Team Collaboration Software Market Report by Components (Solution, Service), Software Type (Conferencing, Communication and Co-Ordination), Deployment (On-Premises, Cloud-based), Industry Vertical (BFSI, Manufacturing, Healthcare, IT and Telecommunications, Retail and E-commerce, Government and Defense, Media and Entertainment, Education, and Others), and Region 2026-2034

Team Collaboration Software Market Size:

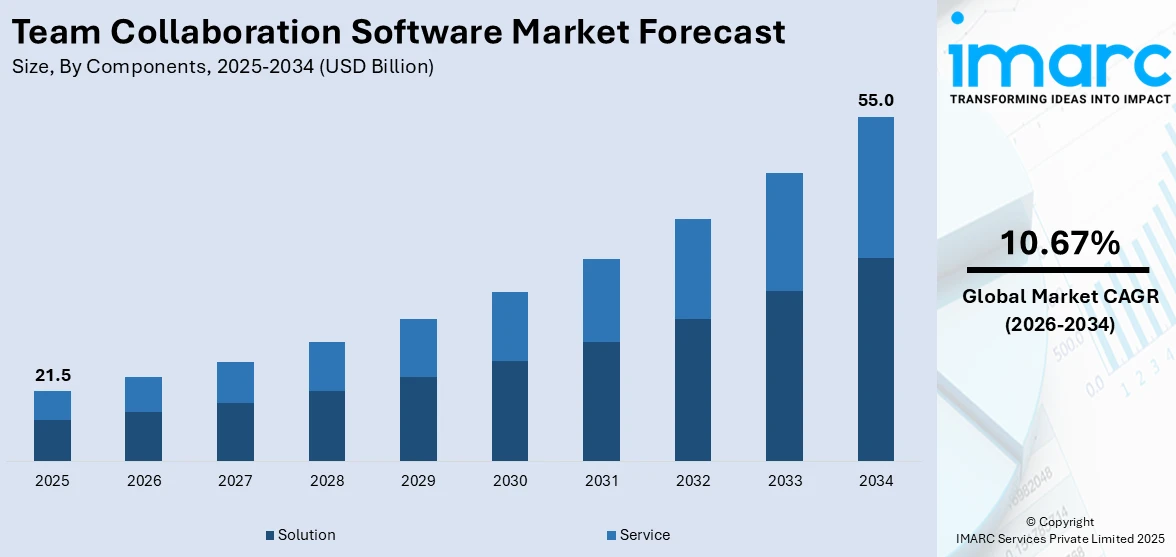

The global team collaboration software market size reached USD 21.5 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 55.0 Billion by 2034, exhibiting a growth rate (CAGR) of 10.67% during 2026-2034. North America dominates the market owing to its widespread adoption of remote and hybrid work models and strong presence of leading vendors. The market is experiencing significant growth, driven by the rising adoption of remote work, rapid technological advancements, increasing focus on employee productivity, growing need for streamlined project management, and the heightened software adoption among small and medium-sized enterprises (SMEs).

|

Report Attribute

|

Key Statistics |

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034 |

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 21.5 Billion |

|

Market Forecast in 2034

|

USD 55.0 Billion |

| Market Growth Rate (2026-2034) | 10.67% |

Team Collaboration Software Market Analysis:

- Major Market Drivers: The expansion of remote and hybrid work trends has raised the demand for team collaboration software, which enables smooth communication and cooperation across geographically distributed teams. Aside from that, the use of artificial intelligence (AI) and machine learning (ML) has been shown to improve the capabilities of collaboration tools. Furthermore, the increased emphasis on employee productivity and engagement, along with the need for more efficient project management, is boosting the use of powerful collaboration software solutions.

- Key Market Trends: There is a rising trend for unified communication systems, which combine many communication technologies into a single interface, simplifying operations and increasing productivity. Also, the move toward mobile collaboration as the usage of smartphones and tablets has increased, allowing employees to stay connected and productive while on the road is favoring the growth of this industry. Furthermore, better security and compliance capabilities are becoming increasingly vital in this software as companies handle sensitive data that needs protection.

- Geographical Trends: North America has been dominating this industry owing to superior technical infrastructure, high adoption rates of novel solutions, and the presence of large software corporations. Other regions are also experiencing tremendous development as a result of increased digital transformation initiatives and the widespread adoption of remote work practices.

