Transmission Fluids Market Size, Share, Trends and Forecast by Type, Base Oil, Application, and Region, 2026-2034

Transmission Fluids Market Size, Share, Trends & Forecast (2026-2034)

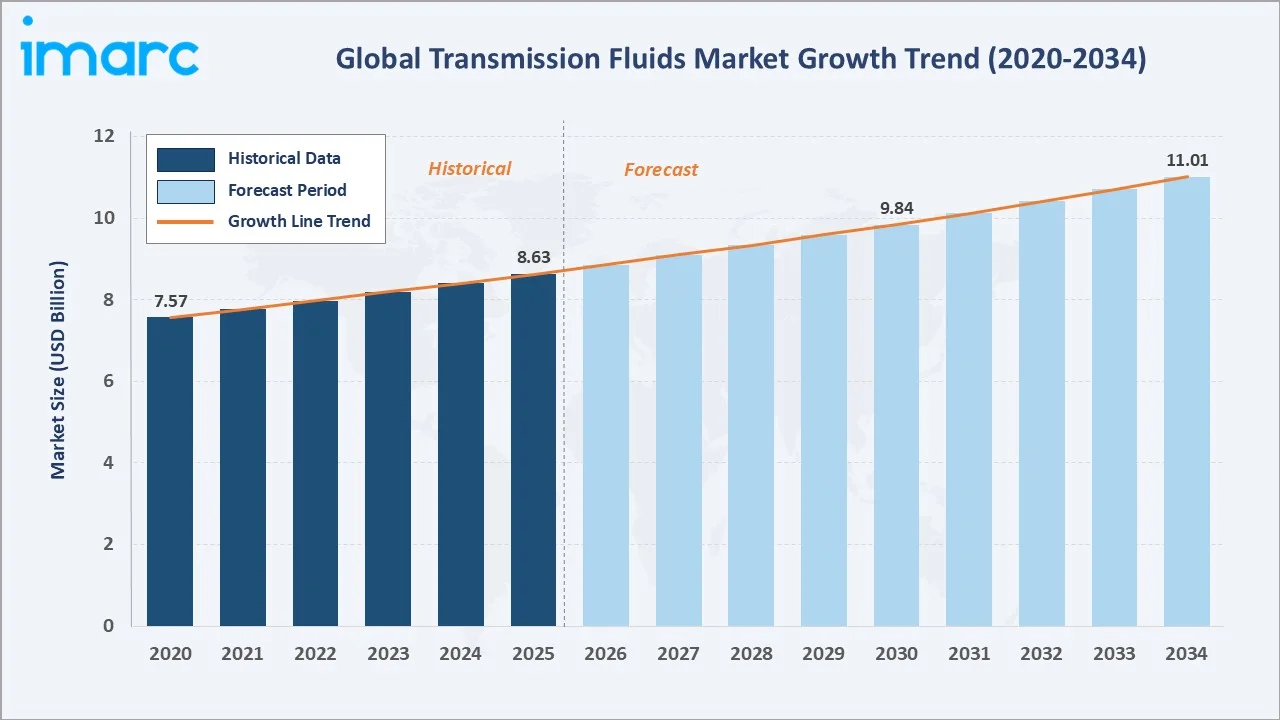

The global transmission fluids market size reached USD 8.63 Billion in 2025 and is projected to reach USD 11.01 Billion by 2034, exhibiting a CAGR of 2.66% during 2026-2034. Rising automotive production, growing preference for automatic transmissions, and stringent OEM fluid specifications are the primary growth forces shaping this market.

