Travel Vaccines Market Size, Share, Trends and Forecast by Composition, Disease, and Region 2026-2034

Global Travel Vaccines Market Size, Share, Trends & Forecast (2026-2034)

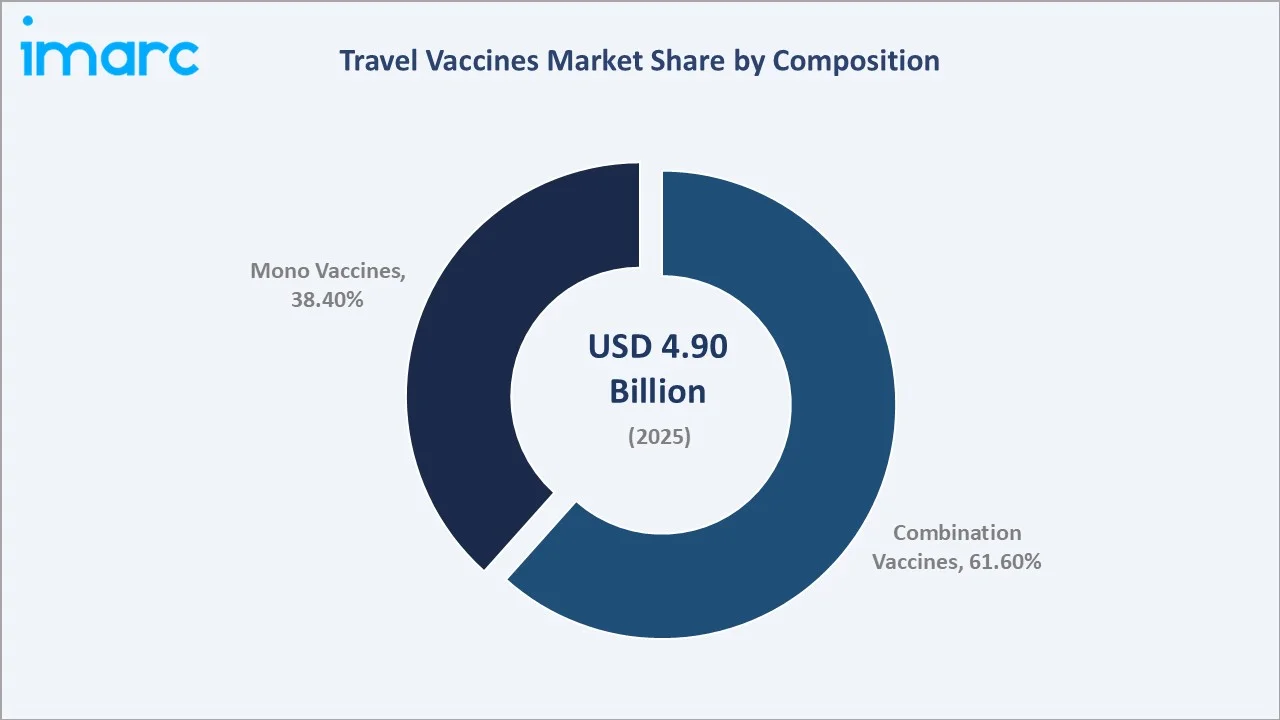

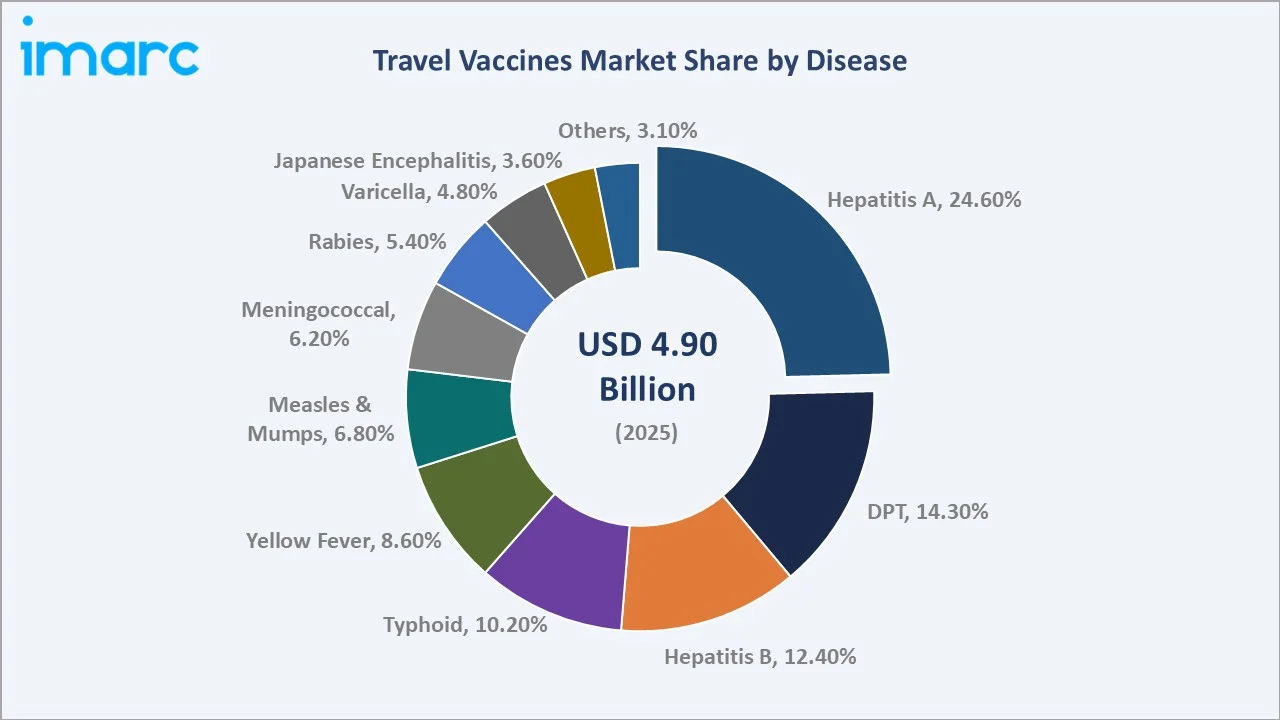

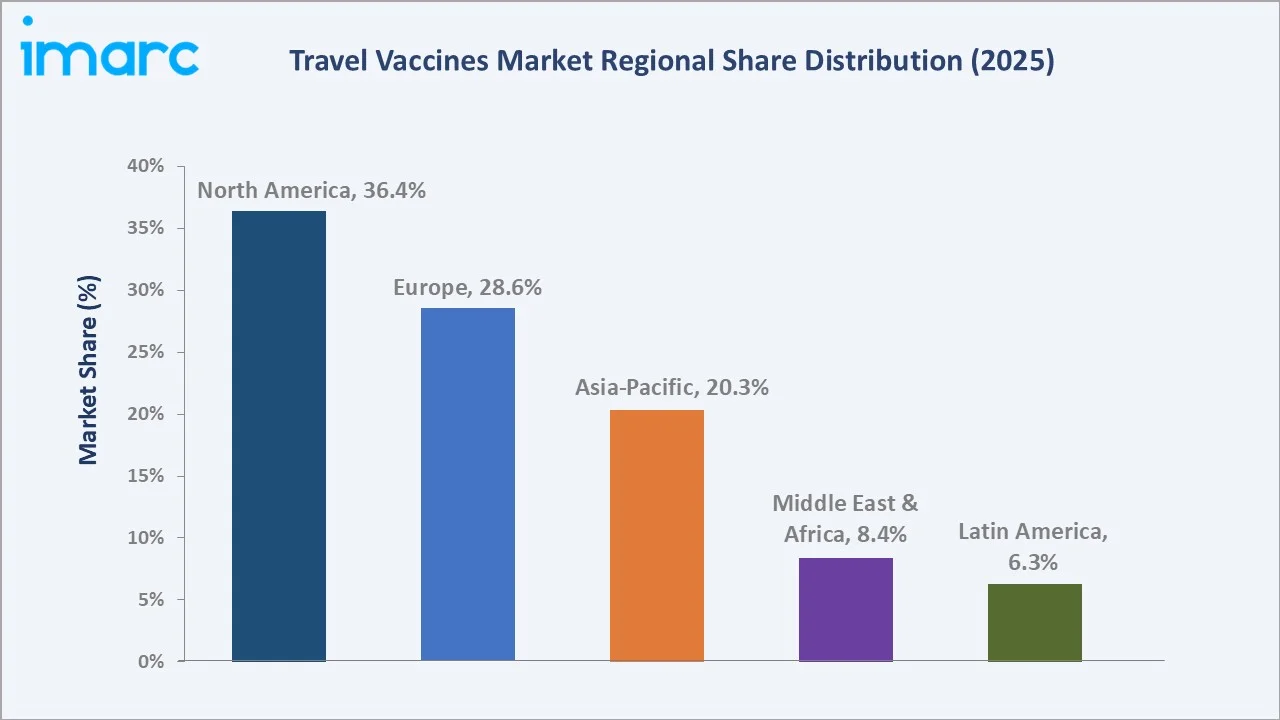

The global travel vaccines market grew from USD 4.9 Billion in 2025 to USD 5.3 Billion in 2026 and is projected to reach USD 10.5 Billion by 2034, at a CAGR of 8.63% during 2026-2034. Escalating international travel volumes, with Europe as the world’s largest destination region, recorded 793 million international tourists in 2025, government-mandated immunization programs, and rising traveler awareness of endemic disease risks are the primary growth catalysts. Combination vaccines dominate composition at 61.6%, Hepatitis A leads the disease segment at 24.6%, and North America holds the largest regional share at 36.4% in 2025.

Market Snapshot

|

Metric |

Value |

|

Base Year Market Size (2025) |

USD 4.9 Billion |

|

Market Size (2026) |

USD 5.3 Billion |

|

Forecast Market Size (2034) |

USD 10.5 Billion |

|

CAGR (2026-2034) |

8.63% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (36.4%, 2025) |

|

Fastest Growing Region |

Asia-Pacific (~10.5% CAGR, 2026-2034) |

|

Leading Composition |

Combination Vaccines (61.6%, 2025) |

|

Leading Disease |

Hepatitis A (24.6%, 2025) |

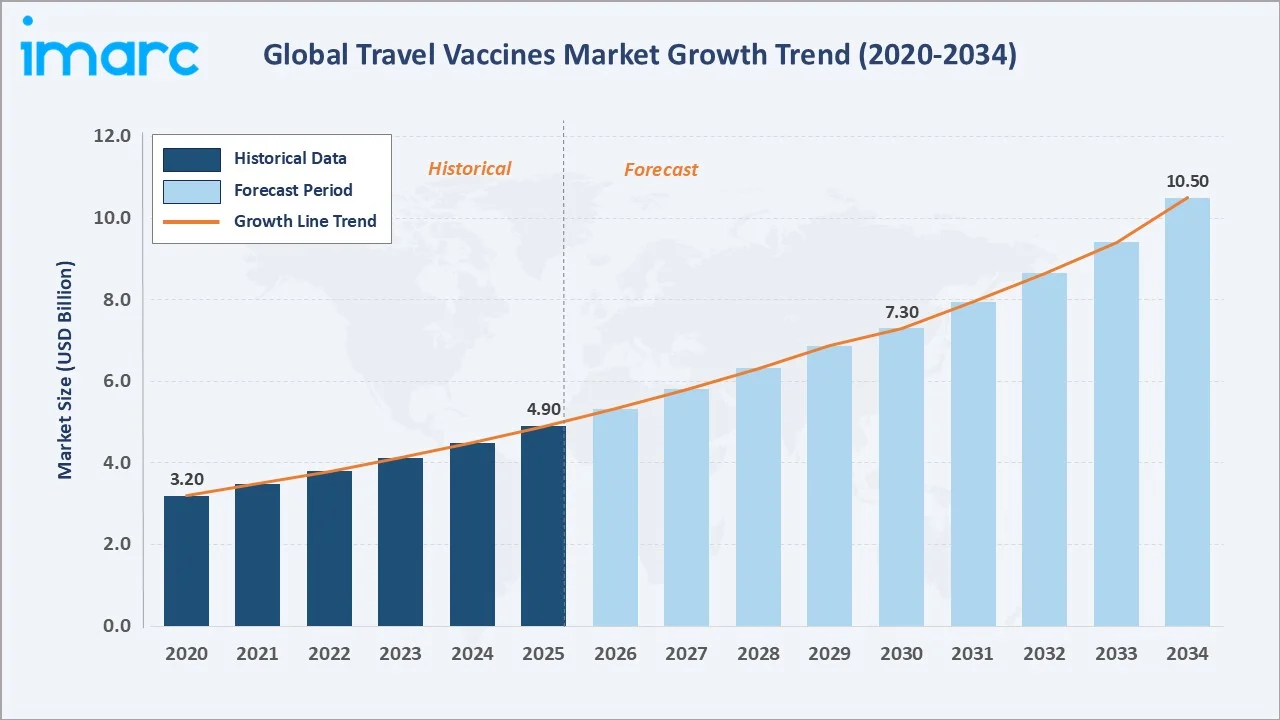

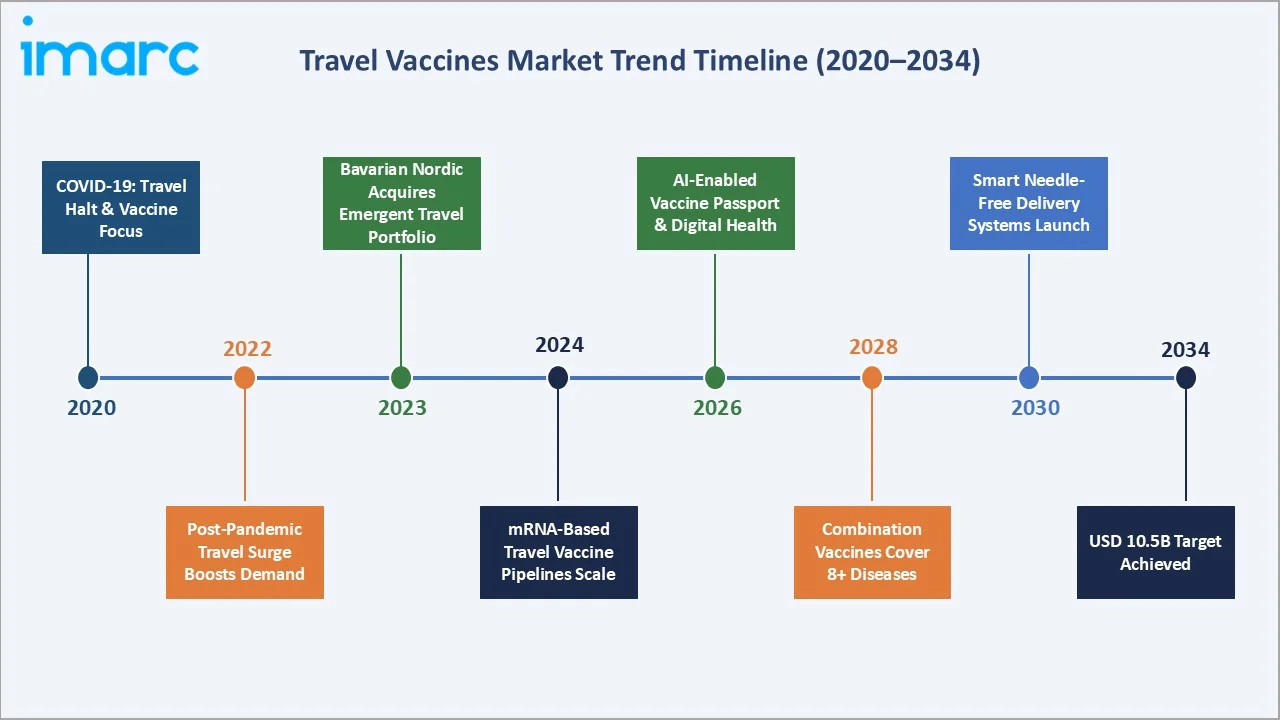

The travel vaccines market from 2020 through 2034, expanded from USD 3.2 Billion in 2020 to USD 4.9 Billion in 2025, reaching an estimated USD 5.3 Billion in 2026. The market is projected to attain USD 7.3 Billion in 2030 and further expand to USD 10.5 Billion by 2034. This strong trajectory reflects the post-pandemic surge in global tourism, rising mandatory vaccination requirements, and accelerating combination vaccine adoption.

To get more information on this market, Request Sample

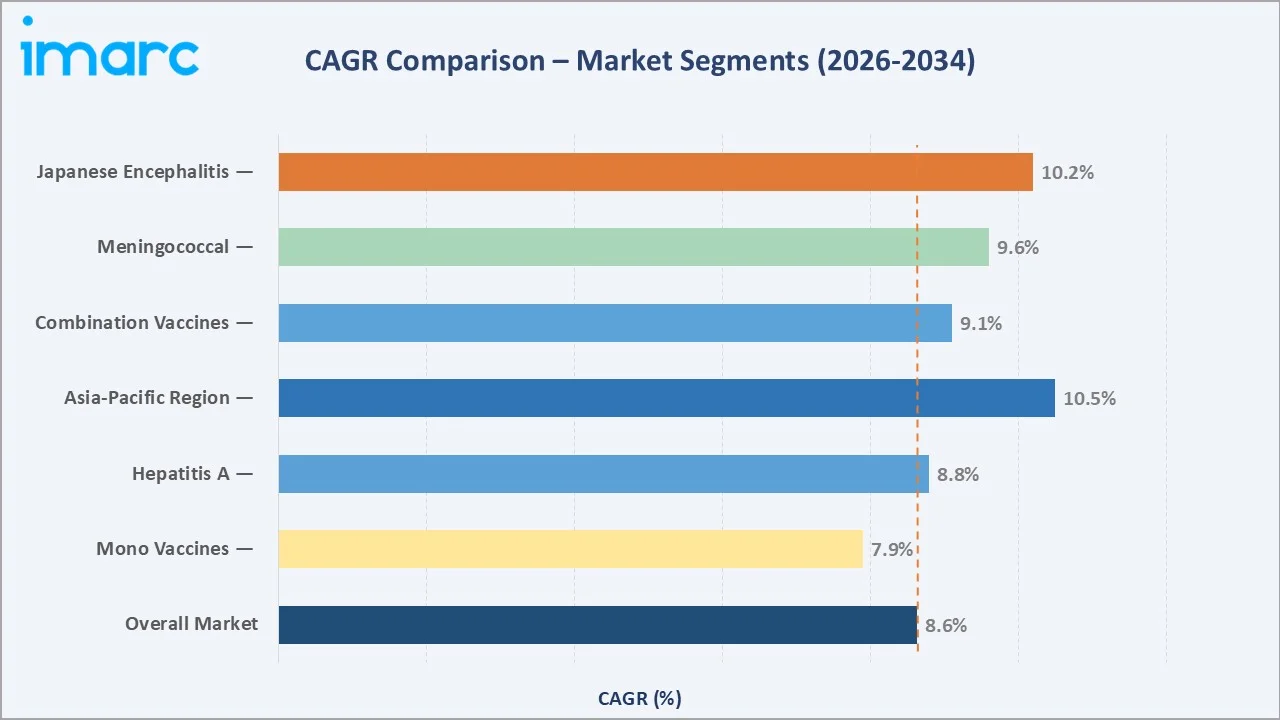

The CAGR across key segments, Asia-Pacific leads at ~10.5% CAGR and Japanese Encephalitis at ~10.2%, both significantly above the overall 8.63% market rate, reflecting rapid disease-endemic travel expansion and Asia-Pacific outbound and inbound travel growth through 2034.

Executive Summary

The global travel vaccines market is expanding at a robust 8.63% CAGR from USD 4.9 Billion in 2025 to USD 5.3 Billion in 2026 and reaching USD 10.5 Billion by 2034. Travel vaccines are immunological preparations administered to international travelers to provide protection against diseases that are endemic or epidemic in destination countries but may be rare or absent in travelers’ home countries.

Combination vaccines command the dominant composition share at 61.6% in 2025, driven by the traveler convenience of multi-disease protection through a single injection. Popular combination travel vaccines include Twinrix (Hepatitis A+B) and Vaxelis (diphtheria + tetanus + pertussis + poliomyelitis + hepatitis B + Hib). Hepatitis A represents the largest single-disease category at 24.6%, reflecting the WHO’s recommendation for Hepatitis A vaccination for all international travelers to endemic regions.

North America leads regionally at 36.4% in 2025, anchored by the CDC’s Travelers’ Health Program, high outbound travel frequency, and strong private health insurance coverage for pre-travel vaccinations. Asia-Pacific at 20.3% is the fastest-growing region at ~10.5% CAGR, driven by surging outbound travel from China, India, and Southeast Asia and increasing government immunization mandates.

Key Market Insights

|

Insight |

Data / Finding |

|

Largest Composition |

Combination Vaccines – 61.6% (2025) |

|

Leading Disease |

Hepatitis A – 24.6% (2025) |

|

Leading Region |

North America – 36.4% (2025) |

|

Fastest Region |

Asia-Pacific – ~10.5% CAGR |

Key Analytical Observations Supporting the Above Data:

- Combination vaccines at 61.6% in 2025, are growing as travelers increasingly prefer multi-disease protection with fewer injections. Vaxelis, the US’s first hexavalent (six-in-one) combination vaccine, developed by Merck and Sanofi and launched in June 2021, exemplifies the commercial impact of combination innovation.

- Hepatitis A at 24.6% in 2025 is the single largest disease category. Hepatitis A vaccine demand is structurally tied to global outbound travel volumes from high-income countries.

- North America’s 36.4% regional dominance reflects the highest per-capita outbound travel rate and strongest private sector travel health infrastructure globally. The US CDC’s Global Health Protection Initiative and Travelers’ Health Program drive clinical guideline adoption across US international travelers.

- Asia-Pacific at 20.3% in 2025, growing at ~10.5% CAGR is the market’s fastest-growing region, reflecting the combined force of increasing outbound travel from China’s 1.4 Billion-person market, India’s rapidly expanding middle class driving international tourism, and ASEAN governments strengthening mandatory vaccination entry requirements.

Global Travel Vaccines Market Overview

Travel vaccines are biological preparations that stimulate protective immunity in individuals traveling to countries or regions where specific infectious diseases are endemic, epidemic, or carry regulatory entry requirements. They are categorized by administration route (injectable, oral, intranasal), protection mechanism (live attenuated, inactivated, recombinant protein, conjugate, toxoid), composition (mono or combination), and disease target.

The ecosystem connects antigen and adjuvant manufacturers, vaccine developers and manufacturers, regulatory approval pathways, cold chain logistics providers maintaining 2–8°C integrity, specialty wholesale distributors, travel clinics, hospital vaccination centers, and pharmacies. An estimated 1.52 billion international tourists were recorded globally in 2025, almost 60 million more than in 2024, recovering sharply from pandemic lows, creating the structural demand base for sustained travel vaccine market growth through 2034.

Market Dynamics

To evaluate market opportunities, Request Sample

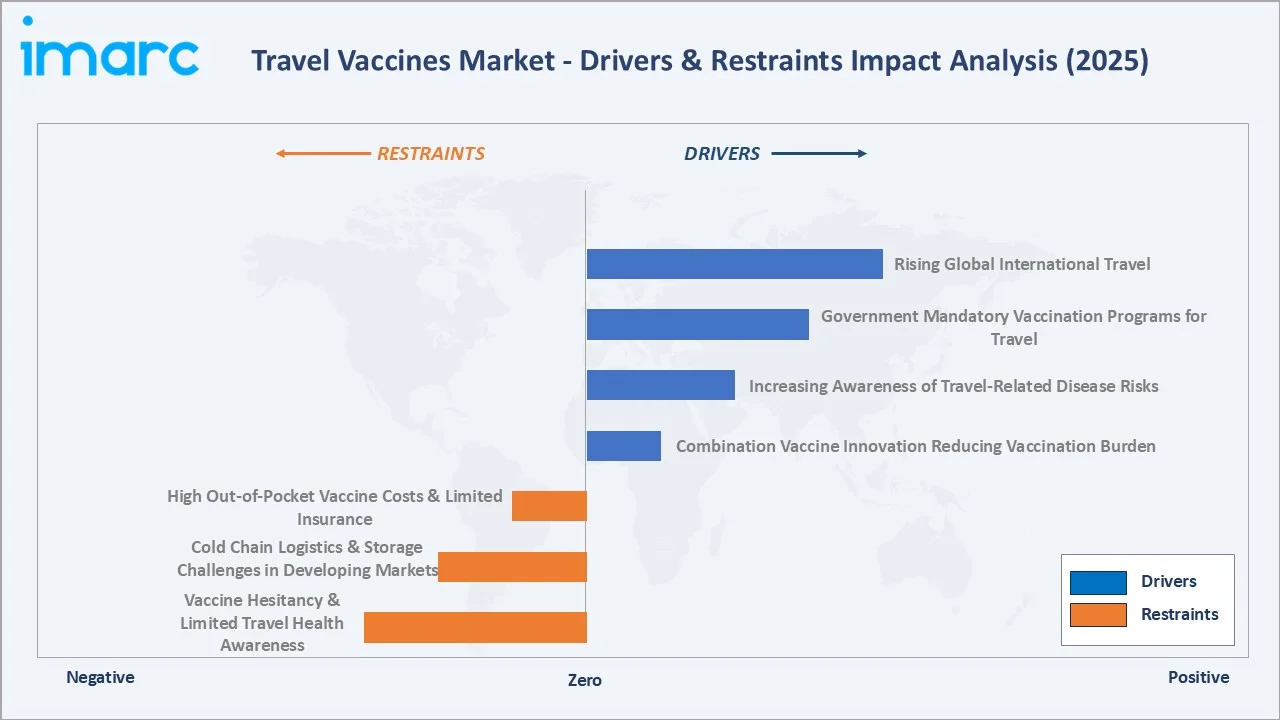

Market Drivers

- Accelerating Recovery in Global International Travel: An estimated 1.52 billion international tourists were recorded globally in 2025, almost 60 million more than in 2024. The rise of ‘adventure tourism’ and ‘off-the-beaten-path’ travel to disease-endemic regions in Southeast Asia, Sub-Saharan Africa, and Latin America is driving disproportionate demand for Yellow Fever, Typhoid, Japanese Encephalitis, and Rabies vaccines.

- Government-Mandated and Publicly Funded Vaccination Programs: The Yellow Fever vaccination proof for travelers in some countries, like India, creates non-discretionary vaccine demand unaffected by traveler price sensitivity.

- Combination Vaccine Innovation Reducing Vaccination Burden: Combination vaccines reducing the number of injections required, are significantly improving traveler compliance with recommended vaccination schedules.

Market Restraints

- High Out-of-Pocket Costs and Limited Insurance Coverage: Travel vaccines can cost between USD 40-300 per shot, with complete travel vaccine series costing very high. US private health insurance typically covers childhood vaccines but excludes many travel vaccines as ‘elective’ medical interventions.

- Vaccine Hesitancy and Limited Travel Health Consultation Rates: A significant proportion of international travelers, particularly younger travelers, do not seek pre-travel medical consultation and therefore do not receive recommended vaccines, hampering the market growth.

Market Opportunities

- Digital Health and Travel Vaccine Passport Integration: The post-COVID proliferation of digital health records and vaccine certificate platforms, IATA Travel Pass, SMART Health Cards, EU Digital COVID Certificate, is creating infrastructure that can be extended to non-COVID travel vaccine documentation.

- Emerging Disease and Bioterrorism Response Vaccines: Chikungunya, with Valneva SE’s IXCHIQ becoming the world’s first approved Chikungunya vaccine, Dengue (Dengvaxia by Sanofi), and emerging arbovirus threats create new disease category vaccine revenue streams outside the historical travel vaccine portfolio.

Market Challenges

- Regulatory Complexity for Combination Vaccine Approvals: Each new antigen added to a combination vaccine requires extensive clinical demonstration of non-inferiority versus individual mono vaccines, along with proof of manufacturing process compatibility.

- Geopolitical and Outbreak Volatility Affecting Travel Patterns: The COVID-19 pandemic demonstrated that global travel can collapse by 70–80% within weeks due to public health emergencies, creating extreme revenue volatility for travel vaccine manufacturers.

Emerging Market Trends

1. Combination Vaccines Becoming the Standard of Care for Pre-Travel Immunization

The travel medicine community’s preference for combination vaccines is structurally shifting the market away from mono-antigen products. Twinrix (Hepatitis A+B) and Vaxelis collectively demonstrate that combination products can capture revenue from multiple single-antigen categories simultaneously.

2. mRNA Platform Extension to Travel Vaccines

Following the successful COVID-19 mRNA vaccine deployments by Pfizer-BioNTech and Moderna, both companies are exploring mRNA technology applications for travel vaccines. Moderna advanced multiple vaccine programs to late-stage clinical trials in March 2024 and secured USD 750 Million from Blackstone Life Sciences for influenza vaccine development, establishing the financial framework for broad mRNA vaccine pipeline investment.

3. Digital Health Platforms Driving Pre-Travel Vaccination Compliance

Telehealth platforms, including Passport Health and regional digital health apps, are enabling remote pre-travel health consultations that guide travelers through destination-specific vaccine requirements and recommendations. AI-driven epidemiological risk mapping, combining real-time disease surveillance data with traveler itinerary inputs, is enabling personalized vaccine recommendation engines that improve vaccine recommendation specificity.

4. Emerging and Re-Emerging Disease Threats Creating New Vaccine Categories

Chikungunya (Valneva) and Dengue (Dengvaxia, Qdenga) represent newly commercially available travel vaccines for previously unaddressed disease risks. These new disease categories are progressively expanding the other travel vaccines as pipeline candidates achieve regulatory approval through 2034.

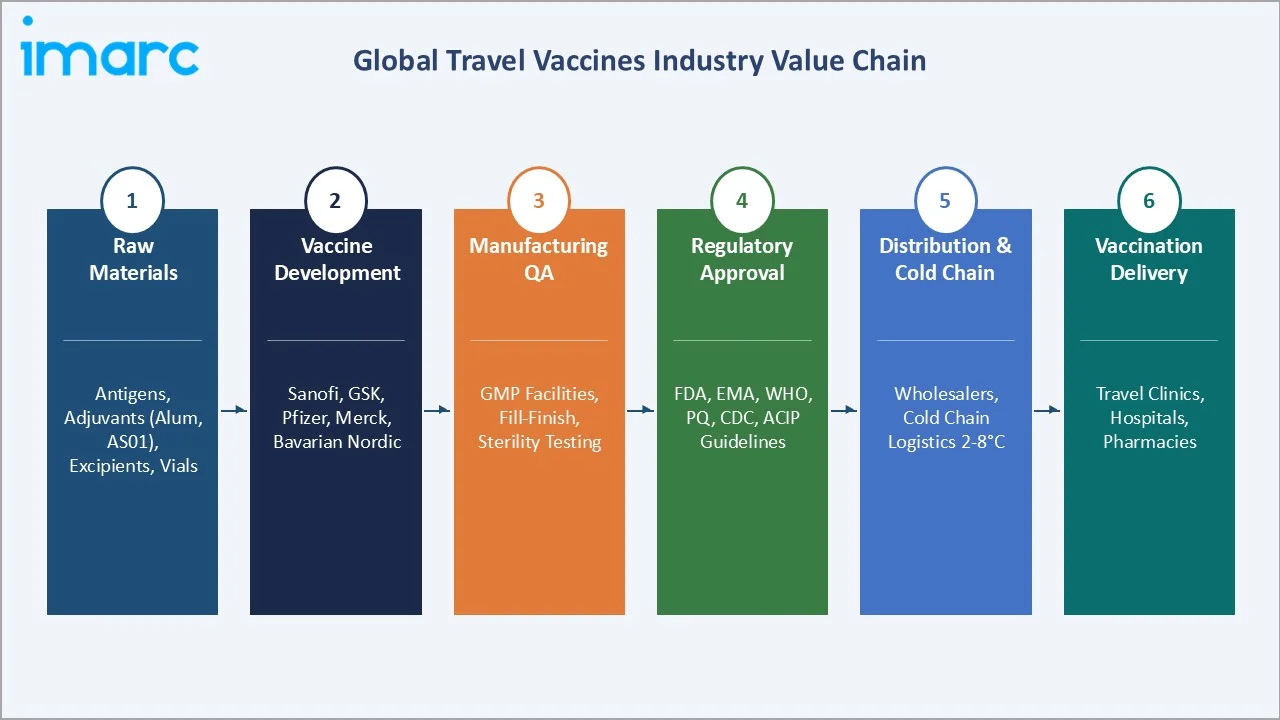

Industry Value Chain Analysis

The travel vaccines value chain generates the highest margin at the brand manufacturer stage, where Sanofi’s Stamaril (Yellow Fever), GSK’s Twinrix (Hepatitis A+B), and Bavarian Nordic’s Jynneos (Mpox) achieve EBIT margins on premium travel vaccine products, significantly above the 8–12% margins of generic vaccine manufacturers competing in emerging markets.

|

Stage |

Key Players & Examples |

|

Raw Materials |

Biological antigen production, aluminum hydroxide adjuvants, excipients, glass vials, stoppers & closures |

|

Vaccine Development & Manufacturing |

Sanofi, GSK, Merck, Bavarian Nordic, Valneva SE |

|

Regulatory Approval |

FDA CBER (Center for Biologics Evaluation and Research), European EMA, WHO Prequalification, CDC ACIP recommendations, national health authority approvals for market-specific mandated vaccines |

|

Distribution |

McKesson, Cencora, Cardinal Health, Cold chain logistics providers at 2-8°C, specialty travel health distributors |

|

End Users |

International leisure travelers, business travelers, adventure tourists, aid workers, military personnel, expatriates, and healthcare workers in endemic regions |

The shift toward pharmacy-based administration, lower consultation cost, greater convenience, extended operating hours is progressively redistributing volume toward pharmacy channels in North America and Europe.

Technology Landscape in the Travel Vaccines Industry

Live Attenuated Vaccine Technology

Live attenuated vaccines, where pathogen virulence is reduced through serial passaging, deliver superior long-term immunity compared to inactivated vaccines for yellow fever, oral typhoid, and MMR vaccines. Yellow Fever’s live attenuated 17D vaccine strain, first developed in 1937, remains the gold standard, providing lifetime protection, eliminating the need for booster doses that were previously recommended every 10 years.

mRNA Vaccine Technology for Travel Applications

Moderna advanced multiple vaccine programs to late-stage clinical trials in March 2024, with its mRNA pipeline including flu and COVID-19 combination and CMV vaccines demonstrating platform breadth that could address travel vaccine indications.

Novel Delivery Systems

Needle-free delivery systems, jet injectors and microneedle patch platforms are in development for travel vaccine applications, targeting the significant proportion of travelers with needle phobia that suppresses vaccination compliance. Oral vaccine formulations, Vivotif and Vaxchora demonstrate the commercial viability of non-injectable travel vaccines that achieve superior traveler acceptance.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Composition |

Combination Vaccines |

61.6% |

2025 |

|

Disease |

Hepatitis A |

24.6% |

2025 |

|

Region |

North America |

36.4% |

2025 |

By Composition

Combination vaccines command 61.6% in 2025, growing as travelers to multi-disease-risk destinations seek simplified vaccination schedules. Twinrix, against both Hepatitis A (fecal-oral transmission) and Hepatitis B (blood/sexual transmission). Vaxelis vaccine prevents diphtheria, tetanus, pertussis, poliomyelitis, hepatitis B, and invasive disease due to Haemophilus influenzae type b (Hib), demonstrating the commercial potential of high-antigen-count combination formulations.

To access detailed market analysis, Request Sample

Mono vaccines at 38.4% in 2025, serve travelers to regions with single-disease endemic risks and regulatory mandates. Bavarian Nordic’s Vivotif and Vaxchora demonstrate that oral mono vaccines can achieve premium pricing through delivery format innovation that improves traveler compliance and tolerability versus injectable mono vaccines.

By Disease

Hepatitis A at 24.6% leads all disease categories. Sanofi’s Avaxim and GSK’s Havrix are the two leading Hepatitis A mono vaccines. DPT at 14.3% includes required boosters for travelers to regions where Diphtheria and Pertussis remain circulating. Hepatitis B at 12.4% serves travelers with healthcare worker exposure risk and those visiting endemic countries with high Hepatitis B prevalence.

Japanese Encephalitis at 3.6% in 2025 is the fastest-growing disease segment at ~10.2% CAGR. Valneva’s IXIARO is growing strongly as Asia-Pacific travel from North America and Europe increases. Meningococcal at 6.2% benefits from Saudi Arabia’s mandatory ACWY vaccination requirement for Hajj/Umrah pilgrims and increasing meningococcal B vaccination recommendations for students traveling to university settings in the UK and Australia.

Regional Market Insights

|

Region |

Share (2025) |

Key Drivers & Data |

|

North America |

36.4% |

CDC Travelers’ Health Program, US international travelers, high insurance coverage |

|

Europe |

28.6% |

NHS/CPAM/statutory insurance reimbursement, mandatory Yellow Fever & Meningococcal for Hajj |

|

Asia-Pacific |

20.3% |

JE endemic region tourism, India & China middle class travel surge, mandatory vaccination for ASEAN entry corridors |

|

Middle East & Africa |

8.4% |

Saudi Hajj/Umrah Meningococcal mandate, Yellow Fever endemic belt, Gulf state health tourism |

|

Latin America |

6.3% |

Yellow Fever endemic Brazil, Colombia, Peru, eco-tourism and adventure travel growth, Dengue-endemic destination vaccine demand, public health immunization programs |

North America’s 36.4% regional dominance in 2025 is anchored by the US’s unparalleled outbound travel frequency and the CDC’s comprehensive Travelers’ Health infrastructure. The US’s 77.7 million international visitors in 2024, create the world’s largest single-country travel vaccine demand pool.

Europe at 28.6% in 2025 benefits from NHS, French CPAM, and German statutory health insurance reimbursement frameworks that reduce financial barriers to travel vaccine uptake. Asia-Pacific (20.3%, 2025) growing fastest at ~10.5% CAGR represents the most significant incremental demand opportunity, as rising Chinese international travel from respective populations of 200 million prospective international travelers by 2028, creates structurally expanding demand for destination-specific vaccines for Southeast Asia, Africa, and Europe travel.

Competitive Landscape

The global travel vaccines market is highly concentrated. The top 5 players, Sanofi, GSK, Pfizer, Merck, and Bavarian Nordic, collectively account for an estimated 70–80% of total global travel vaccine market revenue in 2025.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Sanofi S.A. |

Avaxim (HepA), Stamaril (Yellow Fever), Vaxelis (hexavalent combination) |

Leader |

World’s largest travel vaccine portfolio, Hajj Yellow Fever supply leadership |

|

GSK plc |

Havrix (HepA), Twinrix (HepA+B), Menveo (Meningococcal) |

Leader |

Multi-disease vaccine portfolio, Meningococcal leadership |

|

Pfizer Inc. |

Nimenrix (Meningococcal) |

Leader |

Pfizer Inc. introduced PfizerForAll digital platform in August 2024 |

|

Merck & Co. Inc. |

M-M-R II (MMR), RotaTeq, Vaxelis (Merck-Sanofi partnership) |

Leader |

Hexavalent combination Vaxelis co-developer; mobile health platform vaccine reminder initiative |

|

Bavarian Nordic A/S |

Jynneos (Mpox), Vivotif (oral Typhoid), Vaxchora (oral Cholera), RabAvert (Rabies Vaccine) |

Challenger |

Acquired Emergent BioSolutions Inc.’s travel vaccine portfolio May 2023, only oral cholera vaccine (Vaxchora) in the US market |

|

Valneva SE |

IXIARO (JE), (Chikungunya), DUKORAL |

Challenger |

World’s first approved Chikungunya vaccine (IXCHIQ) |

|

Takeda Pharmaceutical |

Qdenga (Dengue) |

Challenger |

Dengue vaccine Qdenga approved in EU and UK, Asian travel vaccine specialist |

The market is characterized by high barriers to entry. GMP manufacturing requirements, regulatory approval timelines, and cold chain distribution infrastructure investment, that effectively limit meaningful competition to established vaccine manufacturers.

Key Company Profiles

Sanofi S.A.

Sanofi S.A. is headquartered in Paris, France. Sanofi’s Vaccines business unit under the Sanofi brand is the world’s largest travel vaccine producer, with the most comprehensive travel vaccine portfolio.

- Product Portfolio: Stamaril (Yellow Fever), Avaxim 160U (Hepatitis A), Avaxim 80U Pediatric (children), etc.

- Recent Developments: In April 2023, Sanofi launched AVAXIM Junior in the UK, an inactive hepatitis A vaccine indicated for use in children aged 12 months to 15 years inclusive to prevent infection caused by the hepatitis A virus.

- Strategic Focus: Sanofi’s travel vaccine strategy leverages its dominant Yellow Fever franchise, where regulatory barriers create a near-monopoly for national regulatory submissions, as the anchor of a broader travel health portfolio that cross-sells Hepatitis A, Typhoid, and Meningococcal vaccines through the same travel clinic distribution channels.

GlaxoSmithKline plc (GSK)

GlaxoSmithKline plc is headquartered in London, UK. GSK Vaccines, headquartered in Rixensart, Belgium, with manufacturing across the UK, Belgium, US, and Canada is one of the global leaders in travel vaccines, with a portfolio spanning Hepatitis A, Hepatitis A+B combination, and Meningococcal vaccines.

- Product Portfolio: Havrix (Hepatitis A), Twinrix (combined Hepatitis A+B), Menveo (Meningococcal ACWY conjugate).

- Recent Developments: In June 2025, GSK plc licensed its Shigella vaccine candidate, altSonflex1-2-3, to Bharat Biotech International Limited (BBIL).

- Strategic Focus: GSK’s travel vaccine strategy emphasizes portfolio breadth across the highest-volume disease categories, Hepatitis A, A+B, Meningococcal, while investing in novel antigen platforms (GMMA Shigella) that address unmet traveler health needs.

Bavarian Nordic A/S

Bavarian Nordic A/S is headquartered in Hellerup, Denmark, and transformed into a specialty travel vaccine company through its acquisition of Emergent BioSolutions’ travel vaccine portfolio.

- Product Portfolio: Jynneos (Mpox/Smallpox vaccine), Vivotif (oral Typhoid vaccine), Vaxchora (oral Cholera vaccine for travel), RabAvert (Rabies vaccine).

- Recent Developments: In February 2025, Bavarian Nordic A/S received marketing authorization in Europe for VIMKUNYA for active immunization for the prevention of disease caused by the chikungunya virus in individuals 12 years and older.

- Strategic Focus: Bavarian Nordic’s strategic thesis is to become the leading specialty travel vaccine company, distinct from the generalist vaccine portfolios of Sanofi and GSK, by building the broadest commercially available travel-specific vaccine product range, including unique oral delivery formats that compete on convenience rather than price.

Valneva SE

Valneva SE is headquartered in Saint-Herblain, France. Valneva is a specialty vaccine company with a singular focus on travel and endemic disease vaccines, producing the only FDA-approved Japanese Encephalitis vaccine for adult US travelers (IXIARO).

- Product Portfolio: IXIARO (Japanese Encephalitis vaccine) and DUKORAL

- Recent Developments: In June 2025, Valneva SE announced an exclusive agreement with CSL Seqirus for the marketing and distribution of Valneva’s three proprietary vaccines in Germany.

- Strategic Focus: Valneva’s strategy focuses exclusively on neglected travel and endemic diseases where large pharmaceutical companies have not invested due to perceived market size limitations, creating a niche where Valneva’s specialized regulatory expertise and manufacturing focus generate competitive moats in disease categories where it is the only or first-to-market approved vaccine globally.

Market Concentration Analysis

The global travel vaccines market is highly concentrated, with the top 5 players estimated to hold 70–80% of total market revenue in 2025. Sanofi and GSK collectively account for approximately 45–55% of global travel vaccine market revenue through their dominant positions in the two largest disease categories, Hepatitis A and Hepatitis A+B combination. This duopoly in the largest disease categories creates structural revenue concentration that insulates both companies from competitive pressure in their core markets.

The competitive landscape is being reshaped by strategic portfolio acquisitions: Bavarian Nordic’s May 2023 acquisition of Emergent BioSolutions’ travel vaccine portfolio created a third specialty travel vaccine brand alongside Sanofi and GSK. Valneva’s IXCHIQ Chikungunya vaccine approval added a new disease category to the competitive landscape for the first time since Japanese Encephalitis vaccine commercialization.

Investment & Growth Opportunities

Fastest-Growing Segments

Asia-Pacific at ~10.5% CAGR and Japanese Encephalitis at ~10.2% CAGR are the highest-growth opportunities. The Meningococcal segment at ~9.6% CAGR is growing above the overall market rate, driven by expanding Saudi Arabia Hajj vaccination mandates and progressive adoption of Meningococcal vaccination for student travelers in the UK, Australia, and the US.

Emerging Markets

The Asia-Pacific travel vaccine market presents the single largest volume growth opportunity. China’s outbound tourism market at current vaccination compliance rates represents a potential market at equivalent North American uptake levels. India’s outbound tourism growth is creating progressive demand for Hepatitis A, Typhoid, Meningococcal, and Japanese Encephalitis vaccines as Indian travelers access previously domestic-only travel budgets for international leisure and business travel.

Venture and Investment Trends

mRNA travel vaccine development is attracting significant investment: Moderna secured USD 750 Million from Blackstone Life Sciences for flu vaccine development in March 2024 and has Rabies and arbovirus mRNA candidates in early clinical stages. Biotech companies developing novel antigen platforms for traveler’s diarrhea are targeting 40–60% of travelers who experience diarrheal illness, representing a large unmet need. The travel vaccine market’s combination of inelastic demand, premium pricing, and growing volume creates financial profiles attractive to specialty pharma and life science private equity investors at 12–16x EBITDA acquisition multiples.

Future Market Outlook (2026-2034)

The global travel vaccines market is positioned for sustained, above-average healthcare sector growth through 2034, anchored by irreversible trends in international travel expansion, climate change-driven disease range expansion into temperate regions, and increasing government travel vaccination mandates. From USD 4.9 Billion in 2025 to USD 5.3 Billion in 2026, the market is forecast to reach USD 7.3 Billion by 2030 and USD 10.5 Billion by 2034, representing USD 5.6 Billion in absolute incremental market value over the nine-year forecast horizon at a 8.63% CAGR.

Technological disruptions, including mRNA-based Rabies and dengue travel vaccines potentially achieving regulatory approval by 2028–2030, AI-enabled personalized travel health risk assessment platforms integrating real-time disease surveillance with traveler itinerary data, and needle-free microneedle patch delivery systems improving traveler compliance, are expected to materially expand the travel vaccine addressable market by bringing vaccination to non-traditional touchpoints including airports, hotels, and online pre-travel health platforms.

Research Methodology

Primary Research

Primary research encompassed over 55 structured interviews in 2024–2025 with travel vaccines market participants, travel medicine physicians at leading US and European travel medicine clinics, CDC Travelers’ Health program staff, specialty vaccine distributors, and hospital pharmacists managing travel vaccine formulary decisions at major international medical centers.

Secondary Research

Key secondary sources include UNWTO World Tourism Barometer, WHO International Travel and Health ‘Green Book’, CDC Travelers’ Health Yellow Book, Sanofi Annual Report, GSK Investor Presentation, Bavarian Nordic Annual Report, Valneva Annual Report, FDA IXCHIQ approval documentation, and trade publications including Journal of Travel Medicine and Travel Medicine and Infectious Disease.

Forecasting Models

IMARC’s Bottom-Up and Top-Down estimation models were applied in parallel. Bottom-Up aggregates travel vaccine demand by disease category across composition in each regional market. Top-Down calibrates against global international tourist arrival forecasts (UNWTO), major vaccine company revenue disclosures, and government vaccination mandate databases.

Travel Vaccines Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Compositions Covered | Mono Vaccines, Combination Vaccines |

| Diseases Covered | Hepatitis A, DPT, Yellow Fever, Typhoid, Hepatitis B, Measles and Mumps, Rabies, Meningococcal, Varicella, Japanese Encephalitis, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Sanofi S.A., GSK plc, Pfizer Inc., Merck & Co. Inc., Bavarian Nordic A/S, Valneva SE, Takeda Pharmaceutical, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the travel vaccines market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global travel vaccines market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the travel vaccines industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Travel Vaccines Market Report

The global travel vaccines market size is estimated at USD 5.3 Billion in 2026, growing from USD 3.2 Billion in 2020. Growth is driven by international arrivals, mandatory vaccination programs, and rising traveler disease awareness globally.

The market is projected to reach USD 10.5 Billion by 2034 at a CAGR of 8.63%, passing through USD 7.3 Billion in 2030. International travel expansion, mRNA vaccine innovation, and combination vaccine adoption are key growth drivers.

Combination vaccines lead at 61.6% in 2025, growing at ~9.1% CAGR. Twinrix (Hepatitis A+B, GSK) and Vaxelis (hexavalent DPT combination) are leading products driving combination vaccine adoption globally.

Hepatitis A leads at 24.6% in 2025, driven by Sanofi’s Avaxim and GSK’s Havrix Hepatitis A vaccines.

North America leads at 36.4% in 2025. CDC Travelers’ Health Program and US international travelers underpin North America’s dominance in the global travel vaccines market.

Asia-Pacific at 20.3% (2025) is fastest-growing at ~10.5% CAGR. Rising Chinese and Indian middle-class outbound travel, Japanese Encephalitis vaccination mandates, and expanding government immunization programs across ASEAN drive above-average regional growth.

Key players include Sanofi S.A., GSK plc, Pfizer Inc., Merck & Co. Inc., Bavarian Nordic A/S, Valneva SE, and Takeda Pharmaceutical.

Key drivers include international arrivals, Yellow Fever entry mandates, Saudi Hajj Meningococcal vaccination, and rising adventure tourism to endemic disease destinations.

IXCHIQ is the world’s first FDA-approved Chikungunya vaccine. Developed by Valneva SE, it is a live attenuated single-dose vaccine for adults 18+ traveling to Chikungunya-endemic regions across the Caribbean, Latin America, Africa, and Asia.

Bavarian Nordic acquired Emergent’s travel vaccine portfolio (Vivotif oral typhoid and Vaxchora oral cholera) in May 2023 to build a comprehensive specialty travel vaccine portfolio. The deal included R&D facilities and commercial operations, establishing Bavarian Nordic as the only company with both oral typhoid and oral cholera vaccines.

Key challenges include high out-of-pocket vaccine costs, cold chain logistics failures, only 36-40% of US travelers seeking pre-travel medical consultation (CDC), and regulatory complexity for new combination vaccine approvals.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade