Tire Pressure Monitoring System (TPMS) Market Size, Share, Trends and Forecast by Type, Technology, Vehicle Type, Distribution Channel, and Region, 2026-2034

Tire Pressure Monitoring System (TPMS) Market Size, Share, Trends & Forecast (2026-2034)

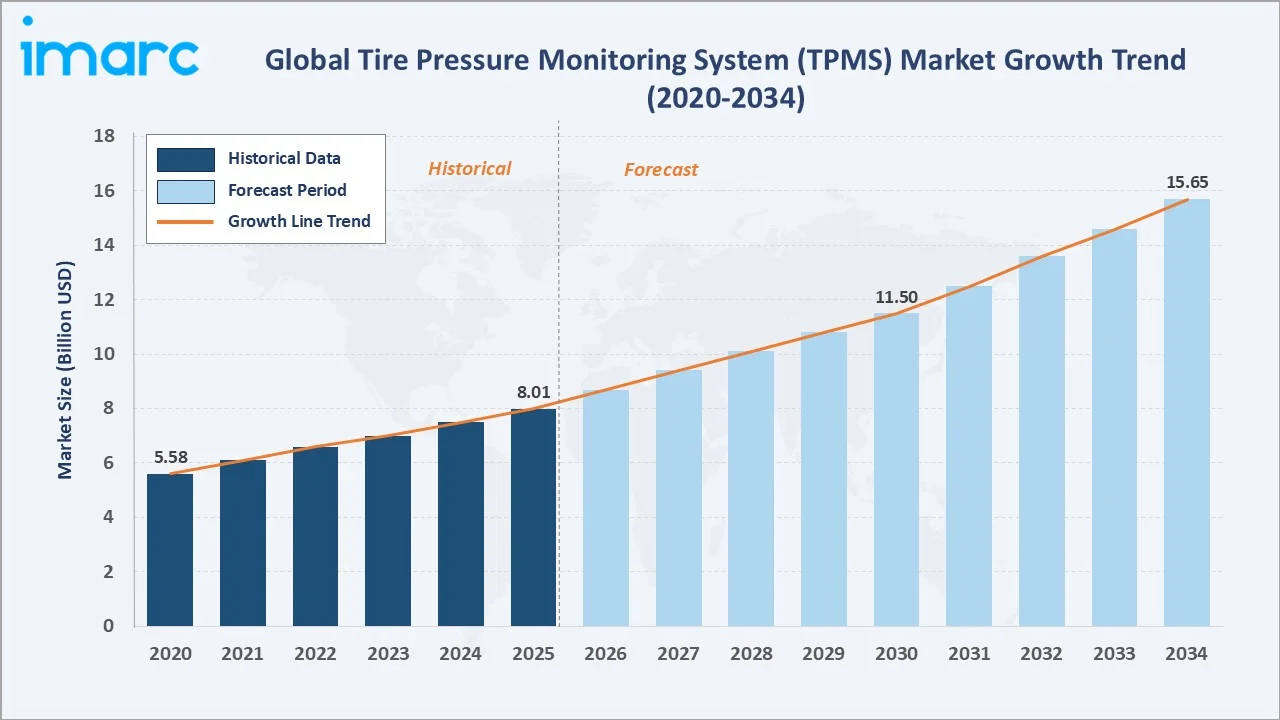

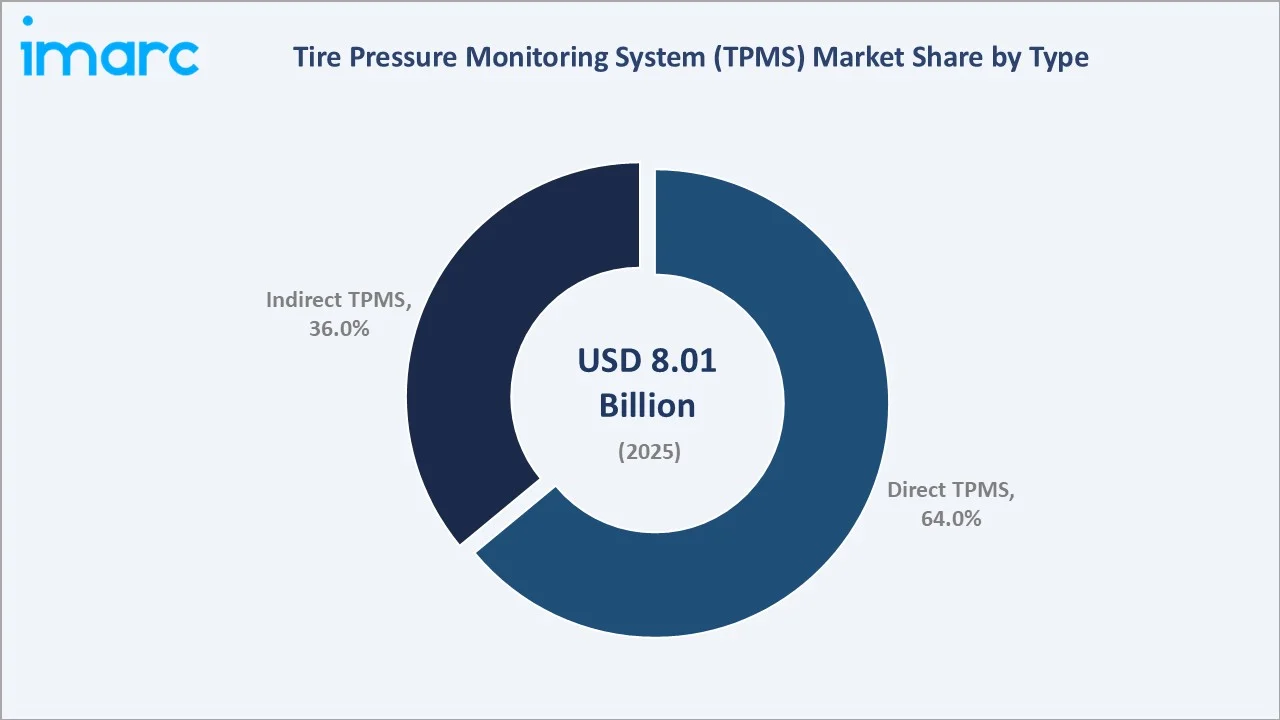

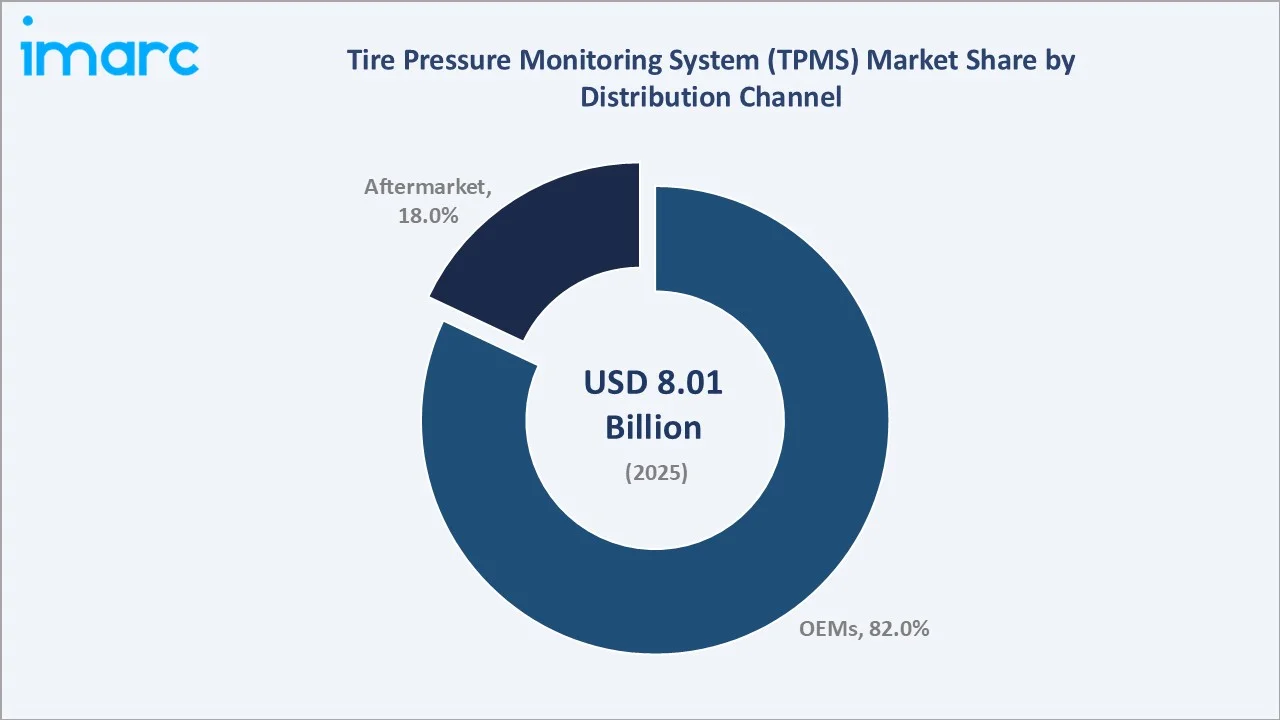

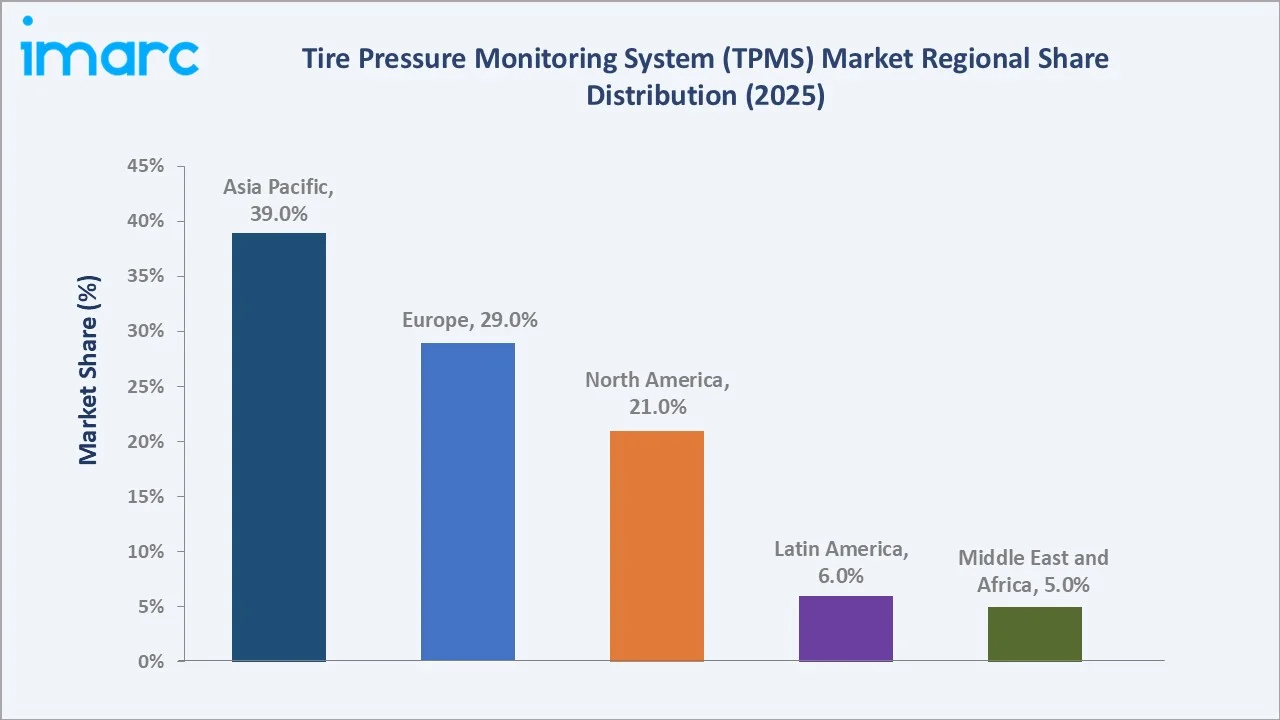

The global Tire Pressure Monitoring System (TPMS) market reached USD 8.01 Billion in 2025 and is projected to reach USD 15.65 Billion by 2034, growing at a CAGR of 7.49% during 2026-2034. The market is driven by mandatory government safety regulations, rising global vehicle production, and growing consumer awareness of road safety and fuel efficiency.

Direct TPMS dominates at 64.0%. OEMs lead distribution at 82.0%. Asia Pacific commands 39.0% of the global market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 8.01 Billion |

|

Forecast Market Size (2026-2034) |

USD 15.65 Billion |

|

CAGR (2034) |

7.49% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Direct TPMS (64.0%, 2025) |

|

Dominant Distribution Channel |

OEMs (82.0%, 2025) |

|

Leading Region |

Asia Pacific (39.0%, 2025) |

The global TPMS market expanded from USD 5.58 Billion in 2020 to USD 8.01 Billion in 2025, anchored at USD 11.50 Billion in 2030, and forecast to reach USD 15.65 Billion by 2034. Regulatory mandates in the US, EU, South Korea, Japan, and expanding Asian markets have created consistent OEM demand, while an aging vehicle fleet is driving aftermarket replacement growth.

To get more information on this market, Request Sample

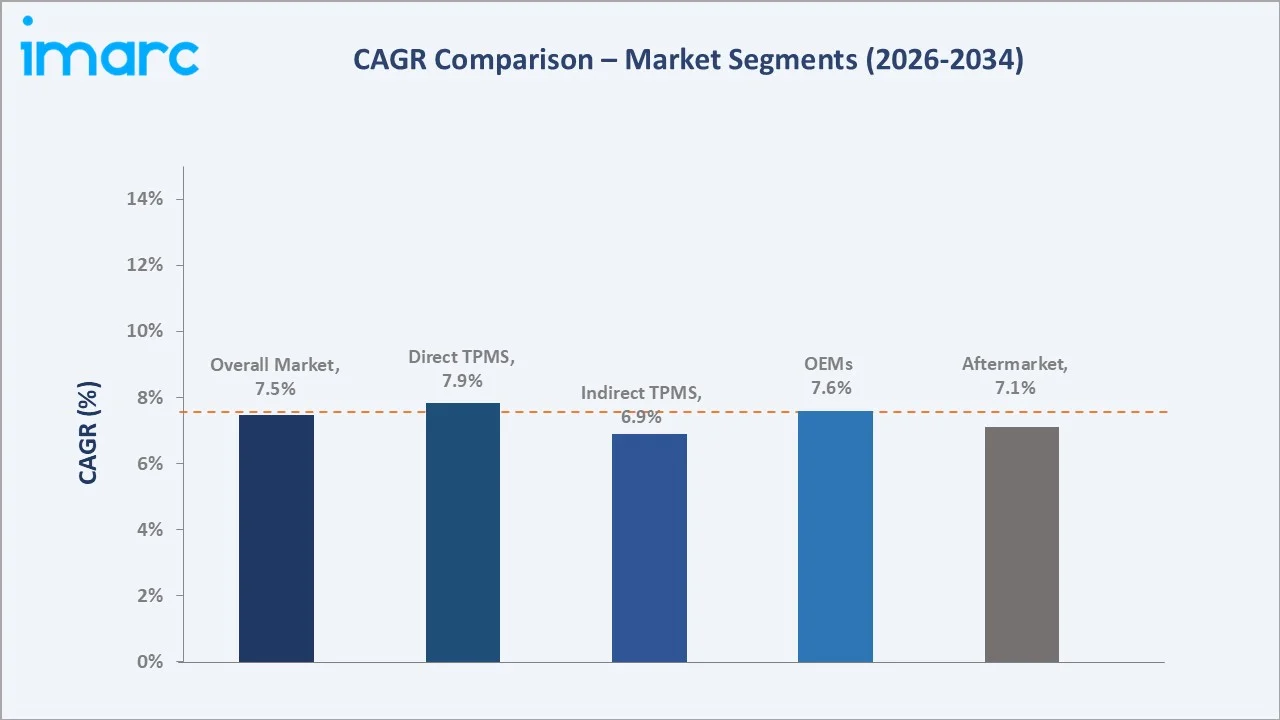

Direct TPMS grows faster than Indirect TPMS through accuracy advantages and expanding regulatory requirements. OEMs grow at a higher rate through factory-fitment mandates in major automotive markets globally.

