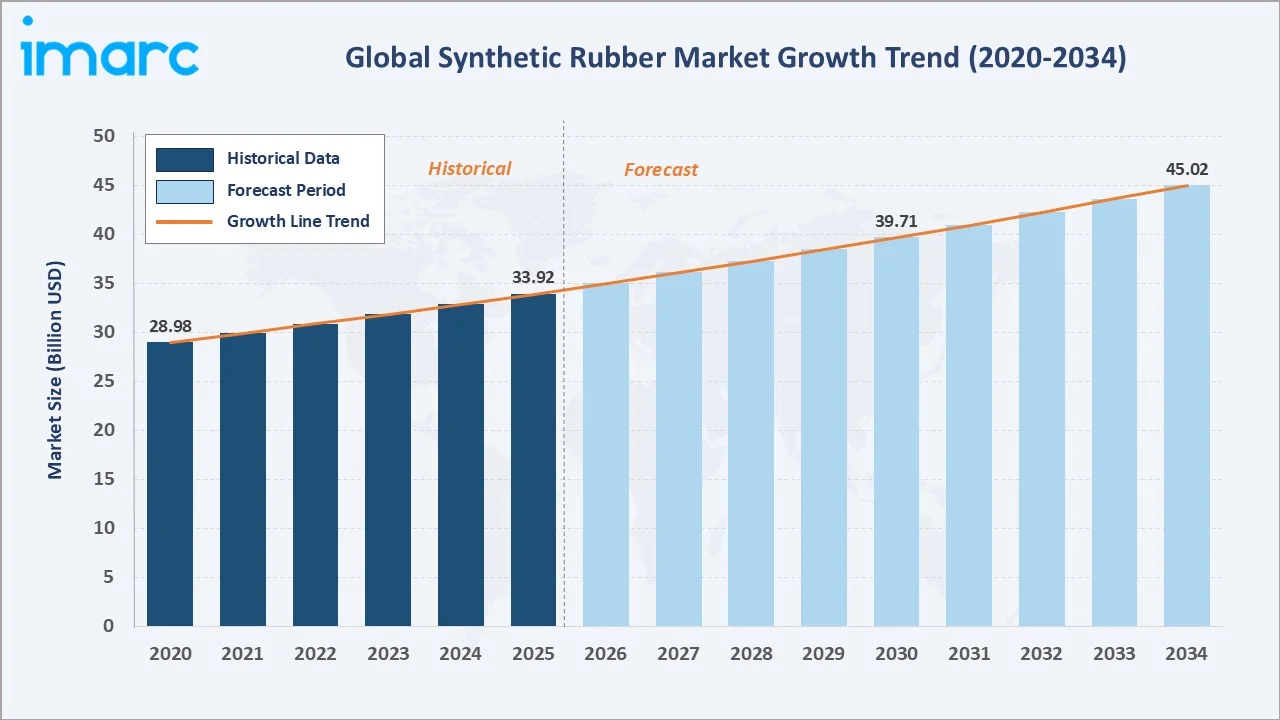

The global synthetic rubber market size was valued at USD 33.92 Billion in 2025 and is projected to reach USD 45.02 Billion by 2034, exhibiting a CAGR of 3.2% during the forecast period 2026-2034. Expanding automotive production, accelerating electric vehicle adoption, rising tire replacement demand, and growing specialty elastomer consumption are driving the synthetic rubber market growth.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 33.92 Billion |

|

Forecast Market Size (2034) |

USD 45.02 Billion |

|

CAGR (2026-2034) |

3.2% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

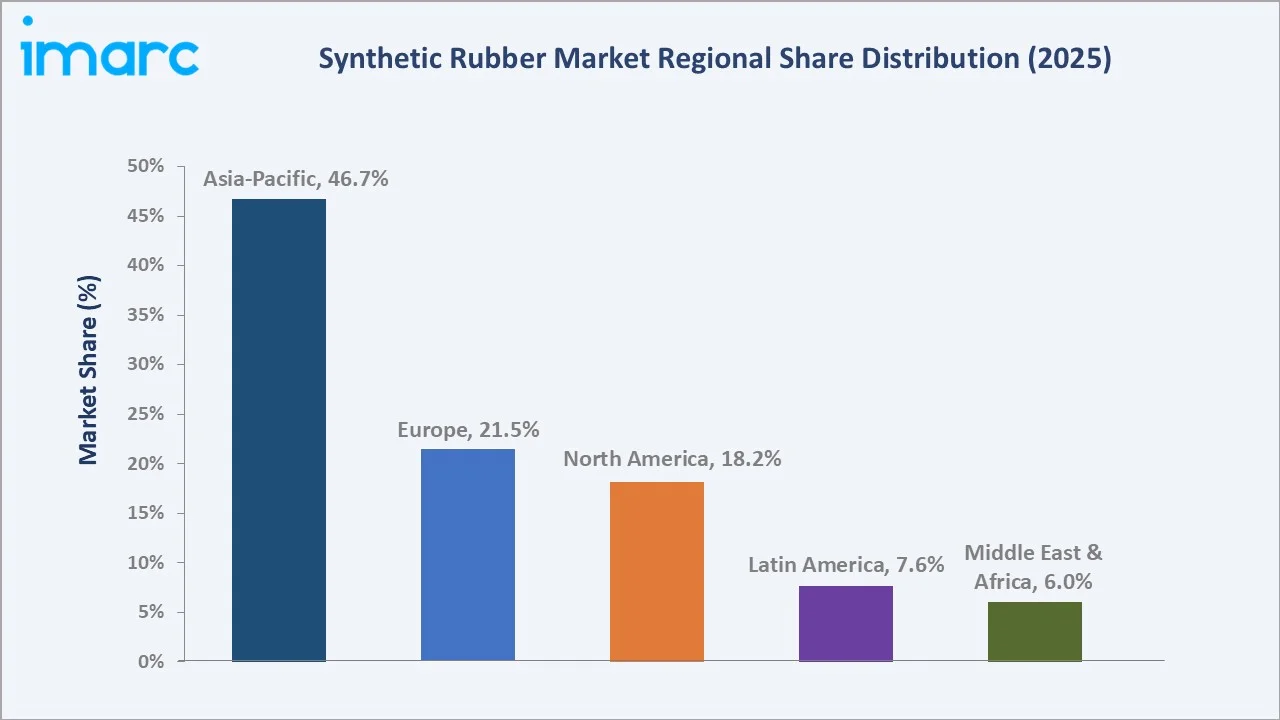

Largest Region |

Asia-Pacific (46.7% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific (~3.8% CAGR) |

|

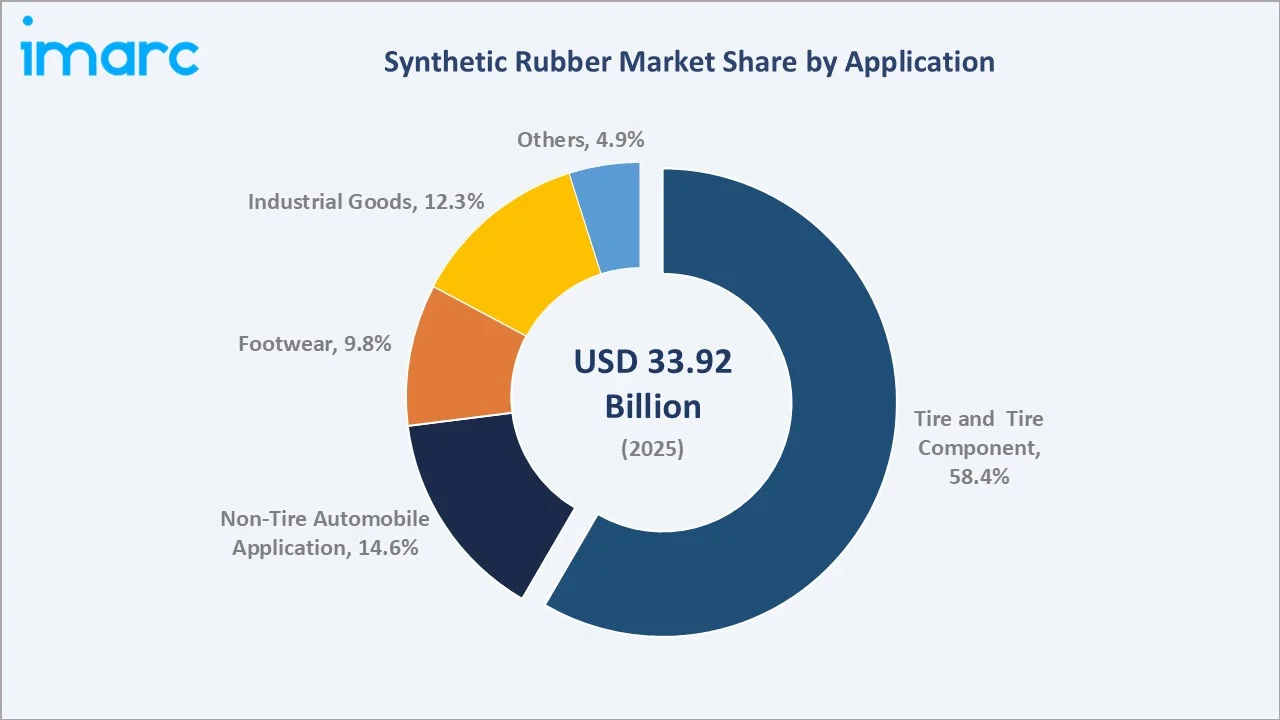

Leading Application |

Tire & Tire Component (58.4%, 2025) |

|

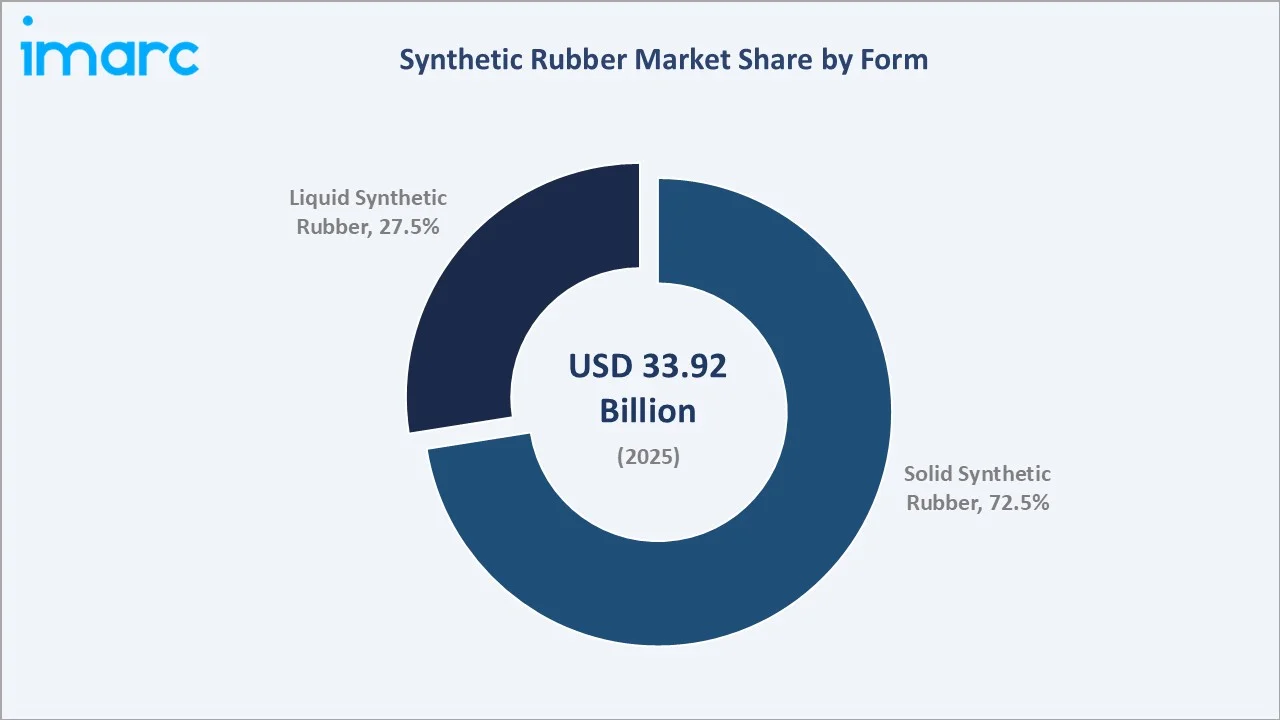

Leading Form |

Solid Synthetic Rubber (72.5%, 2025) |

The global synthetic rubber market growth trajectory from 2020 through 2034 reflects steady expansion, shifting from historical momentum anchored at USD 28.98 Billion in 2020 to a forecast USD 45.02 Billion in 2034. Demand is powered by automotive production, tire replacement cycles, and rising specialty grade consumption across industrial sectors.

To get more information on this market, Request Sample

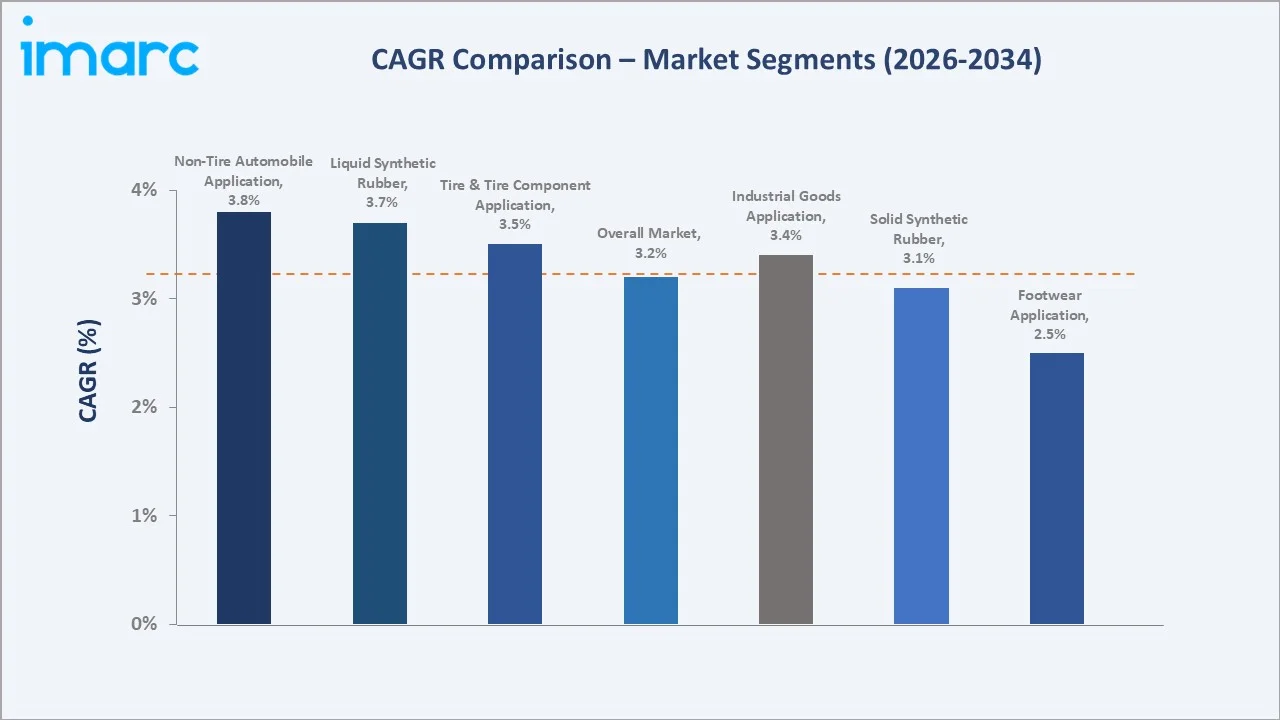

Segment-level CAGR comparisons highlight non-tire automotive and liquid synthetic rubber as the fastest-growing sub-categories within the global synthetic rubber market forecast through 2034, outpacing mature tire and solid rubber segments.

Executive Summary

The global synthetic rubber market is undergoing structural transformation driven by automotive electrification, sustainable tire technology, and specialty elastomer innovation. Valued at USD 33.92 Billion in 2025, the market is forecast to reach USD 45.02 Billion by 2034 at a CAGR of 3.2%. Historical growth from USD 28.98 Billion in 2020 reflects resilient demand despite raw material volatility.