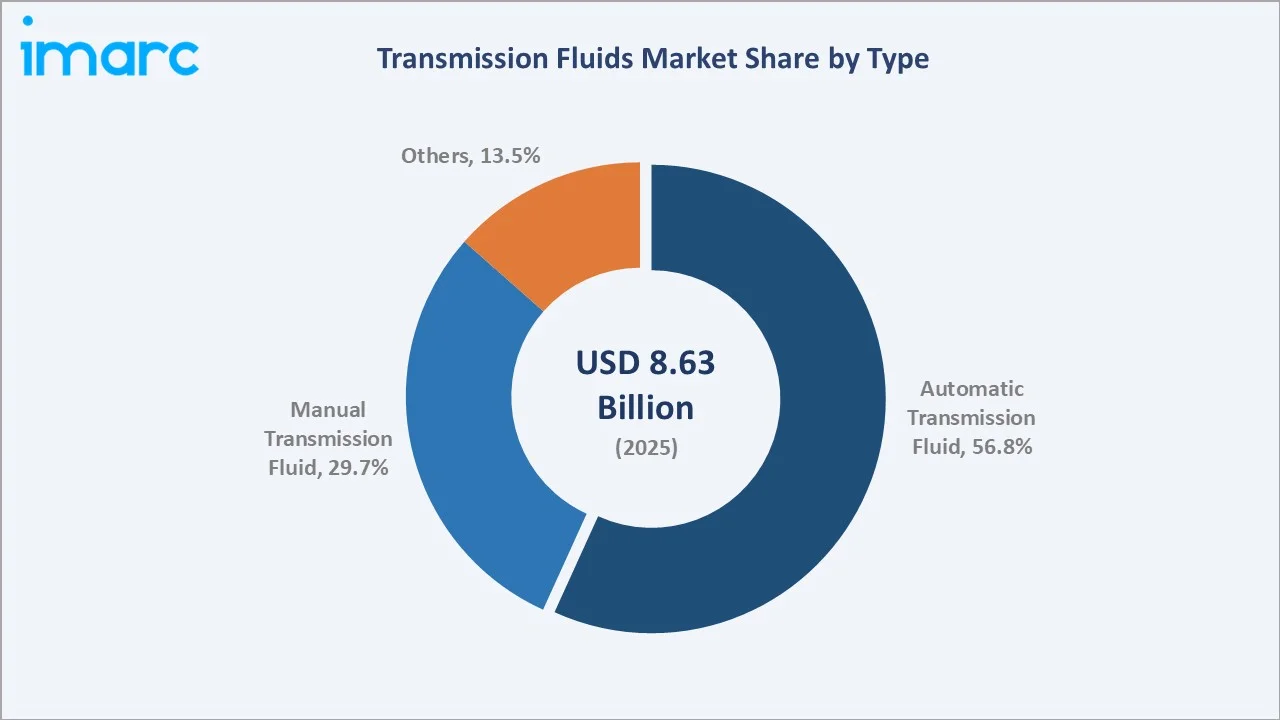

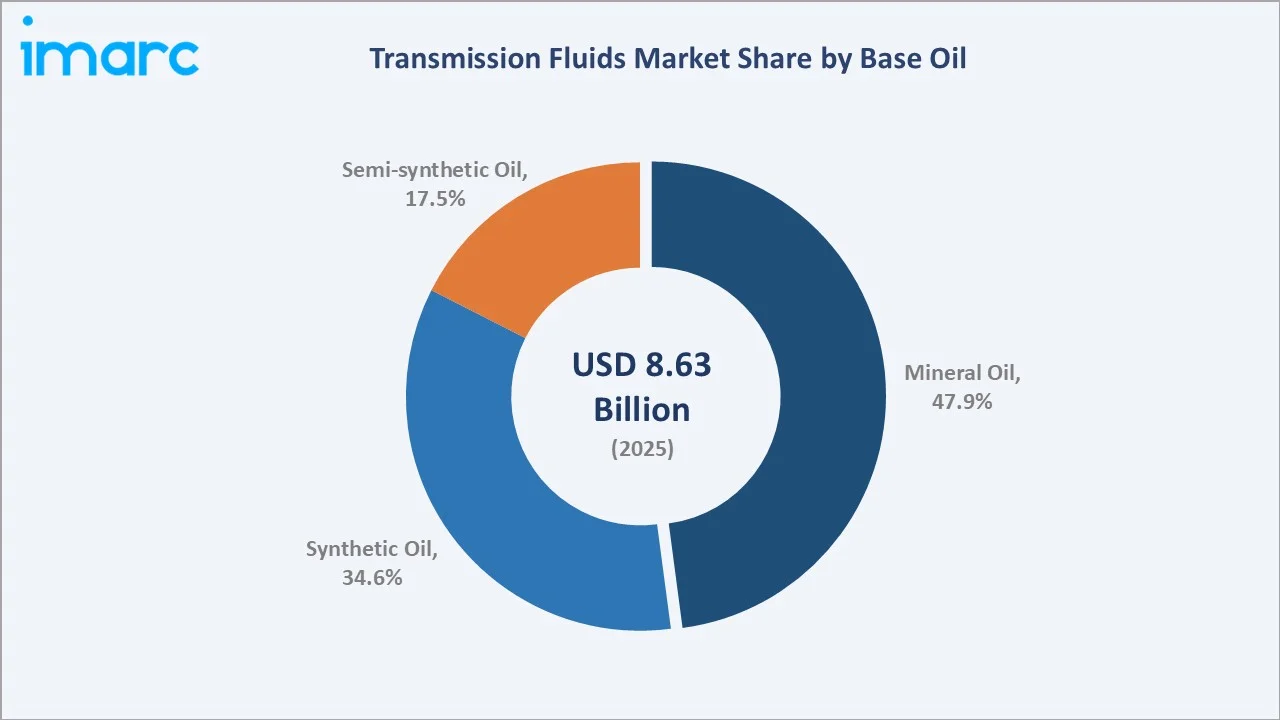

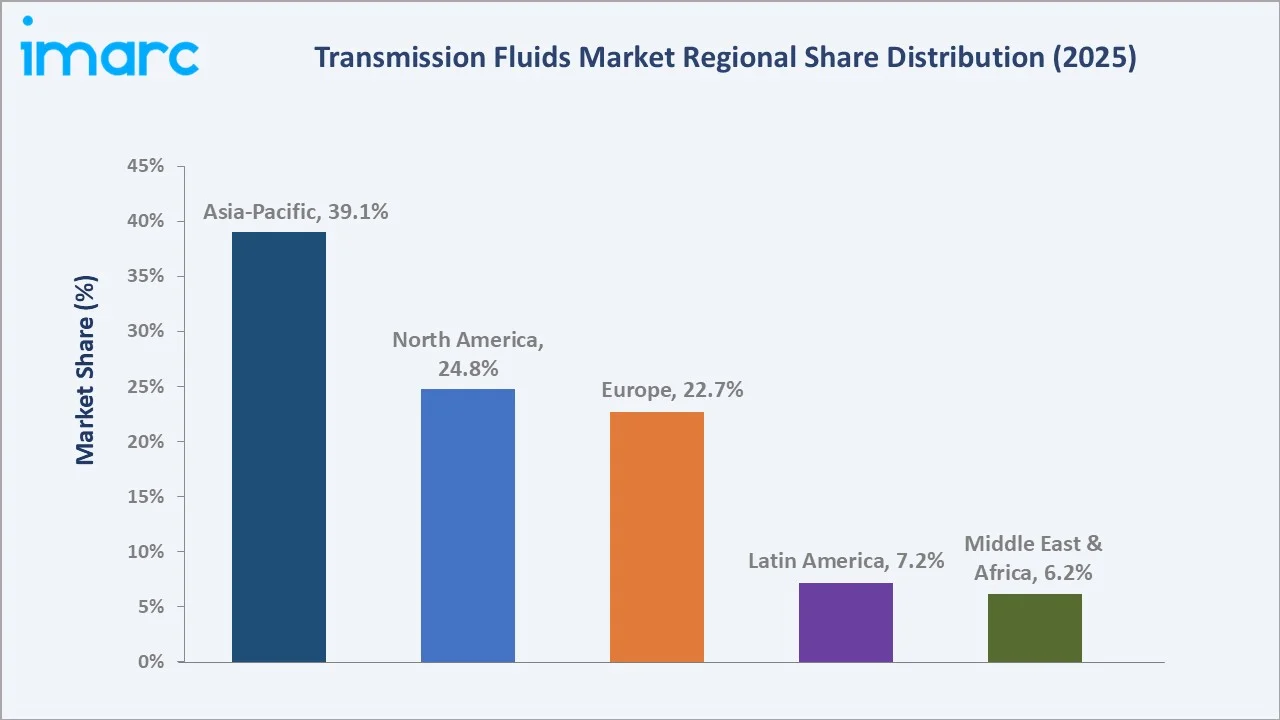

Automatic Transmission Fluid leads the type segmentation at 56.8% in 2025, driven by surging automatic vehicle adoption globally. Mineral Oil commands 47.9% base oil share. Asia-Pacific dominates the regional landscape with a 39.1% share underpinned by strong automotive manufacturing across China, India, Japan, and South Korea.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 8.63 Billion |

|

Forecast Market Size (2034) |

USD 11.01 Billion |

|

CAGR (2026-2034) |

2.66% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Type |

Automatic Transmission Fluid (56.8% share, 2025) |

|

Leading Base Oil |

Mineral Oil (47.9% share, 2025) |

|

Leading Region |

Asia-Pacific (39.1% share, 2025) |

The transmission fluids market growth from 2020 through 2034 reflects steady demand driven by global automotive fleet expansion and growing aftermarket maintenance requirements. The forecast to USD 11.01 Billion by 2034 captures ongoing synthetic fluid premiumization and expanding vehicle parc across emerging economies worldwide.

To get more information on this market, Request Sample

CAGR trajectories across key type and base oil sub-segments highlight Synthetic Oil at approximately 3.38% CAGR and Others (Type) at approximately 3.05% CAGR as the fastest-growing categories within the transmission fluids market through 2034.

Executive Summary

The transmission fluids market is on a sustained growth trajectory from USD 8.63 Billion in 2025 to USD 11.01 Billion by 2034. The market encompasses automatic, manual, and specialty transmission fluids deployed across passenger vehicles, commercial vehicles, and off-road equipment worldwide.

Automatic Transmission Fluid leads at 56.8% in 2025, owing to rising consumer preference for automatic and continuously variable transmissions across all vehicle categories. Manual Transmission Fluid (29.7%) remains significant in commercial and emerging-market segments.

Mineral Oil commands 47.9% base oil share in 2025, driven by cost-effectiveness and broad OEM compatibility. Synthetic Oil (34.6%) is the fastest-growing segment as OEMs specify high-performance fluids for advanced transmission systems requiring extended service intervals.

Asia-Pacific dominates at 39.1% in 2025, supported by large automotive production bases across China, India, Japan, and South Korea. North America follows at 24.8%, with Europe at 22.7%, both driven by mature aftermarket demand and premium fluid specifications.

Key Market Insights

|

Insight |

Data |

|

Leading Type |

Automatic Transmission Fluid – 56.8% share (2025) |

|

Leading Base Oil |

Mineral Oil – 47.9% share (2025) |

|

Leading Region |

Asia-Pacific – 39.1% share (2025) |

|

Second Largest Region |

North America – 24.8% share (2025) |

|

Top Companies |

Exxon Mobil Corporation, Chevron Corporation, BP p.l.c, FUCHS, and TotalEnergies, among others |

- Automatic Transmission Fluid at 56.8% dominates because consumer preference for automatic and CVT transmissions continues to rise globally. The proliferation of automatic vehicles in developing markets and growing hybrid vehicle production sustain robust ATF demand across automotive manufacturing and aftermarket channels.

- Mineral Oil commands 47.9% base oil share because of its wide OEM compatibility and cost advantage over synthetic alternatives. It remains the default choice in cost-sensitive emerging markets and for conventional vehicle platforms across Asia-Pacific and Latin America.

- Asia-Pacific's 39.1% regional dominance reflects the region's unrivalled automotive manufacturing scale. China and India are rapidly expanding vehicle fleets while Japan and South Korea sustain demand through advanced OEM fluid specification requirements for next-generation transmission systems.

Transmission Fluids Market Overview

The transmission fluids market encompasses automatic, manual, and specialty fluids deployed across passenger cars, commercial trucks, and off-road equipment. Market structure integrates base oil producers, additive manufacturers, fluid formulators, OEM specification bodies, distributors, and end-users across automotive service and industrial sectors.

The ecosystem integrates global petrochemical majors, specialty chemical companies, additive technology providers, OEM technical partners, automotive aftermarket distributors, quick-lube chains, and regulatory bodies setting performance and emissions standards that govern fluid approvals worldwide.

