Turkey Real Estate Market Size, Share, Trends and Forecast by Property, Business, Mode, and Region, 2026-2034

Turkey Real Estate Market Size, Share, Trends & Forecast (2026-2034)

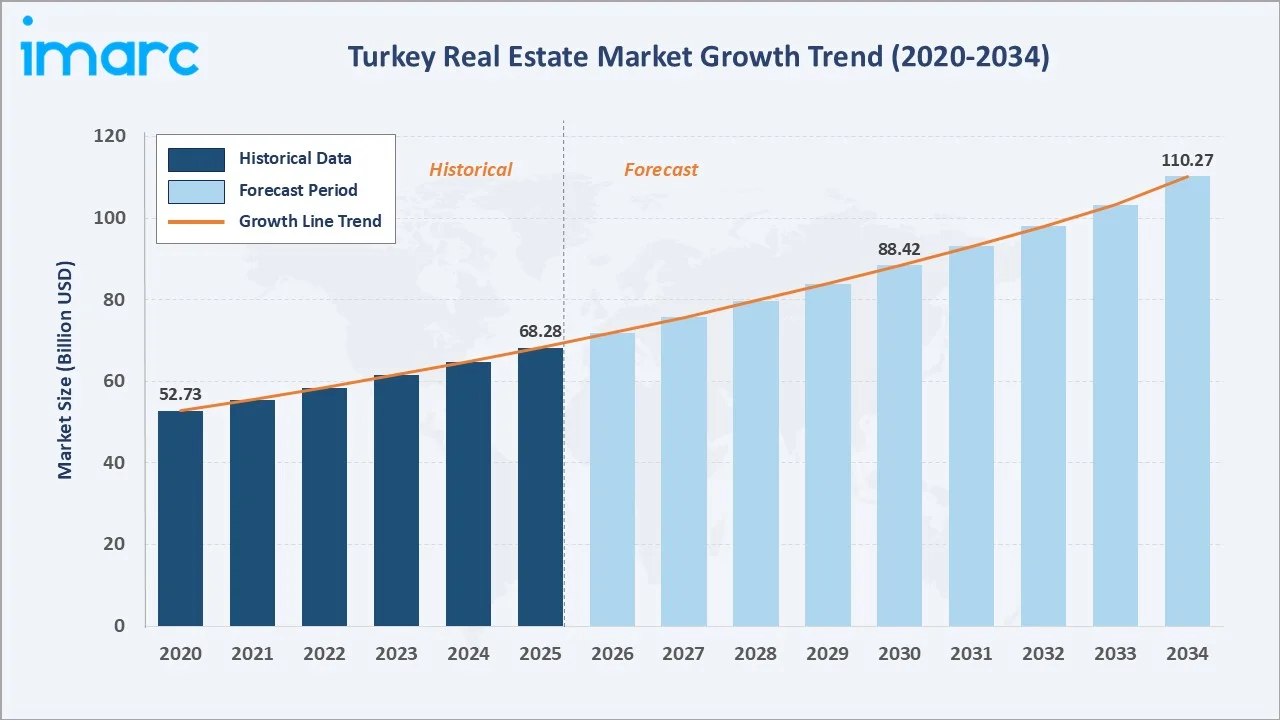

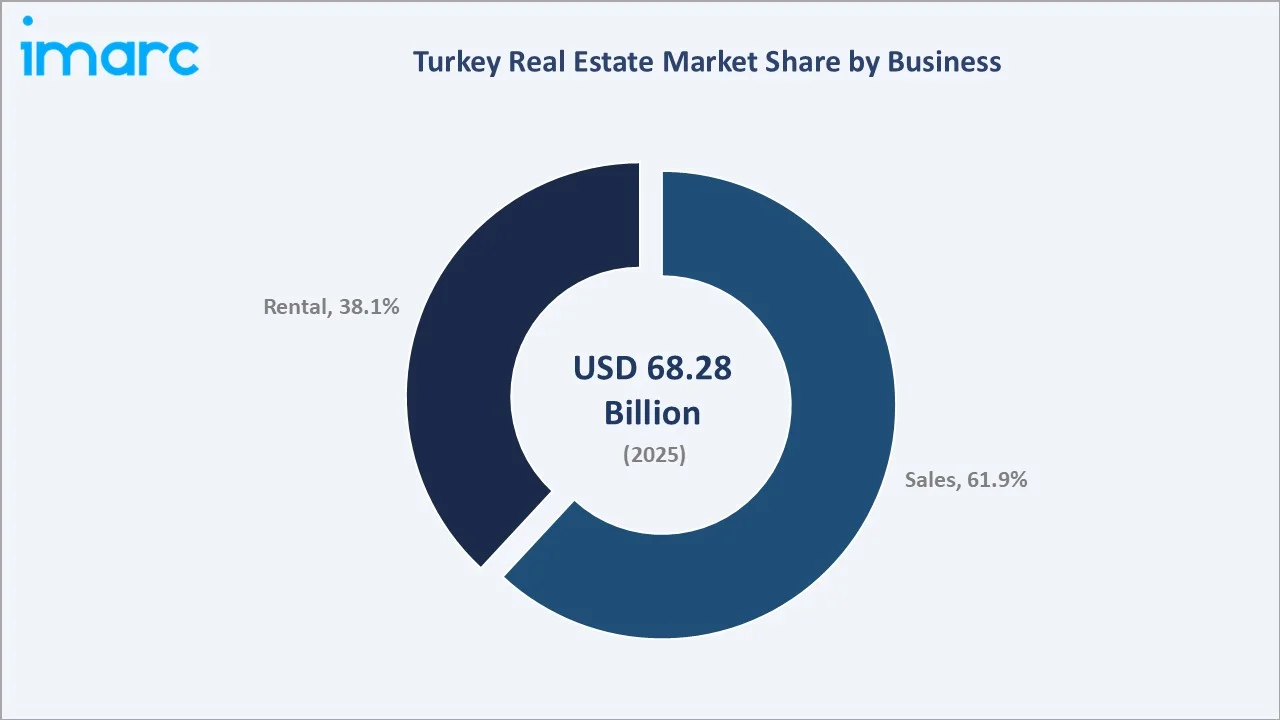

The Turkey real estate market reached USD 68.28 Billion in 2025 and is projected to reach USD 110.27 Billion by 2034, growing at a CAGR of 5.31% during 2026-2034. Market growth is driven by rapid urbanization, strong population growth, favorable government housing programs, robust foreign investor interest fueled by the citizenship-by-investment scheme, and sustained infrastructure development across Turkey's major metropolitan regions.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 68.28 Billion |

|

Forecast Market Size (2034) |

USD 110.27 Billion |

|

CAGR (2026-2034) |

5.31% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

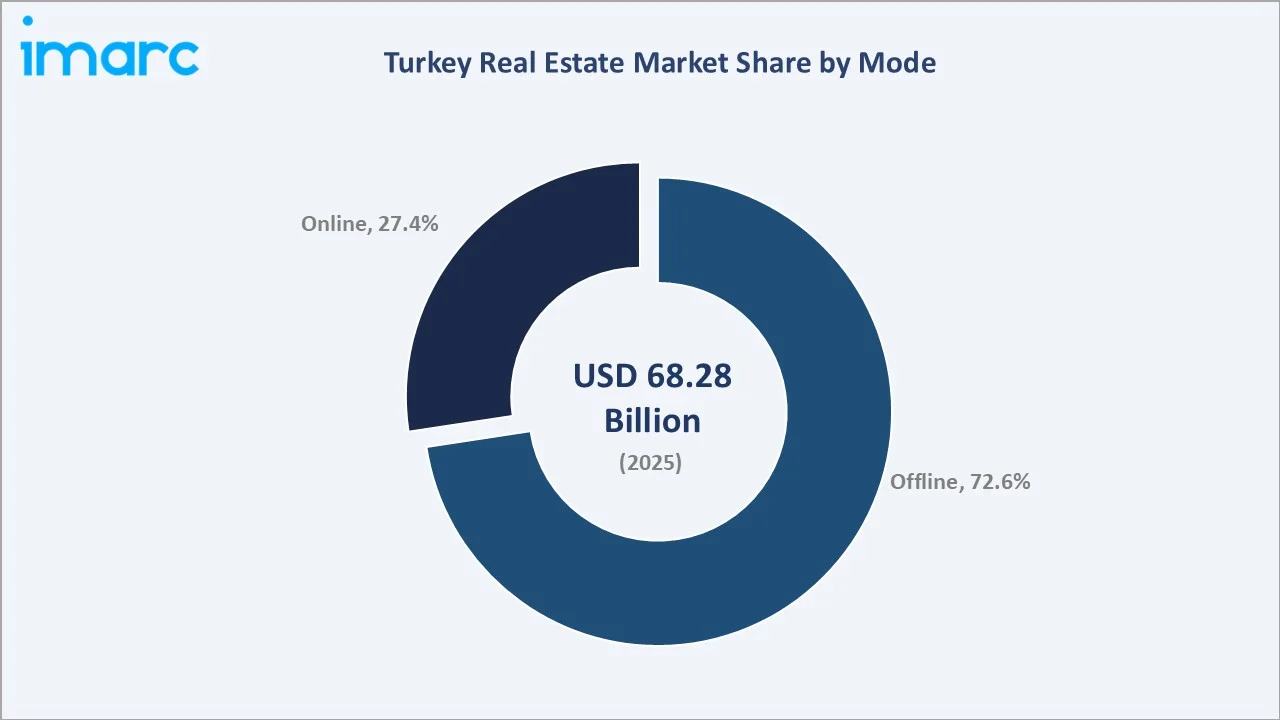

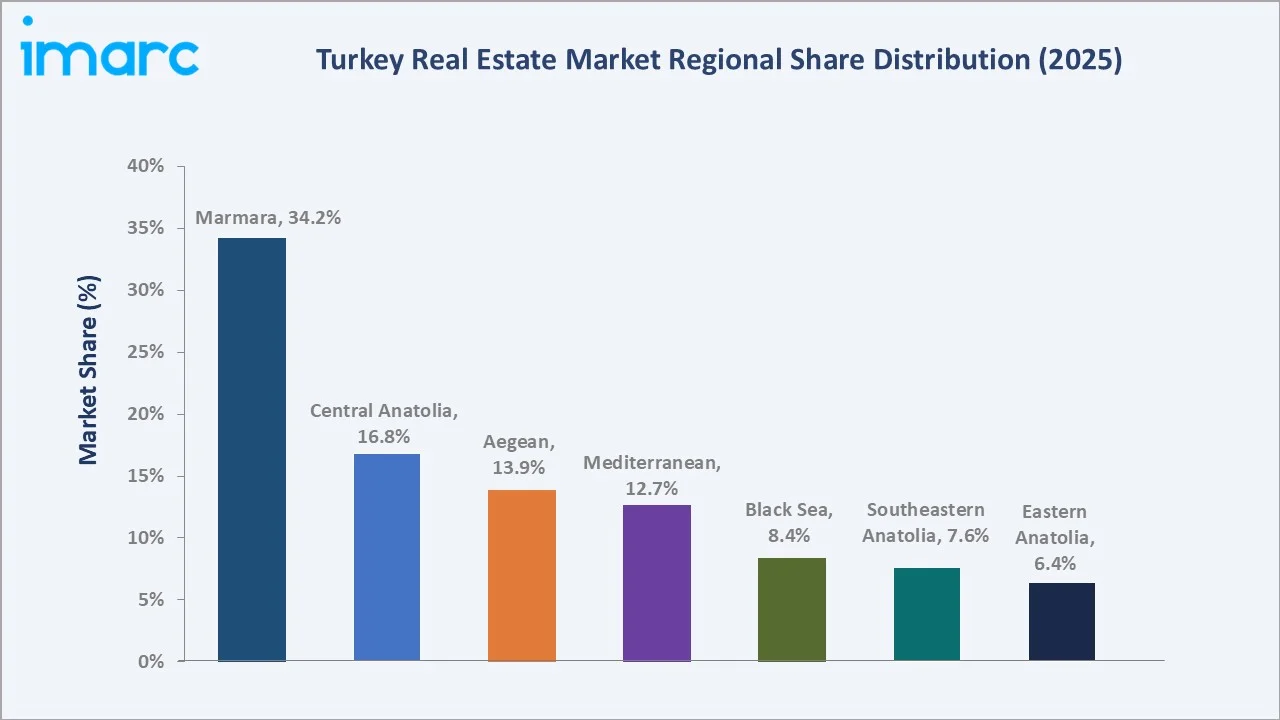

Marmara's 34.2% dominance is anchored by Istanbul, Turkey's economic and demographic capital, which alone accounts for approximately 15-20% of all national real estate transactions. The offline channel's 72.6% share reflects Turkey's traditional preference for in-person property transactions, direct developer show-home visits, and estate agent brokerage relationships.

To get more information on this market, Request Sample

The market's 5.31% CAGR reflects Turkey's fundamental demand drivers: according to TurkStat, Turkey’s total population reached 86.09 million in 2025, with 80,555,475 people residing in provincial and district centers, and ongoing government urban transformation programs that are replacing earthquake-vulnerable housing stock across Istanbul and other major cities with modern, compliant residential units.

Executive Summary

The Turkey real estate market is one of the most dynamic property markets among G20 and emerging market economies, underpinned by structural demand from urbanization, population growth, and significant foreign investor participation. From USD 68.28 Billion in 2025, the market is forecast to reach USD 110.27 Billion by 2034, creating incremental value of USD 41.99 Billion at a 5.31% CAGR.

Offline transactions at 72.6% dominate in 2025, reflecting established agent networks and developer show-home sales models, but online platforms are gaining rapidly as PropTech portals like Sahibinden.com and Hepsiemlak expand their digital transaction capabilities. The sales segment leads at 61.9%, driven by first-time buyer demand, investor acquisitions, and foreign purchases, while rental at 38.1% is growing as housing affordability constraints push more households into the rental market.

Key players, including Emlak Konut GYO, Torunlar GYO, Sinpaş Holding, and Sur Yapı, compete across residential, commercial, and mixed-use segments through government partnership programs, branded lifestyle developments, and strategic land bank acquisitions in high-demand urban corridors.

Key Market Insights

|

Insight |

Data |

|

Largest Mode Segment |

Offline – 72.6% share (2025) |

|

Fastest Growing Mode |

Online – ~8.20% CAGR (2026-2034) |

|

Largest Business Segment |

Sales – 61.9% share (2025) |

|

Fastest Growing Business |

Rental – growing as affordability pressures intensify |

|

Leading Region |

Marmara – 34.2% share (2025) |

|

Top Companies |

Emlak Konut GYO, Torunlar GYO, Sinpaş Holding, and Sur Yapı |

Key Analytical Observations:

- Offline transactions at 72.6% in 2025 remain the dominant mode due to Turkey's strong in-person property purchase culture. For both domestic buyers and foreign investors, visiting show homes, reviewing physical title deed documentation at notary offices, and negotiating directly with developer sales teams remains the norm.

- Online platforms at 27.4% are growing fastest at approximately 8.20% CAGR as Turkey's PropTech ecosystem matures. Sahibinden.com, Turkey's largest classifieds platform, and Hepsiemlak, a major real estate portal, together host over 3 million active property listings as of 2025.

- The sales segment at 61.9% reflects Turkey's traditionally high homeownership aspiration, supported by Emlak Konut's mass-market housing campaigns, TOKİ's affordable housing programs, and the citizenship-by-investment scheme that requires a minimum USD 400,000 property purchase.

- Marmara's 34.2% dominance is structurally anchored by Istanbul's status as Turkey's commercial, financial, and cultural capital. Istanbul accounts for approximately 30% of Turkey's GDP and attracts the highest property valuations, the densest foreign buyer concentration, and the largest share of commercial real estate investment across offices, retail, and logistics assets.

Turkey Real Estate Market Overview

Turkey's real estate market encompasses the development, sale, and rental of residential properties, commercial properties, industrial properties, and land. The market is structurally supported by Turkey's young and growing population, rapid urban migration, earthquake-driven urban renewal requirements, and active government housing delivery programs through the Housing Development Administration (TOKİ) and Emlak Konut GYO.

Turkey's unique market dynamics include the citizenship-by-investment program attracting USD 400,000+ property purchases from Middle Eastern, Russian, and Central Asian buyers; large-scale urban transformation projects replacing non-earthquake-resistant buildings across Istanbul and other cities; and a growing PropTech sector digitizing discovery, valuation, and transaction workflows across the property lifecycle.

Market Dynamics

To evaluate market opportunities, Request Sample

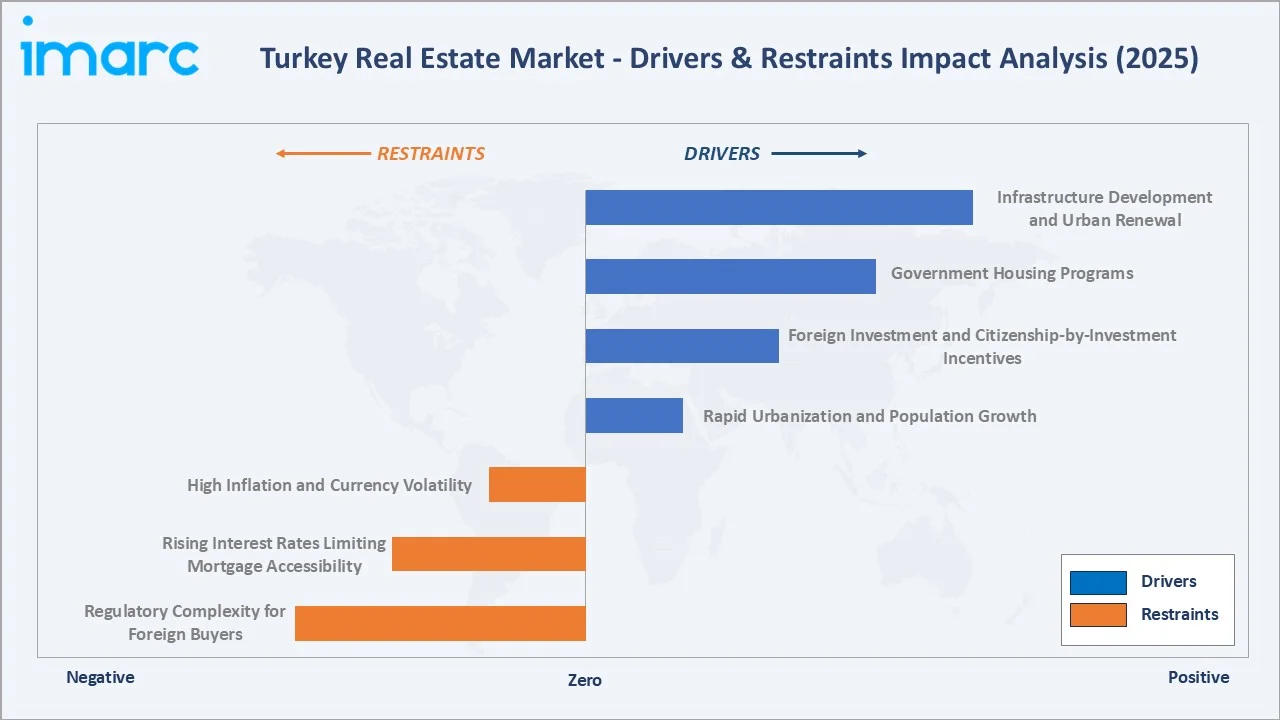

Market Drivers

- Rapid Urbanization and Population Growth: According to TurkStat, Turkey’s population rose by 427,224 in 2025, reaching a total of 86.09 million. In addition, urban population accounted for 77.5% of its total population in 2023, with approximately 500,000+ new urban households formed annually.

- Foreign Investment and Citizenship-by-Investment Incentives: Turkey's citizenship-by-investment program, requiring a minimum real estate purchase of USD 400,000, attracted tens of thousands of applications from Middle Eastern, Russian, Iranian, and Central Asian buyers through 2022–2024.

- Government Housing Programs: The Turkish government's Housing Development Administration (TOKİ) delivers affordable housing with annual construction targets of 500,000 units. In February 2025, Emlak Konut launched a zero-down-payment, decreasing-instalment housing campaign across 25 projects in Istanbul, Izmir, Antalya, and Balıkesir, directly addressing middle-income homeownership demand.

- Infrastructure Development and Urban Renewal: Istanbul's Istanbul Canal project, new metro line extensions across Ankara and Istanbul, the planned new Istanbul airport zone development, and post-earthquake urban renewal requirements across Turkey's seismic zones are generating significant demand for new residential and commercial property in infrastructure-connected corridors.

Market Restraints

- High Inflation and Currency Volatility: Turkey's inflation rate reached 85.5% in October 2022 and remains elevated in 2025, eroding real purchasing power and creating uncertainty for property valuation. The Turkish lira's depreciation against the USD has increased construction input costs for developers, compressing project margins and slowing new supply delivery.

- Rising Interest Rates Limiting Mortgage Accessibility: Turkey's Central Bank raised policy rates significantly from 2023 onwards to combat inflation, with mortgage rates reaching 40–50% annually at peak. This has severely curtailed mortgage-financed home purchases, shifting demand toward developers offering direct instalment programs.

- Regulatory Complexity for Foreign Buyers: While Turkey actively courts foreign real estate investment, the regulatory framework for foreign property purchases, including military zone restrictions, title deed verification requirements, mandatory translation of documents, and valuation reporting obligations, adds transaction complexity and cost that deters international investors.

Market Opportunities

- PropTech and Digital Transaction Platforms: Turkey's PropTech sector is experiencing rapid growth, with online listing platforms, virtual tour providers, digital mortgage brokers, and blockchain-based title deed verification services attracting significant venture capital.

- Commercial Real Estate Demand from Business Expansion: Turkey's position as a regional hub for multinationals and its growing technology and creative economy sectors are generating demand for Grade A office space, modern logistics facilities, and data centers.

Market Challenges

- Property Affordability Gap in Major Cities: Istanbul continued to rank among the most expensive major markets, with property prices reaching TRY 74,101 per square meter, creating a severe affordability gap between market prices and median household incomes.

- Land Scarcity and Zoning Constraints in Istanbul: Developable urban land in Istanbul's preferred districts is extremely scarce, driving developers toward more distant suburban locations and increasing urban transformation project reliance for development pipeline replenishment.

Emerging Market Trends

1. PropTech Platform Growth and Digital Transactions

Turkey's real estate portal ecosystem, led by Sahibinden.com, Hepsiemlak, and Zingat, is transitioning from listing aggregation to full-service transaction platforms. Virtual 3D property tours, AI-powered valuation tools, secure online offer submission, and integrated mortgage pre-approval are reducing the necessity of in-person visits for initial property discovery.

2. Demand for Earthquake-Resilient and Green-Certified Properties

Following the February 2023 Kahramanmaraş earthquakes that caused extensive building damage and casualties, Turkish buyers have dramatically increased their requirements for earthquake-resistant construction certification. Developers offering TBDY 2018-compliant and BREEAM or LEED-certified buildings are commanding premiums of 15–25% over standard-specification equivalents.

3. Foreign Buyer Market Diversification

The foreign buyer segment is diversifying beyond traditional Russian, Iranian, and Iraqi buyers. European retirees seeking Mediterranean coastal properties, UK diaspora returning capital to Aegean and Mediterranean holiday home markets, and Gulf sovereign wealth fund exploration of Istanbul Grade A commercial assets represent emerging buyer cohorts.

4. Mixed-Use Mega-Project Development

Turkey's largest real estate developers, Torunlar GYO, Ağaoğlu Group, and Rönesans Gayrimenkul are increasingly pursuing mega mixed-use developments integrating residential towers, retail malls, hotels, and office components within a single masterplan. These projects create self-contained urban districts that command brand premiums, attract anchor retail tenants, and provide developers with diversified revenue streams across all property types simultaneously.

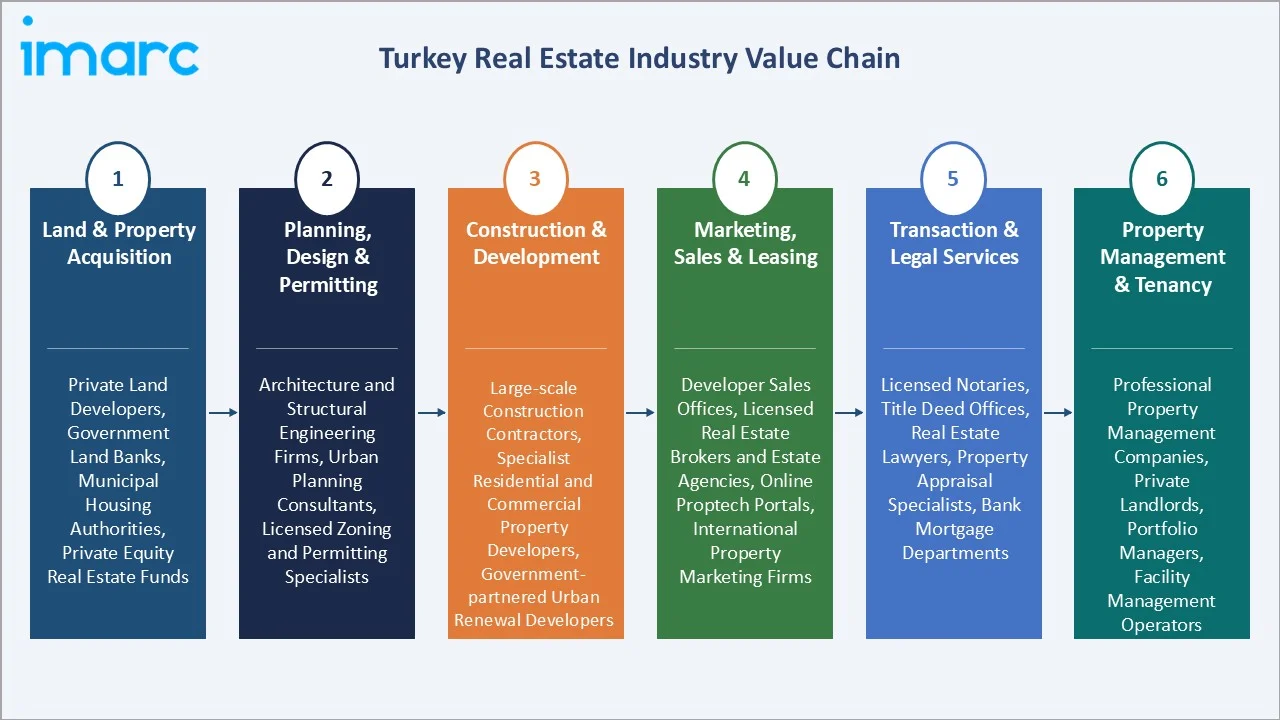

Industry Value Chain Analysis

Turkey's real estate value chain spans land acquisition through long-term property management, with each stage involving specialized regulatory, financial, and construction expertise tailored to Turkey's unique urban development and legal framework.

|

Stage |

Key Players / Examples |

|

Land & Property Acquisition |

Private land developers, government land banks, municipal housing authorities, private equity real estate funds |

|

Planning, Design & Permitting |

Architecture and structural engineering firms, urban planning consultants, licensed zoning and permitting specialists |

|

Construction & Development |

Large-scale construction contractors, specialist residential and commercial property developers, government-partnered urban renewal developers |

|

Marketing, Sales & Leasing |

Developer sales offices, licensed real estate brokers and estate agencies, online PropTech portals, international property marketing firms |

|

Transaction & Legal Services |

Licensed notaries, title deed offices, real estate lawyers, property appraisal specialists, bank mortgage departments |

|

Property Management & Tenancy |

Professional property management companies, private landlords, portfolio managers, facility management operators |

Technology Landscape in the Turkey Real Estate Industry

PropTech Platforms and Digital Listings

Sahibinden.com is Turkey's dominant classifieds platform hosting the largest real estate listing inventory, supplemented by Hepsiemlak and Zingat. These platforms are integrating 3D virtual tour capabilities, AI-driven property valuation, neighborhood analytics, and secure digital communication between buyers, sellers, and agents. Sahibinden.com attracts 58.1 million monthly users, generating 463.4 million visits and 12.7 billion page views, reflecting the central role of online discovery even when final transactions remain offline.

Building Information Modelling (BIM) in Construction

Turkey's Ministry of Environment, Urbanization and Climate Change has mandated BIM adoption for public construction projects above a specified threshold value. Leading developers including Torunlar GYO and Rönesans Gayrimenkul are using BIM-based project management to reduce construction waste, improve cost forecasting accuracy to within ±5%, and streamline regulatory permit submission processes.

Blockchain-Based Title Deed Registration

Turkey's Land Registry and Cadastre General Directorate (TKGM) is conducting a pilot blockchain-based title deed system, designed to reduce title fraud, eliminate manual documentation errors, and enable digital property ownership verification. Full rollout of digital title deeds is targeted for 2027–2028 and will significantly accelerate transaction timelines and reduce reliance on notary intermediaries.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Mode |

Offline |

72.6% |

2025 |

|

Business |

Sales |

61.9% |

2025 |

|

Property |

🔒 |

🔒 |

2025 |

|

Region |

Marmara |

34.2% |

2025 |

By Mode

Offline transactions dominate with a 72.6% market share in 2025. Turkey's real estate transaction culture is deeply rooted in face-to-face engagement; buyers visit developer show homes, meet with agents at physical office locations, review hard-copy title deed documentation, and complete notary-mediated transaction signing in person.

To access detailed market analysis, Request Sample

Online channels at 27.4% are growing fastest at approximately 8.20% CAGR. The COVID-19 period accelerated digital discovery adoption, and the sustained growth of Turkey's internet penetration (now exceeding 85% of the population), smartphone usage, and PropTech portal sophistication are structurally shifting the first-stage discovery and shortlisting process online, even when final transactions remain offline.

By Business

The sales segment leads with a 61.9% market share in 2025. Property ownership is a deeply embedded aspiration in Turkish culture, reinforced by real estate's role as a primary inflation hedge, the citizenship-by-investment program driving foreign purchases, and government campaigns such as Emlak Konut's zero-down-payment programs targeting middle-income first-time buyers.

The rental segment at 38.1% is growing as affordability pressures intensify. Turkey's rapid property price appreciation has pushed homeownership beyond the reach of significant portions of the working-age population, particularly in Istanbul and Ankara.

Regional Market Insights

Marmara leads Turkey's real estate market with a commanding 34.2% share in 2025. The region's dominance is anchored by Istanbul, home to approximately 16 million residents and generating Turkey's highest property values, transaction volumes, and commercial real estate investment activity.

Central Anatolia's 16.8% share reflects Ankara's established commercial property market and the broader region's industrial and logistics real estate expansion. The Aegean region at 13.9% benefits from Izmir's technology and start-up economy and the sustained coastal holiday home market in Bodrum, the Çeşme peninsula, and nearby islands attracting premium domestic and foreign buyers.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Marmara |

34.2% |

Istanbul's dominant economic role, highest property valuations, foreign buyer concentration, new metro corridor development |

|

Central Anatolia |

16.8% |

Government and administrative sector driving commercial real estate demand, industrial expansion, rapidly urbanizing secondary cities |

|

Aegean |

13.9% |

Technology economy and port logistics growth, coastal holiday home demand, strong foreign buyer presence |

|

Mediterranean |

12.7% |

Tourism-driven residential demand, foreign buyer activity, growing urban real estate in Mersin's expanding port economy |

|

Black Sea |

8.4% |

Position as a gateway city attracting Arab buyers, industrial expansion, infrastructure-linked residential development |

|

Southeastern Anatolia |

7.6% |

Post-earthquake urban renewal, major infrastructure investment, industrial zone expansion across the southeastern economic corridor |

|

Eastern Anatolia |

6.4% |

Emerging winter tourism property market, government investment in infrastructure, incremental urban expansion |

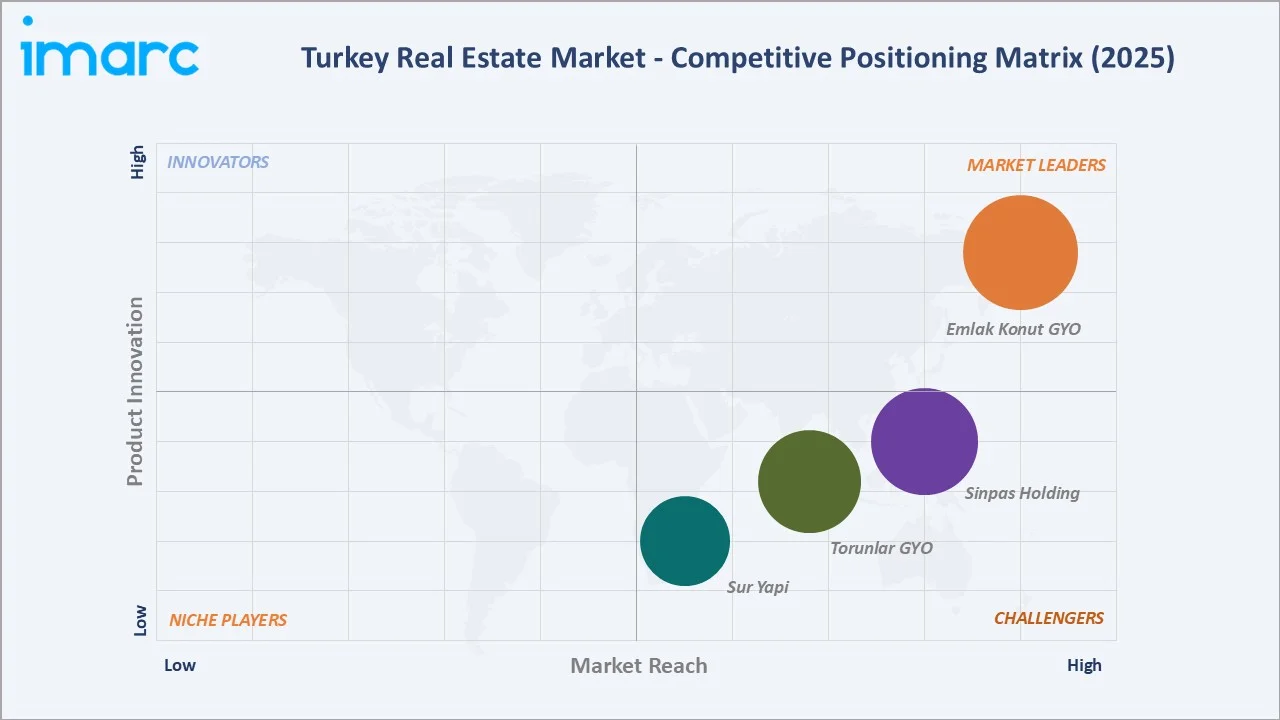

Competitive Landscape

Turkey's real estate market features a dual competitive structure: state-backed developers dominating large-scale social and urban transformation projects, and private-sector REITs and developers competing in premium residential, commercial, and mixed-use segments.

|

Company Name |

Brand/Platform |

Market Position |

Core Strength |

|

Emlak Konut GYO |

Emlak Konut |

Market Leader |

Urban transformation leadership, mass-market housing campaigns |

|

Torunlar GYO |

Torunlar GYO |

Strong Challenger |

Premium shopping mall, office, and hotel portfolios; private-sector mega-project leadership |

|

Sinpaş Holding |

Sinpaş, Paylı Gayrimenkul, Sinpaş Yapı |

Strong Challenger |

Branded lifestyle residential communities, integrated school and healthcare amenity developments, Istanbul focus |

|

Sur Yapı |

Sur Yapı |

Challenger |

Premium residential compounds in Istanbul and coastal markets, high-specification unit focus, foreign buyer appeal |

Emlak Konut GYO dominates the affordable-to-mid-market residential segment, while Torunlar GYO, and Sinpaş Holding. lead in premium and commercial real estate.

Key Company Profiles

Emlak Konut GYO

Emlak Konut GYO is Turkey's largest real estate investment trust and a pivotal force in mass-market and mid-market residential development. It has a vast government land bank; Emlak Konut operates Turkey's most impactful private-public partnership housing delivery model.

- Project Portfolio: Istanbul Canal-adjacent Dursunköy residential parcels (USD 2.8 billion tender opened May 2025), Başakşehir and Kayaşehir mega-residential estates, Etiler premium residential developments, and Bizim Mahalle in Küçükçekmece spanning one million square meters.

- Recent Developments: In August 2025, Emlak Konut REIT raised TRY 21.41 billion (USD 525.8 million) through a real estate certificate IPO for its Damla Kent project, driven by strong investor demand. The offering is intended to finance the construction of 2,214 residential units, with demand for the base offer reaching 1.87 times the available certificates.

- Strategic Focus: Urban transformation project leadership, Istanbul Canal corridor positioning, middle-income housing affordability programs, green-building certification expansion, and digital sales channel development.

Torunlar GYO

Torunlar GYO is Turkey's leading private-sector real estate investment trust, with a portfolio spanning premium retail malls, luxury hotels, Grade A office towers, and mixed-use city districts.

- Project Portfolio: Mall of Istanbul, Torun Center mixed-use tower, and multiple premium residential tower developments across Istanbul's premium business and residential districts.

- Strategic Focus: Premium commercial REIT leadership, mixed-use mega-project development, green building certification, BIST REIT value maximization, and expansion beyond Istanbul into Izmir and Ankara commercial markets.

Market Concentration Analysis

Turkey's real estate market is moderately fragmented at the national level. Emlak Konut GYO together dominates the large-scale affordable-to-mid-market residential segment with an estimated 20–25% of residential construction output. In the commercial sector, Torunlar GYO leads in premium retail and mixed-use, with Torunlar GYO holding the largest single mall portfolio in Turkey by gross lettable area.

Below the top tier, the market is highly fragmented with 1,000+ licensed developers and real estate investment companies operating across Turkey's 81 provinces. The market's fragmentation creates ongoing consolidation opportunities, as scale advantages in land procurement, construction financing, and regulatory relationship management continue to favor larger players over small and medium-sized developers in competitive tender and urban transformation project bidding.

Investment & Growth Opportunities

Fastest Growing Segments

Online real estate platforms (~8.20% CAGR), premium Istanbul waterfront residential, logistics and industrial real estate serving Turkey's growing e-commerce sector, and data center development represent the highest-growth investment vectors through 2034. Together, these sub-segments address a combined incremental addressable market of approximately USD 25 Billion by 2034.

Emerging Market Expansion

Turkey's Aegean and Mediterranean coastal markets represent growing second-home and retirement destination demand from European, Gulf, and UK buyers. Bodrum, Çeşme, Alanya, and Fethiye are emerging as recognized international real estate destinations, with luxury villa developments attracting USD 1–10 Million transactions from international buyers seeking both lifestyle value and Turkish citizenship eligibility.

Venture and Institutional Investment Trends

- International institutional investors including GIC (Singapore), Blackstone, and GLP are exploring Turkish logistics real estate as e-commerce penetration grows from 16% to projected 25%+ of total retail sales by 2030, driving modern warehouse demand in Istanbul, Izmir, and Bursa logistics hubs.

- PropTech venture capital investment in Turkey has grown 40%+ annually since 2021, with Sahibinden.com, Hepsiemlak, and emerging players attracting both domestic and international VC for AI valuation, digital mortgage, and virtual tour platform development.

Future Market Outlook (2026-2034)

Turkey's real estate market is positioned for consistent, long-term growth through 2034. From USD 68.28 Billion in 2025, the market will reach USD 110.27 Billion by 2034, representing total incremental value creation of USD 41.99 Billion at a 5.31% CAGR. Growth will be anchored by Turkey's structural housing demand from continued urbanization, the large-scale earthquake urban renewal program, and sustained foreign buyer interest in both investment and lifestyle properties.

The online transaction share will grow from 27.4% in 2025 to an estimated 40–45% by 2034 as PropTech platforms mature and digital title deed systems enable end-to-end digital transactions. The rental market will gain share relative to sales as affordability constraints continue to delay homeownership among younger urban households, creating a growing professionally managed rental sector modelled on European Build-to-Rent formats.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 90 industry participants in 2024–2025, including Turkish real estate developers, GYO executives, estate agents, PropTech entrepreneurs, mortgage bankers, and international real estate investors active in Turkey. Expert input validated market sizing, regional dynamics, and technology adoption trends.

Secondary Research

Secondary research encompassed GYO and developer annual reports, Turkish Statistical Institute (TÜİK) property transaction data, Land Registry General Directorate (TKGM) statistics, Central Bank of Turkey interest rate data, and trade publications including GYODER sector reports and CBRE Turkey market surveys.

Forecasting Models

Market size estimations used top-down and bottom-up forecasting incorporating TÜİK residential and commercial transaction volumes, average transaction values by property type and region, rental yield data, and infrastructure investment pipeline values. A base-case CAGR of 5.31% reflects consensus validated against GYO development pipeline disclosures and government housing program targets.

Turkey Real Estate Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Properties Covered | Residential, Commercial, Industrial, Land |

| Businesses Covered | Sales, Rental |

| Modes Covered | Online, Offline |

| Regions Covered | Marmara, Central Anatolia, Mediterranean, Aegean, Southeastern Anatolia, Blacksea, Eastern Anatolia |

| Companies Covered | Emlak Konut GYO, Torunlar GYO, Sinpaş Holding, Sur Yapı, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the turkey real estate market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the turkey real estate market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the turkey real estate industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Turkey Real Estate Market Report

The market reached USD 68.28 Billion in 2025 and is projected to grow to USD 110.27 Billion by 2034 at a 5.31% CAGR.

Marmara leads with a 34.2% share in 2025, anchored by Istanbul's dominant economic role and highest property valuations.

Offline transactions dominate at 72.6% in 2025, reflecting Turkey's face-to-face property purchase culture and developer show-home sales model.

The sales segment leads at 61.9% in 2025, driven by homeownership aspiration, citizenship-by-investment demand, and government housing campaigns.

Emlak Konut GYO, Torunlar GYO, Sinpaş Holding, and Sur Yapı, are some of the leading players.

Online real estate platforms are growing fastest at approximately 8.20% CAGR, driven by PropTech portal adoption and digital transaction capability expansion.

Urbanisation, population growth, foreign investment incentives, government housing programs, and large-scale earthquake urban renewal are primary drivers.

High inflation, currency volatility, rising interest rates limiting mortgage accessibility, and property affordability gaps in major cities are key challenges.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)