Taiwan EdTech Market Size, Share, Trends and Forecast by Sector, Type, Deployment Mode, End User, and Region, 2026-2034

Taiwan EdTech Market Size, Share, Trends & Forecast (2026-2034)

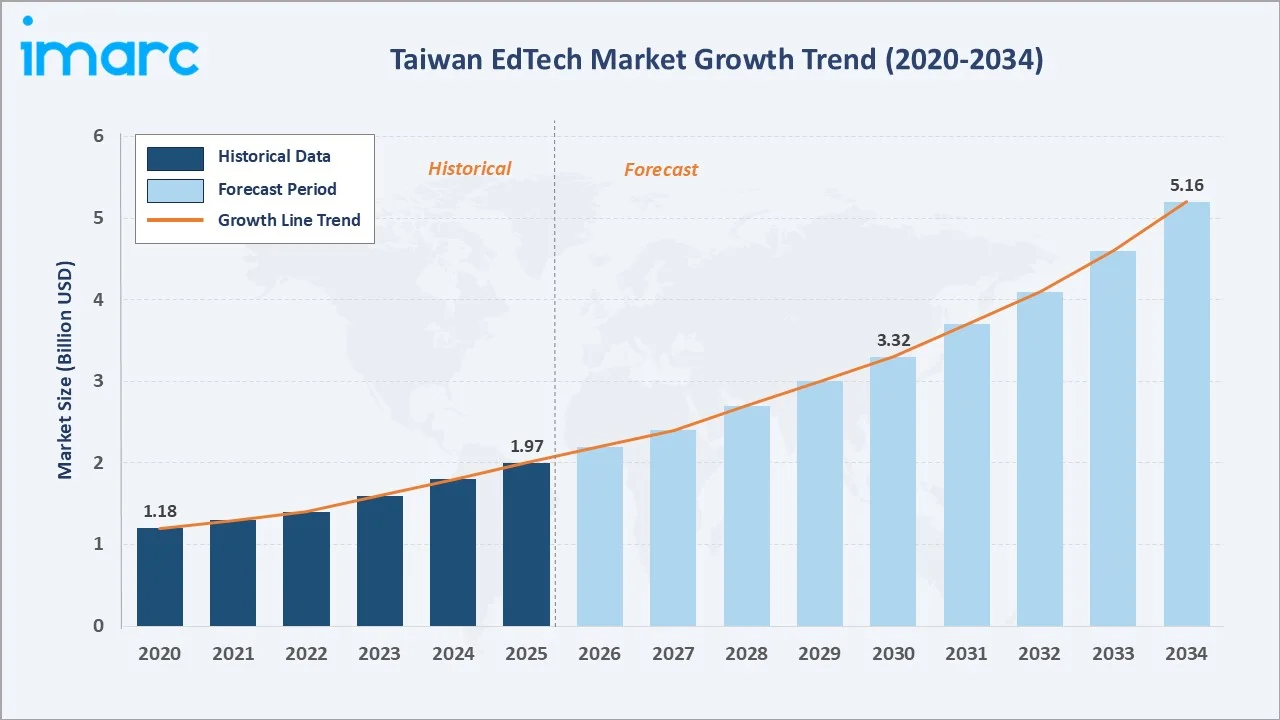

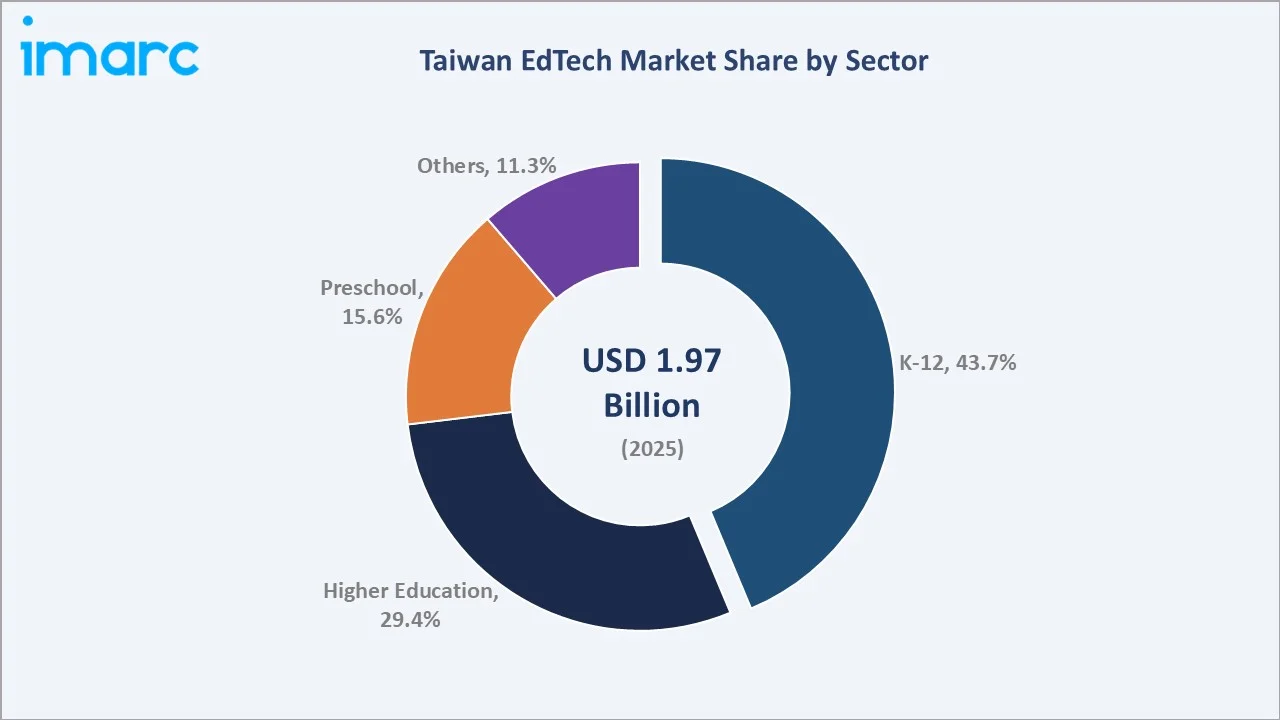

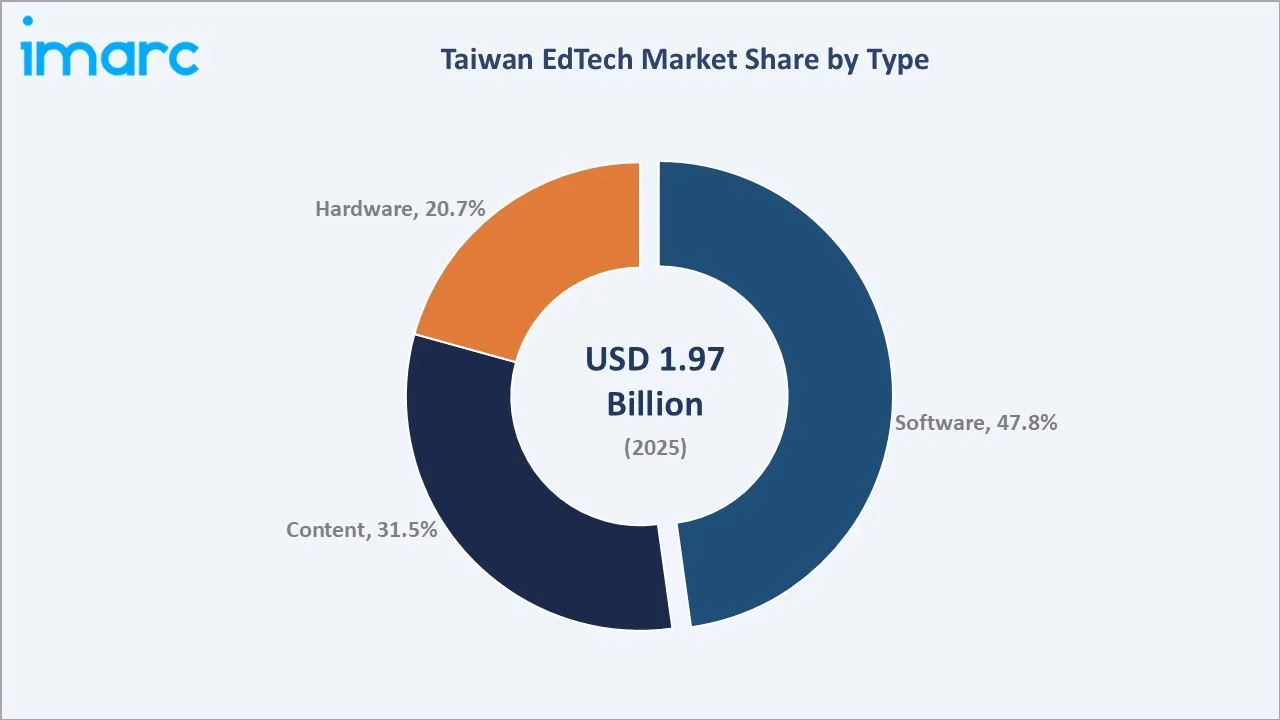

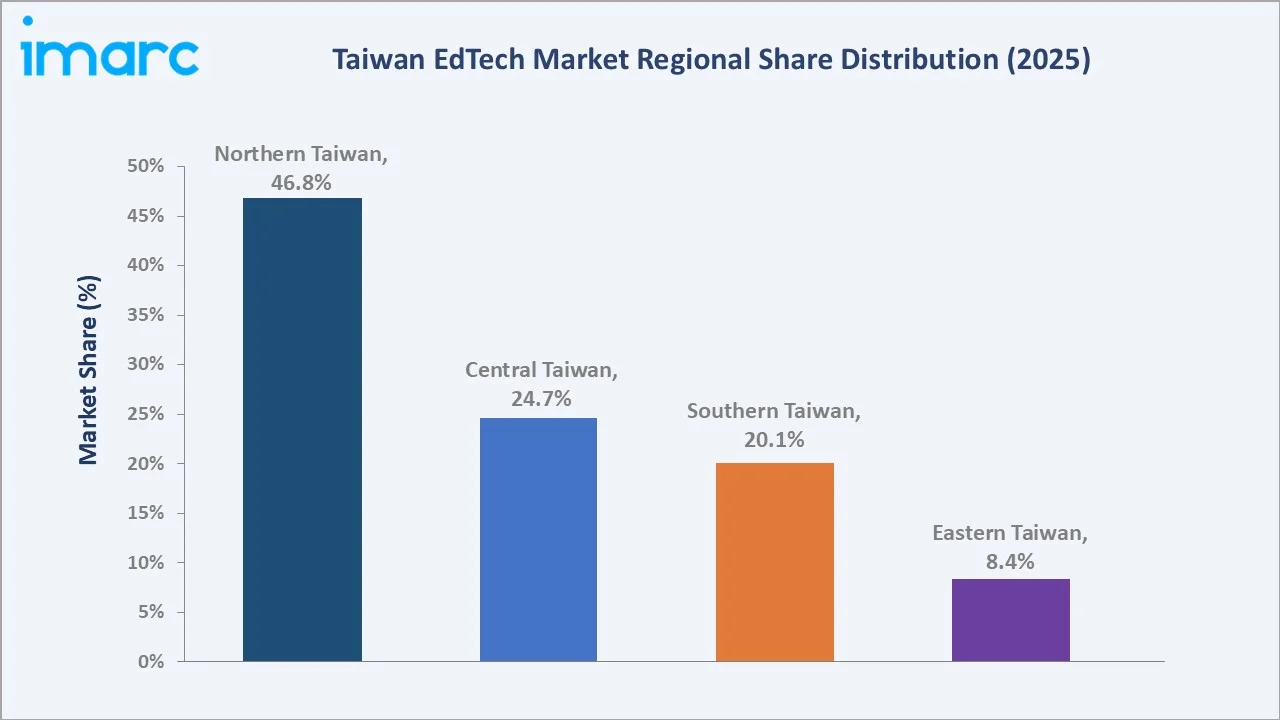

The Taiwan EdTech market reached USD 1.97 Billion in 2025 and is projected to reach USD 5.16 Billion by 2034, growing at a CAGR of 10.92% during 2026-2034. The market is driven by strong digital learning adoption, high internet penetration, and growing demand for online tutoring, test preparation, and skill-based learning platforms. According to the Ministry of Digital Affairs (MODA), Taiwan’s digital adoption continues to strengthen, with household internet penetration reached 93.4% and individual internet usage reached to 90.3% in 2025. High connectivity also supports remote learning, personalized education, and broader access to lifelong learning and professional upskilling programs across the country. K-12 leads the sector at 43.7%. Software leads the type at 47.8%. Northern Taiwan leads regionally at 46.8%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.97 Billion |

