Telecom Order Management Market Size, Share, Trends and Forecast by Component, Deployment Mode, Organization Size, Network Type, and Region, 2026-2034

Telecom Order Management Market Size, Share, Trends & Forecast (2026-2034)

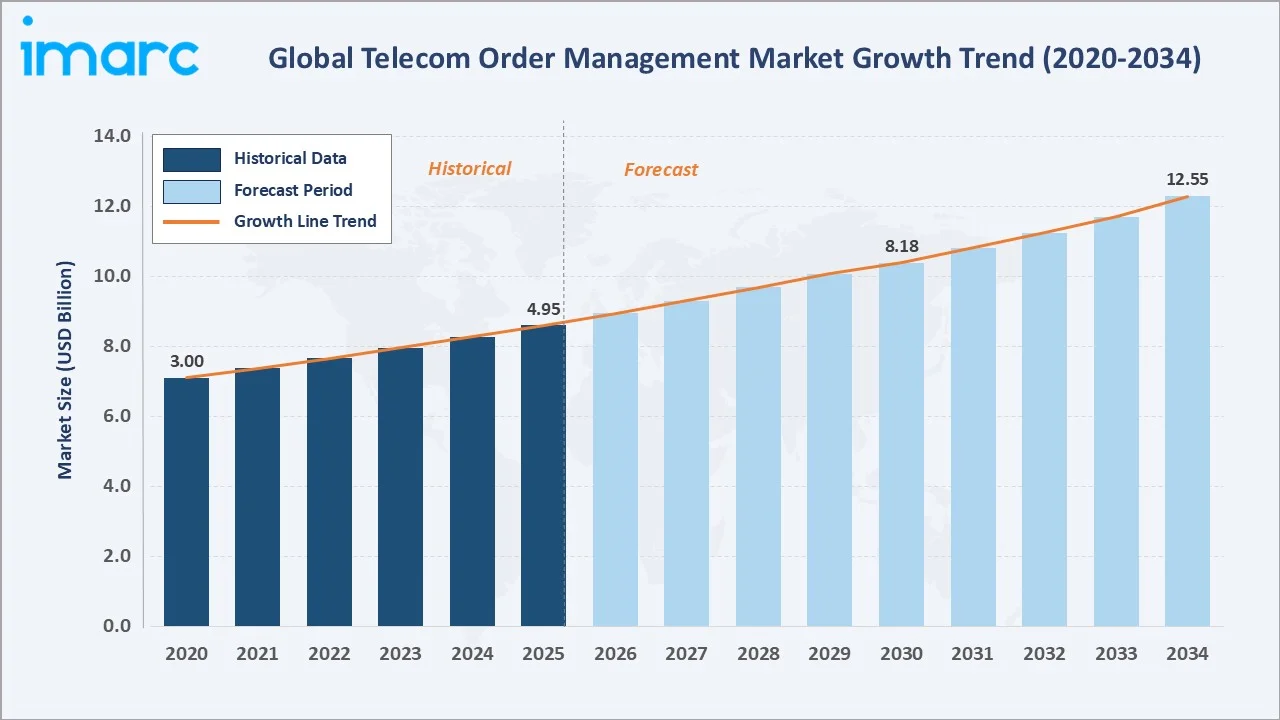

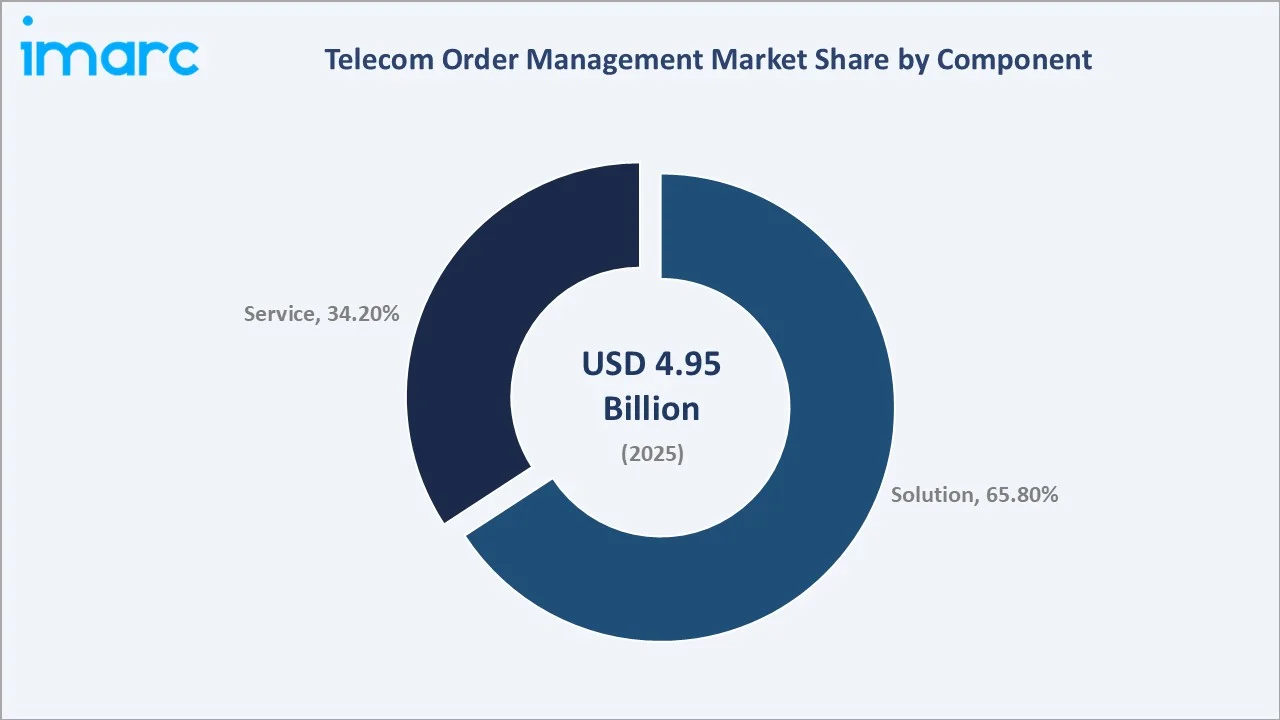

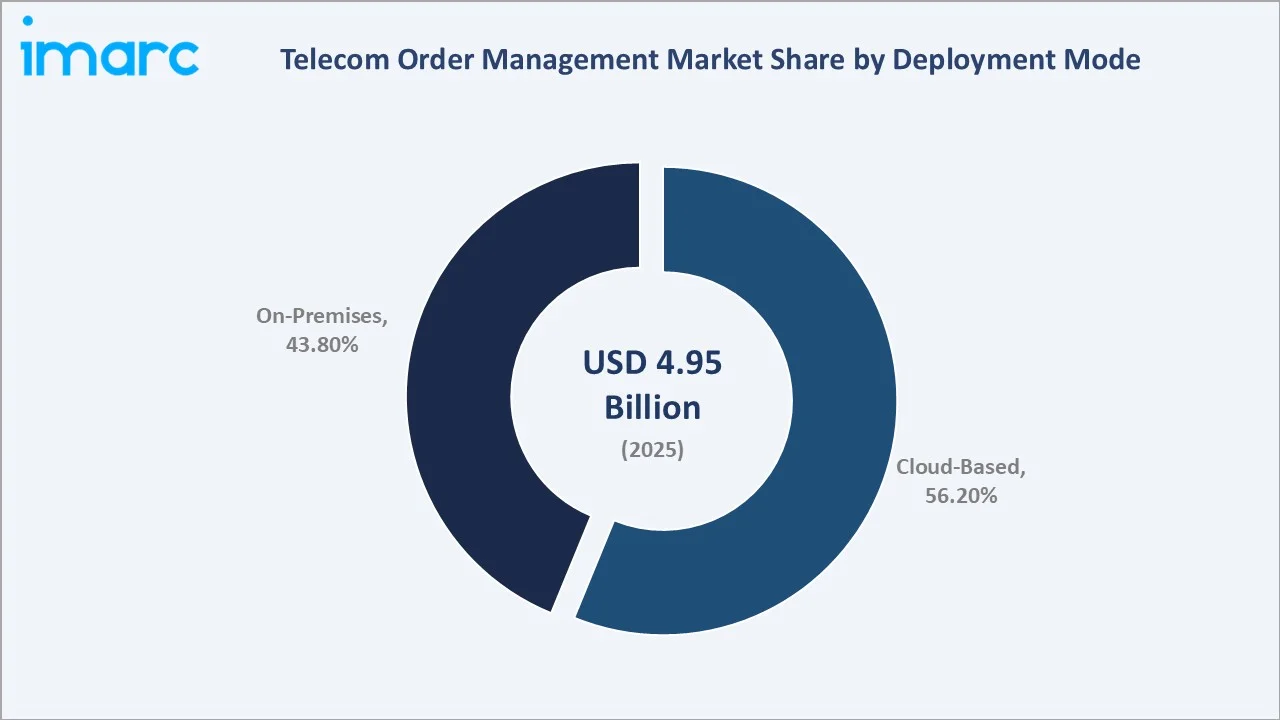

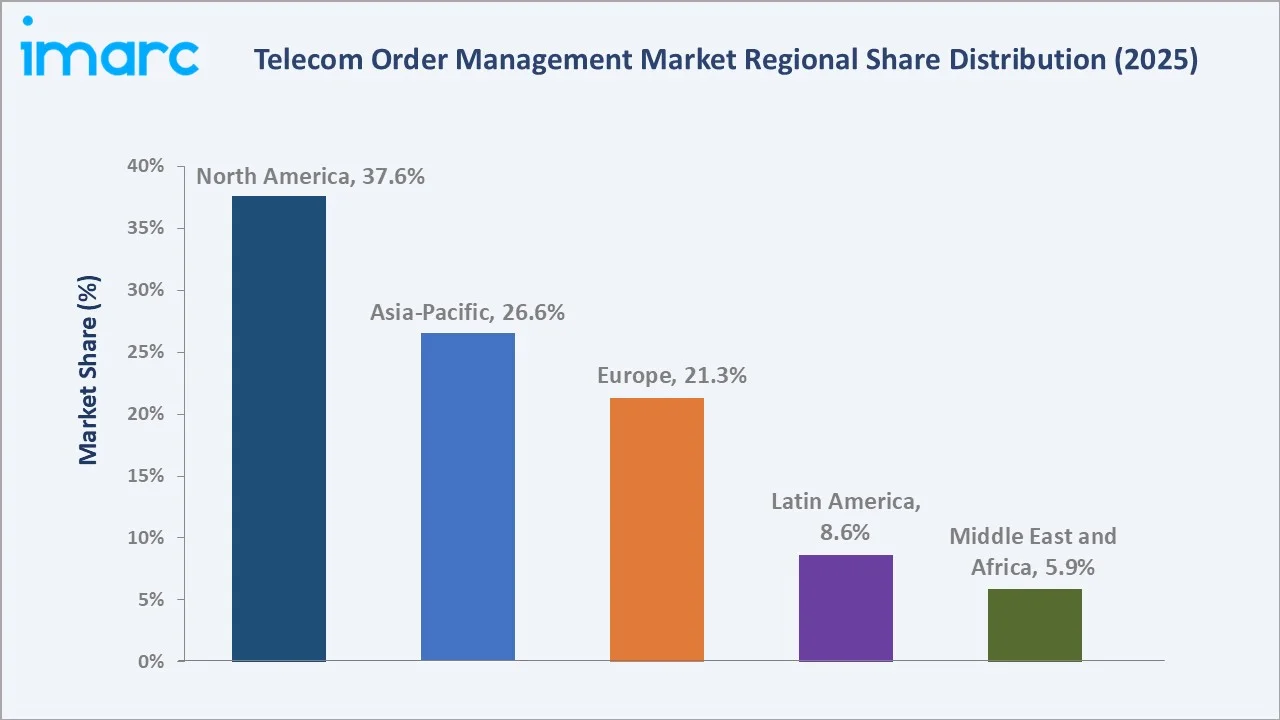

The global telecom order management market size was valued at USD 4.95 Billion in 2025 and is projected to reach USD 12.55 Billion by 2034, exhibiting a CAGR of 10.55% during the forecast period 2026-2034. The accelerating global rollout of 5G networks with around 360 networks launched worldwide, the rapid adoption of cloud-based operations support systems (OSS), and the integration of artificial intelligence and machine learning into order orchestration workflows are the primary drivers of telecom order management market growth. The Solution component dominates with a 65.8% share in 2025, while cloud-based deployment has overtaken on-premises with a 56.2% share in 2025. North America leads regional demand at 37.6% in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 4.95 Billion |

|

Forecast Market Size (2034) |

USD 12.55 Billion |

|