Executive Summary

The global TPMS market reached USD 8.01 Billion in 2025, representing one of the fastest-growing automotive safety technology segments. The market encompasses pressure sensors, electronic control units, valve assemblies, antenna systems, and integrated software platforms that monitor and report tire pressure in real time.

Direct TPMS at 64.0% dominates through accuracy and mandatory regulatory compliance. OEMs at 82.0% lead through factory-fitment requirements. Asia Pacific at 39.0% leads through China and India vehicle production scale and expanding mandatory TPMS regulations.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Direct TPMS – 64.0% share (2025) |

|

Dominant Distribution Channel |

OEMs – 82.0% market share (2025) |

|

Leading Region |

Asia Pacific – 39.0% market share |

|

Market Opportunity |

EV-specific TPMS; AI predictive tire management; smart TPMS integration; emerging market mandates; aftermarket retrofit demand |

Key Analytical Observations Supporting the Above Data:

- Direct TPMS at 64.0%: Direct TPMS systems use dedicated pressure sensors in each wheel, providing real-time accurate readings. These systems are mandated across major automotive markets and preferred for premium and commercial vehicles requiring precise tire pressure monitoring.

- OEMs at 82.0%: OEM dominance reflects mandatory factory-fitment requirements across global automotive markets driven by NHTSA, EU, and expanding Asia Pacific TPMS mandates, making OEM integration the primary TPMS adoption channel.

- Asia Pacific at 39.0%: Asia Pacific leads through China and India vehicle production scale, expanding TPMS legislation, and increasing consumer awareness of road safety. South Korea and Japan contribute through advanced automotive technology adoption.

Tire Pressure Monitoring System (TPMS) Market Overview

The global TPMS market encompasses the design, manufacturing, and integration of tire pressure monitoring solutions for passenger and commercial vehicles. The market covers direct and indirect sensing hardware, electronic control systems, software platforms, and aftermarket service and replacement components.

Macroeconomic factors include rising global vehicle production, increasing road safety regulations, growing fuel economy concerns, and the rapid expansion of electric vehicles. Government mandates requiring TPMS in new vehicles across major automotive markets create consistent baseline demand that supports both OEM and aftermarket growth.

Market Dynamics

To evaluate market opportunities, Request Sample

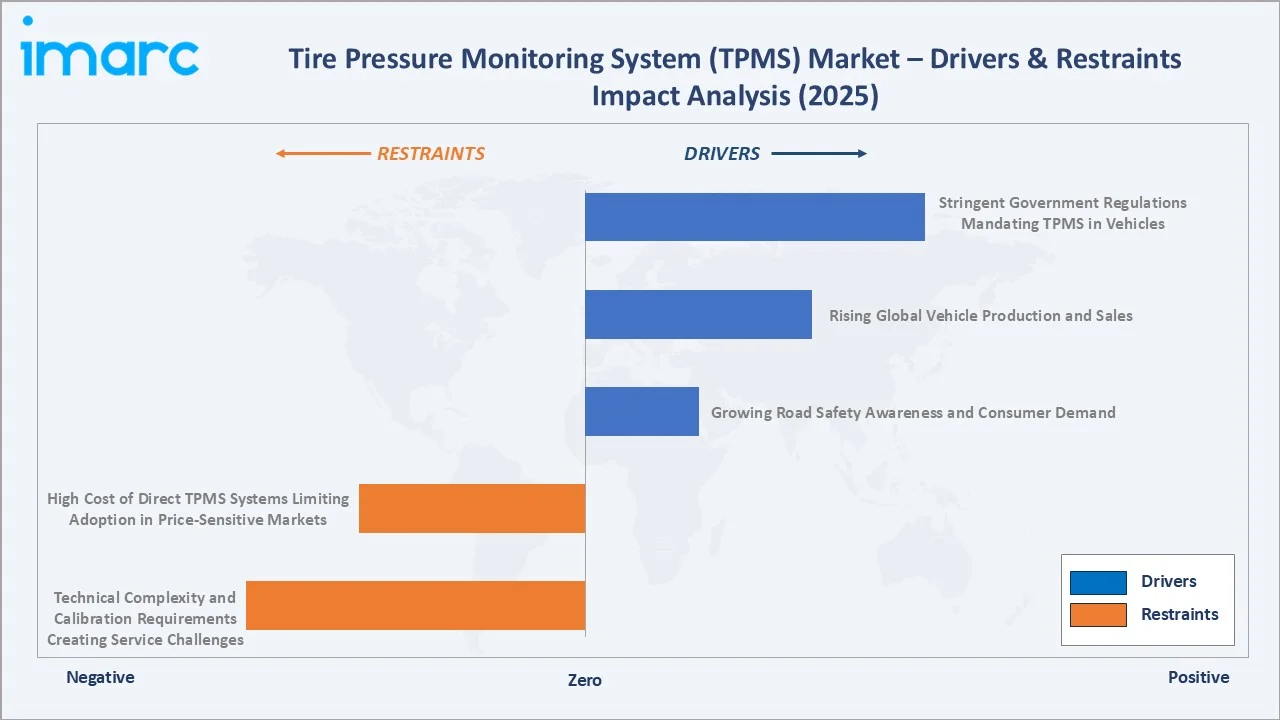

Market Drivers

- Stringent Government Regulations Mandating TPMS in Vehicles: Mandatory TPMS regulations are the primary market driver, with requirements in the US, EU, South Korea, Japan, and expanding Asian markets creating legal obligations for new vehicle TPMS fitment. These regulations create consistent, policy-mandated demand that supports predictable OEM volume growth and a growing replacement aftermarket as mandated vehicles age.