Market Dynamics

To evaluate market opportunities, Request Sample

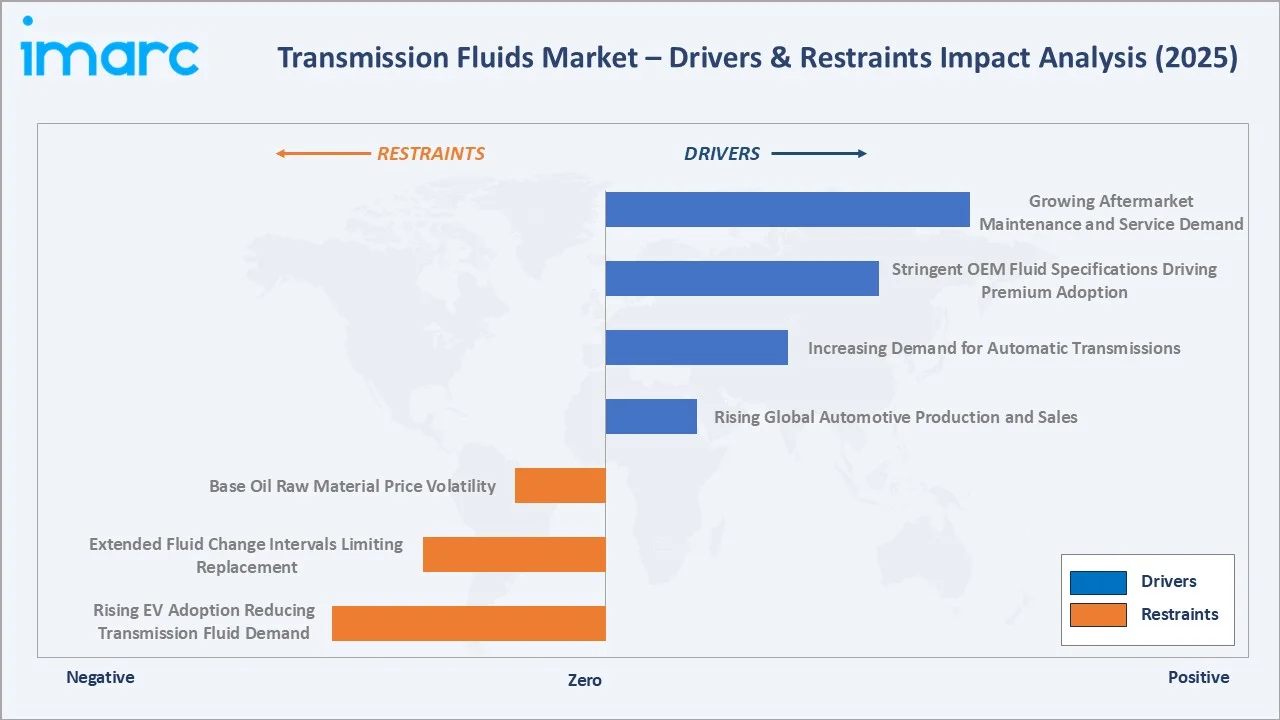

Market Drivers

- Rising Global Automotive Production and Sales: Steady global vehicle production expansion, particularly in Asia-Pacific and Latin America, is driving sustained demand for transmission fluids. Growing vehicle parc and rising fleet ownership rates in emerging economies continue to support OEM fill and aftermarket replacement volumes across all transmission types.

- Increasing Demand for Automatic Transmissions: Consumer preference for automatic and continuously variable transmissions is accelerating ATF demand across all vehicle classes. The rapid adoption of automatic vehicles in previously manual-dominated markets such as China and India is significantly expanding the addressable automatic transmission fluid market.

- Stringent OEM Fluid Specifications Driving Premium Product Adoption: Leading OEMs including ZF, Aisin, and GM are issuing increasingly demanding transmission fluid specifications requiring advanced additive packages. These specifications promote premium and synthetic fluid adoption, elevating average selling prices and expanding revenue for specialty formulators globally.

- Growing Aftermarket Maintenance and Service Demand: Expanding vehicle populations and growing consumer awareness of transmission maintenance are driving robust aftermarket fluid demand. Quick-lube networks, independent workshops, and dealership service centers are increasing transmission fluid change frequency, sustaining global replacement volumes.

Market Restraints

- Rising Adoption of Electric Vehicles Reducing Transmission Fluid Demand: Battery electric vehicles eliminate conventional gearboxes, directly displacing transmission fluid demand in affected segments. As BEV penetration accelerates across Europe and China, long-term structural demand erosion represents a growing headwind for the conventional transmission fluids market.

- Extended Fluid Change Intervals Limiting Replacement Frequency: Modern synthetic transmission fluids offer significantly longer service lives than legacy mineral oil products. Extended OEM drain intervals reduce aftermarket replacement frequency and constrain volume growth per vehicle, partially offsetting fleet expansion benefits across developed markets.

- Base Oil Raw Material Price Volatility: Transmission fluid production depends on Group II, III, and IV base oils whose prices fluctuate with crude oil markets and refinery capacity. Price volatility squeezes formulator margins and complicates long-term pricing strategies across the transmission fluids value chain.

Market Opportunities

- Growing Demand for Synthetic and High-Performance Fluids: Rising OEM specifications and consumer awareness are creating premiumization opportunities for synthetic ATF and MTF products. Synthetic fluids command higher margins and are increasingly preferred for performance vehicles, luxury cars, and commercial fleet applications globally.

- Expanding Commercial Vehicle Fleet in Emerging Markets: Rapid infrastructure development and e-commerce logistics growth in Asia-Pacific, Africa, and Latin America are driving commercial vehicle sales. Heavy-duty transmission fluids for trucks and construction equipment represent a significant growth opportunity for specialty fluid manufacturers.

Market Challenges

- Increasing Regulatory Pressure on Emissions and Environmental Compliance: Evolving environmental regulations across Europe and North America require increasingly stringent fluid formulations. Compliance with REACH, EPA, and equivalent standards increases formulation complexity and R&D costs for transmission fluid manufacturers globally.

- Intense Competition from Private Label and Low-Cost Alternatives: The market faces significant pressure from private label brands, retailer-owned products, and low-cost alternatives that compete on price in cost-sensitive segments. Maintaining brand differentiation and technical credibility represents an ongoing commercial challenge for major manufacturers.

