UAE Ice Cream Market Size, Share, Trends and Forecast by Flavor, Category, Product, Distribution Channel, and Region, 2026-2034

UAE Ice Cream Market Size, Share, Trends & Forecast (2026-2034)

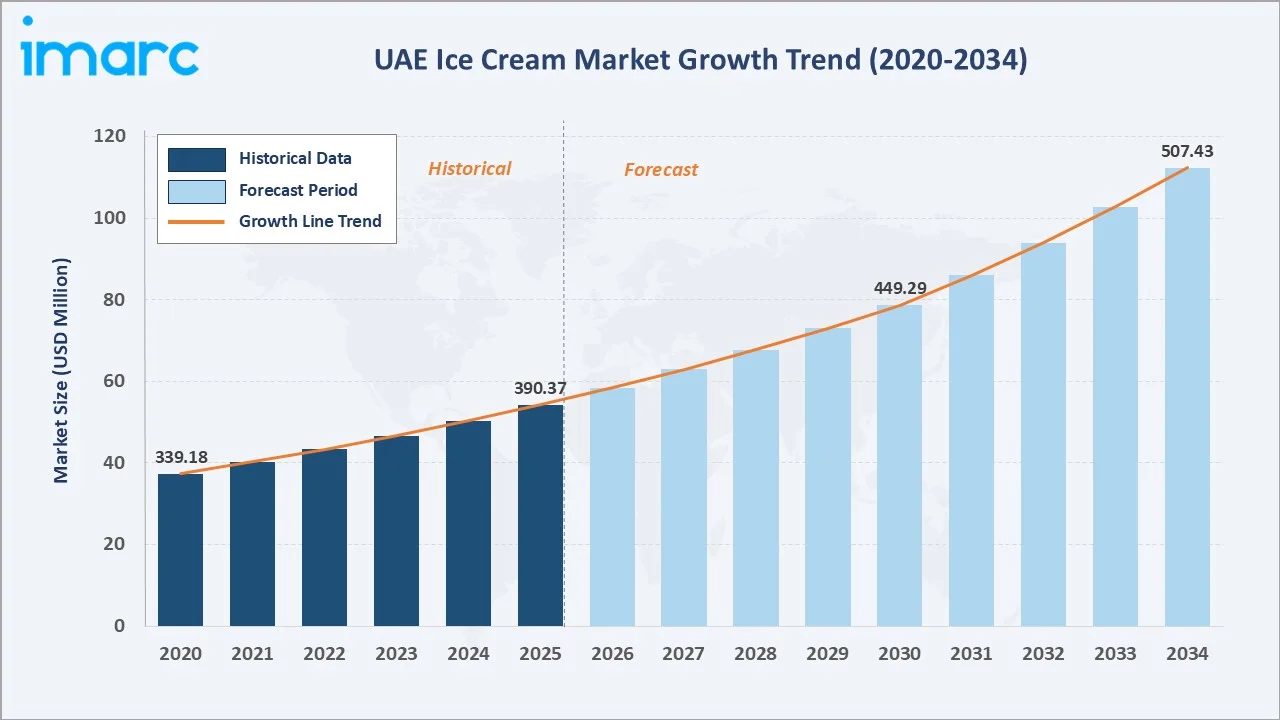

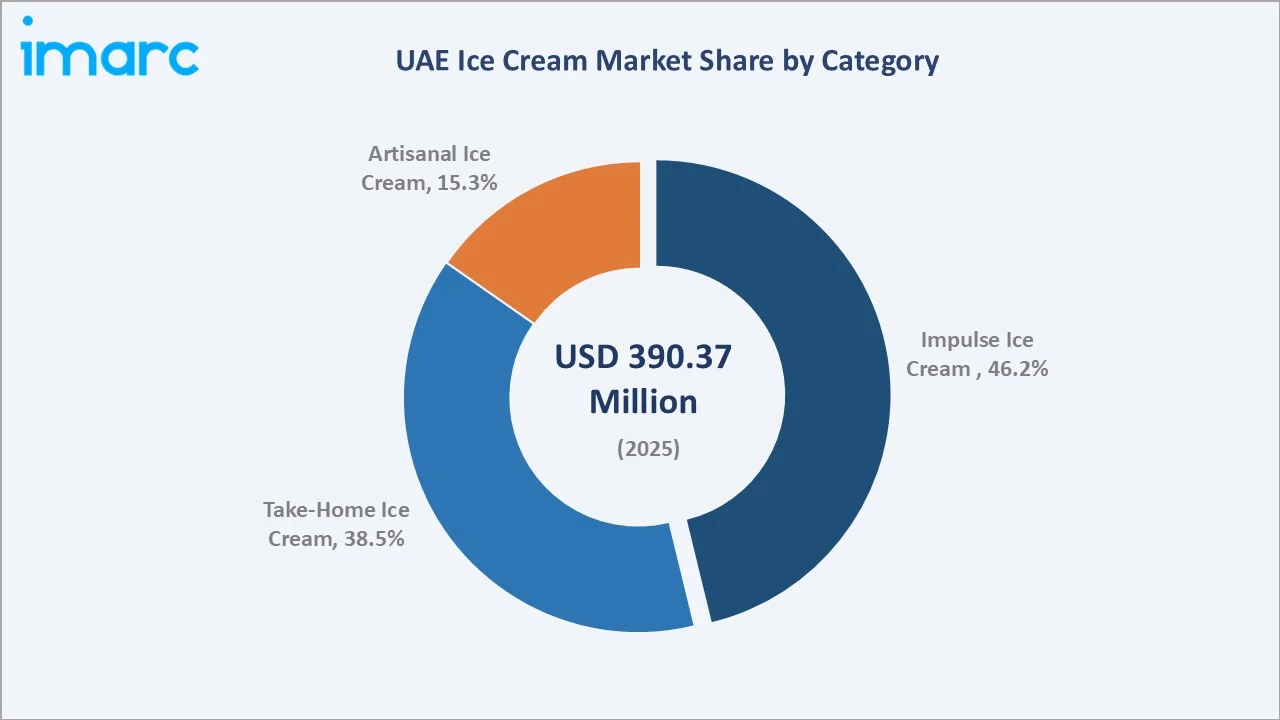

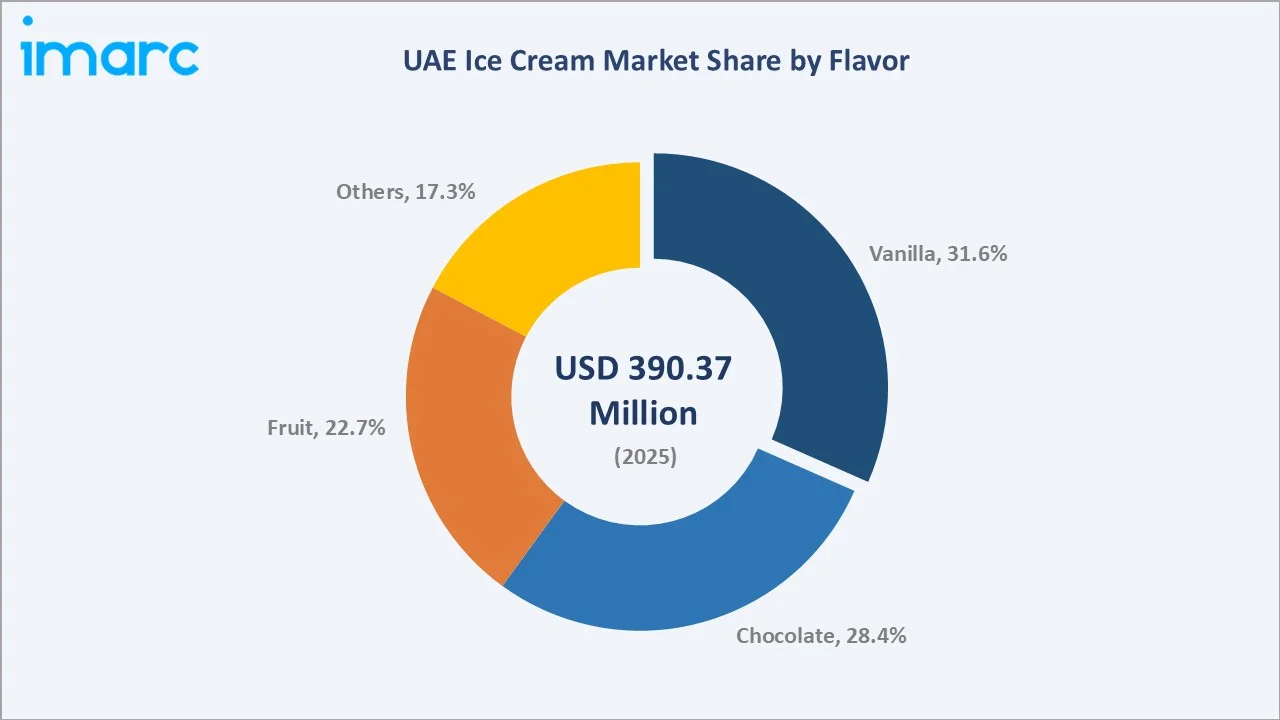

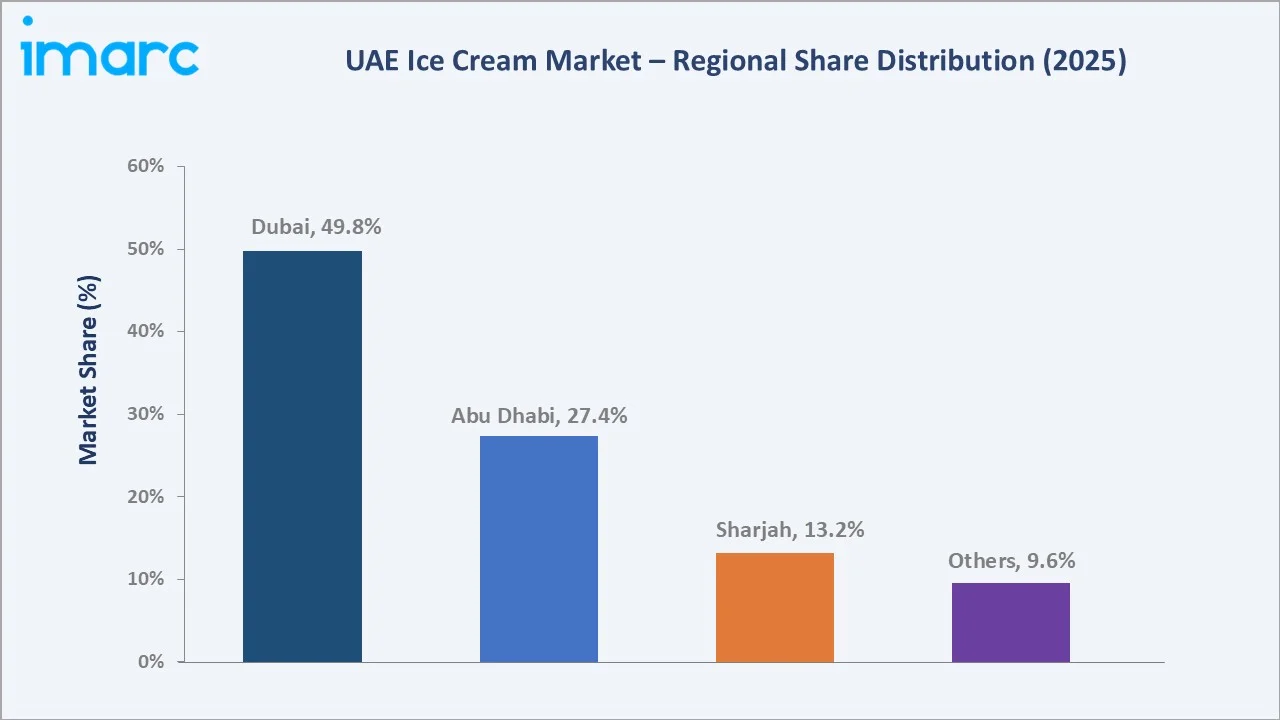

The UAE ice cream market size reached USD 390.37 Million in 2025 and is projected to reach USD 507.43 Million by 2034, exhibiting a CAGR of 2.85% during 2026-2034. Rising disposable incomes, a young multicultural population, premiumization, and robust tourism-led HoReCa demand are the primary forces driving market growth.

Impulse ice cream dominates the category mix at 46.2% in 2025, while vanilla leads the flavor segment at 31.6%. Dubai commands a dominant 49.8% regional share in 2025, reflecting its tourism density and premium retail footprint.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 390.37 Million |

|

Forecast Market Size (2034) |

USD 507.43 Million |

|

CAGR (2026-2034) |

2.85% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Dubai (49.8% share, 2025) |

|

Second Largest Region |

Abu Dhabi (27.4% share, 2025) |

|

Leading Category |

Impulse Ice Cream (46.2%, 2025) |

|

Leading Flavor |

Vanilla (31.6%, 2025) |

The UAE ice cream market growth trajectory from 2020 through 2034, expanding to USD 390.37 Million in 2025, reflects consistent consumption-led demand, while the forecast to USD 507.43 Million captures accelerating premiumization, tourism recovery, and digital distribution-led expansion across emirates.

To get more information on this market, Request Sample

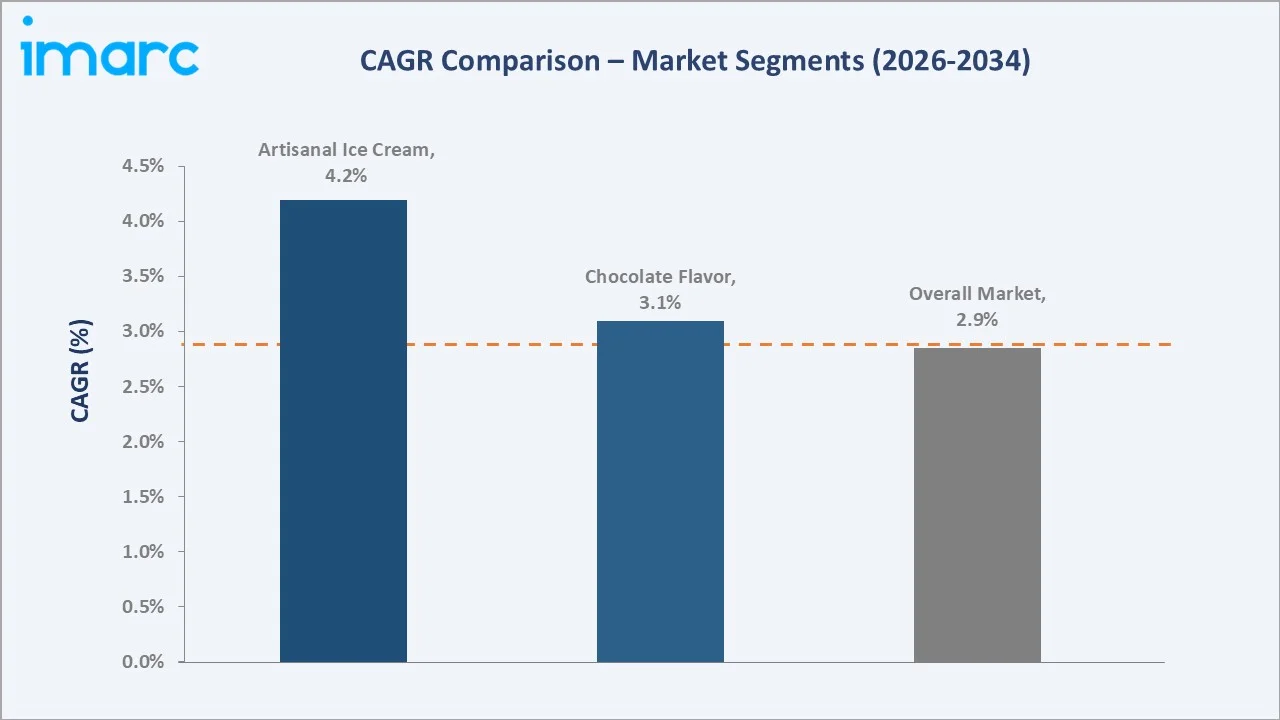

The CAGR trajectories across key category, flavor, and regional sub-segments, with premium health-oriented products at ~4.8% and online stores at ~4.6% CAGR, are the fastest-growing sub-segments within the UAE ice cream industry analysis through 2034.

Executive Summary

The UAE ice cream market is on a steady growth trajectory from USD 390.37 Million in 2025 to USD 507.43 Million by 2034. Ice cream, a widely consumed indulgence across retail and foodservice, benefits from a young demographic, high disposable incomes, tourism density, and year-round hot-weather consumption, reinforcing non-seasonal demand.

Impulse ice cream dominates the category mix at 46.2% in 2025, reflecting convenience-store, forecourt, and vending-led sales. Take-home ice cream (38.5%) benefits from large expatriate households and hypermarket penetration. Artisanal ice cream at 15.3% is the fastest-growing category at ~4.2% CAGR, driven by Dubai's premium dessert cafés, gelato parlors, and culturally inspired flavor innovation across the emirate.

Dubai commands a 49.8% share in 2025, reflecting its tourism scale, premium retail density, and expanding quick-commerce network. Abu Dhabi (27.4%) and Sharjah (13.2%) follow, driven by family-household consumption and supermarket expansion.

Vanilla leads the flavor segment at 31.6%, with chocolate at 28.4% and fruit at 22.7%, reflecting both mainstream preference and regional dessert heritage.

Key Market Insights

|

Insight |

Data |

|

Largest Category |

Impulse Ice Cream - 46.2% share (2025) |

|

Leading Flavor |

Vanilla - 31.6% share (2025) |

|

Leading Region |

Dubai - 49.8% revenue share (2025) |

|

Second Largest Region |

Abu Dhabi - 27.4% revenue share (2025) |

|

Top Companies |

DesertChill, Nestlé, General Mills Inc., Ferrero, IFFCO, The Brooklyn Creamery |

Key Analytical Observations Expanding on the Above Data:

- Impulse ice cream, with 46.2% in 2025, leads because the UAE's convenience retail density - ADNOC, ENOC forecourts, and urban quick-stop outlets - plus high year-round temperatures drive single-serve consumption across residents and tourists.

- Vanilla, at 31.6% in 2025, remains the reference flavor because it anchors scoop-shop, cone, tub, and HoReCa dessert menus. Its pairing versatility with regional ingredients like date, saffron, and pistachio underpins its sustained leadership.

- Dubai's 49.8% share in 2025 reflects concentrated tourism spend (nearly 18.72 million overnight visitors in 2024), dense hotel and F&B infrastructure, premium mall-based parlors, and advanced quick-commerce penetration through Noon Minutes, Talabat, and Careem.

- Abu Dhabi, at 27.4% in 2025, benefits from large family households, strong hypermarket penetration led by Lulu and Carrefour, and rising leisure tourism around Yas Island and Saadiyat, generating premium HoReCa ice cream demand.

UAE Ice Cream Market Overview

Ice cream in the UAE encompasses frozen dairy and non-dairy desserts sold as impulse single-serve formats, take-home packs, and artisanal scoop formats. Product configurations span sticks, cups, cones, bricks, tubs, and novelty bars, delivered across supermarkets, convenience stores, parlors, online stores, and HoReCa channels.

The UAE ecosystem integrates dairy and raw material suppliers (Al Rawabi, Almarai, Arla), global and regional manufacturers, specialized cold-chain logistics operators, modern and general trade distributors, and a diverse end-use base spanning residential households, hotels, cafés, restaurants, cloud kitchens, and tourist-facing foodservice operators across the seven emirates.

Market Dynamics

To evaluate market opportunities, Request Sample

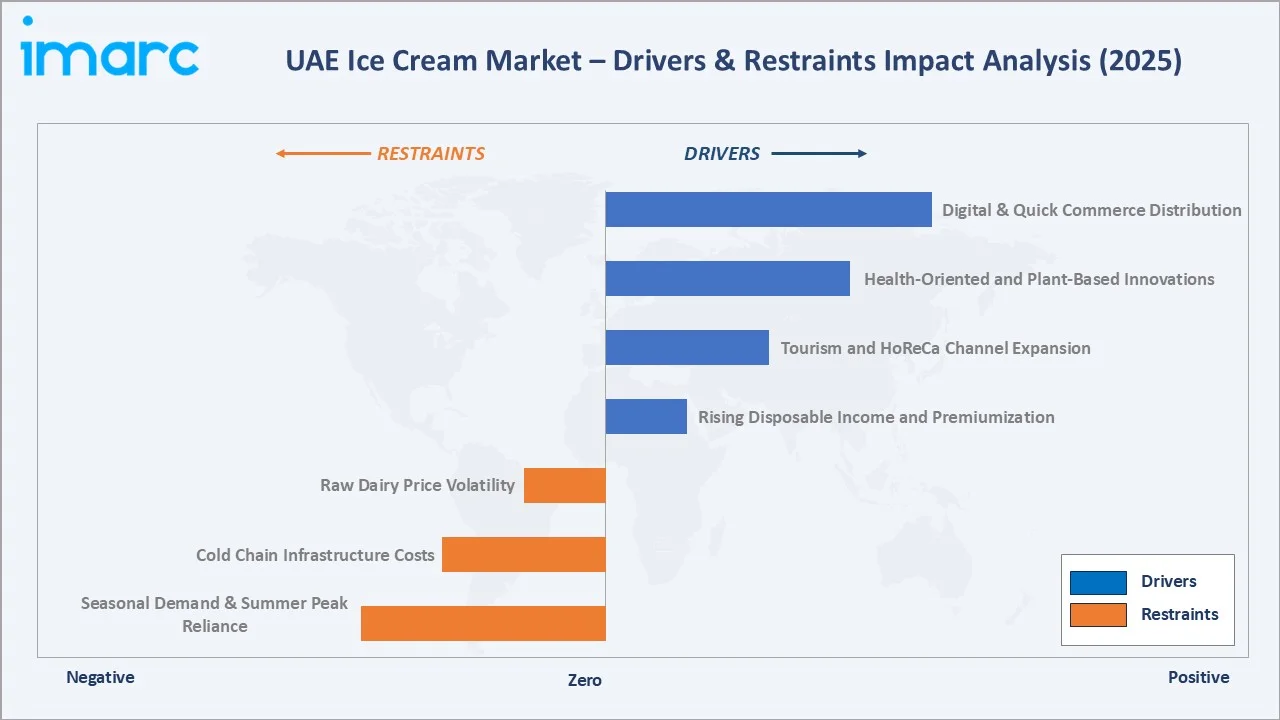

Market Drivers

- Rising Disposable Income and Premiumization: The UAE's high per-capita income and a growing preference for premium indulgence are driving demand for artisanal, gourmet, and culturally inspired ice cream across Dubai and Abu Dhabi. The UAE has the second-highest per capita income (US$50,600) in the MENAP region and is expected to rise to about US$60,000 by 2028.

- Tourism and HoReCa Channel Expansion: The UAE welcomed nearly 18.72 million overnight tourists in 2024, expanding demand across hotels, beach clubs, dessert cafés, and parlors, with strong uplift during peak winter and summer travel seasons.

- Health-Oriented and Plant-Based Innovation: Launches such as The Brooklyn Creamery's keto-friendly Caramel Pecan Crunch in September 2024 reflect rising demand for low-sugar, low-calorie, and dairy-free formulations targeting health-conscious UAE consumers.

Market Restraints

- Raw Dairy Price Volatility: Global dairy commodity swings - skim milk powder, butter fat, and cream - directly pressure UAE ice cream manufacturers' margins, particularly given near-total import dependence for dairy and cocoa inputs.

- Cold-Chain Infrastructure and Energy Costs: Maintaining -18°C to -25°C cold-chain integrity across extreme summer temperatures (often exceeding 45°C) drives significant energy, logistics, and in-store freezer capex, raising the delivered cost base.

Market Opportunities

- Digital and Quick-Commerce Distribution: Rapid growth of Noon Minutes, Talabat, Careem, Instashop, and Kibsons in 15–30-minute grocery delivery is opening incremental ice cream demand occasions, particularly for impulse tubs and premium pints.

- Cultural Fusion Flavors: Growing specification of regional flavors - kunafa, pistachio, saffron, date, cardamom - as seen in Barakat's Kunafa Pistachio bites (November 2024), is creating a differentiated premium segment tailored to local heritage and tourist curiosity.

Market Challenges

- Seasonal Demand and Summer-Peak Reliance: Although consumption is year-round, demand peaks sharply during May-September, creating inventory, distribution, and trade-marketing pressure during transition months and post-Ramadan retail cycles.

- Regulatory and Labeling Complexity: UAE FDA, ESMA, and Dubai Municipality requirements across labeling, Halal certification, sugar disclosure, and ingredient provenance add compliance complexity, especially for plant-based and functional ingredient ice creams.

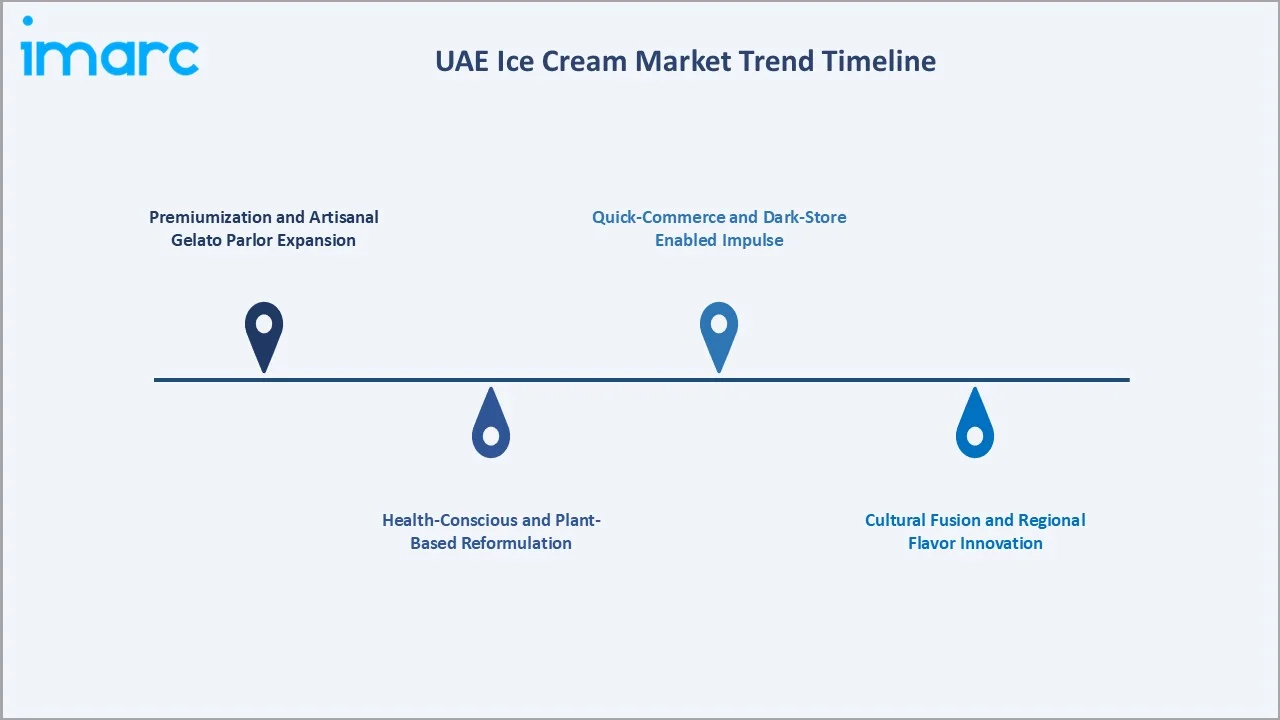

Emerging Market Trends

1. Premiumization and Artisanal Gelato Parlor Expansion

Dubai and Abu Dhabi are seeing rapid expansion of premium gelato and artisanal ice cream parlors, anchored by mall locations and beachfront destinations. Small-batch production, natural ingredients, and signature flavors are driving higher basket values and repeat visit frequency among affluent residents and tourists.

2. Health-Conscious and Plant-Based Reformulation

Manufacturers are reformulating around stevia, lower fat, and non-dairy bases (almond, coconut, oat). The Brooklyn Creamery's keto and low-calorie launches typify the shift, enabling brands to position ice cream as a guilt-free indulgence for fitness-oriented and diabetic-aware UAE consumers.

3. Quick-Commerce and Dark-Store Enabled Impulse

Quick-commerce platforms - Noon Minutes, Talabat, Instashop, Careem - are unlocking new impulse occasions, particularly for single-serve tubs and premium pints delivered in under 30 minutes. Brand portfolios are being re-engineered around pack sizes and price points optimized for dark-store assortments.

4. Cultural Fusion and Regional Flavor Innovation

Flavor innovation blending Emirati and Levantine heritage - kunafa, pistachio, saffron, cardamom, rose - with global formats is gaining share. Barakat's Kunafa Pistachio bites and Ferrero's Kinder-Bueno and Raffaello launches reflect a broader push to own both heritage and globally recognized premium identifiers.

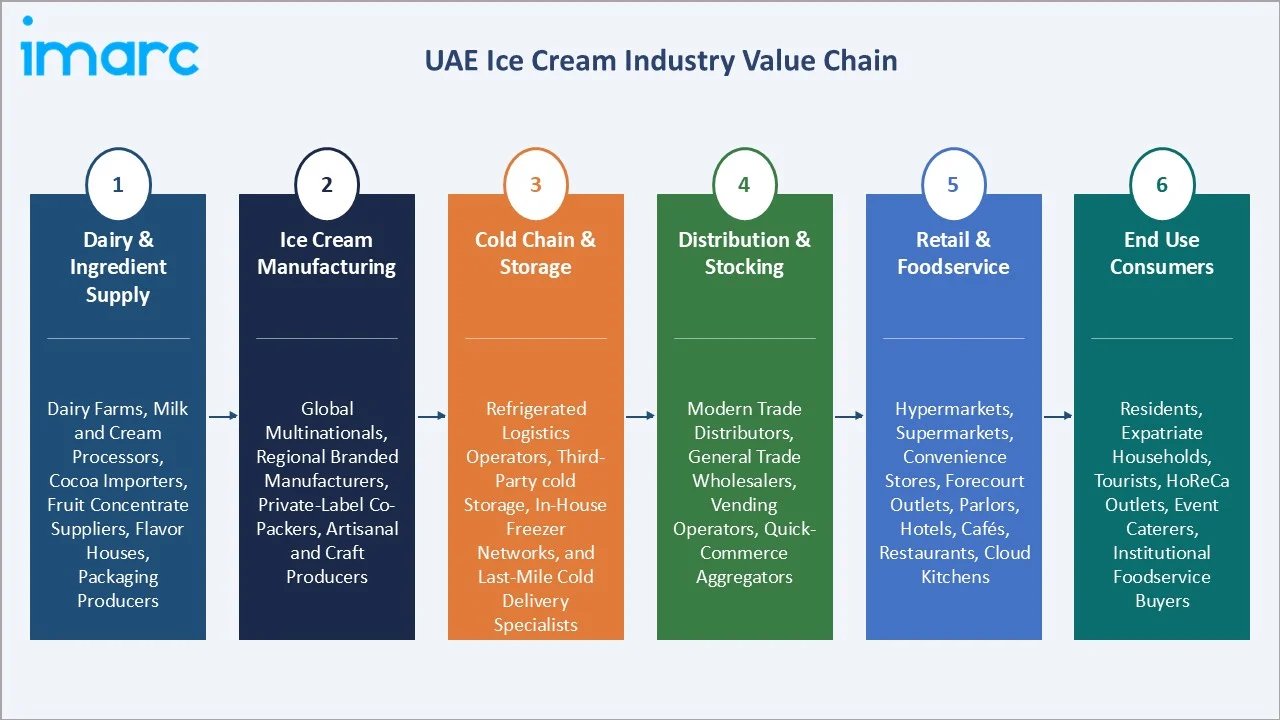

Industry Value Chain Analysis

The UAE ice cream value chain spans six stages from dairy and raw material supply through end-use consumption. Manufacturing and cold-chain logistics capture the highest margin pools, while distribution and retail activation drive working-capital intensity and trade-spend pressure, particularly across modern trade and HoReCa.

|

Stage |

Key Players / Examples |

|

Dairy & Ingredient Supply |

Dairy farms, milk and cream processors, cocoa importers, fruit concentrate suppliers, flavor houses, packaging producers |

|

Ice Cream Manufacturing |

Global multinationals, regional branded manufacturers, private-label co-packers, artisanal and craft producers |

|

Cold Chain & Storage |

Refrigerated logistics operators, third-party cold storage, in-house freezer networks, and last-mile cold delivery specialists |

|

Distribution & Stocking |

Modern trade distributors, general trade wholesalers, vending operators, quick-commerce aggregators |

|

Retail & Foodservice |

Hypermarkets, supermarkets, convenience stores, forecourt outlets, parlors, hotels, cafés, restaurants, cloud kitchens |

|

End Use Consumers |

Residents, expatriate households, tourists, HoReCa outlets, event caterers, institutional foodservice buyers |

Integrated participants with captive or contracted dairy sourcing achieve a cost advantage versus importers dependent on global commodity cycles. For global multinational brands, UAE leadership hinges on brand equity, cold-chain execution, trade-marketing investment, and advantaged placement across hypermarkets, forecourts, parlors, and HoReCa accounts.

Technology Landscape in the UAE Ice Cream Industry

Freezing and Formulation Technology

Continuous freezers with low-draw-temperature capability, inline flavor dosing, and high-shear mixers are enabling finer ice-crystal structures and richer textures. Cryogenic nitrogen dosing in artisanal parlors supports instant freezing, preserving flavor integrity and enabling on-demand premium experiences for walk-in customers.

Clean-Label and Alternative Ingredient Innovation

Stevia, monk fruit, erythritol, and allulose are replacing sucrose in reduced-sugar lines, while oat, almond, and coconut bases serve plant-based launches. Functional add-ins - probiotics, protein isolates, added fiber - are positioning select SKUs as wellness-oriented indulgences across UAE pharmacy and specialty retail channels.

Cold-Chain and Digital Retail Technology

IoT-enabled freezer monitoring, GPS-tracked refrigerated fleets, and temperature-integrity compliance platforms are reducing spoilage across UAE's long hot-season supply routes. Quick-commerce APIs and retail-media platforms are enabling brands to activate precise demand-moment targeting across dark-store catchments.

Sustainable Packaging and Circular Material Innovation

Recyclable paper-based cups and cones, plant-based bioplastic lids, and reduced-gauge flexible films are being adopted to meet UAE's sustainability mandates and consumer ESG expectations. Low-carbon refrigerant systems and energy-efficient freezer cabinets are further reducing operational emissions across manufacturing and retail cold-chain networks.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Flavor | Vanilla | 31.6% | 2025 |

| Category | Impulse Ice Cream | 46.2% | 2025 |

| Product | 🔒 | 🔒 | 2025 |

| Distribution Channel | 🔒 | 🔒 | 2025 |

| Region | Dubai | 49.8% | 2025 |

By Category

Impulse ice cream commands a 46.2% majority share in 2025, driven by UAE's dense forecourt and convenience retail footprint, year-round hot weather, and high on-the-go consumption by residents and tourists. Sticks, cones, and cups dominate the format mix for this category across ADNOC, ENOC, and urban corner-store locations.

To access detailed market analysis, Request Sample

Take-home ice cream at 38.5% in 2025 reflects the UAE's large expatriate household base and strong weekly hypermarket shopping patterns at Carrefour, Lulu, and Spinneys. Artisanal ice cream, with 15.3% in 2025, is the fastest-growing category at ~4.2% CAGR, benefitting from Dubai's premium dessert café culture and tourist willingness to pay for craft experiences.

By Flavor

Vanilla dominates the flavor segment at 31.6% in 2025, anchored by its universal pairing versatility across cones, sundaes, cakes, and HoReCa dessert menus. Its role as a base for premium flavor innovation - bourbon vanilla, Madagascar vanilla, vanilla bean - sustains its relevance across both mass and premium price tiers.

Chocolate at 28.4% in 2025 is the second-largest flavor, led by premium launches from Ferrero (Kinder Bueno, Ferrero Rocher). Fruit at 22.7% benefits from tropical and mango variants, while Others (17.3%) captures heritage flavors - pistachio, saffron, rose, kunafa - that increasingly anchor premium and cultural-fusion innovation.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Dubai |

49.8% |

Tourism density; premium parlors; hypermarket and quick-commerce leadership |

|

Abu Dhabi |

27.4% |

Family-household consumption; Lulu/Carrefour scale; Yas/Saadiyat leisure tourism |

|

Sharjah |

13.2% |

Value-conscious take-home demand; dense residential clusters; forecourt impulse |

|

Others |

9.6% |

Ajman, RAK, Fujairah, UAQ; rising tourism and organized retail penetration |

Dubai's 49.8% dominance in 2025 is driven by a unique combination of tourism scale, premium retail density, and advanced quick-commerce penetration. Dubai attracted nearly 18.72 million overnight tourists in 2024, anchoring demand across hotels, beach clubs, mall parlors, and nightlife-adjacent dessert destinations year-round.

Abu Dhabi, with 27.4% in 2025, benefits from a large family-household base, strong hypermarket penetration, and a steadily expanding leisure and MICE tourism flow around Yas Island, Saadiyat, and the Corniche. Sharjah and the Northern Emirates together add roughly 22.8%, driven by value-led take-home demand.

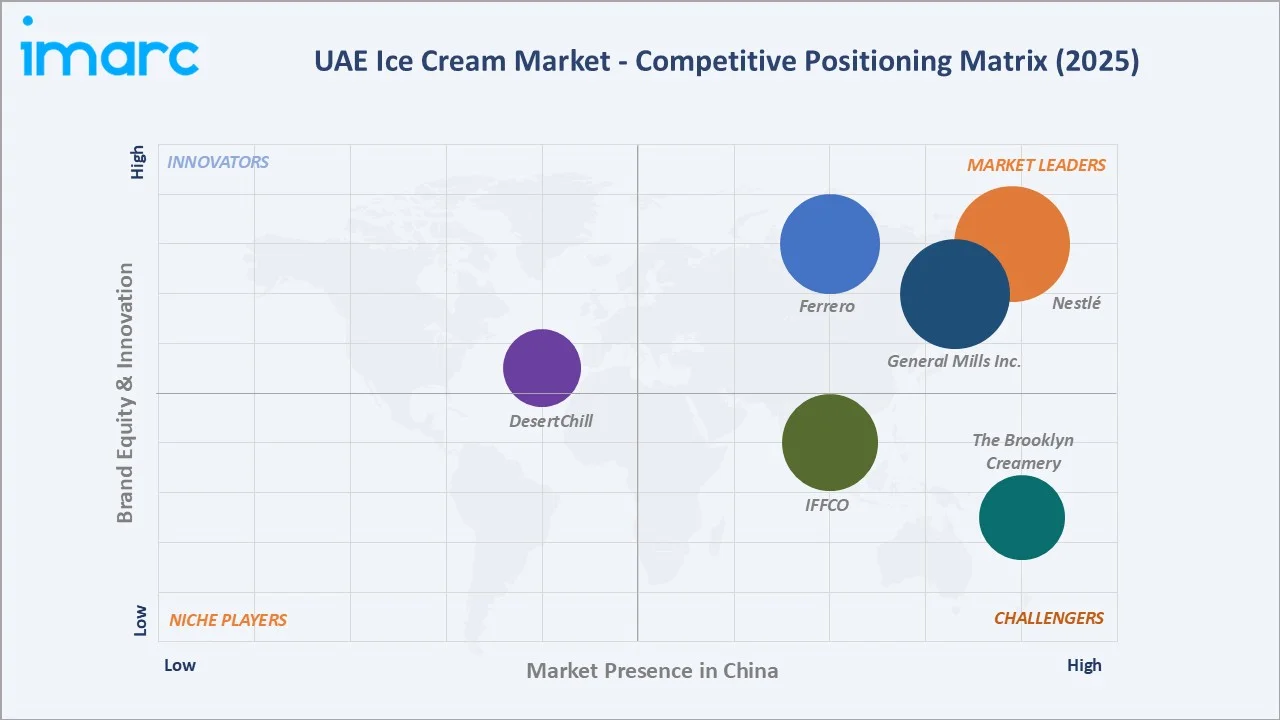

Competitive Landscape

The UAE ice cream market is moderately fragmented, with global multinationals holding leading positions in branded impulse and take-home, while regional specialists and homegrown artisanal players are scaling in premium and cultural-fusion niches. Modern trade drives most branded volume; parlors and HoReCa anchor premium value share.

|

Company Name |

Key Products |

Market Position |

UAE Strategic Focus |

|

Nestlé |

Mövenpick branded tubs, Sticks |

Leader |

Premium take-home leadership via Mövenpick; HoReCa and hotel channel strength |

|

General Mills Inc. |

Häagen-Dazs pints, bars, stick formats |

Leader |

Super-premium tubs; mall-based parlor footprint; luxury gifting |

|

Ferrero |

Kinder Bueno, Ferrero Rocher, Raffaello ice creams |

Leader |

Premium launch in 2024; leveraging chocolate brand equity into frozen desserts |

|

IFFCO |

London Dairy premium tubs and bars, Igloo |

Challenger |

Locally manufactured premium brand; strong modern trade presence |

|

The Brooklyn Creamery |

Keto, low-calorie, no-added-sugar ice creams |

Challenger |

Health-positioned; digital-first launches via Noon Minutes |

|

DesertChill |

Hand-crafted gelato sticks, sorbets, mochi, pints, lollies, soft-serve, and ice cream sandwiches |

Emerging |

Franchise model extend the experiential playbook across the UAE while preserving premium niche positioning |

Key players include Nestlé, General Mills Inc., Ferrero, IFFCO, The Brooklyn Creamery, DesertChill, and others.

Key Company Profiles

Ferrero

Ferrero formally entered the UAE ice cream segment in May 2024, launching Kinder Bueno, Ferrero Rocher, and Raffaello ice cream ranges with a high-profile Palm Jumeirah drone-show event. The launch leverages Ferrero's entrenched chocolate brand equity to accelerate premium frozen dessert adoption.

- Product Portfolio: Offers Kinder Bueno, Ferrero Rocher, and Raffaello ice cream sticks, cones, and tubs for UAE impulse and take-home channels.

- Recent Developments: In May 2024, Ferrero Group launched a new range of ice cream products in the UAE, bringing its well-known chocolate brands into a frozen dessert format. The lineup includes flavors inspired by popular products such as Kinder Bueno, Ferrero Rocher, and Raffaello, allowing consumers to enjoy familiar tastes in a new way.

- Strategic Focus: Ferrero's UAE strategy translates its confectionery equity into premium ice cream adjacency, targeting gifting, in-home indulgence, and HoReCa dessert menus, supported by experiential activation and prominent secondary placement at Carrefour, Spinneys, and Lulu premium fixtures.

The Brooklyn Creamery

The Brooklyn Creamery is a UAE-based health-positioned ice cream brand specializing in keto-friendly, low-calorie, and no-added-sugar formulations. Its differentiated positioning and digital-first distribution through Noon Minutes and premium supermarkets have driven rapid share gains within the functional indulgence niche.

- Product Portfolio: Offers keto-friendly tubs and low-calorie creamsicle bars across vanilla, mango, raspberry, and pecan-caramel variants.

- Recent Developments: In September 2025, The Brooklyn Creamery introduced a new gelato range in the UAE, expanding its portfolio with a product that combines indulgence with healthier positioning. Inspired by traditional Italian gelato and reimagined with a modern twist, the offering delivers a rich and creamy experience while maintaining a lighter nutritional profile.

- Strategic Focus: Brooklyn Creamery focuses on health-positioned differentiation, lean SKU innovation cycles, and digital-first distribution as its primary competitive levers, targeting fitness-oriented, diabetic-aware, and premium-indulgence consumer cohorts across Dubai, Abu Dhabi, and Sharjah modern-trade networks.

DesertChill

Desert Chill is the UAE's premier mobile and hand-crafted ice cream company, positioned as a homegrown experiential brand rather than a mass-market manufacturer. Desert Chill combines a branded ice cream van fleet with the DesertChill Kitchen production facility in Al Quoz to serve Dubai, Abu Dhabi, Sharjah, Al Ain, and Umm Al Quwain with event-led, schools, and corporate-catering ice cream experiences.

- Product Portfolio: Offers a hand-crafted range of premium gelato sticks, sorbets, ice cream sandwiches, mochi, pints, lollies, and soft serve across signature flavors.

- Strategic Focus: Desert Chill's UAE strategy centers on experiential premium ice cream delivered through mobile-van distribution at schools, corporate offices, brand activations, and family gatherings rather than modern-trade retail, leveraging its homegrown hand-crafted production model, bespoke flavor innovation tuned to UAE expatriate and Emirati tastes, and co-branded truck-activation partnerships with blue-chip corporates.

Market Concentration Analysis

The UAE ice cream market is moderately fragmented, with the top three participants – Ferrero, Nestlé, and General Mills - accounting for an estimated 40-45% combined value share in 2025. The remainder is distributed across Ferrero, Baskin-Robbins, regional specialists, and a long tail of artisanal parlors and homegrown brands.

Consolidation pressure is rising in the premium artisanal niche, where scaling parlor chains and private-equity-backed dessert groups are acquiring single-location operators. At the mass level, global multinationals are deepening UAE footprints through selective M&A, co-packing partnerships, and brand-extension launches into frozen desserts.

Investment & Growth Opportunities

Fastest-Growing Segments

Premium health-oriented ice cream at ~4.8% CAGR and artisanal parlor formats at ~4.2% CAGR are the highest-growth sub-segments through 2034, driven by Dubai's affluent consumer base, tourism inflow, and continued reformulation toward low-sugar, plant-based, and clean-label indulgence profiles.

Emerging Regional Pockets

Sharjah and the Northern Emirates collectively at ~3.0% CAGR are the fastest-growing regional pockets beyond Dubai and Abu Dhabi, driven by rising tourism in Ras Al Khaimah, expanding organized retail in Ajman and Fujairah, and increasing household penetration of branded take-home formats across value-focused consumers.

Venture & Investment Trends

Private equity and regional food-tech investment is flowing into health-positioned and quick-commerce-native ice cream brands. Sovereign-linked F&B investment vehicles continue to back premium artisanal concepts, while multinationals are investing in local co-manufacturing and cold-chain partnerships to reduce import dependency.

Future Market Outlook (2026-2034)

The UAE ice cream market is forecast to expand from USD 390.37 Million in 2025 to USD 507.43 Million by 2034, adding roughly USD 117 Million in incremental value at a CAGR of 2.85%. This steady growth reflects the market's combination of year-round consumption, tourism tailwinds, and structural premiumization across key emirates.

Three forces will most significantly shape the UAE ice cream landscape through 2034. Quick-commerce penetration will recast the impulse channel and pack architecture; health-led reformulation will redefine premium positioning across sugar, fat, and plant-based dimensions; and cultural-fusion innovation will anchor tourist-facing and heritage indulgence occasions.

Research Methodology

Primary Research

Primary research included structured interviews with UAE ice cream industry stakeholders in 2024-2025, including senior commercial managers at multinational manufacturers, procurement leads at Carrefour, Lulu, and Spinneys, quick-commerce category managers, HoReCa procurement heads, and independent parlor operators across Dubai and Abu Dhabi.

Secondary Research

Key secondary sources include UAE Federal Competitiveness and Statistics Centre data, Dubai Department of Economy and Tourism statistics, UAE FDA and ESMA publications, Statista UAE frozen desserts dashboards, Euromonitor ice cream reports, company annual reports, press releases, and trade publications covering UAE and GCC food and beverage.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches, incorporating UAE GDP growth, tourism arrivals, disposable income trends, category penetration curves, and historical category evolution. Scenario analysis across base, optimistic, and conservative cases was performed.

UAE Ice Cream Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Flavours Covered | Vanilla, Chocolate, Fruit, Others |

| Categories Covered | Impulse Ice Cream, Take-Home Ice Cream, Artisanal Ice Cream |

| Products Covered | Cup, Stick, Cone, Brick, Tub, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Convenience Stores, Ice Cream Parlors, Online Stores, Others |

| Regions Covered | Dubai, Abu Dhabi, Sharjah, Others |

| Companies Covered | Nestlé, General Mills Inc., Ferrero, IFFCO, The Brooklyn Creamery, DesertChill, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the UAE ice cream market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the UAE ice cream market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the UAE ice cream industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the UAE Ice Cream Market Report

The UAE ice cream market reached USD 390.37 Million in 2025, reflecting steady demand from rising disposable incomes, a young multicultural population, year-round consumption, and robust tourism-led HoReCa activity.

The UAE ice cream market is projected to reach USD 507.43 Million by 2034, growing at a CAGR of 2.85% during 2026-2034, driven by premiumization, tourism, quick-commerce, and health-oriented innovation.

Impulse ice cream leads with a 46.2% category share in 2025, supported by the UAE's dense forecourt network, hot year-round climate, and high on-the-go consumption by residents and tourists across the emirates.

Vanilla dominates the UAE flavor mix at 31.6% in 2025, owing to its versatility across cones, sundaes, cakes, and HoReCa dessert menus, and its role as a premium base for heritage and gourmet flavor pairings.

Dubai commands a 49.8% share in 2025, driven by concentrated tourism, premium retail density, hotel and beach-club HoReCa demand, and advanced quick-commerce penetration through Noon Minutes, Talabat, Careem, and Instashop.

Artisanal ice cream is the fastest-growing category at ~4.2% CAGR through 2034, driven by Dubai's premium parlor expansion, cultural-fusion flavor innovation, and tourist willingness to pay for craft and experiential dessert formats.

Leading companies include Nestlé, General Mills Inc., Ferrero, IFFCO, The Brooklyn Creamery, DesertChill, and others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)