- Rising Global Vehicle Production and Sales: Increasing vehicle production in major automotive markets, particularly across Asia Pacific, directly expands the addressable TPMS market. Higher new vehicle sales volumes translate into proportional TPMS unit demand through OEM fitment requirements, making vehicle production growth a fundamental market driver.

- Growing Road Safety Awareness and Consumer Demand: Rising awareness of the role of proper tire inflation in preventing road accidents and improving fuel efficiency is driving aftermarket TPMS adoption. Consumer demand for advanced vehicle safety features supports both OEM integration of premium TPMS systems and voluntary aftermarket retrofit installations.

- Integration of Advanced Sensor and IoT Technologies: The integration of IoT connectivity, smart sensor platforms, and vehicle telematics is expanding TPMS capabilities beyond basic pressure monitoring. Connected TPMS systems providing predictive maintenance insights and real-time fleet monitoring are increasing the value proposition and adoption rates in commercial vehicle fleets.

Market Restraints

- High Cost of Direct TPMS Systems Limiting Adoption in Price-Sensitive Markets: Direct TPMS systems require individual pressure sensors in each wheel, increasing vehicle production costs. In price-sensitive emerging markets, these cost pressures can slow mandatory adoption timelines and limit voluntary aftermarket uptake, particularly for lower-segment passenger vehicles and two-wheelers.

- Technical Complexity and Calibration Requirements Creating Service Challenges: TPMS systems require periodic recalibration after tire service events, and the technical expertise required for proper service represents a barrier in markets with limited automotive service infrastructure. Diagnostic tool availability and technician training requirements add complexity to aftermarket service operations.

- Lack of Standardization Across Regions Creating Interoperability Challenges: Regional differences in TPMS operating frequencies and communication protocols create interoperability challenges for global vehicle manufacturers and aftermarket suppliers, increasing development costs and supply chain complexity for companies serving multiple automotive markets.

Market Opportunities

- EV-Specific TPMS Integration for the Global Electric Vehicle Transition: The rapid growth of electric vehicles creates specialized TPMS product opportunities. EVs carry higher battery weight and generate higher torque, increasing tire wear rates and the importance of precise pressure management for range optimization. EV-specific TPMS integration with battery management systems represents a differentiated growth segment.

- AI-Driven Predictive Tire Management for Connected Vehicle Platforms: AI-powered predictive TPMS platforms that analyze pressure trends, driving patterns, and environmental conditions to forecast tire failure represent a high-value growth opportunity, particularly for commercial fleet operators seeking to reduce maintenance costs and prevent downtime.

Market Challenges

- Battery Life Limitations in Wireless Sensor Systems: Wireless TPMS sensors have finite battery lifespans requiring tire dismounting for replacement. As mandated vehicle fleets age, increasing battery replacement rates create servicing demand while also presenting consumer satisfaction challenges related to maintenance costs and inconvenience.

- Counterfeit Products in Aftermarket Channels: The proliferation of low-quality counterfeit TPMS sensors in aftermarket channels creates reliability and safety concerns, undermines consumer confidence, and exerts pricing pressure on genuine component suppliers, creating challenges for maintaining product quality standards across distributed service networks.

Emerging Market Trends

-market_market_ppt_by-neha-2.webp)

1. Global Expansion of Mandatory TPMS Legislation Accelerating Market Growth

Mandatory TPMS regulations are expanding beyond the traditional US and European markets into Asia Pacific, Latin America, and the Middle East. This regulatory expansion is creating consistent new OEM fitment demand and supporting an expanding aftermarket as older mandated vehicles require sensor replacement. Countries introducing TPMS mandates gain from documented road safety improvements and fuel efficiency benefits at the fleet level.

2. Smart TPMS Integration with Connected Vehicle and Telematics Platforms

TPMS systems are increasingly integrating with connected vehicle platforms, enabling real-time data sharing with fleet operators and cloud analytics services. Smart TPMS provides continuous monitoring, predictive maintenance alerts, and driving behavior optimization. Fleet operators are primary adopters, driven by documented fuel savings and tire lifecycle cost reductions from precision pressure management.

3. Electric Vehicle Growth Creating Specialized TPMS Requirements

The global EV transition creates specialized TPMS requirements and product development opportunities. EVs generate higher torque and carry greater battery weight, increasing tire wear rates and the criticality of pressure management for range optimization. EV manufacturers are integrating advanced TPMS systems with battery management platforms, creating new product categories for TPMS suppliers.

4. Aftermarket TPMS Retrofit Demand Growing with Aging Vehicle Fleet

As the global mandated vehicle fleet ages and early TPMS vehicles require sensor battery replacement, the aftermarket TPMS sector is expanding. Universal TPMS sensors covering multiple vehicle applications and growing service network capabilities are making aftermarket service more accessible, supporting aftermarket segment growth above OEM rates through the forecast period.

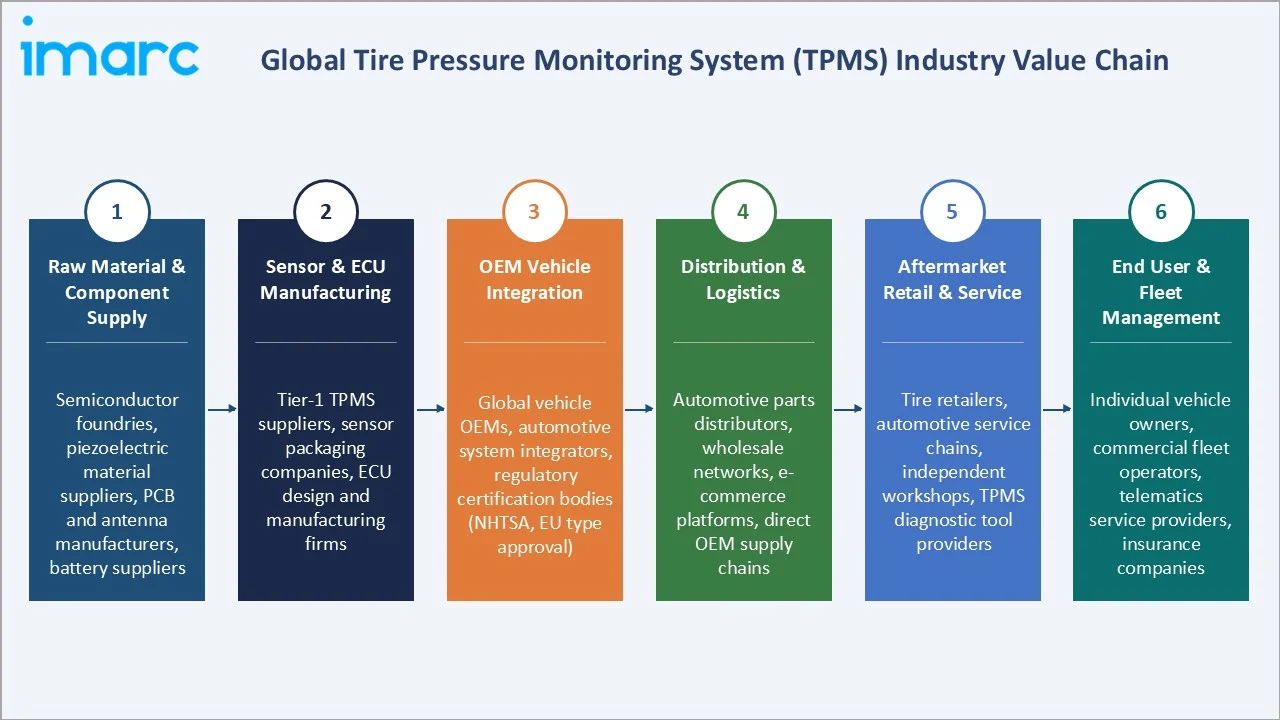

Industry Value Chain Analysis

The TPMS value chain integrates semiconductor and component supply, sensor and ECU manufacturing, OEM vehicle integration, distribution, and end-user service. Each stage creates value through precision engineering, regulatory certification, and system integration depth.

|

Stage |

Key Participants |

|

Raw Material & Component Supply |

Semiconductor foundries, piezoelectric material suppliers, PCB and antenna manufacturers, battery suppliers |

|

Sensor & ECU Manufacturing |

Tier-1 TPMS suppliers, sensor packaging companies, ECU design and manufacturing firms |

|

OEM Vehicle Integration |

Global vehicle OEMs, automotive system integrators, regulatory certification bodies (NHTSA, EU type approval) |

|

Distribution & Logistics |

Automotive parts distributors, wholesale networks, e-commerce platforms, direct OEM supply chains |

|

Aftermarket Retail & Service |

Tire retailers, automotive service chains, independent workshops, TPMS diagnostic tool providers |

|

End User & Fleet Management |

Individual vehicle owners, commercial fleet operators, telematics service providers, insurance companies |

The sensor and ECU manufacturing stage is the most technically differentiated phase. OEM platform integration requirements and regulatory certification create significant entry barriers, concentrating market share among established Tier-1 automotive suppliers with proven OEM relationships.

Technology Landscape in the TPMS Industry

Direct TPMS Sensor Technology

Direct TPMS uses pressure sensors mounted inside each wheel, transmitting real-time data to the vehicle ECU. Advanced systems now incorporate temperature sensors, acceleration-based wheel position detection, and low-power RF protocols. Next-generation platforms are exploring energy harvesting from wheel rotation to extend sensor operational life beyond current battery constraints.

Indirect TPMS Algorithm Technology

Indirect TPMS uses existing ABS wheel speed sensors to detect pressure loss through changes in tire rotation rates. Advanced algorithms now incorporate machine learning to improve accuracy and reduce false warnings. While less accurate than direct systems, indirect TPMS provides a cost-effective solution for markets where extreme precision is not mandated.