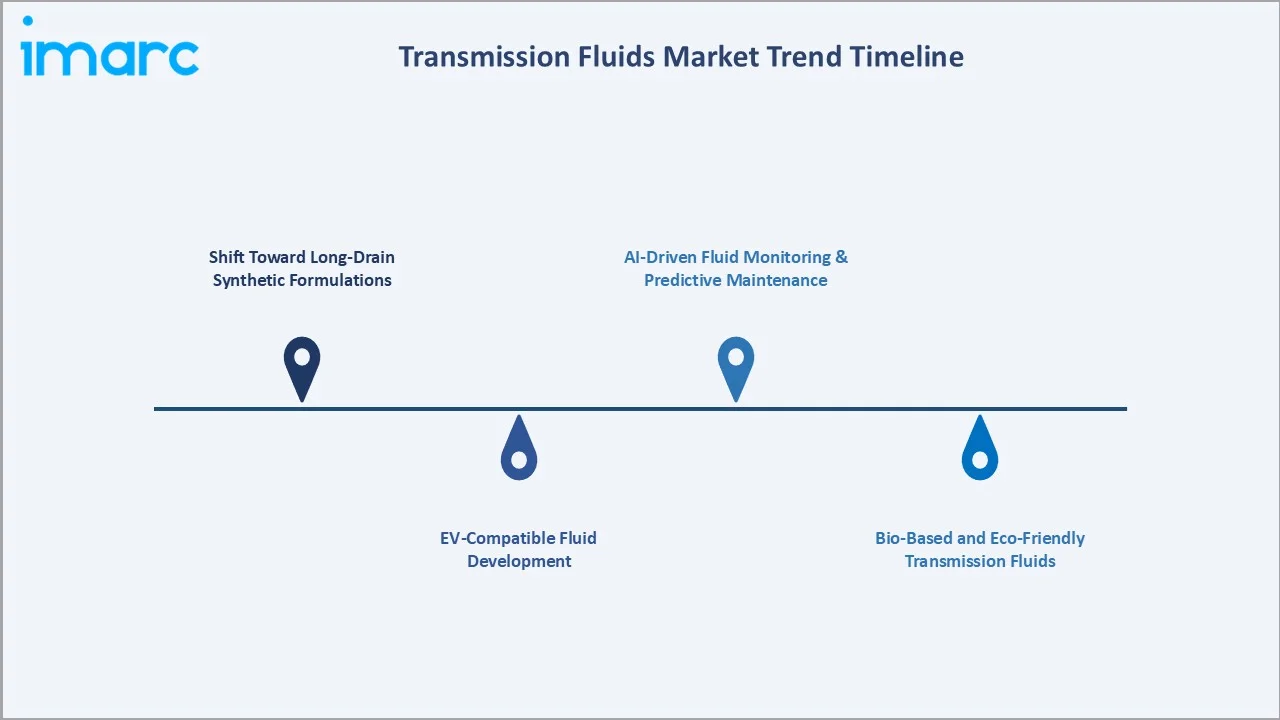

Emerging Market Trends

1. Shift Toward Long-Drain Synthetic Formulations

Advanced synthetic transmission fluids with extended drain intervals are reshaping the aftermarket. Formulators investing in Group IV and ester-based technologies are capturing premium market share as OEMs mandate longer service intervals for new transmission platforms across all vehicle categories.

2. EV-Compatible Fluid Development

Hybrid and electric drivetrains require novel fluid formulations compatible with electric motor windings and high-torque single-speed reducers. Specialty EV transmission and e-axle fluids are a rapidly growing product category attracting significant R&D investment from major lubricant companies globally.

3. Bio-Based and Eco-Friendly Transmission Fluids

Sustainability pressures are driving development of bio-based transmission fluids from vegetable oils and renewable feedstocks. These products reduce lifecycle carbon emissions and appeal to environmentally conscious fleet operators, particularly in Europe where sustainability regulations are most stringent.

4. AI-Driven Fluid Monitoring and Predictive Maintenance

IoT-enabled fluid condition sensors integrated with vehicle telematics enable real-time transmission fluid health monitoring. AI algorithms analyzing fluid viscosity, contamination, and degradation data allow predictive maintenance scheduling, improving fleet uptime and creating new service revenue streams globally.

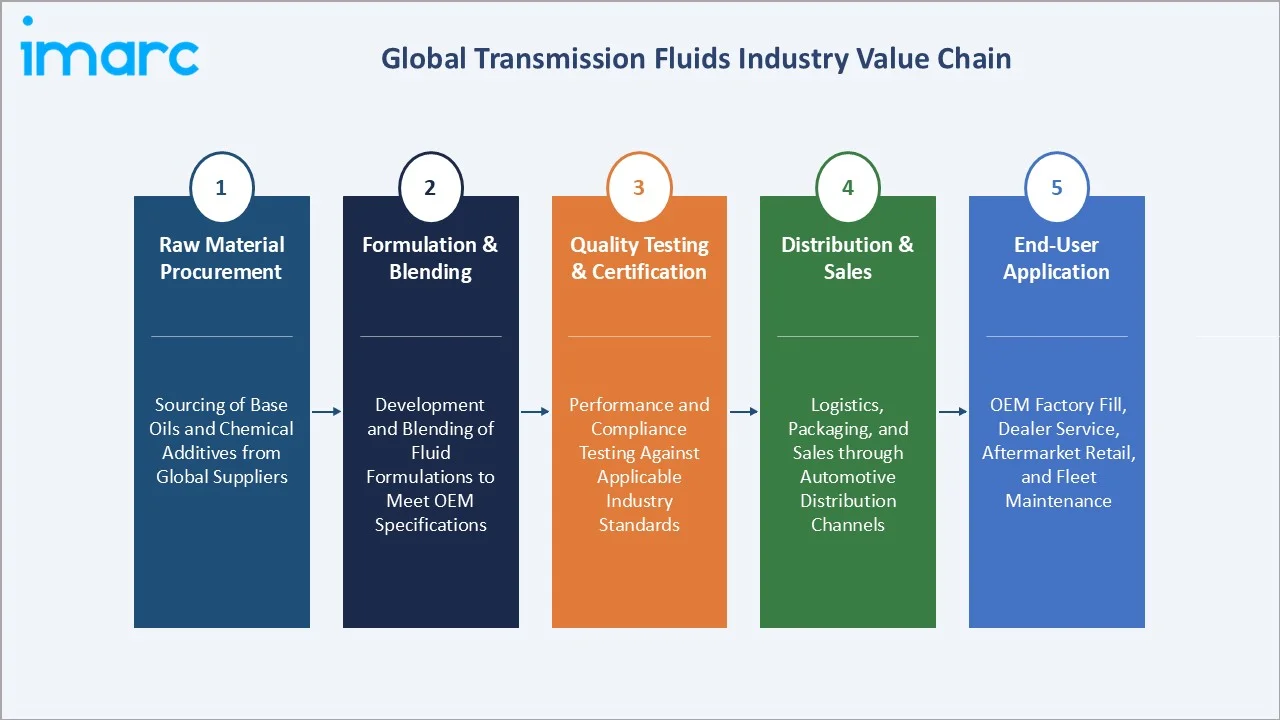

Industry Value Chain Analysis

The transmission fluids value chain spans five integrated stages from base oil procurement through end-user application. Fluid formulators capture primary value through additive technology and OEM approval management, while distribution networks generate recurring revenue through aftermarket service channels globally.

|

Stage |

Key Activities |

|

Raw Material Procurement |

Sourcing of base oils and chemical additives from global suppliers |

|

Formulation & Blending |

Development and blending of fluid formulations to meet OEM specifications |

|

Quality Testing & Certification |

Performance and compliance testing against applicable industry standards |

|

Distribution & Sales |

Logistics, packaging, and sales through automotive distribution channels |

|

End-User Application |

OEM factory fill, dealer service, aftermarket retail, and fleet maintenance |

Formulation and OEM approval management stages capture the highest value in the chain, requiring specialized additive chemistry expertise and investment in multi-year OEM qualification programs. Aftermarket distribution through branded service networks represents growing recurring revenue improving manufacturer long-term margins.

Technology Landscape in the Transmission Fluids Industry

Synthetic and Ester-Based Fluid Chemistry

Polyalphaolefin (PAO) and ester-based base stocks deliver superior thermal stability, low-temperature performance, and extended drain capability. These Group IV and V base oils enable next-generation transmission fluid formulations meeting the most stringent OEM specifications for dual-clutch and continuously variable transmission systems.

Nanotechnology-Enhanced Lubricant Additives

Nano-scale friction modifiers and wear-protection additives are emerging as advanced technologies for transmission fluid performance enhancement. These additives deliver superior boundary lubrication, reduce component wear in high-stress contact zones, and extend transmission service life beyond conventional additive technology capabilities.

AI-Powered Fluid Degradation Monitoring

Machine learning algorithms integrated with on-vehicle fluid sensors enable predictive fluid life assessment. These systems analyze temperature cycles, load profiles, and fluid property changes to optimize service intervals, reducing unnecessary maintenance costs while preventing transmission damage from degraded fluid conditions.

Bio-Based Fluid Innovation

Renewable and bio-derived base stocks from vegetable oils and agricultural feedstocks are being developed as sustainable alternatives. These bio-based fluids reduce dependence on petroleum-derived base oils, offer improved biodegradability, and support corporate sustainability commitments across automotive and fleet sectors globally.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Automatic Transmission Fluid |

56.8% |

2025 |

|

Base Oil |

Mineral Oil |

47.9% |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Region |

Asia-Pacific |

39.1% |

2025 |

By Type

Automatic Transmission Fluid commands a 56.8% majority share in 2025 owing to rapid global adoption of automatic transmissions across passenger cars, SUVs, and light commercial vehicles. Rising consumer preference for driving convenience and growing hybrid vehicle production are sustaining robust ATF demand across all major automotive markets worldwide.

To access detailed market analysis, Request Sample

Manual Transmission Fluid (29.7%) maintains significant share driven by commercial vehicle applications, off-road equipment, and continued manual use in cost-sensitive markets. Others (13.5%) encompasses CVT and specialty dual-clutch fluids representing the fastest-growing type sub-segment through 2034.

By Base Oil

Mineral Oil dominates at 47.9% in 2025, driven by cost-effectiveness, broad OEM compatibility across legacy transmission platforms, and established supply chain infrastructure. Conventional mineral-based ATF remains the default choice for high-volume, cost-sensitive automotive markets across Asia-Pacific and Latin America.

Synthetic Oil (34.6%) is the fastest-growing base oil segment at approximately 3.38% CAGR, reflecting OEM mandates for high-performance ATF across premium and performance vehicles. Semi-synthetic Oil (17.5%) serves mid-tier automotive applications balancing performance and cost across mainstream vehicle segments.

Regional Market Insights

|

Region |

Share (2025) |

Overview |

|

Asia-Pacific |

39.1% |

Largest region driven by extensive automotive production and rising vehicle ownership |

|

North America |

24.8% |

Mature market with high synthetic fluid penetration and strong aftermarket demand |

|

Europe |

22.7% |

Advanced OEM specifications and growing EV-compatible fluid development underpin demand |

|

Latin America |

7.2% |

Growing vehicle fleet and expanding automotive aftermarket support demand growth |

|

Middle East & Africa |

6.2% |

Rising vehicle sales and growing aftermarket maintenance awareness drive adoption |

Asia-Pacific's 39.1% market dominance in 2025 is driven by rapid automotive production expansion and rising vehicle ownership across China, India, and Southeast Asia. Government initiatives promoting domestic automotive manufacturing and growing consumer income sustain the region's leading transmission fluid demand position.

North America at 24.8% is anchored by the United States’ sophisticated automotive aftermarket and high synthetic fluid penetration. Europe at 22.7% maintains strong demand through OEM engineering leadership and growing hybrid drivetrain adoption.