- Competitive Landscape: Some of the major market players in the team collaboration software industry include Adobe Inc., AT&T Inc, Avaya Inc., Blackboard Inc. (Anthology Inc.), Cisco Systems Inc., Citrix Systems Inc, International Business Machines Corporation, Microsoft Corporation, Open Text Corporation, Oracle Corporation, Slack Technologies LLC (Salesforce Inc.), and SMART Technologies ULC (Hon Hai Precision Industry Co. Ltd.), among many others.

- Challenges and Opportunities: Ensuring data security and compliance with several industry-specific and regional requirements is posing significant hurdles, as they can be complex and resource-intensive. Nonetheless, the industry has the potential to expand as more sophisticated features, like automation and AI-driven insights, are developed. These features can improve user experience and efficiency.

To get more information on this market Request Sample

Team Collaboration Software Market Trends:

Demand for Efficiency and Centralization

Companies are facing rising pressure to streamline workflows and minimize wasted time toggling between applications. Collaboration software provides a centralized space where projects, conversations, and documents can be managed collectively. By cutting down on repetitive manual updates and miscommunication, these platforms offer efficiency gains that directly affect output and cost savings. As global operations expand, shared visibility into project status and resource use becomes essential, and centralized systems make it easier to maintain consistency in communication and workflows. Integrations with existing software are also valued, as they lower the burden of repetitive updates. In 2024, Zoom launched Zoom Workplace, an AI-powered collaboration platform that unified meetings, chat, document collaboration, and workplace management into a single hub. It enhanced productivity with features like AI Companion, multi-share, continuous chat, and integrated workspace tools. The platform supported flexible work and integrated with over 2,500 third-party apps, illustrating the importance of collaboration tools in digital transformation strategies.

Rising Focus on Employee Experience

Employee satisfaction and retention are crucial for business performance, and collaboration software is seen as a tool to enhance the workplace. Tools that minimize obstacles in communication, enable flexible access on various devices, and facilitate asynchronous work empower employees to feel more in charge of their schedules. These attributes are especially appreciated in knowledge-based sectors, where innovation and solutions flourish when unnecessary obstacles are eliminated. Younger workers joining the workforce anticipate digital tools that resemble the ease of use found in user apps, turning intuitive collaboration platforms into a competitive edge for attracting talent. Organizations acknowledge that enhanced collaboration leads to reduced frustration, faster decision-making, and improved team unity. As companies compete for skilled workers, investment in tools that enhance the employee experience is seen as a way to boost engagement and loyalty, while simultaneously improving productivity.

Shift Toward Remote and Hybrid Work

The rapid move to distributed work environments is driving the need for seamless communication across teams that may never share the same physical space. Organizations now prioritize tools that support real-time messaging, video conferencing, and file sharing in one environment to reduce friction. Instead of relying on fragmented systems, businesses want integrated platforms that help teams stay aligned, regardless of location. This structural shift is catalyzing the demand for collaboration platforms, as they are no longer optional but essential infrastructure for day-to-day productivity. In 2024, Lucid Software announced new AI-powered features to enhance team collaboration, including team hubs for centralized project coordination and AI-generated diagrams in Lucidchart. The updates aimed to streamline workflows, improve alignment, and boost productivity, especially in hybrid work environments. Integration with Microsoft Copilot also enabled AI-powered document summaries. Such enhancements reflect how collaboration software is evolving to support long-term remote work strategies and reinforce alignment, productivity, and clarity within distributed teams.

Team Collaboration Software Market Growth Drivers:

Integration with Emerging Technologies

Collaboration software is evolving rapidly through the integration of AI, automation, and cloud technologies. These advancements enhance productivity by minimizing repetitive tasks and offering contextual support, such as smart meeting summaries, AI-generated task suggestions, and automated scheduling. Cloud-based platforms add further value by ensuring access across locations and devices without requiring extensive information technology (IT) infrastructure. Organizations are increasingly adopting solutions that not only facilitate teamwork but also function as intelligent systems capable of improving decision-making and operational flow. Integration with tools used in development, client management, and enterprise planning is expanding the scope of collaboration platforms. In 2024, Miro launched Innovation Workspace, an AI-powered collaboration platform aimed at streamlining product design and innovation. It featured tools like AI Sidekick, Catch-up summaries, and deep integrations with tools like Jira and Adobe Express. The platform repositioned Miro beyond whiteboarding into a full innovation lifecycle solution for enterprise teams.