|

Forecast Market Size (2034) |

USD 5.16 Billion |

|

CAGR (2026-2034) |

10.92% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Sector |

K-12 (43.7%, 2025) |

|

Dominant Type |

Software (47.8%, 2025) |

|

Leading Region |

Northern Taiwan (46.8%, 2025) |

The Taiwan EdTech market grew from USD 1.18 Billion in 2020 to USD 1.97 Billion in 2025, reflecting strong adoption of online learning, tutoring platforms, and digital education tools. The market is expected to reach USD 3.32 Billion by 2030, supported by high internet penetration, government-backed digital transformation, and rising use of AI-enabled learning solutions. By 2034, it is forecast to reach USD 5.16 Billion, driven by lifelong learning, professional upskilling, and hybrid education models. Overall, the market shows steady long-term growth as digital learning becomes more integrated across schools, universities, and workforce training.

To get more information on this market, Request Sample

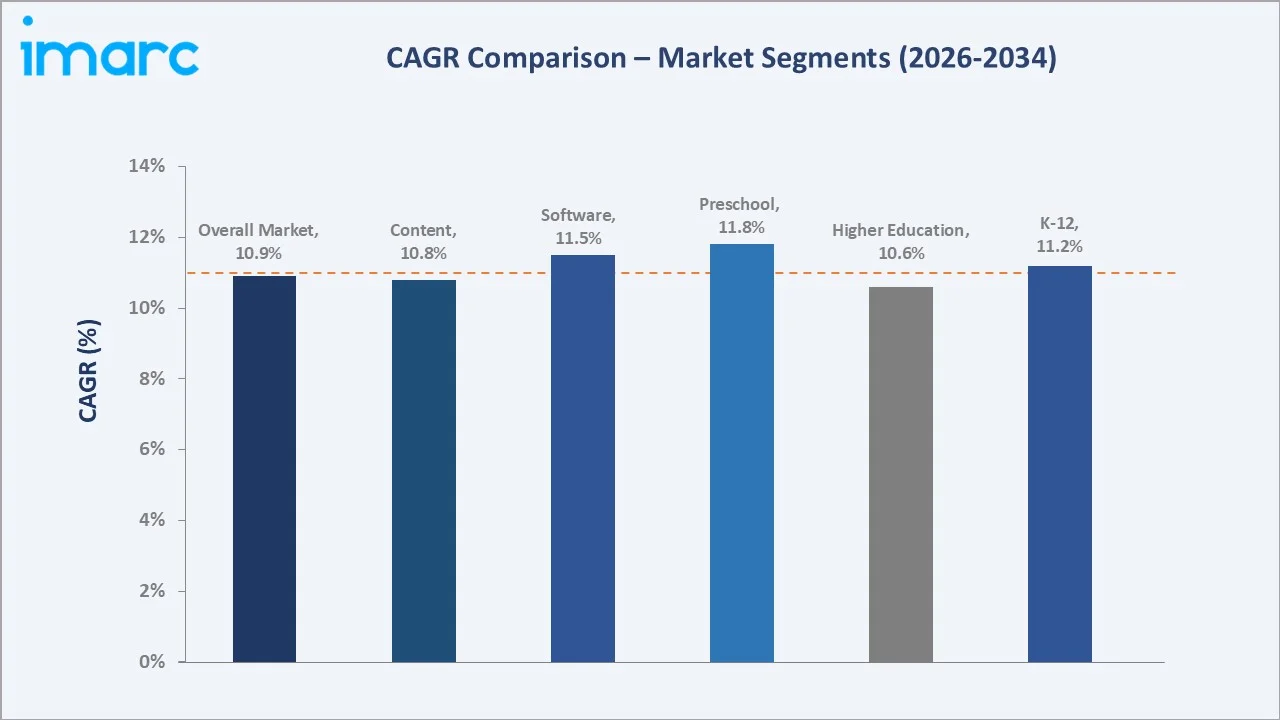

Preschool grows fastest at ~11.8% CAGR through bilingual education policy and AI-assisted early learning. Software grows at ~11.5% CAGR through generative AI tutoring and LMS SaaS. K-12 grows at ~11.2% CAGR through the smart classroom and 12-year basic education digital transformation.

Executive Summary

The Taiwan EdTech market is expanding steadily as digital learning becomes mainstream across schools, universities, tutoring centers, and corporate training. High internet access, strong device adoption, and government-led digital education initiatives are supporting wider use of online platforms and hybrid learning models. Demand is also rising for AI-enabled personalized learning, test preparation, language learning, and professional upskilling solutions. EdTech providers are focusing on interactive content, learning analytics, cloud-based classrooms, and mobile-first platforms to improve engagement. Overall, Taiwan’s mature digital infrastructure and skilled learner base position the market for sustained growth through 2034. K-12 at 43.7% leads through the smart classroom. Software at 47.8% leads through LMS and AI tutoring. Northern Taiwan leads regionally at 46.8%.

Key Market Insights

|

Insight |

Data |

|

Dominant Sector |

K-12 - 43.7% share (2025) |

|

Dominant Type |

Software - 47.8% market share (2025) |

|

Leading Region |

Northern Taiwan - 46.8% share (2025) |

|

Market Opportunity |

Generative AI personalized tutoring; AR/VR immersive classroom; adult reskilling; Southeast Asia EdTech export; corporate L&D platform |

Key Analytical Observations Supporting The Above Data:

- K-12 at 43.7%: The K-12 segment leads the market as schools increasingly adopt digital classrooms, e-learning platforms, smart content, and online assessment tools. Strong demand for tutoring, exam preparation, STEM learning, and personalized learning solutions further supports segment dominance.

- Software at 47.8%: The software leads the market due to widespread adoption of learning management systems (LMS), virtual classrooms, AI-powered learning applications, and digital assessment platforms. Its scalability, ease of deployment, and ability to deliver personalized learning experiences make it the preferred EdTech solution across educational institutions and corporate training environments.

- Northern Taiwan at 46.8%: Northern Taiwan leads regionally due to its concentration of schools, universities, technology companies, and higher-income urban households. Strong digital infrastructure and early adoption of AI-enabled learning platforms further support regional dominance.

Taiwan EdTech Market Overview

The Taiwan EdTech market encompasses digital learning platforms, learning management systems, virtual classrooms, online tutoring, test preparation, and mobile-based education applications. It also includes AI-powered personalized learning tools, digital assessment solutions, interactive content, and analytics-driven student performance tracking. The market serves K-12 schools, higher education institutions, tutoring centers, corporates, and lifelong learners. Growth is supported by strong digital infrastructure, high internet penetration, hybrid learning adoption, and demand for flexible skill-based education. Macroeconomic factors include Taiwan’s high internet penetration, strong digital infrastructure, and continued investment in information and communication technologies.

Market Dynamics

To evaluate market opportunities, Request Sample

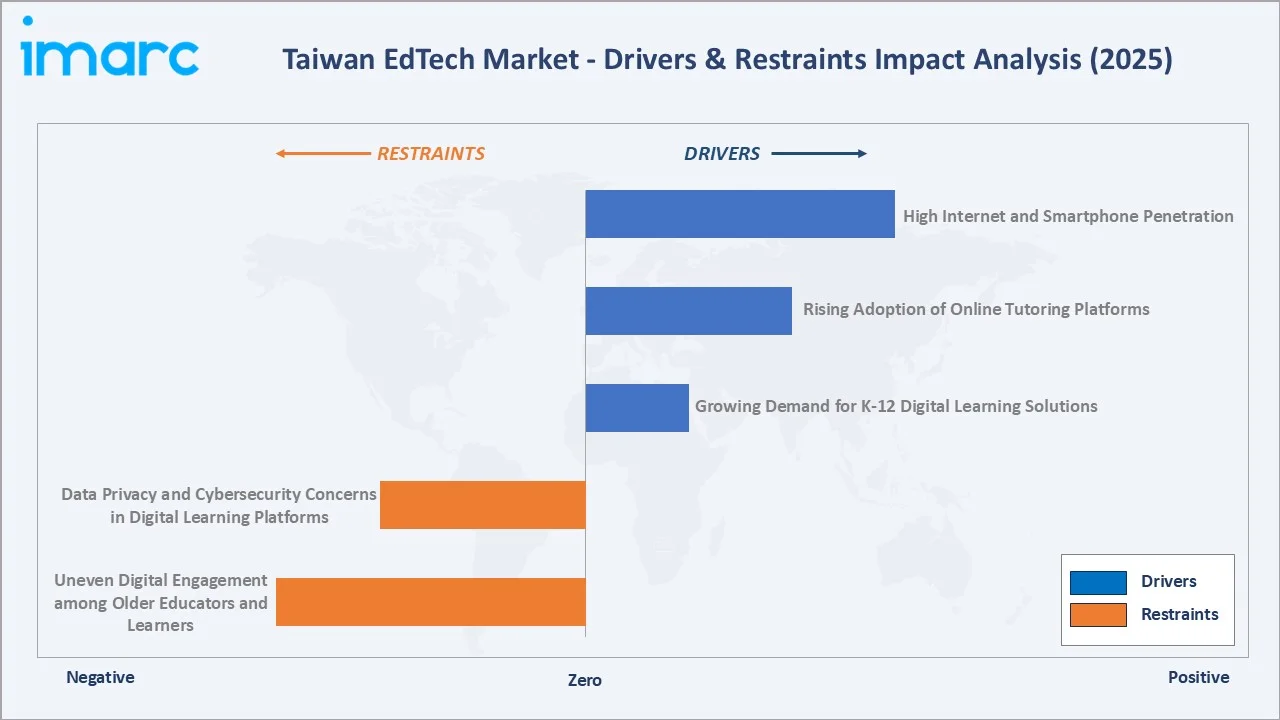

Market Drivers

- High Internet and Smartphone Penetration: By late 2025, Taiwan had 29.4 million active cellular mobile connections, equivalent to 127% of the total population, indicating widespread multi-device and mobile connectivity. The number of internet users reached 22.3 million, with online penetration standing at 96.7%. This high internet and smartphone penetration enables seamless access to online learning platforms, virtual classrooms, and educational applications. With a large share of the population connected to the internet, students can engage in learning anytime and from virtually any location. Widespread smartphone usage also supports mobile learning, microlearning, and personalized educational content delivery. This strong digital connectivity encourages higher adoption of AI-powered learning tools, online tutoring services, and cloud-based education platforms across all age groups.