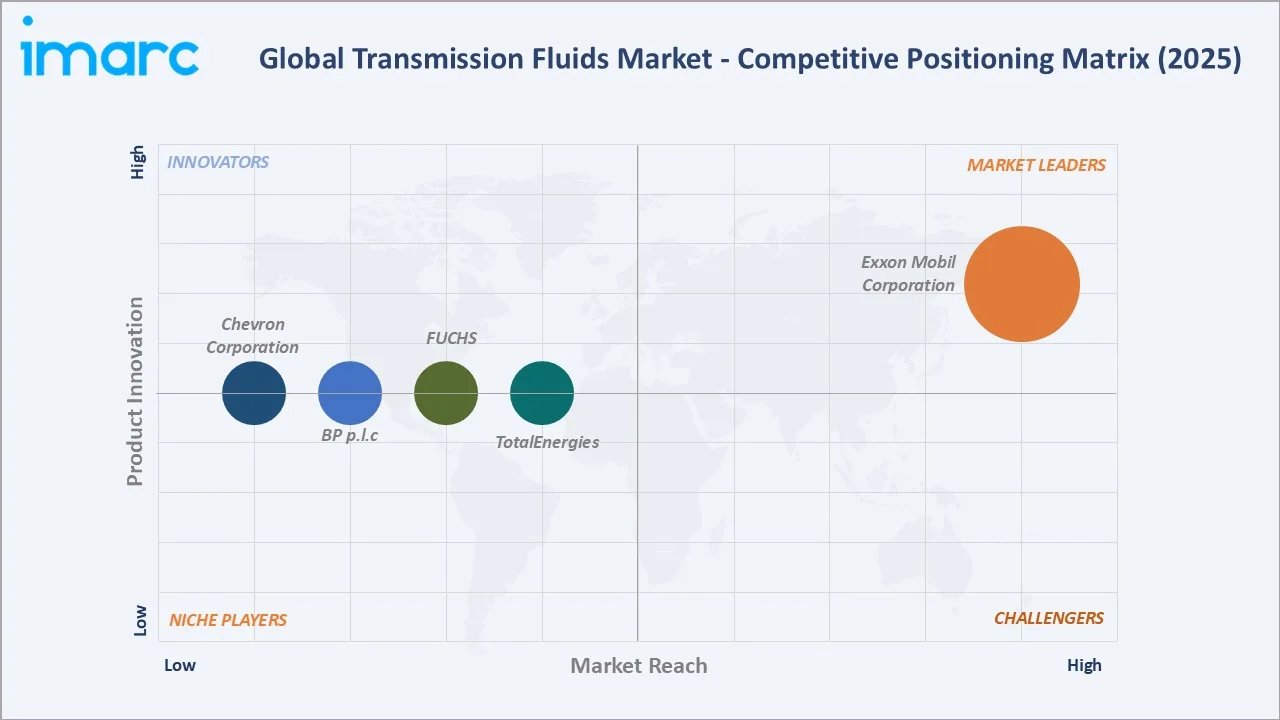

Competitive Landscape

The transmission fluids market is highly competitive, with global petrochemical majors and specialty lubricant companies collectively commanding the largest market shares. Leading players leverage OEM approval portfolios, global brand equity, and integrated base oil supply positions to maintain competitive advantage.

|

Company Name |

Key Products / Operations |

Market Position |

Global Strategic Focus |

|

Exxon Mobil Corporation |

Mobil 1 Synthetic ATF, Mobil 1 Synthetic LV ATF HP, Mobil Multi-Vehicle ATF, Mobil ATF D/M, Mobil ATF +4, Mobil ATF 3309 |

Leader |

Expanding premium synthetic ATF portfolio and deepening OEM approvals across transmission platforms globally |

|

Chevron Corporation |

Havoline Automatic Transmission Fluid Type F, Havoline Automatic Transmission Fluid MD-3, Havoline CVT, Havoline Global Multi-Vehicle ATF |

Established |

Strengthening aftermarket distribution and advancing premium synthetic fluid innovation for commercial applications |

|

BP p.l.c |

Autran Dex/Merc, Autran DX II, BP Autran Syn-295 |

Established |

Leading in synthetic and hybrid fluid formulations |

|

FUCHS |

TITAN ATF 1, TITAN ATF 3353, TITAN ATF 4134, TITAN ATF 4400, TITAN ATF 5500, TITAN ATF 6008, TITAN SINTOFLUID FE SAE 75W, TITAN SINTOFLUID SAE 75W-80 |

Established |

Focusing on specialty and OEM-approved transmission fluids for European automotive and industrial sectors |

|

TotalEnergies |

FLUIDMATIC LV MV, FLUIDMATIC XLD FE, FLUIDMATIC MV, TRANSMISSION AXLE 8 FE 75W-140, TRANSMISSION AXLE 8 FE 80W-140, TRANSMISSION AXLE 9 80W-90, TRANSMISSION GEAR 8 75W-80 |

Established |

Expanding global distribution reach and advancing bio-based and low-viscosity transmission fluid formulations |

Key players include Exxon Mobil Corporation, Chevron Corporation, BP p.l.c, FUCHS, and TotalEnergies, among others.

Key Company Profiles

Exxon Mobil Corporation

Exxon Mobil Corporation is a global leader in petroleum and petrochemical products, offering comprehensive transmission fluid solutions under the Mobil brand for automotive, commercial, and industrial applications.

- Product Portfolio: Mobil 1 Synthetic ATF, Mobil 1 Synthetic LV ATF HP, Mobil Multi-Vehicle ATF, Mobil ATF D/M, Mobil ATF +4, Mobil ATF 3309

- Strategic Focus: ExxonMobil is executing a dual strategy of deepening OEM approvals across conventional and hybrid transmission platforms while accelerating next-generation synthetic and e-compatible fluid development, reinforcing Mobil's technical leadership globally.

Chevron Corporation

Chevron Corporation is a major integrated energy company whose lubricants division markets transmission fluids under the Havoline, Texaco families globally. Chevron's Oronite additive technology division provides proprietary additive systems underpinning its OEM-approved fluid formulations.