Expansion of Subscription-Based Models

The shift toward subscription-based pricing, which offers organizations predictable costs and scalable access to advanced collaboration tools, is impelling the market growth. This model reduces the financial barrier for adoption by eliminating heavy upfront investments and allows companies to tailor subscriptions according to workforce size and evolving needs. Vendors benefit from recurring revenue streams, enabling continuous product development and feature upgrades that keep platforms competitive. For businesses, the flexibility of adding or reducing licenses ensures alignment with budgetary constraints and growth cycles. This approach is becoming central to digital transformation strategies, making subscription-based offerings a powerful driver of collaboration software market growth. In 2024, Alibaba’s DingTalk launched DingTalk 365, a subscription-based AI workplace collaboration suite featuring tools like AI-powered search, a virtual meeting assistant, and project tracking support. The service enhanced productivity through automation and intelligent summaries, priced at 339 yuan/year.

Rising Adoption by Small and Medium Enterprises

Small and medium enterprises (SMEs) are progressively embracing collaboration platforms as part of broader efforts to modernize their operations and remain competitive. Due to tight budgets and small teams, SMEs take advantage of cost-effective cloud-based subscription services that remove the requirement for significant capital outlays in IT infrastructure. These tools unify communication, task coordination, and file sharing, allowing for enhanced operational oversight with reduced resources. SMEs utilize collaboration software to improve client interaction, facilitate remote or hybrid teams, and guarantee consistent project execution. As business conditions become more challenging, smaller companies look for platforms that provide the adaptability to expand while ensuring effective workflows and high professional standards. This need is encouraging software providers to customize their solutions, including both features and costs, to align more closely with the requirements of smaller organizations.

Team Collaboration Software Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on components, software type, deployment, and industry vertical.

Breakup by Components:

- Solution

- Service

Solution accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the components. This includes solution and service. According to the report, solution represented the largest segment.

As per the team collaboration market analysis and forecast, solutions represented the largest market share, driven by the extensive adoption of collaboration tools such as video conferencing, instant messaging, document management, and project management software. These solutions offer comprehensive features that streamline communication, enhance productivity, and facilitate seamless collaboration across teams, making them indispensable for modern businesses. Moreover, the increasing demand for integrated platforms that combine multiple functionalities into a single interface is propelling the market growth.

Breakup by Software Type:

- Conferencing

- Communication and Co-Ordination

Communication and co-ordination hold the largest share of the industry

A detailed breakup and analysis of the market based on the software type have also been provided in the report. This includes conferencing and communication and co-ordination. According to the report, communication and co-ordination accounted for the largest market share.

Based on the team collaboration software market research report and insights, communication and co-ordination accounted for the largest market share. This is attributed to the essential role of communication and co-ordination tools in facilitating seamless interaction and collaboration among team members, regardless of their location. They include tools like instant messaging, email integration, shared calendars, and collaboration platforms for maintaining continuous and effective communication within organizations. Moreover, the widespread adoption of remote and hybrid work models, amplifying the demand for robust communication and co-ordination software, is boosting the team collaboration software market growth.

Breakup by Deployment:

- On-Premises

- Cloud-based

On-premises represents the leading market segment

The report has provided a detailed breakup and analysis of the market based on the deployment. This includes on-premises and cloud-based. According to the report, on-premises represented the largest segment.

According to the team collaboration software market outlook, on-premises deployment constituted the largest segment. The growing popularity of this deployment mode among large enterprises and organizations with stringent data security and compliance requirements is fueling the market growth. Moreover, it allows companies to host their collaboration software on their servers, providing them with complete control over their data and infrastructure. Besides this, the rising ability to customize and integrate the software with existing systems is catalyzing the market growth. Additionally, the growing preference for on-premises solutions among industries, such as finance, healthcare, and government, to ensure compliance with regulatory standards and to maintain high levels of data confidentiality is positively impacting the team collaboration software market revenue.

Breakup by Industry Vertical:

Access the comprehensive market breakdown Request Sample

- BFSI

- Manufacturing

- Healthcare

- IT and Telecommunications

- Retail and E-commerce

- Government and Defense

- Media and Entertainment

- Education

- Others

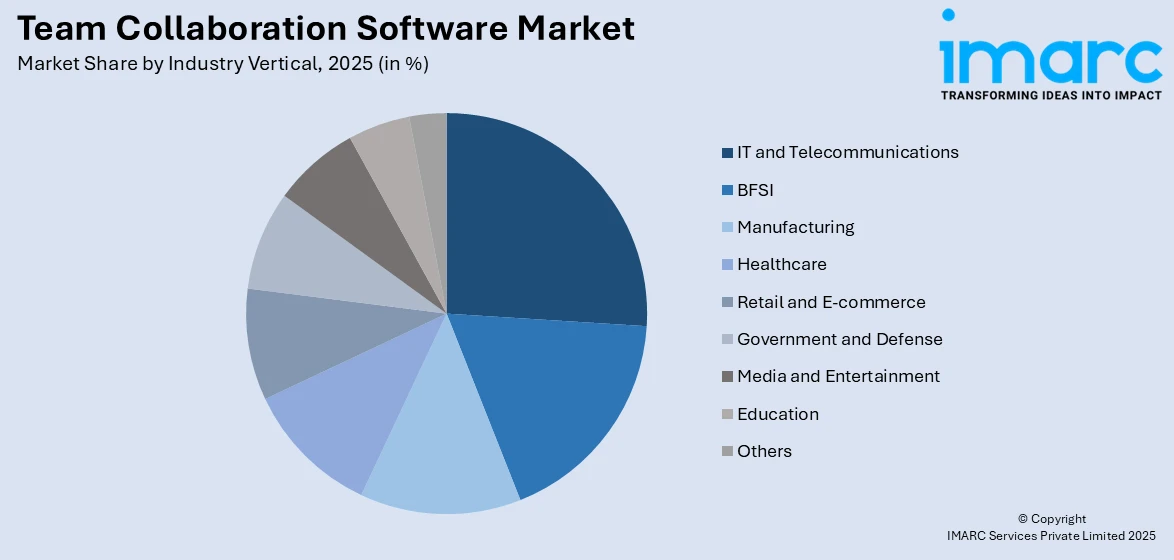

IT and telecommunications exhibit a clear dominance in the market

A detailed breakup and analysis of the market based on the industry vertical have also been provided in the report. This includes BFSI, manufacturing, healthcare, IT and telecommunications, retail and e-commerce, government and defense, media and entertainment, education, and others. According to the report, IT and telecommunications accounted for the largest market share.

As per the team collaboration software industry report and outlook, information technology (IT) and telecommunications accounted for the largest market share. This is driven by the industry's inherent need for efficient and effective communication tools to manage complex projects and coordinate among distributed teams. Moreover, the growing need for robust collaboration software as technology companies operate on a global scale with employees and stakeholders spread across different geographies is creating a positive outlook for the market. These tools enable seamless communication, real-time collaboration, and streamlined project management, which are critical for maintaining productivity and innovation in such a dynamic and fast-paced environment.

Breakup by Region:

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America leads the market, accounting for the largest team collaboration software market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, North America represents the largest regional market for team collaboration software.

North America is dominating this market, attributed to the region's advanced technological infrastructure, high adoption rate of innovative solutions, and a significant concentration of leading software companies. Moreover, the presence of major players that drive continuous innovation and development in collaboration tools, thereby catering to the diverse needs of businesses across various industries, is fueling the market growth. Additionally, the widespread adoption of remote and hybrid work models, accelerating the demand for robust collaboration software, is enhancing the market growth. Besides this, the heightened prioritization of organizations on seamless communication, productivity, and efficient project management is contributing to the market growth.

Competitive Landscape:

- The market research report has also provided a comprehensive analysis of the competitive landscape in the market. Detailed profiles of all major companies have also been provided. Some of the major market players in the team collaboration software industry include Adobe Inc., AT&T Inc, Avaya Inc., Blackboard Inc. (Anthology Inc.), Cisco Systems Inc., Citrix Systems Inc, International Business Machines Corporation, Microsoft Corporation, Open Text Corporation, Oracle Corporation, Slack Technologies LLC (Salesforce Inc.), SMART Technologies ULC (Hon Hai Precision Industry Co. Ltd.), etc.

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

- The major players in the market are continuously innovating and enhancing their product offerings to maintain a competitive edge and meet the evolving demands of businesses. They have been integrating advanced features like AI-driven meeting insights, task automation, and improved security protocols to enhance user experience and productivity. Moreover, some companies are focusing on expanding their integrations with other enterprise tools and improving their workflow automation capabilities. Besides this, they are enhancing their collaboration features, such as real-time editing and smart suggestions, to facilitate seamless teamwork. Apart from this, some are investing in advanced video conferencing technologies, incorporating AI for noise cancellation, real-time transcription, and enhanced security measures to cater to the increasing demand for remote communication solutions.

Team Collaboration Software Market News:

- In August 2025, Anthropic launched a major update to its developer platform, enhancing collaboration and control for its Claude 3.7 Sonnet AI model. The new Anthropic Console allows cross-functional teams to co-develop prompts and manage extended reasoning modes for deeper problem-solving whil e controlling costs. This shift aims to democratize AI development across technical and non-technical users in enterprises.