- Rising Adoption of Online Tutoring Platforms: Rising adoption of online tutoring platforms is driving the market as students increasingly use digital channels for exam preparation, subject support, language learning, and after-school coaching. These platforms offer flexible scheduling, recorded lessons, live classes, and personalized study plans, making learning more accessible and convenient. Parents are also turning to online tutoring for performance tracking and customized academic support. This trend is strengthening demand for AI-based learning analytics, interactive content, and subscription-based education models.

- Growing Demand for K-12 Digital Learning Solutions: Growing demand for K-12 digital learning solutions is driving the market as schools and parents increasingly seek interactive, personalized, and curriculum-aligned tools for students. Digital platforms support smart classrooms, online assignments, assessments, and performance tracking, improving learning efficiency. Rising focus on STEM education, language learning, and exam preparation is further increasing adoption among K-12 learners. This demand is encouraging EdTech providers to develop AI-enabled content, adaptive learning modules, and engaging mobile-first solutions.

Market Restraints

- Data Privacy and Cybersecurity Concerns in Digital Learning Platforms: Digital learning platforms collect sensitive student data, academic records, payment details, and user behavior information. Schools, parents, and institutions may hesitate to adopt platforms that lack strong encryption, identity protection, or secure data storage. Any breach or misuse of learner data can reduce trust and slow platform adoption. As a result, EdTech providers must invest heavily in cybersecurity, compliance, and transparent data governance, which can increase operating costs.

- Uneven Digital Engagement among Older Educators and Learners: Some users may be less comfortable adopting online platforms, learning apps, and AI-enabled tools. This can slow classroom integration, reduce platform usage, and increase the need for training and technical support. Resistance to digital teaching methods may also limit the effectiveness of blended learning models. As a result, EdTech providers must focus on user-friendly interfaces, onboarding support, and educator training to improve adoption.

Market Opportunities

- AI-Powered Personalized and Adaptive Learning Solutions: AI-powered personalized and adaptive learning solutions enable customized learning paths based on individual student performance, strengths, and learning pace. In December 2025, BenQ hosted education leaders from international schools in the Middle East in Taiwan for the EduVision Summit 2025 – Bridging Innovation Across Borders, creating a platform for cross-regional discussions on AI-driven education and future talent development. The program included classroom visits and on-site exchanges at Taipei Renai Junior High School, where educators observed the practical use of AI, STEAM education, and bilingual learning. These platforms use data analytics and machine learning to deliver targeted content, real-time feedback, and intelligent assessments, improving learning outcomes and engagement.

- Development of Immersive AR/VR-Based Educational Content: Development of immersive AR/VR-based educational content, making learning more interactive, engaging, and experiential. AR and VR technologies enable students to visualize complex concepts, conduct virtual science experiments, and explore simulated real-world environments that enhance knowledge retention. These tools are particularly valuable for STEM education, vocational training, medical education, and language learning. Taiwan’s advanced technology ecosystem and growing investment in digital education create favorable conditions for the wider adoption of immersive learning solutions across schools and training institutions.

Market Challenges

- Rapid Technological Changes Requiring Continuous Platform Upgrades: Rapid technological changes requiring continuous platform upgrades are challenging as providers must constantly update software, AI tools, cybersecurity features, and learning interfaces to remain competitive. Frequent upgrades can increase development costs and create pressure on smaller EdTech companies with limited technical resources. Schools and institutions may also face disruption when platforms change too often or require new training.

- Dependence on Stable Internet Connectivity and Digital Infrastructure: Dependence on stable internet connectivity and digital infrastructure is challenging as online learning platforms require reliable broadband, cloud access, and device availability to function effectively. Any connectivity gap can disrupt live classes, assessments, content streaming, and learner engagement. Although Taiwan has a strong digital infrastructure, uneven access or network issues can still affect remote areas and lower-income users.

Emerging Market Trends

1. Generative AI and LLM-Powered Education Platforms

Generative AI and LLM-powered education platforms are emerging as institutions adopt AI tutors, automated content generation, intelligent feedback, and personalized study support. These tools can help students receive instant explanations, practice questions, writing assistance, and adaptive learning recommendations. For teachers, generative AI supports lesson planning, grading assistance, and customized learning material creation. As Taiwan strengthens its AI ecosystem, LLM-enabled education platforms are expected to reshape digital learning delivery and improve learner engagement.

2. Gamification and Game-Based Learning

Gamification and game-based learning are emerging as educators use points, badges, leaderboards, quizzes, and interactive challenges to improve student engagement. These tools make learning more enjoyable and help increase course completion, especially among K-12 and language-learning users. Game-based platforms also support problem-solving, collaboration, and real-time progress tracking. As demand grows for interactive digital education, gamified learning solutions are becoming an important differentiator for EdTech providers.

3. AI and XR Learning Technologies

AI and XR learning technologies are emerging as educators combine artificial intelligence with extended reality tools to create more personalized and immersive learning experiences. In February 2024, EON Reality launched Taiwan’s first Spatial AI Center, marking a significant step forward in immersive education and training. The initiative aims to enhance learning experiences for both students and professionals by integrating artificial intelligence (AI) and extended reality (XR) technologies. AI supports adaptive learning paths, automated feedback, and learner performance analytics, while XR enables virtual labs, 3D simulations, and interactive classroom environments. This trend is especially relevant for STEM, vocational, medical, and technical education.

4. Coding and Computational Thinking in K-12

Coding and computational thinking in K-12 are emerging as schools place greater emphasis on digital literacy, problem-solving, and STEM readiness from an early age. EdTech platforms are offering coding games, robotics modules, logic-based exercises, and AI learning tools to make technical skills more accessible for younger students. This trend supports Taiwan’s broader technology-driven economy by preparing students for future careers in software, semiconductors, AI, and advanced manufacturing. It also creates demand for curriculum-aligned digital content, teacher training tools, and interactive learning platforms.

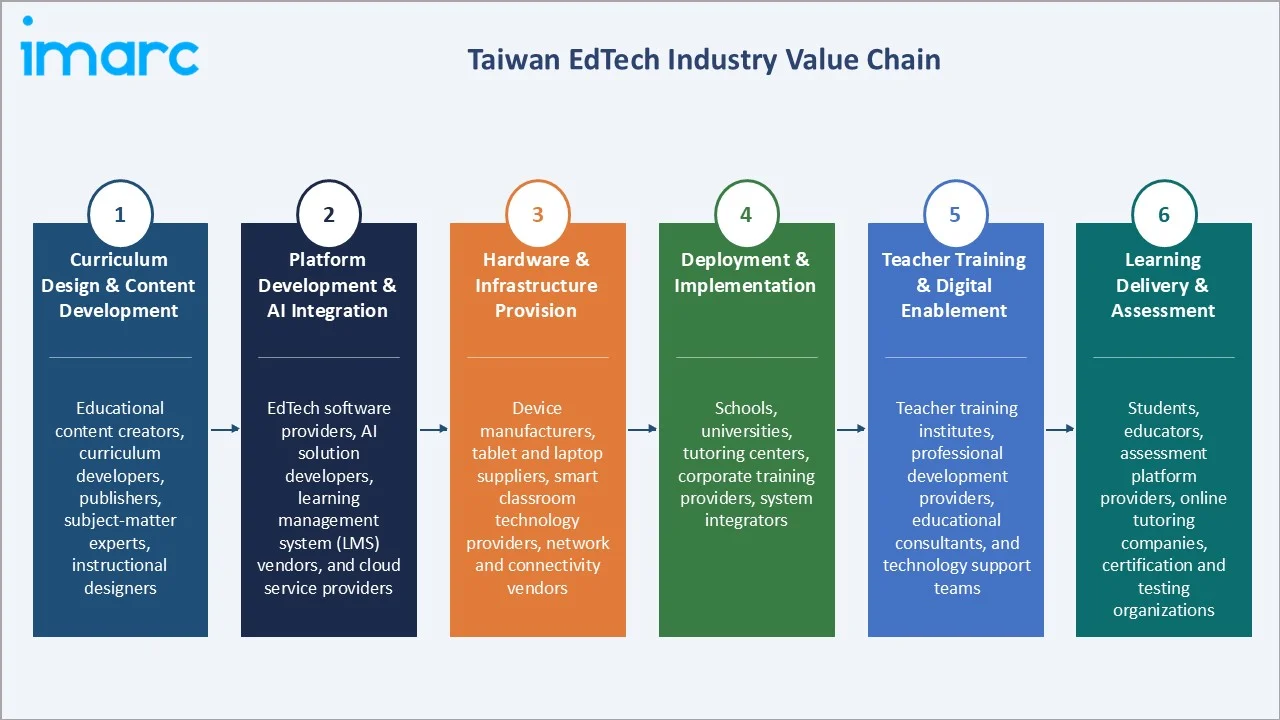

Industry Value Chain Analysis

Taiwan EdTech value chain integrates curriculum design & content development, platform development & AI integration, hardware & infrastructure provision, deployment & implementation, teacher training & digital enablement, and learning delivery & assessment.

|

Stage |

Key Participants |

|

Curriculum Design & Content Development |

Educational content creators, curriculum developers, publishers, subject-matter experts, instructional designers |

|

Platform Development & AI Integration |

EdTech software providers, AI solution developers, learning management system (LMS) vendors, and cloud service providers |

|

Hardware & Infrastructure Provision |

Device manufacturers, tablet and laptop suppliers, smart classroom technology providers, network and connectivity vendors |

|

Deployment & Implementation |

Schools, universities, tutoring centers, corporate training providers, system integrators |

|

Teacher Training & Digital Enablement |

Teacher training institutes, professional development providers, educational consultants, and technology support teams |

|

Learning Delivery & Assessment |

Students, educators, assessment platform providers, online tutoring companies, certification and testing organizations |

The platform development & AI integration stage is the most value-added stage in the Taiwan EdTech value chain. This is where learning management systems, AI-powered personalization, adaptive learning algorithms, analytics engines, and digital learning experiences are developed, creating the core differentiation, intellectual property, and revenue-generating capabilities of EdTech solutions.

Technology Landscape in the Taiwan EdTech Industry

Generative AI Learning Technology

Generative AI learning technology is shaping the Taiwan EdTech industry by enabling AI teaching assistants, automated content creation, real-time translation, smart presentations, and transcription tools. In April 2026, National Taipei University of Technology launched its Generative AI Application Platform, marking one of the few fully in-house developed systems in Taiwan, created entirely by its faculty and students. The platform brings together multiple applications, including AI teaching assistants, real-time multilingual interpretation, smart presentation tools, AI-based meeting transcription, and enterprise solutions. These solutions help educators reduce administrative workload while improving lesson delivery, student support, and multilingual learning access.

Virtual Classroom Technology

Virtual classroom technology enables live online classes, remote collaboration, screen sharing, digital whiteboards, and real-time student interaction. These platforms support hybrid learning across schools, universities, tutoring centers, and corporate training programs. They also improve access to education for learners outside physical classrooms while allowing teachers to deliver lessons more flexibly. As Taiwan’s digital infrastructure strengthens, virtual classrooms are becoming a core part of modern education delivery.

Digital Assessment and Proctoring Technology

Digital assessment and proctoring technology enable secure online examinations, automated grading, and real-time performance evaluation. AI-powered proctoring tools help maintain exam integrity through identity verification, behavior monitoring, and anomaly detection during remote assessments. These technologies reduce administrative workload while providing faster and more accurate feedback to students and educators. As online and hybrid learning models expand, digital assessment solutions are becoming essential for scalable and reliable education delivery.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Sector |

K-12 |

43.7% |

2025 |

|

Type |

Software |

47.8% |

2025 |

|

Deployment Mode |

🔒 |

🔒 |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Region |

Northern Taiwan |

46.8% |

2025 |

By Sector

K-12 leads at 43.7% (2025), due to strong adoption of digital classrooms, online tutoring, smart content, and assessment tools across schools. Rising demand for STEM learning, exam preparation, language learning, and personalized education further supports its dominance.

To access detailed market analysis, Request Sample

Higher education at 29.4% reflects university LMS, research EdTech platforms, and university programs. Preschool at 15.6% grows fastest at ~11.8% CAGR through bilingual preschool mandate, AI phonics early learning, and tablet-based early childhood education. Others at 11.3% include corporate training, adult reskilling, and vocational education.

By Type

Software leads at 47.8% (2025)2025 through LMS platforms, AI tutoring software, gamified SaaS, and generative AI EdTech platforms.

Content at 31.5% reflects digital open textbooks, digital curriculum content, video lectures, and gamified learning content. Hardware at 20.7% reflects tablets and Chromebooks, smart interactive displays, and RFID attendance systems.

Regional Market Insights

|

Region |

Share (2025) |

Key Taiwan EdTech Market Drivers & Characteristics |

|

Northern Taiwan |

46.8% |

Reflecting its concentration of leading universities, technology companies, innovation hubs, and digitally advanced educational institutions. |

|

Central Taiwan |

24.7% |

Reflects growing investment in digital education, increasing adoption of online learning platforms, and expanding integration of EdTech solutions across schools, universities, and vocational training centers. |

|

Southern Taiwan |

20.1% |

Reflects rising demand for remote learning, workforce upskilling, digital classrooms, and technology-enabled education supported by regional industrial and economic development. |

|

Eastern Taiwan |

8.4% |

Reflects the use of EdTech solutions to improve educational accessibility, support distance learning, and bridge geographic barriers through cloud-based and mobile learning platforms. |

Northern Taiwan's 46.8% dominance is supported by its strong concentration of universities, schools, technology firms, and innovation hubs. Central Taiwan's 24.7% growing steadily as digital learning adoption expands across schools, vocational institutes, and training centers.

Southern Taiwan's 20.1% benefits from rising demand for workforce upskilling, smart classrooms, and online education linked to industrial development. Eastern Taiwan's 8.4% shows smaller but important growth, as EdTech improves access to learning in less urbanized areas.

Competitive Landscape

The Taiwan EdTech market is moderately fragmented, with competition among global EdTech providers, local digital learning companies, online tutoring platforms, and education software developers. Market participants compete through AI-powered learning solutions, adaptive learning technologies, virtual classrooms, and digital assessment tools. Companies are increasingly investing in generative AI, learning analytics, and immersive AR/VR content to differentiate their offerings.

|

Company |

Key Products |

Market Position |

Core Strength |

|

HABOOK Group |

HiTeach Smarter Teaching System, HiTeach Web, HiTeach + AI Sokrates |

Market Leader |

HABOOK Group plays a pioneering role in Taiwan’s EdTech ecosystem, primarily by driving the digital transformation of K-12 schools through its TEAM Model AI Smarter Schools framework. |

|

Hahow |

Audio Visual Courses, Learning Supplies |

Market Leader |

Hahow is Taiwan's largest interdisciplinary crowdfunding and online learning platform. It revolutionized the local EdTech sector by allowing educators and professionals to validate and fund their course ideas before production, effectively monetizing specialized skills and making adult cross-domain learning highly accessible. |

|

Microsoft |

Microsoft 365 Education |

Strong Challenger |

Microsoft plays a foundational role in Taiwan's EdTech ecosystem, focusing on cloud infrastructure, generative AI integration, and nationwide digital literacy. Through strategic partnerships with the government and local tech firms, Microsoft is reshaping how the island teaches and learns. |

|

ViewSonic Corporation |

myViewBoard, TeamOne, Manager |

Niche Player |

ViewSonic Corporation has transformed Taiwan’s educational technology (EdTech) sector by transitioning from a hardware-centric display provider to a comprehensive ecosystem developer. |

Strategic partnerships with schools, universities, and corporate training providers are becoming an important growth strategy. The competitive landscape is further shaped by continuous innovation, cloud-based learning platforms, and demand for personalized education experiences.

Key Company Profiles

HABOOK Group

HABOOK Group is a Taiwan-based education technology company with experience in developing digital learning and smart education solutions. The company has built the TEAM Model AI Smarter Schools ecosystem, which includes HiTeach smart teaching systems, student learning platforms, cloud-based management and analytics services, and AI-powered teaching analytics tools. HABOOK serves schools and educational institutions through solutions covering smart classrooms, digital assessment, teacher professional development, hybrid learning, and AI-driven education management.

- Key Products: HiTeach Smarter Teaching System, HiTeach Web, HiTeach + AI Sokrates.

- Strategic Focus: Advancing AI-powered smart education ecosystems through its HiTeach platform and TEAM Model AI Smarter Schools framework. The company emphasizes intelligent classrooms, real-time learning analytics, digital assessment, and personalized learning solutions to improve teaching effectiveness and student outcomes.

Microsoft

Microsoft is a technology leader with a strong presence in Taiwan’s EdTech market through its cloud, productivity, AI, and education-focused solutions. The company supports schools, universities, and training institutions with products such as Microsoft 365 Education. Microsoft’s solutions enable virtual classrooms, collaboration, digital content management, assessment, and hybrid learning environments.

- Key Products: Microsoft 365 Education.

- Strategic Focus: Accelerating AI-driven digital learning and cloud-based education transformation. The company promotes the adoption of Microsoft 365 Education, Teams for Education, Copilot, and Azure AI to support personalized learning, virtual classrooms, collaboration, and administrative efficiency.

Market Concentration Analysis

The Taiwan EdTech market is moderately fragmented, with a mix of global technology companies, local EdTech specialists, online tutoring providers, and education software developers competing across different segments. Large technology firms leverage cloud infrastructure, AI capabilities, and established education ecosystems, while domestic players focus on localized content and curriculum-aligned solutions. Competition is increasing around AI-powered learning, adaptive education platforms, digital assessment tools, and immersive learning technologies. Strategic partnerships with schools, universities, and government agencies are key competitive differentiators. The market remains innovation-driven, with continuous investments in generative AI, analytics, and smart classroom solutions shaping competitive positioning.

Investment & Growth Opportunities

Highest Growth Segments

Preschool (~11.8% CAGR), software GenAI (~11.5% CAGR), K-12 AI smart classroom (~11.2% CAGR), corporate L&D reskilling (~10% CAGR), and AR/VR immersive learning (~15% CAGR from emerging base) represent Taiwan EdTech's highest-growth investment vectors through 2034.

Investment Themes

- Generative AI EdTech platform: Growing adoption of AI tutors, content generation, automated assessments, and personalized learning creates strong investment opportunities in generative AI-powered education platforms serving schools, universities, and corporate learners.

- Southeast Asia EdTech export: Taiwan’s strengths in AI, digital learning technologies, and smart education solutions position local EdTech providers to expand into Southeast Asian markets, where demand for scalable online learning platforms continues to grow rapidly.

Future Market Outlook (2026-2034)

Taiwan EdTech market is projected to grow from USD 1.97 Billion in 2025 to USD 5.16 Billion by 2034, delivering a 10.92% CAGR over the forecast period through government funding, generative AI personalized learning mainstream, bilingual Taiwan 2030 policy, and Southeast Asia EdTech export. The market's anchor value of USD 3.32 Billion in 2030 represents Taiwan EdTech at the generative AI mainstream and bilingual inflection.

Three structural forces define Taiwan EdTech growth through 2034. First, widespread digital connectivity and government-backed education digitalization initiatives are accelerating the adoption of online and hybrid learning models. Second, increasing demand for AI-powered personalized learning, adaptive education platforms, and generative AI tools is transforming how students learn and how educators teach. Third, growing emphasis on workforce upskilling, lifelong learning, and STEM education is expanding EdTech usage beyond traditional classrooms.

Research Methodology

Primary Research

Primary research comprised interviews with EdTech providers, school administrators, university representatives, tutoring centers, teachers, and corporate training managers across Taiwan. It also included discussions with technology vendors, LMS providers, AI learning platform developers, and digital classroom solution providers. Inputs from students, parents, and educators helped assess adoption patterns, learning preferences, platform usability, and demand for AI-enabled education tools.

Secondary Research

Secondary research encompassed company annual reports, investor presentations, government publications, education ministry data, and industry association reports. It also included analysis of EdTech company websites, product portfolios, academic studies, market databases, and technology publications. Additional sources such as news articles, policy announcements, and digital education initiatives were reviewed to validate market trends, competitive developments, and technology adoption patterns across Taiwan.

Forecasting Models

Forecasting models combined historical market performance, EdTech adoption rates, digital learning penetration, and education technology spending trends to estimate future market growth. The analysis incorporated macroeconomic indicators such as internet penetration, digital infrastructure development, education expenditure, and workforce upskilling demand. Forecasts also considered the impact of AI adoption, hybrid learning models, government digital education initiatives, and technological innovation across the education ecosystem.

Taiwan EdTech Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Sectors Covered | Preschool, K-12, Higher Education, Others |

| Types Covered | Hardware, Software, Content |

| Deployment Modes Covered | Cloud-based, On-premises |

| End Users Covered | Individual Learners, Institutes, Enterprises |

| Regions Covered | Northern Taiwan, Central Taiwan, Southern Taiwan, Eastern Taiwan |

| Companies Covered | HABOOK Group, Hahow, Microsoft, ViewSonic Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Taiwan EdTech market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Taiwan EdTech market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Taiwan EdTech industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Taiwan EdTech Market Report

The Taiwan EdTech market reached USD 1.97 Billion in 2025, driven by high internet and smartphone penetration, strong government support for digital education, and rising adoption of AI-enabled learning platforms. Growth is further supported by online tutoring, K-12 digital learning demand, and workforce upskilling needs.

The Taiwan EdTech market grows at 10.92% CAGR during 2026-2034, reaching USD 5.16 Billion by 2034. The CAGR reflects GenAI disruption, bilingual policy, STEM demand, and ASEAN export.

K-12 leads at 43.7% due to strong demand for digital classrooms, online tutoring, STEM learning, and exam preparation tools. Wider adoption of smart content, adaptive learning, and digital assessment platforms across schools further supports its dominant position.

Software leads at 47.8% due to strong adoption of learning management systems, virtual classrooms, AI learning platforms, and digital assessment tools. Its scalability, lower deployment complexity, and ability to support personalized and hybrid learning make it the preferred solution across schools, universities, and training providers.

Northern Taiwan leads at 46.8% due to its high concentration of universities, schools, technology firms, and innovation hubs. Strong digital infrastructure, higher institutional spending, and early adoption of AI-enabled learning platforms further support the region’s dominance.

Leading companies include HABOOK Group, Hahow, Microsoft, and ViewSonic Corporation, among others.

The market is projected to reach approximately USD 3.32 Billion by 2030, supported by the rising adoption of AI-enabled learning platforms, online tutoring, and hybrid classrooms. Growth will be driven by strong digital infrastructure, K-12 demand, software-led solutions, and increasing focus on lifelong learning and workforce upskilling.

Three priority investment opportunities are emerging in Taiwan’s EdTech market. First, generative AI and adaptive learning platforms offer strong potential as institutions seek personalized and data-driven education solutions. Second, AR/VR/XR-based immersive learning technologies are gaining traction across STEM, vocational, and professional training applications. Third, Southeast Asia-focused EdTech exports present growth opportunities for Taiwanese providers leveraging their strengths in AI, digital content, and smart education technologies.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)