Intelligent TPMS and Predictive Analytics

Intelligent TPMS platforms combine direct pressure sensing with AI analytics to deliver predictive tire health management. These systems analyze historical pressure trends, driving patterns, load conditions, and environmental data to predict potential failures before occurrence. Integration with cloud fleet management platforms enables centralized monitoring across entire commercial vehicle fleets.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Direct TPMS |

64.0% |

2025 |

|

Technology |

Conventional TPMS |

🔒 |

2025 |

|

Vehicle Type |

Passenger Vehicles |

🔒 |

2025 |

|

Distribution Channel |

OEMs |

82.0% |

2025 |

|

Region |

Asia Pacific |

39.0% |

2025 |

By Type

Direct TPMS leads at 64.0% (2025). The direct TPMS segment encompasses wheel-mounted pressure sensors, ECUs, and RF communication systems that deliver real-time, accurate tire pressure readings. Direct TPMS is mandated for new passenger vehicles in the US, EU, South Korea, and other markets, driving consistent OEM demand globally.

To access detailed market analysis, Request Sample

Indirect TPMS at 36.0% leverages existing ABS infrastructure, offering a cost-effective alternative in markets with less stringent mandates or lower vehicle price segment constraints. Indirect TPMS growth is supported by cost-sensitive markets in Southeast Asia, Latin America, and the Middle East.

By Distribution Channel

OEMs lead at 82.0% (2025). OEM dominance reflects mandatory factory-fitment requirements and technical integration needs of modern TPMS with vehicle electronics and driver information systems. TPMS is a regulated safety component creating stable, predictable demand tied directly to new vehicle production volumes.

Aftermarket at 18.0% encompasses replacement sensors for vehicles with end-of-life batteries, retrofit installations, and replacement after tire service. Universal TPMS sensors and growing service network awareness support aftermarket growth, with the segment expected to grow at a faster rate than OEM through the forecast period.

Regional Market Insights

|

Region |

Share (2025) |

Key TPMS Market Drivers & Characteristics |

|

Asia Pacific |

39.0% |

Driven by large vehicle production volumes in China and India, expanding mandatory TPMS regulations, and rapid automotive sector growth across Southeast Asia. |

|

Europe |

29.0% |

Driven by EU mandatory TPMS regulations, a strong automotive OEM base in Germany and France, and high adoption of advanced vehicle safety technologies. |

|

North America |

21.0% |

Driven by the NHTSA TPMS mandate, a large and aging vehicle fleet generating replacement sensor demand, and strong aftermarket service infrastructure. |

|

Latin America |

6.0% |

Supported by growing vehicle production in Brazil and Mexico, expanding regulatory safety frameworks, and rising vehicle safety standards across the region. |

|

Middle East and Africa |

5.0% |

Driven by increasing vehicle imports, expanding road safety regulations, and rising demand for advanced automotive safety systems in key markets. |

Asia Pacific's 39.0% market leadership is anchored by China's position as the world's largest vehicle production and sales market, combined with India's rapidly expanding automotive sector and TPMS mandate implementation. South Korea and Japan contribute through premium vehicle technology adoption.

Europe's 29.0% reflects EU-wide mandatory TPMS requirements and Germany's dominance as a premium automotive technology hub. North America's 21.0% is underpinned by the NHTSA mandate and a large aging fleet creating strong replacement sensor demand.

Competitive Landscape

The global TPMS competitive landscape encompasses distinct tiers: Tier-1 automotive component suppliers with integrated TPMS product lines, semiconductor specialists supplying sensor ICs, and specialized TPMS technology companies serving OEM and aftermarket channels globally.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Continental AG |

Tire Pressure Monitoring Systems (TPMS) |

Market Leader |

Continental plays a central role in TPMS through integrated sensor systems, broad OEM relationships, and advanced sensor fusion capabilities for vehicle safety systems. |

|

Robert Bosch LLC |

Bosch TPMS Sensors , TPA 300 |

Market Leader |

Bosch plays a central role in TPMS through extensive OEM integration expertise and a comprehensive aftermarket service tool ecosystem supporting global workshops. |

|

DENSO Corporation |

DENSO TPMS Sensors and Receivers |

Market Leader |

DENSO plays a central role through deep OEM integration with major Asian automakers, backed by precision manufacturing capabilities and technical reliability. |

|

NXP Semiconductors |

TPMS IC Solutions, Sensor MCUs |

Established Player |

NXP provides core TPMS semiconductor solutions enabling advanced sensor integration, low-power RF communication, and secure vehicle network connectivity. |

OEM integration concentration creates sustainable competitive advantages for established Tier-1 suppliers through long-term platform contracts and regulatory certification depth. The aftermarket segment shows higher fragmentation, with universal sensor manufacturers competing on compatibility breadth and price.

-market_market_ppt_by-neha-9.webp)

Key Company Profiles

Continental AG

Continental AG is a leading global automotive technology company providing TPMS solutions as part of its broad vehicle safety and chassis technology portfolio. The company specializes in integrated direct TPMS sensor systems for OEM and aftermarket applications worldwide.

- Key Products: ContiSys Check, EasyPoint TPMS sensors, aftermarket sensor programming tools.

- Recent Developments: In March 2025, Continental announced the integration of its ContiConnect digital tire monitoring solution with Samsara's Connected Operations Platform, enabling fleet operators to monitor tire pressure and temperature data directly through Samsara's interface for improved predictive maintenance and fleet efficiency.

- Strategic Focus: Focused on integrated safety system solutions combining TPMS with chassis control, advanced driver assistance systems, and connected vehicle platforms.

Robert Bosch LLC

Robert Bosch LLC is one of the world's largest automotive component suppliers, providing TPMS sensors and comprehensive aftermarket service solutions. The company leverages broad OEM relationships across European, American, and Asian vehicle manufacturers for TPMS integration.

- Key Products: Bosch TPMS sensors, TPMS service tools, KTS diagnostic platforms for TPMS service.

- Recent Developments: In June 2025, Robert Bosch introduced its next-generation SMP290 tire-pressure sensor module featuring an integrated Bluetooth Low Energy (BLE) interface, enabling simplified vehicle architectures, direct smartphone connectivity, and ultra-low power consumption. The sensor was also nominated for the Best Sensors Awards 2025 in the Automotive & Mobility category.

- Strategic Focus: Centered on integrated automotive safety systems, comprehensive aftermarket service tools, and connected vehicle diagnostic solutions.

Market Concentration Analysis

The global TPMS market is moderately concentrated at the OEM Tier-1 supplier level, with Continental, Bosch, and DENSO collectively holding significant OEM fitment share. The aftermarket segment is more fragmented, with universal sensor manufacturers and regional suppliers competing alongside Tier-1 aftermarket divisions.

Semiconductor concentration is higher, with NXP Semiconductors and Infineon Technologies supplying a significant share of TPMS sensor ICs globally. Increasing consolidation in the aftermarket is driven by universal sensor coverage and programming tool compatibility as key competitive differentiators.

Investment & Growth Opportunities

Highest Growth Segments

Direct TPMS for EV platforms (~9.5% CAGR), intelligent TPMS with predictive analytics (~15% CAGR from small base), aftermarket universal sensors (~8.5% CAGR), Asia Pacific OEM fitment (~10% CAGR through mandate expansion), and connected fleet TPMS management platforms (~20% CAGR from small base) represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

Asia Pacific regulatory expansion represents the largest near-term TPMS opportunity. Companies establishing OEM supply relationships with Chinese, Indian, and Southeast Asian vehicle manufacturers ahead of mandatory TPMS regulation timelines are positioned for above-market volume growth as new mandates take effect.

Investment Themes

- EV-optimized TPMS sensor development for the global electric vehicle transition: EV-specific TPMS systems integrated with battery management and range optimization platforms represent a product differentiation opportunity. Companies co-developing EV TPMS solutions with major EV OEMs are positioned to capture factory-fitment contracts across rapidly expanding EV production volumes.

- Universal aftermarket TPMS platform expanding vehicle coverage and service network reach: A universal TPMS sensor and programming tool platform covering the broadest possible vehicle application range creates a durable competitive advantage. Cloud-connected programming tools enabling firmware updates further strengthen service provider relationships and support recurring revenue.

Future Market Outlook (2026-2034)

The global TPMS market is projected to grow from USD 8.01 Billion in 2025 to USD 15.65 Billion by 2034, delivering a 7.49% CAGR over the forecast period. The anchor value of USD 11.50 Billion in 2030 reflects a market at peak global regulatory expansion, with EV-specific TPMS achieving mainstream OEM adoption across major automotive markets.

Three structural forces define TPMS growth through 2034. Mandatory regulatory expansion creates government-mandated demand across the largest automotive growth markets in Asia Pacific and Latin America. The EV transition creates both volume growth through rising EV production and value growth through more sophisticated EV-integrated TPMS systems. Aging global vehicle fleets create expanding aftermarket replacement demand as sensor battery lifecycles expire in early-mandate vehicle cohorts globally.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders (2025) including automotive Tier-1 technology directors, TPMS product managers, OEM procurement specialists, aftermarket distribution executives, and regional regulatory compliance experts.

Secondary Research

Secondary research encompassed automotive safety technology publications, NHTSA and EU regulatory databases, vehicle production statistics, automotive component company annual reports, and industry trade association data. Over 60 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using a segment bottom-up model incorporating OEM fitment volumes by region, aftermarket replacement cycles, regulatory mandate timelines, and technology adoption rates for advanced TPMS systems.

Tire Pressure Monitoring System (TPMS) Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Direct TPMS, Indirect TPMS |

| Technologies Covered | Intelligent TPMS, Conventional TPMS |

| Vehicle Types Covered | Passenger Vehicles, Commercial Vehicles |

| Distribution Channels Covered | OEMs, Aftermarket |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Continental AG, Robert Bosch LLC, DENSO Corporation, NXP Semiconductors, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the tire pressure monitoring system (TPMS) market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global tire pressure monitoring system (TPMS) market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the tire pressure monitoring system (TPMS) industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Tire Pressure Monitoring System Market Report

The global TPMS market reached USD 8.01 Billion in 2025, driven by mandatory safety regulations, rising vehicle production, and increasing consumer awareness of road safety and fuel efficiency.

The market grows at 7.49% CAGR during 2026-2034, reaching USD 15.65 Billion by 2034. Direct TPMS for EV platforms grows fastest through EV production volume growth and specialized integration requirements.

Direct TPMS leads at 64.0% through accuracy advantages, mandatory regulatory compliance requirements in major markets, and integration with advanced vehicle safety platforms globally.

OEMs lead at 82.0% through mandatory factory-fitment requirements across global automotive markets, driven by NHTSA, EU, and expanding Asia Pacific TPMS mandates.

Asia Pacific leads at 39.0% through China and India vehicle production scale, expanding mandatory TPMS legislation, and rapid automotive sector growth across Southeast Asia.

Leading companies include Continental AG, Robert Bosch LLC, DENSO Corporation, and NXP Semiconductors, among others.

The market is projected to reach approximately USD 11.50 Billion by 2030, with EV-specific TPMS achieving mainstream OEM adoption, AI-powered predictive tire management entering commercial deployment, and Asia Pacific mandatory TPMS expansion driving peak volume growth.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)