- In July 2025, MoirAI Cloud launched its first AI-powered app, MoirAI Chat, a collaborative chat tool with built-in Teams functionality. Designed for real-time group collaboration with AI, it runs on MoirAI’s energy-efficient cloud platform, which cuts data center energy use by up to 95%. The launch marks a milestone for sustainable, AI-native infrastructure.

- In March 2025, Zoho launched Projects Plus, an AI-rich, data-driven project management platform designed for mid-sized and enterprise organizations. It integrates Zoho Projects, WorkDrive, Sprints, and Analytics to support hybrid workflows, team collaboration, and predictive insights. Projects Plus enhances efficiency, resource planning, and cross-department visibility for complex projects.

- In March 2025, Motif launched a cloud-based collaboration platform tailored for architects and engineering trams, enabling real-time design review through integrated 2D and 3D workflows. It supports live model streaming from tools like Revit and Rhino, in-browser markups, and accessible web-based participation. The platform aims to streamline feedback and eliminate costly software barriers for stakeholders.

- In March 2024, Adobe and Microsoft announced plans to bring Adobe Experience Cloud workflows and insights to Microsoft Copilot for Microsoft 365. This will help marketers overcome application and data silos and more efficiently manage everyday workflows. These new integrated capabilities will bring relevant marketing insights and workflows from Adobe Experience Cloud applications and Microsoft Dynamics 365 to Microsoft Copilot, assisting marketers as they work in tools such as Outlook, Microsoft Teams, and Word to develop creative briefs, create content, manage content approvals, deliver experiences, and more.

- In October 2023, Cisco revealed the latest progress in collaborating with NVIDIA to provide AI-enhanced meetings for hybrid employees. Cisco introduced Room Kit EQX and expanded its Cinematic Meetings features, utilizing NVIDIA's AI technology to improve collaboration through advanced audio and video capabilities for more inclusive hybrid meetings.

Team Collaboration Software Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Solution, Service |

| Software Types Covered | Conferencing, Communication and Co-Ordination |

| Deployments Covered | On-premises, Cloud-based |

| Industry Verticals Covered | BFSI, Manufacturing, Healthcare, IT and Telecommunications, Retail and E-commerce, Government and Defense, Media and Entertainment, Education, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Adobe Inc., AT&T Inc, Avaya Inc., Blackboard Inc. (Anthology Inc.), Cisco Systems Inc., Citrix Systems Inc, International Business Machines Corporation, Microsoft Corporation, Open Text Corporation, Oracle Corporation, Slack Technologies LLC (Salesforce Inc.), SMART Technologies ULC (Hon Hai Precision Industry Co. Ltd.), etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the team collaboration software market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global team collaboration software market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the team collaboration software industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Team Collaboration Software Market Report

The global team collaboration software market was valued at USD 21.5 Billion in 2025.

We expect the global team collaboration software market to exhibit a CAGR of 10.67% during 2026-2034.

The sudden outbreak of the COVID-19 pandemic has led to the growing adoption of team collaboration software across numerous organizations for making work more transparent and efficient, while maintaining business continuity, during the remote working scenario.

The rising deployment of team collaboration software for day-to-day business operations, that allows teams to interact from any location on the cloud, which boosts productivity with enhanced security, is primarily driving the global team collaboration software market.

Based on the components, the global team collaboration software market has been segmented into solution and service. Currently, solution holds the majority of the total market share.

Based on the software type, the global team collaboration software market can be divided into conferencing and communication and co-ordination, where communication and co-ordination currently exhibits a clear dominance in the market.

Based on the deployment, the global team collaboration software market has been categorized into on-premises and cloud-based. Currently, on-premises account for the majority of the global market share.

Based on the industry vertical, the global team collaboration software market can be segregated into BFSI, manufacturing, healthcare, IT and telecommunications, retail and e-commerce, government and defense, media and entertainment, education, and others. Among these, the IT and telecommunication industry holds the largest market share.

On a regional level, the market has been classified into North America, Asia-Pacific, Europe, Latin America, and Middle East and Africa, where North America currently dominates the global market.

Some of the major players in the global team collaboration software market include Adobe Inc., AT&T Inc, Avaya Inc., Blackboard Inc. (Anthology Inc.), Cisco Systems Inc., Citrix Systems Inc, International Business Machines Corporation, Microsoft Corporation, Open Text Corporation, Oracle Corporation, Slack Technologies LLC (Salesforce Inc.), and SMART Technologies ULC (Hon Hai Precision Industry Co. Ltd.).

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)