CAGR (2026-2034) |

10.55% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (37.6% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific (CAGR ~13.4%) |

|

Leading Component |

Solution (65.8%, 2025) |

|

Leading Deployment Mode |

Cloud-Based (56.2%, 2025) |

The telecom order management market growth trajectory from 2020 through 2034, capturing steady historical expansion and a sharply accelerating forecast curve propelled by 5G network complexity, digital BSS transformation, and the shift to cloud-native order management platforms.

To get more information on this market, Request Sample

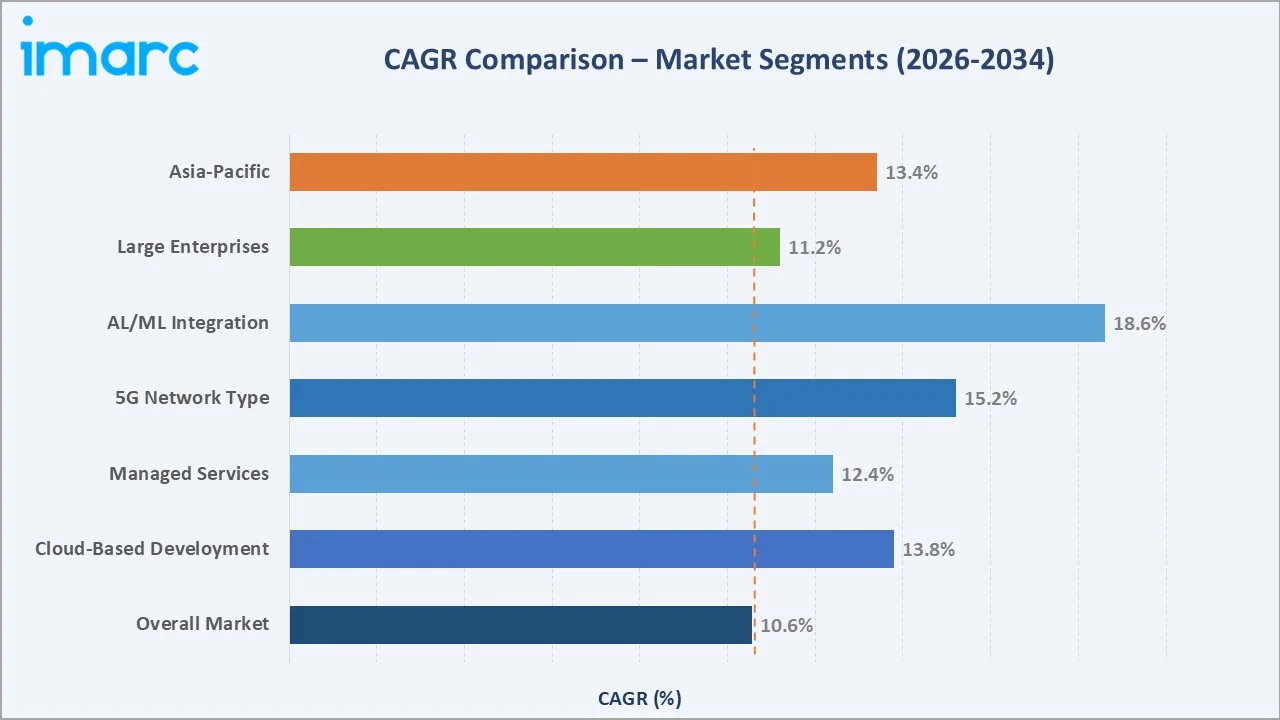

The CAGR trajectories across key segments and technologies, with AI/ML-integrated order management and cloud-based deployment emerging as the highest-growth categories within the global telecom order management industry analysis through 2034.

Executive Summary

The global telecom order management market is at the forefront of a digital transformation wave reshaping how Communications Service Providers (CSPs) capture, process, and fulfil customer orders across voice, data, and emerging next-generation service portfolios. Valued at USD 4.95 Billion in 2025, the market is forecast to reach USD 12.55 Billion by 2034 at a CAGR of 10.55%. The 5G network rollout is a primary structural driver, with GSMA estimating over 2 billion 5G connections globally by 2025 and 5.3 billion by 2030, as each 5G service introduces exponentially more complex order orchestration requirements compared to legacy 4G subscriptions.

The Solution component leads with a 65.8% market share in 2025, encompassing order capture, order decomposition, orchestration, and fulfilment software platforms. The Service segment (34.2%) includes professional services, managed services, and system integration that are critical for CSPs migrating from legacy OSS/BSS stacks to modern cloud-native architectures. Cloud-based deployment has overtaken on-premises with a 56.2% majority share in 2025, a decisive inflection point reflecting the telecom industry's migration toward scalable, API-first BSS platforms.

North America dominates the global telecom order management market share at 37.6% in 2025, driven by T-Mobile, AT&T, and Verizon's large-scale 5G deployment investments and their digital BSS modernization programs. Asia-Pacific follows at 26.6% and is the fastest-growing region at ~13.4% CAGR, driven by China, Japan, South Korea, and India's aggressive 5G rollouts.

Key Market Insights

|

Insight |

Data |

|

Largest Component |

Solution - 65.8% share (2025) |

|

Leading Deployment Mode |

Cloud-Based - 56.2% share (2025) |

|

Leading Region |

North America - 37.6% revenue share (2025) |

|

Second Region |

Asia-Pacific - 26.6% revenue share (2025) |

|

Key Technology Driver |

5G Network Rollout & Service Complexity |

|

Top Companies |

Oracle, Amdocs, Netcracker, Huawei, Nokia, Comarch |

Key Analytical Observations Supporting The Above Data:

- The Solution segment's 65.8% market dominance in 2025 reflects the strategic priority CSPs place on software platforms that automate order capture-to-fulfilment workflows.

- Cloud-based deployment at 56.2% in 2025 represents a structural inflection point, having surpassed on-premises for the first time in the market's history.

- North America's 37.6% dominance reflects AT&T's 5G capital program, T-Mobile's nationwide 5G SA rollout, and Verizon's enterprise 5G private network business, all requiring sophisticated, high-throughput order management platforms capable of processing complex multi-service bundles in real-time.

- Asia-Pacific's 26.6% share and ~13.4% CAGR leadership reflects the region's 5G investment scale. The number of 5G base stations in China reached 4.838 million by 2025, with China Mobile, China Unicom, and China Telecom all undergoing large-scale BSS/OSS transformation programmes to support 5G SA order complexity.

Global Telecom Order Management Market Overview

Telecom order management refers to the end-to-end business process and supporting software systems that manage customer orders for telecommunications services, from initial order capture through decomposition, validation, orchestration, provisioning, and final order completion confirmation. Modern telecom order management platforms integrate with billing systems, CRM platforms, network inventory, and service provisioning engines to create a unified, automated order-to-activate workflow.

Applications span consumer mobile and broadband service activation, enterprise B2B connectivity orders (MPLS, SD-WAN, private 5G), IoT device provisioning, wholesale carrier services, and increasingly complex multi-service bundles combining cloud, connectivity, and managed services.

The market is governed by TM Forum Open API standards, 3GPP service provisioning specifications, and CSP-specific enterprise architecture frameworks. Macroeconomic enablers include the 5G, which is expected to accelerate global GDP growth and enable a $1.5 Trillion revenue potential by 2030, and the shift toward digital-first customer interactions requiring real-time order processing.

Market Dynamics

To evaluate market opportunities, Request Sample

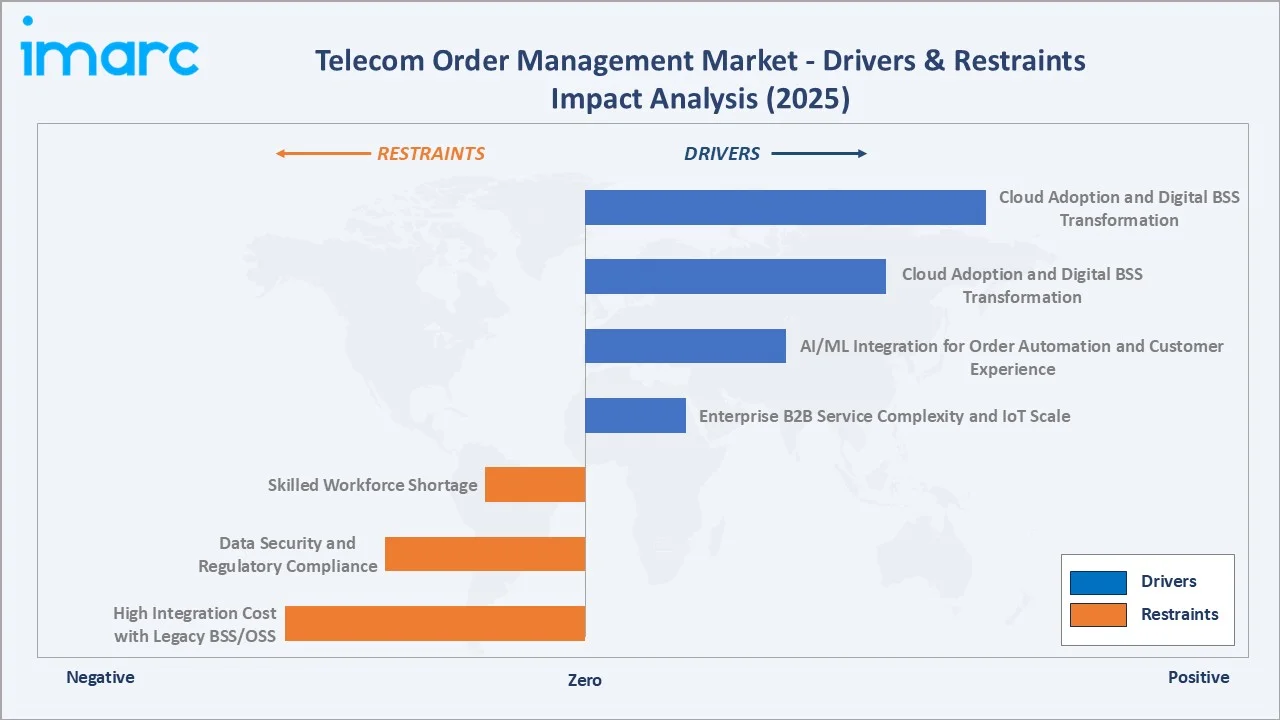

Market Drivers

- 5G Network Rollout and Service Complexity: The global 5G rollout is the single most powerful growth catalyst for the telecom order management market. 5G Standalone (SA) architecture introduces network slicing, dynamic QoS, and programmable service APIs that require fundamentally new order decomposition and orchestration capabilities. GSMA forecasts 5.3 billion 5G connections by 2030.

- Cloud Adoption and Digital BSS Transformation: CSPs globally are accelerating the migration of legacy OSS/BSS stacks to cloud-native, microservices-based platforms.

- AI/ML Integration for Order Automation and Customer Experience: Telecom operators are deploying AI-powered order management to eliminate manual exception handling, predict order fallout risks before they occur, and provide real-time status transparency to customers.

- Enterprise B2B Service Complexity and IoT Scale: B2B telecom services, private 5G networks, SD-WAN, multi-site MPLS, and managed services involve hundreds of individual service component orders per enterprise contract. IoT deployments add massive order volume scale: a single IoT platform deployment may require simultaneous provisioning of 100,000+ device connections.

Market Restraints

- High Integration Cost with Legacy BSS/OSS: Migrating from legacy order management systems, which may have been in production for 15-20 years at incumbent operators, to modern cloud-native platforms involves complex, multi-year transformation programmes, costs high.

- Data Security and Regulatory Compliance: Order management systems process sensitive customer personal data, enterprise connectivity configurations, and financial billing information.

- Skilled Workforce Shortage: Modern cloud-native order management platforms require expertise spanning telecom domain knowledge, cloud architecture, DevOps, API development, and AI/ML model management.

Market Opportunities

- 5G Managed Services for Emerging Market CSPs: Smaller CSPs in emerging markets, Southeast Asia, Africa, and Latin America, lack the capital and engineering talent to build in-house cloud-native order management capabilities.

- Intent-Based and Self-Healing Order Management: Next-generation order management platforms are evolving toward intent-based architectures where customer service specifications are automatically translated into network provisioning instructions without manual order decomposition.

Market Challenges

- Legacy System Technical Debt: Many CSPs operate monolithic order management systems built on COBOL, J2EE, or early-generation .NET architectures that are deeply intertwined with billing and provisioning platforms.

- Real-Time Order Processing at 5G Scale: 5G mass IoT scenarios, smart city deployments, connected vehicle fleets, industrial IoT, require order management platforms to process millions of concurrent provisioning requests with sub-second latency.

Emerging Market Trends

The telecom order management market trends analysis identifies five structural forces reshaping platform architectures, vendor positioning, and CSP adoption patterns across the 2026-2034 forecast period.

1. Cloud-Native and Microservices-Based Order Management Replacing Monolithic Platforms

The architectural shift from monolithic, proprietary order management systems to cloud-native, microservices-based platforms is the defining structural trend of the 2025-2030 era. Dell Technologies' 2025 Open Telecom Transformation Program is a landmark industry initiative accelerating this migration, offering CSPs pre-integrated cloud BSS stacks on major public cloud platforms.

2. AI-Driven Order Fallout Management and Self-Healing Capabilities

Order fallout, where orders fail to complete automatically due to system errors, data quality issues, or network capacity constraints, costs more in manual intervention costs. AI-powered order fallout management systems, using machine learning to predict, diagnose, and automatically resolve exceptions, are reducing fallout rates from 15-25% to below 3% at deploying CSPs.

3. 5G Network Slicing and Dynamic Service Orchestration

5G Standalone architecture's network slicing capability requires order management platforms to dynamically create, modify, and delete virtual network slices in response to enterprise customer service requests, often within seconds. This demands real-time order orchestration capabilities that legacy systems cannot deliver.API-First Order Management and Open Ecosystem Integration

TM Forum's Open API initiative, with 60+ standardized APIs covering order management, product catalog, billing, and provisioning, is enabling CSPs to compose best-of-breed order management ecosystems from multiple vendor components.

4. Real-Time Order Visibility and Customer Self-Service

Customer expectations for real-time order status transparency, driven by the Amazon-standard of real-time delivery tracking, are forcing CSPs to build consumer-grade order tracking interfaces on top of their back-office order management systems.

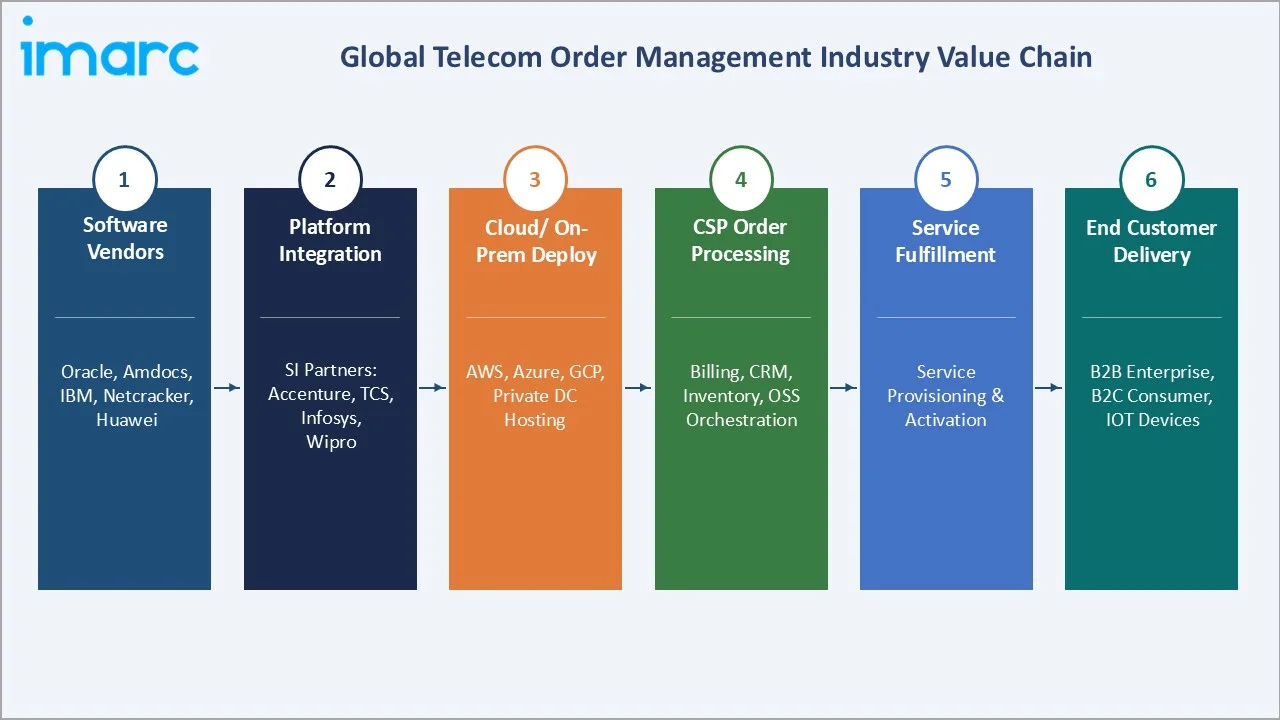

Industry Value Chain Analysis

The telecom order management industry value chain connects software platform development through system integration, deployment, CSP order processing operations, and ultimately end-user service delivery. Each stage reflects distinct competitive dynamics, margin profiles, and technology adoption patterns.

|

Stage |

Key Players / Examples |

|

Software Platform Vendors |

Oracle (COSM), Amdocs, Netcracker, Huawei (OSS), Nokia (NSP), Comarch |

|

System Integration & Consulting |

Accenture, TCS, Wipro, Cognizant, Capgemini – TM Forum API-certified SI partners |

|

Cloud & Infrastructure Providers |

AWS Telco (Connect), Microsoft Azure for Operators, Google Cloud Telecom, Private DC hosting |

|

CSP Order Processing Layer |

AT&T, T-Mobile, Verizon, Deutsche Telekom, Vodafone, China Mobile, Jio – BSS/OSS operators |

|

Service Fulfilment & Activation |

Network provisioning engines, eSIM/SIM activation platforms, IoT device management, SD-WAN portals |

|

End Customers |

B2C subscribers (voice, broadband, 5G), B2B enterprises (private networks, SD-WAN), IoT devices |

System integration partners occupy a structurally critical and high-margin position in the telecom order management value chain. Large-scale BSS/OSS transformation projects, which may span 3-5 years and USD 50-200 Million in professional services fees, are almost exclusively delivered through SI partners, including Accenture and TCS, who combine telecom domain expertise, platform certifications, and global delivery capability that individual software vendors cannot replicate.

Technology Landscape in the Telecom Order Management Industry

Cloud-Native and Microservices Architecture

Cloud-native order management platforms built on Kubernetes, Docker, and microservices architecture are the technology standard for new platform deployments in 2025. Red Hat OpenShift and VMware Tanzu are the leading containerization platforms for CSP BSS workloads.

Artificial Intelligence and Machine Learning Integration

AI/ML is transforming telecom order management across three primary application areas: (1) Predictive order fallout prevention; (2) Natural language processing (NLP) for automated order capture, and (3) Intelligent order routing, where AI dynamically assigns orders to optimal fulfilment paths based on network conditions and SLA requirements.

TM Forum Open APIs and Interoperability Standards

TM Forum's Open API standard, with over 60 APIs covering order management (OM Open API), product catalog (PC Open API), and service provisioning (SO Open API), has become the de-facto interoperability standard for modern telecom BSS integration.

5G Core and Network Slice Management Integration

Integration between order management platforms and 5G Core (5GC) network functions, specifically the Network Slice Management Function (NSMF) and Network Slice Subnet Management Function (NSSMF), is emerging as a critical technology capability for 5G SA-supporting order management systems. 3GPP Release 17 and 18 specifications define the northbound APIs through which order management platforms interact with 5GC for slice creation and modification.

Intent-Based Networking and Zero-Touch Provisioning

Intent-based networking (IBN), where high-level service intent is automatically translated into network configuration without manual order decomposition, is the emerging frontier for advanced order management platforms.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

Solution |

65.8% |

2025 |

|

Deployment mode |

Cloud-based |

🔒 |

2025 |

|

Organisation size |

Large Organization |

73.8% |

2025 |

|

Network type |

Wired |

🔒 |

2025 |

|

Region |

North America |

37.6% |

2025 |

By Component

The solution segment (customer order management, service order management, service inventory management) commands a 65.8% majority share of the telecom order management market in 2025, reflecting the strategic priority CSPs place on software platforms as the foundation of their order-to-activate workflows. Order management solution revenues span perpetual license, subscription SaaS, and consumption-based models. SaaS and subscription licensing, representing approximately 45% of Solution revenues in 2025.

To access detailed market analysis, Request Sample

The service segment at 34.2% in 2025 encompasses professional services (consulting, implementation, customization), managed services (outsourced order management operations), and training and support. Managed services are the fastest-growing service sub-segment at ~12.4% CAGR, as smaller CSPs in emerging markets outsource end-to-end order management operations to specialist vendors rather than building in-house capabilities.

By Deployment Mode

Cloud-based deployment has achieved majority share at 56.2% in 2025, a structural shift that marks the telecom industry's decisive migration away from on-premises order management infrastructure. This inflection reflects both the imperative of 5G service agility and the economics of cloud hosting, which reduces infrastructure capex by 30-50% versus equivalent on-premises deployments.

On-premises deployment retains a 43.8% share in 2025, primarily concentrated among large incumbent operators in regulated markets (Europe, China, India), operators with existing on-premises infrastructure investments in mid-lifecycle, and operators handling highly classified government or defence communications services with strict data sovereignty requirements.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

37.6% |

AT&T/T-Mobile/Verizon 5G SA, cloud BSS migration, enterprise private network growth |

|

Asia-Pacific |

26.6% |

China 5G scale, India Jio 5G expansion, Japan/Korea advanced services, SEA digital telcos |

|

Europe |

21.3% |

5G multi-operator sharing, GDPR-compliant cloud deployment, Deutsche Telekom/Vodafone BSS refresh |

|

Latin America |

8.6% |

América Móvil, Claro 5G deployments, Brazil/Mexico digital service expansion, managed services |

|

Middle East & Africa |

5.9% |

Saudi Vision 2030 smart city, STC/Etisalat 5G, Africa's first-generation 4G/5G digital BSS build |

North America commands a 37.6% global revenue share in 2025, the market's single largest region, anchored by the world's most advanced 5G SA deployments and the most mature digital BSS transformation programmes among major CSPs. T-Mobile provides extensive network coverage across the United States, reaching 99% of the population with 4G LTE and 98% with 5G, and serving a total of 142.4 million customers as of Q4 2025.

Asia-Pacific holds a 26.6% market share in 2025 and is the fastest-growing region at ~13.4% CAGR through 2034. By the end of 2025, China had built 4.838 million 5G base stations, according to the Ministry of Industry and Information Technology. This equates to 34.4 stations per 10,000 people, surpassing the national target by 8.4 units. India's Jio and Airtel 5G rollouts, covering 100+ cities by 2025 and Southeast Asia's rapidly growing digital telco sector are additional high-growth drivers.

Competitive Landscape

The telecom order management market is characterized by moderate concentration among established BSS platform vendors competing alongside specialist order management software providers and large technology conglomerates.

|

Company Name |

Platform / Brand |

Market Position |

Core Strength |

|

Oracle Corporation |

COSM / ASAP Order Mgt |

Leader |

TM Forum Open API, 5G cloud-native, SaaS expansion |

|

Amdocs Limited |

Amdocs Order Mgt Suite |

Leader |

End-to-end BSS/OSS, managed services, AI automation |

|

Netcracker (NEC) |

Netcracker Digital BSS |

Leader |

Full cloud BSS/OSS, 5G network automation, APAC strength |

|

Huawei Technologies |

Huawei OSS/BSS Suite |

Leader |

5G-native OM, China market dominance, emerging markets |

|

Nokia Corporation |

Nokia Network Services Platform |

Leader |

NSP 5G OM, Open API leadership, Europe + APAC |

|

Ericsson AB |

Ericsson Order Care / Ericsson Digital BSS |

Challenger |

5G OSS/BSS integration, zero-touch, SA networks |

|

Comarch SA |

Comarch BSS Suite |

Challenger |

Modular cloud BSS, Poland/CEE leadership, mid-tier CSPs |

|

TELARIX Inc. |

TELARIX iBill / iXLink |

Challenger |

Wholesale & inter-carrier OM, B2B order automation |

|

Cognizant Technology Solutions |

Cognizant Telecom OM |

Emerging |

SI-led OM transformation, TCS competitor |

Oracle and Amdocs together leads the global market revenue in 2025. The competitive positioning matrix for key telecom order management market participants, mapping market presence against strategic investment levels to reveal the structural distinction between global platform leaders, specialized challengers, and emerging SI-led players.

Key Company Profiles

Oracle Corporation

Oracle is the global leader in telecom order management with its Communications Order and Service Management (COSM) platform, part of the Oracle Communications portfolio serving 30+ of the world's top 50 CSPs.

- Platform & Product Portfolio: Oracle COSM (Communications Order and Service Management), Oracle Communications Digital Platform (CDP), Oracle Communications Service Activation (OCSA), Oracle Communications Billing and Revenue Management (BRM), and Oracle AI/ML-powered order fallout management module.

- Recent Developments: In October 2025, Oracle announced the general availability of Oracle AI Data Platform.

- Strategic Focus: Oracle's telecom order management strategy centers on three pillars: cloud-native migration (encouraging on-premises customers to Oracle Cloud), AI-native order orchestration (reducing operational costs for CSPs by 40-60%), and 5G SA service automation (enabling zero-touch network slice order management for enterprise private network customers).

Netcracker Technology (NEC)

Netcracker Technology, a wholly-owned subsidiary of NEC Corporation, is a leading global provider of BSS/OSS and cloud-native network management solutions. The company holds a particularly strong position in the Asia-Pacific market through NEC's deep telecommunications infrastructure relationships in Japan, South Korea, and Southeast Asia.

- Platform & Product Portfolio: Netcracker Digital BSS (including Order Management), Netcracker Network Automation, Netcracker Revenue Management, Netcracker 5G Orchestration, and Netcracker Cloud-Native Platform (based on Kubernetes and Red Hat OpenShift).

- Recent Developments: In November 2025, Netcracker Technology recognized as a Leader in the IDC MarketScape’s 2025 Vendor Assessment for Worldwide Customer Experience Platforms in the telecommunications sector.

- Strategic Focus: Netcracker's growth strategy prioritises APAC market expansion leveraging NEC's infrastructure relationships, cloud-native BSS migration for on-premises installed base customers, and the emerging BSS-as-a-Service market for mid-tier and emerging market CSPs seeking enterprise-grade order management without the capital investment of traditional licence deployments.

Huawei Technologies

Huawei Technologies is a global leader in telecommunications equipment, providing advanced BSS/OSS solutions for operators around the world.

- Product Portfolio: Known for its Huawei OSS/BSS Suite, Huawei leads in 5G-native operational management and telecom network solutions.

- Recent Developments: In October 2025, Omdia, in collaboration with Huawei and other industry partners, released the Telco Cloud Manifesto: Building an Intelligent Telco Cloud Infrastructure for Service Innovation in the Mobile AI Era.

- Strategic Focus: Huawei focuses on 5G technology and is positioning itself as a dominant player in emerging markets, with a particular emphasis on network automation and digital transformation for telecom operators.

Market Concentration Analysis

The telecom order management market exhibits moderate concentration among established BSS platform vendors, with significant fragmentation in the system integration and managed services layers. The top 3 vendors, Oracle and Amdocs, collectively account for approximately 40-48% of global market revenue in 2025.

The telecom order management market is experiencing a bifurcated consolidation dynamic. At the top tier, the three leading vendors, Oracle and Amdocs, are expanding their market share through managed services contracts that generate recurring revenue and deepen customer lock-in. Large-scale BSS transformation projects at Tier-1 CSPs have increasingly become multi-year managed services engagements rather than one-time licence sales, converting previously transactional relationships into long-duration commercial partnerships.

Investment & Growth Opportunities

Fastest-Growing Segments

AI/ML-integrated order management is the market's highest-growth investment theme at ~18.6% CAGR through 2034. Cloud-based deployment is the second-fastest-growing market dimension at ~13.8% CAGR through 2034. Investment in dedicated telco cloud platforms, combining cloud infrastructure, order management software, and DevOps tooling optimized for CSP workloads, is attracting capital from hyperscalers (AWS, Azure, GCP), infrastructure vendors (Dell, HPE), and pure-play telecom software companies.

Emerging Market Expansion

5G private network enterprise order management represents a high-value emerging sub-market. Enterprise 5G private networks, deployed at factories, stadiums, hospitals, and logistics centers, require complex, multi-domain order management integrating mobile, edge compute, and IoT connectivity. Wholesale and inter-carrier order automation is a structurally underpenetrated market. TM Forum's Catalyst initiative is standardising API-based B2B order exchange, and vendors offering automated inter-carrier order management platforms are targeting a first-mover advantage in a market that is estimated to shift 60%+ of volume to API-based automation by 2030.

Venture & Private Investment Trends

Notable transactions include Symphony Ventures' acquisition of Sigma Systems (cloud-native BSS), Marlin Equity's investment in TELARIX, and multiple venture rounds in cloud-native entrants including Etiya (Turkey), Optiva (Canada), and Tecnotree (Finland). Hyperscaler investment is also significant: AWS's Telco Partner Network, Microsoft's Azure for Operators programme, and Google's Global Mobile Edge Cloud provide funded incentives for telecom software vendors to build and deploy on their respective platforms, reducing customer acquisition costs and accelerating cloud migration.

Future Market Outlook (2026-2034)

The global telecom order management market forecast projects sustained expansion from USD 4.95 Billion in 2025 to USD 12.55 Billion by 2034 at a CAGR of 10.55%. This trajectory positions the market for a 2.5x revenue multiplication over the forecast period, driven by 5G service proliferation, enterprise digital connectivity demand, and the structural shift from capital-intensive on-premises systems to subscription-based cloud-native platforms.

Three technology discontinuities are most likely to reshape the telecom order management market through 2034. Intent-based, AI-autonomous order management, where customer service intent is automatically translated to network configuration without any manual decomposition or exception handling, is expected to reach commercial deployment at leading-edge CSPs by 2028-2030.

By 2034, the telecom order management market is expected to have completed its transformation from a back-office operational system to a front-line revenue enablement platform. Real-time order APIs will enable CSPs to offer programmable connectivity as a service, where enterprise customers configure, order, and activate network services through self-service portals with no human operator involvement.

Research Methodology

Primary Research

Primary research encompassed over 55 structured interviews conducted in 2024-2025 with telecom industry stakeholders, including BSS/OSS platform product managers, senior telecom transformation architects at Tier-1 CSPs, SI practice leaders at Accenture and TCS telecom practices, TM Forum technical committee members, and institutional investors in telecom software. Primary data validated market sizing, segmentation split estimates, competitive positioning, and technology adoption timelines.

Secondary Research

Secondary sources include TM Forum Annual Industry Reports, GSMA Intelligence 5G adoption and CSP investment reports, IDC Worldwide Telecom Software Market Tracker, Gartner Magic Quadrant for Communications Service Provider BSS Platforms, Ovum/Omdia BSS/OSS software market reports, vendor annual reports and investor presentations, 3GPP Release 17/18 service management specifications, and trade publications including Telecoms.com, Light Reading, and Total Telecom.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, urbanization indices, consumer expenditure data, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic uncertainty.

Telecom Order Management Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered |

|

| Deployment Modes Covered | On-premises, Cloud-based |

| Organization Sizes Covered | Large Organization, Small and Medium Organization |

| Network Types Covered | Wireless, Wired |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Oracle Corporation, Amdocs Limited, Netcracker (NEC), Huawei Technologies, Nokia Corporation, Ericsson AB, Comarch SA, TELARIX Inc., Cognizant Technology Solutions, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the telecom order management market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global telecom order management market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the telecom order management industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Telecom Order Management Market Report

The global telecom order management market was valued at USD 4.95 Billion in 2025.

The market is projected to reach USD 12.55 Billion by 2034, growing at a CAGR of 10.55% during 2026-2034, driven by 5G complexity, AI automation, and cloud-native BSS transformation.

The Solution segment leads with a 65.8% share in 2025, encompassing order management software platforms handling capture, decomposition, orchestration, and fulfilment workflows for global CSPs.

Cloud-based deployment at 56.2% in 2025 is growing at ~13.8% CAGR through 2034, having surpassed on-premises for the first time, driven by 5G agility requirements and cloud economics.

North America leads with a 37.6% revenue share in 2025, anchored by AT&T, T-Mobile, and Verizon's 5G SA deployments and large-scale digital BSS transformation investment programs.

Asia-Pacific is the fastest-growing region at ~13.4% CAGR through 2034, driven by China's vast 5G base station deployment, India's Jio 5G expansion, and SEA digital telco growth.

Key drivers include 5G network complexity requiring dynamic order orchestration, cloud-native BSS migration, AI/ML integration for automated fallout management, and enterprise B2B/IoT order volume growth.

Leading companies include Oracle (COSM), Amdocs, Netcracker (NEC), Huawei, Nokia (NSP), Ericsson, Comarch, etc., together serving 300+ CSPs globally.

5G SA introduces network slicing and programmable services requiring real-time, multi-domain order orchestration, making legacy rule-based systems obsolete and driving modern cloud-native OM adoption.

AI reduces order fallout from 15-25% to below 3%, automates exception handling, and enables predictive order management at 5G IoT scale.

TM Forum Open API provides 60+ standardized telecom OSS/BSS APIs covering order management, enabling interoperability between vendors and reducing integration costs by 20-30% per deployment.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)