Tire and tire components command 58.4% share in 2025, underpinned by global vehicle production and replacement tire cycles. Solid synthetic rubber represents 72.5% of global form-based demand, while liquid synthetic rubber is the faster-growing category at an estimated CAGR of 3.7% through 2030. Non-tire automotive applications are gaining traction as EV component demand rises.

Asia-Pacific leads with 46.7% global revenue share in 2025, driven by China, India, Japan, and South Korea. Europe holds 21.5% and North America 18.2%. The synthetic rubber market outlook remains positive as premiumization, sustainability-led bio-based elastomers, and circular economy adoption converge across all major geographies through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Application |

Tire & Tire Component – 58.4% share (2025) |

|

Second Application |

Non-Tire Automobile – 14.6% share (2025) |

|

Largest Form |

Solid Synthetic Rubber – 72.5% share (2025) |

|

Fastest Growing Form |

Liquid Synthetic Rubber – ~3.7% CAGR (2025-2030) |

|

Leading Region |

Asia-Pacific – 46.7% revenue share (2025) |

|

Top Companies |

ARLANXEO, Exxon Mobil Corporation, China Petrochemical Corporation, LG CHEM., Asahi Kasei Corporation, ZEON CORPORATION, TSRC, Denka Company Limited, and Apcotex |

|

EV Tire Elastomer Demand |

Rising penetration of EVs in Asia-Pacific and Europe boosting demand |

Key Analytical Observations Supporting the Above Data:

- Tire and tire components' 58.4% dominance in 2025 reflects record global vehicle production of 96.4 million units in 2025and rising replacement tire cycles, particularly in Asia-Pacific and North America.

- Non-tire automotive applications' 14.6% share is driven by EPDM rubber use in weather-sealing, hoses, and NVH components, with EV adoption reaching 17 million units sold globally in 2024 per IEA data.

- Solid synthetic rubber's 72.5% majority is underpinned by styrene butadiene rubber (SBR) and polybutadiene rubber (BR), which collectively serve a significant share of global tire elastomer demand.

- Asia-Pacific's 46.7% global dominance reflects China's role as the world's largest tire producer and China tire output to exceed 840 million units in 2026.

Global Synthetic Rubber Market Overview

Synthetic rubber comprises man-made elastomers produced through polymerization of petroleum-based monomers, serving as a critical substitute for natural rubber across tire, automotive, footwear, and industrial applications. The global market spans multiple product grades including styrene butadiene rubber, polybutadiene, EPDM, polyisoprene, and butyl rubber, each engineered for specific performance characteristics.

The industry operates at the convergence of petrochemical feedstock supply, automotive OEM demand, and sustainability mandates. Growth is supported by macroeconomic drivers including rising vehicle parc globally, electric mobility transition, and capacity expansions across Asia-Pacific. Simultaneously, the market is undergoing a structural shift toward bio-based elastomers, recycled content integration, and specialty high-performance grades through 2034.

Market Dynamics

To evaluate market opportunities, Request Sample

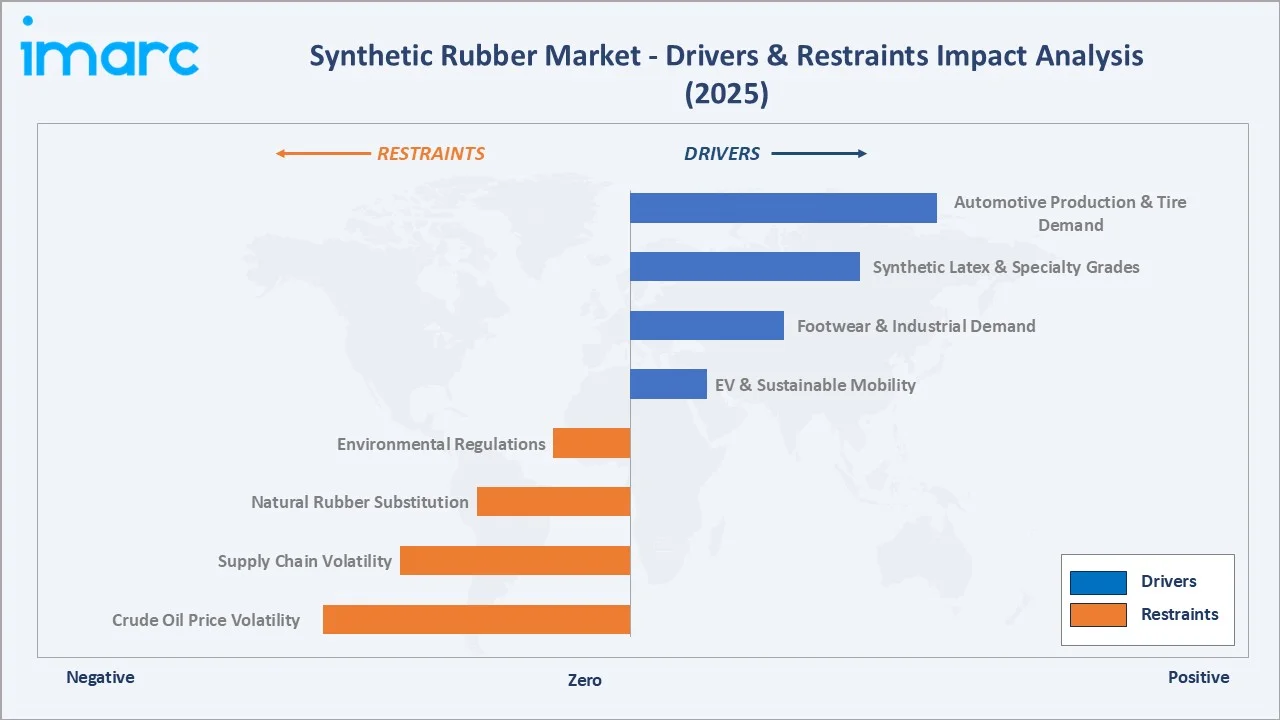

Market Drivers

- Automotive Production and Tire Demand: Global automotive production reached approximately 96.4 million units in 2025 per OICA data, directly driving tire and component elastomer consumption. Replacement tire cycles across mature markets sustain volume demand, while rising vehicle parc in Asia-Pacific fuels incremental synthetic rubber offtake.

- EV and Sustainable Mobility Transition: Electric vehicle sales crossed 17 million units globally in 2024 according to the International Energy Agency. EVs require specialized low-rolling-resistance tires with silica-reinforced SBR compounds, creating premium demand for high-performance elastomer grades through 2034.

- Footwear and Industrial Goods Demand: Footwear manufacturing across Vietnam, Indonesia, and India continues to expand, driving consumption of SBR and polybutadiene soles. Industrial goods including conveyor belts, hoses, and seals represent a stable share, supported by global infrastructure spending.

- Specialty Grades and Synthetic Latex: Medical gloves, adhesives, and specialty coatings are driving liquid synthetic rubber growth. Global synthetic latex demand expanded from 2022 through 2024, with capacity additions in Malaysia, Thailand, and China supporting forecast demand.

Market Restraints

- Crude Oil Price Volatility: Butadiene, styrene, and isoprene feedstock prices track crude oil and naphtha, exposing producers to raw material cost swings that directly compress margins, particularly for commodity-grade SBR and polybutadiene.

- Natural Rubber Substitution: Natural rubber remains cost-competitive in tire applications, with global natural rubber production at 14.89 million tons in 2025, limiting synthetic rubber pricing power in price-sensitive tire and footwear categories.

- Environmental Regulations: Tightening VOC emissions and petrochemical compliance standards across Europe and North America increase production complexity and capital expenditure for legacy plants unable to meet evolving sustainability benchmarks.

Market Opportunities

- Bio-Based and Recycled Elastomers: Bio-butadiene and bio-isoprene commercialization is accelerating, with pilot facilities in Europe and North America targeting scaled capacities through 2028. Devulcanized rubber reclaim programs are expanding in Germany, Japan, and South Korea.

- EV-Specific Tire Grades: Specialty SBR, high-cis polybutadiene, and functionalized elastomers for low-rolling-resistance formulations represent a premium-priced, high-growth category.

- Asia-Pacific Capacity Expansion: Sinopec, Reliance Industries, and LG Chem. have announced new synthetic rubber capacity across China, India, and South Korea through 2027, positioned to capture regional tire and automotive OEM demand growth.

Market Challenges

- Feedstock Supply Chain Fragmentation: Butadiene availability is constrained by ethylene cracker shifts toward lighter feedstocks, particularly in the United States, creating structural tightness that challenges pricing stability for downstream SBR and polybutadiene producers.

- Decarbonization and Scope 3 Pressure: Automotive OEMs including Stellantis, Toyota, and Volkswagen have announced Scope 3 emission reduction targets that cascade procurement pressure onto tire and rubber suppliers to reduce carbon intensity per kilogram of elastomer produced.

- Chinese Capacity Oversupply Risk: Aggressive capacity additions in China since 2022 risk creating regional oversupply, particularly in commodity SBR grades, pressuring export prices across Southeast Asia and global markets.

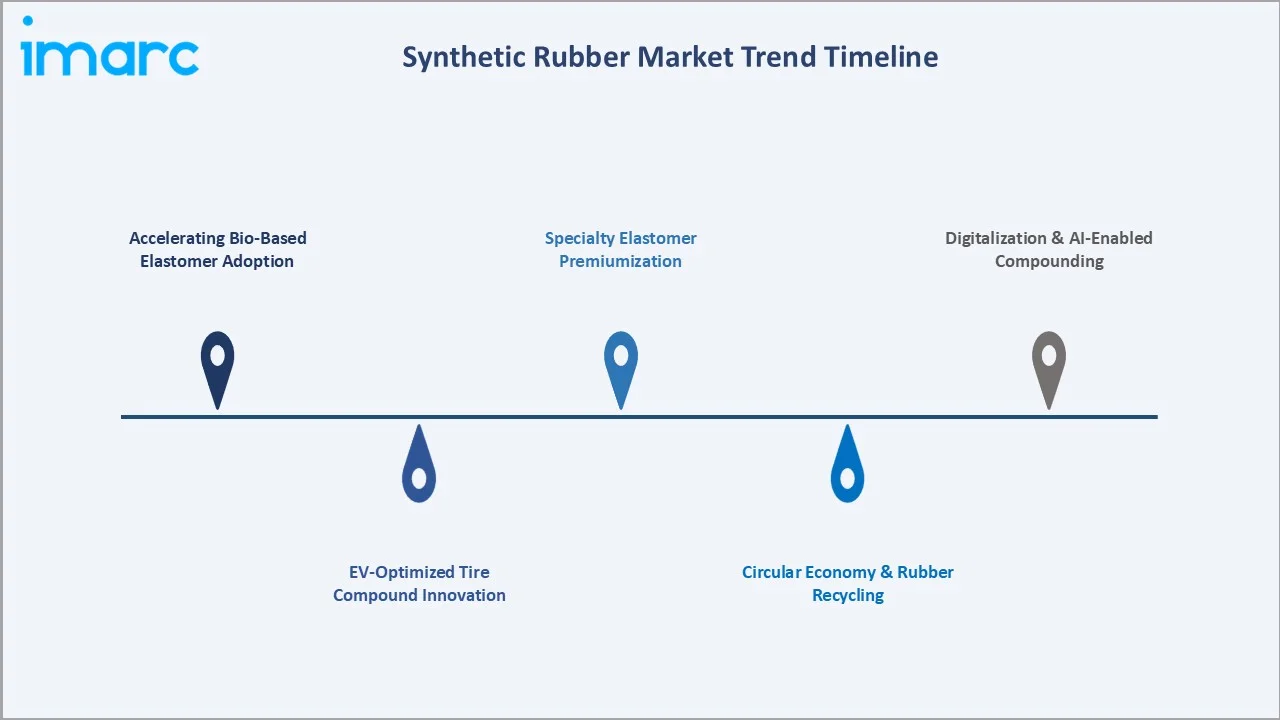

Emerging Market Trends

1. Accelerating Bio-Based Elastomer Adoption

Bio-butadiene and bio-isoprene production is transitioning from pilot to commercial scale, with companies such as Braskem, Genomatica, and Versalis investing in fermentation-based feedstocks. Sustainability-driven procurement mandates from automotive and tire OEMs are accelerating this transition through 2030.

2. EV-Optimized Tire Compound Innovation

Silica-reinforced SBR, functionalized styrene butadiene rubber, and high-cis polybutadiene are emerging as preferred elastomers for EV tire applications. Manufacturers are investing in compound development to deliver lower rolling resistance compared to conventional formulations, directly extending EV range performance.

3. Circular Economy and Rubber Recycling

Devulcanization, pyrolysis, and mechanical reclaim technologies are scaling rapidly, with global reclaimed rubber volumes projected to exceed significant levels by 2030. Regulatory mandates in the European Union and Japan are driving mandatory recycled content requirements in new tire and industrial rubber products.

4. Specialty Elastomer Premiumization

High-performance EPDM, hydrogenated nitrile butadiene rubber (HNBR), and fluoroelastomers command strong price premiums in aerospace, energy, and medical applications. Producers are shifting portfolios toward specialty grades to escape commodity price pressure and capture margin expansion through 2034.

5. Digitalization and AI-Enabled Compounding

Artificial intelligence and machine learning are being deployed across polymer formulation, predictive process control, and quality assurance. Leading producers including ARLANXEO, Exxon Mobil Corporation and material efficiency gains through digital manufacturing investments.

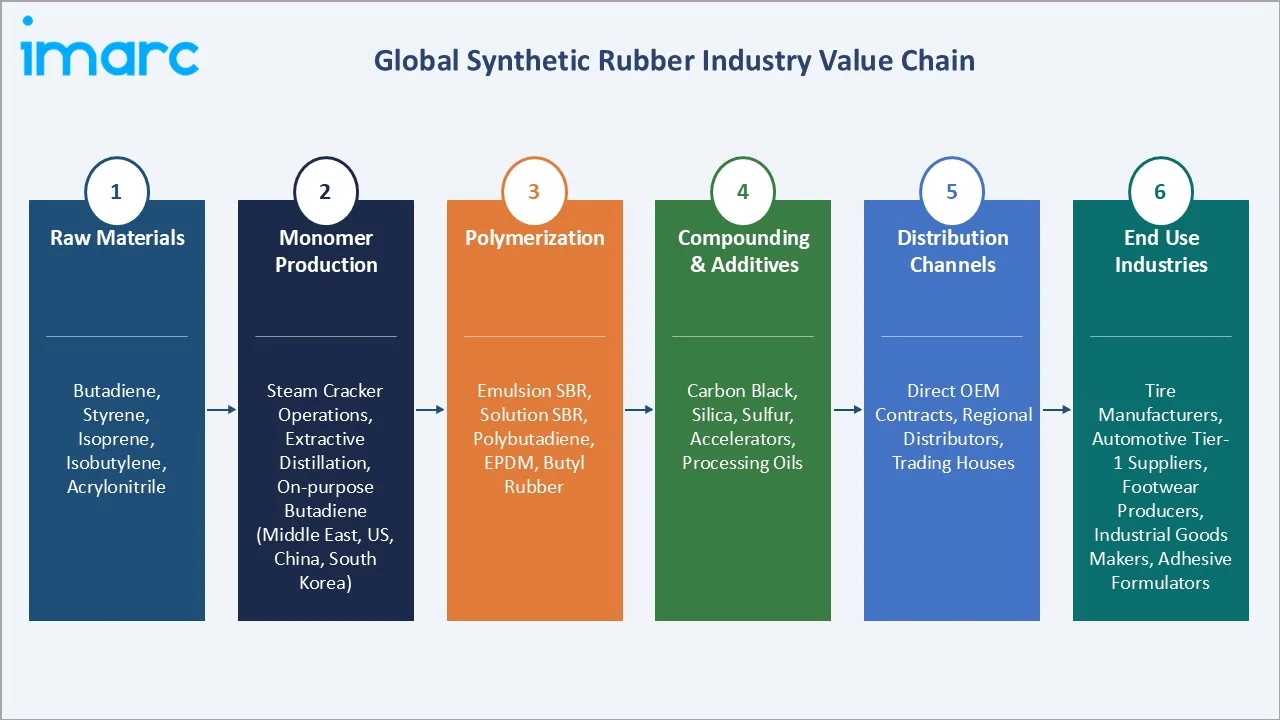

Industry Value Chain Analysis

The global synthetic rubber industry value chain spans six integrated stages from petrochemical feedstock supply through end-user application, with distinct competitive dynamics and margin profiles at each level relevant to the overall synthetic rubber market analysis.

|

Value Chain Stage |

Description |

|

Raw Materials |

Butadiene, styrene, isoprene, isobutylene, acrylonitrile |

|

Monomer Production |

Steam cracker operations, extractive distillation, and on-purpose butadiene technology – concentrated in the Middle East, United States, China, and South Korea |

|

Polymerization |

Emulsion SBR, solution SBR, polybutadiene, EPDM, butyl rubber |

|

Compounding & Additives |

Carbon black, silica, sulfur, accelerators, oils |

|

Distribution Channels |

Direct OEM contracts, regional distributors, and trading houses – tire manufacturers represent ~58% of direct offtake in 2025 |

|

End Use Industries |

Tire manufacturers, automotive Tier-1 suppliers, footwear producers, industrial goods makers, and specialty adhesive formulators |

Polymerization producers hold the highest strategic value by integrating feedstock flexibility with specialty product portfolios. Simultaneously, tire OEMs are back-integrating into rubber compounding to secure supply chain resilience and capture margin through vertical integration strategies.

Technology Landscape in the Synthetic Rubber Industry

Polymerization Technology

Solution polymerization increasingly dominates high-performance SBR and polybutadiene production, offering superior molecular weight control versus traditional emulsion processes. Ziegler-Natta and anionic catalyst systems enable tailored microstructures critical for EV tire compound performance and low-rolling-resistance applications.

Bio-Based Monomer Innovation

Fermentation-based butadiene and isoprene technologies are progressing from laboratory to semi-commercial scale. Genomatica, Braskem, and Versalis have announced strategic partnerships with tire manufacturers to deliver bio-content elastomers at commercial volumes by 2028, supporting carbon-reduction targets across the automotive value chain.

Recycling and Devulcanization

Thermomechanical devulcanization and pyrolysis technologies are scaling globally, enabling rubber reclaim at purity levels suitable for high-performance tire compounds. Leading players including are investing in joint ventures and licensed technology partnerships to secure recycled feedstock streams through 2030.

Silica Compounding and Functionalization

Functionalized SBR compatible with high silica loading is now mainstream for premium tire formulations, delivering rolling resistance reductions versus legacy compounds. Producers are investing in silane coupling agent chemistry and end-group functionalization to differentiate portfolios and capture EV-segment premium pricing.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Type | Styrene Butadiene Rubber | 🔒 |

2025 |

| Form | Solid Synthetic Rubber | 72.5% |

2025 |

| Application | Tire and Tire Component | 58.4% |

2025 |

| Region | Asia-Pacific | 46.7% |

2025 |

By Form

To access detailed market analysis, Request Sample

Solid synthetic rubber is the dominant form-based segment at 72.5% of global revenue in 2025, comprising the majority of tire, automotive, and industrial applications. Styrene butadiene rubber and polybutadiene are the largest sub-categories by volume, produced in bale or crumb form and consumed directly by tire and rubber goods manufacturers globally.

By Application

Tire and Tire Components lead the global synthetic rubber market application with a 58.4% share in 2025. Demand is driven by global vehicle production and accelerating EV tire consumption.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia-Pacific |

46.7% |

China tire production, India auto expansion, Japan specialty grades, Korean chemistry |

|

Europe |

21.5% |

EU sustainability mandates, German automotive OEMs, specialty elastomer leadership |

|

North America |

18.2% |

U.S. light vehicle production, EV tire innovation, shale-advantaged feedstocks |

|

Latin America |

7.6% |

Brazil tire manufacturing, Mexico auto assembly, footwear industry growth |

|

Middle East & Africa |

6.0% |

GCC petrochemical integration |

Asia-Pacific commands 46.7% of global revenue share in 2025, making it the single largest regional market. China represents the most important national market, combining massive tire manufacturing capacity and rapidly expanding EV production.

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

Exxon Mobil Corporation |

Exxon Butyl, Exxon Bromobutyl, Vistalon EPDM |

Leader |

Its primary manufacturing hubs for rubber are Baton Rouge |

|

China Petrochemical Corporation |

S-SBR |

Leader |

Integrated tire-chemical value chain |

|

ARLANXEO |

Buna, Krynac, Therban, Keltan, Perbunan |

Leader |

Specialty elastomer portfolio, EV tire grades |

|

LG Chem. |

Lutex (NBL), LETZero |

Challenger |

Global NBL leadership for medical gloves; high-performance SSBR for EV tires; bio-based rubber under LETZero |

|

Asahi Kasei Corporation |

Asadene, Asaprene, Tufdene |

Challenger |

Japanese specialty elastomers, premium grades |

|

ZEON CORPORATION |

Nipol, Zetpol |

Challenger |

Hydrogenated NBR, specialty chemistry |

|

TSRC |

TAIPOL, VECTOR |

Emerging |

Taiwan specialty SBR, Southeast Asia |

|

Denka Company Limited |

Denka Chloroprene |

Emerging |

Chloroprene rubber leadership, Japan |

|

Apcotex |

NBR latex, nitrile latex, SBR latex |

Emerging |

India latex specialty, synthetic nitrile |

The global synthetic rubber market competitive landscape is moderately fragmented, with global petrochemical majors competing alongside regional specialists and tire-integrated producers.

Key Company Profiles

China Petrochemical Corporation (Sinopec)

China Petrochemical Corporation, commonly known as Sinopec, is one of the world's largest integrated petrochemical producers, headquartered in Beijing, China. Founded in 1998, Sinopec operates across upstream, refining, petrochemical, and marketing sectors with significant synthetic rubber production capacity.

- Product & Platform Portfolio: Sinopec's synthetic rubber portfolio includes styrene butadiene rubber, polybutadiene rubber, EPDM, and butyl rubber.

- Recent Developments: In 2025, Sinopec has initiated early-stage construction activities for its new Tianjin rubber plant, issuing the first tender for foundation works as part of its green high-end synthetic rubber project in China. The facility is designed to produce solution styrene butadiene rubber (SSBR) and butadiene rubber, strengthening Sinopec’s downstream presence in high-performance tire and automotive elastomer markets.

- Strategic Focus: Sinopec's strategy centers on vertical integration with refining operations, capacity expansion in specialty elastomers, and deeper engagement with global tire OEMs, particularly Chinese tire majors expanding international market share.

Exxon Mobil Corporation

Exxon Mobil Corporation is one of the largest publicly traded integrated energy companies in the world, headquartered in Spring, Texas. Through its Chemical division, ExxonMobil is a leading producer of butyl rubber and specialty elastomers serving tire, pharmaceutical, and industrial markets.

- Product & Platform Portfolio: ExxonMobil's portfolio includes Vistalon EPDM, Exxon Butyl and halogenated butyl rubbers, and EscorezTM tackifying resins, serving tire innerliners, pharmaceutical stoppers, and automotive weather-seal applications.

- Recent Developments: In 2026, ExxonMobil is expanding its Vistalon EPDM rubber business through new production growth plans and downstream supply chain strengthening, reinforcing its position in the global synthetic rubber market.

- Strategic Focus:ExxonMobil's strategy focuses on leveraging feedstock-advantaged positions in the United States and Singapore, expanding halobutyl and EPDM capacity, and developing next-generation specialty elastomers for electrification and sustainability applications.

LG Chem.

LG Chem. is South Korea's largest diversified chemical company, headquartered in Seoul. LG Chem operates across petrochemicals, advanced materials, life sciences, and battery materials, with a significant synthetic rubber and elastomer business serving global tire and automotive markets.

- Product & Platform Portfolio: LG Chem. produces styrene butadiene rubber, nitrile butadiene latex (NBL), and polybutadiene rubber. The company is a global leader in NBL for medical and industrial gloves, with significant capacity in South Korea and Malaysia.

- Recent Developments: In 2025, LG Chem is strengthening its position in the rubber and elastomer industry by expanding high-value specialty materials and sustainability-driven product lines, supported by its LETZero eco-friendly materials brand focused on bio-based and recycled solutions.

- Strategic Focus: LG Chem's strategy centers on high-performance SSBR leadership for EV tire applications, expansion of specialty NBL capacity, and portfolio integration with the group's battery materials business for electrified mobility end markets.

Market Concentration Analysis

The global synthetic rubber market exhibits moderate fragmentation with regional concentration dynamics. The top five players - ARLANXEO, Exxon Mobil Corporation, China Petrochemical Corporation, LG CHEM., Asahi Kasei Corporation - collectively account for approximately 35-42% of global market revenue in 2025.

The market is experiencing a bifurcated dynamic. At the specialty elastomer tier, consolidation is occurring around technology platforms, sustainability credentials, and deep automotive OEM relationships.

Investment & Growth Opportunities

Fastest-Growing Segments

Liquid synthetic rubber represents the highest-growth form segment at approximately 3.7% CAGR through 2030, driven by adhesives, medical gloves, and specialty coatings. Non-tire automotive applications are expanding at an estimated 3.8% CAGR, supported by EV component demand.

Emerging Market Expansion

India represents the highest-potential emerging market, driven by automotive production growth, tire capacity additions announced through 2027, and make in India incentives. Southeast Asia’s footwear manufacturing base, Gulf Cooperation Council petrochemical integration projects, and Sub-Saharan Africa tire imports collectively represent significant growth opportunities for producers with regional supply capabilities.

Venture and Strategic Investment Trends

Sinopec expanded SSBR capacity in 2024, while LG Chem. announced a functional SSBR facility in Malaysia for 2026 startup. Venture capital is also flowing to bio-based elastomer startups and rubber recycling technologies, reflecting strong global momentum in synthetic rubber sustainability and next-generation material innovation.

Future Market Outlook (2026-2034)

The global synthetic rubber market forecast projects steady value expansion from USD 33.92 Billion in 2025 to USD 45.02 Billion by 2034 at a CAGR of 3.2%. Asia-Pacific will retain regional dominance and accelerate faster than the global average, while Europe and North America will sustain premium value growth through specialty elastomer demand and sustainability-driven premiumization.

Three structural shifts will reshape the synthetic rubber market through 2034. EV-optimized tire compounds will drive demand for functionalized SSBR and high-cis polybutadiene, making specialty grades standard in premium tire lines by 2028-2030. Bio-based and recycled content will move from pilot to commercial scale. Meanwhile, Chinese producers are expected to challenge legacy global leaders on specialty grade quality, intensifying competition across all price tiers.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024-2025 with synthetic rubber industry stakeholders, including plant directors at polymerization producers, procurement managers at global tire OEMs, specialty elastomer product managers, and institutional investors covering the chemicals sector. Primary insights validated market sizing, segmentation estimates, capacity utilization data, and technology adoption timelines.

Secondary Research

Secondary sources include International Energy Agency mobility reports, OICA global vehicle production data, International Rubber Study Group statistics, American Chemistry Council petrochemical data, Ministry of Heavy Industries India data, company annual reports, trade publications including Rubber & Plastics News and European Rubber Journal, and regional petrochemical association databases across Asia-Pacific, Europe, and North America.

Forecasting Models

Market size estimations and growth projections were derived using combined top-down and bottom-up forecasting models, incorporating GDP growth rates, automotive production indices, tire demand patterns, feedstock pricing, and historical market evolution. Scenario analysis (base, optimistic, and conservative cases) was performed to account for crude oil volatility, capacity expansion timing, and macroeconomic uncertainty.

Synthetic Rubber Market Report Scope

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Styrene Butadiene Rubber, Ethylene Propylene Diene Rubber, Polyisoprene, Polybutadiene Rubber, Isobutylene Isoprene Rubber, Others |

| Forms Covered | Liquid Synthetic Rubber, Solid Synthetic Rubber |

| Applications Covered | Tire and Tire Component, Non-Tire Automobile Application, Footwear, Industrial Goods, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Exxon Mobil Corporation, China Petrochemical Corporation, ARLANXEO, LG Chem., Asahi Kasei Corporation, ZEON CORPORATION, TSRC, Denka Company Limited, Apcotex, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the synthetic rubber market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global synthetic rubber market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the synthetic rubber industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Synthetic Rubber Market Report

The global synthetic rubber market was valued at USD 33.92 Billion in 2025, driven by automotive production, tire demand, and expanding specialty elastomer consumption across industrial and footwear applications globally.

The market is projected to reach USD 45.02 Billion by 2034, growing at a CAGR of 3.2% during 2026-2034, supported by EV tire demand, bio-based innovation, and Asia-Pacific capacity expansion.

Tire and tire components lead with a 58.4% share in 2025, driven by global vehicle production exceeding 93 million units, EV tire demand, and replacement tire cycles across all major regions worldwide.

Liquid synthetic rubber is the fastest-growing form segment, expanding at an estimated CAGR of 3.7% through 2030, driven by adhesive, sealant, medical glove, and specialty coating application demand globally.

Asia-Pacific dominates with a 46.7% share in 2025. China's tire manufacturing, India's automotive growth, and Japan-Korea specialty elastomer leadership underpin regional market dominance through 2034.

Key drivers include automotive production, EV tire demand, footwear manufacturing, specialty latex growth, and capacity expansions across Asia-Pacific supporting steady value creation through 2034 globally.

Major players include ARLANXEO, Exxon Mobil Corporation, China Petrochemical Corporation, LG CHEM., Asahi Kasei Corporation, ZEON CORPORATION, TSRC, Denka Company Limited, and Apcotex.

Functionalized SSBR and bio-based elastomers are the fastest-growing technologies, driven by EV tire compound requirements, sustainability mandates from automotive OEMs, and circular economy regulations worldwide.

Key opportunities include specialty elastomer capacity, EV-grade compounds, bio-based elastomer scale-up, India and Southeast Asia expansion, and rubber recycling technologies across the automotive value chain globally.

Solid synthetic rubber holds 72.5% of global revenue in 2025 while liquid synthetic rubber accounts for 27.5%, with liquid growing faster due to adhesive, medical glove, and coating application expansion.

EV adoption drives demand for low-rolling-resistance functionalized SSBR, high-cis polybutadiene, and EPDM for battery sealing, collectively creating premium-priced growth opportunities across tire and automotive component markets.

Crude oil price volatility, natural rubber substitution, tightening environmental regulations, and Chinese capacity oversupply risk.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)