UK Cheese Market Size, Share, Trends and Forecast by Source, Type, Product, Format, Distribution Channel, and Region, 2026-2034

UK Cheese Market Size & Forecast 2026-2034

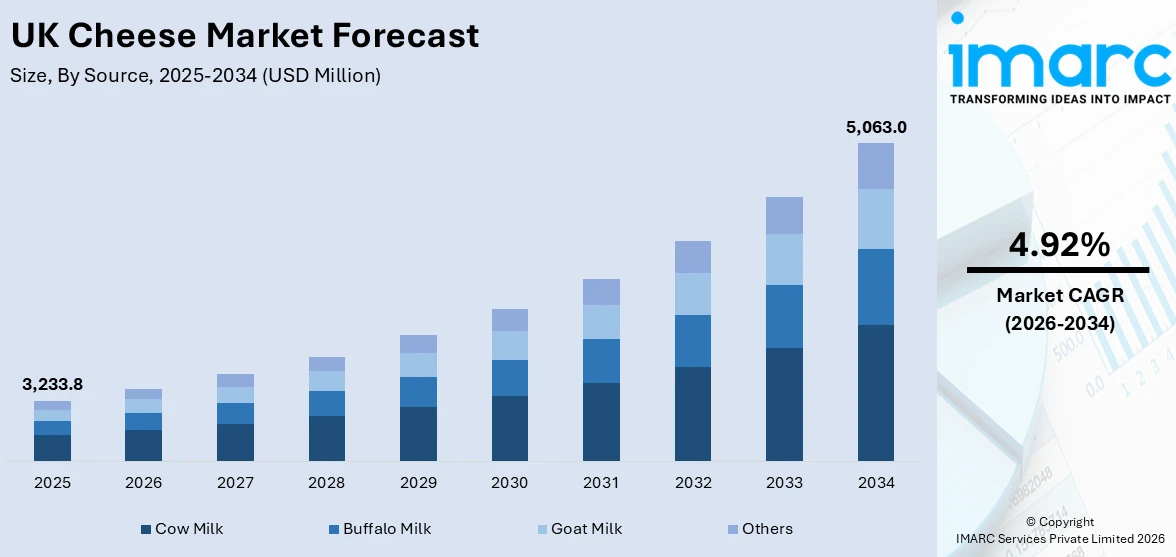

The UK market size, valued at USD 3,233.8 Million in 2025, is projected to reach USD 5,063.0 Million by 2034, growing at a CAGR of 4.92% during 2026-2034, driven by deepening consumer appetite for premium and artisanal varieties, robust export growth, and sustained foodservice demand for mozzarella and cheddar. According to AHDB, UK cheese export volume grew by 2.4% to 3.7T year-on-year in 2025.

To get more information on this market Request Sample

UK Cheese Industry Analysis - Key Insights

- Cow milk commands 90.5% of source share in 2025 - an overwhelming structural anchor of UK cheese supply. The GB milk deliveries reached 1,100 million liters for October 2025, ensuring abundant cow milk for cheddar, mozzarella, and territorial cheese production at a commercial scale.

- Natural cheese leads type at 78.4% in 2025 - nearly four in five cheese purchases in the UK are unprocessed, reflecting a broad and accelerating consumer preference for clean-label, provenance-led dairy products over processed alternatives. Premiumization and PDO-anchored varieties are reinforcing this dominance.

- Cheddar owns 33.2% of product share in 2025 - the definitive volume leader of British cheese. Cheddar accounted for a 3.9% increase in all cow cheese sales volumes for October 2024, making it the structural backbone of both manufacturing output and household consumption.

- Blocks lead format at 42.6% in 2025 - the dominant physical presentation, preferred by households for versatility across cooking, snacking, and sharing occasions. The block format benefits from both value-positioning in cheddar and premium-positioning in aged and territorial varieties purchased at retail.

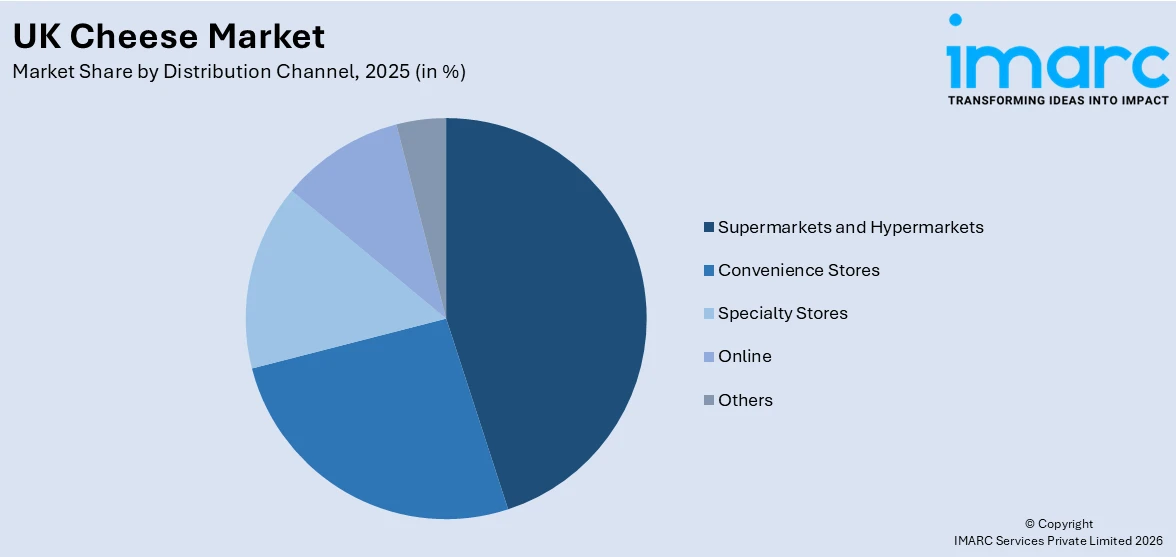

- Supermarkets and hypermarkets command 48.3% of distribution channel in 2025 - nearly half of all UK cheese flows through major grocery multiples. Tesco, Sainsbury's, ASDA, and Morrisons collectively provide the volume throughput and promotional infrastructure that defines mainstream UK cheese accessibility and brand exposure.

- London leads regionally at 15.7% in 2025 - the highest single-region concentration, underpinned by premium foodservice density, a large hospitality and restaurant ecosystem, multicultural population driving specialty and imported cheese demand, and the highest per-capita grocery spending of any UK region.

UK Cheese Market Trends and Dynamic 2026

Premiumization and the Rise of Artisanal and PDO-Anchored Varieties

Consumer demand is splitting in two: value-tier staple cheddar maintains volume growth, while premium artisanal, territorial, and PDO cheeses are recording disproportionate value growth. Specialty brand sales grew 12% across all channels in 2024, fueled by consumers seeking products with provenance credentials, a craft story, regenerative farming, and transparent milk sourcing.

Export Expansion and Growing International Demand for British Cheese

UK cheese exports have become a structural growth driver, underpinning consistent demand from international markets for British cheddar and other cheeses, thereby becoming an important UK cheese market trend. According to AHDB, there was an increase in cheddar export volume to European countries like Germany, Denmark, the Netherlands, Belgium, and Spain. This post-Brexit trade environment, along with the UK-New Zealand trade deal, has positively impacted the market.

- Sustainability and Circular Manufacturing: Carbon-neutral cheddar, regeneratively farmed milk sourcing, and recyclable packaging are becoming strategic differentiators as environmentally conscious consumers prioritize provenance and supply-chain transparency in their cheese purchasing decisions.

- Plant-Based and Dairy-Free Alternatives: Growing veganism and lactose intolerance awareness are expanding the dairy-free cheese segment, with soy, nut, and coconut-based variants gaining incremental shelf space in major multiples and foodservice menus across the UK.

- Private Label Premiumization: Major grocery multiples, including Tesco and Waitrose, are developing premium private-label cheese ranges - including regionally sourced artisanal lines - to capture value-seeking consumers who still want quality differentiation at competitive price points.

- Digital and E-Commerce Channel Growth: Online cheese retail is expanding access for artisan, specialty, and plant-based formats, with home delivery and virtual cheese board platforms enabling smaller producers to reach national audiences beyond traditional retail footprints.

Growth Drivers

Record UK Milk Supply Supporting Competitive Cheese Production Economics

The high milk-to-feed price ratio has incentivized record milk production, which in turn lowers cheese manufacturing costs. GB milk production for the season from April to October stood at 7,661 million liters, reflecting a rise of 5.5% over the same period in 2024. This has led to increased supply and enabled competitive pricing in both the mass-market and premium segments of the cheese market, which in turn positively impacts the UK cheese market.

Foodservice Recovery and Hospitality Sector Expansion

The recovery and expansion of UK foodservice, encompassing restaurants, hotels, quick-service operators, and catering, is generating structural demand growth for mozzarella, cheddar, and continental varieties. Mozzarella consumption is driven by pizza and fast-food chains, while premium cheddar and brie anchor gastropub and restaurant cheese boards. In April 2025, Arla Foods broke ground on its GBP 179 million mozzarella plant at Taw Valley Creamery in Devon, expanding UK production capacity to supply global foodservice customers from a domestic manufacturing base by 2027.

- Government Export Promotion: The active export promotion policy and active participation in international food trade shows by the UK government have contributed to the growth of British cheese brands in export markets like the EU, Asia, and MENA, thus generating incremental revenues for local producers.

- Post-Brexit Trade Deals: The NZ-UK Free Trade Agreement has helped increase dairy export volumes from NZ, with figures rising from NZD 2 million in 2022 to NZD 157 million in June 2025, with NZ dairy products like cheese and butter being major contributors. This has not only increased consumer options but has also encouraged UK-based producers to become more innovative and competitive in terms of value and quality.

- Increasing Grocery Retail Investment in Cheese Counters: Grocery retail chains and high-end food stores are investing in in-store cheese counter experiences, including dedicated staff and artisanal cheese options, thus increasing basket value per cheese counter transaction and attracting high-end consumers.

Market Restraints

High Level of Competition from Continental and Imported Cheese Varieties: The UK is already under intense competition from existing continental cheese varieties such as French brie, Italian parmesan, and Greek feta, among others. These types of cheese command high loyalty from consumers and are being imported on a large scale through existing distribution networks to retailers.

Vulnerability in Supply Chains and Seasonal Variations in Milk Supplies: UK-based cheese manufacturers are vulnerable to seasonal variations in milk supplies. As spring and autumn are associated with milk flushes in the UK, this poses a problem for cheese manufacturers. Decisions regarding milk usage are made on a farm-by-farm basis, while considering competition from butter and powder production causing structural uncertainty for long-term cheese manufacturing commitments.

Shifting Consumer Preferences Toward Non-Dairy and Hard-Surface Alternatives: Growing veganism, flexitarian dietary patterns, and rising lactose-intolerance awareness are gradually redirecting purchasing from traditional dairy cheese to plant-based alternatives, while broader macroeconomic pressures on household discretionary spend can cause consumers to trade down or reduce premium cheese purchase frequency during periods of financial constraint.

.webp)

UK Cheese Market Segmentation Analysis

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Source | Cow Milk | 90.5% | 2025 |

| Type | Natural | 78.4% | 2025 |

| Product | Cheddar | 33.2% | 2025 |

| Format | Blocks | 42.6% | 2025 |

| Distribution Channel | Supermarkets and Hypermarkets | 48.3% | 2025 |

| Region | London | 15.7% | 2025 |

Source Insights

Cow Milk - 90.5% market share (2025) | Leading Source

Cow milk's near-total dominance of the UK cheese market reflects both the depth of the country's bovine dairy farming infrastructure and consumer familiarity with cow milk-derived varieties across all price tiers. The AHDB reported that in December 2025, UK milk production was 1,342 million liters, a 5.2% change from the previous year, confirming cow milk as the overwhelming feedstock for cheddar, mozzarella, territorial, and soft cheese production nationwide. The GB dairy herd supports a mature manufacturing base serving both domestic and export demand at a commercial scale.

|

Segment Breakdown Cow Milk (90.5%) · Buffalo Milk · Goat Milk · Others |

Type Insights

Natural - 78.4% market share (2025) | Leading Type

The dominance of natural cheese is a result of the UK's strong tradition of consuming unprocessed dairy products with genuine flavor characteristics, identifiable ingredient lists, and traceable country of origin. The premiumization of dairy products is fueling consumers to opt for natural cheese over processed variants, as the latter contain emulsifiers, preservatives, and artificial flavor enhancers that are causing consumers to look for alternative products. PDO-protected varieties, including Stilton, Double Gloucester, and Wensleydale, anchor the premium natural tier.

|

Segment Breakdown Natural (78.4%) · Processed |

Product Insights

Cheddar - 33.2% market share (2025) | Leading Product

The dominance of Cheddar's structure is a result of its dual function as the UK's staple cooking product and its most iconic territorial variety. AHDB data from December 2025 shows that Cheddar maintains its position as 44.8% of total cow cheese volumes, enjoying a 1.3% increase. This increase is a testament to its enduring strength in household demand and its position within the UK's retail and foodservice landscape.

|

Segment Breakdown Cheddar (33.2%) · Mozzarella · Feta · Parmesan · Roquefort · Others |

Format Insights

Blocks - 42.6% market share (2025) | Leading Format

The block format holds the largest share within UK cheese retail due to its ability to meet the UK's largest consumer base of household cooking and grating. Cheddar block volumes are the largest individual cheese SKU within UK supermarkets, ranging from economy 400g private-label formats through to premium aged vintage formats from brands such as Wyke Farms, which produces over 13,000 tons of cheddar annually.

|

Segment Breakdown Blocks (42.6%) · Slices · Diced/Cubes · Shredded · Spreads · Liquid · Others |

Distribution Channel Insights

Access the comprehensive market breakdown Request Sample

Supermarkets and Hypermarkets - 48.3% market share (2025) | Leading Distribution Channel

Supermarkets/hypermarkets continue to hold their position as the major channel for British household access to cheese products, underpinned by their extensive inventory breadth, promotional activity, and convenience of shopping during a typical week's groceries. In addition, own-label cheese products form a larger proportion of total category sales as part of supermarket private label initiatives.

|

Segment Breakdown Supermarkets and Hypermarkets (48.3%) · Convenience Stores · Specialty Stores · Online · Others |

Regional Insights

London - 15.7% market share (2025) | Leading Region

London dominates the UK cheese market by regional share. Several key factors are centered within London that are unique to this market compared to other UK cities or regions. These factors include the highest population density and per capita grocery spend within the UK, a multicultural population that drives demand for specialty cheese products, imported cheese products, and international cheese variants. In addition, London has a very dense foodservice and hotel market that requires premium cheese products and Continental-style cheese variants at a massive scale. London has hundreds of specialist cheese retailers and food markets that specialize in cheese products, such as those found at Borough Market.

|

Metric

|

Details

|

|---|---|

|

Market Share in 2025

|

15.7%

|

|

Key States

|

City of London, Westminster, Camden, Southwark, Tower Hamlets, Canary Wharf, Islington, Hackney, Greenwich, Lambeth |

|

Major Growth Drivers

|

Foodservice density, multicultural specialty demand, premium grocery retail investment, food market culture |

|

Outlook

|

Sustained premium-led regional leadership |

|

Regional Breakdown London (15.7%) · South East · North West · East of England · South West · Scotland · West Midlands · Yorkshire and The Humber · East Midlands · Others |

South East:

The South East is driven by a high-income, high-density population, as well as being geographically close to London's thriving food scene and having a long tradition of artisanal dairy farming in areas like Kent, Sussex, and Hampshire. The South East is geographically close to large-scale dairy processing centers as well as developed retail infrastructure, which is beneficial for high-volume as well as high-value cheese spending, mostly focusing on premium products. The high-end retailer Waitrose is another major player that contributes to high-value cheese spending.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Kent, Sussex, Surrey, Hampshire, Berkshire, Oxfordshire, Buckinghamshire |

|

Major Growth Drivers

|

High household income, proximity to London food culture, premium grocery retail density, artisan dairy farming |

|

Outlook

|

Stable premium-led growth with artisan expansion |

North West:

The North West includes Lancashire and Cheshire, two of the most famous cheese-producing areas in England. It has a high concentration of manufacturing and high-density population centers, including Manchester and Liverpool. These two, Lancashire and Cheshire, are two of the oldest types of cheese in England and in the UK. Lancashire and Cheshire cheese makers have been, and still are, significant contributors in the large-scale and specialist retail channels in the UK.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Lancashire, Cheshire, Manchester, Liverpool, Cumbria |

|

Major Growth Drivers

|

Territorial cheese heritage, urban foodservice demand, manufacturing base efficiency, export logistics hubs |

|

Outlook

|

Heritage cheese production driving sustained regional output |

East of England:

The East of England includes some of the most significant dairy farming areas in the country, including Norfolk, Suffolk, and Essex, and the food technology cluster in and around the Cambridge area. According to data from AHDB, cow's cheese retail volume continues to increase in the 52 weeks up to February 2025. It has the advantage of having a high concentration of supermarket-served population, which would guarantee an outlet for conventional blocks of cheddar cheese and other types at value and middle-range price points.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Norfolk, Suffolk, Essex, Cambridgeshire, Hertfordshire, Bedfordshire |

|

Major Growth Drivers

|

Supermarket logistics efficiency, dairy farming density, urban population growth, convenience format demand |

|

Outlook

|

Steady volume growth anchored by grocery multiples |

South West:

The South West is the industrial heartland of cheese manufacturing in Britain. The area is also home to Wyke Farms in Somerset, Barbers Cheese in Somerset, and Taw Valley Creamery in Devon. These companies produce cheddar and mozzarella cheese at industrial levels. The expertise of the South West in cheddar cheese is further complemented by the Cave Aged and Vintage segments, which have the highest retail value per kg compared to other cheddar cheese products in the UK market.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Somerset, Devon, Dorset, Cornwall, Gloucestershire, Wiltshire |

|

Major Growth Drivers

|

Cheddar heritage, record milk supply volumes, new mozzarella manufacturing investment, export infrastructure |

|

Outlook

|

Largest manufacturing region, export-led output growth |

Scotland:

Scotland's cheese manufacturing is underpinned by its traditional cheese manufacturing expertise in farmhouse cheese as well as its industrial-scale dairy manufacturing. The Scottish Dairy Growth Board has identified opportunities for artisan cheese manufacturers in Scotland to replace imported European cheese with Scottish cheese as a result of Brexit. In February 2025, Arla proposed a GBP 90 million investment at its site in Lockerbie site to expand Scottish dairy manufacturing capacity.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Lockerbie, Glasgow, Edinburgh, Ayrshire, Dumfries, Galloway, Highlands |

|

Major Growth Drivers

|

Artisan farmhouse tradition, organic dairy growth, Arla Lockerbie investment, post-Brexit import substitution |

|

Outlook

|

Growing premium artisan tier with manufacturing scale-up |

Market Outlook 2026-2034

What is the future outlook of the UK cheese market?

The UK cheese market is expected to sustain steady revenue growth through 2034.

The UK cheese market has tremendous scope for further growth, and the trajectory of the market will remain strong over the next five years. This is owing to record levels of home milk production, growing export trends, and the consumer environment becoming more favorable to quality, authenticity, and functional innovation. Ongoing investments in mozzarella and cheddar production facilities, such as Arla's plant in Devon, will further enhance the robustness of the supply chain. The cumulative impact of the reformulation trend, the growth of the online channel, and the foodservice channel will ensure the continued growth trajectory of the UK cheese market.

UK Cheese Market - Leading Key Players

The UK market for cheese is a competitive market dominated by the large multinational dairy cooperative groups, established British cheese manufacturers, and a growing segment of artisan and specialist manufacturers. The large players compete on brand investments, scale of manufacture, and innovation in premium and functional products, as well as export success, with several of them benefiting from long-term supplier relationships with the large grocery multiples that are necessary for leading a category in the UK market.

| Company | Leading Brands | Highlights |

|---|---|---|

| Saputo Dairy UK | Cathedral City, Davidstow | Cathedral City is the UK's best-selling cheese brand; expanded lactose-free range in 2024 to meet health-focused demand; strong cheddar manufacturing base in Cornwall |

| Arla Foods UK | Arla, Castello, BOB | Committed GBP 179M to Taw Valley mozzarella plant (April 2025 groundbreak); UK's largest dairy cooperative with ~2,000 British farmer-owners |

| Wyke Farms | Wyke Farms Cheddar, Ivy's Reserve | Produces over 13,000 tons of award-winning cheddar annually; secured GBP 30 million General Export Facility for international expansion; world's first carbon-neutral branded cheddar |

Latest Development & News

- In January 2026, Arla Foods entered the UK cottage cheese segment with a new range targeting the category's resurgence among health-conscious consumers seeking high-protein, low-fat dairy alternatives. The launch is aimed at extending Arla's UK fresh dairy portfolio into a fast-growing functional segment that has seen significant volumes shift from traditional yogurt and soft cheese formats.

- In May 2025, Lactalis UK & Ireland launched Leerdammer Original Spreadable (125g). This was the first time that the brand had entered the spreadable cheese market, apart from its traditional sliced products. It has a mild, nutty taste that customers expect from Leerdammer, in a convenient and versatile format that can be enjoyed on sandwiches, bagels, and crackers.

- In October 2024, Saputo launched several new products under its portfolio, including Wensleydale and Vandersterre, with innovative flavors like Mango Ginger Wensleydale, Hot & Spicy Cheddar, and specialty Gouda. Along with these products, Saputo reaffirmed its sustainability pledge through the Saputo Promise, supporting sustainable farming practices throughout the supply chain.

UK Cheese Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Sources Covered | Cow Milk, Buffalo Milk, Goat Milk, Others |

| Types Covered | Natural, Processed |

| Products Covered | Mozzarella, Cheddar, Feta, Parmesan, Roquefort, Others |

| Formats Covered | Slices, Diced/Cubes, Shredded, Blocks, Spreads, Liquid, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Convenience Stores, Specialty Stores, Online, Others |

| Regions Covered | London, South East, North West, East of England, South West, Scotland, West Midlands, Yorkshire and The Humber, East Midlands, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the UK Cheese Market Report

The UK cheese market was valued at USD 3,233.8 Million in 2025.

The market is anticipated to reach a value of USD 5,063.0 Million by 2034.

Cow milk dominates the market with a share of 90.5% in 2025, reflecting the depth of the UK's bovine dairy farming infrastructure, well-established supply chains, and strong consumer preference for traditional cow-milk dairy products.

Natural dominates the market with a share of 78.4% in 2025, driven by consumer preference for clean-label, provenance-led dairy products without additives or emulsifiers.

Cheddar dominates the market with a share of 33.2% in 2025, representing over 70% of total UK cheese production by milk utilization, making it both the defining industrial product and the most consumed household cheese in Britain.

Blocks dominate the market with a share of 42.6% in 2025, as the preferred format for UK household cooking, grating, and sharing occasions, spanning economy private-label options through to premium vintage cheddar truckles and artisanal waxed territorial blocks.

Supermarkets and hypermarkets lead the market with a share of 48.3% in 2025, owing to major grocery multiples including Tesco, Sainsbury's, ASDA, and Morrisons, which provide the national distribution scale and promotional infrastructure.

London leads the UK cheese market with a share of 15.7% in 2025, driven by the capital's highest per-capita grocery spend, multicultural specialty cheese demand, dense foodservice and hospitality ecosystem, and premium grocery retail concentration that generates above-average consumption of both mass-market and artisanal varieties.

Key trends include growing consumer adoption of functional and high-protein cheese formats such as cottage cheese and lactose-free cheddar, accelerating private-label premiumization by grocery multiples investing in regionally sourced artisanal ranges, and the expansion of digital and subscription-based cheese retail platforms.

Challenges include intensifying competition from imported Continental PDO cheeses that retain strong consumer loyalty, seasonal volatility in domestic milk utilization creating manufacturing planning complexity, and the need for continuous product reformulation to meet evolving health and sustainability consumer requirements.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade