UAE Real Estate Market Size, Share, Trends and Forecast by Property, Business, Mode, and Region, 2026-2034

UAE Real Estate Market Size, Share, Trends & Forecast (2026-2034)

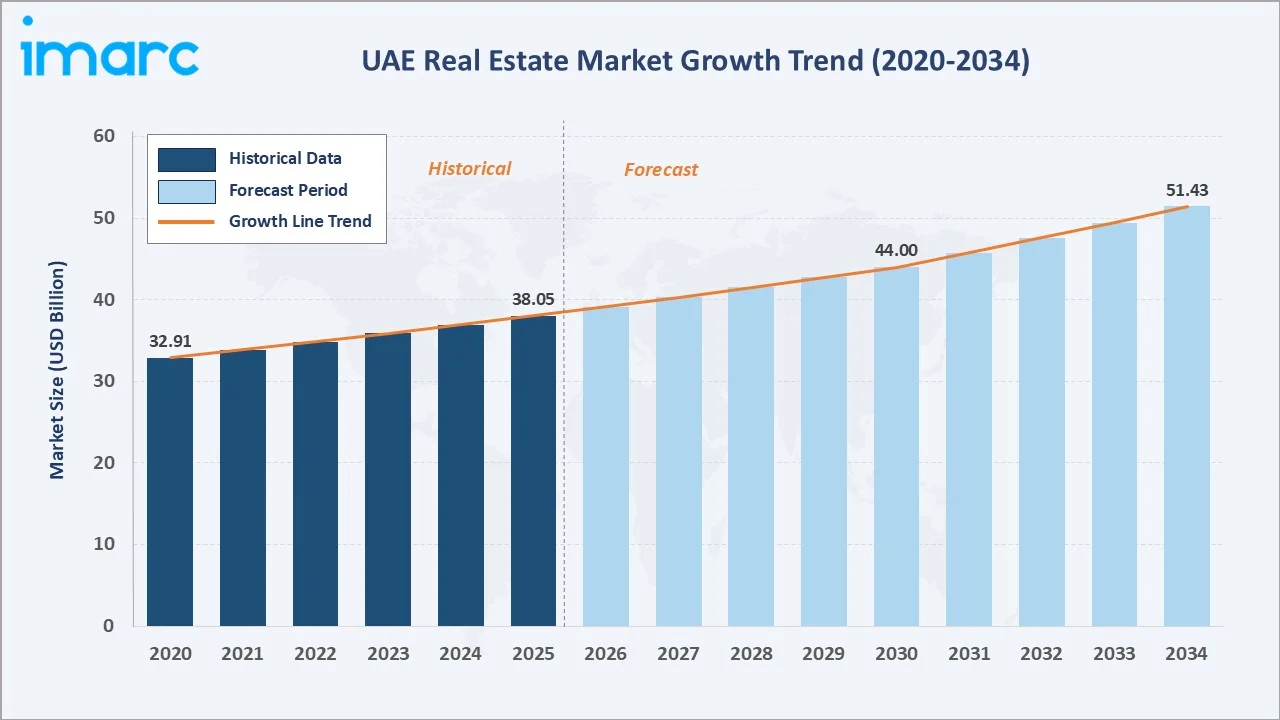

The UAE real estate market reached USD 38.05 Billion in 2025 and is projected to reach USD 51.43 Billion by 2034, growing at a CAGR of 2.95% during 2026-2034. Robust population growth, a sustained influx of high-net-worth expatriates, progressive visa reforms, the Dubai 2040 Urban Master Plan, and strong tourism and hospitality demand are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 38.05 Billion |

|

Forecast Market Size (2034) |

USD 51.43 Billion |

|

CAGR (2026-2034) |

2.95% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Dubai (52.7%, 2025) |

|

Fastest Growing Region |

Abu Dhabi |

Sales transactions account for 59.4% of the market in 2025, driven by strong investor demand for off-plan developments, luxury villas, and branded residences. Dubai’s continued dominance at 52.7% reflects its global city positioning, superior connectivity, and world-class lifestyle infrastructure that attract both regional and international capital flows.

To get more information on this market, Request Sample

With applications spanning residential, commercial, industrial, and land segments across Dubai, Abu Dhabi, Sharjah, and the northern emirates, the market is positioned for steady, structurally-anchored growth through 2034, supported by sustained global investment, government-led economic diversification, and rapid urbanization of the UAE’s growing population.

Executive Summary

The UAE real estate market demonstrates resilient, broad-based growth underpinned by the confluence of progressive policy reforms, sustained investor interest, and structural demographic tailwinds. The market grew from USD 32.91 Billion in 2020 to USD 38.05 Billion in 2025, a CAGR of approximately 2.95%, and is forecast to reach USD 51.43 Billion by 2034, cementing the UAE’s position as the Middle East’s most liquid and internationally accessible real estate market.

Dubai remains the undisputed engine, commanding a 52.7% market share in 2025. Dubai’s real estate transactions reached 226,000, with a total value of AED 761 billion, reflecting a 36% year-on-year increase in volume and a 20% rise in value. It reflects sustained demand across residential, commercial, and hospitality segments. Abu Dhabi (27.6%) is the fastest-growing emirate, driven by the Yas Island, Saadiyat Island, and Al Reem Island mega-developments and favorable mortgage policies from ADREC.

Sales transactions lead at 59.4% of market value, anchored by off-plan purchases from HNW investors seeking UAE Golden Visa qualification and lifestyle migration. Offline transaction channels retain a 68.2% share, though PropTech platforms, including Property Finder, Bayut, and dubizzle, are rapidly digitizing the brokerage and listing ecosystem.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Business) |

Sales – 59.4% share (2025) |

|

Largest Segment (Mode) |

Offline – 68.2% share (2025) |

|

Leading Region |

Dubai – 52.7% share (2025) |

|

Fastest Growing Region |

Abu Dhabi (Saadiyat, Yas Island expansion) |

|

Top Companies |

Emaar Properties PJSC, Aldar Properties, DAMAC, Deyaar Development PJSC, and Dubai Holding |

|

Market Opportunity |

PropTech-enabled off-plan sales and affordable housing segments |

Key Analytical Observations:

- Sales transactions command 59.4% of market value in 2025, reflecting strong investor appetite for UAE property as a wealth preservation asset class. Off-plan sales account for approximately 65% of all Dubai residential sales, enabled by developer payment plans and Golden Visa qualification thresholds.

- Offline channels hold 68.2% of transactions in 2025, reflecting the high-value, relationship-driven nature of UAE real estate. However, PropTech platforms are rapidly gaining share; Property Finder secured USD 170 million from Mubadala in January 2026 to scale its AI-driven marketplace.

- Dubai dominates at 52.7%, driven by Dubai’s delivery of 44,000 units in 2025, the highest in five years (Cushman & Wakefield Core), sustained demand from India, UK, Russia, and China-based investors, and the Dubai 2040 Urban Master Plan targeting a population of 5.8 million by 2040.

- Abu Dhabi is the fastest-growing emirate, recording a 47.43% year-on-year increase in residential sales transactions in 2025 per ADREC, driven by Aldar’s mega-community launches and relaxed foreign ownership rules.

- Rental market growth (40.6% of transactions) is accelerating. Dubai's average gross rental yield currently ranges from 6% to 8%, making the UAE one of the highest-yielding real estate markets among global gateway cities.

UAE Real Estate Market Overview

The UAE real estate market encompasses residential (apartments, villas, townhouses), commercial (offices, retail, hospitality), industrial (warehouses, logistics parks), and land transactions across seven emirates. The market is structured around a dual-track system: primary sales by master developers (Emaar, Aldar, DAMAC), and Dubai has over 4,500 registered real estate brokerage firms as of Q1 2026

Macroeconomic fundamentals are supportive. UAE real GDP growth accelerated to 4.8% in 2025 per IMF estimates, with 5.0% projected for 2026, the fastest rate among GCC countries. As of April 2026, the population of the UAE is estimated at 11,596,422, based on Worldometer’s analysis of the latest United Nations data, driven by skilled expatriate inflow from South Asia, Europe, Russia, and China, each cohort generating distinct property demand profiles. The UAE’s political stability, zero personal income tax, and transparent property registration system remain structural competitive advantages relative to other global property markets.

Market Dynamics

To evaluate market opportunities, Request Sample

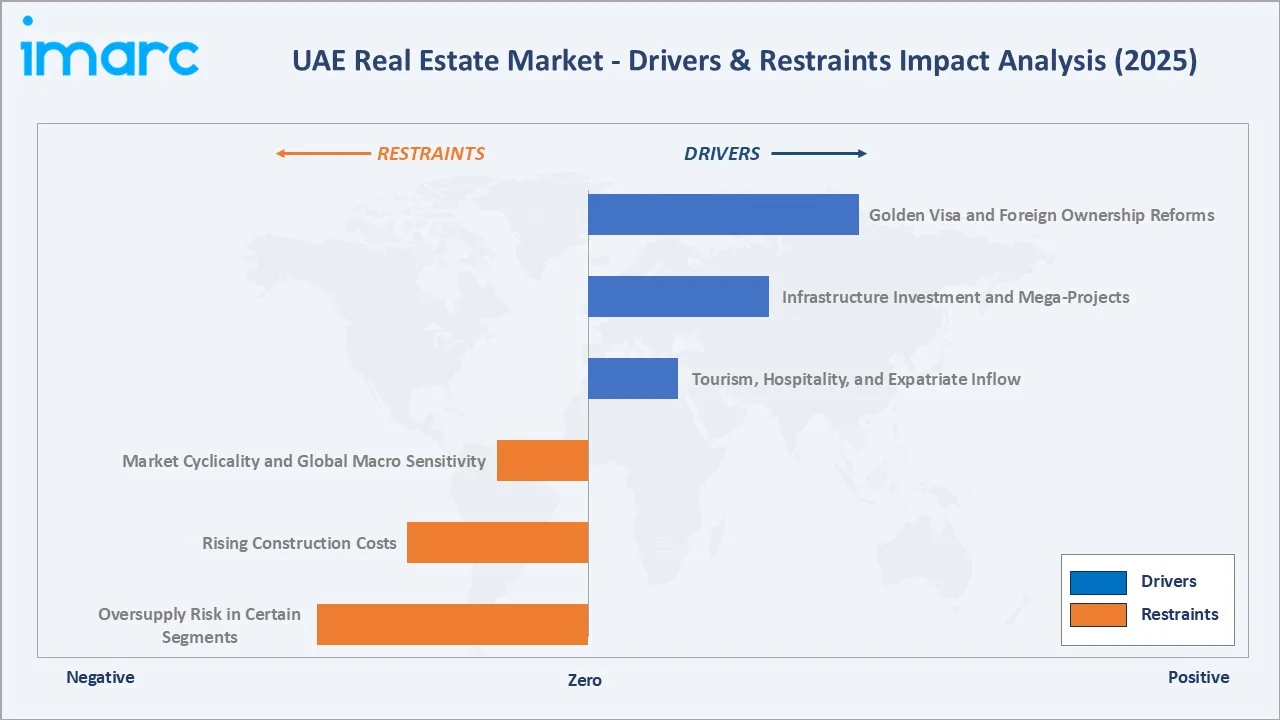

Market Drivers

- Golden Visa and Foreign Ownership Reforms: The minimum threshold remains AED 2 million (approximately USD 545,000), as determined by Dubai Land Department (DLD) valuation or title deed. 100% foreign freehold ownership rights in designated zones across all seven emirates continue to attract international capital, with resident expatriates and foreign direct investment collectively accounting for 62% of the total residential sales value in Abu Dhabi.

- Tourism, Hospitality, and Expatriate Inflow: Dubai received 18.72 million international visitors in 2024, sustaining demand for short-term rentals, holiday homes, and hospitality-linked real estate. Corporate migration from Europe and Asia-Pacific into UAE free zones and DIFC drives Grade A office demand.

- Infrastructure Investment and Mega-Projects: Dubai 2040 Urban Master Plan designates five urban centers and targets significant expansion of affordable housing, green corridors, and transport networks. Aldar and Dubai Holding’s joint announcement of AED 38 billion in new Dubai plots (February 2026) to deliver 14,000 homes signals sustained pipeline investment.

- Population Growth and Urbanization: UAE’s population is projected to reach 20 million by 2075, driven by continued economic diversification under UAE Vision 2030 and digital economy initiatives.

Market Restraints

- Rising Construction Costs: Construction material costs in the UAE rose 18–22% between 2022 and 2024, driven by global supply chain disruptions, steel price volatility, and skilled labor shortages. Developer margins on affordable and mid-market projects are compressed, potentially limiting the supply pipeline in the sub-AED 1.5 million segment where demand is structurally strongest.

- Oversupply Risk in Certain Segments: Dubai’s housing stock grew from 556,000 units in 2019 to 752,000 units in 2024, reflecting a compound annual growth rate (CAGR) of 6.2%, potentially exceeding organic demand in select micro-markets such as Jumeirah Village Circle and Business Bay.

Market Opportunities

- Off-Plan Sales and Payment Plan Innovation: Off-plan sales reached 65% of total Dubai transactions in 2024. Digital platforms enabling off-plan sales to international buyers without site visits represent a USD 4+ billion annual incremental opportunity.

- Affordable and Mid-Market Housing Demand: The UAE government’s Mohammed Bin Rashid Housing Establishment program and Abu Dhabi Housing Authority investments signal policy support for affordable supply creation, with an addressable market of USD 6–8 billion annually by 2030.

- PropTech and Digital Real Estate: Property Finder, Bayut, dubizzle, and emerging AI-native platforms are transforming search, valuation, and transaction workflows. Real estate tokenization is progressing toward regulatory approval under ADGM and DIFC frameworks, potentially opening a USD 1–2 billion fractional ownership market by 2030.

Market Challenges

- Market Cyclicality and Global Macro Sensitivity: UAE real estate is sensitive to global risk sentiment, oil price cycles, and US dollar strength. The 2008–2009 crash and 2014–2020 correction cycles demonstrated significant downside volatility during global financial stress. Post-COVID recovery has been exceptional, but the concentration of the buyer base in a few key expatriate nationalities creates single-cohort demand risk during geopolitical disruptions.

- Regulatory Harmonization Across Emirates: Each emirate maintains separate real estate regulatory authorities (RERA in Dubai, ADREC in Abu Dhabi, Sharjah Real Estate Registration Department). Divergent escrow, registration, and ownership rules create friction for cross-emirate investment portfolios and complicate due diligence for international institutional investors seeking UAE-wide exposure.

Emerging Market Trends

1. Golden Visa Reform and Lifestyle Migration

The UAE’s 2020–2022 Golden Visa reforms, expanding categories, reducing property thresholds to AED 2 million, and introducing retirement visas, triggered a structural shift in the buyer composition. Foreign nationals accounted for 68% of Dubai residential transactions by value in Q1 2026, with Indian, Russian, British, and Chinese investors leading volumes. This internationalization of the buyer base has deepened market liquidity and reduced cyclical volatility.

2. Off-Plan Sales Boom and Developer Innovation

Dubai’s off-plan market accounted for 65% of total residential sales in 2024, with developers including Emaar, DAMAC, and Sobha Realty launching 47,000+ new units across master-planned communities. Sobha Realty’s USD 13.6 billion Sobha Sanctuary (20,000 planned homes, January 2026) exemplifies the mega-community model that is reshaping Dubai’s residential supply landscape.

3. PropTech and Digital Listing Disruption

UAE’s real estate portal ecosystem, led by Property Finder, Bayut, and dubizzle, is transitioning from listing aggregators to AI-powered transaction platforms. Property Finder’s USD 170 million investment from the Mubadala Investment Company (January 2026) will fund AI-driven valuation, mortgage origination, and virtual tour capabilities.

4. Green Buildings and Smart City Developments

UAE’s Green Building Code and Estidama Pearl Rating System are reshaping new supply standards. Meraas’ 18 million sq ft Dubai Design District (d3) expansion (January 2026) and BEEAH’s Khalid Bin Sultan City sustainable urban development (June 2025) illustrate the mainstreaming of ESG credentials in property development.

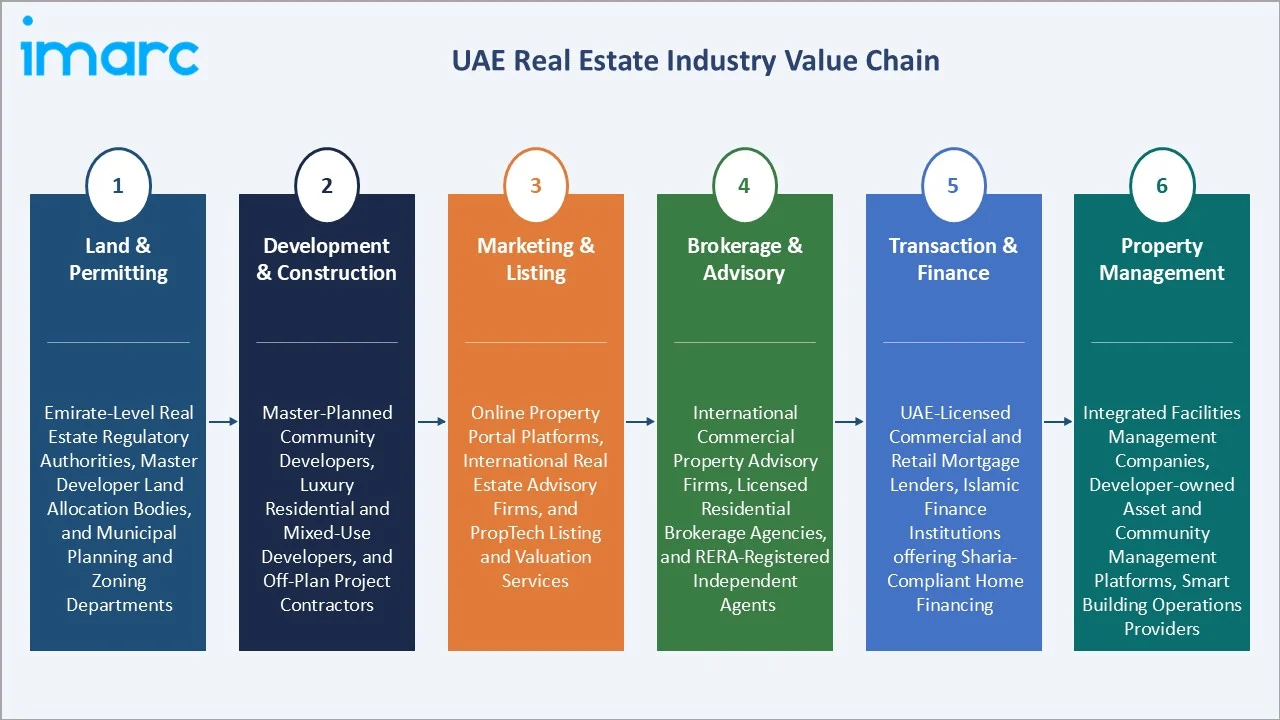

Industry Value Chain Analysis

The UAE real estate value chain spans land and regulatory permitting through construction, marketing, brokerage, transaction settlement, and ongoing property management, with specialized operators at each stage whose performance directly shapes asset quality, transaction liquidity, and investor returns.

|

Stage |

Key Players / Examples |

|

Land & Permitting |

Emirate-level real estate regulatory authorities, master developer land allocation bodies, and municipal planning and zoning departments |

|

Development & Construction |

Master-planned community developers, luxury residential and mixed-use developers, and off-plan project contractors |

|

Marketing & Listing |

Online property portal platforms, international real estate advisory firms, and PropTech listing and valuation services |

|

Brokerage & Advisory |

International commercial property advisory firms, licensed residential brokerage agencies, and RERA-registered independent agents |

|

Transaction & Finance |

UAE-licensed commercial and retail mortgage lenders, Islamic finance institutions offering Sharia-compliant home financing |

|

Property Management |

Integrated facilities management companies, developer-owned asset and community management platforms, and smart building operations providers |

Technology Landscape in the UAE Real Estate Industry

AI-Powered Property Search and Valuation

AI algorithms deployed by Property Finder, Bayut, and dubizzle personalise property recommendations, automate AVM (automated valuation model) estimates, and predict rental yield performance across micro-markets. Machine learning models trained on 10+ years of DLD transaction data now achieve sub-5% pricing error rates in established Dubai communities.

Real Estate Tokenization and Fractional Ownership

ADGM and DIFC regulatory sandboxes are advancing frameworks for property tokenization under blockchain protocols. SmartCrowd and Stake have pioneered fractional ownership platforms enabling investments from AED 500, democratizing access to Dubai’s prime property yields.

Virtual Tours, BIM, and Digital Twin Infrastructure

Emaar, DAMAC, and Aldar deploy 3D virtual tour technology and building information modelling (BIM) to enable remote buyers to transact on off-plan properties without site visits. Digital twin platforms integrating IoT sensor data, energy performance, and predictive maintenance analytics are being deployed in Aldar’s Yas Island master communities.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Property | 🔒 | 🔒 | 2025 |

| Business | Sales | 59.4% | 2025 |

| Mode | Offline | 68.2% | 2025 |

| Region | Dubai | 52.7% | 2025 |

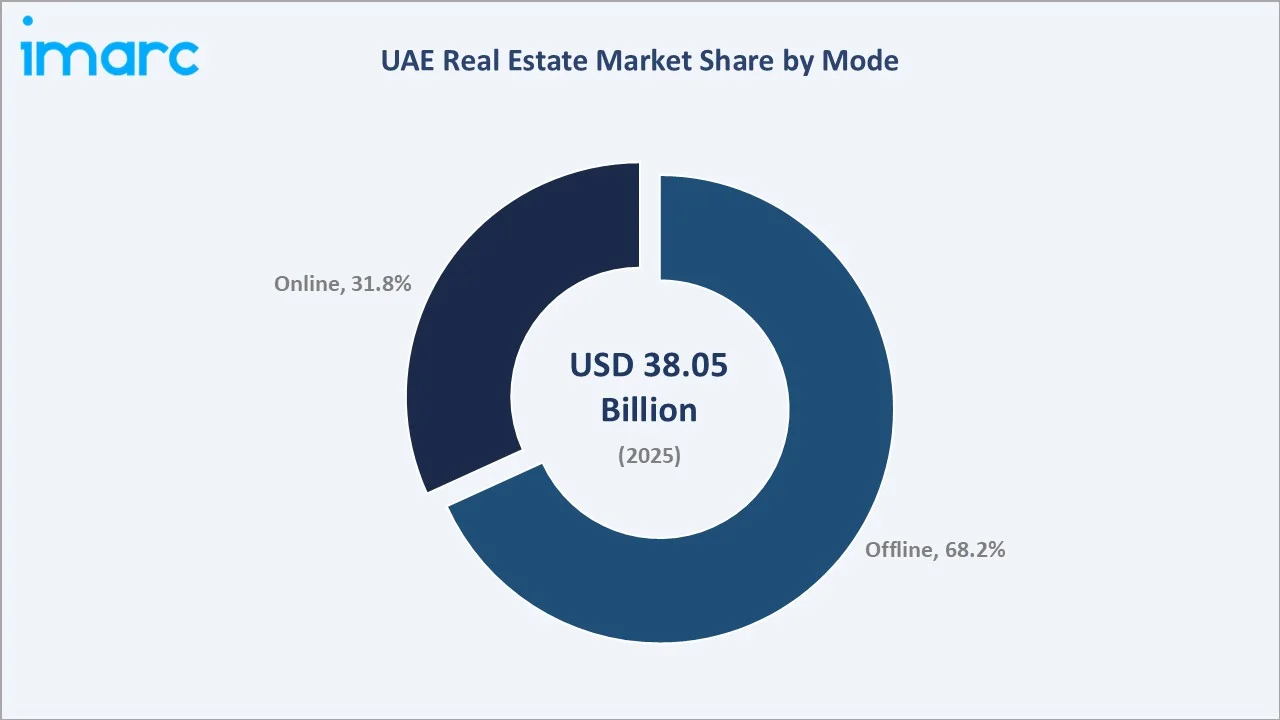

By Mode

Offline transactions dominate the UAE real estate market with a 68.2% share in 2025. The high-value, documentation-intensive nature of UAE property transactions, requiring DLD registration, notarized sale agreements, and mortgage or cash settlement, sustains the primacy of in-person brokerage relationships.

To access detailed market analysis, Request Sample

Online channels hold a 31.8% share and represent the fastest-growing distribution mode. Property discovery is overwhelmingly digital, with over 85% of buyers in Dubai initiating their property search online, though transaction closure typically migrates offline. PropTech investment is accelerating the digitization of transaction workflows, including e-signature, mortgage origination, and DLD registration.

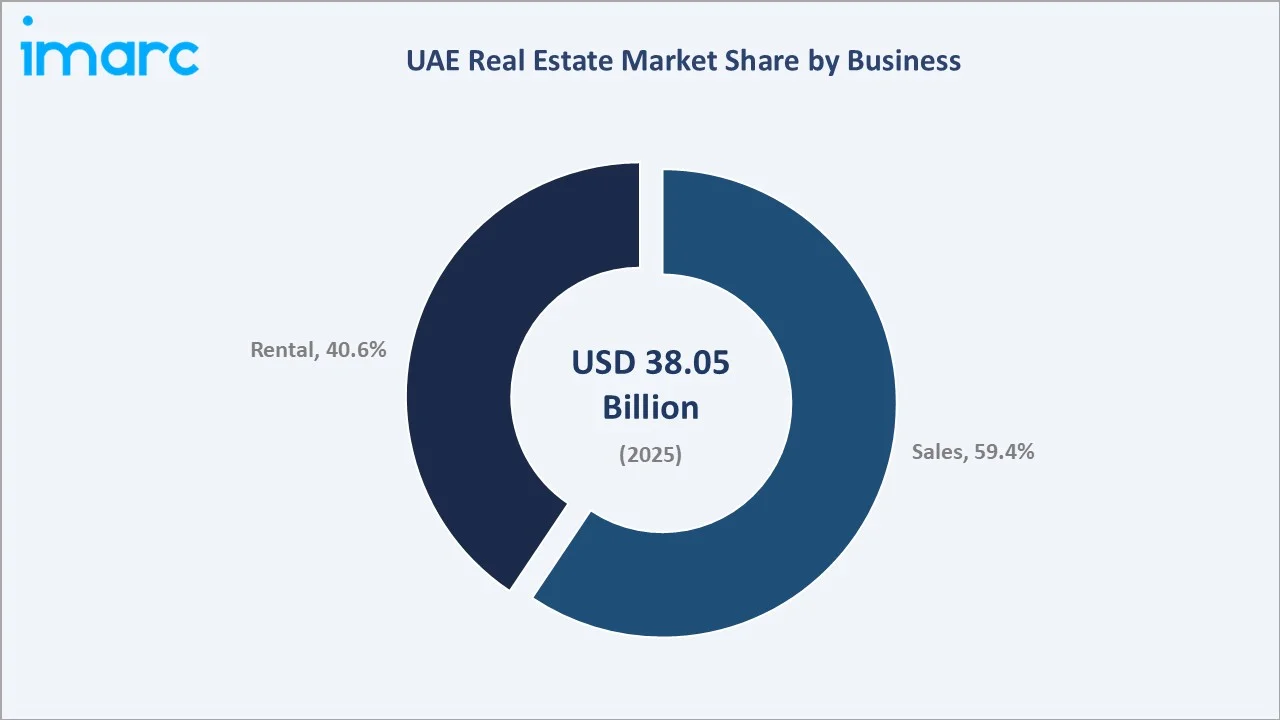

By Business

Sales transactions lead the business segment with a 59.4% share in 2025. Dubai’s off-plan market is the dominant sales driver, accounting for 65% of all Dubai residential transactions. Developer incentives, including post-handover payment plans, guaranteed rental returns, and service charge waivers, have expanded the buyer base to include first-time buyers and mid-income investors previously priced out of UAE property ownership.

Rental transactions account for 40.6% of market value. Dubai residential gross rental yields range from 6% to 8%, making it among the highest-yielding real estate markets in any global gateway city. Annual rent increases across prime Dubai communities averaged 14–22% in 2024, reflecting a structural supply-demand imbalance in established neighborhoods.

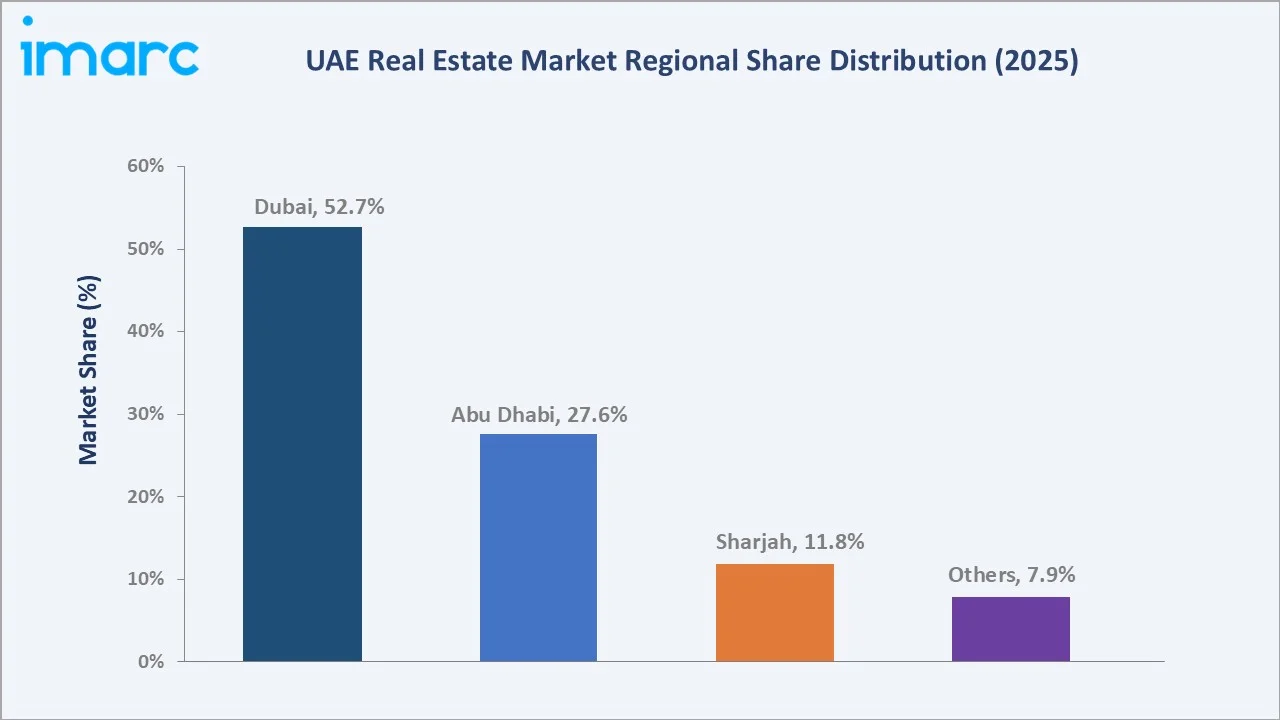

Regional Market Insights

Dubai commands a 52.7% share of the UAE real estate market in 2025, driven by its position as the MENA region’s premier global city, luxury lifestyle destination, and international financial hub. Dubai’s real estate market transacted AED 761 billion across 180,987 deals in 2024, a 36% volume increase year-on-year.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Dubai |

52.7% |

Golden Visa investors, luxury lifestyle, off-plan demand |

|

Abu Dhabi |

27.6% |

Foreign ownership reform, Saadiyat, Yas Island |

|

Sharjah |

11.8% |

Affordable housing, commuter demand, and industrial zones |

|

Others |

7.9% |

RAK, Ajman: value investment; Fujairah: industrial |

Abu Dhabi (27.6%) is the fastest-growing emirate per unit growth rate, with ADREC recording a 47% year-on-year increase in residential transactions in 2025. Saadiyat Island’s cultural and luxury positioning and Yas Island’s entertainment-anchored community are driving premium residential demand. Sharjah (11.8%) serves the affordable housing market, with SIBCA-registered developments attracting price-sensitive buyers.

Competitive Landscape

The UAE real estate market exhibits a moderately concentrated structure at the primary developer level, with Emaar Properties, Aldar Properties, DAMAC, and Nakheel collectively accounting for an estimated 45–50% of primary residential sales revenue in 2025.

|

Company |

Entity |

Market Position |

Core Strength |

|

Emaar Properties PJSC |

Emaar Properties PJSC |

Market Leader |

Largest UAE developer; Downtown Dubai, Dubai Hills Estate, Emaar Beachfront; consistent delivery record |

|

Aldar Properties |

Aldar Properties PJSC |

Market Leader |

Abu Dhabi market leader; Saadiyat, Yas Island communities; strong ESG credentials |

|

DAMAC |

DAMAC Properties |

Strong Challenger |

Luxury branded residences (Cavalli, Trump, Versace); strong international investor relations |

|

Deyaar Development PJSC |

Deyaar Development PJSC |

Challenger |

Dubai-listed affordable to mid-market; strong Dubai Silicon Oasis presence |

|

Dubai Holding |

Dubai Holding |

Market Leader |

Jumeirah, a global leader in luxury hospitality; City Walk; Madinat Jumeirah Living; Aldar JV (USD 10.3 Bn Dubai pipeline) |

The secondary market, brokered through 8,000+ licensed agents and 400+ registered agencies in Dubai alone, is highly fragmented.

Key Company Profiles

Emaar Properties PJSC

Emaar Properties PJSC, listed on the Dubai Financial Market (DFM), is the UAE’s largest publicly listed real estate developer by market capitalization and the creator of Downtown Dubai, one of the world’s most visited urban destinations.

- Product Portfolio: Residential communities (Dubai Hills Estate, Emaar Beachfront, Arabian Ranches); retail malls (The Dubai Mall, Dubai Marina Mall); hospitality (Address Hotels, Vida Hotels).

- Recent Developments: In February 2026, Emaar Properties inaugurated three new mosques across its Dubai communities. The newly opened mosques are located in Dubai Creek Harbour, Emaar South, and Arabian Ranches III.

- Strategic Focus: Master-planned community development; recurring income from malls and hospitality; international expansion in India, Egypt, and Saudi Arabia.

Aldar Properties

Aldar Properties is Abu Dhabi’s premier real estate developer, operating an integrated business spanning development, property management, and facilities management across residential, commercial, retail, and hospitality assets.

- Product Portfolio: Yas Island communities (Ansam, Noya), Saadiyat Island (Saadiyat Grove), Al Reem Island developments; Aldar Facilities Management, Aldar Retail.

- Recent Developments: As of April 2026, Aldar Properties reported that its Yas Island project in Abu Dhabi exceeded AED 800 million in sales, driven by strong local and international investor demand. Residents and overseas buyers accounted for 54% of sales, with high participation from investors in Jordan, China, Taiwan, and the UK.

- Strategic Focus: Cross-emirate expansion; recurring income from investment portfolio; sustainability leadership (Estidama Pearl ratings); institutional-grade build-to-rent platform.

DAMAC

DAMAC is the UAE’s leading luxury developer, known for internationally branded residences in partnership with fashion houses (Roberto Cavalli) and hotel groups. DAMAC targets the premium and ultra-luxury segment, with strong brand recognition among Middle Eastern, European, and South Asian HNW investor communities.

- Product Portfolio: DAMAC Hills, Safa One, Cavalli Tower, Lagoons (Dubai); DAMAC Maison (serviced apartments); international developments in the UK, Canada, and KSA.

- Recent Developments: DAMAC recorded AED 3.12 billion in March 2026 sales across 1,106 transactions, leading Dubai’s property market and capping a strong Q1 performance with 3,663 units sold.

- Strategic Focus: Ultra-luxury branded residential development; international investor marketing; serviced apartment income diversification.

Market Concentration Analysis

The UAE real estate market is moderately concentrated in the primary development segment, with the top four developers (Emaar, Aldar, DAMAC, Nakheel/Dubai Holding) controlling approximately 45–50% of primary sales value. The secondary brokerage market is highly fragmented, with no single agent or agency holding more than 3–4% market share across the UAE.

PropTech consolidation is accelerating rapidly. Property Finder’s USD 170 million Mubadala funding round in January 2026 signals an intent to acquire smaller portals and build an end-to-end transaction platform. Dubizzle Group’s MENA-wide platform (Bayut + dubizzle) and Allsopp & Allsopp’s franchise expansion exemplify different consolidation vectors in the ecosystem.

Investment & Growth Opportunities

Fastest Growing Segments

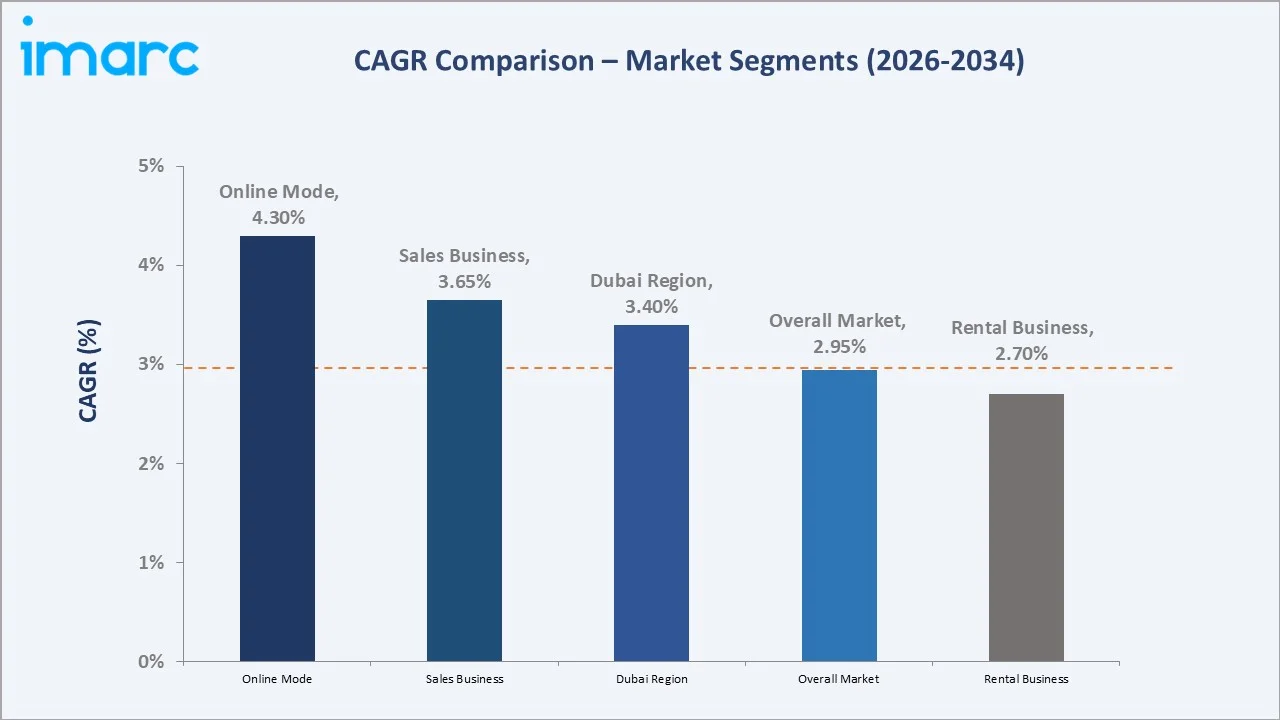

Online real estate transaction platforms (estimated CAGR 15–18%), affordable and mid-market residential communities (8–10% CAGR), and build-to-rent institutional portfolios (12% CAGR) represent the three highest-growth investment vectors through 2034. These segments collectively address an incremental market exceeding USD 8 Billion within the UAE by 2034.

Emerging Market Expansion

Ras Al Khaimah represents the UAE’s highest-growth emirate opportunity through 2034. The Wynn Al Marjan Island integrated resort (2027 opening), RAK’s expanding free zones, and affordable villa communities targeting Dubai overflow demand are driving a forecast 10%+ CAGR. Investment entry via RAK Properties’ listed equity, off-plan purchases in Al Marjan Island, or joint venture development partnerships with Al Hamra Real Estate are preferred strategies.

Venture and Institutional Investment Trends

- Mubadala’s USD 170 million investment in Property Finder (January 2026) signals sovereign wealth fund conviction in UAE PropTech platforms as long-term infrastructure assets.

- ADGM’s and DIFC’s advancing real estate tokenization frameworks are expected to unlock fractional ownership markets, creating a USD 1–2 billion investable asset class by 2030.

- Institutional build-to-rent platforms in the UAE are nascent but accelerating: Aldar’s Residential platform and Nakheel’s managed community portfolio represent the emerging model, attracting pension fund and family office mandates seeking stable, yield-bearing real estate exposure in a zero-tax jurisdiction.

Future Market Outlook (2026-2034)

The UAE real estate market is positioned for sustained, structurally-anchored growth through 2034. From USD 38.05 Billion in 2025, the market will reach USD 44.00 Billion by 2030 and USD 51.43 Billion by 2034, representing total incremental value creation of approximately USD 13.38 Billion over the forecast decade at a CAGR of 2.95%.

Three macro-themes define the long-term trajectory: the UAE’s ongoing success in attracting human capital through visa reforms and zero-tax residency; the Dubai 2040 and Abu Dhabi Economic Vision 2030 infrastructure pipelines; and the PropTech revolution that is digitizing discovery, transaction, and management.

Developers, investors, and service providers that build digital transaction capabilities, ESG-certified asset portfolios, and affordable product lines aligned with the UAE’s growing mid-market professional demographic will be disproportionately positioned to capture the market’s USD 51 billion trajectory through 2034.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 140 industry participants in 2024–2025, including property developers, real estate brokers, RERA-licensed agents, mortgage bankers, PropTech executives, institutional investors, and DLD policy advisors across Dubai, Abu Dhabi, and Sharjah.

Secondary Research

Secondary research encompassed DLD transaction databases, ADREC monthly statistical releases, JLL UAE property market reports, Knight Frank Wealth Report, REIDIN rental yield indices, UAE Federal Competitiveness Authority economic data, and IMF UAE Article IV consultation reports. Over 250 secondary sources were reviewed and triangulated.

Forecasting Models

Market size estimations used a combination of top-down GDP and population-linked real estate penetration models and bottom-up emirate-level transaction value aggregation, validated against DLD and ADREC reported transaction values. Base-case CAGR of 2.95% reflects structural demand growth net of expected supply additions through 2034.

UAE Real Estate Market Report Coverage

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Properties Covered | Residential, Commercial, Industrial, Land |

| Businesses Covered | Sales, Rental |

| Modes Covered | Online, Offline |

| Regions Covered | Dubai, Abu Dhabi, Sharjah, Others |

| Companies Covered | Emaar Properties PJSC, Aldar Properties, DAMAC, Deyaar Development PJSC, Dubai Holding, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the UAE real estate market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the UAE real estate market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the UAE real estate industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the UAE Real Estate Market Report

The UAE real estate market reached USD 38.05 Billion in 2025, up from USD 32.91 Billion in 2020. It is projected to reach USD 51.43 Billion by 2034 at a CAGR of 2.95%.

The market is projected to grow at a CAGR of 2.95% during 2026-2034, supported by population growth, Golden Visa investor inflow, Dubai 2040 infrastructure, and PropTech-enabled transaction digitization.

Dubai leads with a 52.7% market share in 2025, driven by global investor demand, luxury and lifestyle infrastructure, and the world’s most active off-plan residential sales market. Abu Dhabi is the fastest-growing emirate, recording 47% transaction growth in 2025.

Sales transactions lead with 59.4% of market value in 2025, anchored by Dubai’s off-plan market (65% of residential transactions) and Golden Visa-qualifying property purchases from international investors.

Offline transactions hold 68.2% of the market in 2025, reflecting the high-value, relationship-driven nature of UAE property deals. Online channels (31.8%) are the fastest-growing mode, driven by PropTech investment and AI-powered property search platforms.

Key players include Emaar Properties PJSC, Aldar Properties, DAMAC, Deyaar Development PJSC, and Dubai Holding.

Key opportunities include PropTech platforms (CAGR 15–18%), affordable housing communities (8–10% CAGR), build-to-rent institutional portfolios, Ras Al Khaimah market entry via Al Marjan Island, and real estate tokenization platforms targeting the USD 1–2 billion fractional ownership market expected by 2030.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)