- Product Portfolio: Havoline Automatic Transmission Fluid Type F, Havoline Automatic Transmission Fluid MD-3, Havoline CVT, Havoline Global Multi-Vehicle ATF

- Recent Developments: In August 2021, Chevron Products Company launched Delo Syn ATF 668, a fully synthetic transmission fluid designed for Allison Transmission heavy-duty truck and bus automatic transmissions. The new fluid is used for transmissions requiring TES 668 and is backward compatible with TES 389 and TES 295.

- Strategic Focus: Chevron is strengthening its position in commercial vehicle and industrial transmission fluid segments through Oronite additive technology innovation, while expanding aftermarket distribution for Havoline-branded consumer products globally.

Market Concentration Analysis

The transmission fluids market is moderately concentrated at the formulator level, with global majors including Exxon Mobil Corporation and Chevron Corporation holding significant aggregate shares through extensive OEM approval portfolios and global distribution infrastructure. Regional and specialty players compete effectively in niche segments.

Geographic manufacturing concentration in the US, Europe, and Asia creates competitive dynamics where local producers benefit from logistics advantages while global brands maintain premium positioning. Private label and retailer-branded products exert growing pricing pressure in the consumer aftermarket, compelling major brands to differentiate through technical superiority.

Investment & Growth Opportunities

Fastest-Growing Segments

Synthetic Oil-based fluids represent the highest-growth base oil segment at approximately 3.38% CAGR through 2034, capturing rising OEM synthetic mandates. Others (Type) including CVT and DCT specialty fluids lead type segment growth at approximately 3.05% CAGR, driven by advanced transmission platform proliferation.

Emerging Markets

Asia-Pacific and Latin America are emerging as significant investment frontiers. India and Southeast Asia are rapidly expanding automotive fleets while Brazil and Mexico demonstrate strong aftermarket growth potential. Rising consumer income and vehicle ownership are creating sustained demand for transmission fluids across all quality tiers.

Venture & Investment Trends

Strategic investors are increasing capital allocation to EV-compatible and bio-based transmission fluid technology companies. OEM partnerships for e-axle fluid co-development represent significant co-investment opportunities. Government clean mobility programs in Europe and China are catalyzing R&D investment in sustainable transmission fluid technologies.

Future Market Outlook (2026-2034)

The transmission fluids market is forecast to expand from USD 8.63 Billion in 2025 to USD 11.01 Billion by 2034 at a CAGR of 2.66%, driven by automotive fleet expansion, rising synthetic fluid adoption, and growing aftermarket maintenance demand across emerging and developed markets globally through the forecast horizon.

Three structural forces will shape the market through 2034: global vehicle parc expansion will sustain aftermarket replacement volumes despite EV headwinds; synthetic and specialty fluid premiumization will elevate average selling prices; and electrification will create parallel demand for novel e-axle and hybrid transmission fluid categories.

Research Methodology

Primary Research

Primary research encompassed structured interviews with transmission fluid formulators, OEM procurement specialists, automotive aftermarket distributors, and fleet maintenance managers. Primary data validated market sizing, segment shares, regional demand estimates, and technology adoption trends across the transmission fluids industry globally.

Secondary Research

Key secondary sources include OEM fluid specification documents, industry association publications, annual reports from leading lubricant manufacturers, automotive production databases, trade publications covering the lubricants industry, and market intelligence databases covering automotive and petrochemical sectors globally.

Forecasting Models

Market size estimations and growth projections were derived using combined top-down and bottom-up forecasting models incorporating automotive production analysis, vehicle parc projections, OEM fluid specification trends, and regional economic growth parameters. Scenario modelling encompassed base, optimistic, and conservative cases through 2034.

Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Segment Coverage | Type, Base Oil, Application, Region |

| Region Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Exxon Mobil Corporation, Chevron Corporation, BP p.l.c, FUCHS, TotalEnergies, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Transmission Fluids Market Report

The global transmission fluids market reached USD 8.63 Billion in 2025, reflecting sustained demand driven by global automotive fleet expansion, rising automatic transmission adoption, and robust aftermarket maintenance activity across Asia-Pacific, North America, and Europe.

The market is projected to reach USD 11.01 Billion by 2034, growing at a CAGR of 2.66% during 2026-2034, driven by vehicle fleet expansion, synthetic fluid premiumization, growing emerging market aftermarkets, and emerging demand for EV-compatible transmission fluid products.

Automatic Transmission Fluid leads with a 56.8% share in 2025, driven by rising consumer preference for automatic and CVT transmissions globally. This segment is expected to maintain its leadership as automatic vehicle penetration continues rising across Asia-Pacific markets.

Mineral Oil commands the largest base oil share at 47.9% in 2025. Its cost-effectiveness and broad OEM compatibility sustain leadership in high-volume markets. However, Synthetic Oil is growing fastest at approximately 3.38% CAGR as premium formulations become OEM-mandated for advanced platforms.

Asia-Pacific dominates with a 39.1% share in 2025, underpinned by the world's largest automotive production base across China, India, Japan, and South Korea. The region is expected to maintain leadership through 2034 as vehicle fleet expansion and rising aftermarket activity continue.

Key market drivers include rising global automotive production and sales, increasing demand for automatic transmissions, stringent OEM fluid specifications promoting premium product adoption, and robust growth in automotive aftermarket maintenance demand across both developed and emerging global markets.

Major challenges include long-term structural headwinds from battery electric vehicle adoption, extended service intervals reducing replacement frequency, base oil price volatility, and intense competition from private label and low-cost alternative products across cost-sensitive market segments.

Leading companies include Exxon Mobil Corporation, Chevron Corporation, BP p.l.c, FUCHS, and TotalEnergies, among others.

Key emerging technologies include advanced synthetic PAO and ester-based fluid chemistry enabling long-drain performance, nanotechnology-enhanced additive systems for superior wear protection, AI-powered fluid condition monitoring for predictive maintenance, and bio-based fluid innovation driven by sustainability mandates globally.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)